chapter 8

Interest Rate Products: Vanilla to Exotic

LEARNING OBJECTIVES

This chapter aims to make readers understand the different types of structures/ideas which can be used for hedging against volatility of interest rates accruing from assets or liabilities on balance sheet or for expressing directional/ volatility view on rates market. It takes readers deep into the technicalities and complexities of the market explained in a simple yet effective manner with practical examples. This chapter assumes that readers have an understanding of fixed income mathematics including time values of money and land market calculations. Execution of various kinds of structures depends on prevailing regulations and laws of the land and their suitability for various investors from risk-return perspective. The contents of this chapter are organized in the following order:

5. Key Concepts of Rates Market

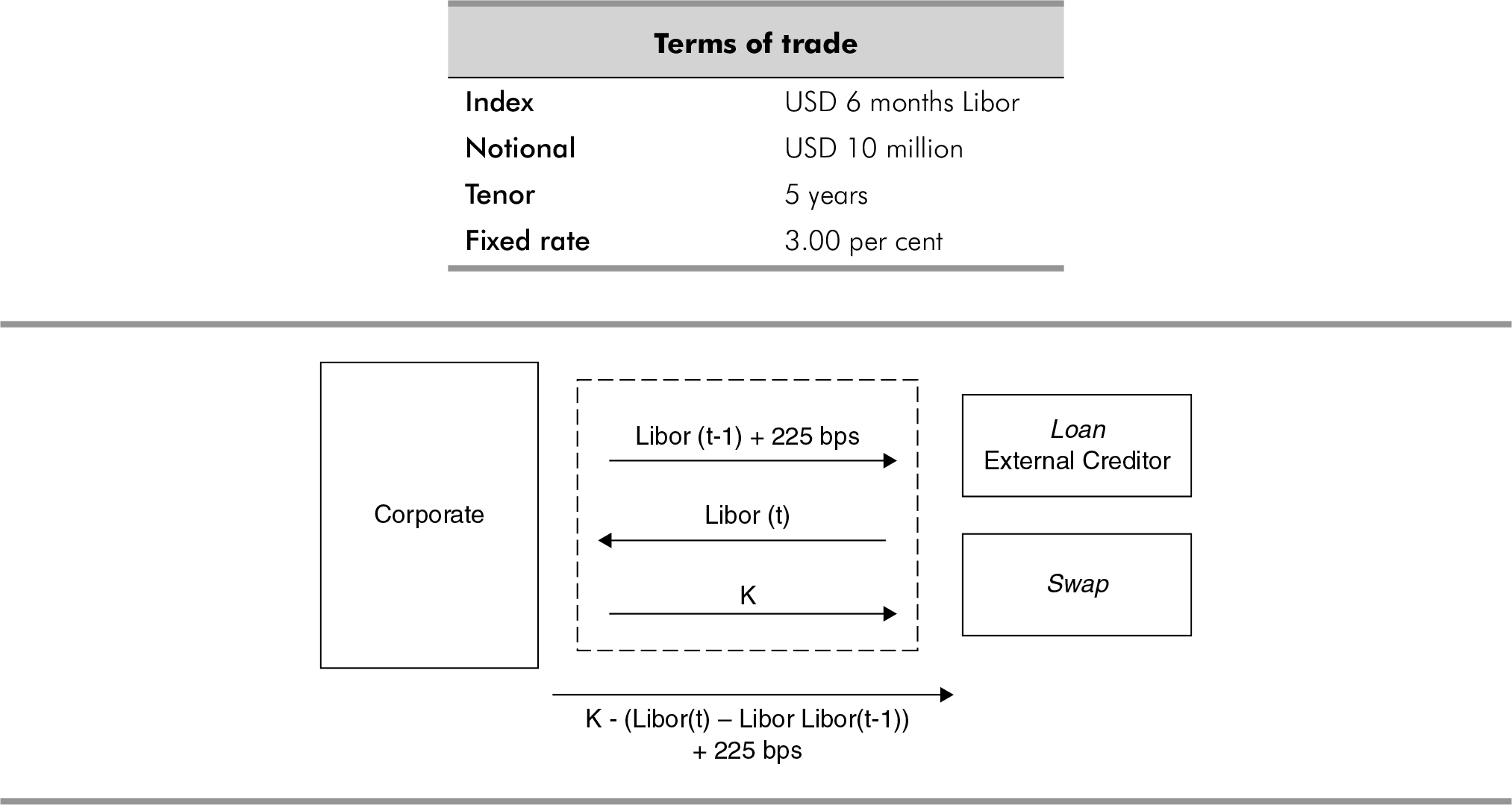

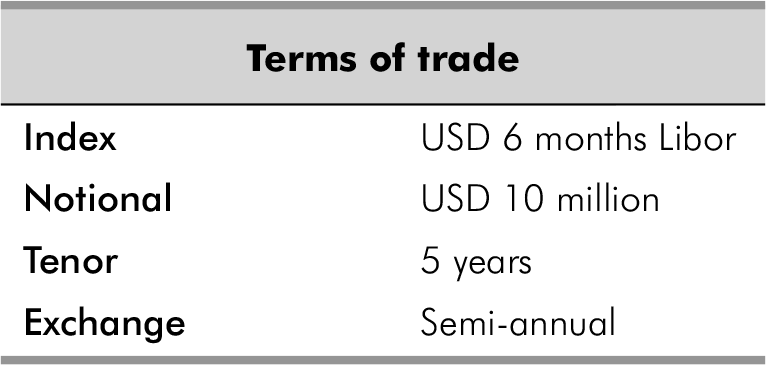

INTEREST RATE SWAPS

Strategy Term: Interest Rate Swap

Strategy Description: It exchanges floating/fix coupon cash flows of a benchmark (e.g. USD six months Libor) for fixed/floating cash flows. Using this strategy, counterparty can either convert his floating rate linked cash flows into fixed rate linked cash flows or vice versa depending on its requirement and market view.

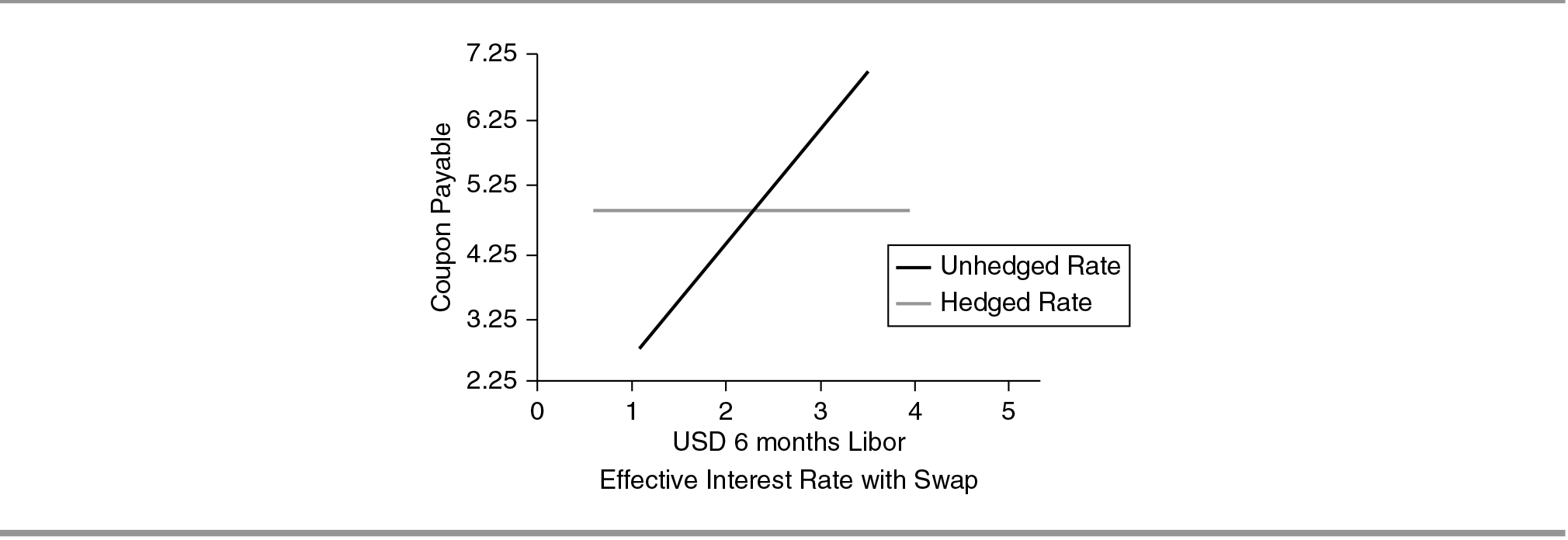

Strategy Application: If the contract holder is concerned about the impact, an increase in interest rate will have on his floating rate payables, and seeks to remove uncertainty from his interest payment, then he can enter into an Interest Rate Swap whereby at periodic intervals, the contract holder receives the floating rate benchmark, and pays a fixed coupon or vice versa in case he has fixed rate payables and has a view that interest rate would come down.

The fixing is done in advance, while the payment is done in arrears. This means that the floating rate to be paid each time is observed at the beginning of the period, while the actual payment exchange is done at the end of the period. (Thus, one coupon payment on the floating side is always known).

The swap can be structured in such a manner that the coupon is exchanged on varying notions each year, to account for the amortization.

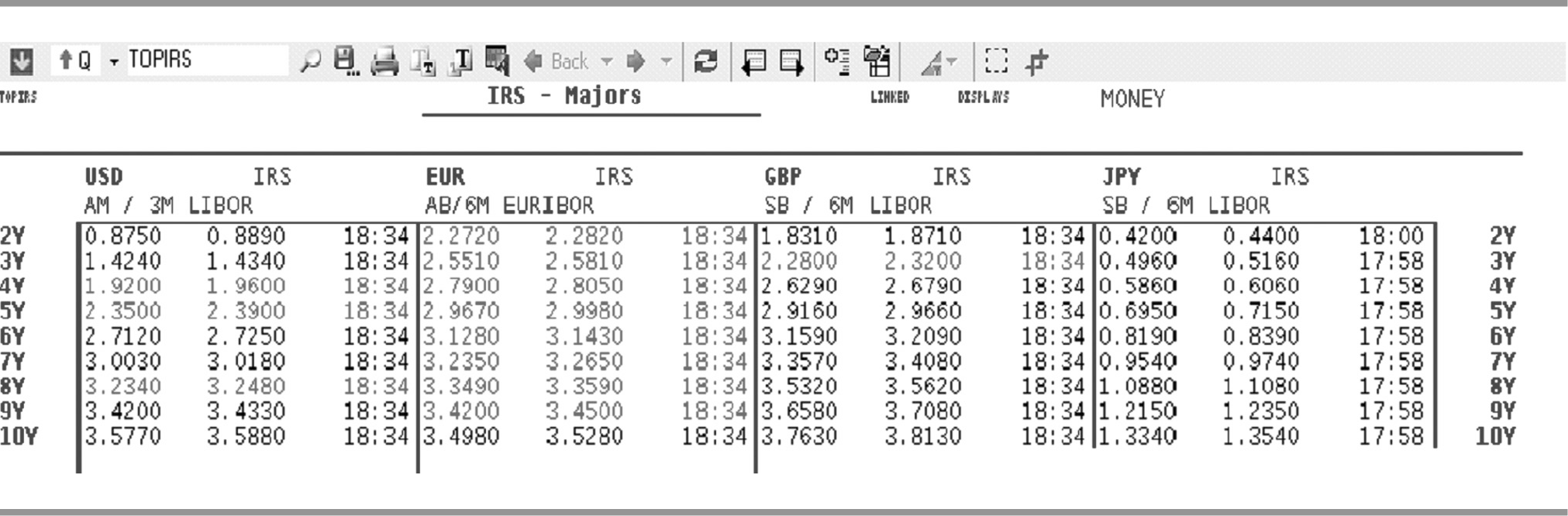

Screenshot 8.1 Swap Rates of Major Currencies USD, EUR, GBP and JPY for Various Tenors Ranging from 2 years to 10 years.

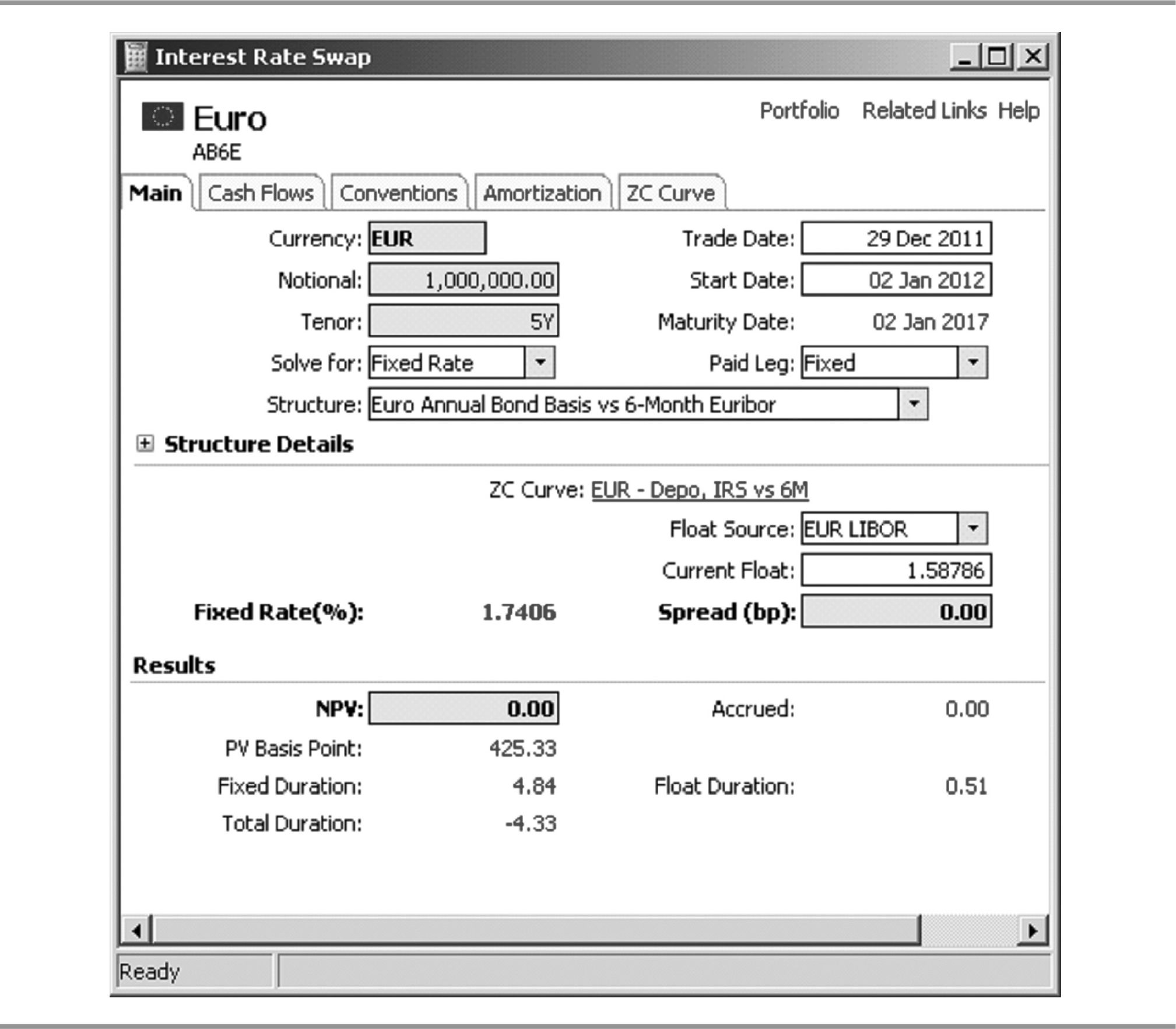

Screenshot 8.2 Interest Rate Swap Calculator

Payoff: Swap with fixed rate K. For each payment period:

- Contract holder pays: K.

- Contract holder receives: Floating benchmark.

Please find below cash flows as they would occur:

Thus, the interest rate risk is mitigated and the interest payments have become fixed.

Graph 8.1

Pros

- There is absolutely no uncertainty in the interest rate to be paid.

- The contract holder can save significant amounts if the floating interest rates rise above the swap level.

Risks Involved

- Even if the interest rates fall, the contract holder still has to pay the same fixed rate and would get no benefit of the favourable movement.

Forward Rate Agreement

Strategy Term: Forward Rate Agreement (FRA)

Strategy Description: It is an agreement to exchange a fixed interest rate with floating or vice versa on a specified notional at a specified future date.

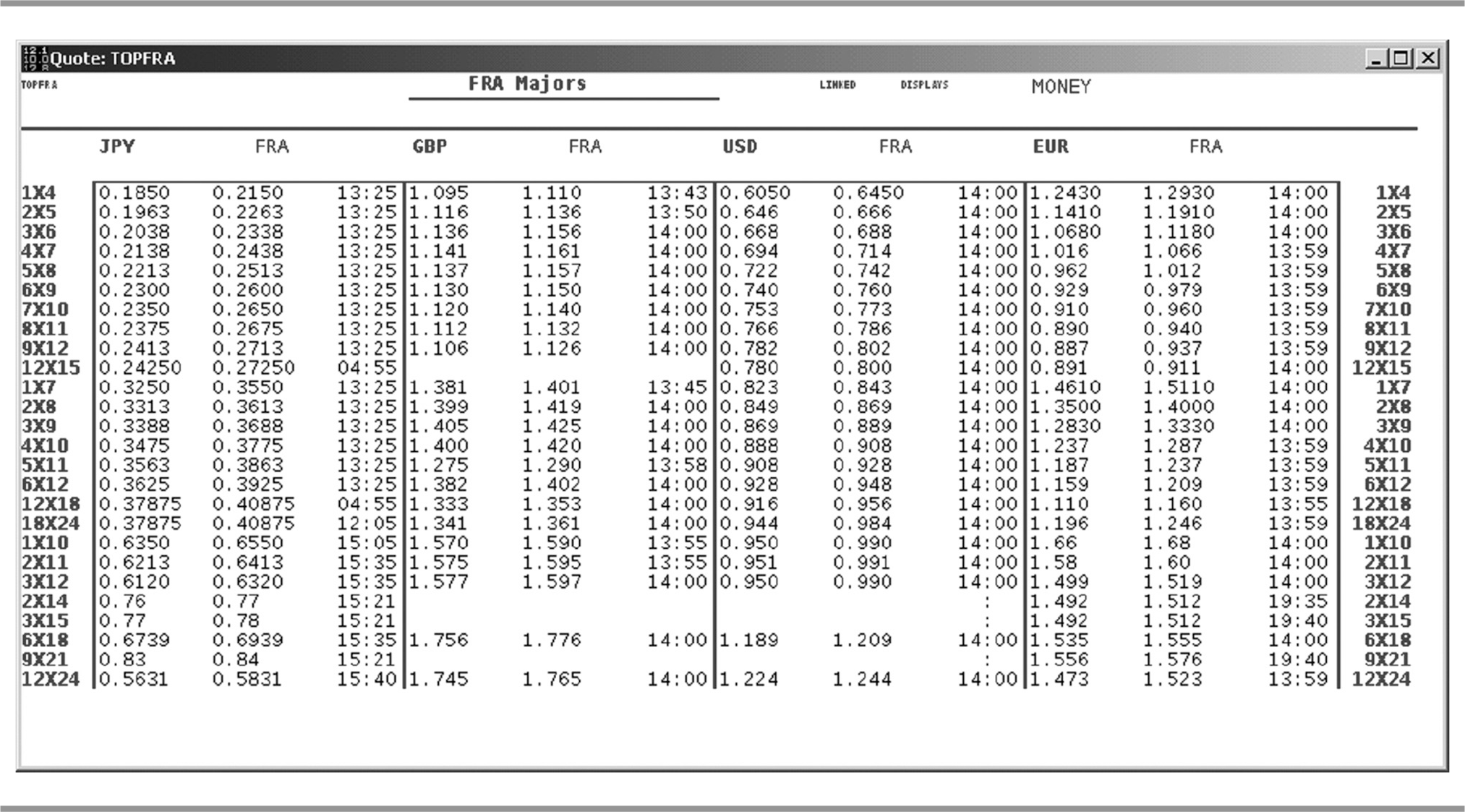

Screenshot 8.3 FRA Levels for Major Currencies

Strategy Application: Consider a counterparty with a one-time exposure to a floating rate index at a future date. The contract holder is concerned about a hike in interest rates which will increase his interest rate liability linked to floating rate.

