appendix B

ACCOUNTING FOR INTERCOMPANY INVESTMENTS

Throughout this text we have shown you excerpts of financial statements from various Canadian and international companies. Without exception, all of those financial statements were consolidated financial statements. Consolidated financial statements become necessary when one company buys a controlling ownership interest in another company, thus creating a more complex organization and the need for more complete financial reporting than for an individual company. Before we end this text, we want to provide you with a broad understanding of how financial statements become consolidated, and the implications of using consolidated statements for decision-making.

Because an investment in a company's common shares carries with it a right to vote, one company can influence and, under the right circumstances, control the activities of another company. As a result of this, some important financial reporting issues arise for organizations that are considered complex due to intercompany investments. We start with a brief discussion of the purpose of such intercompany investments, and then turn to aspects of their accounting and analysis.

PURPOSE OF INTERCOMPANY INVESTMENTS

A company may have many reasons for acquiring an ownership interest in another company. Buying the shares of another company may be viewed as a good short-term or long-term investment, with such investments broadly classified into two types: non-strategic and strategic.

Non-strategic investments are ones where the investing company (the one buying the shares) has little or no influence over the operations of the other company. The equity securities that a company carries in its current asset account, called short-term investments (or marketable securities), which were discussed in Chapter 6, are examples of this type of investment. If the shares are bought for this reason, the number of shares purchased is usually small compared with the number of outstanding shares. Consequently, the acquiring company has little influence or control over the affairs of the company in which it has invested. Such investments are sometimes called passive investments or portfolio investments because the acquiring company cannot exercise any influence or control over the decisions of the acquired company. Some non-strategic investments can also be long-term, if management's intention is to hold the security for long-term returns.

A second major reason for obtaining ownership of the shares of another company is to influence or control the decisions that the other company makes. These are strategic investments, in which the acquiring company (the investor) intends to a have long-term strategic relationship with the acquired company (the investee). Common targets for this kind of purchase are competitors, suppliers, and customers. Acquiring a block of shares in a supplier or customer allows the acquiring company to exercise some influence over the production, buying, and selling decisions of the acquired company, which may benefit the acquiring company. If the block of shares purchased is large enough, the acquiring company could have a controlling interest in a competitor, which would allow it to increase its market share by increasing its productive capacity, its geographic market, or both. Buying a controlling interest in a supplier or customer allows the company to ensure a market in which it can buy its raw materials (in the case of a supplier), or sell and distribute its product (in the case of a customer).

Buying a supplier or customer is sometimes referred to as vertical integration. George Weston Limited is an example of a company that is vertically integrated. It owns 100 percent of Weston Foods, a producer of baked goods, and 62.5 percent of Loblaw Companies Limited, a distributor of food, drug, and general merchandise where the Weston baked goods, among other things, are sold. It had previously also owned dairy and bottling operations that supplied Loblaw.

Combining with a competitor is sometimes referred to as horizontal integration. Horizontal integration may offer benefits that come from economies of scale. The company may be able to reduce its workforce or use a single distribution system to avoid duplication of effort. It might also allow the company to enter and compete in different segments of the market. Cara Operations Limited, a large private Canadian corporation, is an example of a company that is horizontally integrated. Cara owns several different restaurant and food services businesses, including Swiss Chalet, Harvey's, Kelsey's, and Montana's Cookhouse. Through the different chains, it competes in both the fast food segment of the restaurant business and the casual dining segment.

Another reason for buying and controlling another company is diversification. If a company is in a seasonal business, it can protect itself from seasonal declines in one business by investing in another business that is counter-seasonal. Seasonal businesses are those that have significant peaks and valleys of activity during the year. A greeting card company is an example of a seasonal business. Some cards, such as birthday cards, are purchased relatively evenly throughout the year. Other cards, such as Christmas and Valentine cards, cause peaks in revenue generation. Such a company may wish to diversify by buying into an automobile dealership business. The peak times for the dealership are likely to be the late summer, when the new cars are introduced, and early spring, when people anticipate travelling over the summer. The greeting card business and the automobile dealership would have peak activities at different times, which would help to even out the revenue flows for the whole business.

Algoma Central Corporation is an example of a diversified Canadian business. Its main focus of operation is marine transportation. It operates several ships, organizes the transportation of goods, provides for the repair and maintenance of ships, and provides marine-engineering services. This business depends not only on the type of goods shipped, but also on the economic environment of the countries to and from which it transports goods. Algoma has countered some of the shipping industry's cyclical nature by investing in commercial real estate. It owns and manages various commercial properties in Ontario. This business is also subject to the economic environment, but is much more localized and would be unlikely to experience the same peaks and valleys as marine transportation.

METHODS OF OBTAINING INFLUENCE AND CONTROL

Perhaps the simplest way to obtain control of the assets of another company is to purchase the assets directly from that company. This is called an asset purchase. The accounting for asset purchases is discussed in Chapter 8. If several assets are acquired at one time, such as in the acquisition of an entire division or plant, a single price may be negotiated. As discussed in Chapter 8, this type of purchase is called a basket purchase. The total cost of the purchased assets must be allocated to the individual assets based on their relative fair market values.

When a company buys all the assets of another company, this does not give it influence or control over the second company: the buyer only controls the assets it has purchased. The company that sold the assets can continue to operate, but must now make arrangements to use different assets to generate revenue. An asset purchase does not require consolidated financial statements. Once the new assets are recorded in the accounting system of the buying company, there are no further accounting implications.

The only way to obtain influence or control over another company is to buy its common shares in a share acquisition. The investor purchases the shares from the shareholders of the investee in exchange for cash, some of its own shares, some of its debt, or with a combination of all three (cash, shares, and debt). In a share acquisition, the investor can obtain a large degree of influence or control over the investee by acquiring more shares. That influence or control is obtained by exercising the voting rights that the investor obtains with the shares. Ultimate control over the investee's assets and liabilities will occur when the percentage ownership of the voting rights is greater than 50 percent. This is called a controlling interest.

An investor can sometimes effectively control an investee even though it owns less than 50 percent of the shares. This can occur in situations where the remaining shares are owned by a large number of investors, none of whom has a very large percentage ownership in the investee (the shares are said to be widely held in such situations). For example, if an investor owns, say, 40 percent of an investee and the rest of the shares are widely held, the investor may be able to effectively control the investee's assets and liabilities. Because it is possible to control with less than 50 percent, control is defined as occurring when one company has the “power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.”1

In a share acquisition, the investee remains a separate legal entity from the investor. The investor company is like any other owner in that it has limited liability with regard to the investee's debts. The investor's liability is limited to the amount invested in the shares. The separation of the legal status of the two companies is one reason this form of acquisition is appealing. The tax status of each company is also separate. Each company must file its own return. For accounting purposes, the separate legal status also means that the investor and the investee each keep their own accounting records, even if the investor has acquired 100 percent of the investee's shares. This presents an accounting problem if the investor controls the investee, because they are, in substance, one accounting entity.

VALUATION ISSUES AT DATE OF ACQUISITION

In any type of acquisition, whether the purchase is of a single asset or an entire company, the fundamental accounting valuation method at the time of acquisition is historical cost. Thus, the new asset or the investment in the investee is recorded at its cost. If the asset is acquired with a payment of cash, the amount of cash serves as the proper measure of the cost. If debt is exchanged for the asset or company, the present value of the debt should be used as the measure of cost.

When shares are issued in the acquisition, their fair market value at the date of acquisition should be used as the measure of cost. A problem exists in valuing shares when the share issue is large, because the number of shares outstanding increases significantly and the value of the investment acquired is not exact. How the market will adjust the existing share price to reflect this acquisition is not known at the date of the transaction. In these situations, instead of using the value of the shares to measure the acquisition, accountants sometimes turn to the fair market value of the assets acquired to measure the value of the shares given up.

