chapter 13

ISDA Agreement: Documenting Derivatives

LEARNING OBJECTIVES

ISDA (International Swap and Derivatives Association) Master Agreement with its various schedules, annexure, etc. has been widely accepted by majority of the market participants as a global standard for documenting over-the-counter derivative transactions. This chapter aims to provide readers an overview of the contents of this agreement. The contents of this chapter are organized in the following order:

4. Architecture of the Agreement

7. Advantages of the Agreement

INTRODUCTION

ISDA was established in the year 1985 as a trade organization for the participants of over-the-counter derivatives market. It has its headquarter in New York and its first President was Mark C. Brickell. He held this position from 1988 to 1992.

ISDA was formally called International Swap Dealers Association but gradually it changed its name and became International Swap and Derivatives Association. This change was made to focus more attention on its efforts to improve the more broad derivatives markets and to stay away from interest rate swap contracts.

Today, ISDA has more than 825 members from 57 countries on six continents. These members include a broad range of OTC derivatives market participants: global, international and regional banks, asset managers, energy and commodities firms, government and supranational entities, insurers and diversified financial institutions, corporations, law firms, exchanges, clearinghouses and other service providers.

The primary motive of ISDA was to make the over-the-counter (OTC) derivatives markets, all over the world, a safe and efficient place for the parties dealing in OTC derivatives. So it developed a master agreement known as ISDA master agreement.

ISDA MASTER AGREEMENT

The ISDA master agreement is a contract between two parties, stating the terms and conditions to be followed by the parties in the contractual relationship. Derivatives listed on the exchange are standardized contracts with terms and conditions of trade specifically listed and thus there exists no confusion. However, in the case of OTC derivatives, a lot of complexities exist as contracts are not standardized. However, each contract is unique and customized as per the requirements of the client. Thus, here, ISDA agreement plays an important role in deciding the terms of the trade.

The ISDA master agreement is the most widely accepted master agreement for drafting customized contracts in OTC derivatives market. It is a framework of documents which enables parties to design highly flexible contracts, yet fully documented. Its framework consists of a master agreement, a schedule, confirmations, definition booklets and a credit support annex.

Although ISDA master agreement could be viewed as a beneficial tool for financial institutions like banks, it is equally advantageous for other counterparties which are entering into a contractual relationship for derivatives.

HISTORY

In 1985, the ISDA developed a swap code which had standard definitions, representations and warranties, events of default and remedies. But later in 1986 it revised this swap code and made it the ISDA master agreement.

ISDA has updated its master agreement time and again for the better. First, it updated the master agreement in 1986 and then again in 1987 when it produced three documents:

- A standard form master agreement for US dollar interest-rate swaps.

- A standard form master agreement for multi-currency interest-rate and currency swaps (collectively known as the ‘1987 ISDA Master Agreement’).

- The interest rate and currency definitions.

ISDA upgraded the agreement several times in the 1990s and presented a number of documents including:

- A revised version of the swaps code, known as the 1991 ISDA definitions, drafted and replaced later by the 2000 ISDA definitions.

- A revision to the 1987 master agreement resulting in the 1992 master agreement.

- The User’s Guide to the 1992 master agreement, drafted in 1993, explaining in detail each section of the 1992 master agreement.

- The commodities derivatives definitions, drafted in 1993 and supplemented in 2000.

- The annex, providing for collateral documentation, finalized in 1994 followed by its User’s Guide in 1995.

The latest revision was made in 2002 and henceforth the ISDA master agreement has been known as the 2002 ISDA master agreement. All these updates had their origin in the succession of crises that the global financial markets faced in the late 1990s. Events such as the liquidation of Hong Kong broker-dealer Peregrine Investments Holdings, the 1998 Russian financial crisis and many others tested the ISDA documentation to a previously unseen degree.

Although it withstood that test, ISDA decided to establish a regular strategic review of its documentations so that any concealed flaw could be dealt with. The 2002 ISDA master agreement was the result of same upgradation of the 1992 master agreement.

