Peer-to-Peer Energy Matching: Transparency, Choice, and Locational Grid Pricing

James Johnston Open Utility, London, United Kingdom

Abstract

Peer-to-peer (P2P) energy matching could support the transformation of the traditional energy industry into a digital, decentralized, and renewable-powered one. This chapter introduces the P2P energy matching concept, using UK start-up Open Utility as an example. It presents the first commercial use case for P2P energy matching: providing customers with transparency and choice over their renewable energy supply. It also presents Open Utility’s proposed modification to UK Distribution System Operator (DSO) charging regulations to incorporate locational pricing, and concludes with an overview of how P2P energy matching can lead to the development of a community-driven and democratized energy industry.

Keywords

peer-to-peer energy matching

local energy markets

renewable energy

transparency

choice

Piclo Platform

locational grid pricing

local balancing

1. Introduction

As other chapters of this volume have already explained, the electricity industry is rapidly transforming away from an analog, centralized, and fossil-fuel powered model toward a digital, decentralized, and renewable-powered one.

Traditionally, power flowed unidirectionally from a small number of large thermal power stations through an elaborate transmission and distribution network to end users, who were passive and uninterested in what happened upstream of the meter. Most users paid regulated tariffs and had minimal and infrequent interactions with their suppliers, if at all, beyond paying the utility bills.

This picture is rapidly changing. Businesses and households are taking control and installing on-site renewable generation (plus energy storage in the near future). These distributed energy resources (DERs) mean that power flows are no longer guaranteed to be unidirectional, complicating the traditional roles of balancing, transmission, and distribution. Furthermore, energy customers are no longer passive and uninterested; they are evolving into a new sophisticated type of user with the capability, interest, and financial motivation to participate actively in energy markets.

In the future, many experts see the needs of customers and generators being served by peer-to-peer (P2P) models, where they can exchange energy with each other and participate in wider energy markets through online platforms. With flexible generation, storage, and smart devices, customers can better manage their consumption, shift loads, and provide balancing services to local and national grids. Over the coming decades a smart, flexible, and decentralized energy system could deliver trillions of dollars of savings globally (Lovins, 2011).

While many experts agree on the long-term vision of a decentralized energy system, there are fewer practical guidelines on how the existing centralized energy system can migrate toward this vision. The existing energy industry is built on centralized principles, which during a century of development have been baked into regulations, software systems, and business models and all serve to maintain the status quo. Customer attitudes may be changing, but the industry so far has been slow to catch up.

Real innovation lies at the interface between the current centralized energy system and the proposed future decentralized energy system. This chapter will focus on these practical solutions—that can both function in today’s world, but also act as stepping stones toward the decentralized vision.

Section 2 focuses on present day commercial opportunities for P2P energy, and illustrates this with a case study on Open Utility, one of the first companies in the world to launch a commercial P2P offering. Section 3 looks into the near future and explore how P2P models and regulatory frameworks could evolve over the next few years to lay down the stepping stones toward the vision of a decentralized and democratized energy system followed by the chapter’s conclusions.

2. Transparency and choice

All across the world, individuals and businesses are seeking different ways to cut their carbon emissions and reduce their ecological footprint. As a first measure, they look to reduce their net demand through energy efficiency actions and as a secondary measure install on-site renewable generation. Most buildings cannot go fully off grid due to space limitations or leasing restrictions. Additionally, as renewable generation sources are intermittent, they might have surplus power at certain times of the year, while requiring top-up at others. Energy storage helps alleviate this on an hour-by-hour basis, but cannot be relied upon for interseasonal variations.

For these reasons, many people and businesses want to buy zero carbon electricity via the electricity network. But how is it possible to match customers with specific renewable generators? As everyone knows, electrons, once injected into the network, are mixed up with others and there is no physical way to route electrons from a specific generator to a specific customer.

However, you don’t need to reroute electrons for matching to work. A good analogy is that the grid is just like an online bank account. When you digitally transfer money to a friend, there is no direct transfer of physical currency (e.g., dollar bills) between the two bank accounts. Instead, it’s an accounting process facilitated by a trusted intermediary—the bank. One account is debited and the other credited by the same amount. In the same way, you can buy renewable electricity from the grid: customers’ accounts are credited when they take energy off the grid and generators’ accounts are debited when they put energy onto the grid. Similar to banking, you also need a trusted intermediary (a licensed electricity retailer) to facilitate the transactions.