In such a case, the contract holder can enter into a FRA. This deal would result in the contract holder receiving Libor in exchange of a fixed coupon at a future date. Hence, this would convert the contract holder’s floating rate liability into the fixed rate liability.

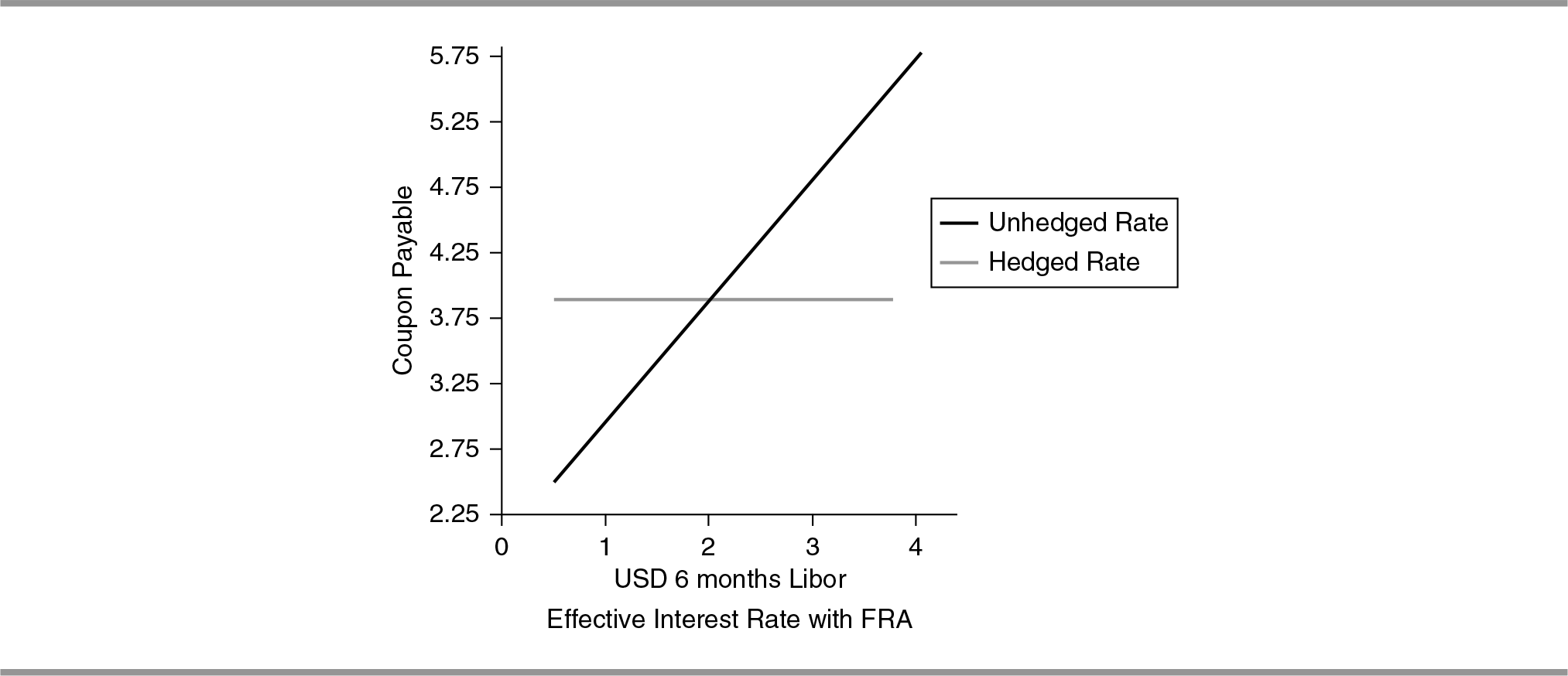

Payoff: FRA with fixed rate K. Today time: time t0

Period specified: t1 × t2

Contract holder receives/pays: one-time payment at time t1. This is calculated as Floating benchmark at t1– K. This can be positive (+ve) or negative (–ve).

Pros

- There is absolutely no uncertainty in the interest rate to be paid.

- The contract holder can save significant amounts if US interests rates rise above the swap level.

Risks Involved

- Even if interest rates fall, the contract holder still has to pay the same fixed rate.

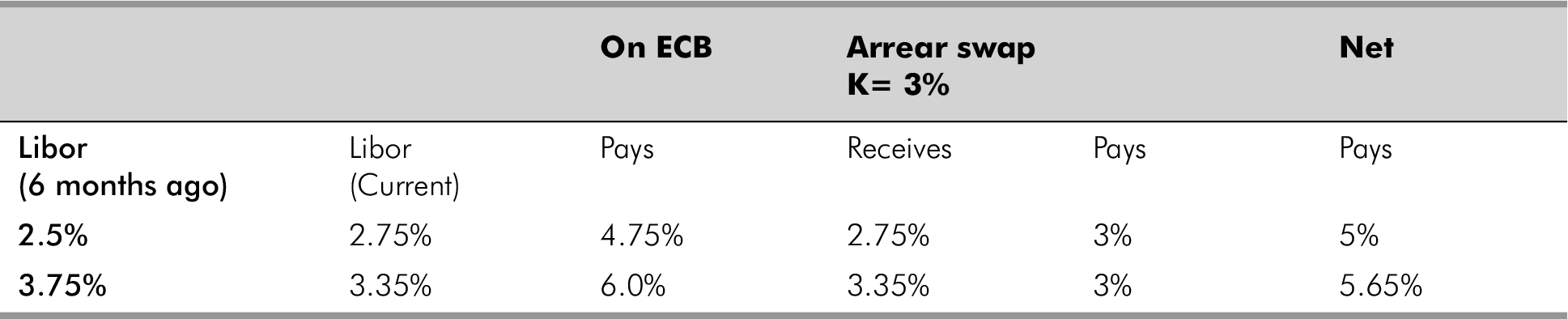

Arrear Swap

Strategy Term: Arrear Swaps

Strategy Description: It pays a fixed cash flow against a floating rate, but fixing is done at the end, simultaneously with the payment.

Strategy Application: The contract holder, who wants to hedge his interest rate risk, is of the view that USD Libor rates are going to increase sharply, even over a six months horizon.

In such a case, the contract holder can enter into an Arrear Swap.

There is a difference between this swap and a regular swap. In a regular interest rate swap, the fixing of interest rate on the fixed leg is done at the beginning of the tenor but in case of arrear swap, it is done at the end, simultaneously with the date on which the interest exchange happens.

Payoff: Swap with fixed rate K. Each payment date (t):

- Contract holder pays: K.

- Contract holder receives: Floating benchmark (t).

To clarify further, it is required to find cash flows as they would occur.

Pros

- If, within the reset interval, the floating benchmark rises by an amount which is more than the premium charged over a regular (fixed-in-advance) swap, the contract holder gains this differential over a regular swap.

Risks Involved

- If the interest rates fall, the contract holder still has to pay the same fixed rate.

- If within the reset interval, the floating benchmark falls, then the contract holder will receive the current fixing and pay the previous fixing on his payable. Effectively, he will have to meet the difference on his own.