Share Acquisition

In a share acquisition, the investor records the acquisition cost in an investment account. There is no breakdown of this cost into individual assets and liabilities in the investor's books, because the assets and liabilities do not technically belong to the investor; they remain the investee's legal property or legal obligation. An investor that owns a large enough percentage of the investee's shares may control the assets economically, through its voting rights, but it does not hold the title to the assets. Nor is it legally obliged to settle the liabilities. Under IFRS, we currently use the acquisition method to account for an acquisition of a controlling interest.

When a share acquisition results in gaining control of another company, the acquiring company (investor) is called the parent and the acquired company (investee) is called the subsidiary. As previously explained, both the parent company and the subsidiary company are separate legal entities that keep separate books, prepare separate financial statements, and pay separate taxes. To provide users with information about the whole economic entity or group (parent and subsidiaries), accountants prepare consolidated financial statements, which add the components of the various financial statements of the parent and the subsidiaries together. The consolidated statements enable users to see the total cash that the entity controls, the total inventory it owns, the total revenues it earns, and so forth. Complications arise in the consolidation process if there have been transactions between the parent and the subsidiaries. Because such transactions occur within the group or economic entity (parent and subsidiaries), they are deemed not to have occurred and they must be eliminated. More will be said about this later.

The annual report for H&M presented in Appendix A shows the financial statements for both the parent company and the group, or consolidated, financial statements. Normally in North America the parent company's financial statements are not presented in the annual report, only the consolidated ones. H&M's report gives us an opportunity to see the difference between the two sets of financial statements.

The Parent Company financial statements for H&M (pages A13–A16) present the legal view of the parent company. The shares it owns in all of the subsidiaries are reported on the Parent Company Balance Sheet in Financial Fixed Assets under the heading “Shares and participation rights.” The amount reported is SEK572 million. The names of all of the individual subsidiaries owned by H&M are listed in Note 24, shown in Exhibit B-1. The SEK572 million represents the cost paid by H&M for the shares of the subsidiaries. It is equal to the net asset value of those companies at the time of acquisition (remember, net asset value = assets − liabilities).

EXHIBIT B-1 H&M 2009 ANNUAL REPORT Excerpt from Note 24 to the Financial Statements

H&M 2009 ANNUAL REPORT Excerpt from Note 24 to the Financial Statements

In contrast, the Group Balance Sheet for H&M (page A10) includes all of the individual assets and liabilities of the subsidiaries added to the parent's assets and liabilities. Note that there is no “Shares and participation rights” asset on the group balance sheet; that single amount for the net assets is replaced by all of the assets and liabilities. When all of the assets of the subsidiaries are included (instead of only the net assets) the total group assets are SEK54,363 million, more than three times greater than the SEK17,148 million that the parent H&M reported! You can easily see how the group or consolidated financial statements paint a more complete picture of the assets that are under the control of H&M than the parent financial statements did.

As well as providing information about the total entity, consolidated financial statements hide information about the individual companies in the group. Because users are usually not given information about these individual companies, they have difficulty determining the risks and rewards contributed by each. To address this problem, if a company, through its activities, is involved in various industries or geographic locations, it is required to disclose segmented information in the notes to its financial statements. The segmented information provides some breakdown of accounts in the different segments (industries or geographic locations) so that users can evaluate the segments' potential future impact on the total entity. Note 3 on Segmented Information (page A22) from the H&M annual report provides information about sales, operating profits, and assets and liabilities in different regions. The information is still very highly aggregated—only a total asset and liability figure net of tax assets or liabilities is reported, not individual ones—but it helps a reader understand some of the risks and opportunities facing the enterprise.

As mentioned earlier, when the parent purchases a controlling number of shares in a subsidiary company, it has an investment on its books that it has recorded at the cost of the purchase. Because another company is being controlled and consolidated financial statements are therefore going to be prepared, the transaction is viewed as a basket purchase. The cost to acquire the subsidiary needs to be allocated to the subsidiary's individual assets and liabilities based on their fair market values at the date of acquisition, just as with any other basket purchase. This allocation is not recorded on the actual books of either the parent or the subsidiary, but instead is determined during the work sheet preparation of the consolidated financial statements. When the subsidiary's assets and liabilities are added to those of the parent so that consolidated financial statements can be prepared, it is the fair values of the subsidiary's assets and liabilities at the date of acquisition that are added to the historical cost assets and liabilities of the parent. The fair value at the date of acquisition is the “cost” to the parent company of these assets and liabilities and is normally different from the cost of the same assets and liabilities when the subsidiary purchased them.

The Acquisition Method

When allocating the purchase price, all the assets and liabilities in the subsidiary are first measured at their fair market values. Some assets that did not exist on the subsidiary's books may be found and included in this measurement process. For example, if the subsidiary developed a patent or a trademark internally, the costs of such an item would have been expensed (see Chapter 8 for a discussion of whether to capitalize or expense the costs of these types of assets). The parent would need to identify all the assets that the subsidiary owned or had the right to use, and establish values for those items using current items similar to them in the market, estimations of future benefits, or appraisals as a guide. By buying the shares, the parent is now also controlling these assets, and part of the acquisition cost should be allocated to them if they have a measurable market value. All of these assets and liabilities—those on the books and those that have value but are not on the books—are known as the subsidiary's identifiable net assets. In the year that a parent buys a subsidiary, the components of the assets and liabilities that were purchased will be disclosed in the notes to the consolidated financial statements. In 2008, H&M acquired 60 percent of Swedish fashion company FaBric Scandinavien AB. Exhibit B-2 is an excerpt from Note 21 of the 2008 financial statements and itemizes how the total acquisition cost of SEK927 million was allocated to the assets and liabilities. Note that SEK470 million was allocated to an intangible fixed asset for Brands, which had not previously been recognized on FaBric's financial statements.

EXHIBIT B-2 H&M 2008 ANNUAL REPORT Note 21 to the Financial Statements

If the purchase price is more than the fair market value of the identifiable net assets (often referred to as excess fair market value), another asset called goodwill must be reported (see Chapter 8). It represents all the unidentifiable intangible reasons that motivated the investor to pay more for the investee than the sum of the fair market values of the purchased company's individual assets and liabilities. For example, perhaps the investor expects to earn extra future cash flows as a result of economies of scale or synergies, or perhaps the business is located in a high-traffic area and so has a greater chance at higher revenues than businesses located elsewhere. Perhaps the sales personnel in the business have created a loyal customer following that leads to consistent revenues, or previous advertising campaigns may have made this a well-known business. In H&M's acquisition of FaBric, of the SEK927 million total acquisition cost, SEK496 million was allocated to identifiable assets and liabilities (including the intangible asset Brands discussed earlier). The balance of the cost, SEK431 million, was recognized as goodwill. If, on the other hand, the purchase price is less than the fair value of the identifiable net assets, negative goodwill is created. This negative goodwill is recognized as a gain on the purchase in the year it occurs. This is a topic for an advanced accounting course.

INCOME RECOGNITION ISSUES SUBSEQUENT TO ACQUISITION

Income recognition issues subsequent to acquisition are a consequence of the valuation decisions made at the date of acquisition. In the following subsections, these issues are discussed for asset acquisitions and share acquisitions.

Asset Purchases

Subsequent to purchase, these are accounted for in the same way as any other acquisition of assets. If the asset acquired is property, plant, or equipment, it is amortized like any other such asset. If the asset purchased is inventory, it ultimately affects the cost of goods sold when it is sold.

Share Acquisitions

The accounting treatment of income subsequent to a share acquisition depends on the level of control that the investor exerts over the investee. As examples of the conceptual differences, consider two extreme cases. The first case is one in which the investor owns only a few shares in the investee, and the second is one in which the investor buys 100 percent of the investee's shares.