Traditionally, there are two methods for tracking the buying and selling of renewable generation over the grid and providing authentication of supply. The first method is using a regulated Guarantee of Origin (GoO) certification process. According to the EU guideline 2009/28/EC, all EU member states are required to establish a national GoO registry for electricity generated from renewable sources. In the United Kingdom, these certificates [called Renewable Energy Guarantee of Origin (REGOs)] are managed by Ofgem E-serve who verifies that no double counting has occurred and administers the certificates to electricity retailers.1

A secondary method for achieving authentication of supply is setting up a power purchase agreement (PPA) bilaterally between a generation site and a customer—called corporate PPAs. This contractual approach provides a stronger linkage between the customer and generators, and also enables the price to be fixed over a longer time period.

However, there are problems with both of these traditional approaches. The GoO process is opaque and complicated. In the United Kingdom, generators need to manually submit their information to Ofgem every year. Customers don’t necessarily trust that the process stops double counting. For example, in Europe many certificates originate from hydro sites in Norway, even though many consumers in Norway do not realize that they are giving away the “renewable benefit” from their local generators (Jensen et al., 2016). Studies have shown that many businesses do not trust their electricity retailers, as they do not provide enough granular data on the source of their energy (Aasena et al., 2010; Hast et al., 2015). Finally, as matching is done on an annual basis, it does not reflect the true nature of intermittent renewables—which could further exacerbate perceptions that buying renewable energy over the grid is “greenwash.”2

Corporate PPAs are more effective at determining authenticity of supply, however they do so in a clunky way. Due to the bespoke nature of the contracts, they are very expensive and complex to set up and hence are only an option for the largest of global corporations (Labrador, 2015).

P2P energy markets are disrupting these traditional approaches. A perfect storm is brewing due to a number of far-reaching changes across the industry:

• Smart meters: over 1 billion smart meters will be deployed across the world by 2022 (Martin, 2013). Remote access to near-realtime data on consumption and generation will become the norm rather than the exception.

• Distributed generation: by the end of 2015, the global capacity of distributed solar PV (installations less than 4 MW) was around 160 GW.3

• Sharing economy: through the successes in other sectors (most prominently Uber and Airbnb in transportation and hospitality, respectively), customers are becoming comfortable with online “sharing economy” business models.

• Blockchain technology: the distributed ledger technology promises a new era of distributed business models across every sector, including energy. Regulators and incumbents are taking notice of the potential and setting up trials across the world (Burger et al., 2016).

As a result, there are now few barriers to the development of highly scalable online P2P transactive models, which can automatically match generation and consumption using near-realtime smart meter data. Provenance of supply could become a central feature of market design, rather than an inefficient afterthought.

P2P energy markets are still in their infancy and a number of start-ups developing solutions are emerging across the world.4 One of the most established platforms is called Piclo and is run by Open Utility, a technology company based in London, United Kingdom.5

In October 2015, the Piclo Platform was trialed by UK electricity retailer Good Energy in a project funded by the UK government. Good Energy is a UK electricity retailer with around 75,000 residential customers and 4,000 business customers. They source their electricity from more than 1000 distributed renewable generators across the United Kingdom.6 The trial was composed of 25 renewable generators (covering wind, solar, and hydro technologies) and 12 business customers (tourist sites, hotels, factories, and farms). Full results of the trial were published in the report “Piclo—A Glimpse Into the Future of Britain’s Energy Economy.”7

In August 2016, Open Utility signed a multiyear commercial agreement with Good Energy to roll out the Piclo Platform to all their business customers and renewable generators. At time of writing in December 2016, the service—under the Selectricity brand, was the largest P2P energy matching platform in the United Kingdom.

More details on Open Utility’s Piclo Platform are outlined in Box 16.1.

Box 16.1How Piclo Platform Works?

The Piclo Platform enables a virtual P2P connection between customers and generators and automatically allocates energy between them according to their smart meter data (Fig. 16.1).

Figure 16.1Connecting virtually with local generators.

Customers can control which set of generators they match with by setting preferences on the online service. Effectively, customers are creating a priority list of generators, which is analogous to a merit order, a concept that underpins traditional spot markets.8 In P2P markets, every single customer can build their own unique merit order. The definition can also be relaxed to include multiple prioritization criteria, including cost, technology type, ownership, location, and other characteristics.

Once the merit order is set, the process is entirely automated. On behalf of each customer the matching algorithms try to match as much energy as possible with the highest priority generators. For example, a customer might prioritize a local community wind turbine but depending on the available wind resource it might only get a fraction of their needs from that source. The algorithms would then run through the merit order continually trying to match as much as possible.