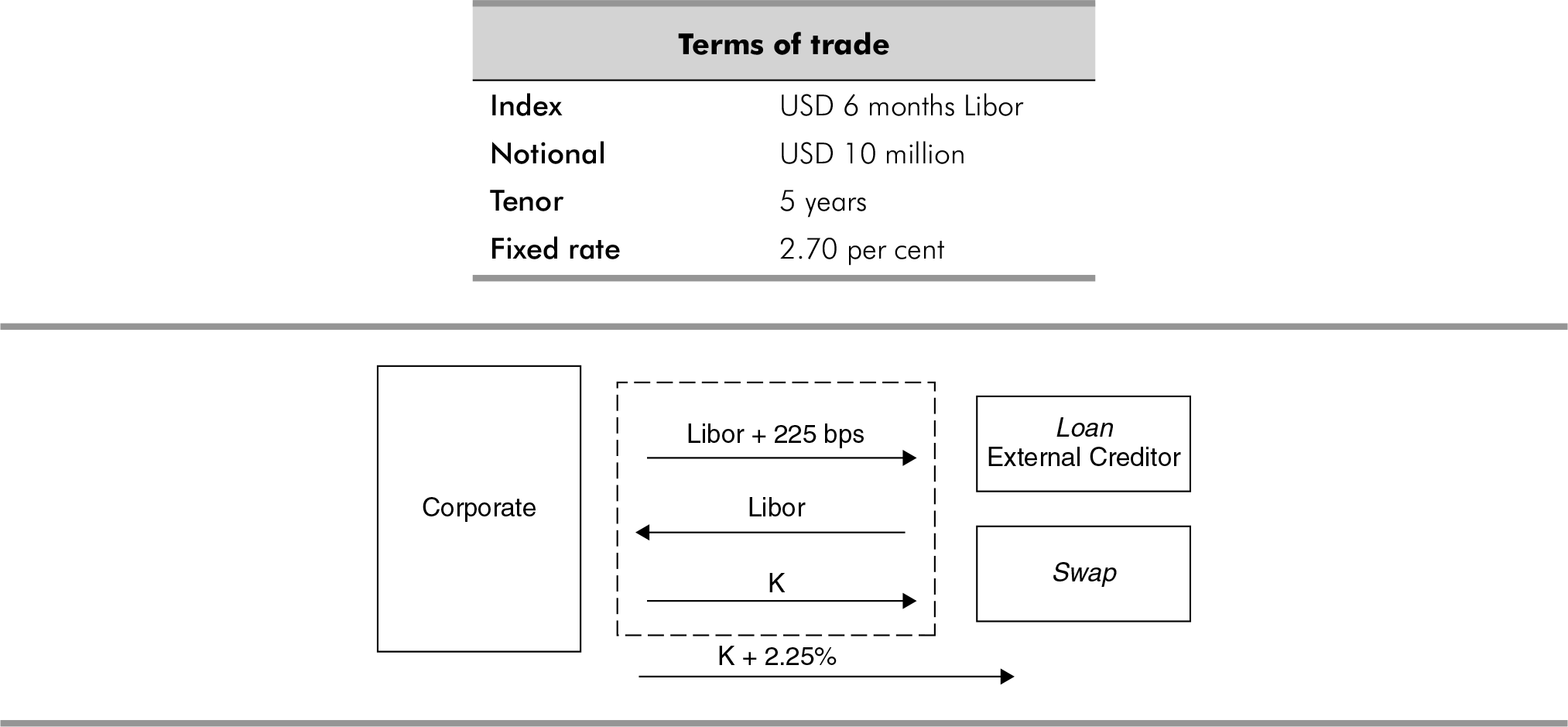

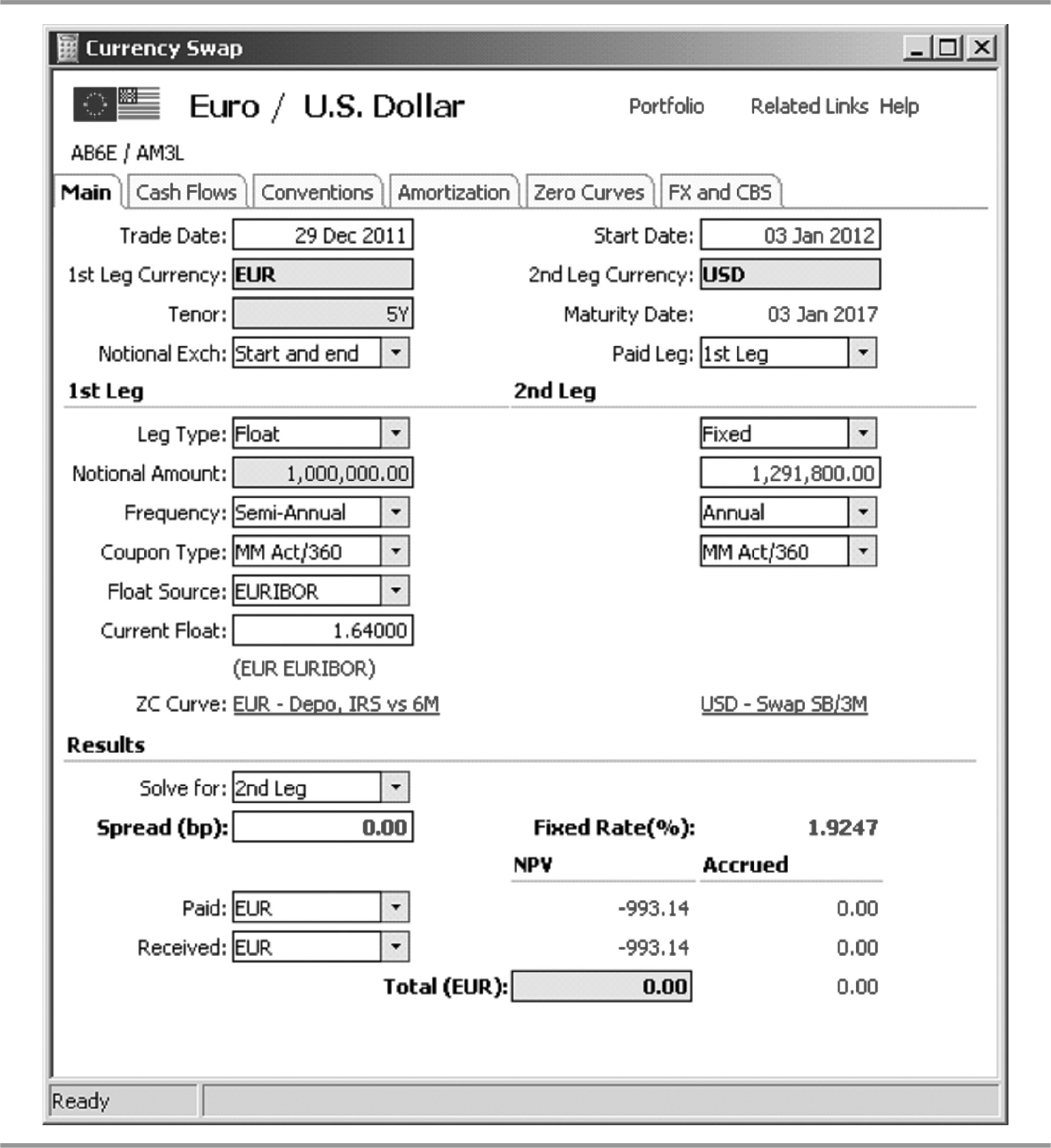

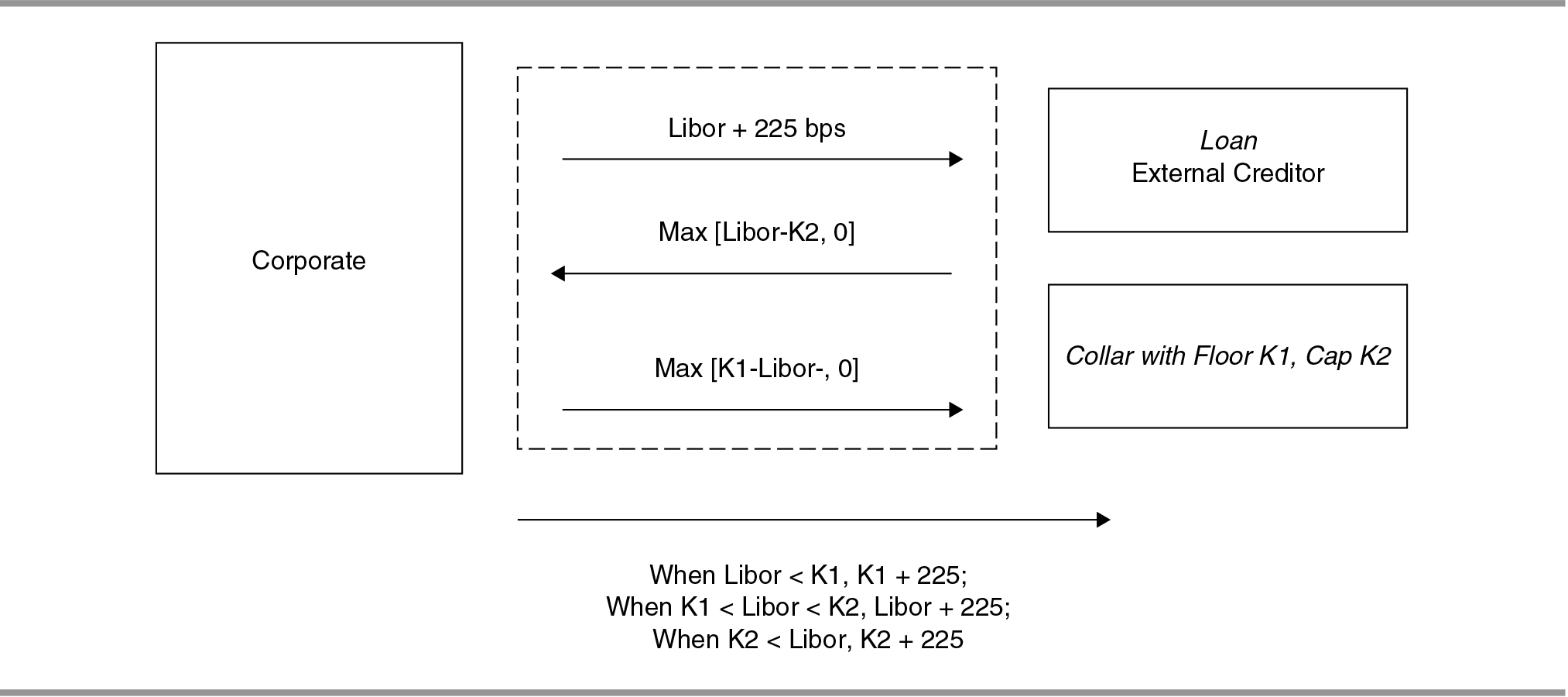

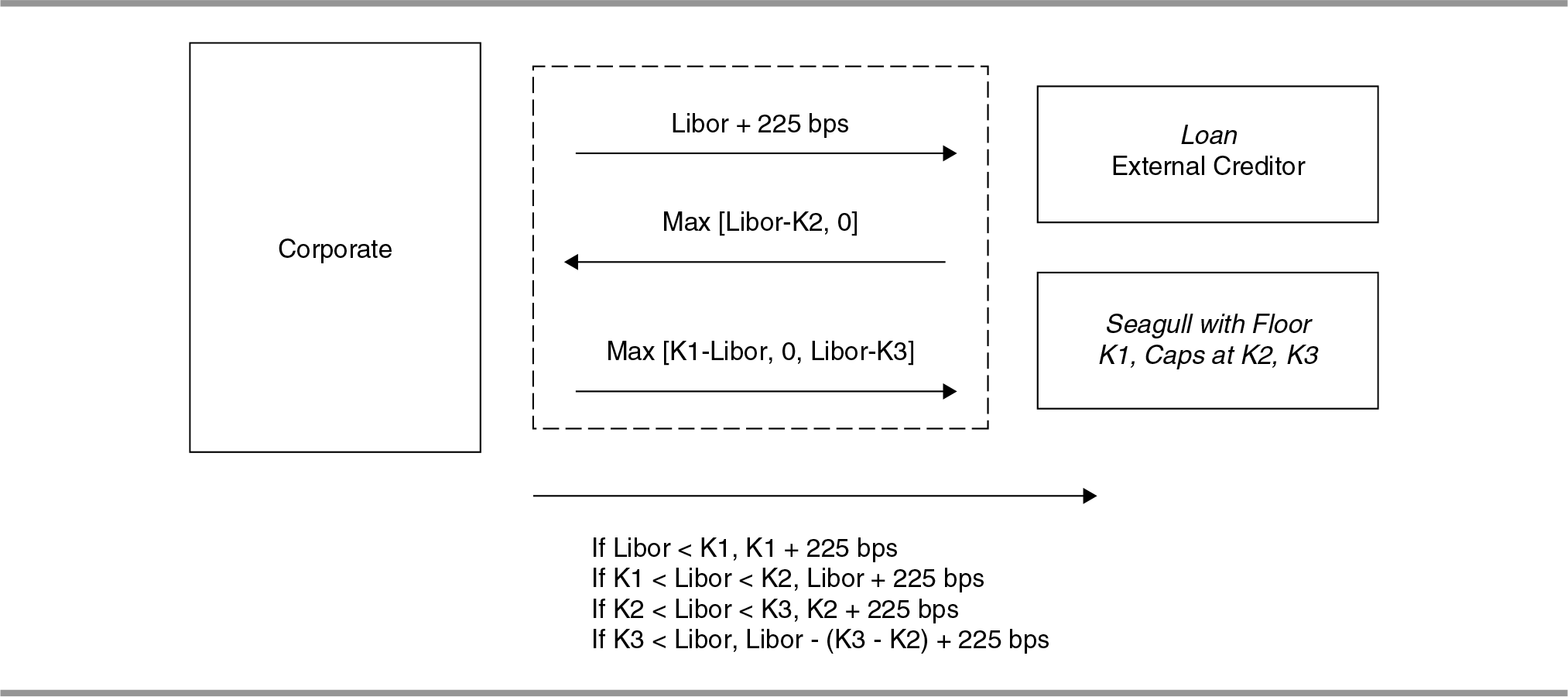

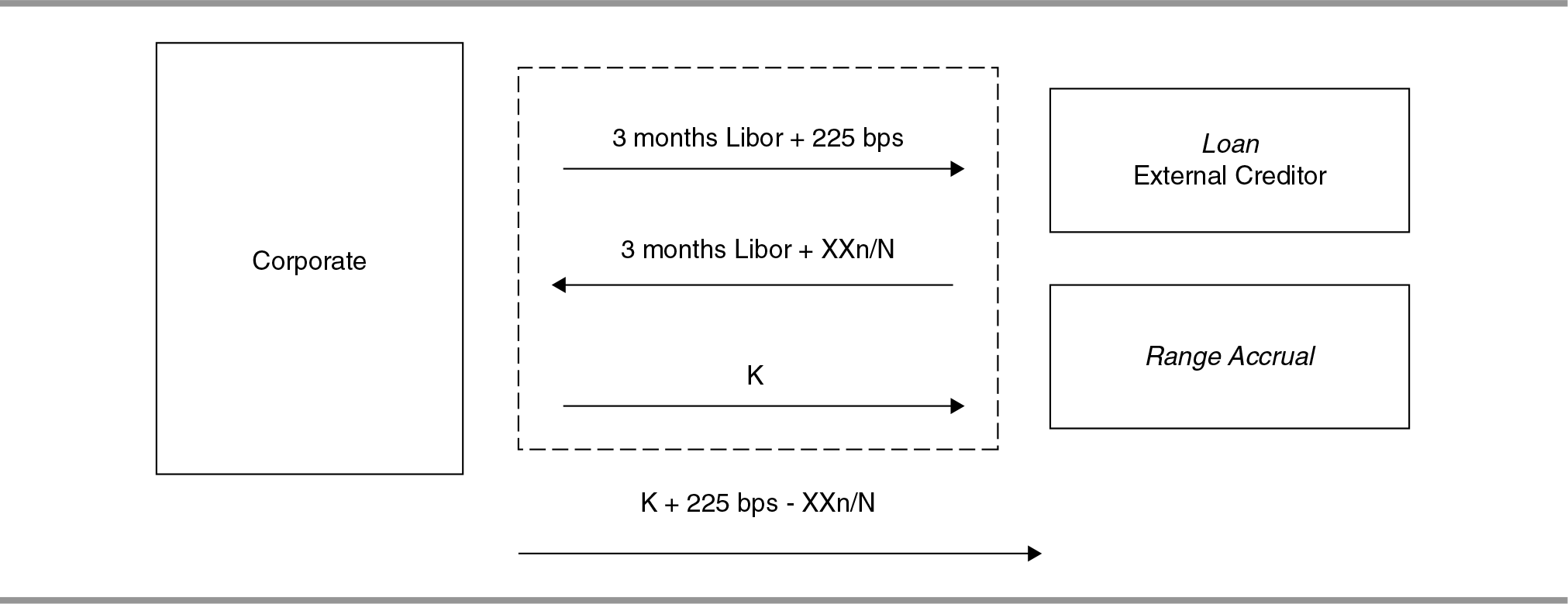

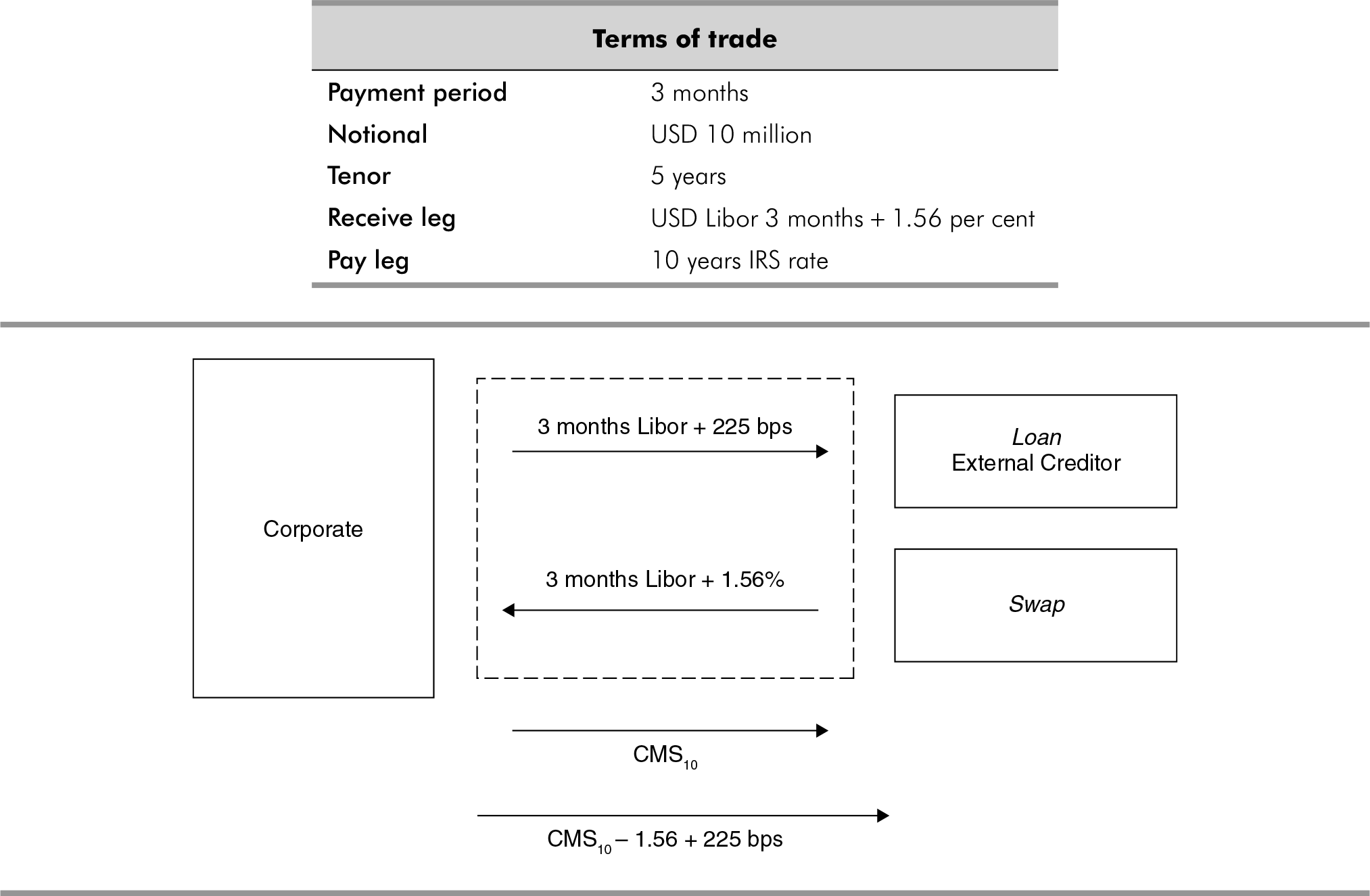

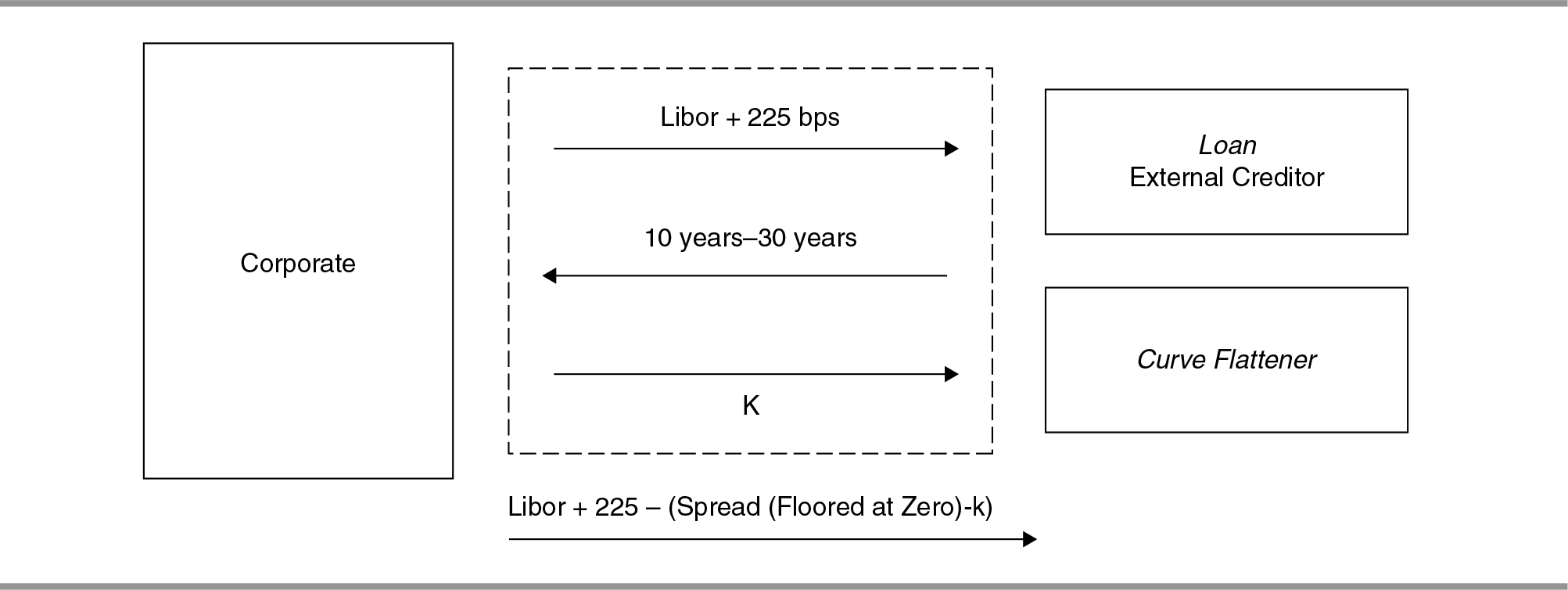

Full Currency Swap

Strategy Term: Full Currency Swap

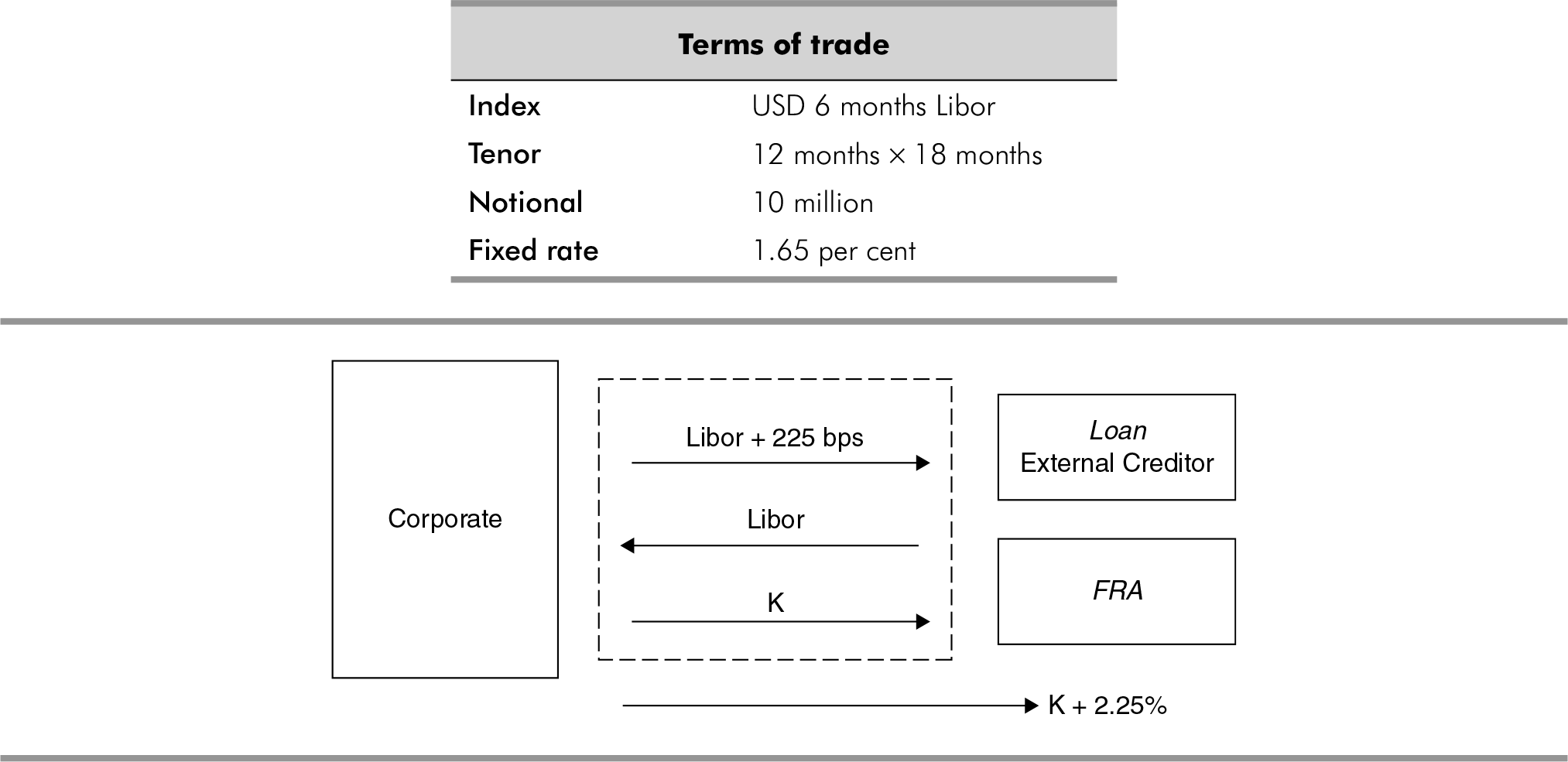

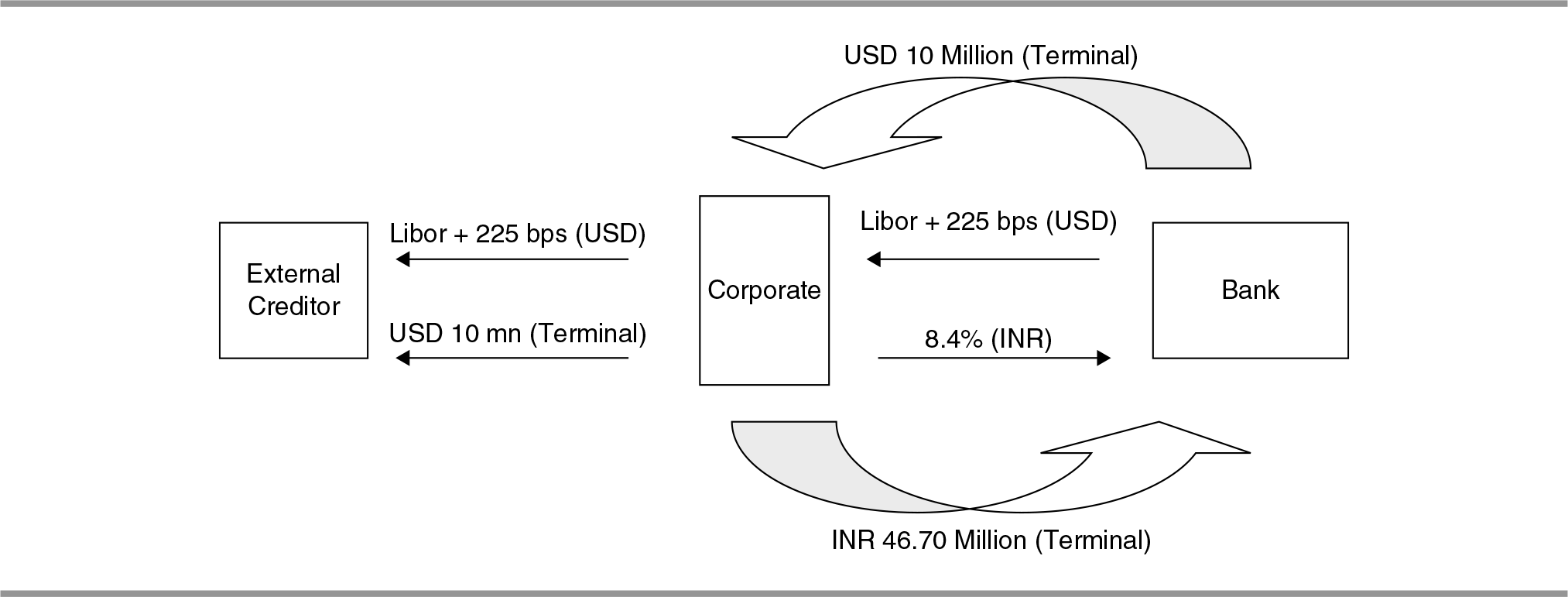

Strategy Description: It is an agreement in which two parties exchange specific amounts of different currencies initially (optional), and a series of interest payments on the initial cash flows, followed by exchanging the principal amounts back on maturity. The instrument enables hedging against both interest rate risk and currency risk on both interest and principal.

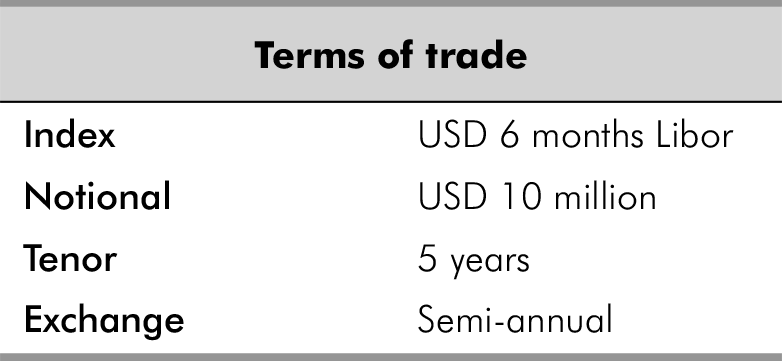

Screenshot 8.4 Currency Swap Calculator

Strategy Application: If the contract holder wants to convert his liability including coupon from foreign currency (FCY) to local currency (LCY) or vice versa, then he can enter into a Full Currency Swap.

In a currency swap, the initial exchange of currency may or may not take place but the interest rate will be exchanged on the outstanding notional.

At maturity, the principal amount will be exchanged.