Case 1

If the investor buys only a few shares of the investee, it has virtually no control or influence over the investee. The investor cannot dictate the dividend policy or any other strategic policy to the investee. As indicated earlier, this is a non-strategic investment. The shareholders of the investor company in such a situation are unlikely to be interested in the full details of the investee's operating performance. They are probably more interested in the cash flows that have come in from their investment (dividends) and in the current market value of the investment. Therefore, income recognition should show dividend revenue and the change in the value of the investment. As noted in Chapter 6, held-for-trading investments are valued at their fair market value, and any gains or losses resulting from the change since the last valuation are recognized in income of the period.

Case 2

In this case, where the investor owns 100 percent of the investee's shares, the investor's shareholders will likely want to know the operating details of the investee's performance because they economically control all of its assets and liabilities. For example, if the investee that was purchased was a competitor, the sales results of the purchasing company's product are the combined results of the investor and the investee. To show only the details for the investor would be misleading in terms of the resources controlled by the shareholders. The investor's shareholders would probably find information about the two companies' combined assets and liabilities more useful than simply a listing of the investor's assets and liabilities. A set of statements that conveys this information is a set of consolidated financial statements, as mentioned earlier. Consolidated financial statements are prepared as if the investor and investee were one legal company, because the two companies represent one economic accounting entity.

What Is Canadian Practice?

This section of the appendix will describe the guidelines that have been established under IFRS for the acquisition of various blocks of shares. It is important to understand these guidelines because they tell you how companies will describe their various acquisitions and how they are accounting for them. You will need to know the various methods used so that you can understand each one's effects on the financial statements.

Under IFRS, control is determined by the investor's power to govern the financial and operating policies of the investee so as to obtain benefits from its activities. As mentioned previously, this usually means that the investor owns more than 50 percent of the investee's voting shares; but in some situations, as mentioned previously, control can occur with less than 50 percent ownership.

Because control is evidenced by the ability to determine certain activities in another company, IFRS provides guidelines or recommended cut-offs for the percentages of ownership (in voting shares) that require different accounting treatments. Exhibit B-3 outlines these cut-offs:

- Small investments (less than 20 percent), ones that we will refer to as non-strategic investments, are accounted for as either held-for-trading or available-for-sale. Held-for-trading investments were covered in Chapter 6. For the purpose of the discussion in this appendix, we will assume non-strategic investments are classified as available-for-sale. Non-strategic investments can be subdivided into those that are current, which we usually label “short-term investments,” and those that are non-current, which are generally labelled “investments” and are long-term.

- Larger investments where control is present (greater than 50 percent) require consolidation; that is, consolidated financial statements must be prepared.

- For investments that fall between these two extremes, the companies are considered to be associated and the acquiring company is considered to have significant influence over activities in the investee. Significant influence is evidenced by being able to elect a person to the board of directors, having significant transactions between the two companies, or having an exchange of technology or managerial personnel. When significant influence exists, another method, called the equity method, is required. Each of these methods is discussed in detail in the following pages.

The percentage cut-offs identified in Exhibit B-3 are only a guide. If a company can demonstrate that it possesses either more or less control than the percentage ownership indicates, it can apply a different method. For example, a company may only own 15 percent of another company but, due to the volume of intercompany transactions, or the ability to elect someone to the board of directors, the investor may be able to exercise significant influence over the investee. The key issue in determining the appropriate accounting method to be used is not the percentage of ownership, per se, but whether the investor has significant influence or control over the investee. Each method carries its own set of accounting implications for the company, as discussed in the following subsections.

EXHIBIT B-3 ACCOUNTING METHODS FOR INVESTMENTS

Available for Sale

In Chapter 6, we identified four types of financial instruments: held-for-trading, available-for-sale, held-to-maturity, and loans and receivables. For simplicity, we assumed that all short-term investments were held for-trading, but management classifies the investment based on its intention and the features of the asset. Management can elect to not classify an investment as held for trading and instead classify it as available for sale. These investments are reported at their market value on each statement of financial position date, but the gains and losses arising from the change in market values are reported in other comprehensive income and not directly in net earnings. When an available-for-sale security is sold, the gains and losses are said to be realized and they are reclassified from other comprehensive income to net earnings. The basic difference between the two methods is that under the available-for-sale classification fluctuations in the market value of the security will not affect net earnings until the asset is sold. The reasoning behind this treatment is that, because the fluctuations in value are not a result of management decisions, the unrealized gains and losses should not be considered part of regular operations as depicted on the statement of earnings. Any dividends received while owning the shares are reported as investment income under both methods.

The details of the distinction between the held-for-trading and available-for-sale classifications are best left for intermediate level accounting courses. What you need to understand for the purpose of this appendix is that under both methods the investments are carried at market value on the statement of financial position; however, although the gains and losses on held-for-trading securities are recognized in net earnings as they occur, gains and losses on available-for-sale investments are recognized in net earnings only when the securities are sold.

Available-for-sale investments can be classified as either current or non-current assets, depending on management's intended holding period. For example, if management expects to build a new production facility in two years, it may start setting aside some cash or excess funds in investments. As management intends to hold the securities for longer than a year, the securities would be classified as non-current assets; but if management did need those funds before then, the securities would be available for management to sell.

It is possible for there to be no market value that is readily available for a security that management has designated as available for sale. This would be the case if the securities were part of a private corporation, or for some other reason were not actively trading on the stock market (for example, if the company were in bankruptcy protection). In these cases, it is not possible to value the investment at market value on the statement of financial position date and the cost method is instead used.

Cost Method

In the cost method, the investment is carried in the investment account at its cost. During the period in which the investment is held, dividend revenue is recognized as investment income. Because the security is not revalued to market, there are no gains and losses recognized until the security is sold.

IFRS INSIGHTS

The International Accounting Standards Board (IASB) has approved a new standard, IFRS 9, which replaces the existing standard for financial instruments. The new standard is not mandatory until January 1, 2013, and will modify some of the accounting for non-strategic investments and eliminate the option to use the cost method. The material in this appendix reflects the existing standard, although companies may choose to adopt the new standard before 2013.

Consolidation Method

As explained earlier in this appendix, consolidation is required when an investor (parent company) controls the activities of an investee (subsidiary). For instructional purposes, we will assume here that the investor owns more than 50 percent of the investee's outstanding shares. Because the subsidiary is still legally a separate company, the parent company records its investment in the subsidiary company in an investment account in the parent company's accounting system. However, because the parent company, through its ownership of the majority of shares, controls the subsidiary's assets and liabilities, it is probably more useful to the parent company's shareholders to report the full details of the subsidiary's assets, liabilities, and earnings, rather than a single amount in the investment account and a single amount of income from the subsidiary on the statement of earnings. The purpose of consolidating, therefore, is to replace the investment account with the subsidiary's individual assets and liabilities. On the consolidated financial statements, it then looks as though the two companies are one; that is, as if they had merged. You must recognize, however, that this is simply an “as if” representation of the combined company. The accounting systems are not merged. In fact, the consolidated statements are prepared on “working papers”; no actual entries are made to either company's accounting system.

Because consolidation reflects an acquisition, the consolidated statements are prepared using the fair market value of the subsidiary's assets and liabilities acquired, as well as any goodwill. These amounts are combined with the book values of the parent's assets and liabilities.

Equity Method

Between the two extremes of no control and complete control lies the situation in which the two companies are associated and the investor can significantly influence the investee but not completely control its decisions. Canadian practice is to refer to these investments as “investments in significantly influenced companies,” whereas IFRS uses the term “investment in associated companies.” In practice you may see both terms. The accounting method used, the equity method, tries to strike some middle ground between showing all the assets, liabilities, and income items in the financial statements (consolidation) and showing only the dividend revenue from the investment (available-for-sale method). The equity method requires that the investor reflect the effects of its proportionate share of the investee's financial results. Its share of the net assets (assets minus liabilities) is therefore reported as a single line item, “Investment in shares,” or “Investment in associated companies,” on the investor's statement of financial position. Its share of the net earnings is also reported as a single revenue item, “Equity in earnings of investee,” on the statement of operations. Because of the netting of assets and liabilities as well as revenues and expenses, this method is sometimes referred to as one-line consolidation.

