chapter 4

REVENUE RECOGNITION AND STATEMENT OF EARNINGS

Summary of the Cash-to-Cash Cycle

Applications of Revenue Recognition

Revenue Recognized from Multiple Lines of Business

Earnings from Non-Operating Sources

Earnings from Unusual or Infrequent Events

Variations in Statement of Earnings Formats

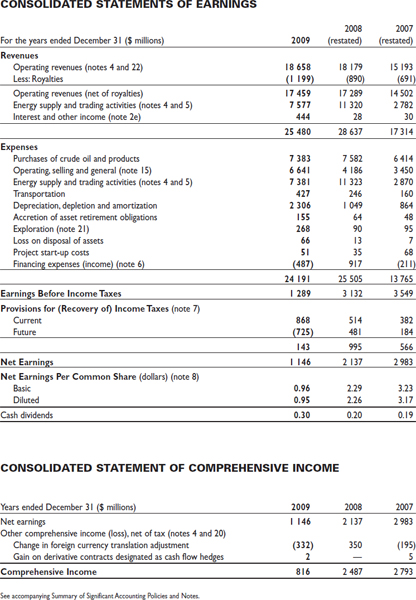

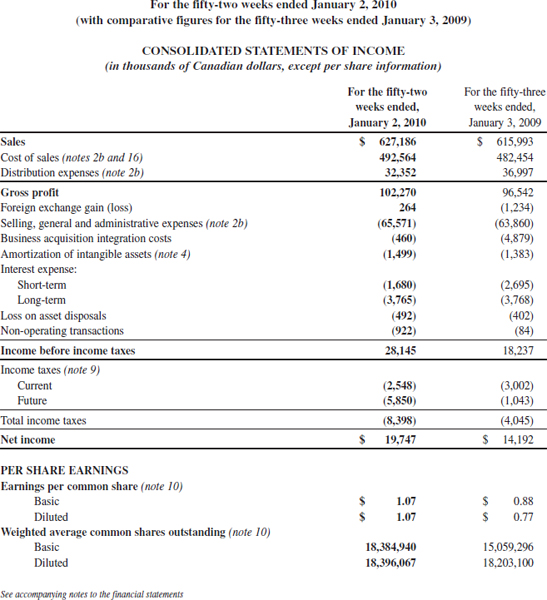

Examples of Actual Statements of Earnings

The Return on Investment (ROI) Ratio as a Measure of Performance

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Describe the cash-to-cash cycle of a retail company.

- List and explain the basic criteria for revenue recognition.

- Define earnings management as it relates to revenue recognition and explain why and how it can occur.

- Describe the specific revenue recognition criteria and how they apply to the sale of goods, the provision of services, and the use by others of a company's assets.

- Explain the impact that various revenue recognition methods have on earnings recognition.

- Calculate amounts to be recognized under the percentage of completion method.

- Understand the difference between a multi-step statement of earnings and a single-step one.

- Describe the criteria for unusual or infrequent items and discontinued operations.

- Describe how the return on investment can give you one measure of performance.

- Calculate the return on investment under some basic scenarios.

Charting a Course—When to Recognize Revenue

“A more adventurous and realistic look at the world and how people travel through it” is what Outpost magazine offers readers through real-life stories of journeys off the beaten track. Since its March 1996 launch, the Toronto-based publication has grown from a quarterly to six issues per year and seen its circulation climb to approximately 28,000.

What does it take to keep a magazine running smoothly? Publisher Matt Robinson says it pays to have a revenue recognition policy that makes sense.

“Advertising is our principal source of revenue,” explains Mr. Robinson. “We bill on a per-issue basis. Payment is against service rendered, so billing has to take place when the issue is published.” Since Outpost publishes every other month, the company sends out a new set of invoices every eight weeks or so.

Outpost's advertisers can then take anywhere from 30 to 90 days to pay. “We follow the standard 30–60–90 days to collect on invoices that all companies follow,” says Mr. Robinson. “We begin to place pressure on clients after 30 days, first with a phone call, then a letter, and then through other collection resources, if necessary. We also offer a two percent early payment discount to encourage clients to pay their invoices within 10 days.” Meanwhile, the magazine has to pay all its principal suppliers—the printer, landlord, and contributors.

“Circulation revenue does help mitigate cash flow issues between invoicing and payments,” says Mr. Robinson. When Outpost sells a subscription, it recognizes the entire sale as revenue right away. “Magazines are atypical in that we get people to pay up front before the service is rendered,” he points out. Subscriptions can begin and end with any issue, with each individual subscriber having his or her renewal dates. To recognize the revenue on a per-issue basis for every subscriber would be too complicated and cumbersome for a small operation like Outpost. The liability created by recognizing revenue on issues not yet published is understood.

As for newsstand sales, the company typically receives payment from distributors six months after an issue has gone out, based on the number of copies left over. The magazine is unable to plan for revenue from distributors with any kind of accuracy, despite the fact that it has already paid production and shipping costs for those magazines, says Mr. Robinson.

Outpost's own spending is focused on boosting circulation figures, and thus increasing revenues. Its website and participation in consumer shows are two areas where it markets itself. The magazine has also sponsored several speaking tours for Ian Wright, host of the travel show Pilot Guides, which airs on OLN (formerly Outdoor Life Network). “Because we're a small business, we like to keep focused on the core product,” says Mr. Robinson. “Increasing the number of subscribers is a priority.”

The opening story describes a company that publishes an adventure magazine called Outpost. The magazine publishing industry is very competitive. Among other things, it is difficult to find a focus that will attract readers year after year. Outpost has managed to do this despite the downturn in the travel market since the recent rise in fuel costs and the slowdown in the economy.

From an accounting perspective, the company provides an opportunity to look at a variety of revenue models, as it has three distinct sources of revenue, including the most important one, its advertising revenue. As Outpost has contracts with advertisers for ads in future issues of its magazine, the main question that arises is when it should recognize this revenue. When it signs the agreement with the advertiser? When it puts the advertisement in the magazine? When it gets paid for the advertisement? Outpost's practice is to recognize revenue when it sends an invoice to the advertiser, which is done as each issue is published. This delays the recognition of revenue until the invoice is sent, and it also means that the receipt of cash from the advertiser happens after the revenue has been recognized.

The second form of revenue is from individual subscribers. These people pay in advance. Subscriptions are of varying lengths and start at different times during the year. Outpost first recognizes this revenue when it receives the subscription request and the money. However, the company is also aware that some of this revenue should not be included in an accounting period if the company must provide additional issues to the subscriber in the following periods. As a result, while Outpost initially recognizes the total amount paid by the subscriber as revenue, it later backs out some of this revenue and records it as a liability. This liability is then reduced as the remaining issues are sent to the subscriber, which has the effect of then recognizing the revenue.

The third form of revenue is from sales of magazines to distributors who supply retailers with individual copies to sell. In this case, the company does not even know how much revenue it has earned until about six months after it sends the magazines to the distributors. It receives revenue from the number of issues sold and gets the unsold issues back from the distributors. This means that the revenue recognition is delayed until the cash is received, which is much later than when the magazines were issued. Outpost has little choice here as to when to recognize this revenue. It must wait until it knows how much has been earned.

Outpost's three sources of revenue thus provide an introduction to some guidelines that companies can use when making decisions about when to recognize revenue.

In Chapters 1 through 3, three basic financial statements were described, and we saw that two of these, the statement of earnings and the statement of cash flows, measure the company's performance across a time period. In this chapter, the accounting concepts and guidelines for the recognition of earnings are discussed, more detail is provided about the statement of earnings, and some of the problems that are inherent in performance measurement are considered. Chapter 5 is a more detailed discussion of the statement of cash flows and the measurement of performance using cash flows.