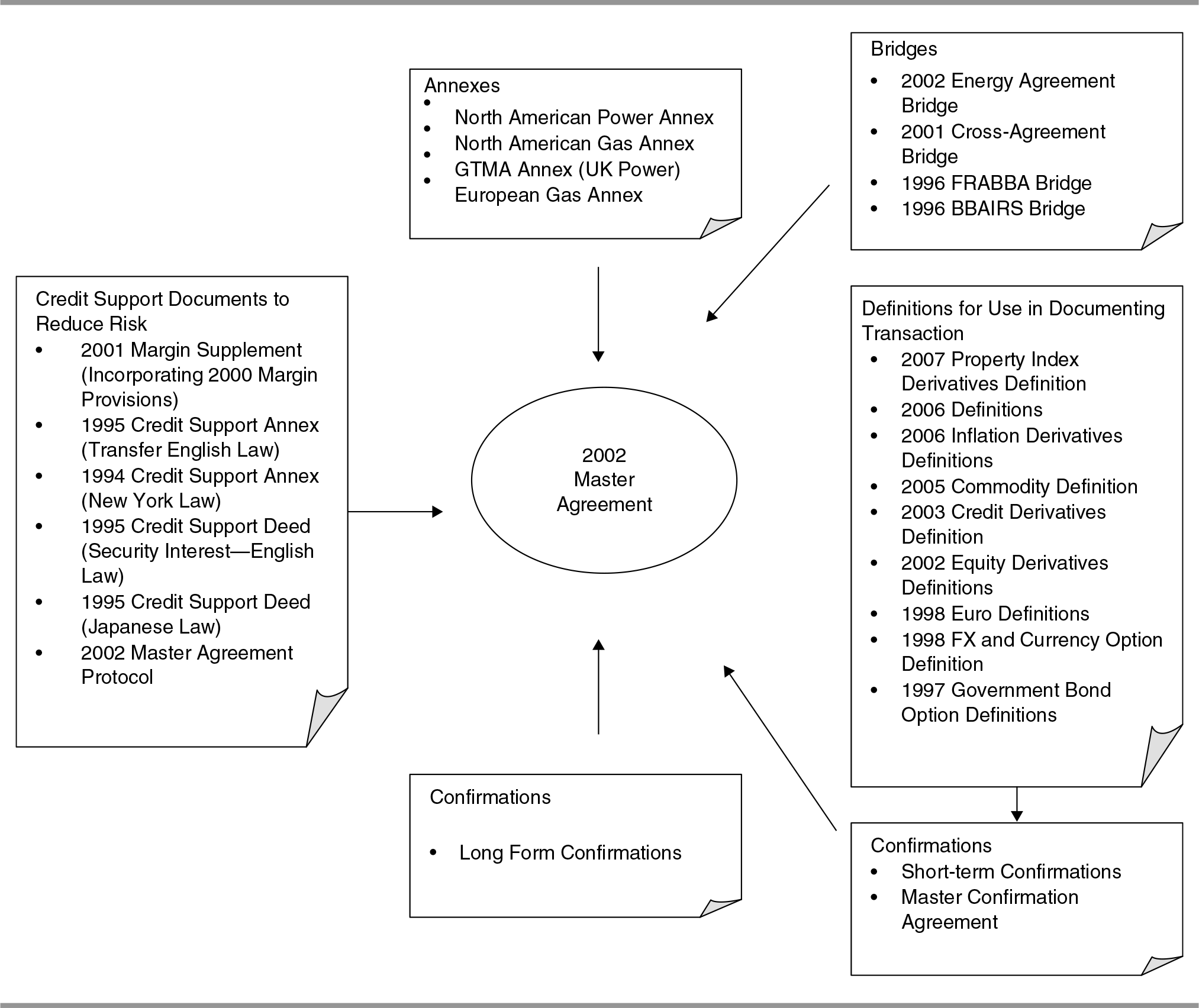

ARCHITECTURE OF THE AGREEMENT

It is clear from the ISDA Agreement Structure that the master agreement is the central document around which the rest of the ISDA documentation structure is built. The master agreement has no scope of any alteration except the name of the parties. All the other changes to customize agreement are done through schedules. Schedule is a document containing elections, additions and amendments to the master agreement.

The master agreement, together with the schedule, lays out all the general terms and conditions that are necessary for the proper allocation of the risks which are innate in all the transactions. But it does not contain any specific commercial terms for any particular transaction. Hence, once the master agreement is executed, the parties can enter into numerous transactions by agreeing to the material commercial terms over the telephone, as evidenced by a written confirmation, without any need to revisit the underlying terms contained in the master agreement.

The master agreement basically has two versions: the local version and the multicurrency version.

- Local version: It is for the transaction between the parties located in the same jurisdiction which are transacting in only one currency.

- Multicurrency version: It is used when parties are located in different jurisdictions transacting in different currencies. It resolves issues such as taxes, currency of payment, the use of multiple offices to enter into transactions and the designation of an agent for service of process.