To illustrate the entries made in a simple case using the available-for-sale method and the equity method, let us assume the following facts and refer to the investee as the associate company. The investor bought 30 percent of the associate's outstanding shares for $10,000. During the first year of the investment, the associate's earnings were $3,000 and dividends of $1,000 were declared. At the end of the year, the market value of the associate's shares was $11,000. In Case A, it is assumed that the 30 percent does not give the investor significant influence (available-for-sale method required), and in Case B, it is assumed that significant influence is present (equity method required). The entries that the investor makes to account for the investment in the first year are as follows:

Under the equity method, the entry to record the earnings shows that the investment account increases by the investor's share of the associated company's earnings. The investment account represents the investor's investment in the associate (its share of the associate's equity) and, as the associate company earns income and increases its shareholders' equity, the investor's records reflect that increase in value by the increase in the investment account. The credit part of this entry is to the statement of earnings in a line item called “Equity in earnings of investee” (abbreviated as EEI).

The entry to record the associate's dividends causes a decrease in the investor's investment account. This should make sense because, on the associate company's books, the declaration of dividends causes a decrease in the shareholders' equity of the company. Because the investor's investment account measures its share of that equity, the investment account should decrease with the declaration of dividends. Another way to think about this is to imagine that the investment represents a deposit in a savings account. The interest on the savings account would be equivalent to the subsidiary's earnings. Withdrawals from the savings account would be the equivalent of the dividends declared. Withdrawals decrease the balance in the savings account in the same way that dividends reduce the investment account.

The effects of those entries on the statement of operations and statement of financial position year-end balance are summarized in the following table:

CONSOLIDATION PROCEDURES AND ISSUES

There are many procedures and issues that are important to understanding consolidated statements, but they are complex enough that an advanced accounting course is usually necessary to thoroughly understand them. To give you a general idea of the procedures that are necessary under consolidation, we will show you the consolidation of a subsidiary that is 100 percent owned. This will be followed by a discussion of the issues surrounding the handling of a subsidiary that is less than 100 percent owned, and of intercompany transactions.

Consolidation Procedures—100 Percent Acquisition

To illustrate the concepts behind the preparation of a consolidated set of financial statements, we will consider a share acquisition in which the parent acquires 100 percent of the subsidiary. To make the example as concrete as possible, let's assume that the statements of financial position of the parent (referred to as Parent Company) and the subsidiary (referred to as Sub Company) just prior to the acquisition are as shown in Exhibit B-4.

EXHIBIT B-4 PARENT AND SUBSIDIARY STATEMENTS OF FINANCIAL POSITION

Assume that, at acquisition, Parent Company pays $1,400 in cash for all the outstanding shares of Sub Company. Because the book value of Sub Company's equity (net assets) is $1,000 at the date of acquisition, Parent Company has paid $400 more than the book value of the acquired company's assets and liabilities. Assume further that $250 of this $400 relates to the additional fair market value of Sub's property, plant, and equipment. It will be assumed that the fair market value of Sub's other assets and liabilities are equal to their book values. This means that the remainder of the $400, or $150, is due to goodwill. Exhibit B-5 illustrates these assumptions.

Parent Company records its investment in an account called Investment in Sub Company. Because Parent Company owns more than 50 percent of the shares of Sub Company, it controls Sub Company and will have to prepare consolidated financial statements. For its part, because Sub Company remains a separate legal entity, it will continue to record its transactions in its own accounting system. Parent Company will also continue to keep track of its own transactions in its own accounting system on what are known as the parent-only books. At the end of each accounting period, the two entities' separate financial statements will be combined on a work sheet to produce the consolidated financial statements, as if the two companies were one legal entity. Because the Investment in Sub Company account will be replaced in the consolidation process by the individual assets and liabilities of Sub Company, it does not really matter, from a consolidated point of view, how Parent accounts for its investment on the parent-only statements. However, it will make a difference in the parent-only financial statements. Some companies use the equity method to account for the investment, and some use the cost method. Assuming that Parent Company uses the equity method, the investment entry is as follows:

INVESTMENT ENTRY

![]()

EXHIBIT B-5 REPRESENTATION OF THE PURCHASE PRICE COMPOSITION

After recording the investment, the statements of financial position of Parent Company and Sub Company will appear as in Exhibit B-6.

EXHIBIT B-6 PARENT AND SUBSIDIARY STATEMENTS OF FINANCIAL POSITION At Date of Acquisition

To prepare a consolidated statement of financial position for Parent Company at the date of acquisition, the Investment in Sub Company account must be replaced by the individual assets and liabilities of Sub Company. This would normally be done on a set of consolidating working papers. The consolidating entries that are discussed next are made on the consolidating working papers, and no entries would be made directly in either the parent company's or the subsidiary company's accounting system. The accountant starts the working papers by placing the financial statements as prepared by the parent company and the subsidiary side by side, as shown in Exhibit B-7. The working papers will then have columns for the consolidating entries and for the consolidated totals. Note that the exhibit shows debit and credit columns for all four items.

EXHIBIT B-7 CONSOLIDATING WORKING PAPERS

On the consolidating working papers, each row will be added across to obtain the consolidated totals. If no adjustments are made to the balances shown in Exhibit B-7, several items will be double-counted. First, the subsidiary's net assets will be counted twice: once in the individual accounts of Sub and again as the net amount in Parent's investment account. One or the other of these two amounts must be eliminated. Because the idea of consolidated statements is to show the subsidiary's individual assets and liabilities in the consolidated totals, the best option is to eliminate the parent's investment account. The second item that will be counted twice is in the shareholders' equity section. The only outside shareholders of the consolidated company are the parent company's shareholders. The shareholders' equity represented by the subsidiary's balances is held by the parent company. The shareholders' equity section of the subsidiary must, therefore, be eliminated. Both of these items are eliminated in a working paper entry called an elimination entry. The elimination entry for our example is as follows:

WORKING PAPER ELIMINATION ENTRY

In the preceding entry, you can see that, in order to balance the entry, additional debits totalling $400 are needed. What does this $400 difference represent? It represents the excess amount that Parent Company paid for its interest in Sub Company over the net assets' book value. Remember the assumption that this excess is broken down into $250 for the excess of the fair market value of property, plant, and equipment over its book value, and $150 for goodwill. Therefore, the complete entry would be as follows:

WORKING PAPER ELIMINATION ENTRY (ENTRY 1)

As a result of the elimination entry, the consolidating working papers would appear as in Exhibit B-8. The working paper entries are numbered so that you can follow them from the journal entry form to the working paper form.

Note that shareholders' equity on a consolidated basis is the same as on the parent company's books. This is true because all that consolidation has really done is replace the net assets represented in the investment account with the individual assets and liabilities that make up the subsidiary's net assets. In this sense, the statements of the parent company (which are referred to as the parent-only statements) portray the same net results to the shareholders as the consolidated statements. However, the consolidated statements present somewhat different information to the shareholders in that ratios, such as the debt to equity ratio, can be quite different from those found in parent-only statements. For example, from Exhibit B-8 you can calculate the debt to equity ratio for the parent-only statements as 1.0 ($2,000/$2,000), whereas in the consolidated statements, it is 1.75 ($3,500/$2,000). This occurs because consolidating the two companies produces a leverage ratio that reflects both the parent's and the sub's debt, yet only the parent's equity. However, although the debt to equity ratio appears to be less favourable on the consolidated statements, users must remember that Sub Company is a separate legal entity and is responsible for its own debts. Parent Company has limited liability. For this reason, creditors such as banks prefer to see parent-only financial statements when they assess a company's ability to repay debt.