USER RELEVANCE

Why is it important for users to know about the recognition of revenue? First, the revenue amount is often the largest single amount on the financial statements. Total revenues need to be large enough to cover all the expenses. When users see that total revenues are greater than total expenses (when the company has a positive net earnings), they take this as a sign that the company is viable, that it has the ability to take advantage of opportunities, and that it is growing. On the other hand, companies can and do sometimes experience losses—a signal that all is not well with the company. When losses occur, it is important for users to evaluate both the size and cause of the loss. They need to observe the company over time to see how serious the problems are.

When evaluating revenue information, users also want to assess the quality of the earnings: how well management's decisions are reflected in predictable earnings. All earnings must, at some time, translate into cash. Cash is essential to a company's ultimate survival. One way to measure the quality of earnings is to compare the cash flow from operations (statement of cash flows) with the net earnings. If these two amounts are moving together (both up or both down) and if the cash flow is greater than the net earnings, we consider the earnings to be of high quality. If the two amounts do not move together and if the cash flow is less than the net earnings, we consider the earnings to be of low quality.

The second reason users need to be aware of a company's revenue recognition policies is that the revenues that are earned by companies are not all the same, as our opening story showed. Sometimes cash is received when the revenue is recognized; sometimes it precedes it or comes after it. A company can have different revenue recognition policies associated with different types of revenue. Users need to be aware of the company's revenue recognition policies so that they can make judgements about the validity of the revenue amount that is reported. As the article on the previous page shows, sometimes investors are surprised by the revenue source.

accounting in the news

Rolling Stone Goes Digital

Rolling Stone magazine has sought—and likely found—a new revenue stream with the revamping of its website. The magazine has put complete digital replicas of its 43-year archive on-line, along with its current issue, and is charging readers for access to them. In doing so, Rolling Stone has become one of the most prominent magazines to add a “pay wall” to make money on the Web. The magazine's home page will remain mostly free, offering news updates and slide shows of bands on tour; however, reminders will be placed throughout that full access to Rolling Stone's latest issue as well as its archive going back to 1967 is available once credit card information is provided. A one-month pass costs $3.95; annual access is $29.99 and includes a print subscription, which usually costs $19.95 a year. Print subscribers do not get Web access.

Rolling Stone, like the rest of the publishing industry, had a painful 2009—it sold nearly 20% fewer ads than the year before. However, it still has a devoted print readership—average paid circulation in 2009 was about 1.5 million, up from 1.3 million in 2000. With the average age of its readership at 30, the magazine continues to be profitable.

Source: Andrew Vanacore, “Rolling Stone's Archive Going Online, for a Price,” The Globe and Mail, April 16, 2010.

Rolling Stone magazine has found a new source of revenue. While other magazine and newspaper companies are making more of their products available on the internet usually for no cost, Rolling Stone has decided to charge people who want to see back issues of their magazine. Many newspapers allow access to their feature stories for free but charge for their other features. If you buy a paper subscription to a newspaper, you often get access to the total on-line version. Rolling Stone has gone the opposite way. If you pay for the on-line subscription, you will receive the paper version but if you pay for the paper version, you do not get access to the on-line version. Rolling Stone has repackaged an old product in a creative way and is earning revenue on it again.

As you will see later in this chapter, there are standards under IFRS for revenue recognition. Those standards can, however, be applied in various ways. Even within the same industry, companies may choose to recognize the same type of revenue in a different manner. In evaluating a company's performance, it is therefore very important to understand the impact of various revenue recognition policies on the financial statements, and therefore essential to read the disclosures about revenue recognition that accompany the financial statements.

Before we look at the revenue recognition policies in detail, it is important to first understand how cash typically flows through a company. As you saw in the opening story, cash and revenue sometimes coincide and sometimes do not.

LEARNING OBJECTIVE 1

Describe the cash-to-cash cycle of a retail company.

CASH-TO-CASH CYCLE

As we have seen, corporate managers engage in three general types of activities: financing, investing, and operating. Let's focus for a moment on operating activities (the ones that generate most of the revenue).

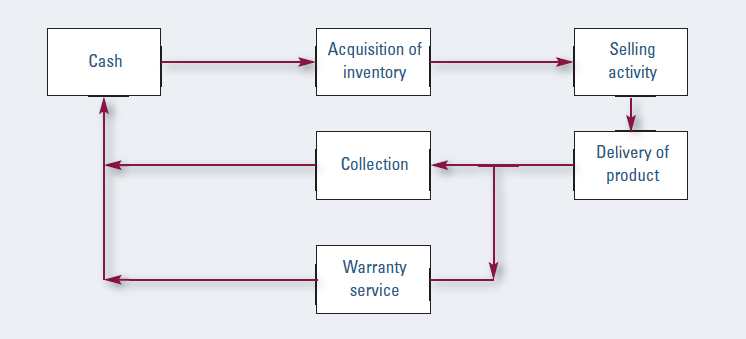

Operating activities include all the normal, day-to-day activities of every business that almost always involve cash. These activities include the normal buying and selling of goods and/or services for the purpose of earning profits. The typical business operation involves an outflow of cash that is followed by an inflow of cash, a process commonly called the cash-to-cash cycle. Exhibit 4-1 shows the cash-to-cash cycle of a typical retail company. Each phase in the cycle is discussed in the following subsections.

Cash

The initial amount of cash in a company comes from the original investment by shareholders and from any loans that the company may have received as start-up financing. To simplify matters, let us assume that the company is being totally financed by shareholders—i.e., without any loans.

Acquisition of Inventory

Before the company acquires the inventory that it will sell to customers or will use to provide its services, it must first undertake the investing activities of acquiring property, plant, and equipment. It then hires labour and purchases the first shipments of inventory (or signs contracts to acquire them). Note that in a retail company, the costs in this initial phase may be larger than those of a service-oriented company. If you visualize even a small retail store, the amount of inventory that must be purchased to initially fill the shelves can be substantial.

EXHIBIT 4-1 CASH-TO-CASH CYCLE OF A RETAIL COMPANY

Selling Activity

The selling phase includes all activities that are designed to promote and sell the product. These may include pricing the product, advertising the product, hiring and managing a sales force, establishing retail sales outlets, contracting with agencies, signing supply agreements, and attending trade shows, among other activities. The end results of this phase are sales contracts between buyers and the seller. These may be verbal agreements, where a customer selects and pays for a product, or formal written documents. For most retail companies selling to customers, the agreement occurs when the goods are paid for in the sales outlet (the store). Some companies, however, sell to other businesses or to large enterprises such as hospitals or schools. For these sales, it is more likely that a formal contract is drawn up, specifying prices, times of delivery, and methods of payment.

Delivery of Product

Once a sales contract has been agreed upon, the product must be delivered to the customer. Depending on the type of product, this may be instantaneous (as in a grocery store), or it may take time (as with a car dealership). Some sales contracts require periodic deliveries of inventory (as with fresh produce to a restaurant).

Collection

Upon delivery of the product, collection of the sales price in cash may be immediate, as in a shoe store, or it could take place at some later date, resulting in an amount owing at the time of delivery, which is called an account receivable. Payment at a later date is the same as the seller making a loan to the buyer and accepting the risk that the buyer will not pay (this is called credit risk). The loan to the buyer may carry interest charges, but usually no interest is charged if payment is made within a short period of time that is specified (typically 30 to 60 days). If the buyer does not pay within the specified time, the seller may try to get the product back (repossession) or may try other methods to collect on the account, such as turning it over to a collection agency.

Other events could also occur that would affect the collection of cash. The goods may be returned for various reasons, resulting in no cash collection. The goods may be damaged in shipment, and the buyer may ask for a price adjustment (generally called a price allowance). There may also be an incentive built in to encourage prompt payment of cash, such as a cash discount, which means that less than the full amount will be accepted as full payment. Just as Outpost does with its advertisers, a seller may offer a 2% price discount if the account is paid within 10 days instead of the usual 30 days. These terms are sometimes stated as 2/10 net 30, which means that a 2% discount is offered if payment is made within 10 days; otherwise, the total amount is due at the end of 30 days.

