7

Economics of Manufacturing Pollution Prevention: Toward an Environmentally Sustainable Industrial Economy

7.1 Introduction

The failure of many pollution‐prevention programs can be traced to the inability of the engineers and scientists to convince business leadership to change manufacturing processes unfavorable to the environment. Often, this reluctance to change is not because the recommended process improvements were technically unsound, but because the engineering team failed to speak the language of business, that is dollars and cents. The role of economics in pollution prevention is very important, even as important as the ability to identify technologies changes to the process, new and emerging technologies, process and/or product modification, Zero Discharge technologies, technologies for biobased engineered chemicals, products, renewable energy sources, and its associated costs.

Market acceptance of new technologies, products, processes, and services depend upon the complex interplay of cost, physical properties, environmental performance, public policy, cultural prejudices, and other factors. Accurate forecasting is a difficult and time‐consuming activities best left to the experts. However, cost estimating is a valuable skill that allows an engineer to obtain “ballpark” approximation of project costs. The goal is to obtain an estimate that is within ±30% of the actual cost if the enterprise were pursued. Such estimates are relatively easy to develop. Engineers use a relatively small set of financial tools to assess alternative capital investments and to justify their selections to upper management. Most often, the engineer's purpose is to show how a recommended investment will improve the company's profitability. Spending on capital improvements is largely voluntary. Adding an assembly line or changing from one type of gasket material to another can be postponed, or the proposal, or rejected outright. This is not the case with pollution control devices, which are necessary for compliance with state and federal pollution standards and generally must be installed by or before a mandated deadline. Consequently, a decision to install device X may not originate with the engineer. Instead, the need for pollution control equipment might be identified by a company's environmental manager who then passes the decision to acquire device X down to the engineer. This chapter gives some cost‐estimating methods that can be used to assess the costs of implementing pollution prevention technologies; these methods are useful, as well, in cost comparisons, and in considerations of cost‐effectiveness, best available technologies and emerging technologies. Also provided is some information about the cost of renewable resources and the cost of manufacturing biobased products from such feedstocks. We begin, however, with a few remarks about the economic matrix in which profitable pollution control technology and best control technology are implemented.

7.2 Economic Evaluation of Pollution Prevention

The economic evaluation of engineering projects typically involves estimation of equipment, installation, raw material, energy, and maintenance cost. Disposal and pollution control costs are often factored into these calculations in determining economic rates of return, but other regulatory and social costs are not. In this chapter, total cost assessment of waste management alternatives is described, and the hidden costs, future liabilities, and less tangible costs associated with waste generation are discussed.

7.2.1 Total Cost Assessment of Pollution Control and Prevention Strategies

Traditional economic measure of engineering projects evaluate equipment, raw‐material, energy, operating, and maintenance costs. These evaluations generally overlook some of the costs of waste generation. A more complete accounting of environmental costs is referred to as total cost assessment. Four types of costs are identified, which are labeled as tier 0, tier 1, tier 2, and tier 3. Tier 0 costs are the “usual” costs that are included in a conventional analysis of a project. Tier 1 costs are included in a conventional analysis of a project. Tier 1 costs include permitting, reporting, monitoring, manifesting, and insurance costs and are often referred to as “hidden” costs because they are usually treated as overhead costs and are not directly charged to a project. Waste disposal costs are sometimes treated as overhead costs as well. Tier 2 costs include future liabilities, which are extremely difficult to accurately evaluate. Even more difficult to evaluate are tier 3 costs, which include consumer responses, employee relations, and public image. All four tiers of costs provide information for financial analysis methods, where measures such as ROR and payback periods (PPs) are evaluated.

7.2.2 Economics of Pollution Control Technology

In the present economic system, the goal of a sustainable development process is to maintain intergenerational equity by ensuring quality of life for future generations, which essentially requires the stopping of further damage to the environment. From this point of view the necessity of an integrated system consisting of modern manufacturing production and controlling technologies is being gradually recognized. To this end, various regulatory measures are being implemented, mainly in the industrial sector, which is the major contributor of pollution, for adopting such technologies.

7.3 Cost Estimates

The costs and estimating methodology in this section are directed toward the “study” estimate with a nominal accuracy of ±30%. According to Perry's Chemical Engineer's Handbook, a study estimate is “used to estimate the economic feasibility of a project before expending significant funds for piloting, marketing, land surveys, and acquisition. However, it can be prepared at relatively low cost with minimum data” (Perry and Green 1997). Specifically, the development of a study estimate calls for knowledge of the following:

- Location of the source within the plant

- Rough sketch of the process flow sheet (i.e. the relative locations of the equipment in the system)

- Preliminary sizes of, and material specifications for, the system equipment items

- Approximate sizes and types of construction of any buildings required to house the control system

- Rough estimates of utility requirements (e.g. electricity)

- Preliminary flow sheet and specifications for ducts and piping

- Approximate sizes of motors required

In addition, since the accuracy of an estimate (study or otherwise) depends on the amount of engineering work expended on the project, the user will need an estimate of the labor hours required for engineering and drafting activities. There are four other types of estimate.

The order‐of‐magnitude estimate, a rule‐of‐thumb procedure, can be used only for plant installations of the repetitive type for which there exists good cost history. Its error bounds are greater than ±30%. (However, Perry states that “no limits of accuracy can safely be applied to [an order‐of‐magnitude estimate].”) The sole input required for making an order‐of‐magnitude estimate is the control system's capacity (often measured by the maximum volumetric flow rate of the gas passing through the system).

The other three types of estimate, listed next, are preferable.

- Scope, budget authorization, or preliminary. This estimate, nominally of ±20% accuracy, requires more detailed knowledge than the study estimate regarding the site, flow sheet, equipment, buildings, etc. In addition, rough specifications for the insulation and instrumentation are also needed.

- Project control or definitive. These estimates, accurate to within ±10%, require yet more information than the scope estimates, especially concerning the site, equipment, and electrical requirements.

- Firm or contractor's or detailed. This is the most accurate (±5%) of the estimate types, requiring complete drawings, specifications, and site surveys. Consequently, detailed cost estimates are typically not available until right before construction. Common sense suggests that there is seldom enough time to prepare such estimate before approval to proceed with the project has been obtained.

7.3.1 Elements of Total Capital Investment

Total capital investment (TCI) includes all costs required to purchase equipment needed for the control system (purchased equipment costs), the costs of labor and materials for installing that equipment (direct installation costs), costs for site preparation and buildings, and certain other costs (indirect installation costs). TCI also includes costs for land, working capital, and off‐site facilities.

Direct installation costs include costs for foundations and supports, erecting and handling the equipment, electrical work, piping, insulation, and painting. Typical indirect installation costs are engineering costs, construction and field expenses (i.e. costs for construction supervisory personnel, office personnel, rental of temporary offices, etc.), contractor fees (for construction and engineering firms involved in the project), start‐up and performance test costs (to get the control system running and to verify that it meets performance guarantees), and associated costs with contingencies. “Contingencies” is a catch‐all category that covers unforeseen costs that may arise if, for example, it becomes necessary to redesign, modify equipment, to pay higher costs of equipment or field labor costs, or to compensate for delays in start‐up. Contingency costs are not the same as uncertainty and retrofit factor costs.