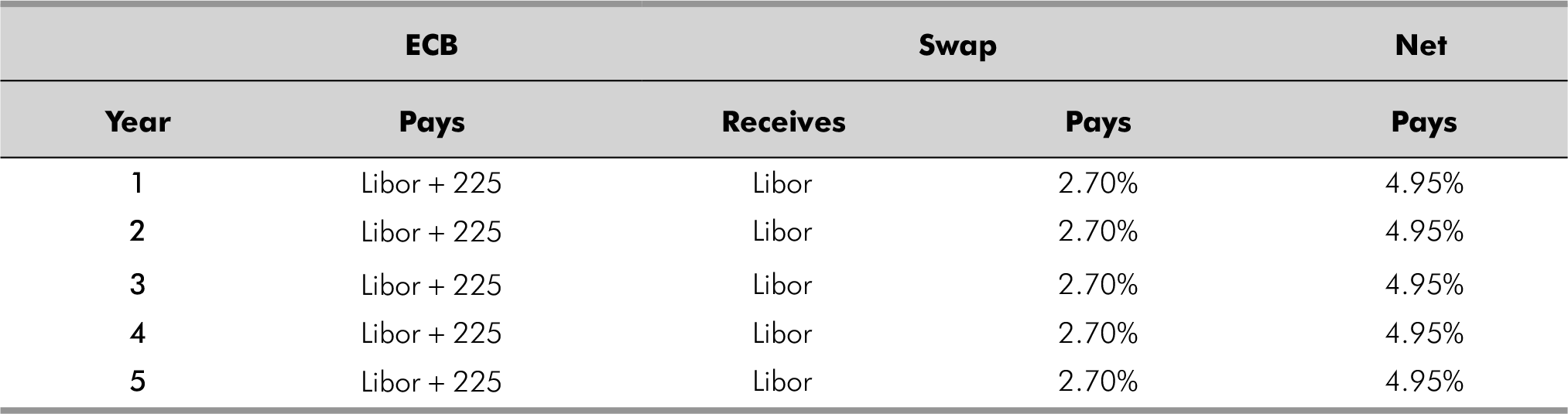

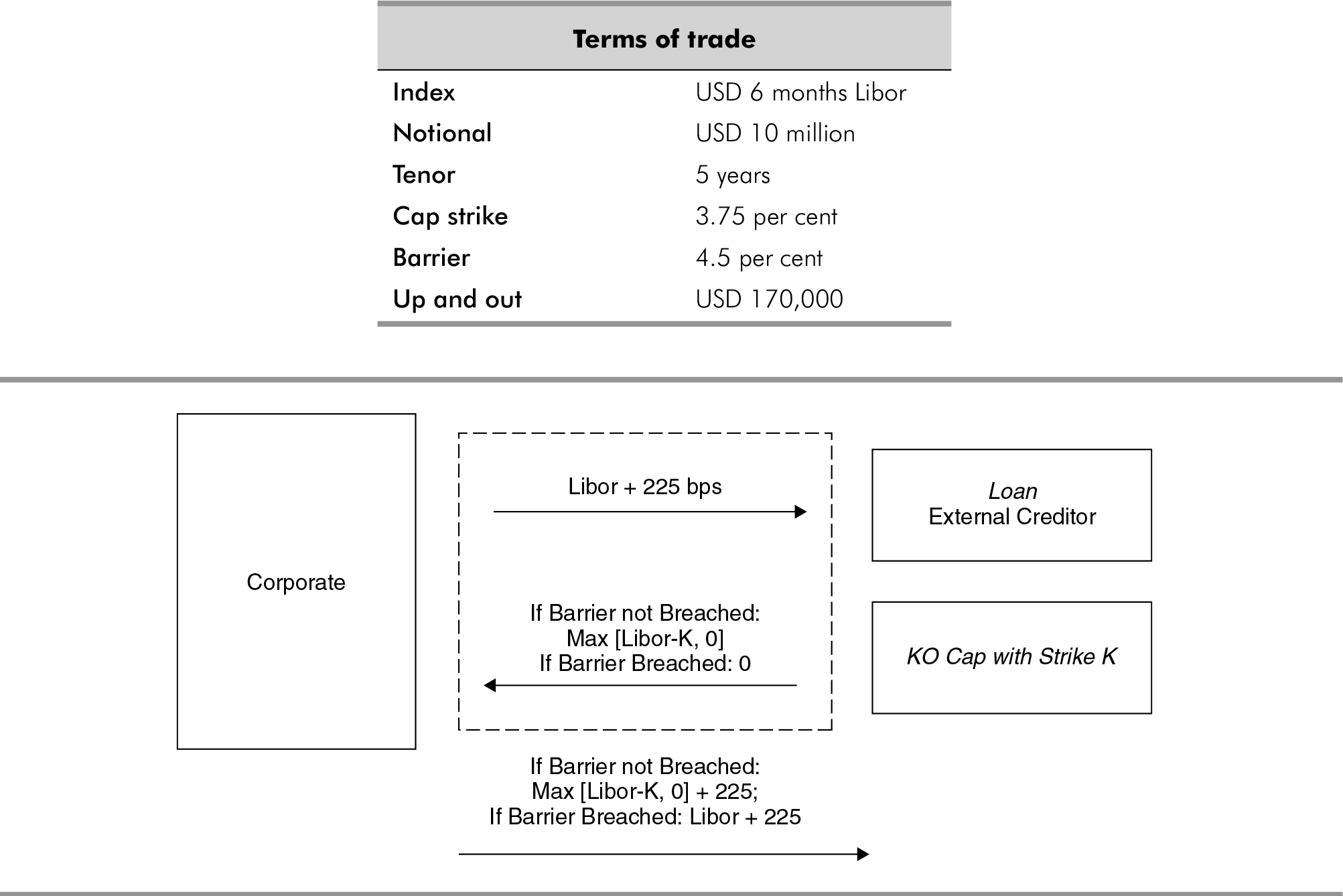

In the following example, the counterparty hedges currency and interest rate risk on FCY (USD) liability into LCY (INR). The same product can be used to transform currency and interest rate risk into any other currency and interest rate benchmark.

At each payment date, the counterparty receives Libor + 225 bps from the bank in USD, which it pays to the external creditor. Also, it is an obligation to pay a fixed rate in INR on INR notional.

It also receives USD 10 million at the end of each year (amortizing loan), in return of which it pays INR at a pre-determined rate.

- Contract holder receives: USD six months Libor + x per cent in USD.

- Contract holder pays: K per cent in INR.

On maturity,

Receive USD notional

Pay INR

Pros

- Contract holder can use a full currency swap to transform currency and interest rate liability.

- The contract holder is also protected against an appreciation in the currency in which the debt is denominated.

Risks Involved

- If interest rates fall, the corporate still has to pay the same fixed rate.

- The corporate also does not get to participate in the upside, if the currency in which the debt is denominated depreciates.

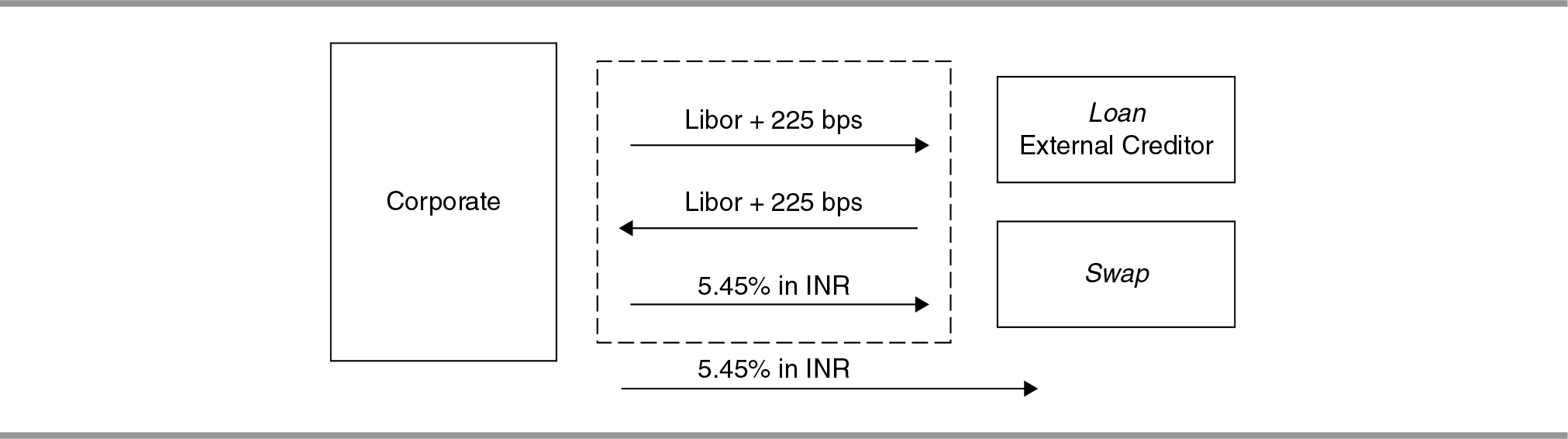

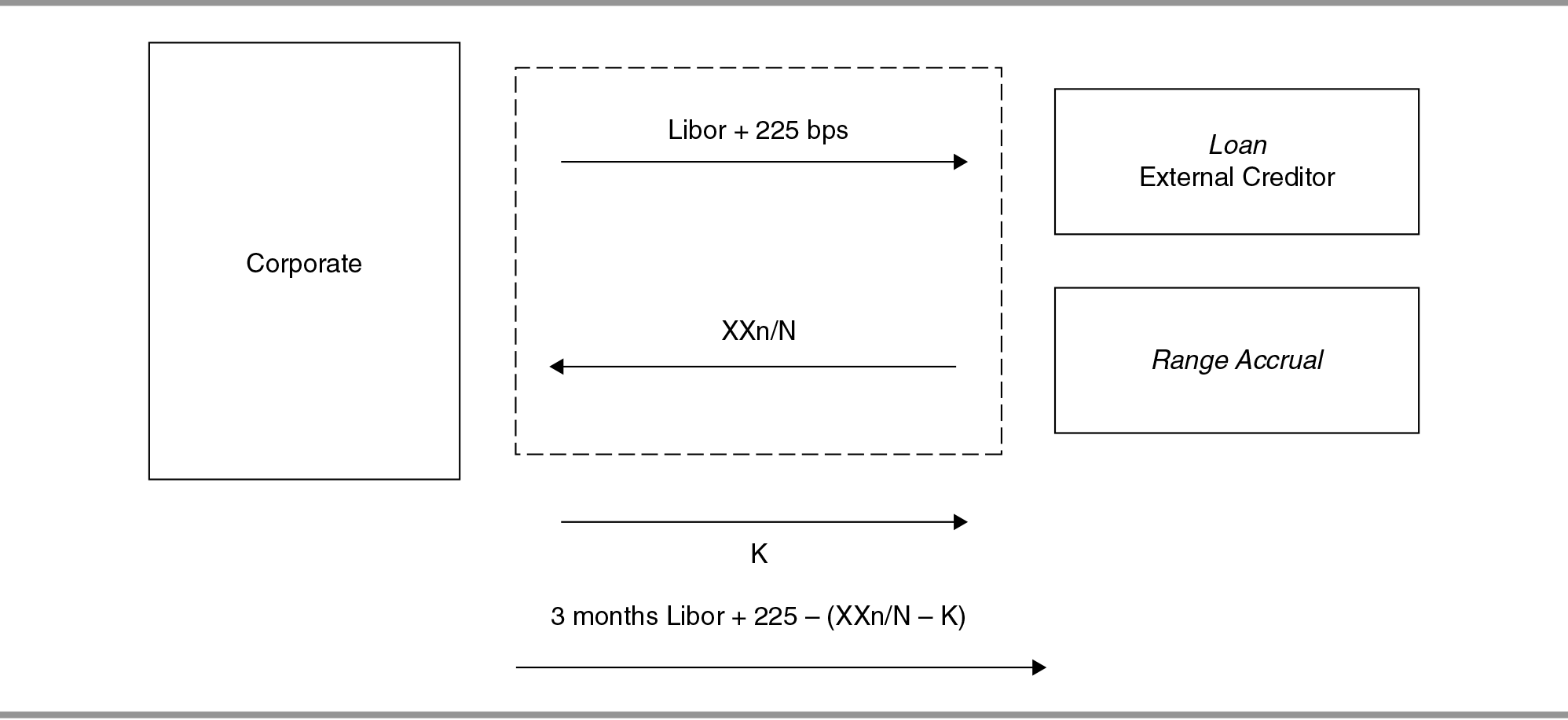

Coupon Only Swap

Strategy Term: Coupon Only Swap

Strategy Description: It refers to a swap where only the interest rate on the notional amount is exchanged between the counterparties, leaving principal untouched. Through a coupon only swap, interest rate risk and currency risk on the coupon are hedged.

Examples

- The counterparty seeks to remove the interest rate risk as well as the currency risk on the coupon payable. In such a case, the contract holder can enter into a coupon only swap.

- In the below swap, stream of USD Libor interest payment is exchanged with INR payments at a fixed (or floating) rate on an equivalent INR notional.

At each payment date, the contract holder receives Libor + 225 bps from the bank in USD, which it pays to the external creditor. In return, the contract holder has to pay a fixed rate in INR.

- Contract holder pays: K (INR)

- Contract holder receives: USD six months Libor + x per cent in USD

Pros

- The contract holder hedges all his interest rate risks and currency risks on coupon payment.

- The contract holder is protected against a rise in Libor and also against an appreciation of the dollar when he makes his coupon payments.

Risks Involved

- If interest rates fall, the contract holder still has to pay the same fixed rate.

- If INR appreciates against USD, the contract holder cannot benefit on the lower (rupee equivalent) coupon payments.

INTEREST RATE OPTIONS

Interest rate options give the contract holder an extra degree of freedom to incorporate views he might have on interest rate movements while hedging their exposures. Through judicious combination of caps and floors, protection can be obtained with significant cost reduction.

Interest rate options include caps and floors. Knock-Ins and knock-Outs provide even more flexibility to the hedger to cover his interest rate risk, at a price much lower than he would have to pay for outright protection in the form of a cap.

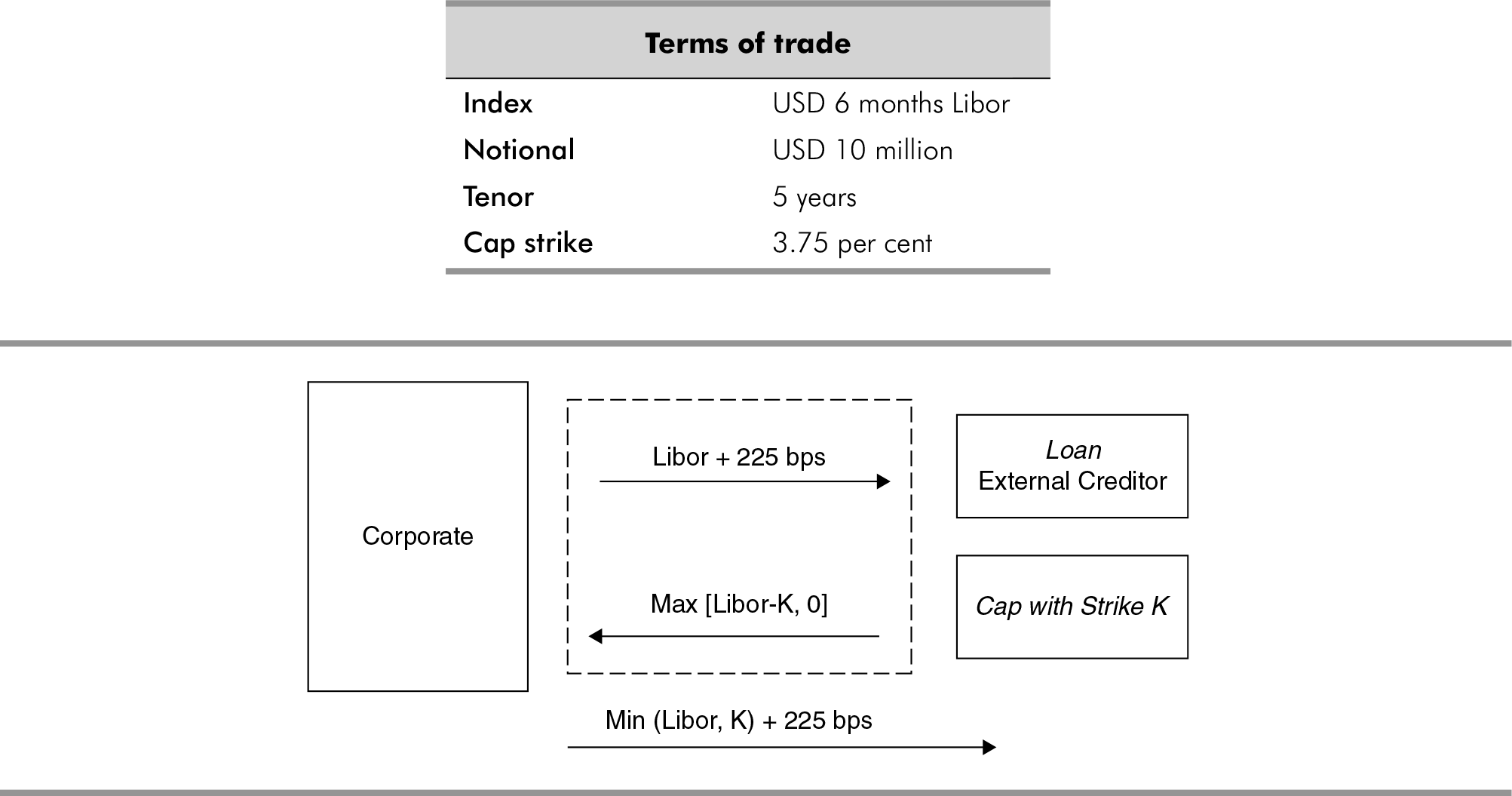

Interest Rate Cap

Strategy Term: Interest Rate Cap

Strategy Description: An option that provides a payoff when the specified rate is above a certain level (strike).

It enforces an upper limit on the floating rate payment and the risk of higher interest rates is crystallized into a single payment to be made upfront, without sacrificing downside risk.

Screenshot 8.5 Interest Rate Cap Calculator

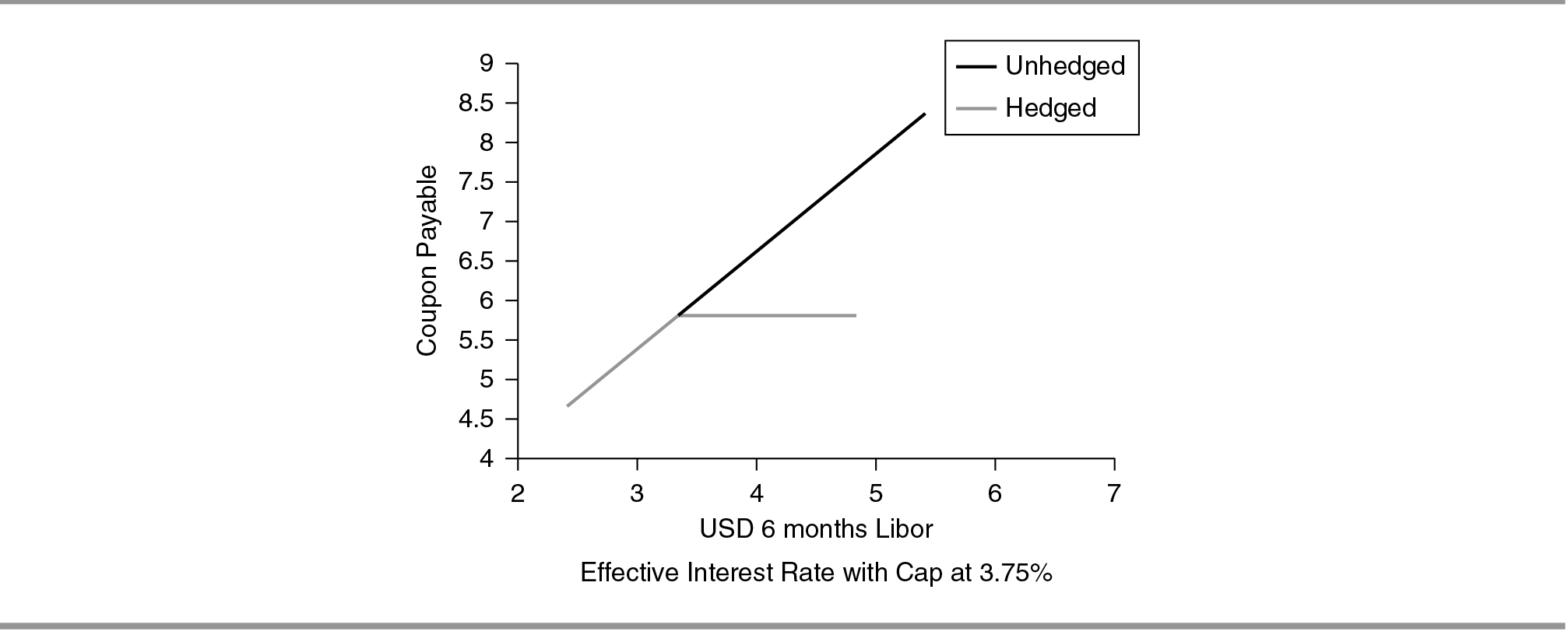

Strategy Application: The contract holder with floating rate linked USD liabilities believes that US Libor rates will fall. So, he does not want to give up his potential upside, but he wants to be hedged against an unexpected hardening of interest rates.

In such a case, the contract holder can buy an Interest Rate Cap, with strike at a level beyond which contract holder seeks protection. Each time the floating rate coupon is to be paid by contract holder on his USD liabilities, the cap will compensate for any interest payment above the strike level of the cap. This means that the contract holder’s floating interest rate is capped at the strike level, in addition to the constant spread (agreed with lender) that he has to pay over Libor.