In the opening story, you read about customers paying for a magazine subscription in advance. In this instance, the company has the cash before using cash to generate magazines. Collecting cash is not a concern for the company, but creating the magazine issues to satisfy the obligation to the customers is. In accepting the cash, the company is agreeing to produce future issues of the magazine and must plan its future activities to satisfy that obligation.

Warranty Service

Some goods carry a written or implied guarantee of quality. Automobiles, for example, are warranted for a certain number of years or for a certain number of kilometres. During this period, the seller is responsible, to some extent, for product replacement or repair. Because the provision of warranty work often involves additional outlays of cash for employees' time and for the purchase of repair parts, warranty service affects the ultimate amount of cash that is available at the end of the cycle. Many retail outlets today that sell products with warranties will cover the warranty for a period of time—perhaps three to six months—and will then sell additional warranty coverage to the customer. If the product needs to be repaired within the extended warranty time, the company has additional funds to offset the cost of that repair. If no repair is needed, the company earns an additional revenue amount.

Summary of the Cash-to-Cash Cycle

The net amount left in cash after this cycle is completed is then available to purchase more goods and services in the next cycle. If the cash inflows are less than the cash outflows, the amount of cash available is reduced, and the company may be unable to begin a new cycle without getting additional cash from outside the company in the form of equity or debt. If cash inflows exceed cash outflows, the company can expand its volume of activity, add another type of productive activity, or return some of the extra cash to shareholders in the form of dividends.

Note that the order of the phases in the cash-to-cash cycle may be different from one company to the next. For example, a transportation contractor such as Bombardier may do most of its selling activity early in the cycle to obtain contracts to deliver products at a future date, with much of the acquisition of raw materials and production taking place after the contract is signed. Also, in some companies, the separate phases may take place simultaneously. At Safeway, for example, the delivery of groceries to the customer and the collection of cash happen at the same time.

REVENUE RECOGNITION

Managers do not want to wait until the end of the cash-to-cash cycle to assess the performance of their company, because they must make day-to-day decisions that will ultimately affect the final cash outcome. If they wait until the end, they may not be able to make appropriate adjustments. For example, if the first few items sold result in significant uncollected accounts or require significant warranty service, they might want to rethink their policies on granting credit and providing warranties. If the cost of warranty service is too high, they might also want to purchase better quality inventory so the products last longer. Furthermore, the cash-to-cash cycle is a continuous process that is constantly beginning and ending for different transactions. There is no specific point in time at which all the cash-to-cash transactions reach an end.

To measure operating performance as accurately as possible, accountants divide normal operating activities into two groups, called revenues and expenses. Revenues are the inflows of cash or other benefits from the business's normal operating activities when these inflows result in an increase in equity that did not come from contributions from equity holders. It is important to note that revenues result from normal operating activities. There are other activities that result in increases in equity that are not from ordinary operating activities. These are not called revenues. Revenues usually involve the sale of goods, the provision of services or allowing others to use the company's assets in exchange for interest, dividends, or royalties. Expenses are the costs incurred to earn revenues. The difference between revenues and expenses, called net earnings (or net income), is one of the key measurements of performance. The expression “in the red” is related to net earnings. In the past, if a company had a negative net earnings (expenses > revenues), the net loss figure was actually written in red ink. The expression came to mean that a company had experienced a loss. Similarly, but less commonly used, the expression “in the black” meant that you had a positive net earnings.

Some companies make profits by charging higher prices, others by controlling costs. New companies in industries where there are already established players face difficult challenges. Note the article on the following page.

The need for timely information in decision-making is an argument for recognizing revenue as early as possible in the cash-to-cash cycle. The earlier in the cycle that revenue is recognized, however, the greater the number of estimates that are needed to measure the net performance. For example, if the company chooses to recognize revenue when the product is delivered to customers (a common practice for many businesses), it will have to make estimates regarding the collectibility of the receivables, the possibility of the customer returning the goods, and the costs of warranty service. To measure the return (profitability) on the sale of a product accurately, these items should be considered; otherwise, the company may be overestimating the profit on the sales of its products. To produce the most accurate measurement of net operating performance, all costs related to the earning of revenues are matched to the revenues they helped earn. In accrual accounting, this is called matching (see Chapter 2). Matching requires the simultaneous recognition of all costs that are or will be incurred (in the past, present, or future) to produce the revenue.

accounting in the news

Discount Fares Not Enough to Cover Costs

Blaming the downturn in the economy and high fuel costs, Zoom Airlines, an Ottawa-based company, suspended operations and filed for bankruptcy protection on August 28, 2008, when one of its planes was seized in Scotland and another in Calgary. The airport authorities in the two locations were owed substantial amounts and held the airplanes to force the airline to pay the amounts owed. Zoom Airlines, a low-fare transatlantic airline, began operating in 2002 hoping to tap into the casual traveller market. It was a small airline operating a small number of airplanes with flights to 15 locations, mainly in Canada and Europe. It offered both scheduled and chartered services. When the seizures occurred, passengers were left stranded, often far from home, and had to scramble to find alternative flights. Those who had purchased tickets for future flights had little hope of recovering their ticket costs.

Source: “Zoom Stops Operations, Strands Passengers,” CTV News, August 28, 2008, http://www.ctv.ca/servlet/ArticleNews/story/CTVNews/20080828/zoom_airline_080828/20080828?hub=TopStories

The question of when to recognize revenue is quite straightforward for some industries (e.g., clothing retailers like H&M). Revenue is recognized when the customer buys the goods in the store. Normally customers pay cash or use a debit or credit card, which means that the collection of cash for the sale is not an issue. While there are no warranty costs for a clothing retailer to consider, items are sometimes returned. Returns are often handled by giving the customer another article of clothing, if one is available, or the value of the returned clothing as a credit to buy a different article. Some retailers return the original cash paid. Clothing stores also usually put a time frame on returns (typically, customers have two weeks to return merchandise), which means the issue of returns is a known quantity very quickly. For other industries, the decision is not as clearly defined. For a manufacturing company such as Bombardier (a maker of trains and airplanes), contracts are signed, merchandise such as a rail car is manufactured, the merchandise is delivered, money is collected from the customer (usually some time after delivery), and warranty services are provided on the merchandise sold. When should such a company recognize revenue: when the contract is signed, when the goods are delivered, when the cash is collected, or when the warranty period expires and all obligations related to the sale have been satisfied?

The earlier in the cash-to-cash cycle the company chooses to recognize revenues, the less reliable the company's estimate of the effects of future events. On the other hand, however, the company receives more timely information. To reduce the uncertainty that is inherent in estimating future events, the company would need to recognize revenues later in the cash-to-cash cycle, when those estimates are more reliable, but the information would be less useful for making management decisions. The decision about when to recognize revenue is a very important one for managers, because it has a major impact on net earnings. Knowing about the revenue recognition policy is also important for users, so that they can assess the reliability of the information and the quality of the earnings.

There is obviously a conflict between the desire to measure performance on a timely basis (early in the cycle) and the ability to measure performance reliably (late in the cycle). Revenue recognition criteria have been developed within IFRS (IAS 18) to resolve this conflict and to produce a measure of performance that is intended to balance the need for timely information with the need for reliable information. The issue is further complicated when the company is involved in two or more lines of business that have different cash-to-cash cycles. A revenue recognition policy must be developed for each line and it is possible that they may not be the same.

Two basic criteria must be met before a revenue item can be recognized. The first is that it is probable that economic benefits will flow to the company. This condition is normally met when the activity that generated the revenue (sometimes referred to as the performance) is substantially completed—in other words, when the earnings process is substantially complete. In general, this would mean that the company has completed most of what it agreed to do and there are very few costs still to be incurred in the cash-to-cash cycle, or the remaining costs can be reasonably estimated, or both. Another way to consider this factor is to determine whether all the risks and rewards of the goods or services have been transferred to the buyer. If they have, there is very little left for the seller to do.