The elements of TCI are displayed in Figure 7.1. Note item “battery limits” cost, which is the sum of the purchased equipment cost, direct and indirect installation costs, and costs of site preparation and buildings. By definition, this is the total estimate for a specific job; any support facilities that may be needed (e.g. control systems) are assumed to already exist at the plant and are not included in the battery limits. For systems installed in new plants, off‐site facilities (special facilities for supporting the control system) also might be excluded from the battery limits. Off‐site facilities are exemplified by units to produce steam, electricity, and treated water; laboratory buildings; and railroad spurs, roads, and other transportation infrastructure items. Pollution control devices rarely consume enough energy to warrant dedicated off‐site capital units. However, it may be necessary – especially in the case of control systems installed in new or “grassroots” plants – to build extra capacity into the site's generating plant to service the system. (A Venturi scrubber, which often requires large amounts of electricity, is a good example.) Nevertheless, that the capital cost of a device does not include utility costs, even if the device were to require an offsite facility. Utility costs are charged to the project as operating costs at a rate that covers both the investment and operating and maintenance costs for the utility.

As Figure 7.1 shows, the installation of pollution control equipment may also require land, but since most add‐on control systems take up very little space (a quarter‐acre or less), this cost tends to be relatively small. Certain control systems, such as those used for flue‐gas desulfurization or selective catalytic reduction (SCR), require larger quantities of land for the equipment, chemicals storage, and waste disposal. In these cases, especially when a retrofit installation must be performed, space constraints can significantly influence the cost of installation, and the purchase of additional land may be a significant factor in the development of the project's capital costs. Land retains its value over time; however, land is not treated the same as other capital investments, retains its value over time, the purchase price of new land needed for sitting a pollution control device can be added to the TCI, but it must not be depreciated. Instead, if the firm plans to dismantle the device at some future time, either the land should be excluded from the analysis or its value included at the disposal point as an “income” to the project, to net it out of the cash flow (CF) analysis.

Figure 7.1 Elements of TCI.

One might expect to include initial operational costs (the initial costs of fuel, chemicals, and other materials, as well as labor and maintenance related to start‐up) in the operating cost section of the cost analysis instead of in the capital component, but such an allocation would be inappropriate. Routine operation of the control does not begin until the system has been tested, balanced, and adjusted to work within its design parameters. Until then, all utilities consumed, all labor expended, and all maintenance and repairs performed are a part of the construction phase of the project and are included in the TCI in the “start‐up” component of the indirect installation costs.

7.3.2 Elements of Total Annual Cost

Total annual cost (TAC) has three elements: direct costs (DC), indirect costs (IC), and recovery credits (RC), which are related by the following equation:

Clearly, the basis of these costs is one year, a period that allows for seasonal variations in production (and emissions generation) and is directly usable in financial analyses. The various annual costs and their interrelationships are displayed in Figure 7.2.

DC are those that tend to be directly proportional (variable costs) or partially proportional (semi‐variable costs) to some measure of productivity – generally the company's productive output, but for purposes of pollution control, the proper metric may be the quantity of exhaust gas processed by the control system per unit time. Conceptually, a variable cost can be graphed in cost/output space as a positive sloped straight line that passes through the origin. The slope of the line is the factor by which output is multiplied to derive the total variable cost of the system. Semi‐variable costs can be graphed as a positive sloped straight line that passes through the cost axis at a value greater than zero – that value being the “fixed” portion of the semi‐variable cost and the slope of the line being analogous to that of the variable cost line discussed above.

Figure 7.2 Elements of TAC.

7.4 Economic Criteria for Technology Comparisons

Technology evaluation encompasses not only technical feasibility of a particular technology but also the economics of its implementation. While there are many measures of economic merit, two measures – investment and net present value (NPV) – provide a complete set of information on which to base an informed, economic decision. “Investment” refers to the money that must be spent initially to design and build the new facilities. NPV is the after‐tax worth in today's dollars of all the future cash that an alternative will either consume or generate; it includes the effects of new investment, working capital, operating costs, revenues, and income taxes. NPV is the most popular singular measure of the economic merit of an alternative, and many spreadsheet programs can easily calculate it.

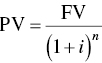

To evaluate alternative pollution control devices, the analyst must be able to compare them in a meaningful manner. Since different controls have different expected useful lives and will result in different CFs, the first step is to use the principle of the time value of money to normalize the returns of the alternatives being compared. The process through which future CFs are translated into current dollars is called present value (PV) analysis. When the CFs involve income and expenses, it is also commonly referred to as NPV analysis. In either case, the calculation is the same: adjust the value of future money to values based on the same (generally year zero of the project), employing an appropriate interest (discount) rate and then add them together. The decision rule for NPV analysis is that projects with negative NPVs should not be undertaken; and for projects with positive NPVs, the larger the NPV, the more attractive the project. Derivation of a CF's NPV involves the following steps:

- Identification of alternatives – for example, the choice between a fabric filter baghouse and an electrostatic precipitator for removing particulate matter from a flue‐gas stream.

- Determination of costs and CFs over the life of each alternative.

The relationship of the future value of money to the PV of a sum of money compounded annually at an interest rate, i, for a total of n years is shown by the following equation:

where

- FV = future value

- PV = present value

- i = annual earnings rate

- n = years in the future

This equation is used to determine how many future dollars will be realized by investing present dollars at the interest rate i for n years. For example, $100 invested today at 5% for 12 years will yield the following return:

Similarly, inflation at 5% per year makes $100 worth of merchandise today cost $180 in 12 years. Discounting is the opposite of compounding: the PV of a sum of money to be spent or received in the future is reduced according to

where i is now referred to as the discount rate. Thus, if the discount rate is 5% per year, we calculate the PV of $100 to be spent 12 years as follows:

Since the PV of money to be spent in the future declines with increasing interest rate and number of years into the future, the importance of accounting for the time at which money is spent or received is evident.

7.5 Calculating CF

A complete financial analysis requires the inclusion of CF. On a year‐by‐year basis, the CF from a manufacturing investment is determined through calculations of cash costs, total costs, and cost‐effectiveness.

Cash costs, those associated with operating and overhead, include raw materials (chemicals, catalysts, solvent, etc.) utilities (steam, electricity, natural gas, water, etc.), maintenance materials and labor, operations labor, technical support, startup costs, taxes and insurance, and administrative costs.

Total costs include the sum of cash costs as just defined and depreciated. Note that depreciation is not a cash cost and is used only to calculate income taxes. If the investment generates revenues or savings from which the total costs may be subtracted, the resulting amount is known as the “pretax earnings.” Income taxes (calculated on pretax earnings) are next subtracted to yield the after‐tax earnings. A year‐by‐year CF can then be determined by summing the four real CFs: investment, cash costs, revenues, and income taxes.

NPV is the sum of the PVs of a series of CFs:

where, CF0, CF1, CF2 represent CF in year 0, 1, 2, and so on, and the D terms are discount factor for the respective years.

In the context of pollution control, cost‐effectiveness is defined as the annualized cost of the control option divided by the annual emission reductions resulting from the control option. The following information is required to calculate the cost‐effectiveness of a proposed control option: (i) the capital cost of purchasing and installing the control equipment or making a process modification, (ii) the annual operating costs of the control option, and (iii) an estimate of the emissions before and after application of the control option.

The capital costs of purchasing the control option should be determined from actual vendor price quotes for each proposed control option. Installation costs should also be based on vendor price quotes. If vendor price quotes are unavailable, elements of the installation cost may be estimated (Vatavuk 2002). To illustrate cost‐effectiveness calculations, let us consider a facility that is a major source of NOx emissions.

7.5.1 Achieving a Responsible Balance

In the real worlds, taking socially desirable action for pollution prevention may not be in the best interest of an industry in the short run, since environmental protection costs money. The type of production, input used, technology employed, space used as well as plant size and the scale of production determine the nature and extent of pollution which, in turn, influence the abatement cost. Hence, the decisions of the profit maximizing private investor for implementation of pollution abatement measure are influenced by the benefit expected as a result of the investment required. On the other hand, the task of government planners and policy makers is to encourage industry to adopt modern production and pollution control technologies to provide a better environment for the society. In upgrading their facilities to meet the near antipollution regulations, industries turn for guidance to the principles of best available control technology (BACT).