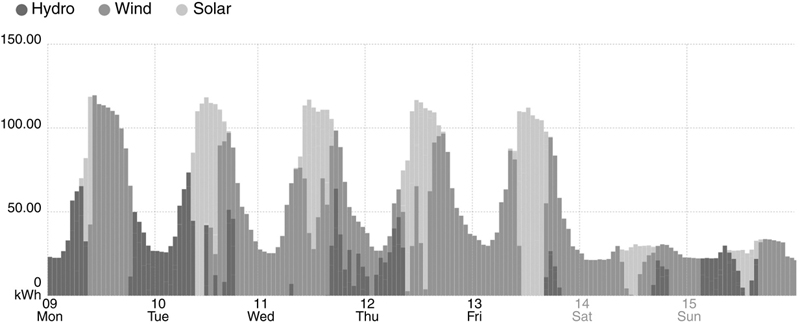

As discussed earlier, no electrons are being rerouted in the matching process—it is simply a more granular way of debiting and crediting electricity being put on and taken off the grid. Matching is done on a half-hourly frequency (as meter data in the United Kingdom is available at that frequency) which means energy mixes made up of solar, wind, and hydro vary throughout the day according to the weather. Fig. 16.2 illustrates a typical week of matching data, where varying amounts of hydro, wind and solar generation sources are matched every half hour.

Figure 16.2Typical week of matching data.

The Piclo Platform enables customers to engage with their energy supply in a unique way. Large business customers who have to spend millions each year on their electricity bills can receive more value: they can choose to buy from local community generators to visibly support the local economy and they get to tell positive marketing stories to better engage their staff and customers. They can, for example, say: “we buy from our local school solar array,” or “our energy comes from the local wind farms,” or “nearby hydro reservoir”—marketing messages that increasingly resonate with environmentally conscious consumers.

To access the Piclo Platform, customers and generators need to sign a contract with an electricity retailer that has bought a license to use the platform. Currently, they can only match with customers and generators who have signed up with the same electricity retailer, though this may change in the future.

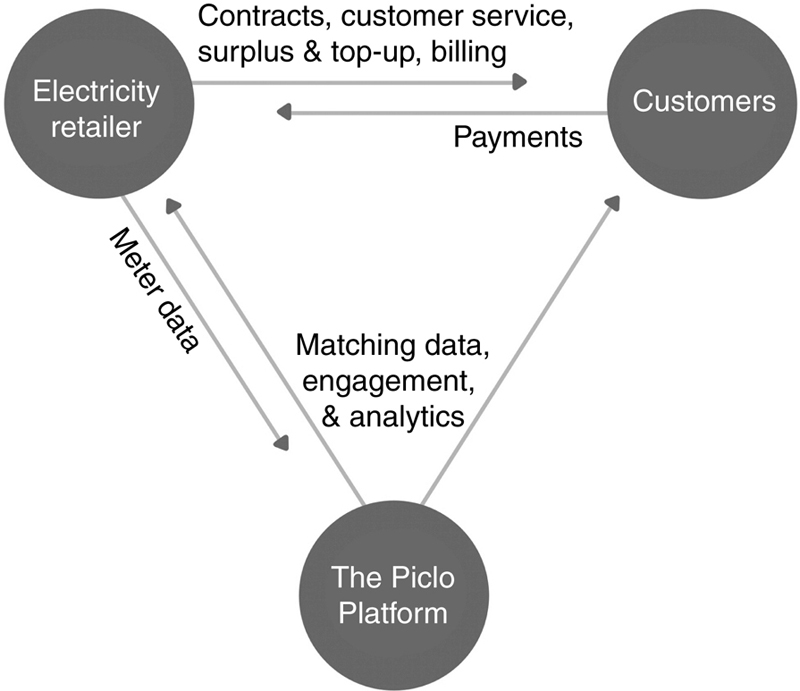

The Piclo Platform is a cloud-hosted service. Smart meter is received from the electricity retailer via an API and both the electricity retailer and their customers get online accounts to access the matching data. The electricity retailer continues to manage customer contracts, customer service, billing, and payment as schematically illustrated in Fig. 16.3.

Figure 16.3Piclo Platform business model.

Electricity retailers pay Open Utility to license the platform and in return they can offer customers a tangible renewable supply—a valuable differentiator in competitive markets. Those electricity retailers with an existing supply chain of contracted renewable generation can better leverage those assets and bring their renewable tariffs to life. They can develop new location-based sales strategies and improve retention metrics through better engagement.

P2P energy matching for provenance of supply could be seen by many as a “nice-to-have” for renewable-focused electricity retailers rather than mandatory function in the energy industry. However, it does offer several benefits over traditional renewable certification processes as outlined earlier, and regulation should recognize this.