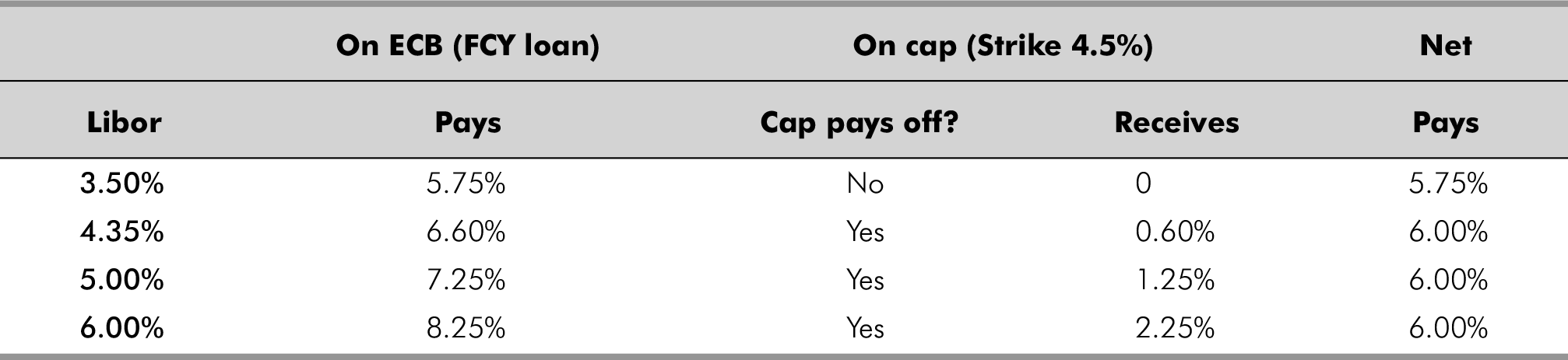

Payoff: Cap with strike K. Each payment period:

Floating benchmark ≤ K: 0.

Floating benchmark > K: then (Floating benchmark − K).

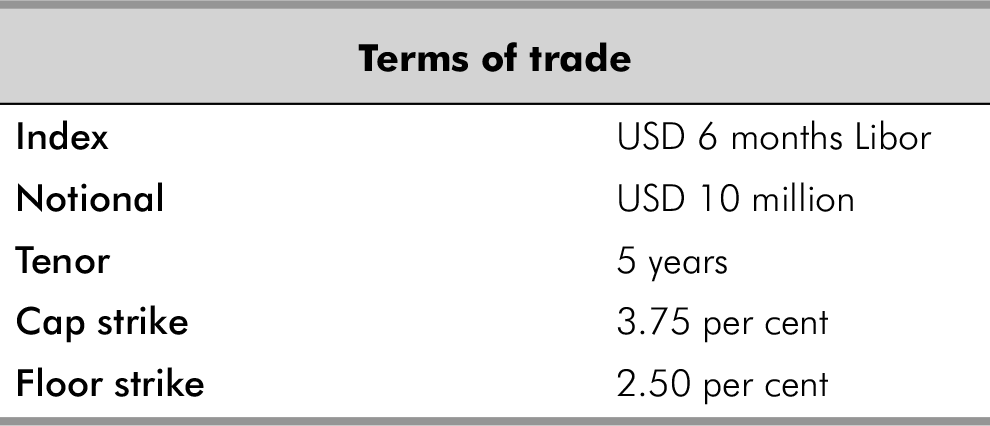

Example

Cap of strike 3.75 per cent.

Interest coupon is capped at 3.75 + 2.25 = 6.0 per cent.

To clarify further, refer to below mentioned scenario analysis:

Thus, the interest rate risk is mitigated without sacrificing any of the potential upside.

Pros

- The contract holder is fully protected in case interest rates go above the strike rate.

- The contract holder gets full participation in case interest rates (Libor) move lower.

Risks Involved

- If the interest rates fall, the buyer of cap stands to lose premium and cap seller is open to interest rate movements.

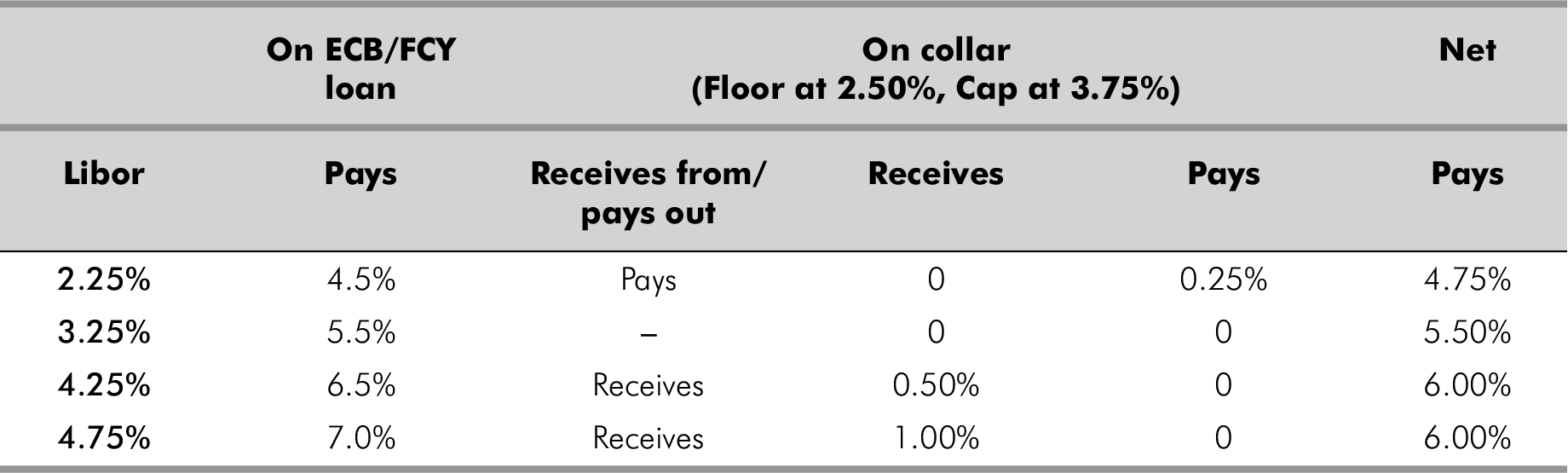

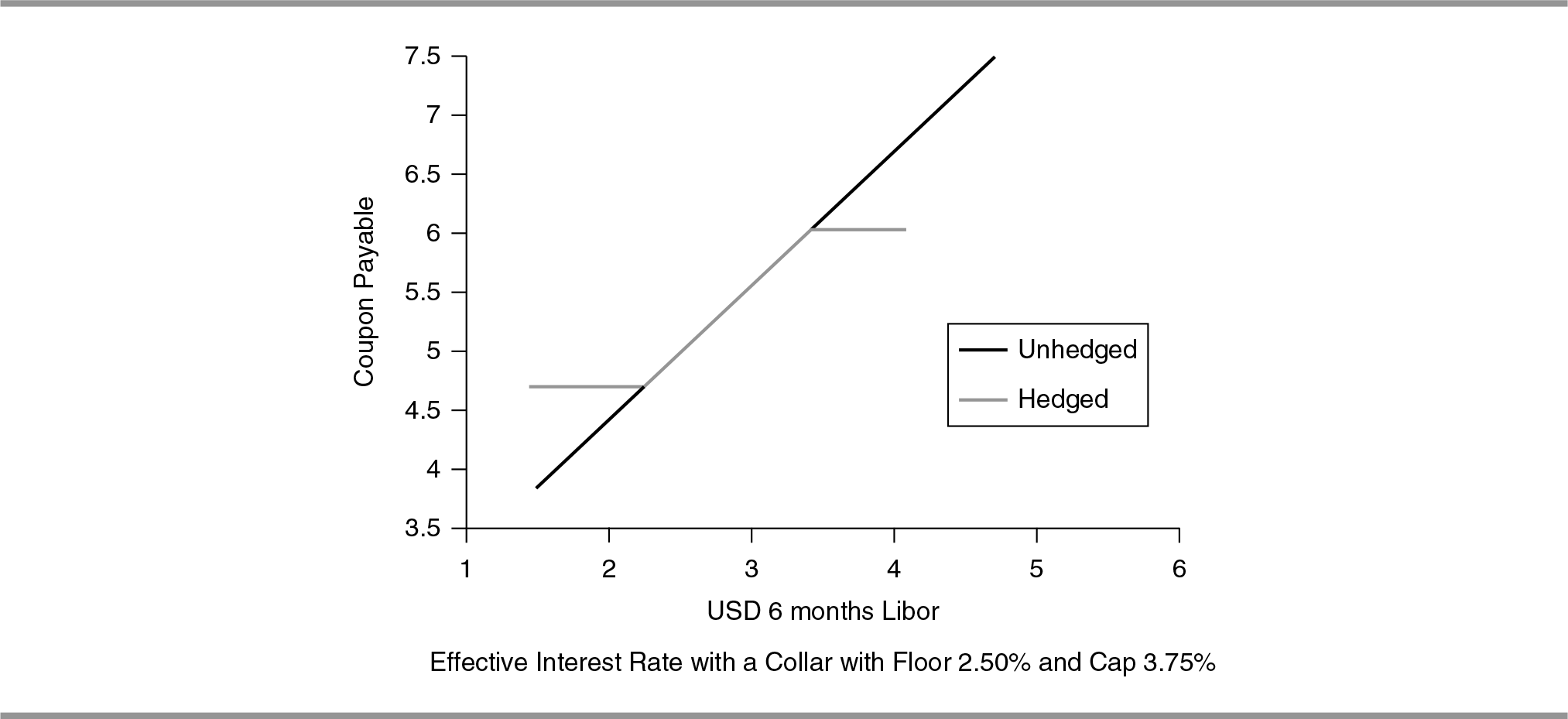

Collar

Strategy Term: Collar

Strategy Description: Collar is a combination of the interest rate cap and the interest rate floor. It keeps the floating payment bound within a range. The contract holder buys a cap and reduces the premium he has to pay by selling a floor, effectively exchanging potential gains from lower rates for protection against losses from a hardening rate scenario.

Hedges Against: Interest Rate Risk

Example

In this case, the contract holder wants to protect the balance sheet from hardening interest rates by buying a cap, but does not want to pay the entire premium. He believes that a sharp fall in interest rates is unlikely. So he is willing to give up some of his potential upside to reduce the premium payable. Therefore, the contract holder enters into an Interest Rate Collar with floor at the minimum interest level and cap at the maximum interest level he wants to pay.

Each time the floating coupon payable exceeds the cap level, the product will payoff the excess interest over the cap level; but each time the floating coupon falls below the floor level, the contract holder will have to pay the shortfall. This, when coupled with the floating rate payments on the USD Liability means that the contract holder’s interest payments will lie within a fixed range.

Payoff: Collar with Floor K1, Cap K2. Each payment period:

Floating benchmark < K1: Contract holder pays (K1-Floating benchmark).

K1 ≤ Floating benchmark ≤ K2: 0.

K2 < Floating benchmark: Contract holder receives (Floating benchmark-K2).

Consider a collar with a floor of 2.50 per cent and a cap of 3.75 per cent. Here, the interest coupon is floored at 2.50 + 2.25 = 4.75 per cent, and capped at 3.75 + 2.25 = 6.00 per cent.

Graph 8.4

Pros

- Even if the interest rates rise, the interest rate payable is limited to the cap level.

- The contract holder gets to enjoy more upside than a regular swap if the interest rates fall.

Risks Involved

- Even if USD Libor falls below the floor rate, the contract holder cannot enjoy the full benefit of the upside.

- When rates increase, the contract holder faces more risk than in case of a simple Interest rate swap.

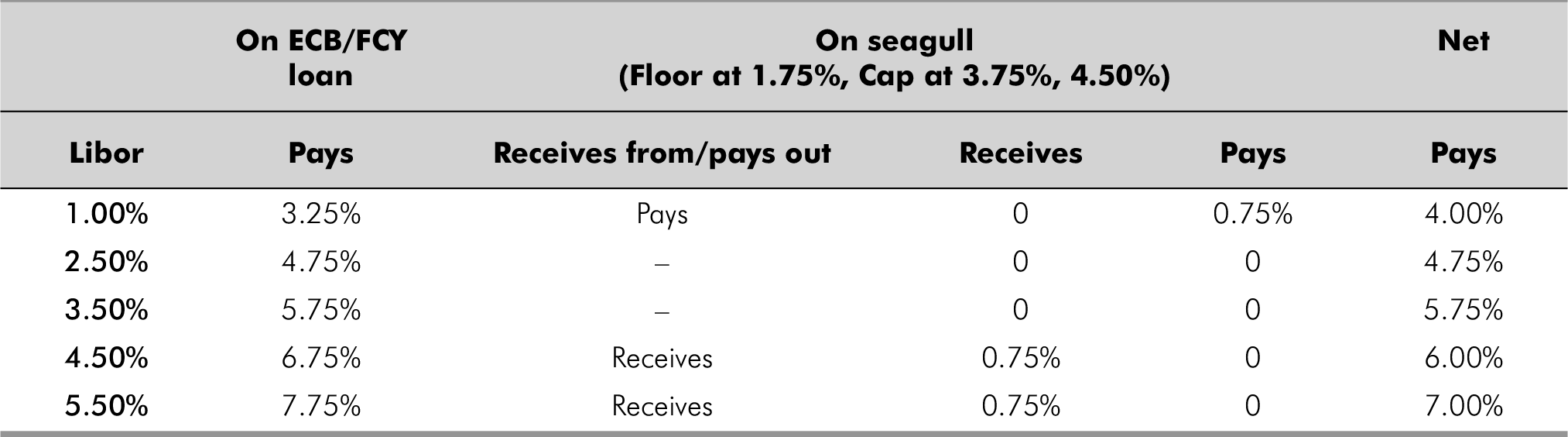

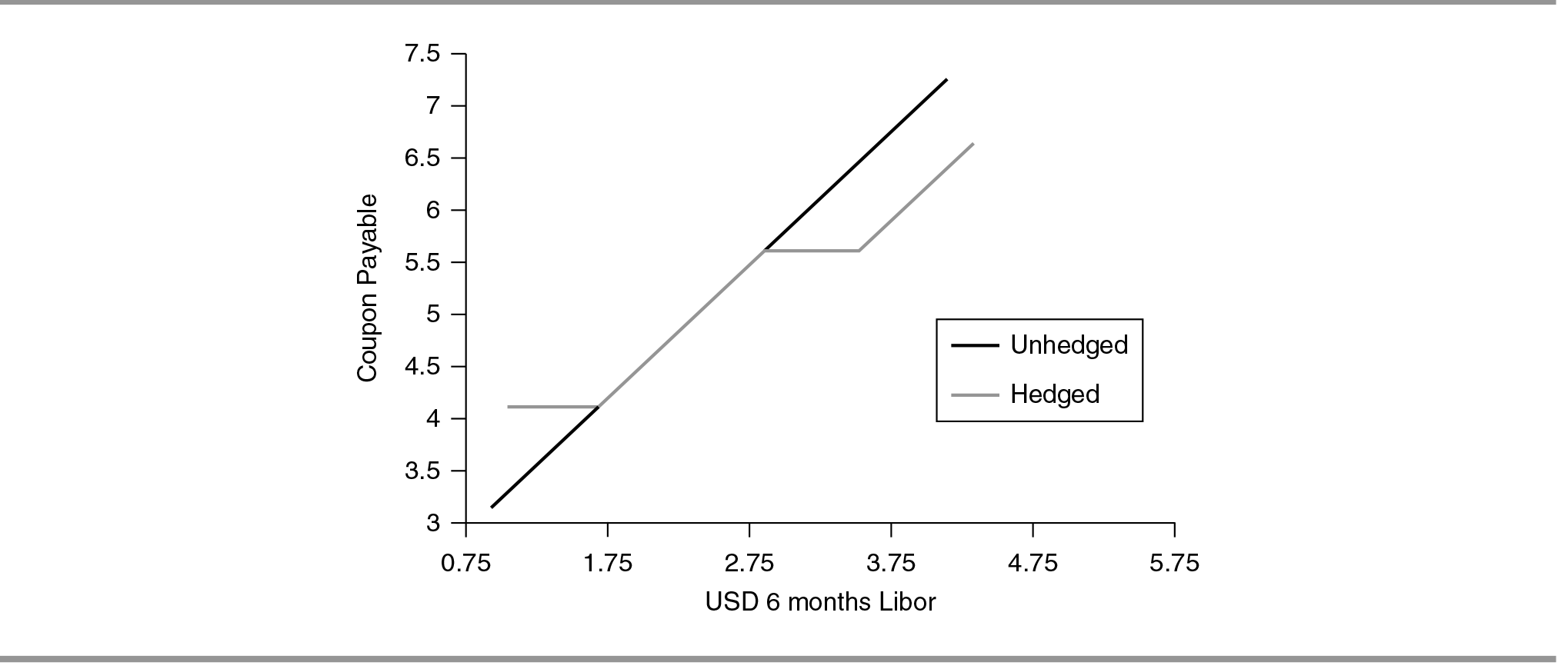

Seagull

Strategy Term: Seagull

Strategy Description: It keeps a floating coupon within a range up to certain level, after which it starts to increase. The contract holder sells two deep out of the money interest rate options—a cap and a floor—and buys a single cap which is relatively less out of the money.

Strategy Application: In this case, the contract holder once again wants to protect the balance sheet from hardening interest rates, but he does not want to make large upfront payment, he does not expect a large move in rates. So, he is willing to take risk of sharp rate increase above some level, and is also willing to give up the upside of a sudden fall in rates. In exchange, he wants protection against small up moves, while being allowed to participate in small down moves in interest rates.

In this case, the contract holder can enter into a Seagull, which offers a better floor at the first cap level than a normal collar. However, the contract holder has to take some of the downside on account of an increase in Libor above the second cap level.

Payoff: Seagull with floor K1, cap K2, cap K3. Each payment period:

Floating benchmark< K1: Contract holder pays (K1–Floating benchmark).

K1 ≤ Floating benchmark≤ K2: 0.

K2 ≤ Floating benchmark≤ K3: Contract holder receives (Floating benchmark–K2).

Libor > K3: Contract holder receives (K3–K2).

Consider a seagull with a floor of 1.75 per cent and a cap of 3.75 per cent and 4.50 per cent

Pros

- Offers a better floor rate and a cap rate than a normal collar, till Libor is below the higher strike cap.

Risks Involved

- Even if USD Libor falls below the floor rate, the contract holder cannot participate fully in the down-move.

- The coupon payable keeps increasing as Libor increases above the upper strike cap, though his rate is still better than an un-hedged rate.

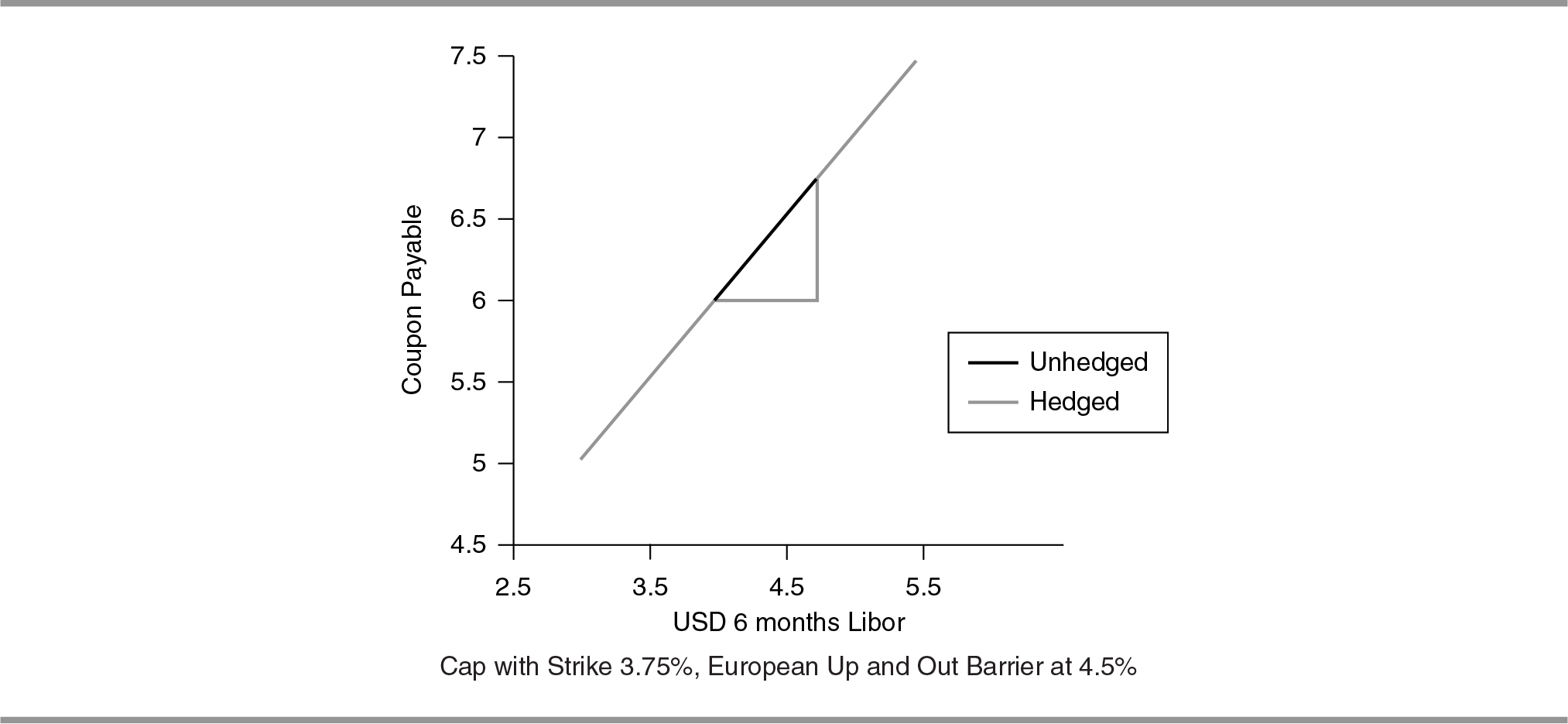

European Knock-Out Cap

Strategy Term: European Knock-Out Cap

Strategy Description: It enforces an upper limit on the floating coupon paid, subject to a maximum or minimum level of floating index rate. The contract holder saves on premium paid by giving up some part of the protection offered by a regular cap.