EXHIBIT B-8 CONSOLIDATING WORKING PAPERS (Statement of Financial Position Only)

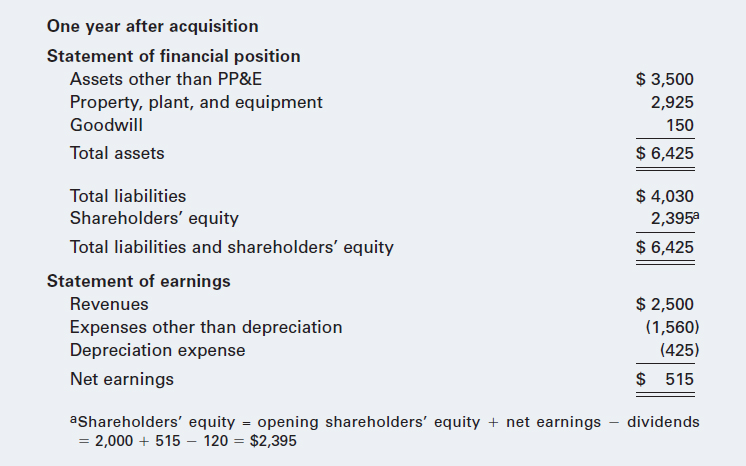

Now consider what the financial statements of Parent Company and Sub Company might look like one year after acquisition. The two companies' accounts are shown in Exhibit B-9 (remember that EEI stands for equity in earnings of the investee).

EXHIBIT B-9 PARENT AND SUBSIDIARY STATEMENTS OF FINANCIAL POSITION AND STATEMENTS OF EARNINGS

Using the equity method, Parent Company would make the following entries in its parent-only books to account for its investment:

ENTRIES USING THE EQUITY METHOD (ON PARENT COMPANY'S BOOKS)

Parent's share (100%) of Sub's income:

![]()

Parent's share (100%) of Sub's dividends:

![]()

After these entries, the ending balance in the investment account will be $1,500 ($1,400 + $150 − $50). However, you will note in the statements in Exhibit B-9 that the investment account has a balance of $1,475. The difference in these amounts is due to the fact that Parent Company paid more than the book value for the net assets of Sub Company. As we assumed earlier, Parent Company paid $400 more than the book value ($1,000). The $400 is due to the extra fair market value of property, plant, and equipment ($250) and goodwill ($150). Subsequent to acquisition, the property, plant, and equipment must be depreciated and the depreciation is shown as part of the EEI. Assume that the property, plant, and equipment have a remaining useful life of 10 years, have a residual value of zero, and are depreciated using the straight-line method. Therefore, Parent Company must take an additional $25 ($250 ÷ 10 years) in depreciation expense over what is shown on the books of Sub Company. The depreciation of the property, plant, and equipment means that Parent Company has to report an additional $25 in expenses during each year subsequent to acquisition. Using the equity method, Parent Company shows these additional expenses as a part of the EEI. The following entry is made (in addition to those shown earlier):

DEPRECIATION ENTRY UNDER EQUITY METHOD (ON PARENT COMPANY'S BOOKS)

![]()

With this additional entry, the balance in the Investment in Sub Company account is $1,475, exactly the balance shown in Exhibit B-9.

The $150 of goodwill is not amortized. Instead, it is checked each year to determine if its value has been impaired. To keep our example simple, we are going to assume that there is no impairment and the goodwill is still worth $150.

The consolidated working papers at the end of the first year are presented in Exhibit B-10. You should note that they are shown in the trial balance phase. In the trial balance phase, the temporary statement of earnings and dividends declared accounts still have balances that have not been closed to retained earnings. (See Chapter 3 if you need to refresh your memory about the meaning of the trial balance phase and the closing process.) Note that shareholders' equity has the same balance as it had at the beginning of the year.

In the year subsequent to acquisition, three basic consolidating working paper entries are made if the parent company is using the equity method to account for the investment on the parent-only financial statements. In addition to eliminating the investment account and the shareholders' equity accounts discussed earlier, the EEI must be eliminated, as must the subsidiary's dividends declared account. Otherwise, the subsidiary's income would be counted twice, once as EEI and a second time as the individual revenue and expense items. Dividends declared by the subsidiary are intercompany transfers of cash, from a consolidated point of view. They are not dividends to outside shareholders and, as such, they should be eliminated in the consolidation process. The entry to eliminate EEI and dividends will be called the reversal of current year entries because the entry is, in effect, removing income and dividends recognized during the period. Once these two entries have been made, the third set of entries recognizes the extra depreciation expense discussed earlier. Exhibit B-10 shows the consolidating working paper entries.

EXHIBIT B-10 CONSOLIDATING WORKING PAPERS (One Year After Acquisition)

CONSOLIDATING WORKING PAPER ENTRIES

Reversal of current year entries (Entry 1):

Investment elimination entry (Entry 2):

Extra Depreciation of PP&E (Entry 3):

The preceding entries are added to the consolidating working papers as shown in Exhibit B-11A and the consolidated financial statements that are prepared. Note that a separate accumulated depreciation account has not been provided and that the amount of extra depreciation for the period has simply been credited to the property, plant, and equipment account. You can think of property, plant, and equipment as a net account—that is, as net of accumulated depreciation.

Note that this is exactly the same as the net earnings that was reported by Parent Company using the equity method, as shown in Exhibit B-9. This will always be the case when the parent company uses the equity method to account for its investment in a subsidiary. As mentioned earlier, the equity method is sometimes referred to as a one-line consolidation. It is a one-line consolidation because the statement of financial position effects of consolidation are captured in the one-line item called the investment account. The statement of earnings effects of consolidation are captured in the one-line item called EEI. The only difference, then, between the equity method and a full consolidation is that the one-line items are replaced with the full details of the subsidiary's assets and liabilities on the statement of financial position and the full details of the subsidiary's revenues and expenses on the statement of earnings.

EXHIBIT B-11A CONSOLIDATING WORKING PAPERS (One Year After Acquisition)

EXHIBIT B-11B CONSOLIDATED STATEMENTS OF FINANCIAL POSITION AND STATEMENTS OF EARNINGS

Consolidation Procedures—Less Than 100 Percent Acquisition

One complication that arises in many acquisitions is that the parent company does not always acquire 100 percent of the subsidiary's shares. Suppose, for example, that Parent Company buys 80 percent of the shares of Sub Company for $1,120. The balance sheets of Parent Company and Sub Company immediately after acquisition are the same as in Exhibit B-6.

Assume that the same fair market values of the assets and liabilities apply to Sub Company as before. The only asset that had extra fair market value is property, plant, and equipment, with an excess value of $250. Even though Parent Company only purchased 80 percent of Sub Company, when it prepares the consolidated financial statements it will include 100 percent of the fair value of the assets and liabilities of Sub Company. The consolidated financial statements portray the assets and liabilities under Parent's control, and they do control 100 percent of the assets and liabilities, even if they only own 80 percent. Additionally, although we only know what Parent paid for its 80 percent, we can use that value to determine what the fair value of 100 percent of Sub is, and apply that when determining goodwill. The calculation of goodwill would be made as follows:

ALLOCATION OF THE PURCHASE PRICE

Because Parent Company controls Sub Company, it must prepare consolidated financial statements. When it prepares consolidated financial statements, Parent Company adds 100 percent of Sub Company's assets, liabilities, revenues, and expenses to its own accounts. But Parent Company only owns 80 percent of Sub Company. It must, therefore, show 20 percent as being owned by the other shareholders. It does this by creating an account called non-controlling interest (NCI) or sometimes minority interest. The NCI account is located in the shareholders' equity section on the consolidated balance sheet. It contains 20 percent of the market value of Sub Company, $280 (20% of $1,400). There is another NCI account that represents 20 percent of Sub Company's net earnings. It appears as a deduction from the consolidated entity's net earnings so that consolidated net earnings include only the 80 percent of Sub's earnings that belongs to Parent Company, plus Parent's own net earnings. These two NCI accounts allow the parent to consolidate 100 percent of its subsidiary and then to “back out” the part that does not belong to it.