The second criterion is the requirement that the revenue can be reliably measured. This is often straightforward. When goods or services are sold for cash or an agreed selling price (an account receivable), the measurement is easy to determine. Sometimes, however, goods or services are sold in exchange for other products, services, or assets (other than accounts receivable). Now the measurement is more difficult. The accountant must examine the value of the goods or services sold and compare it with the value of the products, services, or assets received. In deciding which of these values to use, the accountant will look for the most reliable amount—the amount that can be most objectively determined. If the amount of revenue cannot be measured, it cannot be recognized. Within the measurement issue, there must be reasonable assurance that the amounts earned can be realized, or collected, from the buyer. If cash is given at the time of sale, this assurance is automatically satisfied. If, however, the goods or services are sold on credit, the seller must be reasonably assured that the amount owing will be collected. Companies rarely sell goods or services on credit without a credit check on the buyer. This is to provide assurance of the probable future collection of the accounts receivable. Even with this assurance, it is possible that some customers will not pay the amounts owed. Because of this possibility, companies that recognize credit sales as revenue must, in the same period, recognize an expense that measures the probable uncollectibility of the accounts receivable. This is to keep the revenues from being overstated. We call this expense “bad debt expense.” More will be said about this expense in Chapter 6.

LEARNING OBJECTIVE 2

List and explain the basic criteria for revenue recognition.

BASIC REVENUE RECOGNITION CRITERIA

- The probable inflow of economic benefits to the company.

- The performance has been achieved.

- The risks and rewards are transferred and/or the earnings process is substantially complete with respect to the sale.

- The amount earned can be measured.

In conclusion, if it is probable that future economic benefits will flow to the company and if the amounts earned can be reliably measured, revenues should be recognized in the financial statements. These conditions are usually met at the time of delivery of the product to the customer, so this is the point at which many companies recognize their revenues. The following sections discuss various applications of revenue recognition, including at the sale of goods to the customer and the sale of services.

LEARNING OBJECTIVE 3

Define earnings management as it relates to revenue recognition and explain why and how it can occur.

Earnings Management

The criteria for revenue recognition, and the matching of expenses with revenues, make it possible for management to evaluate the company's revenue stream and establish a revenue recognition policy that best reflects the company's operating results. Sometimes management deliberately chooses how and when to recognize revenues and costs so that net earnings are higher or lower in particular accounting periods, or smoother over time. This practice is called earnings management.

It is not easy for external users of financial statements to determine if earnings management is taking place, because companies are often very complex. They are engaged in many diversified activities, and it is not possible for users to have a thorough knowledge of all their activities. Sometimes external bodies like the Ontario Securities Commission, or the Securities and Exchange Commission (SEC) in the United States, question a company's revenue recognition policy. As the following story shows, sometimes people within the organization itself identify accounting issues.

accounting in the news

School Board Does Homework in Financial Management

Many news stories in recent years have featured corporations restating their financials due to accounting errors. But sound accounting is necessary in all sectors. Teachers in the Langley School District in British Columbia called for financial reform after noting significant accounting errors. Langley School District, which comprises almost 50 schools and has an annual budget of about $150 million, had amassed a $14 million deficit, even though school districts are not allowed to run deficits under the B.C. School Act. The Langley Teachers' Association called on the Education Minister to appoint a special advisor, as had been done for the Vancouver School Board, which had been deemed “unable or unwilling to manage its resources to protect the interests of the students.”

When the Langley School District's financial problems were first identified in 2009, it arranged a review by an outside accounting firm and asked the provincial auditor general to review its financial management. The Deloitte & Touche review found a series of accounting errors, including schools getting authorization to spend money without approval or funding. Some parents and teachers in Langley have called for a forensic audit to determine how a modest projected surplus in 2009 turned into a multi-million-dollar deficit in 2010. Provincial staff have been working with the school board staff to come up with a plan to eliminate the deficit.

Source: Wendy Stueck, “Teachers to Take Calls for Financial Reform to B.C. Minister's Doorstep,” The Globe and Mail, April 22, 2010.

The teachers in the Langley School District called for an investigation into the accounting issues facing the school district. School districts are not-for-profit organizations. As such, they do not have the same access to funds as a profit organization does. It is therefore vital that they have well-formulated processes for managing expenditures. When those processes are not in place, the money spent can exceed the money available, and a deficit results.

Earnings management can be related to the early or late recognition of revenues and/or to the recognition of expenses before or after their related revenues have been recognized. Because it is difficult to detect, users of financial statements rely on auditors to determine whether accounting standards have been applied appropriately or not. Companies that deliberately manage their earnings may be able to affect the market's valuation of their shares, but when earnings management is discovered such companies usually pay a heavy price through shareholder lawsuits and the lowering of their share values.

In the next section, as you read through the different ways that revenue can be recognized, keep earnings management in mind. For each revenue stream, consider whether earnings management could occur. If it could, would it still meet the revenue recognition criteria?

LEARNING OBJECTIVE 4

Describe the specific revenue recognition criteria and how they apply to the sale of goods, the provision of services, and the use by others of a company's assets.

Applications of Revenue Recognition

The revenue recognition criteria can be met at different points in the cash-to-cash cycle. The point at which different companies recognize revenues varies accordingly, as you observed in the opening story about Outpost magazine. IAS 18 provides revenue recognition criteria for specific types of transactions: the sale of goods, provision of services, and use of the company's assets by others. This section will provide more detail on each of these transactions.

Revenue Recognition for the Sale of Goods

For the sale of goods, there are five specific revenue recognition criteria1 that must be met before revenue can be recognized:

- There has been a transfer of the risks and rewards to the buyer.

- The company no longer has managerial involvement or control over the goods sold.

- The revenue can be measured reliably.

- It is probable that economic benefits from the transaction will flow to the seller.

- The costs incurred or to be incurred with respect to the transaction can be measured reliably.

Recognition at the time of sale The most common point at which sales revenues are recognized is the time of sale and/or shipment of the goods to the customer. Once the goods have been taken by or shipped to the customer, the company has usually completed everything it has to do for the transaction. The title to the goods has been transferred, which transfers the risks and rewards to the buyer, and the company no longer has control over the goods. This meets the first two criteria listed above. At the time of sale, the amount that is earned is known and measureable. Often the customer will pay cash, which provides immediate economic benefits to the seller. If the company sells the goods on credit, the amount owed is also measurable. However, the company will have to be reasonably assured of collection of the account receivable before revenue can be recognized. Most companies will not sell on credit if they have doubts about the future collectibility of the amount. An estimate of potential uncollectibility must be made and an allowance for uncollectible accounts established. At the time of sale, the seller usually knows the costs that are related to the transaction. Thus, the last three criteria are also met.

Outpost magazine recognizes two of its revenues at the time of sale. The time of sale occurs when an issue has been printed and sent to subscribers and distributors. At this point, it has completed the earning process on that issue. It recognizes the revenue from individual subscribers and the revenue from advertisers on a per-issue basis. Prior to releasing an issue, the company can measure how much it has earned because subscribers have paid in advance and advertisers have signed a contract that specifies how much they will pay for advertisements in each issue. The only unknown at the point of sale is whether the advertisers will pay when they receive the bill from the magazine. The company would need to estimate the likelihood of uncollectibility of its advertising revenue. The issues sent to distributors pose more of a problem for Outpost. It has completed the printing of the issues but it will have to wait six months before it knows how much has been earned. It needs to wait until distributors provide information about how many issues were sold and how many issues are being returned before it can measure its earnings. Therefore, because revenue must be measureable to be recognized, Outpost cannot recognize this revenue at the time of delivery.