Strategy Application: The contract holder believes that there is a good chance that US Libor rates will fall, and so he does not want to give up his possible upside; but he wants to be protected from an unexpected hardening of rates. However, he has a view on the range of interest rates he needs protection from; either steep or softer interest rate hikes. He does not want to pay for protection against the scenario which he thinks is not likely to occur.

The contract holder buys an Interest Rate Cap, but can give up the protection he does not believe he needs, by putting in a Knock-Out barrier. The Knock-Out is the level on the benchmark that, if reached, cancels the protection for that month.

There are two types of Knock-Outs:

- Up and Out: In an up and out, the cap ceases to exist if the interest rates go up above the barrier level. This gives protection against hardening of rates up to the barrier level.

- Down and Out: In a down and out, the cap ceases to exist if the interest rates are below the barrier level. This gives protection when interest rates rise above the barrier level.

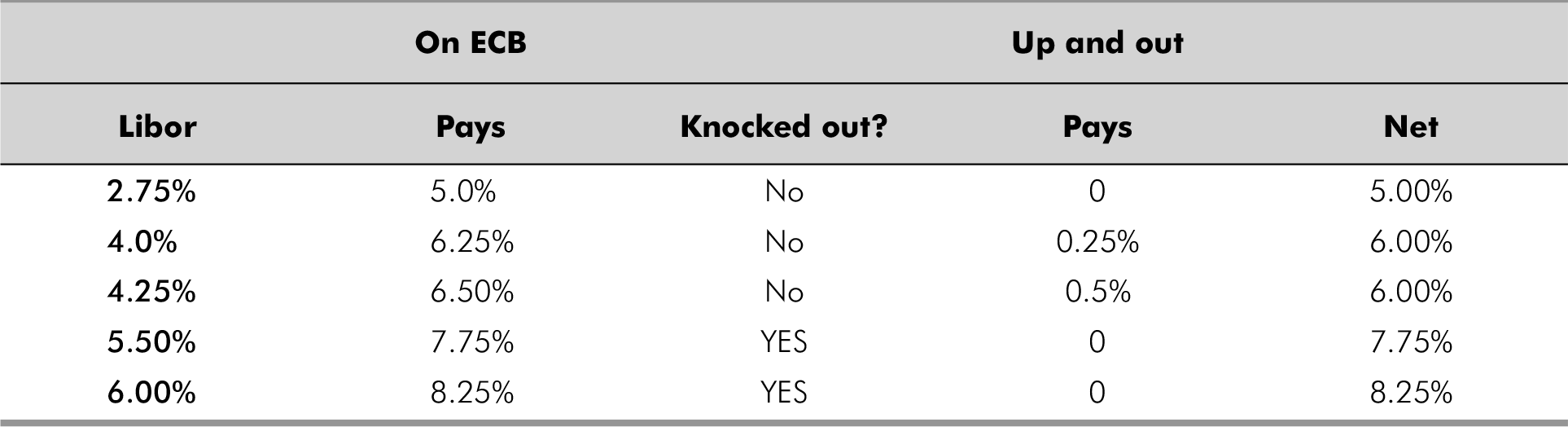

Payoff: Cap with strike K, Knock-Out B. Each payment period:

If barrier not breached:

Libor ≤ K: 0.

Libor > K: (Libor – K).

If barrier breached: 0.

As an example, take a cap of strike 3.75 per cent and a barrier at 4.5 per cent.

Pros

- The contract holder is protected in case interest rates go up above the strike rate, in the expected range (below barrier for up and out, above barrier for down and out).

- Premium payable is lower than a simple interest rate cap.

The contract holder participates in the entire down-move, in case interest rates move lower.

Risks Involved

- If interest rates rise outside the expected range (i.e. rise above the barrier for up and out, below barrier for down and out), the contract holder will find himself without protection.

Knock-Ins and Knock-Outs

Just as you can have an option that gets cancelled above or below a particular level (up-and-out and down-and-out, respectively), you can also have options that go live at predefined levels. Such options are called Knock-Ins.

In European barriers, where the level is observed only on the last day, this distinction need not be made, since a down-and-out is the same as an up-and-in, while an up-and-out is identical to a down-and-in.

There is, however, another type of barrier, called American barrier. In this, the option is Knocked-Out/Knocked-In if the observed parameter hits the barrier at any point during the life of the option.

In such options, the distinction between Knock-Ins and Knock-Outs needs to be made. Such barriers are often used in currency options. American Knock-Ins, naturally, are more expensive, while American Knock-Outs are cheaper than their European counterparts, because of the increased likelihood of the barrier being hit.

RANGE ACCRUALS

A range accrual is a product, where the payout is proportional to the number of days in the observation period where the index floating rate lies within a specified range.

Extra coupon depends upon n/N, where n is number of days, the observed rate lies within the specified range and N is total number of days in the observation period.

A number of variations of range accruals are possible, some of them are discussed further. Though a complete list of all possibilities is repetitive, a few common examples are also discussed in detail.

Variations

- Varying range: When the product maturity consists of a number of years, it can be structured for varying ranges over the different years. Thus, even if the contract holder’s view on the floating range becomes less and less narrow as for longer horizons, the ranges can be appropriately increased for later years. This is an extremely common variation among all types of range accruals.

- Receive/pay continuous: The contract holder can either receive when the rate lies within the range, or pay when the rate lies within the range. Both of them have their own uses, based on the contract holder’s requirements and preferences.

- Range on fixed/range on floating: Even though the observed rate has to be a floating rate, the premium paid can be the appropriate fraction of a fixed rate or the floating rate itself.

Floating to Fixed Range Accrual

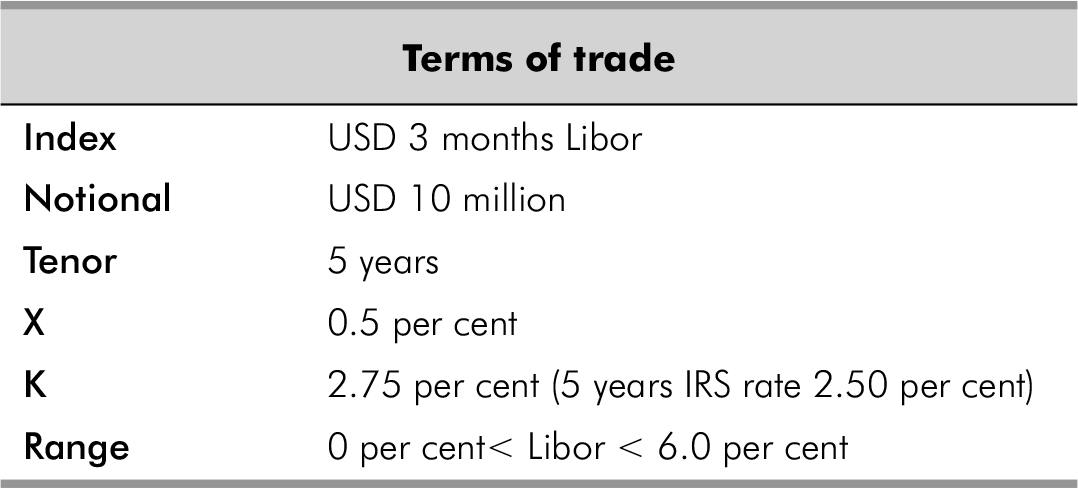

Strategy Term: Floating to Fixed Range Accrual

Strategy Description: Here the contract holder pays a fixed rate which is higher than the swap rate; in exchange, the contract holder receives the floating benchmark with or without an additional payoff, which is proportional to the number of days the floating rate index fixes within a specific range.

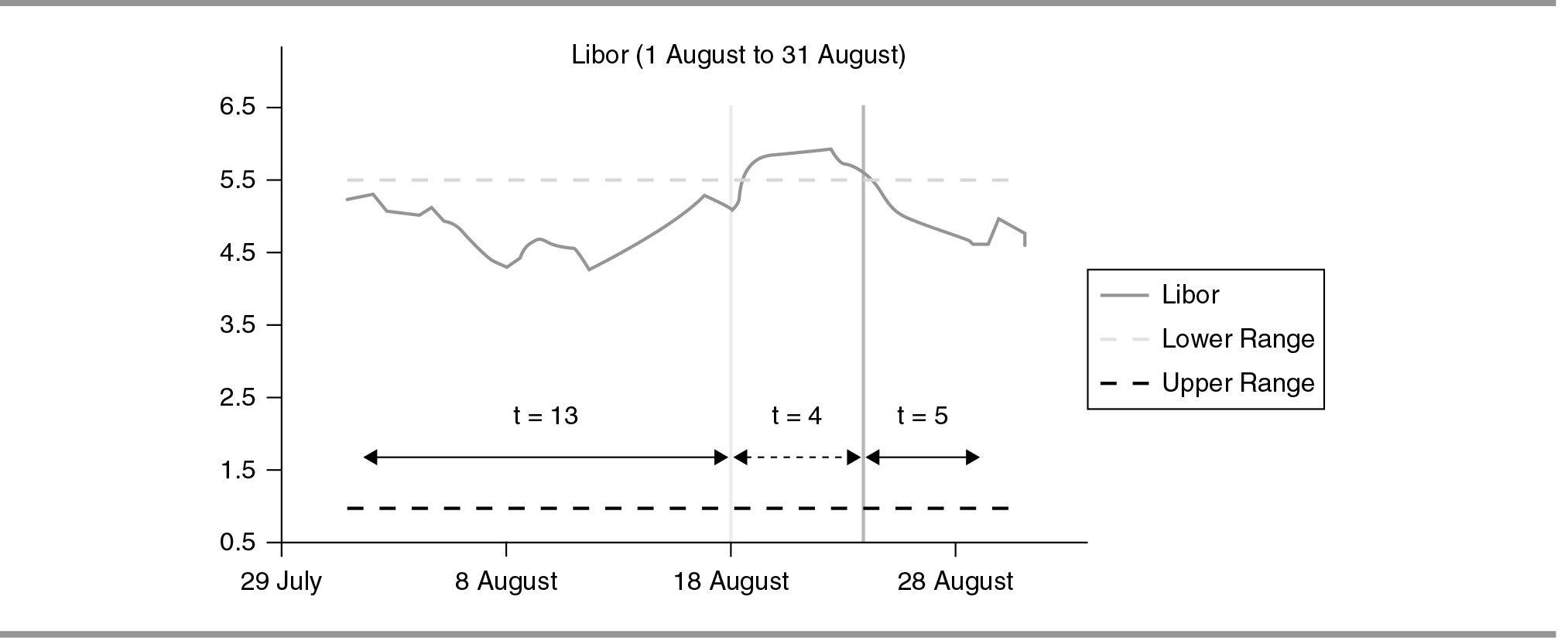

Strategy Application: Here again, the contract holder wants to change his floating liability into a fixed one because he is not sure about the direction of the Libor movement; however, he believes that Libor will stay between 0 per cent and 6 per cent for the entire duration of the loan.

The contract holder can participate in a Range Accrual where the contract holder pays a constant fixed rate, and receives three months Libor, plus a premium for each day the rate stays above 0 per cent but below 6 per cent.

In the below example, the maximum premium is 0.5 per cent, and the constant rate is 2.75 per cent.

Payoff: Each payment period:

- Contract holder pays: K.

- Contract holder receives: Floating benchmark + (XX (n/N)).

N: days in observation period.

n: days where rate is within range.

Variations: Floating to Fixed Range Accrual with Varying Ranges.

Usually, the range within which any rate can be expected to lie is narrower in the beginning of the life of the product, and it widens as the maturity increases.

In the example above, other things being same, the range may be changed to -

| Year 1: | Payoff if 0 < 3 months Libor < 4 |

| Year 2: | Payoff if 0 < 3 months Libor < 5 |

| Year 3–4: | Payoff if 2 < 3 months Libor < 6 |

| Year 5: | Payoff if 0 < 3 months Libor < 7 |

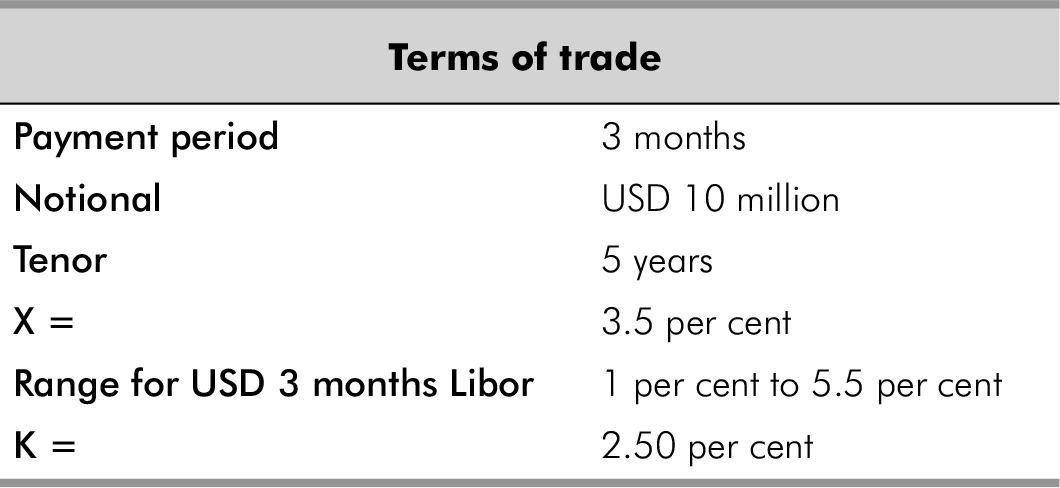

Fixed to Fixed Range Accrual

Strategy Term: Fixed to Fixed Range Accrual

Strategy Description: The contract holder pays a fixed rate continuously and receives another constant rate, but it is possible only on the days when the floating index rate lies within a range; on other days, he receives nothing.

Strategy Application: Again, the contract holder wants to keep his interest rate floating; but he wants a discount whenever US Libor lies within a range. This may be either because of a strong belief that Libor will lie within this range, or an expression of some qualitative relation that the business has to Libor.

In this case, the contract holder can participate in a Fixed-Fixed Range Accrual. The contract holder will have to constantly pay a fixed rate, but he will receive a fixed payment proportional to the number of days where three months Libor lies within the specified range of 1 per cent to 5.5 per cent.

Naturally, the payment on those days will be higher than the fixed leg he pays, to compensate for the fact that he will receive nothing when three months Libor is outside the range.

Payoff: Each payment period:

- Contract holder pays: K.

- Contract holder receives: X X (n/N).

N: days in observation period.

n: days where rate is within range.

X = 3.50 per cent

Total days: 22

Days in range: 18

Contract holder receives: XX(n/N) = 2.86 per cent

Contract holder pays: K = 2.50 per cent

So contract holder gains 36 basis points

Pros

- The contract holder can gain substantial savings on his interest payments if his views on the range are correct.

Risks Involved

- The contract holder, even if right in his views, is exposed to Libor rates going up.

- If for three months Libor goes outside the range, the contract holder receives nothing, but still he has to pay his fixed leg. So effectively, the contract holder pays an additional spread on his interest payments.

Variation (Wedding Cake): One variant which is possible is a structure, i.e., a combination of several range accruals, each paying off in a narrower range than the next. The net result is a payoff that steps up as the band within which the floating benchmark remains narrower.

Examples

Consider three range accruals:

- Contract holder pays a constant 3.5 per cent, and receives 5 per cent X(n1/N), where n is the number of days that the three months Libor remains between 2 per cent and 6 per cent.

- Contract holder pays a constant 1 per cent, and receives 3.5 per cent X(n2/N), where n is the number of days that the three months Libor remains between 3 per cent and 5 per cent.

- Contract holder pays a constant 0.25 per cent, and receives 2 per cent X(n3/N), where n is the number of days that the three months Libor remains between 3.75 per cent and 4.25 per cent.

The net result is that, each day the contract holder pays a constant fixed 4.75 per cent and receives a payoff of:

| 0 | if 6 months Libor =< 2 per cent |

| 5 per cent | if 2 per cent < 3 months Libor =< 3 per cent |

| 8.5 per cent | if 3 per cent < 3 months Libor =< 3.75 per cent |

| 10.5 per cent | if 3.75 per cent < 3 months Libor =< 4.25 per cent |

| 8.5 per cent | if 4.25 per cent < 3 months Libor =< 5 per cent |

| 5 per cent | if 5 per cent < 3 months Libor =< 6 per cent |

| 0 per cent | if 6 per cent < 3 months Libor |

YIELD CURVE STRUCTURES

A parallel shift of the yield curve implies that the rates at all maturities move up or down simultaneously by the same basis points. However, this happens rarely. Usually, there is some amount of twisting that goes on in the yield curve.

Yield curve structures help contract holders incorporate their views on the steepening or flattening of yield curves into their structures, or give them exposure to movements on particular points on the curve. If their views turn out to be correct, they can obtain a significant discount on their interest costs.

Constant Maturity Swap

Strategy Term: Constant Maturity Swap

Strategy Description: It is a variation of interest rate swap wherein constant maturity leg is reset in each period to a long-term swap rate. The other side of the swap can either be fixed or floating.

Strategy Application: The contract holder plans his annual budgeting according to long-term rates, or perhaps has a view that the yield curve will fall in its long end. Either way, he wishes to move his liability to the rates at the far end of the curve.

In such a case, the contract holder can enter into a Constant Maturity Swap. There is a difference between this type of swap and a regular swap. In a regular IRS (Interest Rate Swap), benchmark of fixing has the same tenor as the settlement tenor. However, in a CMS (Constant Maturity Swap), the reset rate is a long-term rate—say the two years or the five years swap rate, while the reset period is less—usually three months.

At each payment exchange date, the contract holder gets paid the six months Libor rate; in return he pays a long-term interest rate (two years, five years, 10 years, etc.) less spread.

Payoff

- Contract holder pays: CMS rate.

- Contract holder receives: USD three months Libor + K.

Pros

Risks Involved

- The contract holder is still not completely hedged, and is open to adverse movements in interest rates.

- The contract holder will lose if yield curve’s steepness increases.