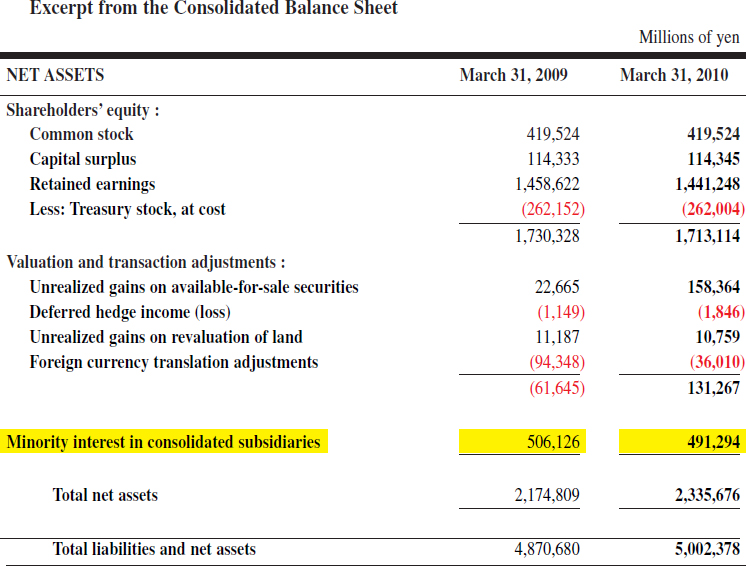

To illustrate NCI (minority interest) disclosure, we have included the fiscal 2009 income statement and net assets (shareholders' equity) section of the balance sheet of Nippon Steel Corporation in Exhibit B-12. Nippon is involved in steel production, transportation, and related businesses, and has investments in over 250 other companies worldwide, with 190 of its investment subsidiaries accounted for through consolidation. Nippon's ownership interest in these subsidiaries ranges from 51 percent to 100 percent. One hundred percent of the income and losses from all of these subsidiaries is included on Nippon's income statement in the 2009 income before income taxes and minority interest amount of ![]() 11,242 million. The minority interest (NCI) of

11,242 million. The minority interest (NCI) of ![]() 6,728 million on the income statement represents the amount of the subsidiaries' income that Nippon does not own. On the balance sheet, 100 percent of the subsidiaries' assets and liabilities are included in the total assets and liabilities. The minority interest (NCI) of

6,728 million on the income statement represents the amount of the subsidiaries' income that Nippon does not own. On the balance sheet, 100 percent of the subsidiaries' assets and liabilities are included in the total assets and liabilities. The minority interest (NCI) of ![]() 491,294 million on the balance sheet represents the portion of those net assets not owned by Nippon.

491,294 million on the balance sheet represents the portion of those net assets not owned by Nippon.

We can also see the importance of other investments to Nippon. In approximately 60 of the investee companies, Nippon only exercises significant influence and uses the equity method to account for those investments. The income earned from these investees on the income statement is ![]() 34,756 million, roughly 20 percent of the total income before taxes and minority interest. The balance sheet account representing these investments is in the fixed asset section and is not shown in the exhibit.

34,756 million, roughly 20 percent of the total income before taxes and minority interest. The balance sheet account representing these investments is in the fixed asset section and is not shown in the exhibit.

EXHIBIT B-12A NIPPON STEEL CORPORATION 2010 ANNUAL REPORT

EXHIBIT B-12B NIPPON STEEL CORPORATION 2010 ANNUAL REPORT

When a parent owns less than 100 percent of a subsidiary, the accounting can become quite complex. The discussion of these aspects will be left to more advanced texts. It is enough that you understand what the non-controlling interest accounts represent.

Consolidations—Intercompany Transactions

One final complication that deserves mentioning is the impact that intercompany transactions have on the consolidated financial statements. When a parent company buys a controlling interest in a supplier or a customer, it is likely that there are many transactions between the two companies. Prior to the acquisition, these transactions are viewed as taking place between two independent parties, but after the acquisition, they are viewed as transactions within a single economic entity and are referred to as intercompany transactions.

Sales of goods and services between a parent and a subsidiary cannot be viewed as completed transactions unless there has been a sale of the goods or services outside the consolidated entity. Therefore, any profits (revenues and expenses) from those transactions that are not completed by a sale outside the consolidated entity must be eliminated. If there are remaining balances in accounts receivable and accounts payable that relate to intercompany transactions, these, too, must be removed.

To show you this elimination process briefly, consider the following example. Company A owns 100 percent of Company B. During 2010, Company A sells a parcel of land to Company B for $60,000. This land had originally cost Company A $45,000. Company A records the transaction on its books as follows:

Company B records the acquisition of the land as follows:

Note that cash went out of one company and into the other company, but the consolidated entity still has the same amount of cash. Land went from $45,000 on one company's statement of financial position to $60,000 on the other company's statement of financial position. To the consolidated entity, this is the same parcel of land that was on last year's consolidated statement of financial position at its historical cost of $45,000. If it is not reduced back to $45,000 on the consolidated statement of financial position, it will be overstated. If we allowed the sale price of items sold in intercompany transactions to appear on the consolidated financial statements, the two entities could sell items back and forth merely to increase asset values and record gains when, in reality, no external transactions with independent third parties took place. The gain on the sale of land must also be removed from the consolidated statement of earnings. No gain can be recognized by the consolidated entity, because the land has not been sold to an outside party. The journal entry to eliminate this unrealized gain and increase in the value of the asset on the consolidating working papers would be as follows:

An entry similar to this would have to be repeated on the consolidating working papers each year, when the consolidated financial statements are prepared. However, the entry in subsequent years would have a debit to Retained Earnings rather than to Gain on Sale of Land because in future years the statement of earnings will not have the gain reported. The gain caused the retained earnings of Company A to increase in the year that the land was sold to Company B.

Entries similar to these are prepared for all the intercompany transactions that occur between the two entities.

STATEMENT ANALYSIS CONSIDERATIONS

The consolidation of a subsidiary considerably changes the appearance of both the statement of earnings and the statement of financial position compared to the parent-only financial statements. The statement of earnings is different only in its detail; the controlling interest's share of net earnings for the period is the same regardless of whether or not the subsidiary is consolidated. The statement of financial position can be dramatically affected when the investment in the subsidiary account is replaced by all of the assets and liabilities of the subsidiary, and this impacts many ratios.

Earlier in the appendix, the effect that consolidation has on the debt to equity ratio was described using the information provided in Exhibit B-8. The debt to equity ratio for Parent Company was 1.0, whereas the debt to equity ratio for the consolidated entity was 1.75. Users who need information about an entity's ability to repay debt should not rely solely on consolidated financial statements. These statements contain the liabilities of all the companies in the consolidated group of companies, but each of those companies is only responsible for its own debt. However, a parent and its subsidiaries often guarantee each other's debt, because this could result in lending institutions charging lower interest rates or loaning larger amounts. When the debt is guaranteed, the consolidated debt to equity ratio is useful, because all the consolidated assets are available to service the debt.

Other ratios will also be affected. The ROA ratio, for example, divides the net earnings before interest by the average total assets. With consolidation, the numerator changes to the extent that the subsidiary's interest expense is included on the consolidated statement of earnings and is, therefore, added back to the net earnings. The denominator (average total assets) also changes because the investment account is replaced by the subsidiary's individual assets and liabilities. In the example in Exhibit B-9, the parent's total assets prior to consolidation were $4,725. After consolidation, |the total assets were $6,425 (Exhibit B-11). This large increase would certainly affect the ROA. The ROA prior to consolidation (ignoring interest expense which was not shown in the example) would have been 10.9 percent ($515/$4,725). After consolidation, the ROA was 8.0 percent ($515/$6,425).

The current ratio will also be affected. The current assets and liabilities that are embedded in the investment account are shown in full detail when they are consolidated, as the subsidiary's current assets and liabilities are added to the parent's when they are consolidated. Because our example in Exhibit B-8 does not distinguish current liabilities from long-term liabilities, it is not possible to demonstrate the change that would occur. Obviously, the quick ratio will also be affected by consolidation, for the same reason as for the current ratio.