In annual reports, most companies state their revenue recognition policy as part of the first note, which includes a summary of the company's significant accounting policies. For example, in its 2009 financial statements, Brickworks Limited states its revenue recognition policy in Note 1 (c) to the financial statements. Brickworks Limited is an Australian company that manufactures and sells bricks, tiles, and building supplies. It also sells land and handles waste management. Part of its revenue recognition statement follows:

BRICK WORKS LIMITED (2009)

Revenue

Sales revenue is recognized when the significant risks and rewards of ownership of the items sold have passed to the buyer, and the revenue is also able to be measured reliably.

For revenue from the sale of goods, this occurs upon the delivery of goods to customers.

For revenue from the sale of land held for resale, this is recognized at the point at which any contract of sale in relation to industrial land has become unconditional, and at which settlement has occurred for residential land.

Profits on disposal of investments and property, plant and equipment are recognized at the point where title to the asset has passed.

This is a fairly detailed statement from Brickworks. Note that it frequently refers to the transfer of the risks and rewards of ownership. Note as well the timing of the recognition—when the product is delivered to its customers. Brickworks also has revenue from interest and dividends that will be discussed later in this section. Like Outpost, Brickworks has different types of revenue and must establish different revenue recognition policies.

If a company's revenue is very homogeneous, it will need only a simple statement about revenue recognition. Maple Leaf Foods Inc., in Note 2 (d) to its 2009 financial statements, states: “The Company recognizes revenues from product sales upon transfer of title to customers. Revenue is recorded at the invoice price for each product. An estimate of sales incentives provided to customers is also recognized at the time of sale and is classified as a reduction in reported sales. Sales incentives include various rebate and promotional programs provided to the Company's customers.” Maple Leaf Foods is a Canadian-based food processing company that sells to retail, wholesale, food service, industrial, and agricultural customers. It sells meat and bakery products, as well as feed for animals. Although it has several different customers, it has a single type of revenue (sale of a product) that does not require lengthy disclosure.

Sometimes when you read the description of a company's revenue recognition policy, you will see reference to the term “F.O.B.” F.O.B. means “free on board” and is a legal term to describe the point at which title to the goods passes from the seller to the buyer. It is used by companies like Maple Leaf Foods that deliver goods in large volumes to customers. If the goods are shipped F.O.B. shipping point, the title (ownership) passes after the goods leave the seller's loading dock (the shipping point). If they were shipped F.O.B. destination, the goods would remain the property of the seller until they reached their destination: the buyer's receiving dock. The way the goods are shipped will affect the point at which revenue can be recognized. The point at which title to the goods passes is a clear indication that the seller has earned the revenue. Prior to that point, the seller is still responsible for the goods.

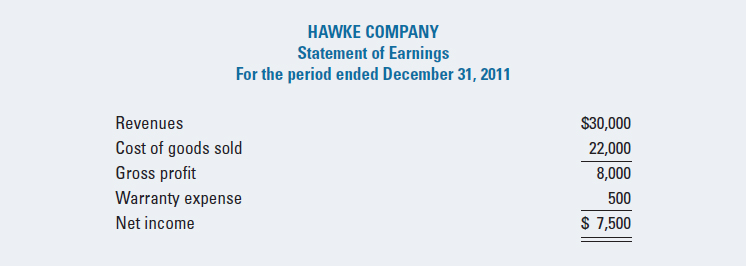

To illustrate revenue recognition at the time of sale, assume that Hawke Company sells 1,000 units of its product during 2011 at $30 per unit. Also assume that the costs of these units totalled $22,000 and that, at the time of sale, Hawke estimated they would cost the company an additional $500 in warranty expenses in the future. Ignoring all other operating expenses, the statement of earnings for Hawke for 2011 would appear as in Exhibit 4-2.

EXHIBIT 4-2 REVENUE RECOGNITION AT TIME OF SALE

Note that although Hawke Company may not have incurred any actual warranty expenses yet, it recognizes an expense for its estimate of what the future warranty costs might be. Recognizing the warranty expense is appropriate because the future warranty costs are directly related to the revenue. Therefore, if the company wants to recognize the revenue before it knows the actual warranty cost, it must estimate what those costs might be so that the income is not overstated. At the same time as it recognizes the warranty expense, it recognizes a liability for these future costs. When actual costs are incurred, the liability is then reduced and no further expense is recognized. In its revenue recognition note, Maple Leaf Foods said that it estimated the cost of the sales incentives and recognized them at the same time as a reduction to the revenue. This treatment is similar to Hawke's treatment of warranty costs.

In some cases, a company might receive a deposit for a product to be delivered in the future. Because it is unlikely that the revenue recognition criteria would be met by this transaction (until the product is delivered, the title has not passed and the risks and rewards of ownership have not been transferred to the buyer), the revenue from this order would not be recorded until the goods are delivered. The deposit is therefore recorded as unearned revenue, deferred revenue, or revenue received in advance (a liability account that represents an obligation either to deliver the goods or to return the deposit). For example, if Hawke Company received a $500 deposit on an order, it would make the following entry:

![]()

When the goods are delivered, the liability to provide the product is satisfied (the company has completed what it had to do in the sale and the title to the goods has passed to the buyer), and the deposit can then be recognized as a revenue item with the following entry:

![]()

Companies that require deposits or advance payments on products or services may disclose this in their footnote on revenue recognition. Note that liabilities are created for the obligation to provide the service or product in the future. Typical disclosures for this type of situation are shown here for WestJet Airlines Ltd. (2009).

WESTJET AIRLINES LTD. (2009)

- Summary of Significant Accounting Policies

d) Revenue recognition

- (i) Guest revenues

Guest revenues, including the air component of vacation packages, are recognized when air transportation is provided. Tickets sold but not yet used are reported in the consolidated balance sheet as advance ticket sales.

- (ii) Charter and other revenues

Charter and other revenues include charter revenue, cargo revenue, net revenues from the sale of the land component of vacation packages, ancillary revenues and other.

Charter and cargo revenue is recognized when air transportation is provided. Revenue from the land component of vacation packages is generated from providing agency services equal to the amount paid by the guest for products and services less payment to the travel supplier, and are reported at the net amounts received. Revenue from the land component is deferred as advanced ticket sales and recognized in earnings on completion of the vacation.

Ancillary revenues are recognized as the services and products are provided to the guests. Included in ancillary revenues are fees associated with guest itinerary changes or cancellations, excess baggage fees, buy-on-board sales and pre-reserved seating fees.

Included in other revenue is revenue from expired non-refundable guest credits recognized at the time of expiry.

- (i) Guest revenues

Users should be aware of one other aspect of revenue recognition: sales returns. In many retail stores, customers are allowed to return merchandise. Usually a time is specified, such as 10 days or one month. When goods are returned, the company either returns the amount paid or gives a credit that allows the customer to buy new merchandise. Technically, the company should take into consideration the cost of possible returns when it recognizes revenue; otherwise, its income may be overstated. In reality, the time period in which returns are allowed is usually short, which means that the income is not materially misstated if the returns are recorded when they happen. For companies that sell to other companies (business-to-business sales), the returns can be substantial. For example, in the bookselling business, publishers often accept back from booksellers the books that have not been sold. This can result in a substantial amount of returns, depending on how well a book sells. If such companies want to recognize revenue when they ship books to a bookseller, they must estimate the amount of returns and recognize that amount when the revenue is recognized. The issue of returns has been particularly problematic for companies that sell through the Internet. Note the following example:

accounting in the news

Growth of On-line Shopping

On-line shopping has been growing steadily in Western Europe. The most popular items bought are books, followed by travel and clothing. Among the big drawbacks that discourage customers from buying on-line are shipping costs and the difficulty to return goods. Buying clothing on-line is difficult because many customers like to feel items and try them on before buying them. This is not possible with on-line shopping, so on-line sellers of clothing have a much higher return rate than a physical retail outlet would have.