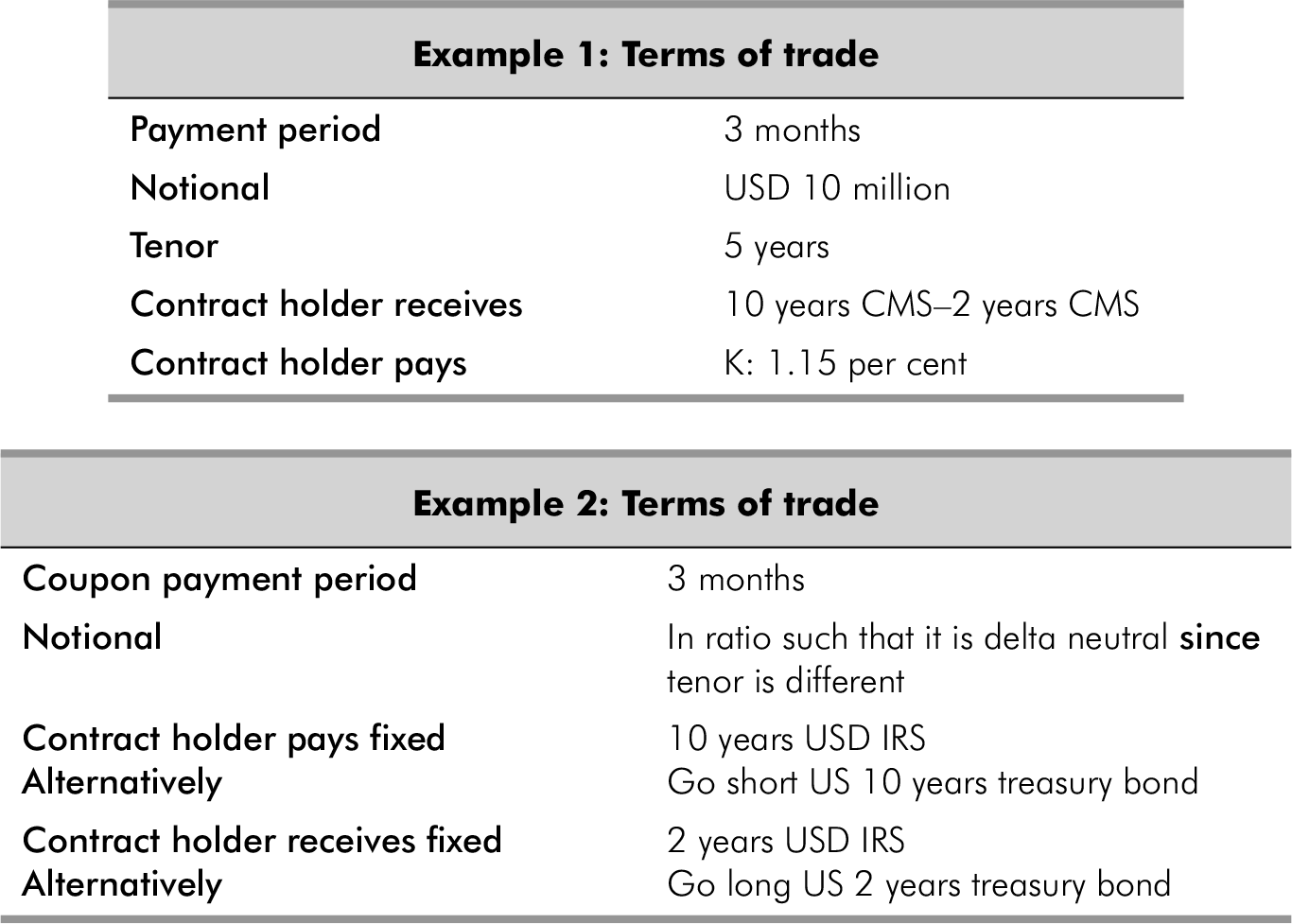

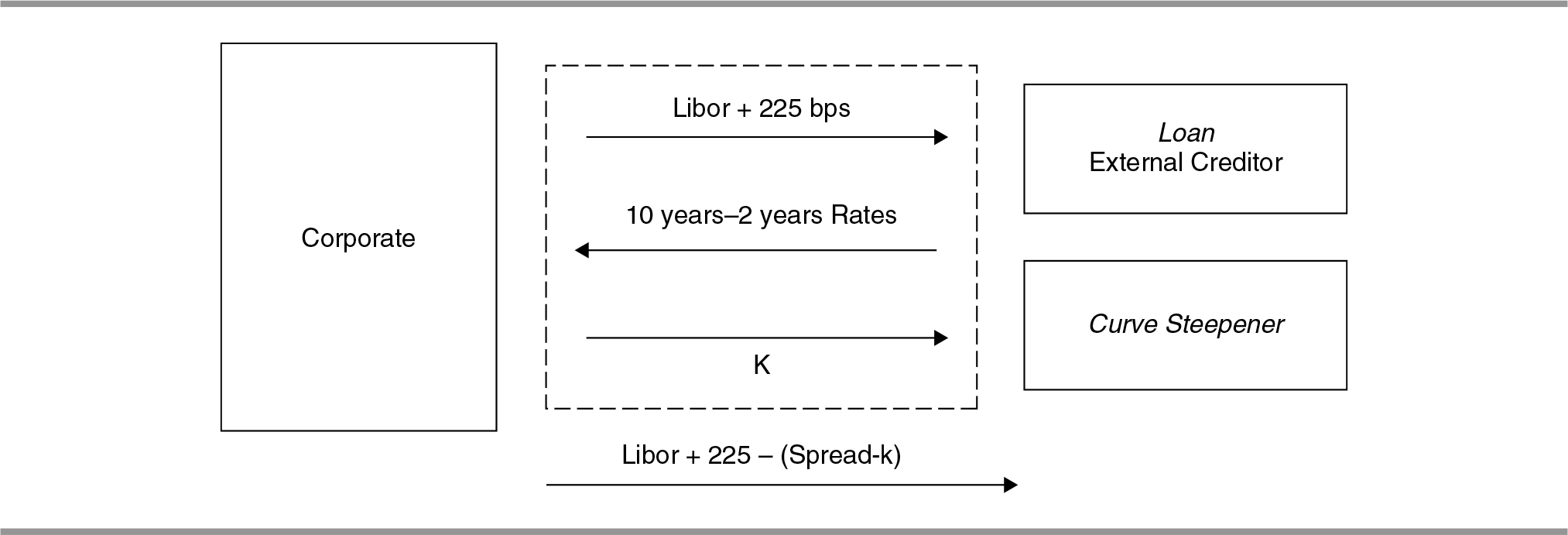

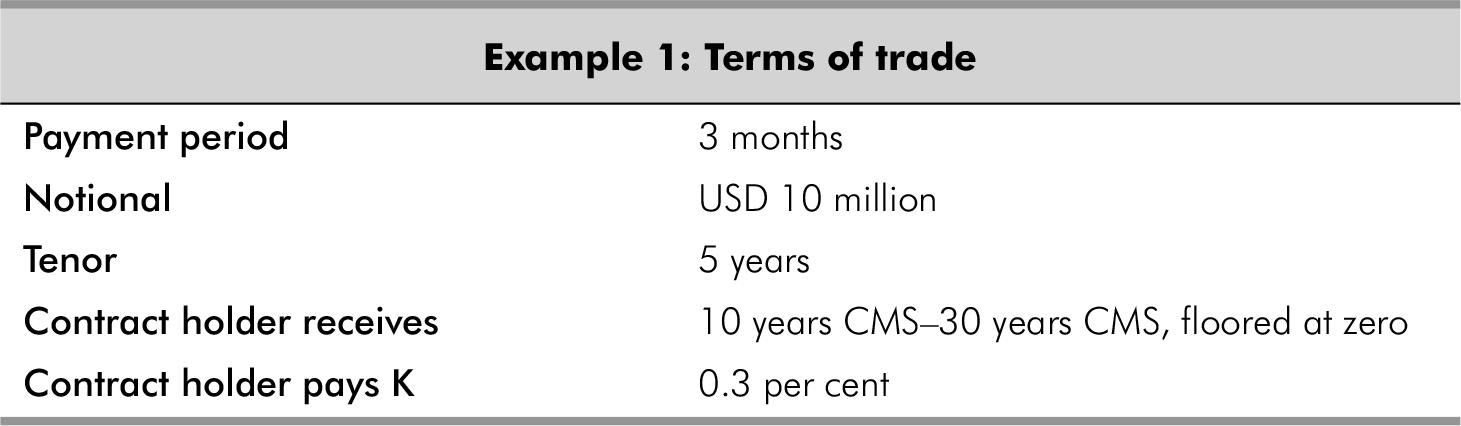

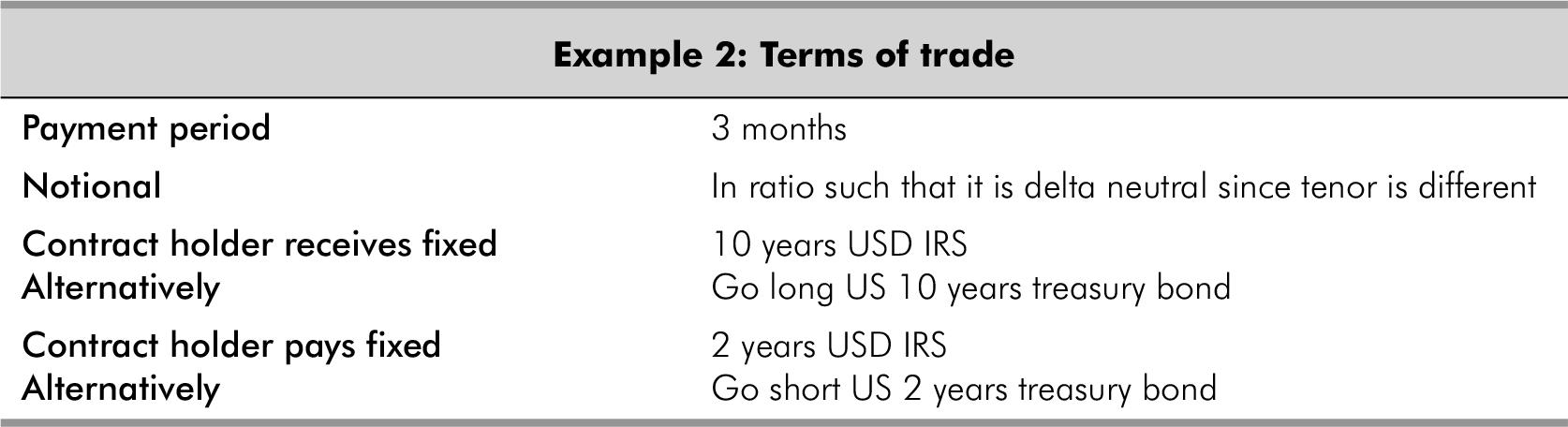

Curve Steepeners

Strategy Term: Curve Steepeners

Strategy Description: It gives a positive payoff if the yield curves steepen, i.e., long-term yields increase relative to the shorter-term yield spread comes down.

Strategy Application: The contract holder believes that the yield curve at higher maturities will go up, relative to the curve at shorter maturities. He wants to benefit from it. In this case, the contract holder can participate in a Curve Steepener.

This consists essentially of receiving a near term CMS swap while simultaneously paying a longer term one.

If the yield curve shifts, as the contract holder believes it will, the contract holder pays lower on the floating leg of the near term CMS, but receives higher payments as the far term floating payments increase.

However, if the curve moves in the opposite direction, the contract holder stands to lose money.

Payoff: Each month

- Contract holder pays: Fixed K.

- Contract holder receives: Long-term rates–Near term rates (Reset Quarterly).

- Contract holder receives fixed: Two years USD IRS.

- Alternatively: Go long US two years treasury bond.

Graph 8.8

Pros

Risk Involved

- If the view is wrong, the company will lose as the spread decreases.

Curve Flatteners

Strategy Term: Curve Flatteners

Strategy Description: It gives a positive payoff if the yield curve flattens, i.e., the long-term yields decrease relative to shorter-term yield and hence the spread comes down.

Strategy Application: The contract holder believes that the yield curve will go down in longer maturities, relative to the curve at shorter maturities. He wants to benefit from this phenomenon by obtaining a discount on his interest payments. In this case, the contract holder can participate in a Curve Flattener.

This consists essentially of paying a near term CMS swap while simultaneously receiving a longer-term CMS.

If the yield curve shifts, as the contract holder believes it will, the contract holder pays lower on the floating leg of the near term CMS, but receives higher payments as the far term floating payments increase.

However, if the curve moves in the opposite direction, the contract holder stands to lose.

Payoff: Each month:

- Contract holder pays: Fixed K.

- Contract holder receives: Near term rates–Long-term rates reset quarterly.

Pros

- The contract holder can gain substantial discounts on his coupon payments, if his view is correct on the yield curve.

Risks Involved

- If the contract holder’s view is wrong, he will lose as the spread increases.

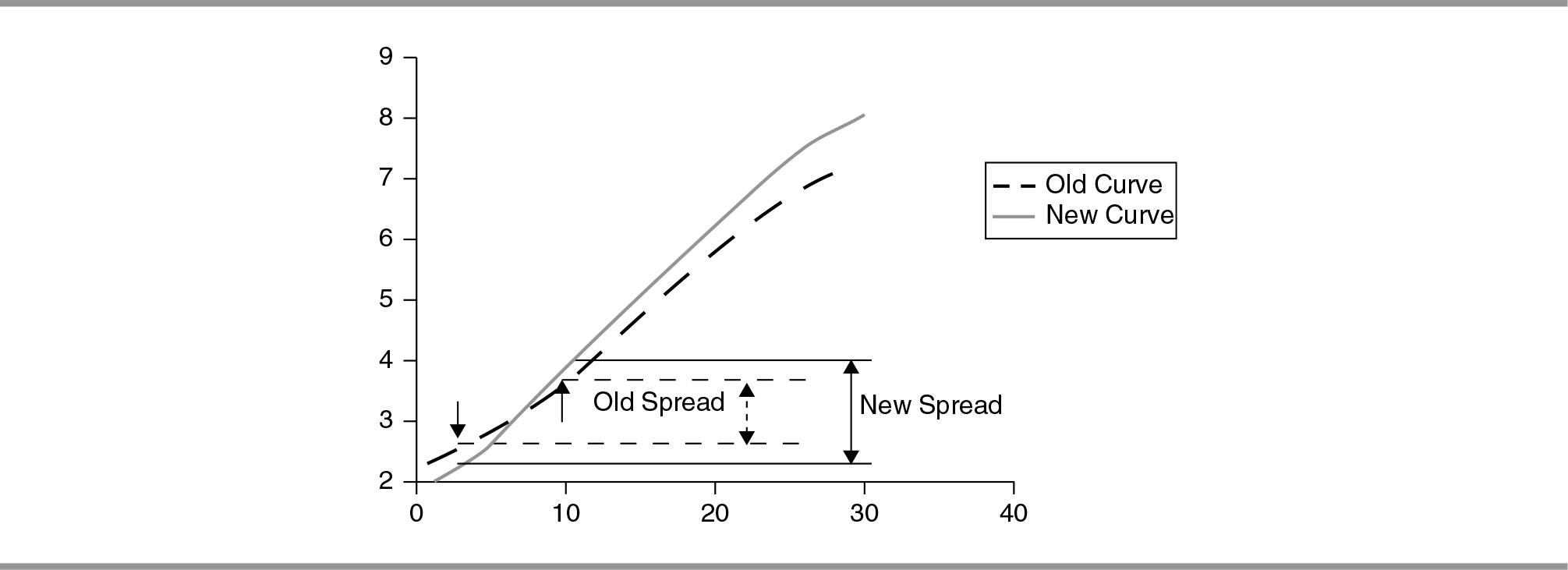

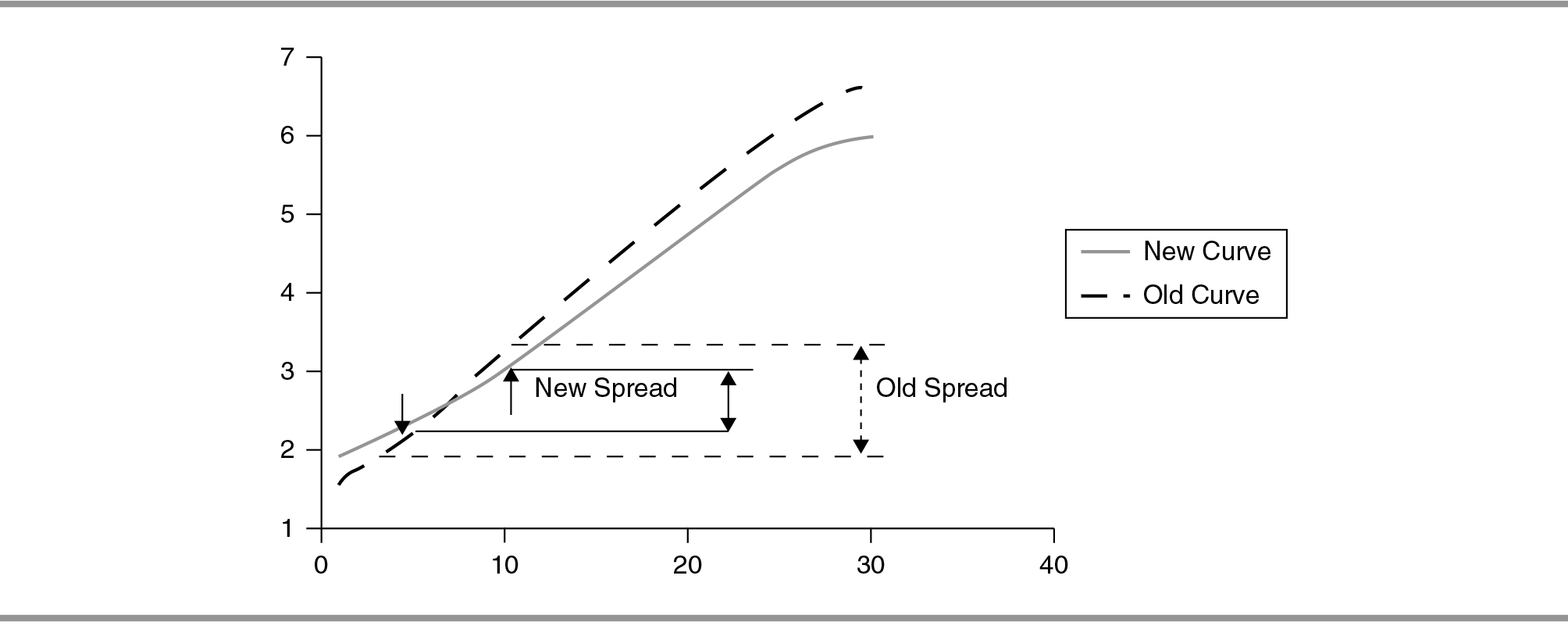

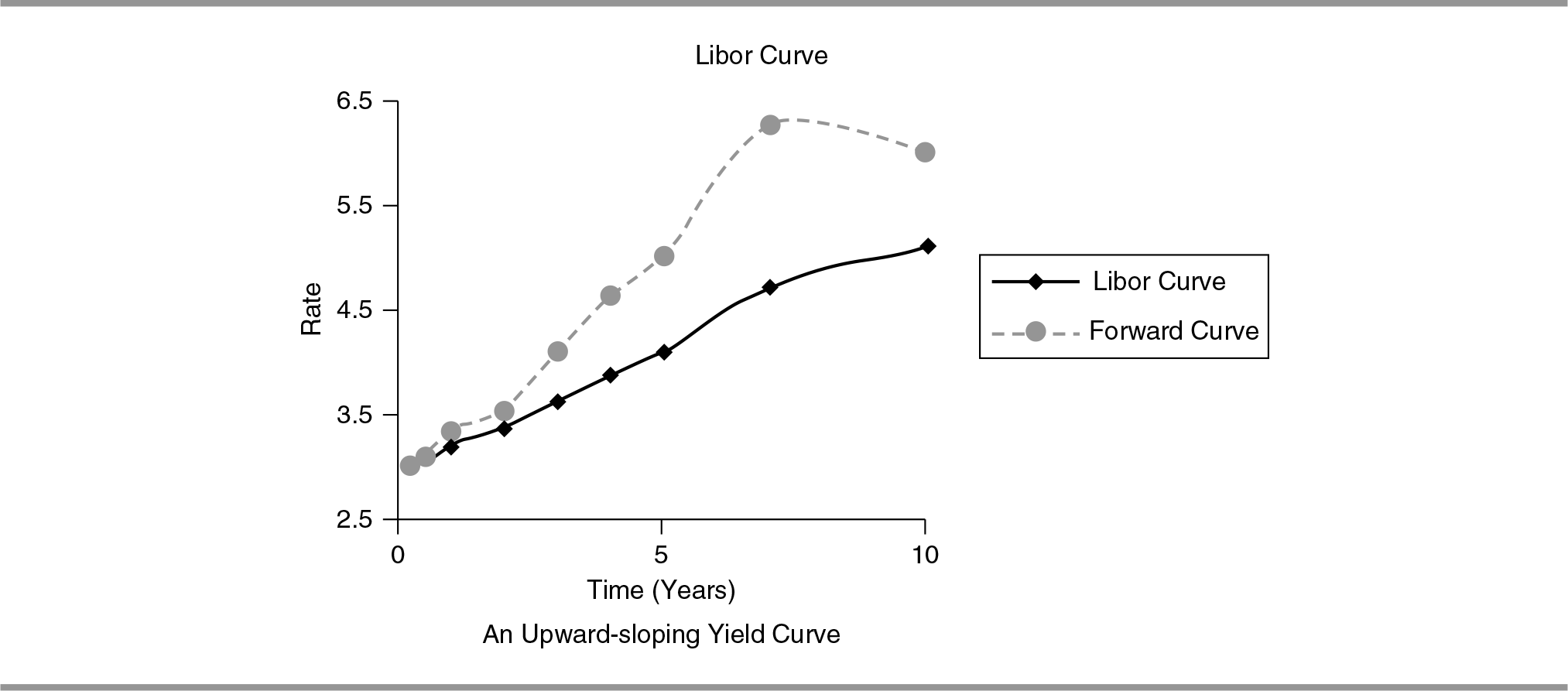

FRAs, Swaps and the Libor Curve: The Libor Curve, or the Swap Curve, is a graph of what the fixed rate in Libor swaps of different maturities is. (The yield curve is similar, but it shows the yields of government bonds instead).