7.6 From Pollution Control to Profitable Pollution Prevention

As companies incorporate pollution prevention approaches in their strategic planning, capital investment priorities, and process design decisions, it is vital that they understand both the quantitative and qualitative dimensions of assessing pollution prevention projects. These projects tend to reduce or eliminate costs that may not be captured in cursory financial analyses due to the way costs are categorized and allocated by conventional management accounting systems. Additionally, pollution prevention projects often have impacts on a broad range of issues, such as market share and public impact that are difficult to quantify but that can be of strategic importance. Identifying and analyzing all costs and less tangible items is an important step in an evaluation of the potential benefits of pollution prevention projects.

Pollution prevention can take many forms – from simple “housekeeping improvements,” which cost little to carry out, to installation of expensive capital equipment. Although many pollution prevention projects, such as material substitution or process redesign, do not require large outlays for purchase of equipment, they may require extensive qualitative assessments related to such issues as product quality or employee health and safety. The analytical tools described here are applicable to the assessment of most pollution prevention initiatives that fit under the umbrella of the capital budgeting process. Pollution prevention projects involving capital budgeting generally include

- new manufacturing equipment

- replacement equipment

- plant expansion and construction

Capital budgeting is a process of evaluating capital investment options based on a company's needs and analyzing the impact of an investment on a company's CF over time. Pollution prevention and other capital projects are justified by showing how the project will increase the company's earnings as well. Financial tools demonstrate the importance of the pollution investment on a life cycle or total cost basis in terms of revenue, expenses, and profits. Key concepts and factors used in capital budgeting are described next.

Life cycle costing (LCC): Also referred to as total cost accounting, this method analyzes the costs and benefits associated with a piece of equipment or a procedure over the entire time the equipment or procedure is to be used. LCC is also a tool to determine the most cost‐effective option among different competing alternatives to purchase, own, operate, maintain and, finally, dispose of an object or process, when each is equally appropriate to be implemented on technical grounds. For example, for a highway pavement, in addition to the initial construction cost, LCC takes into account all the user costs (e.g. reduced capacity at work zones), and agency costs related to future activities, including future periodic maintenance and rehabilitation. All the costs are usually discounted and total to a present‐day value known as NPV. This example can be generalized on any type of material, product, or system.

In order to perform a LCC scoping is critical, what aspects are to be included and what not? If the scope becomes too large, the tool may become impractical to use and of limited ability to help in decision‐making and consideration of alternatives; if the scope is too small, then the results may be skewed by the choice of factors considered such that the output becomes unreliable or partisan. LCC has a broader scope, including environmental costs. To help building and facility managers make sound decisions, the US Federal Energy Management Program provides guidance and resources on applying LCC that permits the cost‐effectiveness of energy and water efficiency investments to be evaluated. LCC can be conducted in two approaches: deterministic and probabilistic method.

Present value (PV): The importance of PV, or present worth, lies in the fact time is money. The preference between a dollar now and a dollar a year from now is driven by the fact that dollar in‐hand can earn interest. Mathematically, this relationship is shown earlier in Eq. (7.2), with an example on present and future values.

Comparative factors for financial analysis: The more common methods for comparing investment options all utilize the PV equation presented in Eq. (7.2). Generally, one of the following four factors is used:

- Payback period (PP): This factor measures how long it takes to return the initial investment capital. Conceptually, the project with the quickest return is the best investment.

- Internal ROR: This factor is also called return on investment or ROI. It is the interest rate that would produce a return on the invested capital equivalent to the project's return. For example, a pollution prevention project with an internal ROR of 20% would indicate that pursing the project would be equivalent to investing the money in a bank and receiving 20% interest.

- Benefits cost ratio: This factor is a ratio determined by taking the total PV of all financial benefits of a pollution prevention project and dividing by the total PV of all costs of the project. If the ratio is greater than 1.0, the benefits outweigh the costs and the project is economically worthwhile to undertake.

- Present value of net benefits: This factor shows the worth of a pollution prevention project as a PV sum. It is determined by calculating the PVs of all benefits, doing the same for all costs and subtracting the two totals. The new result would be an amount of money that would represent the tangible value of undertaking the project.

7.6.1 Life Cycle Costing

While firms can use any of these factors, the importance of the LCC (for total cost analysis) makes the PV of net benefits the preferred method. Additional details of LCC and TCA follows.

LCC tool and the total cost assessment (TCA) tool are introduced as concept overviews. Both tools can be used to establish economic criteria to justify pollution prevention projects. TCA is often used to describe the internal costs and savings, including environmental criteria. LCC includes all internal costs plus external costs incurred throughout the entire life cycle of a process, product, or activity.

LCC has been used for many years by both public and private sector. It associates economic criteria and societal (external) costs with pollution prevention opportunities. The purpose of LCC is to quantify a series of time varying costs for a given opportunity over an extended time horizon, and to represent these costs as a single value. These time varying costs usually include the following:

- Capital expenditures. Cost for large, infrequent investment with long economic lives (e.g. new structures, major renovation and equipment replacement).

- Nonrecurring operations and maintenance (O&M). Costs reflecting items that occur on a less frequent than annual basis that are not capital expenditures (e.g. repair or replacement of parts in a solvent distillation unit).

- Recurring O&M. Costs for items that occur on an annual or more frequent basis (e.g. oil and hydraulic fluid changes).

- Energy. All energy or power generation related costs. Although energy costs can be included as a recurring O&M cost, they are usually itemized because of their economic magnitude and sensitivity to both market prices and building utilization.

- Residual value. Costs reflecting the value of equipment at the end of the LCC analysis period. This considers the effects of depreciation and service improvements.

By considering all costs, a LCC analysis can quantify relationships that exist between cost categories. For example, certain types of capital improvements will reduce operations, maintenance, and energy costs while increasing the equipment's residual value at the end of the analysis period.

Societal (external) costs include those resulting from health and ecological damages, such as those related to unregulated emissions, wetland loss, or deforestation, can also be reflected in a LCC analysis either in a qualitative or in a quantitative manner. LCC includes the following cost components:

- Extraction of natural resources. The costs of extracting the materials for use and any direct or indirect environmental cost for the process.

- Production of raw materials. All of the costs of processing the raw materials.

- Making the basic components and products. The total cost of material fabrication and product manufacturing.

- Internal storage. The cost of packaging and storage of the product before it is shipped to distributors and/or retail stores.

- Distribution and retail storage. The cost of distributing the products to retail stores including transportation costs, and the cost of retail storage before purchase by the consumers.

- Product use. The cost of consumer use of the product. This could include any fuels, oils, maintenance, and repairs which must be made to the equipment.

- Product disposal or reuse and/or recycling. The costs of disposal or recycling of the product.

7.6.2 Total Cost Assessment

The TCA tool is especially interesting because it usually employs both economic and environmental criteria. As with the LCC analysis, the TCA study is usually focused on a particular process as it affects the bottom‐line costs to the user. Environmental criteria are not explicit, i.e. success is not measured by waste reduction or resource conservation, but by cost savings. However, since the purpose of TCA is to change accounting practices by including environmental costs, environmental goals are met through cost reductions.

Because of its focus on cost and cost effectiveness, TCA shares many of the features of LCC analysis by tracking DC, such as capital expenditures and O&M expenses/revenues. However, TCA also includes IC, liability costs, and less tangible benefits – subjects that are not customarily included in both economic and environmental goals, because of its private‐sector orientation, as well as other economic computation methods.