Single Agreement

Section 1(c) of the 2002 ISDA Master Agreement states that:

‘All transactions are entered into in reliance on the fact that this Master Agreement and all Confirmations form a single agreement between the parties... and the parties would not otherwise enter into any Transactions’.

This single agreement concept emphasizes on the fact that all the transactions entered by a single party or one contract. And in case of default, the other party has the right to consider several transactions as one contract to close out those transactions and come up with a single net amount payable.

Events of Default and Termination Events

Section 5 of the ISDA master agreement contains ‘Events of Default’ and the ‘Termination Events’. These are the events which can lead to termination of transactions before their intended maturity.

Events of default could be any event under which one of the parties of the transaction is at fault. Events of default could be a failure to perform under a transaction, breach of a representation or undertaking, and insolvency.

Although events of termination are those events where none of the party is at fault, but the transaction stands terminated. Events of termination could be a change in tax law resulting in taxes being imposed on transactions, illegality or a merger of a party resulting in deterioration in its credit quality.

Close Out Netting

Section 6 of the ISDA master agreement provides parties to the agreement the right to terminate the transaction early if an event of default or termination event occurs in respect to the other party. The party that is terminating the transaction also has the right to set out the procedure to calculate and net the termination values of those transactions to produce a single amount payable between the parties.

There are two elections that the parties make in the schedule which affect the operation of these provisions:

- Whether the party not at fault will be required to pay the party at fault, if the net termination amount calculated is due on the party not at fault. This is a choice of payment or the method of the payment:

- First method: Under this method, the party not at fault does not need to pay at all.

- Second method: This method makes the party not at fault pay to the party at fault.

- Whether the termination values for the transaction will be determined by ‘Market Quotation’ and ‘Loss’. This is a choice of payment measure between:

- Market quotation: Obtaining quotes from dealers in the market for replacement transactions.

- Loss: The party not at fault working out how much it has lost or gained as a result of early termination.

These elections were to be made in respect of the 1992 master agreement. But in the 2002 master agreement, the election between the first method and the second method was withdrawn. The logic behind was that in practice, no one really opted for the first method as it required the relevant financial institutions to report their gross, rather than net, exposure under the master agreement.

Also in the 2002 master agreement, the distinction between market quotation and loss was inhibited and instead a single concept of ‘close-out amount’ was introduced. This is nothing but broadly the profit or loss that would be incurred in entering into a new and equivalent transaction due to the early termination of the transaction.

The aggregate of the close-out amount and the unpaid amount is referred to as the ‘early termination amount’. This is the net amount payable by one party to the other in respect to the terminated transactions.

Taxation

ISDA master agreement has provisions for the events of taxation. Section 2(d) of the agreement sets off the consequences if a tax is imposed on a payment required to be made by a party under a transaction. A gross-up obligation for certain ‘indemnifiable taxes’ is included in the provision. Taxation representation which is contained in Secs. 3(e) & 3(f) and other provisions of the agreement like undertakings in Secs. 4(a) and 4(d), and termination events in Secs. 5(b) (ii) and 5(b) (iii) is extremely complex in nature, and great care has to be taken by the negotiators to ensure that the result is not the opposite to what was intended.

The range of taxation matters which can be relevant to particular derivative transactions includes interest withholding tax, quasi-withholding tax, goods and services tax and stamp duty.

Multi-branch Issues

Such issues crop up when the transaction is of multicurrency version. It is used when parties are located in different jurisdictions transacting in different currencies. It resolves issues such as taxes, currency of payment, the use of multiple offices to enter into transactions and the designation of an agent for service of process.

RELATED DOCUMENTS

Schedule

As already stated, no changes can be made in the master agreement and annex. Hence, a document called schedule and Paragraph 13 are used to facilitate any change and make a customized agreement. Changes like elections of the various options presented to the parties in the master agreement and annex, the addition of provisions not contained in the master agreement, etc. are done through schedules. For example:

- The elections referred to in the master agreement, such as the payment measures and methods, the thresholds relating to certain events of default, and the offices through which parties can act.

- Any amendments that the parties agree to make to the terms of the master agreement.

- Any additional terms that the parties want to include, such as a set-off clause between close-out amounts and amounts owing under other contracts.

Credit Support Annex

The use of credit support annex (CSA) is optional. It is added if the parties to the contract agree that collateral will be provided by a party, if the exposure of the other exceeds an agreed amount. The CSA contains provisions concerning the posting and return of collateral, the types of collateral that may be used and the treatment of collateral by the secured party.