Source: Katie Deatsch, “Online Shopping is Growing Steadily in Western Europe, Forrester Says,” Internet Retailer, March 27, 2009. http://www.internetretailer.com/2009/03/27/online-shopping-is-growing-steadily-in-western-europe-forrester

Recognition at the time of contract signing Even though the point of sale—or more correctly, the point at which title to the product is transferred to the buyer from the seller—is the most common method used to recognize revenues, several situations exist that require exceptions to this application of revenue recognition. Over the years, certain types of transactions have caused concern among investors and accountants because of how the companies chose to recognize revenues. One of those was in the area of retail land sales. This industry initially recognized revenues at the date of contract signing. In the case of retail land sale companies, it was the land sale agreement. The problem was that a considerable amount of uncertainty existed regarding future costs on the seller's part subsequent to contract signing, and to the collectibility of the receivables from buyers. Questions were raised as to whether any of the revenue recognition criteria were being met.

The uncertainty stemmed from industry practices. Retail land sale companies often sell land before it is developed and therefore have yet to incur the development costs. This means that the seller has not completed all the things that must be done; the seller still has continuing management involvement in the development of the property. There is also the problem of matching the future development costs to the revenues. Remember that if you want to recognize revenue before all the costs associated with the sale are incurred (note the warranty example), you must be able to estimate those future costs so that they can be recognized simultaneously with the revenue (according to the matching principle). Sales contracts typically require low down payments and sometimes include below-market interest rates to entice buyers to sign contracts. These conditions make it relatively easy for a buyer to back out of the transaction before all the cash is collected, thereby negating the sale and raising the possibility that future economic benefits may not flow to the seller.

Given that the earning process was rarely complete, and there were uncertainties with regard to future costs and the collectibility of the receivables, revenue for retail land sale companies is now only recognized at the time of contract signing if certain minimum criteria are met. These criteria require, first, that there be only minimal costs yet to be incurred (this means that the seller has completed substantially all the things that have to be done to conclude the sale), and second, that the receivables created in the transaction have a reasonable chance of being collected.

Recognition at the time of production Revenue recognition at the time of production was common in two industries: mining and long-term construction. If the product's market value and sale are both fairly certain at the time of production, as it was in certain mining operations, then the inventories produced can be valued at their net realizable value (selling price) and the resulting revenues can be recognized immediately. The reason for this practice was that the critical event in the revenue earning process for the mine was not the ore's sale, but its production. If the market for the ore was well established with fairly stable prices and there were buyers for the ore, the sale was assured as soon as the ore was produced. By recording the revenues as soon as possible, these companies had more timely information for making decisions. Although this was an acceptable practice at the time, it no longer is. The current mining market is unstable, as prices for various ores fluctuate daily. Therefore, resource companies now delay the recognition of the revenue until the ore is actually delivered. Many companies manage the risk of changing prices by purchasing forward contracts to sell their ore at a fixed price. A forward contract is an agreement between a buyer and a seller that establishes a fixed selling price.

The following example presents the revenue recognition method of the international mining company Barrick Gold Corporation, which operates gold and copper mines:

BARRICK GOLD CORPORATION (2009)

- 5. Revenues

Revenue Recognition

We record revenue when the following conditions are met: persuasive evidence of an arrangement exists; delivery and transfer of title (gold revenue only) have occurred under the terms of the arrangement; the price is fixed or determinable; and collectability is reasonably assured.

Note that for Barrick Gold Corporation, the earning process is complete when title to the gold has passed. At this point, the sale's final amount is certain. Because it uses forward or option contracts, the amount earned is known for certain. A forward or option contract stipulates the amount that will be received for the gold in the future.

The other industry that recognizes revenue at the time of production is the long-term construction industry, which has a long production period. In this industry, revenue is recognized using the percentage of completion method, which recognizes a portion of a project's revenues and expenses during the construction period based on the percentage of completion. The basis for determining the percentage completed is usually the costs incurred relative to the estimated total costs.

LEARNING OBJECTIVE 5

Explain the impact that various revenue recognition methods have on earnings recognition.

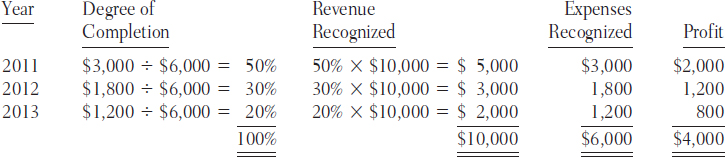

As an example, suppose that Solid Construction Company agrees to construct a building for $300 million. It will take three years to build, and the company expects to incur costs of $75 million, $105 million, and $30 million in 2011, 2012, and 2013, respectively. The total expected cost is $210 million and, therefore, the profit on the project is expected to be $90 million. Assuming that all goes according to plan, Exhibit 4-3 shows how Solid Construction would recognize the revenues and expenses (and related profits) during the three years with the percentage of completion method.

LEARNING OBJECTIVE 6

Calculate amounts to be recognized under the percentage of completion method.

EXHIBIT 4-3 REVENUE RECOGNITION WITH THE PERCENTAGE OF COMPLETION METHOD (amounts in millions)

How well does the percentage of completion method meet the revenue recognition criteria? The total revenue can be measured reliably and, because of the construction contract, it is probable that the economic benefits will flow to the builder. For many long-term construction contracts, the buyer is often billed periodically during the construction process. The periodic billing and collection provide the seller with the ability to estimate collectability. The costs incurred to date are known and can be recognized when the revenue is recognized. It is also possible to reliably measure the cost to complete the contract and the stage of the contract. Has the builder transferred the risks and rewards of ownership to the buyer? It is assumed that the transfer of the risks and rewards of ownership are transferred as the contract proceeds through the building phases. This is not the same as the title but is accepted as a sufficient basis for recognizing revenue.

Instead of waiting until all the contract work has been completed (which can take several years), this method allows the company to measure how much work has been completed so far and then recognize as revenue the same percentage of the total contract price. The expenses for the period and the percentage of revenue earned are recognized each period, which provides timely information to users. The total revenue from the contract is known before the work begins. The company also has an estimate of the total costs that it expects to incur. As actual costs are incurred and some of the work is completed, we can calculate how much of the contract is finished and, therefore, how much revenue has been earned. We do that using the formulae in Exhibit 4-3.

The disclosure below for Bombardier Inc. (used as an example earlier in this chapter) for the fiscal year ending January 31, 2010, illustrates the percentage of completion method of revenue recognition.

BOMBARDIER INC. (2010)

Revenue recognition

Aerospace programs Revenues from the sale of commercial aircraft and light business aircraft (Learjet Series) are recognized upon final delivery of products and presented in manufacturing revenues.

Medium and large business aircraft (Challenger and Global Series) contracts are segmented between green aircraft (i.e., before external painting and installation of customer-selected interiors and optional avionics) and completion. Revenues are recognized based on green aircraft deliveries (when certain conditions are met), and upon final acceptance of interiors and optional avionics by customers. Revenues for green aircraft delivery and completion are presented in manufacturing revenues.

Long-term contracts Revenues from long-term contracts related to designing, engineering, or manufacturing of products, including vehicle and component overhaul, are recognized using the percentage-of-completion method of accounting. The percentage of completion is generally determined by comparing the actual costs incurred to the total costs anticipated for the entire contract, excluding costs that are not representative of the measure of performance. Vehicle and component overhaul revenues are presented in services revenues. System and signaling revenues are presented in other revenues. All other long-term manufacturing contract revenues are presented in manufacturing revenues.

Revenues from maintenance service contracts entered into on or after December 17, 2003, are recognized in proportion to the total costs originally anticipated to be incurred at the beginning of the contract and are presented in services revenues. Maintenance service contracts entered into before this date are recognized using the percentage-of-completion method of accounting.