7.6.3 Economic Consideration Associated with Pollution Prevention

The greatest driving force behind any pollution prevention (P2) plan is the promise of economic opportunities and cost savings over long‐term. Pollution prevention has been recognized as one of the lowest‐cost options for waste/pollutant management. Hence, an understanding of the economics involved in P2 programs/options is important in making decisions at both the engineering and management levels. Every engineer should be able to exercise an economic evaluation of a proposed project. If the project cannot be justified economically after all factors – include those discussed earlier have been taken into account – it should obviously not be pursued. The earlier such a project is identified, the fewer resources will be wasted.

Before the true cost or profit of a P2 program can be evaluated, the factors contributing to the economics must be recognized. As discussed earlier, there are two traditional contributing factors (capital costs, and operating and maintenance costs), but there are also other important costs and benefits associated with P2 that need to be quantified if a meaningful economic analysis is going to be performed. The TCA aims to quantify not only the economic aspect of P2 but also the social costs associated with the process, product, or a service from cradle‐to‐grave (i.e. life cycle). The TCA attempts to quantify less tangible benefits such as the reduced risk derived from not using a hazardous substance. The future is certain to see more emphasis placed on the TCA approach in any P2 program. For example, a utility considering the option of converting from a gas‐fired boiler to coal‐firing is usually not concerned with the environmental effects and implications associated with such activities as mining, transporting, and storing the coal prior to its usage as an energy feedstock. Pollution prevention approaches will become more aware of this kind of need.

7.7 Resource Recovery and Reuse

A critical element of an interim strategy is enhanced recovery. This can be approached from two directions: reuse of products and recycling of materials. Reuse of products includes return, reconditioning, and remanufacturing. The energy required for reuse and recycling is one of the key factors determining recoverability of a product. The closer the recovered product is to the form it needs to be in for recycling, the less energy is required to make that transformation. From the standpoint of economic development it is worth pointing out that the reconditioning or remanufacturing cycle is relative; it requires roughly half the energy and twice the labor per physical unit of output.

Recycling materials means closing the loop between the supply of postconsumer waste and the demand for resources for production. Recycling of materials will be the business of the Zero Emissions engineer; reuse of products will also involve the Zero Emissions engineer, but will have lots of front‐end work from another professional, the concurrent engineer. Concurrent engineering, which incorporates aspects of industrial engineering, product design, and product manufacturing, is an integrated approach that seeks to optimize materials, assembly, and factory operation. These engineers examine the broader context of a product, including technology for managing the environmental impacts of its transport, intended use, recyclability, and disposal, as well as the environmental consequences of the extraction of the raw material used in its production.

The ultimate fate of all materials is thus dissipation, being discarded, or recycling and recovery. With 94% of materials extracted from the environment being converted to wastes, current levels of recovery are clearly not sufficient. Recovery of materials from wastes will reduce the extent of resource extraction (but will not slow the speed of material flows through the economy). Aluminum and lead are two resources currently being heavily recycled, but evidence shows that there is potential for a lot more resources to be recovered from wastes.

Sherwood plots are diagrams that permit the graphic comparison of concentrations of materials in nature against their commodity cost. The sample plot (see Figure 1.7) shows that the price for a commodity depends on its concentration in nature before extraction and refining. In a similar plot (see Figure 1.8) for concentrations of materials in wastes, it again shows a consistent line.

Together, the Sherwood plots demonstrate the recovery potential of materials. The elements plotted above the line shown in Figure 1.7 should be vigorously recycled because they are present in individual by‐products in relatively high concentrations. Lead, zinc, copper, nickel, mercury, arsenic, silver, selenium, antimony, and thallium are more economical to recover from waste than from nature. Extensive waste trading could significantly reduce the quantity of material requiring disposal because resource extraction uses from wastes, not virgin feedstocks (Allen and Rosselot 1997).

7.8 Profitable Pollution Prevention in the Metal‐Finishing Industry

Surface finishing of metal products is a major manufacturing operation performed in thousands of production shops to provide weather‐resistant, wear‐resistant, and aesthetically pleasing finishes for thousands of manufactured products.1 Surface‐finishing technology involves direct atom‐to‐atom bonding between a base material (such as steel, aluminum, brass, or plastics) and a metal or organic surface top coating that provides the desired material performance and appearance properties. Surface pretreatment is crucial for proper performance and durability of the produced part. Cleaning and oxide removal is critical, so pretreatment processes usually involve many tanks with various purposes. Multistep surface preparation processes are generally employed to remove oils, soiling and dirty materials, old coatings, corrosion products, residual cutting fluids, brazing residuals, pickling acid residuals, cleaner residuals, etc. The surface preparation process removes contaminants, preserves the cleaned surface, and/or modifies the surface for the next coating. After the finishing process, the parts require rinsing/cleaning to remove residual plating solution. These baths, both plating and cleaning, ultimately are exhausted because of depletion of strength or buildup of impurities and, as a result, become major waste streams (Burckle and Ferguson 2005; USEPA 2001).

In the past, pollution control in the metal‐finishing industry has been achieved primarily through end‐of‐pipe treatment. Facilities added waste treatment systems as a final process step to meet regulatory discharge limits to municipal sewers or as direct dischargers. This approach results in the production of residual sludges contaminated with heavy metals that require appropriate pretreatment for environmentally safe disposal (the so‐called “Hammer Provisions” of the Resource Conservation and Recovery Act that apply to hazardous waste disposal in the United States). In the mid‐1980s, various facilities began integrating “pollution prevention” into their operations to reduce the amount of wastewater generated and treated. However, the speed of adoption has been relatively slow, most noticeably in smaller facilities (USEPA 1982, 1985).

The most logical and efficient approach to effectively achieve environmental protection is by preventing pollution. Prevention is achieved using techniques that reduce, eliminate, or recycle/reuse waste materials so that the generation of waste is eliminated, avoiding the need for waste disposal, and wastes that are generated are handled responsibly, either through recovery and recycling to displace other material needs and/or to conserve energy, or minimized and made safe for disposal into the environment. The metal‐finishing industry began to apply pollution prevention principles to reduce process waste emissions in the mid‐1980s, but there were no public statistics generated of the impact on pollution avoided or economic benefit accrued. In discussing the progress of domestic metal‐finishing industry in transitioning to operations based upon pollution prevention, we begin by describing the National Metal Finishing Strategic Goals Program (SGP) initiated by the US Environmental Protection Agency (USEPA) in 1998 in cooperation with industry and public interest stakeholders (USEPA 1998, 2001).

7.8.1 National Metal Finishing Strategic Goals Program

This was the first nationwide program initiated by the USEPA to build voluntary participation in a compliance program by providing incentives in return for a real commitment to reducing pollution to levels below those required for compliance. The SGP was created to address environmental problems and institutional barriers to achieving compliance in a number of industries. It was designed to provide a working relation that facilitates and encourages companies to go beyond environmental compliance to pollution prevention–based operations. SGP member companies were offered incentives, resources, and a means for removing regulatory and policy barriers as they work to achieve specific environmental goals.

The SGP program brought together stakeholders to identify important issues, conduct demonstration projects, and develop consensus policy recommendations that offered opportunities for reducing pollution. The stakeholders included industry, labor, environmental groups, state and local government, and other federal agencies. The metal‐finishing industry was represented by the National Association of Metal Finishers, American Electroplaters and Surface Finishers Society, Metal Finishing Suppliers Association, and Surface Finishing Industry Council. Through the SGP (USEPA 2001), the participants worked together to improve environmental performance and the bottom line.