Confirmations

Confirmations are evidence of the terms of the transaction. They are also known as trading advice or contract note. Confirmations are extremely important in OTC derivatives transactions since they are usually entered into orally or electronically and the contract between the parties is formed at this time. Confirmations are in the form of short letter, fax, e-mail, etc. The form of the confirmation is set out in the master agreement and limited period of time is allowed for objections or amendments to the confirmation after its receipt. Confirmations are normally very small, except in case of complex transactions, containing a little more than dates, amount and rates. Confirmations are exchanged to minimize the possibility of a dispute regarding the terms of a transaction.

Definitions

Definitions and User’s Guide are designed by the ISDA as supporting documents for the master agreement. It helps in preventing any sort of dispute between the parties and to facilitate the consistent use and interpretation of the master agreement. These materials are produced by ISDA and are regularly updated to reflect the most recent regulatory or market changes. Each type of derivative transaction, such as credit derivative, currency derivatives, and equity derivatives, has its own definitional booklet.

LEGAL ISSUES

Netting

As per the master agreement, the parties in the contractual relationship should calculate their financial exposure under OTC transactions on a net basis, i.e., a party calculates the difference between what it owes to the counterparty and what the counterparty owes it under the same agreement.

These calculations are made on a mark-to-market basis to reflect the current position of each transaction. Netting is important as it permits the parties under transaction to exchange a single amount rather than numerous payments involving the same transactions. Most counterparties also agree to net all amounts due on a single day regardless of whether amounts are due under a single or multiple transactions.

Set-off

Set-off is a final settlement of account that extinguishes any mutual debt between the counterparties of the transaction for a new net amount due. The timely payment is imposed by enforcing interest on any amounts paid after the due date.

In support of this practice, the US Bankruptcy Code exempts participants in OTC derivative transactions from the automatic stay provisions of the bankruptcy code and permits them to set-off obligations owed between the creditor and the bankrupt party even during the pendency of a bankruptcy stay order.

Authority and Capacity

In case of OTC derivatives, the question that whether an individual has the authority to bind the company or not is not new and is governed by the traditional agency law. To avoid confusion and defaults, both the counterparties should check if the other party is authorized for confirming the transaction. It is common for parties to exchange authorized signatory lists of persons who have authority to execute confirmations and refer this in the schedule to the ISDA master agreement. Also, the ISDA master agreement states that the authority issue is the internal authorization matter of a company and that any person who is held out as being able to enter into OTC derivative transactions has the apparent authority to do so.

Reliance and Suitability

Parties try to limit their liability by including ‘non-reliance’ clause in the agreement. As per this clause, the parties agree that the transaction they are entering into is suitable for both of them and no party is relying on the other party for the transaction, i.e., neither party owes some kind of fiduciary relationship to the counterparty or has engaged in misleading conduct in inducing the counterparty to enter into the trade. If any dispute arises, the principles of equity, contract and trade practices law apply to OTC derivatives in the same way as they apply to other contracts.

Termination

The set-off provision in the master agreement provides a lot of relief to the creditor by permitting the set-off of obligations due and owing in case of counterparty’s bankruptcy, but there is no shield from the exposure to future positions that have not yet become due and owing. Considering this issue, the master agreement contains provisions permitting a creditor party to terminate and liquidate transactions upon counterparty’s bankruptcy or other default.

The master agreement provides the parties with two means by which the master agreement and all transactions thereunder may be terminated upon the occurrence of specified events.

The first is the occurrence of an event of default, which permits a party to terminate the master agreement and liquidate all transactions if the other party is affected by an event of default.

The second is the occurrence of a termination event which may affect both the parties. It is usually the result of the actions of third-parties and may provide the affected party a grace period to cure the termination event before the other party may terminate and liquidate the master agreement.

ADVANTAGES OF THE AGREEMENT

Few advantages of the ISDA master agreement are as follows:

- Although the master agreement is quite lengthy, once the terms and conditions are agreed upon, it becomes easier for the parties in the long run, as the future formalities of contract is reduced to a brief confirmation of the material terms of the transaction.

- The detailed documentation of the contract reduces many disputes by providing extensive resources, defining its terms and explaining the intent of the contract, thereby preventing disputes from beginning as well as providing a neutral resource to interpret standard contractual terms.

- Finally, the master agreement significantly aids in operation risk and credit risk management for the counterparties.

TEST YOUR UNDERSTANDING

- What is the necessity of ISDA in any financial market transaction?

- How many versions does the master agreement have?

- What is the meaning of ‘events of default and termination events’?

- Briefly explain the concept of netting and set-off.

- Briefly explain utility of credit support annex.