Revenues from other long-term service contracts are generally recognized as services are rendered and are presented in services revenues.

Estimated revenues from long-term contracts include revenues from change orders and claims when it is probable that they will result in additional revenues in an amount that can be reliably estimated.

If a contract review indicates a negative gross margin, the entire expected loss on the contract is recognized in cost of sales in the period in which the negative gross margin is identified.

In some cases, it may not be possible to measure how much of the project is completed, which would make it difficult to measure the revenue earned. There could also be a question about the future collectability on the contract, although it is doubtful that a company would continue work on a project if it was concerned about the future payment for its work. If it is not possible to reliably estimate future costs and revenues, revenue can only be recognized at an amount equal to the construction costs already incurred, and assuming also that the recognized revenue will be collectible.

With the percentage of completion method, if an overall loss is projected on the project, IFRS requires that the loss be recognized as soon as it is identified. For example, if, at the end of 2012, the total estimated costs to complete the Solid Construction contract were $315 million (instead of the original $210 million), an overall loss of $15 million would be indicated for the contract. At the end of 2012, Solid Construction would have to recognize a loss of $48 million (the overall loss of $15 million plus the $33 million in profit recognized in 2011). This loss would offset the $33 million profit reported in 2011 and would result in a net loss at this point of $15 million on the contract. If the actual costs equalled the new estimated costs in 2013, no additional profit or loss would be recorded in 2013, as the overall loss on the contract would already have been recognized. The details for an expected loss on a long-term contract do not need to be learned until you take an intermediate accounting course. For now, however, it is important that you understand that contract losses can occur and that the total potential loss is recognized in the year that the loss is determined. Note that Bombardier has a statement about how it recognizes expected contract losses.

Recognition at the time of collection Except for cash sales, revenue recognition criteria are almost always met before cash is collected. Therefore, for reporting purposes, the collectibility of cash rarely delays the recognition of revenue. Magazines such as Outpost have one of those rare circumstances. When Outpost sends magazines to a distributor for sale on newsstands, it does not know how much it has earned until it receives the money from the distributor six months later. It has no choice but to delay the recognition of revenue.

There are other circumstances under which the collection of receivables is so uncertain that accounting standards would require that revenue recognition be postponed until cash is actually collected. Some companies allow their customers to pay for their merchandise through instalments over an extended period of time. Many companies that sell merchandise this way have learned about the probability of collecting all the amounts owed by their customers. These companies will recognize revenue at the time of the original sale and recognize the probability of uncollectibility at the same time. However, there are rare situations where it is not possible to estimate the probability of collection. In these rare cases, the company would need to delay the recognition of revenue until the actual cash is received.

Revenue Recognition for Delivery of Services

Companies that earn revenue from the delivery of services are a growing sector of the economy. The revenue recognized by WestJet for passenger flights is service revenue. Bombardier, as well, described how it accounts for maintenance and long-term service contracts. The criteria for the recognition of service revenue are very similar to the criteria for the sale of goods2:

- The amount of revenue can be measured reliably.

- It is probable that economic benefits from the service will flow to the provider.

- The stage of completion of the service can be measured reliably.

- The costs incurred or to be incurred with respect to the transaction can be measured reliably.

Revenue from the provision of services is normally recognized in the period when the service is completed. If the service takes a long time to complete, the percentage of completion method is used when the costs and the probable revenue can be measured reliably. Financial institutions are one of the largest providers of services. The Toronto-Dominion Bank, one of Canada's major banks, describes its revenue recognition policy as follows:

TORONTO-DOMINION BANK (2009)

Note 1 Summary of Significant Accounting Policies

Revenue Recognition

Investment and securities services include asset management, administration and commission fees, and investment banking fees. Asset management administration and commissions fees from investment management and related services, custody and institutional trust services and brokerage services are all recognized over the period in which the related service is rendered. Investment banking fees include advisory fees, which are recognized as income when earned, and underwriting fees, net of syndicate expenses, which are recognized as income when the Bank has rendered all services to the issuer and is entitled to collect the fee.

Card services include interchange income from credit and debit cards and annual fees. Fee income, including service charges, is recognized as earned, except for annual fees, which are recognized over a 12-month period.

Revenue from the Use by Others of a Company's Assets

Companies can also earn revenue by allowing others to use their assets. The revenue is in the form of interest, dividends, or royalties. The recognition of the revenue from these sources follows the basic revenue recognition criteria plus additional specifications depending on the type of revenue.

Interest revenue is recognized after the issuance of the interest-bearing asset and is proportional to the time that has passed. For example, if a company accepts a $5,000, 3-month, 5% interest-bearing note receivable from a customer on February 1, 2011, interest will be earned on March 1, April 1, and May1, and would be calculated as follows for each month: $5,000 × 0.05 × 1/12 = $20.83.

The journal entries for this note receivable would be as follows:

When a company owns shares (has an investment) in another company, it may receive dividends from the other company. When dividends are declared by the board of directors of the other company, the company is legally obligated to distribute the dividends to shareholders in proportion to the number of shares owned. For example, assume that Hawke Company buys 500 shares in Axle Corporation. On June 1, 2011, the board of directors of Axle Corporation declared a dividend of $0.07 per share payable to shareholders on June 21, 2011. Hawke Company would record the following:

If a company owns a licence, copyright, patent, or other intangible asset, it could allow other companies to use the rights associated with the asset in return for a royalty. Royalty revenue is recognized on the accrual basis according to the contractual agreement that outlines the amount and timing of the payments. For example, assume that on September 24, 2011, Hawke Company purchased 10 airport taxi licences from the city for $5,000 each. Hawke does not own taxis but intends to resell the rights to individual taxi owners for $300 a month, payable monthly. On October 1, Hawke Company drew up a contract with Jonathan Wittly for the use of one taxi licence for six months. Hawke would record the following transactions:

Oct. 1 (no journal entry because Jonathan Wittly has not used the licence yet)

Companies often earn these types of revenue in addition to selling goods or performing services. As the following note shows, Brickworks Limited, the company you met earlier in the chapter and that sells bricks, tiles, and other building products, also has the kind of revenue described above:

Revenue

Interest revenue is recognized on a time proportionate basis that takes into account the effective interest rate applicable to the net carrying amount of the financial asset.

Dividend revenue is recognised when the right to receive a dividend has been established. Dividends received from associates and joint venture entities are accounted for in accordance with the equity method of accounting.

Rental revenue is recognized on an accrual basis

Revenue Recognized from Multiple Lines of Business

In businesses that have multiple lines of business or that sell products in either standard or customized models, the revenue recognition criteria may be met at different points for different products. The disclosures that follow for Finning International Inc. illustrate this point. Finning International is the largest Caterpillar equipment dealer in the world. Caterpillar equipment includes large construction and mining equipment like large earth movers used in highway construction.

FINNING INTERNATIONAL INC. (2009)

- Significant accounting policies

- (o) Revenue Recognition

Revenue recognition, with the exception of cash sales, occurs when there is a written arrangement in the form of a contract or purchase order with the customer, a fixed or determinable sales price is established with the customer, performance requirements are achieved, and ultimate collection of the revenue is reasonably assured. Revenue is recognized as performance requirements are achieved in accordance with the following:

- Revenue from sales of equipment is recognized at the time title to the equipment and significant risks of ownership passes to the customer, which is generally at the time of shipment of the product to the customer;

- Revenue from sales of equipment includes construction contracts with customers that involve the design, installation, and assembly of power and energy equipment systems. Revenue is recognized on a percentage of completion basis proportionate to the work that has been completed which is based on associated costs incurred;

- Revenue from equipment rentals and operating leases is recognized in accordance with the terms of the relevant agreement with the customer, either evenly over the term of that agreement or on a usage basis such as the number of hours that the equipment is used; and

- Revenue from product support services includes sales of parts and servicing of equipment. For sales of parts, revenue is recognized when the part is shipped to the customer or when the part is installed in the customer's equipment. For servicing of equipment, revenue is recognized as the service work is performed. Product support is also offered to customers in the form of long-term maintenance and repair contracts. For these contracts, revenue is recognized on a basis proportionate to the service work that has been performed based on the parts and labour service provided. Parts revenue is recognized based on parts list price and service revenue is recognized based on standard billing labour rates. Any losses estimated during the term of the contract are recognized when identified.

