CASE STUDY 11

Queens Moat Houses plc

The following text is extracted from the Notes to the Accounts for the year to 31 December 1992 of Queens Moat Houses plc.

PRIOR YEAR ADJUSTMENTS AND RECLASSIFICATIONS

Following an investigation into the affairs of the group, including a review of the group's accounting policies and the treatment of certain transactions in prior years, the current directors have concluded that the accounts for 1992 and future years would be unlikely to give a true and fair view of the group's results and financial position if such policies and treatments continued to be adopted. Accordingly, certain changes have been made which, in the opinion of the current directors, ensure that the accounts are prepared in accordance with best practice and give a fairer presentation of the group's results and financial position. In order to ensure comparability, the 1991 accounts have been restated to reflect these changes. In addition, certain profit and loss account and balance sheet items have been reclassified. Further details of the prior year adjustments and reclassifications are set out below together with a summary of their effects on the accounts as at 31 December 1991 and for the year then ended.

Prior Year Adjustments

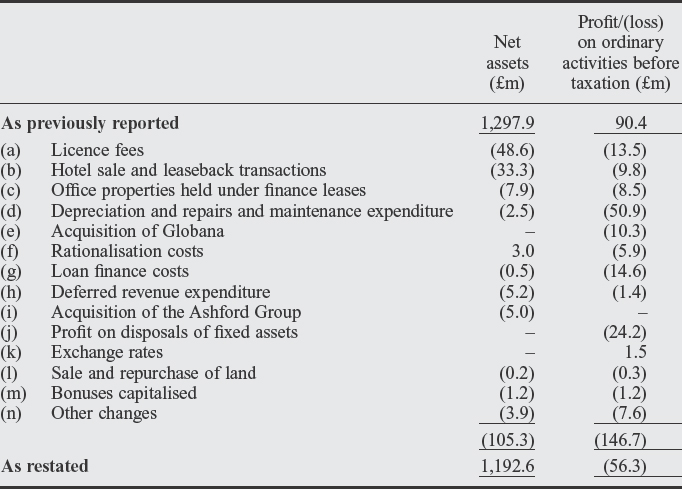

(a) Licence Fees

Previously, licence fees receivable from hotel operations not directly managed by the group were included in income in full at the commencement of the period of the licence and the turnover and net operating costs of such operations were included in group turnover and net operating costs. These policies have been changed and licence fees are now recognised on a straight line basis over the period of the licence. Furthermore, in view of the fact that the group's only contractual entitlement in respect of such operations is the receipt of a licence fee, the turnover and net operating costs of these operations are no longer recognised in the group's profit and loss account.

(b) Hotel Sale and Leaseback Transactions

Previously, sale and leaseback transactions which the group entered into with respect to certain UK hotel properties were accounted for as sales and operating leases, with the sales proceeds and profit on sale included in group turnover and operating profit respectively. In view of the nature of the leases, the current directors consider that they should, more appropriately, be accounted for as finance leases. Accordingly, this treatment has been changed and sale and leaseback transactions of this type are now accounted for as finance leases and the sales proceeds and profit on sale are no longer recognised in the accounts. The accounts have been restated accordingly.

(c) Office Properties Held under Finance Leases

As at 31 December 1991, the group held certain office properties under finance leases in connection with which there were outstanding liabilities amounting to £12.1 million. The properties were included in stocks as properties held for development at their cost of £12.1 million and the outstanding liabilities of £12.1 million were netted off in arriving at the total amount disclosed for stocks. The current directors consider that the nature of these properties was such that it was inappropriate to include them in stocks and that they should have been included in tangible fixed assets at their market value, which has subsequently been determined by the group's independent property advisers at £6.5 million and that the outstanding finance lease obligations of £12.1 million should have been included in creditors and not netted against stocks. The accounts have been restated for these and certain other related adjustments.

(d) Depreciation and Repairs and Maintenance Expenditure

Previously, certain tangible fixed assets comprising fixtures, fittings, plant and equipment were revalued annually and not depreciated. In addition, certain expenditure in respect of hotel repairs and maintenance was capitalised in tangible fixed assets. These policies have been changed, and all fixtures, fittings, plant and equipment, other than certain integral fixed plant, are now depreciated on a straight line basis over periods of four to fifteen years and expenditure in respect of hotel repairs and maintenance is now charged to the profit and loss account when incurred.

(e) Acquisition of Globana

During 1991, the company acquired the remaining 51% interest in the Globana (France) group of companies (“Globana”). As part of the overall transaction the company received a fee of £10.3 million in respect of the cancellation of the management contract under which it previously managed the hotels owned or leased by Globana. This fee was included in the group's turnover in 1991. The current directors consider that the fee was part of a series of transactions which resulted in the acquisition of the remaining 51% of Globana and, accordingly, that it should have been treated as a reduction in the purchase price and not as income to the group. The accounts have been restated accordingly.

Previously, rationalisation costs incurred in connection with the acquisition of new hotels, comprising principally wages, replacements, stationery and advertising for a period of six months following acquisition, were capitalised as part of the cost of acquisition. This policy has been changed and all such costs are now charged to the profit and loss account when incurred.