Participation required top management commitment to the implementation and maintenance of an approved Environmental Management System (EMS). The EMS has caused management to take careful note of the true costs of pollution and institute policies and procedures to eliminate this waste at its source (USEPA 2003a). The results of these efforts have provided the first large‐scale quantification of the power of pollution prevention for achieving significant reductions in pollution and the resulting economic benefits in the metal‐finishing industry. The SGP program was designed to help a metal‐finishing company achieve its goals – both environmental and economic. A wide variety of state and local SGP resources (USEPA 2001) were available to provide a company with the tools need to get the job done. These include the following:

- Free, non‐regulatory environmental audits

- Funding for environmental technologies

- On‐site technical assistance in (evaluation and planning) achieving compliance and improving pollution prevention, safety, and health measures

- Free assistance from interns to help fill out the SGP data worksheets

- Free workshops on energy, water, and waste reduction

- Regulatory flexibility

- EMS training

- Public recognition

All parties benefited from the use of these tools. A few of the advantages listed in the project report are listed here.

- Companies received the incentives and resources needed to take the risk of going beyond compliance requirements.

- As the participating companies employ less‐polluting technologies, waste is reduced, less pollution is discharged to the environment, and the plant saves money, becoming more cost efficient and competitive.

- As the results demonstrated in the participating plants are employed by other plants to reduce pollution and improve competitiveness, the practices of pollution prevention are spread throughout the industry.

- The industry as a whole benefits from the positive action of SGP member companies.

- As the metal‐finishing industry becomes increasingly more self‐regulated, government regulators – from the EPA to the local publicly owned treatment works – save time and money.

The SGP has seven environmental performance goals (USEPA 2001) that form the core of the program (see Table 7.1). Through the end of 2000, many participants had already made significant progress toward meeting the goals, which translated into real environmental gains:

- 380 million gal of water conservation

- 120 million lb of hazardous waste not sent to landfills

- 665 000 lb of organic chemicals not released to the environment.

A comparison of the reductions achieved through 2000 and 2003 shows continuing and significant improvements in pollution prevention. This continued progress of the participants is a positive indicator of the benefits of a program driven by the employment of the EMS. The SGP participants were provided free, non‐regulatory environmental audits and access to technical support in achieving compliance and improving pollution prevention. Data like this readily demonstrates the power of the EMS management tool to reduce pollution. But to see how this progress was achieved, we must examine the role of pollution prevention (P2) technologies in enabling the reductions.

Table 7.1 Progress towards SGP goals.

| SGP goal | Average achievement by SGP metal finishers (over all projects) | |

| 2000 | 2003 | |

| 1) 50% reduction in water usage 2) 25% reduction in energy use 3) 90% reduction in organic toxic release inventory (TRI) releases 4) 50% reduction in metals released to water and air 5) 50% reduction in land disposal of hazardous sludge 6) 98% metals utilization 7) Reduction in human exposure to toxic materials in the facility and surrounding community |

41% reduction 14% reduction 77% reduction 58% reduction 36% reduction 17% utilization factor 51% of activities accomplished |

56% reduction 41% reduction 84% reduction 65% reduction 48% reduction 64% utilization factor 85% of activities accomplished |

7.8.2 The Role of Pollution Prevention Technologies

7.8.2.1 Moving Toward the Zero Discharge Goal

A highly desirable “state” for environmental protection would be Zero Discharge of pollutants to the air, water, and land. Today, this is a goal not yet realized. However, “approaching” Zero Discharge has been found to be realistic, as demonstrated by the continual improvement in environmental performance achieved in the SGP for the metal‐finishing sector. Approaching Zero Discharge can be defined as reducing wastes emitted from a process by a significant amount, with significant reduction ranging from a low defined by the regulatory standard and the high defined by the technology employed.

There are two key elements to achieving movement toward the state of Zero Discharge – implementation of an EMS and deployment of certain technologies based upon pollution prevention. The framework of an EMS is the management tool that provides a state of “continuous assessment and compliance of plant operations,” while P2 technologies provide the technological tools needed to achieve significant improvements in performance and reductions in generation of waste.

7.8.2.2 Planning and Implementation

As part of the planning phase, a compliance assessment of a participating plant is necessary to establish a baseline against which progress and savings in incremental costs can be measured. The goal of the plant assessment is to identify the root causes of the most significant problems, to identify areas in which P2 options could save the most money, and to assign priorities to address the most significant problems. The plant assessment must include an inventory of all chemicals, wastes, bath chemistries; the overall plant layout; and a site inspection. Once the problems are identified and prioritized, various solutions can be proposed and the effects of their deployment evaluated. A comprehensive plan addresses housekeeping and maintenance issues in order to sustain any P2 efforts and also to establish good standard practice.

This planning approach is most efficiently implemented through an EMS. In addition, the imperatives of “total quality management” apply. Management must buy into the process and be willing to provide the necessary resources to achieve success. Experience has shown that often the best solutions come from those working most closely to the problem. It is important that employees be included in the improvement program and kept well informed so that they will become stakeholders in the process.

Implementation through an EMS has several advantages. First it is more effective because it provides a tool for involving management through its provision for continuous improvement in both environmental performance and worker health and safety. Second, it provides a mechanism to integrate process and product quality issues that influence reduction of waste and the improvement of productivity and profitability. The review of these considerations should be incorporated into the process and reviewed over time as a pathway for identifying future opportunities and establishing priorities. This process leads to the identification of the power of pollution prevention technologies to achieve these savings offered by waste reduction. The Agency provides an EMS template tool (USEPA 2004; Stander and Theodore 2008) to assist those who are interested.

Many of the same elements that must be defined for the compliance assessment are also needed to establish an EMS. Certification under the ISO 14001 – an EMS that is standardized worldwide – is being increasingly required of those companies engaged in the manufacture of products for export, including components in the supply chain of such products. Also the EPA offers Compliance Incentives – “policies and programs that eliminate, reduce, or waive penalties under certain conditions for business, industry, and government facilities which voluntarily discover, promptly disclose, and expeditiously correct environmental problems” and is including a requirement for the implementation of EMSs in settlements. Information about these incentives, programs, and the environmental benefits achieved by such programs may be found on the Internet (http://www.epa.gov/compliance/incentives/index.html).

7.8.2.3 Practicing Pollution Prevention

Technologies based on the precept of Pollution Prevention serve to eliminate the generation of wastes or to reduce the disposal of wastes through recycle/reuse. Pollution in the metal‐finishing industry is basically the discharge of some unwanted form of material or other resource (energy, labor, time, etc.). Loss of these resources equates to the loss of profit and economic productivity. It stands to reason that the more of a resource used above the minimum required by the process, the more this incremental use (read: “waste”) adds to the “unnecessary” component of the total costs of the operation. In the case of water use, for example, this unnecessary cost is not just the cost of the excess water wasted. The cost of this waste is magnified by the costs for its overall management for treatment and disposal, including the capital and operating costs for moving the excess water through the process, its cleaning, and the disposal of the treated water and any residual wastes. The treatment and disposal costs are usually more costly than the initial raw material. Often these costs (process operations and compliance costs) are not tracked by a company because the accounting process used is inadequate to perform such tracking.

Companies participating in the SGP have found significant cost savings by implementing P2 practices (USEPA 2001). Significant cost savings result in improved economic efficiency and an improved bottom line on the balance sheet, making the operation more competitive. Other advantages include the protection of employees, reduction of liabilities, and, at the same time, enhancement of the company's business image.

Success in achieving the goals of the SGP for the metal‐finishing sector has been attributed largely to the employment of pollution prevention techniques. A principal purpose of the program was to demonstrate the attractive environmental and economic advantages offered by P2‐based approaches to waste reduction. The outcome anticipated was to “stimulate a keen awareness and appreciation” of these extremely valuable tools so that they would be adopted into everyday practice on a sector‐wide basis. In addition, the adoption of an EMS and integration into company operations ensures continued improvements (both in environmental performance and in cost savings) within the entire fabric of the participating companies.