Ethics in Accounting

ethics in accounting

Pressures to show profit or growth in revenues, or both, can create ethical dilemmas for managers and accountants. Some of these pressures are self-imposed, particularly if the manager's compensation is tied to reported profits or revenues. Other pressures may be externally imposed by someone more senior in the organization or by the shareholders. Suppose, for example, that you are the accountant of a company division and the division manager has asked you to make an adjusting entry for the period to recognize a large order. Revenue in your company is usually recorded when the goods are shipped, not when the order is placed. The manager has indicated that this order will bump the division over its sales target for the year and that the bonuses of several managers in the division will be significantly affected. She has also said that the company is about to issue more common shares and that the company would like to show improved results from last year to get the most favourable price for the shares that will be issued. What should you do? Identify the individuals who will be helped and hurt by your decision, in order to help you determine what to do.

The choice of a revenue recognition policy is one of the critical policy decisions for a company. Current and future profitability measures will be affected by when revenue is recognized. Companies must choose a revenue recognition policy that is appropriate for their revenue streams and must disclose what that policy is so that users can make informed decisions.

STATEMENT OF EARNINGS FORMAT

One of the most fundamental objectives of financial reporting is to ensure that financial statements provide information that is useful to the users. To be useful, the information should enable investors, creditors, and other users to understand the enterprise's performance and financial position, and help them assess the amount, timing, and certainty of future net cash flows to the enterprise.

As you learned in Chapter 1, the purpose of the statement of earnings is to provide information about the company's performance. The statement summarizes all the revenues and expenses to show the net earnings or net income. The information is primarily historical. The revenues are the historical amounts received or receivable from the sale of goods and services, and the expenses are based on the amounts actually paid or payable for the goods and services that were used to produce the revenues. Some of the expenses may represent very old costs—for example, the depreciation of very old assets such as buildings.

For the statement of earnings to provide information about future cash flows, the connection between the amounts presented in the statement and those future cash flows must be understood. As you learned in this chapter, accrual-basis accounting requires that revenues and expenses be recorded at amounts that are ultimately expected to be received or paid in cash. For example, to estimate the actual amount of cash that will be collected from sales, the company estimates the amount of sales that will not be collected (bad debts) and deducts that amount from the sales. On the expense side, estimates are made for some expenses where amounts are not yet paid, such as for warranties or taxes. In both cases, the figures reflect management's estimates about future cash flows. Thus, the statement of earnings provides information to readers about management's assessment of the ultimate cash flows that will result from the period's operations. This means that the statement of earnings, prepared according to IFRS on an accrual basis, actually provides more information about future cash flows than a statement of earnings prepared on a cash basis, which only reflects the cash flows that have already occurred.

A second aspect of providing information about future cash flows is the statement's forecasting ability. If trends in the revenues and expenses over several time periods are examined, the revenues and expenses that will occur in the future may be predicted (assuming that trends in the past continue into the future). An understanding of how revenues and expenses are related to cash flows will allow a reasonable prediction of the amount of cash flows that will result in future periods.

The ability to predict future revenues and expenses depends on the type of item being considered, the industry in which the company operates, and the company's history. If the business is in a fairly stable product line, the sales revenues and cost of goods sold figures may be reasonably predictable. However, this type of forecasting is much more difficult for new businesses and new products.

Some other types of items on the statement of earnings are not very predictable. Sales of capital assets, for example, tend to be more sporadic than normal sales of goods or services. Some items may occur only once and cannot, therefore, be projected into the future. For example, the closing of a plant or the sale of a business unit is an event that has implications for the statement of earnings in the current period, but will likely not be repeated in the future.

To enable readers of the statement of earnings to make the best estimates or projections of future results, the continuing items should be separated from any non-continuing items. For this reason, the format of the statement is designed to highlight these differences.

LEARNING OBJECTIVE 7

Understand the difference between a multi-step statement of earnings and a single-step one.

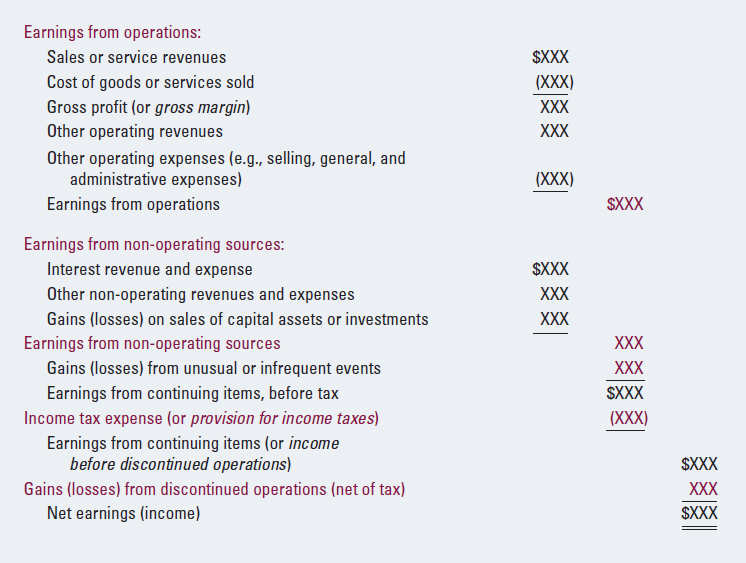

In general terms, there are two approaches to presenting information on a statement of earnings: the multi-step format and the single-step format. We will illustrate and discuss the multi-step format first.

Exhibit 4-4 provides an overview of the major sections of a typical statement of earnings presented in the multi-step format.

EXHIBIT 4-4 MULTI-STEP STATEMENT OF EARNINGS FORMAT

The sections that follow discuss each of the major components.

Earnings from Operations

This section provides information about the revenues and expenses that result from selling goods and services. The operations that are reported are the company's normal operating activities that are expected to continue in the future. Later in the statement, there are sections for items that are not part of regular activities, including the results of any operations that management has decided to discontinue.

A distinguishing feature of many multi-step statements of earnings is that the statement starts with sales less the cost of the goods sold (or cost of sales), to arrive at a gross profit or gross margin amount. If a company's major source of revenue is selling goods, it must make enough profit or margin from the sales of its goods to cover all the other costs of operating the business. By examining the gross margin, users can assess the profitability of the company's products. You can also calculate a gross margin percentage, which is the gross margin divided by the sales. You can then use this percentage to evaluate a company's performance over time (by noting whether this percentage has been increasing, decreasing, or remaining stable) and to compare it with other companies in the same industry. The gross margin can therefore be a very informative and useful figure.

Following this, other normal operating revenues (if any) will be added, and all the usual operating expenses will be deducted, to show the amount of income that was generated from regular business operations that will continue in the future. For predictive purposes, this is usually a key figure on the statement of earnings.

Earnings from Non-Operating Sources

This section of the statement of earnings reports the results of transactions that are not part of the company's core operations. The typical types of items found here are interest income and expense, gains or losses on disposals of capital assets (such as property, plant, and equipment), and other events or transactions that are not considered part of the company's core business operations. IFRS guidelines do not strictly specify what should be included in each section of a multi-step statement.

LEARNING OBJECTIVE 8

Describe the criteria for unusual or infrequent items and discontinued operations.

Earnings from Unusual or Infrequent Events