Presently, there are no mandatory requirements for businesses, individuals, or electricity retailers to adopt it. Indeed, incumbent electricity retailers are resistant to change: they say that moving away from monthly or annual accounting of renewables would increase their administrative burden (Ofgem, 2016). Possibly, the real reason is that they are worried about what the extra transparency would reveal: renewables are commonly thought to be locally generated, when in many cases renewable tariffs are backed by certificates bought from overseas.

3. Locational grid pricing

There is growing interest from DSOs, regulators, and policy experts in using locational grid pricing to incentivize local balancing to reduce network congestion and grid defection (MIT, 2016).

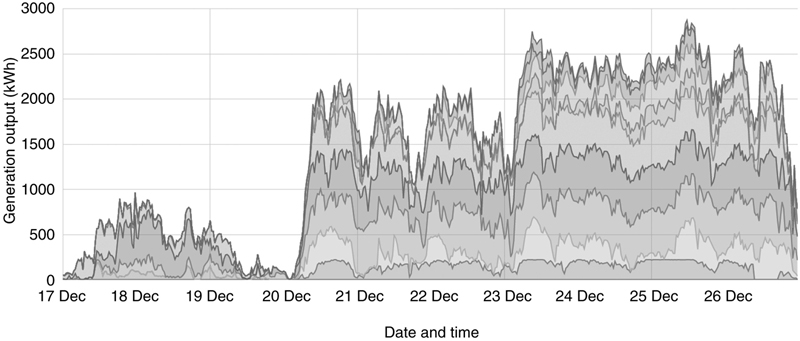

DSOs can no longer rely on the physical reinforcement of networks alone as costs would be prohibitive and networks oversized and underutilized. Renewables have low capacity factors (meaning they only reach their nameplate maximum capacity a fraction of the time) and peaks can often occur at the same time. This phenomenon is illustrated in Fig. 16.4, using data from 10 wind generators (situated across the breadth of the United Kingdom).9

Figure 16.4Generation output from 10 wind turbines across the United Kingdom in December 2016.

Renewables are forcing DSOs to deploy more virtual means of managing congestion in their networks. One method is active curtailment of generators when local network limits are reached (Gill et al., 2014). Other direct control measures include deploying energy storage at substations to defer reinforcement; as of 2015 around 66 MW of energy storage was operational across UK distribution networks (REA, 2015).10

Alternatively, DSOs can create price-based incentives to promote certain behaviors (Eida et al., 2016). They are desirable for DSOs as it allows them to be agnostic to solutions and let the markets decide the most efficient method: thus driving competition and keeping costs down. As a downside, there is less certainty on the magnitude and timeliness of response as they rely on customers to act in their own best (economic) interest (Ruester et al., 2014).

In the United Kingdom, there is already a widespread adoption of price-based incentives. All large industrial and commercial energy customers in the country (accounting for around 50% of the UK demand) have time-of-use tariffs to encourage them to reduce or shift their demand at peak times (Moss and Buckley, 2014). These tariffs are split into red, amber, and green time periods.

The problem with these price incentives is that they only take into account temporal congestion factors. DSOs average out prices across all customers, regardless of where they are situated to create a “socialized” cost structure. This approach is attractive for regulators as it ensures nondiscrimination as customers are treated equally (MIT, 2016).

This system worked well for customers when most of their electricity came from big power stations and the distribution network was used more or less in full by everyone. However, with the rollout of distributed generation and community energy groups, an increasing number of people do not accept that they should be paying for parts of the network they are not using (Bennett, 2015). From a generator perspective, the lack of a financial incentive for local trading is driving them to install their own private wires to sell power direct to local customers and thus cutting out the DSO completely (Urquhart, 2016).11

Locational grid pricing that gives customers and generators a financial benefit for local trading could mediate both these problems. Understandably, regulators are hesitant in moving away from a low-risk socialized charging model. There are very few examples of locational pricing models deployed in the field and not much quantitative data on the value to distribution networks or impact on customers. For this reason, DSOs are keen to run trials to test out different approaches and build evidence for regulatory change (MIT, 2016).