There are many approaches to reduce pollution in various unit processes that were investigated and documented by USEPA sponsored research in the 1980s, including housekeeping and maintenance methods and management of process chemicals and rinse water. These methods are described in the EPA Capsule Report entitled Approaching Zero Discharge in Surface Finishing (USEPA 2000) and the training course document entitled P2 Concepts & Practices for Metal Plating & Finishing (AEFS, American Electroplaters and Surface Finishers Society). These learning aids address a number of process design areas such as those listed in Table 7.2.

Transitions of manufacturing operations to P2‐based systems have been demonstrated using a range of technology options from relatively simple improvements in existing process technology to more sophisticated approaches based upon significant process changes. There are numerous examples of the power of pollution prevention technologies, ranging from relatively simple improvements of water management to more sophisticated recovery processes, as documented in the results of the SGP and other programs.

Table 7.2 Pollution prevention technologies for surface finishers.

| To improve in these operations | Employ these technologies and practices |

Extend bath life

|

|

Reduce water consumption

|

|

Minimize waste

|

|

Reduce the use of hazardous chemicals

|

|

7.8.2.4 Case Study: An Emerging Profitable Pollution Prevention Technology

The USEPA recently completed a study of the proprietary Picklex process. Picklex® is a “‘non‐polluting’ pretreatment/conversion coat which replaces chromate conversion coating and zinc & iron phosphatizing in powder coating, paint and other organic finish applications” (Ferguson and Monzyk 2003; Ferguson et al. 2001).

Description

Metal pretreatment is crucial for cleaning and oxide removal to obtain proper performance and durability of the produced part, and it usually involves many tanks with various purposes. For example, aluminum anodizing may require eight pretreatment tanks; in conventional chromate conversion coating, there are twelve stages, while conventional zinc phosphatizing requires six. All of these baths contain heavy metals and must be dumped periodically.

The volume of hazardous/toxic waste streams produced from metal surface–finishing operations is significant (USEPA 1995a). The elimination of any of the surface‐processing steps is beneficial to the manufacturing process because it reduces processing costs, waste production, and energy consumption. Strong acids used in the pretreatment of metals pose a great health and safety risk to workers. With this in mind, a no‐waste or waste‐reducing surface‐finishing agent designed to lower processing costs for metal‐finishing operations would be of great benefit.

The Picklex process (a proprietary process) is one such alternative to conventional metal surface pretreatment that offers significant reductions in waste generation. The process was developed by International Chemical Products, Inc. with assistance from the USEPA. The Picklex process works in a completely different way than conventional processes. It incorporates the corrosion products from the metal surface into the protective coating that is applied to that same metal surface. This new P2 approach “thinks outside the box” by solving the common environmental problem of metal buildup in the processing tanks while forming a protective surface coating on the work piece. A two‐phase program was undertaken to evaluate the ability of Picklex to perform technically and economically as a pollution prevention–based replacement for conventional metal pretreatment or pretreatment/conversion coat in finishing operations. The goal was to demonstrate its potential to eliminate or significantly reduce the amount of hazardous and toxic chemicals consumed and the amount of pollution generated while maintaining equal or better product performance properties.

A broad laboratory evaluation of Picklex was undertaken in which full multistep, bench‐scale, batch operation tests using side‐by‐side test lines of seven conventional processes and of Picklex were performed. The results of the laboratory tests were quite favorable, and field tests (Ferguson and Monzyk 2003) were conducted to evaluate in‐plant performance in side‐by‐side tests with conventional preparation technologies. Only the most promising applications – the replacing of chromate conversion coating and zinc phosphatizing – were taken to field evaluation. In these focused field tests, Picklex was used to prepare aluminum and steel substrates for powder coating only. Although the testing scope was narrowed, it was more detailed. A total of 41 different combinations of substrate, degreaser, pretreatment, conversion coat, and powder coat were tested in the field evaluation. Only uncontaminated panels and components, without corrosion products, were used. The results for all test cases demonstrated that the quality of the final product was equal in all respects to conventional practice. Product quality was targeted as the single most important acceptance criterion within all the comprehensive results, because if the final product quality was not acceptable, the pollution reductions would not matter. The field test results replicated those obtained earlier, indicating that the lab testing may be used to accurately predict results achievable in practice.

7.8.2.5 Environmental Benefit

Two commercial processes, chromate conversion coating and zinc phosphatizing, were employed in the field tests as the experimental control baseline (Figures 7.3 and 7.4, respectively). Metal buildup in these conventional processes ruined the baths, and the baths had to be dumped. In the metal‐finishing sector, the discarding of such metal‐containing waste streams is a major contributor to pollution. The Picklex chemical used in the process tank is used up on the product; however, with filtering, the bath does not become contaminated. As a result, it is not necessary to dump the bath to control impurity buildup, and the chemical make‐up is simply added to the bath as needed. This process was demonstrated to have a strong potential as a leading technology for pollution prevention in surface preparation operations.

As can be seen in the comparison of the conventional practices to this emerging technology, the Picklex process eliminates up to eleven steps in metal‐finishing processes. The reductions of waste at the source were very significant. These reductions were accomplished by the elimination of the hexavalent chromium tank and subsequent rinsing operations; the elimination of the acid baths used for etching and cleaning along with subsequent rinsing operations; the elimination of the zinc phosphatizing baths and subsequent rinsing operations; and the elimination of the deoxidizing bath and subsequent rinses. All of the steps eliminated are steps that emit pollution. In addition, the Picklex process significantly reduces the pollution from the remaining steps. It does this while providing the same high‐quality finish and wear resistant capabilities as the conventional processes.

Figure 7.3 Comparison of Picklex to conventional chromate conversion coating.

Figure 7.4 Comparison of Picklex to conventional zinc phosphatizing.

Although normally the Picklex bath does not need to be dumped, but, as part of the study, the bath was evaluated for waste treatment issues in the event of a spill or accidental contamination. Fresh, spent, and impurity‐spiked spent Picklex samples were treated using the conventional pH 9 precipitation industrial wastewater treatment method to produce samples for a waste disposal assessment for Picklex. The waste solids were assessed for toxic leachability. The treated water supernatants for discharge were also examined and found as most likely dischargeable. Waste treatment may not be frequent or necessary in many processes. Actual discharge limits from industrial waste treatment plant operations are site‐specific and are determined on a case‐by‐case basis with local, state (and federal only where necessary) regulatory agencies. Hence, no exact classification of these potential waste solutions is possible until a specific location is known. All leachates are passed with respect to the applicable federal regulations (USEPA 1995b). Therefore, Picklex does not appear to present unusual waste treatment issues.

7.8.2.6 Economic Benefit

A cost comparison was made for two most promising processes – replacing chromate conversion coating and zinc phosphatizing. These were chosen based on the potential cost savings that industry could achieve. There would appear to be a significant economic incentive to migrate existing practice to this new technology, based on the significant capital and annual operating costs that is projected for the Picklex technology, summarized in Table 7.3. In fact, a new shop adopting the process in place of chromate conversion coat would save capital costs of $254 000, with the reduction of the process from 12 to 1 tank (Figure 7.3). For zinc phosphatizing on steel, the savings is estimated to be $230 000.

Table 7.3 Potential cost savings.