Shareholders, potential investors, and most other outside users may not be able to determine the impact that various subsidiaries have on the consolidated financial statements. If a parent owns 100 percent of a subsidiary, the subsidiary will often not provide financial statements for external users other than the Canada Revenue Agency. A lender would be able to request individual financial statements from any company that wanted to borrow funds, but most other external users would not have this luxury. This means that users should have some understanding of how ratios are affected by the consolidation process.

If the parent owns less than 100 percent of the shares, the subsidiary must publish publicly available financial statements if it is traded on the stock market. Users then have the opportunity to get more information about the components of the consolidated entity. However, a 100 percent-owned subsidiary does not trade on a stock exchange and does not need to make its financial statements public.

SUMMARY

In this appendix, we provided more background information to improve your understanding of consolidated financial statements. You learned about the different levels of investments in other companies, from non-strategic investments to significant influence investments to controlled subsidiaries. Through simple examples, we demonstrated the acquisition of a 100 percent-owned subsidiary. We expanded your knowledge through a discussion of non-wholly owned subsidiaries and of intercompany transactions. We concluded the appendix with a brief discussion of the impact of the consolidation process on ratio analysis.

The environment of corporate financial reporting is one of constant change and growing complexity. This book has introduced you to most of the fundamental concepts and principles that guide bodies such as the International Accounting Standards Board, as they consider new business situations and issues. You should think of the completion of this appendix as the end of your introduction to and initial understanding of corporate financial reporting. As accounting standard-setting bodies and regulators adjust and change the methods and guidelines used to prepare financial statements, you must constantly educate yourself so that you understand the impacts of these changes on the financial statements of your company or of other companies that are of interest to you.

IFRS VERSUS ASPE

Accounting for strategic investments is one of the areas where the accounting may differ for companies that prepare their financial statements using Canada's Accounting Standards for Private Enterprises. For significantly influenced investments, the investor company can choose to use either the equity method or the cost method. For subsidiaries, the investor company may choose to use the cost method or equity method, or to prepare consolidated financial statements. The investor must use the same method for all investments in each category. Consolidated financial statements do provide a more complete picture of the assets, liabilities, revenues, and expenses under the investor company's control, but as you have seen in this appendix, even very simple consolidated financial statements are more time consuming and complex to prepare. Many private enterprises can adequately assess the performance of all of the companies under their control by studying the financial statements of the individual companies, and they are usually familiar with the extent of intercompany transactions between the companies. In those situations, the preparation of consolidated financial statements may not be necessary.

Additional Practice Problems

PRACTICE PROBLEM

Peck Company (parent) bought 100 percent of the shares of Spruce Company (subsidiary) on January 1, 2011, for $600,000. On that date, the shareholders' equity section of Spruce Company was as follows:

Peck paid $400,000 more for Spruce than the book value of the assets acquired. This excess amount was attributed partially to land ($50,000) and equipment ($250,000); the remainder was attributed to goodwill. The equipment had a remaining useful life of 10 years and an expected residual value of zero. Peck depreciates its assets using the straight-line method.

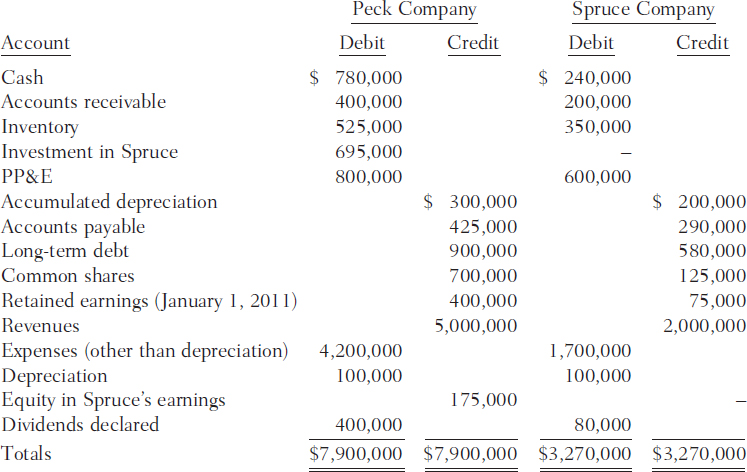

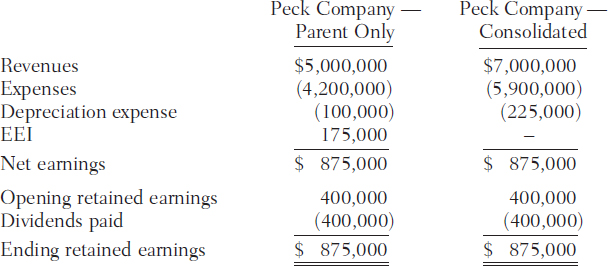

The following represents the trial balances of Peck and Spruce as at December 31, 2011 (the end of the fiscal year):

Trial Balance, December 31, 2011

Required:

- Reconstruct the entries that Peck made during 2011 to account for its investment in Spruce using the equity method.

- Prepare a set of consolidating working papers for Peck and Spruce for 2011, showing the consolidating entries and the amounts that will appear in the consolidated financial statements.

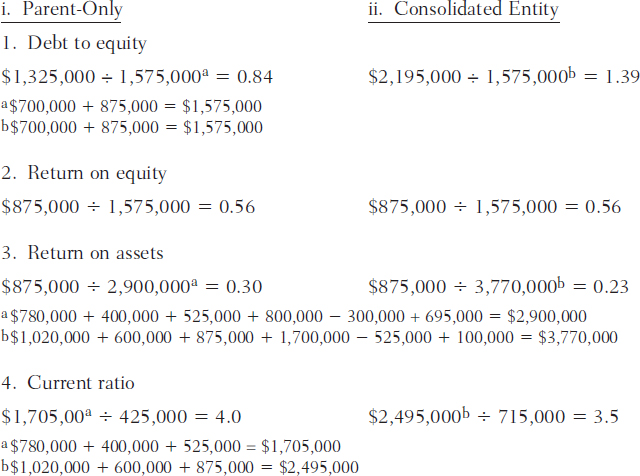

- Calculate the following ratios for Peck Company, using (i) its parent-only financial statement information and (ii) the consolidated entity information. (Hint: It might be easier to first prepare the statements of earnings and retained earnings for the year in order to determine the closing retained earnings balances that would appear on the statements on financial position.)

- Debt to equity ratio

- Return on equity

- Return on assets

- Current ratio

SUGGESTED SOLUTION TO PRACTICE PROBLEM

- Using the equity method, the following entries would be made:

At acquisition

At year end

Spruce's net earnings are calculated as follows:

To recognize dividends: Since Peck's share of Spruce's earnings is 100 percent, the following entry would be made:

To recognize dividends: As Spruce declared $80,000 in dividends and Peck's share is 100 percent, the following entry would be made:

To recognize depreciation of the fair value increment on the equipment: At the date of acquisition, Peck paid $400,000 more for the Spruce shares than the book value of the net assets. This excess amount would be attributable to the following items:

The land is not depreciated, but the excess amount due to the equipment must be depreciated. Since Peck uses straight-line depreciation, the extra depreciation expense would be $25,000 per year ($250,000 ÷ 10 years). Using the equity method, the extra expenses would be recognized with the following entry:

The goodwill is not amortized, but must be written down if there is evidence that its value has been impaired.

Based on these entries, the investment account balance would be $695,000 (600,000 + 200,000 − 80,000 − 25,000) and the equity in Spruce's earnings would be $175,000 (200,000 − 25,000), both as shown in the trial balance.

- The consolidating working paper entries are as follows.

To reverse current income and dividends:

To eliminate the investment account and shareholders' equity and to recognize extra fair market value and goodwill:

To depreciate the extra fair market value of the equipment:

The consolidating working papers are shown in Exhibit B-13.