(g) Loan Finance Costs

Previously, certain loan finance costs incurred in connection with the acquisition, construction or redevelopment of hotel properties were capitalised in fixed assets. This policy has been changed and all such loan finance costs are now charged to the profit and loss account when incurred.

(h) Deferred Revenue Expenditure

Previously, expenditure incurred in the creation and marketing of new projects was deferred and charged to the profit and loss account over a five year period, commencing when income was first derived. This policy has been changed and all such expenditure is now charged to the profit and loss account when incurred.

(i) Acquisition of the Ashford Group

Shares issued by the company as consideration for the acquisition of Ashford Group Holdings Limited (“Ashford Group”) in September 1989 were recorded in both the company's accounts and the group accounts at their nominal value and no share premium or merger reserve was created. As a result, in the consolidated accounts the consideration was not recorded at its fair value, the effect of which was to reduce the amount of goodwill arising on the acquisition. Adjustments have now been made to record the consideration at its fair value by creating additional share premium in both the company's accounts and the consolidated accounts and to increase the amount of goodwill written off to the consolidated profit and loss account. Furthermore, no accrual was made as at 31 December 1991 for deferred consideration payable in respect of the acquisition of the Ashford Group. Such deferred consideration was dependent on the profits of the companies of the Ashford Group for the year then ended, and the current directors consider that an accrual should have been made. The accounts have been restated accordingly.

(j) Profit on Disposals of Fixed Assets

Previously, profits and losses arising on the disposal of fixed assets carried at valuation were included in the profit and loss account based on the difference between the sales proceeds and depreciated historical cost. In accordance with the requirements of FRS 3 this policy has been changed and such profits and losses are now included based on the difference between the sales proceeds and net carrying amount, whether at valuation or at depreciated historical cost.

(k) Exchange Rates

Previously, the results of overseas subsidiary undertakings were translated into pounds sterling at the rates ruling at the balance sheet date. This policy has changed and such results are now translated at the average rates of exchange for the year.

(l) Sale and Repurchase of Land

During 1991, the group disposed of an interest in land which was subsequently repurchased under an option entered into at the time of the sale contract. The current directors consider that the nature of the agreement was such that a realised profit should not have been recognised and that, rather, the sale proceeds should have been treated as a short term loan. The accounts have been restated accordingly.

(m) Bonuses Capitalized

During 1991, a bonus paid to an executive director of the company was capitalised as part of the cost of the company's investment in a subsidiary undertaking which was acquired from the director in March 1988. In view of the nature of the bonus arrangements, this treatment has been changed and all such bonuses are now charged to the profit and loss account.

(n) Other Changes

Certain other changes have been made in order that the accounts are prepared on a more prudent basis. These include: the accrual of holiday pay, the reversal of an adjustment to goodwill written off in prior years which was released to profit and loss account in 1991 and the deferral of part of the profit recognised on a sale and leaseback transaction where the sale was at above market value.

Reclassifications

(a) Stocks

Certain stocks held by hotels as at 31 December 1991, which were previously included in tangible fixed assets or debtors, have been reclassified to stocks.

Certain non-hotel properties, including the group's head office, which were included in stocks as properties held for development as at 31 December 1991, have been reclassified to tangible fixed assets.

(c) Telephone Revenue

Previously, both revenue and expenditure arising from the use of telephones by guests in the group's United Kingdom hotels were included in net operating costs. This has been changed and the revenues arising in this regard are now included in turnover and the related expenditure remains in net operating costs.

(d) Deferred Tax Write Back

During 1991, £1.7 million was credited to operating costs, being the write back of certain deferred tax provisions no longer required. This amount has now been reclassified to taxation in the profit and loss account.

(e) Finance Lease Creditors

Finance lease creditors amounting to £30.5 million, which were included in other creditors as at 31 December 1991, have been reclassified to bank and other borrowings as obligations under finance leases.

Company Balance Sheet

Certain of the above prior year adjustments and reclassifications, principally those relating to the acquisition of Globana, the acquisition of the Ashford Group and bonuses capitalised, also affect the accounts of the company. In addition, certain loan finance costs and deferred revenue expenditure were previously capitalised into the cost of the company's investment in subsidiary undertakings. Adjustments have been made to restate the accounts of the company for the year ended 31 December 1991 on a basis consistent with the revised accounting policies and treatments adopted by the group in the 1992 accounts. Furthermore, as at 31 December 1991, the balance sheet of the company included cash at bank and in hand amounting to £36.8 million which the current directors consider should have been included in the accounts of certain subsidiary undertakings; accordingly, adjustments have now been made to include such amounts in group balances.

A summary of the effects of the above prior year adjustments and reclassifications on consolidated net assets and on the consolidated profit and loss on ordinary activities before taxation for the year ended 31 December 1991 is set out in Table C11.1.

“Case Study: Queens Moat Houses plc”, reproduced with permission from Queens Moat Houses plc Annual Accounts. Copyright Queens Moat Houses plc.