Source: From Ferguson and Wilmoth (2000) and Ferguson et al. (2001).

| Cost type | Savings of Picklex over conventional process | |

| Chromate conversion coat on aluminum ($) | Zinc phosphatizing on steel ($) | |

| Capital cost savings | 254 000 | 230 000 |

| Annual operating cost savings | 46 000 | 32 000 |

7.8.2.7 Technology Transferability

The Picklex technology is very robust and flexible (Ferguson and Monzyk 2003). It is applicable from the very large to very small operations. It can be used in a new installation, in a retrofit for process modernization, or as a drop in replacement for any existing facility. Picklex can be applied by dipping the part in tanks or by spraying or brushing. Cost savings are very significant and are a function of the size of the facility and the number of processing lines that are required. Transferability is enhanced by the prospective significance of the overall facility cost savings and productivity improvements offered.

7.8.3 Value‐Added Chemicals from Pulp Mill Waste Gases

Methanol, formed during the pulping of wood and is contaminated with reduced sulfur compounds and terpenes, is the largest single source of VOC emissions from kraft pulp mills, accounting for 70–80% of total emissions. The Cluster Rule (Cluster Rule Regulation: 40CFR Part 63 1998) limits methanol emissions for all pulp mills in the United States. Canada faces similar legislation (Das 1997, 1999a, b; Das and Houtman 2004; Das and Jain 2001).

Methanol emissions can be reduced by collecting condensate streams from the digesters, evaporators, and other sources in the mill. The collected condensate streams can then be steam‐stripped to concentrate the methanol for incineration. A few mills are “hard‐piped” to send this methanol‐laden stream to bio‐treatment plant, thus avoiding incineration.

Stripper overhead gas (SOG) contains roughly equal part of methanol and water (40–50 wt%) and roughly equal parts of TRS and terpenes (1–5 wt%).

In the United States, the SOG is likely to be burned in an incinerator, kiln, or boiler. Recently, some mills have found it advantageous to rectify the SOG to about 80% methanol and collect it as a liquid, which has a higher fuel value. With this concentrated (70–80%) methanol stream available, plants can cut down on the amount of natural gas that must be bought.

A process has been developed at Georgia‐Pacific that converts the methanol and TRS (mostly mercaptans) in the rectified SOG into formaldehyde. Based on work by Wachs (1999a, b), this patented catalytic process (Burgess et al. 2002) has achieved commercially viable yields of formaldehyde (70–80%) from a typical pulp mill SOG feedstock containing methanol, water, and TRS compounds.

The conversion of methanol and TRS to formaldehyde presents kraft mills with a more profitable alternative for SOG than incinerating the gas as a fuel. The formaldehyde produced can be used by resin manufacturers to produce thermosetting resins commonly used in plywood and other structural panels. A typical pulp mill of 2000 air‐dried tons per day (ADTPD) output may achieve a payout of 2–4 years, depending on the price of methanol and local economics.

Table 7.4 Annualized income, costs, and earnings 2000 ADTPD mill, 14 lb methanol/T SOG.

Source: From Burgess et al. (2002).

| Income 15 000 000 lb/year formaldehyde (50%) at $0.06/lb, FOB mill | $900 000 |

| Operating cost | |

| Direct labor | $110 000 |

| Utilities | $25 000 |

| Methanol in feed at $2.25/MMBTU fuel value | $260 000 |

| Misc., catalyst, supplies, etc. | $70 000 |

| Total operating cost | $465 000 |

| Gross margin | $435 000 |

| Depreciation | $210 000 |

| Earning before tax | $225 000 |

| Credit for steam generated (depending on the mill's steam balance) | $95 000 |

| Credit for terpene recovered and sold | $110 000 |

| Credit for SO2 recycled | $45 000 |

| Total by‐product credits | $250 000 |

| Total earnings, including by‐product credits | $475 000 |

The process also produces two levels of low‐pressure stream, 60 and 70 psig, usable within a paper mill, by reducing most of the methanol to formaldehyde, rather than CO2. The reduction in CO2 emissions is about 80–85% of the amount otherwise generated by incineration or by the bio‐treatment plant. For a 2000 APTDP mill, this equates to 28 T/Y of CO2 emissions that are avoided.

A typical itemization of income, costs, and earnings is given in Table 7.4. For a 2000 ADTPD mill, a payout of 3–4 years is calculated based on formaldehyde prices of $0.06/lb (50%) basis. This assumes a customer‐shipping radius of 500 miles from the mill producing the formaldehyde. A heat value credit to the mill is included (equivalent of natural gas fuel) for the methanol that would otherwise have been incinerated and used to generate steam via heat recovery exchangers.

7.8.4 Recovery and Control of Sulfur Emissions

Sulfur is often considered one of the four basic raw materials in the chemical industry. It can be recovered as a by‐product from sulfur removal and recovery processes (Kirk and Othmer 2004). Historically, sulfur recovery processes focus on the removal and conversion of hydrogen sulfide (H2S) and sulfur dioxide (SO2) to elemental sulfur, as these species represent significant emission from pulping process. Various processes for the removal of SO2 in the combustion gases are available. Direct catalytic oxidation of SO2 to SO3, and subsequent absorption of SO3 in water to produce sulfuric acid, is an alternative method (Paik and Chung 1996). Total mill TRS emissions of 10–20% are contributed by vent streams from brownstock washers, foam tanks, black‐liquor filters, oxidation tanks, and storage tanks that are not typically collected in the noncondensable gas system (Pinkerton 1999). The emissions from these sources can be collected and combusted for energy recovery, reducing the atmospheric emissions of TRS and VOCs.

7.8.4.1 Freshwater Use Reduction and Chemical Recovery and Reuse Save Million at Pulp Mill

Effluent Discharges

Before pulp mill effluents can be released to the environment they must be treated. Primary treatment involves the use of settling ponds or tanks in which suspended solids settle out of the liquid effluent. Solids can be composted and spread on land, converted to other useful products, or incinerated. Secondary effluent treatment includes oxidation and aeration in shallow basins having wide areas or in smaller areas using mechanical agitators and spargers to oxygenate fluids before release. Biological filter systems can be used to remove organic compounds and heavy metals, and often the process can be accelerated by adding nutrients and by using oxygen rather than air. In some areas, natural wetland systems have been designed to achieve this. Other means of treatment include lime coagulation and the elevation of pH to precipitate organic color bodies as calcium lignates. Once precipitated, the sludge is dewatered and incinerated to destroy organics.

It has been reported by NCASI that there was a 30% reduction in effluent flow from mills between 1975 and 1988. During the same period, final effluent 5‐day BOD and TSS decreased by 75 and 45% (NCASI 1991). Data for 1975, 1985, and 1988 are presented in Table 7.5. These reductions will continue as pulp and paper mills implement the so‐called best management plans (BMPs) required by the Cluster Rule. BMPs will require better management of process losses and spills and are expected to reduce effluent discharges. For example, in roughly 10 years, Simpson Tacoma kraft mill reduced its freshwater consumption by approximately 50% through various pollution prevention methods (K. Schumacher and M. Mammenga, personal communication; USEPA 1992a, b).

Table 7.5 Effluent discharges from pulp and paper mills.

Source: From Das (1997).

| 1975 | 1985 | 1995 | |

| Effluent flow (gal/T) | 22 800 | 17 200 | 16 000 |

| BOD (lb/T) | 18.0 | 4.8 | 4.4 |

| TSS (lb/T) | 13.0 | 8.3 | 7.1 |

Simpson Tacoma now uses about 18 million gal of freshwater per day (mgd) vs. 32 mgd in 1990s. This reduction in freshwater usage saves about $1.92 million/year (350/MG, city of Tacoma charges per average fixed and variable cost). The plant also saves money through reducing sodium hydroxide (NaOH) losses to sewers and to product fiber, by stopping overflowing weak washing dilute NaOH solution and through recycling processed water. Otherwise, NaOH would be needed to the process to make up for soda (sodium) lost. The saving is about 3.4 million/year (based on $375/T of NaOH and 25 T of NaOH saving per day). Simpson also saves $0.18 million/year by reducing losses of black liquor sulfur to sewer and stack (K. Schumacher and M. Mammenga, personal communication).