EXHIBIT B-13 CONSOLIDATING WORKING PAPERS Peck Company and Spruce Company, 2011—100% Acquisition

- Statements of Earnings and Retained Earnings for 2011:

SYNONYMS

Non-controlling interest ![]() Minority interest

Minority interest

Non-strategic investment ![]() Passive investment

Passive investment ![]() Portfolio investment

Portfolio investment

Significantly influenced company ![]() Associated company

Associated company

ABBREVIATIONS USED

| EEI | Equity in earnings of investee |

| NCI | Non-controlling interest |

| PP&E | Property, plant, and equipment |

GLOSSARY

Acquisition method An accounting method to record the acquisition of another company. The acquisition is treated as a purchase, and the assets and liabilities acquired are measured at their fair market value. Because this is typically a basket purchase, the cost is allocated to the individual assets and liabilities based on their fair market values.

Asset purchase An acquisition of assets from another company in which the acquiring company purchases the assets directly rather than buying a controlling interest in the shares of the other company. Title to the assets passes to the acquiring company.

Associated company The IFRS term to describe a company that has been invested in by another company and where the investor has the power and ability to participate in financial and operating decisions of the investee but does not have control over it. Synonym for significantly influenced company.

Consolidated financial statements Financial statements that represent the total financial results of a parent company and its various subsidiaries as if they were one company, even though they are separate legal entities.

Consolidating working papers A work sheet that adjusts the financial statements of a parent and its subsidiaries so that the statements can be combined to show the consolidated financial statements.

Consolidation An accounting method that companies are required to use to represent their ownership in other companies when they have control over the activities of these other companies. The method requires the preparation of consolidated financial statements.

Controlling interest The amount of ownership of a subsidiary that a parent company must have in order to control the subsidiary's strategic operating, financing, and investing activities. An ownership interest of greater than 50 percent usually meets this criterion.

Diversification A reason for acquiring ownership in another company. Diversification typically implies that the acquired company is in a business that is very different from the acquiring company's business. The idea is to find a new business that is counter-cyclical to the company's current business.

Elimination entry A working paper consolidating entry that eliminates the balance in the Investment in subsidiary account against the shareholders' equity accounts of the subsidiary. At the same time, if the price paid by the parent company exceeds the book value of the subsidiary's shareholders' equity section, the excess fair market value of the net assets acquired and goodwill are recognized as part of the entry.

Equity in earnings of investee (EEI) An account used in a parent company's books to record its share of the subsidiary's net earnings for the period using the equity method.

Equity method A method that companies use to account for their ownership in companies in which they have significant influence. This is usually true when the percentage of ownership is between 20 percent and 50 percent. In addition, this method is often used in parent-only statements to account for the investment in a subsidiary. In the latter case, the account will be eliminated on the consolidating working papers at the end of the year when consolidated financial statements are prepared.

Excess fair market value The difference between the fair market value and book value of the net assets of a subsidiary company when its shares are acquired by a parent company.

Goodwill An intangible asset that arises when a parent company acquires ownership in a subsidiary company and pays more for the shares than the fair market value of the underlying net identifiable assets at the date of acquisition. The difference between the price paid and these net assets' fair market value is the value of the goodwill. It can represent expected excess earnings that result from, for example, the subsidiary's reputation, its exceptional sales staff, or an advantageous location.

Horizontal integration A type of acquisition in which a parent company buys a competitor company in order to gain a larger market share or to expand its markets geographically.

Identifiable net assets The assets and liabilities that can be specifically identified at the date of a merger or acquisition. Some of the identifiable assets, such as patents and trademarks, may not have been recorded on the subsidiary's books.

Investee A company whose shares are acquired by another company.

Investor A company that acquires shares of another company as an investment.

Minority interest The portion of a less-than 100 percent-owned subsidiary that is owned by other shareholders. Synonym for non-controlling interest.

Non-controlling interest (NCI) The portion of a less-than 100 percent-owned subsidiary that is owned by other shareholders. Synonym for minority interest.

Non-strategic investment An investment by one company in another company in which the acquiring company has little or no influence over the operations of the acquired company. Synonym for passive investment or portfolio investment.

One-line consolidation A term to describe the equity method because it produces the same net results as the full consolidation method, except that the subsidiary's results are shown in a single line on the statement of financial position (the investment account) and a single line on the statement of earnings (the equity in earnings of investee).

Parent company A company that acquires control (usually by purchasing more than 50 percent of another company's voting shares) of another company. The acquired company is referred to as a subsidiary.

Parent-only books The accounting records of a parent company that have not been combined with its subsidiary's records in consolidated financial statements.

Passive investment An investment by one company in another company in which the acquiring company has no ability to control or influence the decisions of the acquired company. Synonym for non-strategic investment or portfolio investment.

Portfolio investment An investment by one company in another company in which the acquiring company has no ability to control or influence the decisions of the acquired company. A synonym for non-strategic investment or passive investment.

Seasonal business A business that is subject to significant swings in the level of its activity according to the time of year, such as the greeting card business.

Share acquisition An acquisition of another company that is accomplished through the purchase of its shares. The acquired company continues as a separate legal entity.

Significantly influenced company A company where the investor company has the power and ability to participate in financial and operating decisions of the investee but does not have control over the investee. Synonym for associated company.

Strategic investment An investment by one company in another company where the investor company intends to a have long-term strategic relationship with the acquired company.

Subsidiary A company controlled by another company (the parent). The parent controls the subsidiary's strategic operating, financing, and investing decisions, usually by owning more than 50 percent of its outstanding shares.

Trial balance phase A phase in the preparation of financial statements in which the temporary accounts still contain revenue, expense, and dividend accounts from the period and have not been closed out to retained earnings.

Vertical integration A type of merger or acquisition in which a parent company buys a supplier or customer company in order to ensure a supply of raw materials or a market for its end product.

Widely held shares Shares of a company that are held by a large number of individuals or institutions, such that no single shareholder has significant influence over the company's decisions.

Additional Practice Problems

ASSIGNMENT MATERIAL

Assessing Your Recall

B-1 Identify and briefly explain the major reasons for a company to buy shares in another company.

B-2 Exhibit B-1 provided information about the subsidiaries of H&M. The largest investment is in FaBric Scandinavien AB. The acquisition of FaBric in 2008 is described in Exhibit B-2. Explain briefly the possible strategic reasons for H&M to have acquired a controlling interest in FaBric. Would this investment be an example of horizontal or vertical integration?

B-3 Compare and contrast a share acquisition and an asset acquisition in terms of their effects on the financial statements.

B-4 What factors other than the percentage of ownership could you use to determine if a company has significant influence over an investee?

B-5 Briefly describe the IRFS guidelines for accounting for long-term acquisitions in the shares of other companies. In your description, identify the criteria used to distinguish the various accounting methods.

B-6 Explain the nature of goodwill and how it arises in the context of an acquisition.

B-7 The equity method is sometimes referred to as a one-line consolidation. Explain.

B-8 Discuss what a consolidation is trying to accomplish.

B-9 Consolidating working paper entries are needed to eliminate double accounting for certain items on the parent's and subsidiary's books. Explain which items would be accounted for twice if the subsidiary company's books were added directly to the parent's books.

B-10 Explain the accounting alternatives that are available to a company that follows Accounting Standards for Private Enterprise GAAP and which has just purchased control of another company. Explain why consolidated financial statements might not be more useful for these companies.

Applying Your Knowledge

B-11 (Accounting alternatives for investments)

On January 1, 2010, Rain Inc. purchased a 20 percent interest in Waterworks Ltd. by buying 50,000 shares for $8.00 per share. During 2010, Waterworks earned income of $160,000 and paid dividends of $20,000. On December 31, 2010, the market value of Waterworks shares was $8.80.

Required:

- Compare the investment income reported on Rain's statement of earnings under each of the following methods of accounting for the investment in Waterworks:

- Cost method

- Available-for-sale method

- Equity method