The FRA rate which is quoted depends on the market expectations of the future Libor rates (shown as forward curve) and it is derived from the Libor curve.

One immediately noticeable characteristic here is that the Forward Curve is much steeper than the Libor curve. This, in general, is true.

The forward curve ‘amplifies’ changes in the Swap Curve. The reason for this is apparent after some reflection.

Consider a swap rate of 3.6 per cent and 3.9 per cent for five years and six years, respectively. The six years swap can be seen as a combination of the five years swap, and a forward starting swap between the fifth and sixth years. The rate on that one forward swap, however, pulls up the entire rate, even for the first five years, up from 3.6 per cent to 3.9 per cent. So, it has to be significantly above 3.9 per cent. (As a matter of fact, it comes to 5.41 per cent).

Graph 8.10

KEY CONCEPTS OF RATES MARKET

- Day count conventions

INR Act. 360 USD Libor Act. 360 EUR Libor Act. 360 CHF Libor Act. 360 JPY Libor Act. 365 CAD Libor Act. 365 GBP Libor Act. 365 INROIS Act. 365 INBMK Act. 360 EURIBOR Act. 365 - Business day convention: It is the convention of adjusting dates specified or determined in respect of a transaction, for example, a payment date. The adjustment is necessary in case the date in question falls on a day which is not a ‘Business Day’.

- MFBD: Under the convention of modified following business day (MFBD), in case the date on which an action has to be taken in respect of particular transaction is not a business day, then the action has to be postponed to a date which is the next succeeding business day unless the first following business day is in the next calendar month, in which case that date will be the first preceding day which is a business day. So if the date specified is 28 February and the first following business day is 1 March, the date will instead be 27 February (if it is a Business Day).

- Preceding business day: A business day convention whereby in case the day on which an action has to be taken in respect of a particular transaction falls on a holiday then the day moves backward to the preceding good business day.

MISCELLANEOUS ILLUSTRATIONS

ILLUSTRATION 1

Company Strong Ltd and Weak Ltd; have been offered the following rate per annum on a USD 200 million five years loan:

| Fixed rate | Floating rate | |

|---|---|---|

| Company Strong Ltd | 12.0 | Libor + 0.1% |

| Company Weak Ltd | 13.4 | Libor + 0.6% |

Company Strong Ltd requires a floating rate loan and Company Weak Ltd requires fixed rate loan. Design a swap with swap counterparty commission as 0.1 per cent p.a. which is equally attractive to both the companies.

Solution

| Strong Ltd | Weak Ltd | |

|---|---|---|

| Fixed rate | 12% | 13.4% |

| Floating | Libor + 0.1% | Libor + 0.6% |

| Choice | Floating | Fixed |

Under their choice: total of interest rates = 13.4 per cent + Libor + 0.1 = Libor + 13.5 per cent

Under swap deal = 12 per cent + Libor + 0.6 = Libor + 12.6

Gross savings = (Libor + 13.5) − (Libor + 12.6) = 0.9 per cent

Swap counterparty commission = 0.1 per cent

Net savings = 0.9 − 0.1 = 0.8 per cent

Share of each party = 0.4 per cent

Cost to party = Payment to lender − Reimbursement from swap counterparties + Swap counterparty commission

Strong Ltd. = 12 per cent − 12 per cent + (Libor + 0.1 per cent − 0.4 per cent)

= Libor − 0.3 per cent

Weak Ltd. = (Libor + 0.6) − (Libor + 0.6)

= (13.4 − 0.4) = 13 per cent

ILLUSTRATION 2

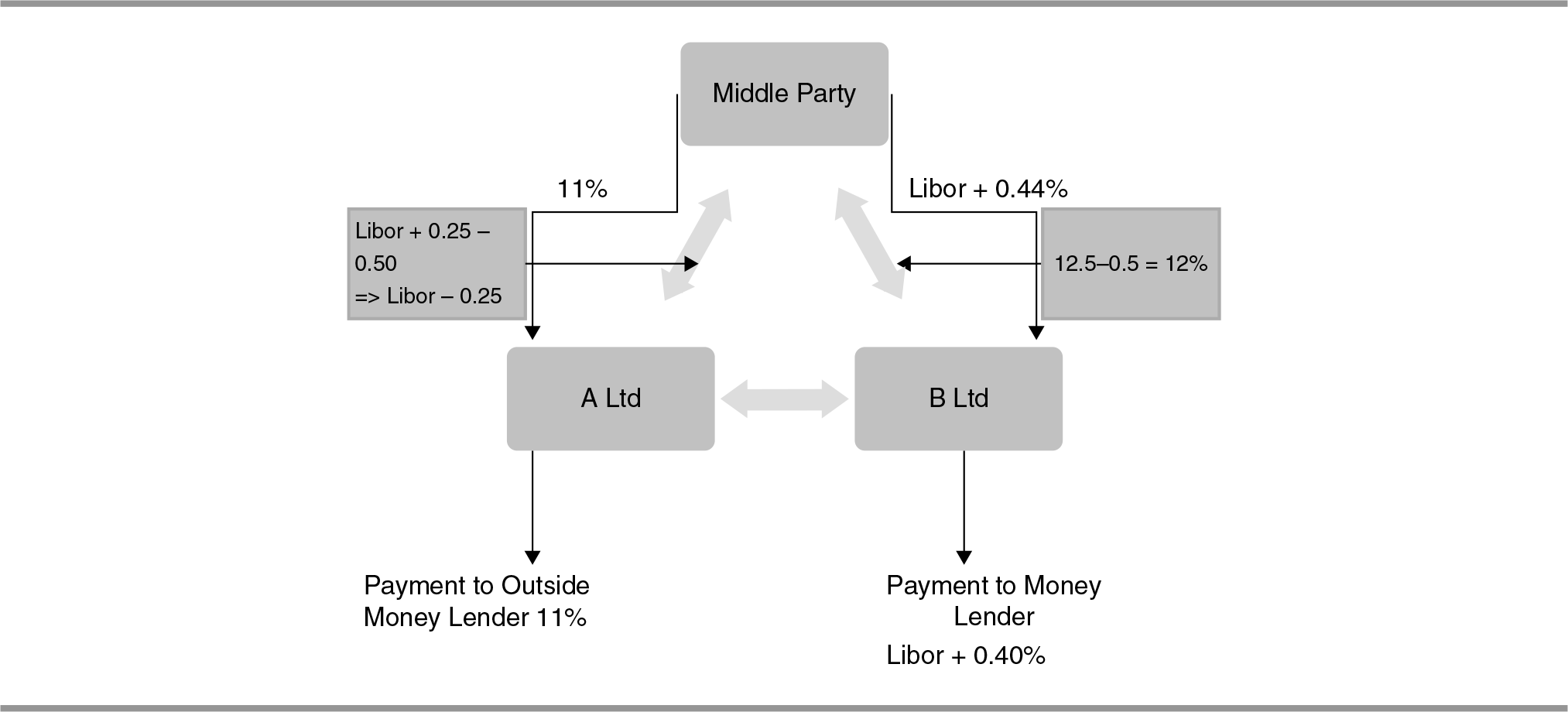

Companies A Ltd and B Ltd are interested in raising loans. The lender has quoted the following interest rates:

Fixed rate |

Floating rate |

|

|---|---|---|

| A Ltd | 11% | Libor + 0.25% |

| B Ltd | 12.50% | Libor + 0.40% |

A is interested in floating rate and B is interested in fixed rate. A financial institution has agreed to arrange a swap with commission of 35 basis point spread. If the swap is equally attractive to A and B, how much do they end up paying?

Solution

| A Ltd | B Ltd | |

|---|---|---|

| Fixed rate | 11% | 12.5% |

| Floating rate | Libor + 0.25% | Libor + 0.40% |

| Choice of type | Floating | Fixed |

Total of interest rate are as follows.

- Under own choice = Libor + 0.25 + 12.5 = Libor + 12.75.

- Under swap deal = 11 per cent + Libor + 0.40 = Libor + 11.40.

- Gross savings = (Libor + 12.75) − (Libor + 11.40) = 1.35 per cent.

- Share of middleman/swap counterparty = 0.35 per cent.

- Net savings = 1.35 − 0.35 = 1.00 per cent.

- It is shared equally by parties = 0.50 per cent each.

Cost to parties = Payment to outside − Reimbursement from middleman + Payment to middleman

A = 11 per cent − 11 per cent + (Libor + 0.25 − 0.50) = Libor − 0.25

B = (Libor + 0.40) − (Libor + 0.40) + (12.5 − 0.50) = 12 per cent

ILLUSTRATION 3

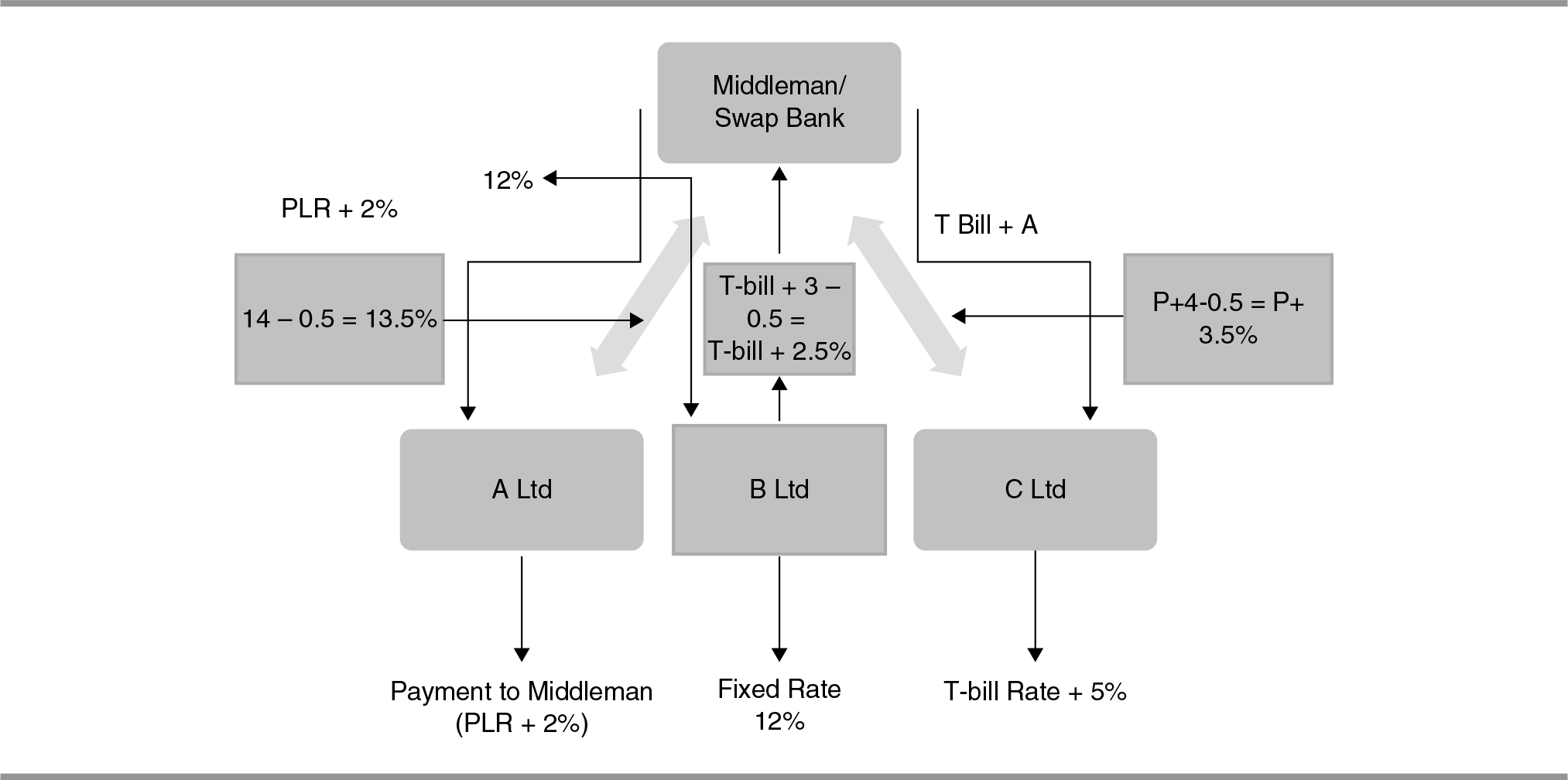

A, B and C are three companies, which are not finding suitable interest rates offered for their funds requirement, have approached a bank for arranging interest rate swap.

| Company | A | B | C |

|---|---|---|---|

| Objectives | Fixed Rate (%) | T-bill rate-based funds (%) | PLR-based funds (%) |

| Fixed rate | 14 | 12 | 15 |

| T-bill rate-based funds | T-bill + 4 | T-bill + 3 | T-bill + 5 |

| PLR-based funds | PLR + 2 | PLR+3 | PLR+4 |

The bank wants to arrange swaps among the three parties in such a way so that it can retain 25 per cent of the total gain. The rest of the gain is to be distributed equally among the three parties.

Solution

| A | B | C | |

|---|---|---|---|

| Fixed rate | 14% | 12% | 15% |

| T-bill rate | T-bill+4 | T-bill+3 | T-bill+5 |

| PLR rate | P+2 | P+3 | P+4 |

| Choice of type | Fixed | T-bill | PLR-based rate |

- Take the three types of interest rates with high rate, and difference under that type.

- Mark the highest difference, mark the lowest rate against that. Assign this type to the party to whom this rate belongs.

| High | Low | Difference | |

|---|---|---|---|

| Fixed | 15 | 12 | 3 |

| T-bill | T+5 | T+3 | 2 |

| PLR | P+4 | P+2 | 2 |

The highest difference is 3 per cent, the lowest rate against it 12 per cent. It is a fixed rate. This rate belongs to B. Assign fixed rate to B.

Now repeat the process with the remaining two rates under the parties A and C.

| High | Low | Difference | |

|---|---|---|---|

| T-bill | T+ 5 | T+4 | 1 |

| PLR | P+4 | P+2 | 2 |

Now the highest difference is 2 per cent and it is under type PLR-based rate. The lowest rate under this type belongs to A. Hence A will be assigned a PLR-based rate.

Finally, C will be assigned a T-bill rate.

Total of interest rate:

- Under own choice = 14 per cent + (T + 3) + (P + 4) = T + P + 21.

- Under swap deal = (P + 2) + 12 + (T + 5) = T + P + 19.

- Gross savings = (T + P + 21) = (T + P + 19) = 2 per cent.

- Share of middleman = 25 per cent of Gross saving (2) = 0.5 per cent.

- Net savings = 2 − 0.5 = 1.5 per cent.

It will be spread equally amongst three parties’ at 0.5 per cent each.

Cash to parties:

- A = (PLR + 2 per cent) − (PLR+2 per cent) + (14 − 0.5) = 13.5 per cent.

- B = 12 per cent − 12 per cent + (T-bill + 3 − 0.5) = T + 2.5 per cent.

- C = (T-bill + 5 per cent) − (T-bill + 5 per cent) + (PLR + 4 − 0.5)= PLR + 3.5.

ILLUSTRATION 4

A US Fortunate Ltd company wishes to lend USD 1,00,000 to its Japanese subsidiary. At the same time another Japanese company wishes to lend approximately the same amount to its US subsidiary. The parties are brought together by an investment bank for making parallel loans. The US company will lend USD 1,00,000 to the US subsidiary of Japanese company for four years @ 13 per cent (compounded annually). Principal and interest are payable only at the end of four years in dollars.

The Japanese company will lend to the Japanese subsidiary of the US company 14 million yens at 10 per cent (compounded annually) for four years. The current exchange rate is JPY 140 per USD. However, USD is expected to decline by 5 JPY per USD per year for each of next four years.

What amount of JPY, the Japanese company will receive (from Japanese subsidiary of US company) after four years? What will be USD equivalent of this amount?

How many USDs, the US company will receive after four years (from US subsidiary of Japanese Co.)? Which party is better off in this deal? What would happen if the value of JPY did not change?

Solution

- A US company has to provide a loan of USD 1,00,000 to a Japanese company subsidiary in the United States. The loan will be for four years @ 13 per cent p.a. compounded annually.

A Japanese company has to provide equivalent JPY currency loan 14 million JPY, i.e., 140 lakhs JPY to US subsidiary. In Japan, the loan will be for four years @10 per cent p.a.

Spot rate USD 1 = JPY 140

USD 100,000 = JPY 140 lakhs

The receipt by US company at the end of four years = Loan × (1+Interest rate) × 4

= USD 1,00,000 × (1 + 0.13) × 4 = USD 1,63,047.36.The receipt by Japanese company at the end of four years = 1,40,000 JPY × (1+0.10) × 4

= 2,04,97,400 JPY.- Exchange rate USD 1 = JPY (140 − 5 − 5 −5 − 5) = JPY 120.

- Equivalent dollar

- The Japanese company gains

- The amount of gain is 1,70,811.67 − 1,63,047.36 = USD 7,764.31.

- If there is no change in exchange rate @ four years end USD 1 = JPY 140.

- Equivalent dollars receipt by the Japanese Company

- The gain to US company will be = USD 1,63,047.36 − 1,46,410 = USD 16,637.36.

TEST YOUR UNDERSTANDING

- Explain why FRA is equivalent to the exchange of a floating rate of interest for a fixed rate of interest.

- A financial institution has entered into an interest rate swap with company X. Under the terms of the swap, it receives 10 per cent per annum and pays six months Libor on a principal of USD 10 million for five years. Payments are made every six months. Suppose company X defaults on the sixth payment date (at the end of year 3) when the interest rate (with semi-annual compounding) is 8 per cent per annum for all maturities. What is the loss to the financial institution? Assume that six months Libor was 9 per cent per annum halfway through year three.

- A financial institution has entered into a 10-year currency swap with company Y. Under the terms of the swap, the financial institution receives interest at 3 per cent per annum in Swiss francs and pays interest at 8 per cent per annum in US dollars. Interest payments are exchanged once a year. The principal amounts are seven million dollars and 10 million francs. Suppose that company Y declares bankruptcy at the end of year six, when the exchange rate is USD 0.80 per franc. What is the cost to the financial institution? Assume that, at the end of year six, the interest rate is 3 per cent per annum in Swiss francs and 8 per cent per annum in US dollars for all maturities. All interest rates are quoted with annual compounding.

- Companies A and B are interested in raising loans. The financiers have quoted the following interest rates:

Bank A 17% Fixed Libor + 1.00% Floating Bank B 14.50% Fixed Libor + 0.50% Floating A is interested in floating, while B is interested in fixed. A financial institution named Bank C is planning to arrange the swap and requires 50 basis points spread.

- If the swap is equally attractive to A and B, what rates of interest will A and B end up paying?

- What do you mean by interest rate caps and floors? Explain with an example.

- Alt, Balt and Calt are three companies, which are not finding suitable interest rates for their funding needs have approached a bank for arranging interest rate swap.

Company Alt Balt Calt Objectives Fixed Rate (%) T-bill rate-based funds (%) PLR-based funds (%) Fixed rate 24 22 25 T-bill rate-based funds T-bill + 5 T-bill + 4 T-bill + 6 PLR-based funds PLR + 3 PLR+4 PLR+5 The bank wants to arrange swaps among the three parties in such a way so that it can retain 25 per cent of the total gain. The rest of the gain is to be distributed equally among the three parties.