Other firms save water by installing savealls (devices which separate fiber from process water), heat exchangers, and other equipment which permit more reuse of process water. Internal water cleaning systems make it possible to substitute filtered white water for clean water. Separating process cooling and clean water is often necessary to achieve balance in operations and water use.

7.8.4.2 Brine Concentrator for Recycling Wastewater

Brine concentrators are vapor compression evaporator systems that produce distilled water and a very small salt concentrate stream. These are ideal for water recycling because the concentrate stream is so low that wastewater can be treated economically with a very high recovery and with no liquid discharge (Dalan 2005).

To comply with the regulations, both new and existing power plants that were using river water had to recycle their water wastes. Although vapor compression was not new to industry as an energy source, the technological fit with power plants was a natural because it allowed these facilities to use electricity they were generating as the source of the mechanical energy needed in recycling water.

Federal law was not the only factor prompting industry to turn to the use of brine concentrators for recycling wastewater. All over the country, there were local siting regulations, as well. Thus, with the advent of the private power industry in the early 1990s, entrepreneurs turned to Zero Discharge water systems, which allowed them to use sites with a limited water supply, far away from discharge points. Similarly, the move to clean‐burning natural gas diminished the importance of locating power plants near sources of fuel or water.

As of 2004, there were approximately 60 brine concentrators in the Unites States. They are sold as package plants, designed and constructed with energy conservation principles. All the original units were at coal‐fired power plants, but as metal smelters, manufacturers of chemicals and semiconductors, and other enterprises began to recognize the need to eliminate water discharges, the use of brine concentration has spread.

7.8.4.3 Economics of Brine Concentrator Systems

Based on the parametric cost information on brine concentrator systems, we will now overview some economic aspects of these systems.

Brine concentrators, and by extension, integrated zero liquid discharge systems, only make sense in grassroots facilities only when

- there is a shortage of surface or well water

- the facility needs water to operate

- there is no water discharge option, such as a source of potable water or a river

- a discharge permit is unobtainable

Zero Liquid Discharge takes away the siting constraint; that is, it is no longer necessary to locate the plant near a large usable water source or suitable discharge point. The economic advantage of such an effect is hard to generalize, being very specific to the actual circumstance.

The NPV of a Zero Discharge facility is negative. Dalan and Rosain (1992) found that a 265 gpm brine concentrator had operating costs of $8.94/1000 gal of water treated (total of $1 252 600/year), while the avoided cost of extra demineralizer regeneration chemicals was $216 000/year. The avoided cost amounts to 1.54/1000 gal. Since any dollar amount here is an operating expense, the CF is negative.

Table 7.6 Operating cost breakdown for a 265 gpm system resulting in a cost of $9.62/1000 gal of feed.

Source: From Dalan and Rosain (1992), updated by Dalan (2005).

| Item | Consumption | Unit cost ($) | Annual cost ($) |

| Operating labor | 1 mhr (maximum hourly rate)/h | 50/mhr | 438 000 |

| Maintenance (labor) | 2 mhr/h | 50/mhr | 87 600 |

| Maintenance (materials, including spare parts) | 80 000 | ||

| Electricity | 1 617 kWh | 0.05/kWh | 707 000 |

| Chemicals | |||

| Sulfuric acid | 293 lb/day | 0.06/lb | 6 416 |

| Polymers | 40 lb/day | 1.50/lb | 21 900 |

| Total chemicals | 28 316 | ||

| Total annual operating cost | 1 340 916 | ||

| $/1000 gal of feed | 9.62 |

A typical specific operating expense is in the $5–7/1000 gal treated range. In this estimate is the price of electricity at a retail price of 0.05/kWh. In grassroots power plant planning, the electricity is many times considered a parasitic load on the power plant (electricity needed to produce the power). In this accounting method, the cost of electricity is zero. The elimination of electricity as an operating cost brings the total treatment cost down to the $2–3/1000 gal range. The typical energy load for a brine concentrator is 100 kWh/1000 gal of water produced.

The determination of water economics is very geography specific. For example, in western Washington, water and sewer bills typically are in the $1–2/1000 gal range, whereas in eastern Washington, water costs more, if indeed it is economically available.

For non‐power plant applications, local high prices for electricity can be overcome by seeking out alternate energy sources. Compressors (the majority energy user) in brine concentrator plants have been installed that are steam driven or natural gas (via a natural gas engine) driven. Table 7.6 presents breakdown of typical operating costs (Dalan 2005; Haussman and Rosain 1996).

For existing facilities, installing a Zero Discharge plant makes sense when

- the discharge permit conditions change, with the result that the existing facility can no longer be operated economically

- the cost of water rights plus treatment fees exceed the operating costs of a Zero Discharge facility

This last point is illustrated by a mini‐case study.

7.9 Use of Treated Municipal Wastewater as Power Plant Cooling System Makeup Water: Tertiary Treatment vs. Expanded Chemical Regimen for Recirculating Water Quality Management

7.9.1 Introduction

Every day, water‐cooled thermoelectric power plants in the United States withdraw from 60 billion to 170 billion gal of freshwater from rivers, lakes, streams, and aquifers, and consumes from 2.8 billion to 5.9 billion gal of that water. Freshwater withdrawals for cooling in thermoelectric power production account for about 40% of all withdrawals, essentially the same amount as withdrawals for agricultural irrigation, as documented by the U.S. Geological Survey. Sustained droughts nationwide underscore the critical need to think about using treated municipal wastewater (MWW) for use in cooling in electric power generation. It needs a great deal of water for electric power production, to condense stream in the power plant stream cycle. Air cooling is possible, but it is more costly and less efficient. Water will continue to be the preferred coolant for new thermoelectric power plants (Dzombak 2013).

Motivation for the project: Increase in demand for electricity brings with it an increase in water needed for cooling. The cooling of thermoelectric power plants accounts for 41% of all freshwater withdrawal in the United States, i.e. approximately the same amount of water as is withdrawn for agricultural irrigation. Some areas of the United States have little or no freshwater available for use. Alternative sources of water are needed for new electric power production. The U.S. Department of Energy has been conducting and sponsoring research to investigate the feasibility and costs of using alternative sources of water for power plant cooling, especially in recirculating cooling systems which are required for most new power production in the United States.

Goals and highlights of the project: Treated MWW is a common, widely available alternative source of cooling water for thermoelectric power plants across the United States, as determined in a predecessor DOE project (2006–2009) by the project team. However, the biodegradable organic matter, ammonia–nitrogen, carbonate, and phosphates in the treated wastewater pose challenges with respect to enhanced biofouling, corrosion, and scaling, respectively. The overall objective of this study was to evaluate the benefits and LCC of implementing tertiary treatment of secondary treated MWW prior to use in recirculating cooling systems.

The study comprised bench‐and pilot‐scale experimental studies with three different tertiary treated MWWs, and LCC and environmental analyses of various tertiary treatment schemes. Sustainability factors and metrics for reuse of treated wastewater in power plant cooling systems were also evaluated. The three tertiary treated wastewaters studied were secondary treated MWW subjected to acid addition for pH control (MWW_pH); secondary treated MWW subjected to nitrification and sand filtration (MWW_SF); and secondary treated MWW subjected to nitrification, sand filtration, and GAC adsorption (MWW_NFG).