P2P energy matching can facilitate new locational pricing models. It can be used to trace how much of the distribution network has been used in every energy transaction. In 2016, Open Utility in collaboration with economists Reckon LLP proposed a modification to UK DSO charging regulations to incorporate locational pricing. A summary of the model is shown in Box 16.2. A link to the full report (along with details on the industry change proposal) is in the footnote.12

Box 16.2Locational Pricing Case Study

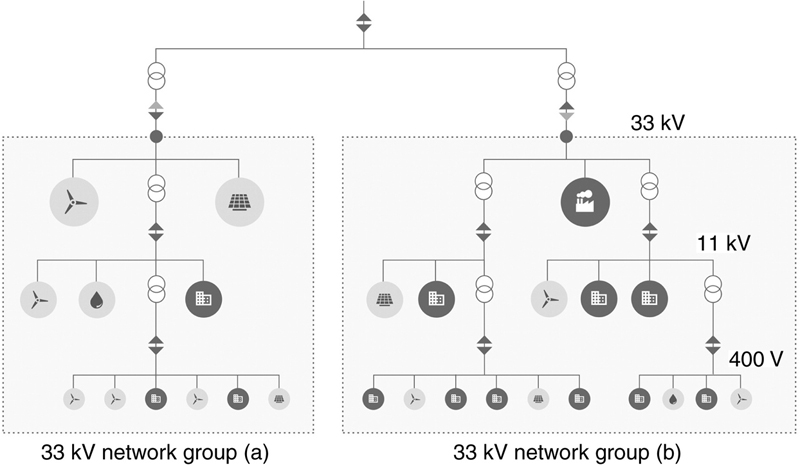

Open Utility’s proposed solution was to offer customers a lower DUoS rate for any energy sourced within the same 33 kV network group (Fig. 16.5). Effectively, if a customer matched with a local generator, they only pay the unit charges for the section of the network they used in those transactions. Any energy matched with generators via the parent 132 kV network is charged at normal DUoS rates.

Figure 16.5Schematic outline of Open Utility’s locational pricing model.

Customers who modify their demand profiles to match more with local generation (e.g., undertake local balancing) would end up paying less DUoS charges than customers who act more passively. Therefore, a locational pricing incentive could reduce the amount of grid reinforcement required upstream which would offset the DSO’s lost revenues (in offering the lower DUoS rates). In the example in Fig. 16.5, an upgrade on the 132 kV network could be avoided because of better local balancing within the two separate 33 kV network groups.

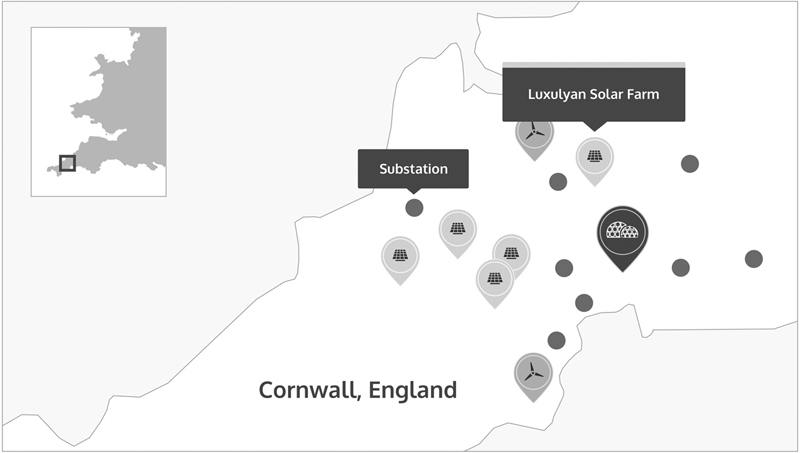

A desktop case study using the Eden Project, a large visitor attraction in the south-west of England was completed. Analyzing the potential for local matches, it was discovered that five solar farms and two generation wind turbine sites were connected to the same 33 kV network group (Fig. 16.6). With representative data on levels of local matching, it was estimated that the Eden Project could reduce its overall DUoS rates by 39% or around £20,000 per annum.

Figure 16.6Distributed generation connected to the same 33 kV network group.

4. Conclusions

Much of the value of distributed renewable generation is locked up in the outdated and centralized energy industry business models and regulations.

P2P energy matching introduces to the energy industry a simple concept of recording the source and destination of every energy transaction over the grid. The applications are widespread: from enabling electricity retailers to provide their customers with transparency and choice, to enabling DSOs to develop locational grid pricing.

A lack of transparency and choice is holding back the adoption of renewable tariffs. Some do not trust that buying renewable energy over the grid will have any meaningful impact. P2P energy matching is a relatively simple, yet powerful antidote to this and could help drive a strong customer demand for renewables into the future.

Finally, locational grid pricing could have a number of benefits for DSOs. By incentivizing local balancing it could help reduce losses on distribution networks, lower carbon emissions, and remove the need for network reinforcement to meet the same demand. Unlocking a financial benefit for local trading could support the development of a community-driven and democratized energy industry.

Acknowledgments

The author would like to acknowledge the assistance of Fereidoon Sioshansi and the Open Utility team in finalizing this chapter.