Chapter 11

Financial Reporting and the Comprehensive Annual Financial Report

Learning objectives

- Recall the minimum requirements for general-purpose external financial statements.

- Identify what must be included in management’s discussion and analysis (MD&A).

- Identify what must be included in required supplementary information (RSI).

- Identify what must be included in a comprehensive annual financial report (CAFR).

Refer to appendix C for an example of MD&A and a statistical section.

Contents of a CAFR

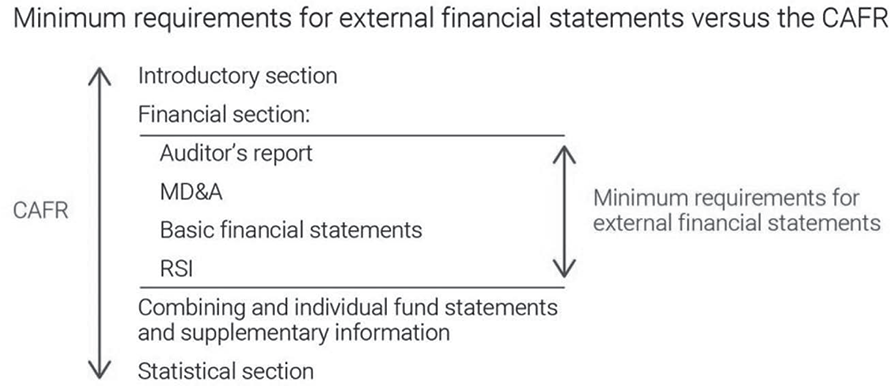

Governments must include certain minimum financial statements, reports, and other information in their external financial reports. Governments are encouraged, however, to go beyond the minimum requirements and to issue a CAFR. What information must be included in the different reports and where does it go? This chapter will try to answer those questions.

The minimum requirements for general-purpose external financial statements

The key objective of financial reporting for governments is accountability. To meet this objective, certain minimum requirements have been established for external financial reports; these requirements are designed to meet the basic needs of a broad group of external users. A government’s general-purpose external financial statements must contain, at minimum, the following items:

- MD&A

- Basic financial statements

- Government-wide financial statements

- Fund financial statements

- Notes to the financial statements

- RSI (other than MD&A)

The relationship among the different elements required for general-purpose financial statements can be seen in the following chart.

Some of these minimum requirements have been discussed in earlier chapters, such as government-wide financial statements and fund financial statements. To recap, the basic financial statements are as follows:

- Government-wide financial statements

- Statement of net position

- Statement of activities

- Fund financial statements

- Governmental funds

- Balance sheet

- Statement of revenues, expenditures, and changes in fund balances

- Proprietary funds

- Statement of net position or balance sheet

- Statement of revenues, expenses, and changes in fund net position

- Statement of cash flows

- Fiduciary funds

- Statement of fiduciary net position

- Statement of changes in fiduciary net position

- Governmental funds

Governments have unique requirements for notes to the financial statements. Items that must be included in the notes are contained in GASB Statement No. 38, Certain Financial Statement Note Disclosures, and in other statements. In addition to the information presented here, it should be noted that paragraph 13, “Disaggregation of Receivable and Payable Balances,” of GASB Statement No. 38 is amended by GASB Statement No. 63, Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position. Additionally, paragraph 8 is amended by GASB Statement No. 68, Accounting and Financial Reporting for Pensions — An Amendment of GASB Statement No. 27.

MD&A and RSI are discussed in succeeding sections of this chapter.

MD&A

MD&A should be presented before the basic financial statements and is part of the RSI that must be presented in the financial statements. (The nature of RSI is discussed in the next section.) It provides an objective and easily readable analysis of the government’s financial activity for the year.

MD&A is based on currently known facts, decisions, and conditions; it must discuss both positive and negative aspects of current-year activity.

Depending on the government, MD&A comprises eight separate elements, as follows:

A discussion of the basic financial statements. The MD&A should focus on the activities of the primary government. The decision to include comments about a government’s component units is a matter of professional judgment and should be based on the significance and relationship of the component unit with the primary government. Any information presented for a component unit should be clearly distinguished from that of the primary government.

The MD&A includes a discussion on the basic financial statements and the relationship between government-wide statements and fund financial statements. This discussion enables readers to understand the differences between financial results reported in the two sets of financial statements.

Condensed comparative data. The MD&A should compare current-year results with those of the prior year. This is the only place in the general-purpose external financial reports where governments are required to present comparative information.

An analysis of the government’s overall financial position and results of operations. The MD&A discusses the overall financial position and results of operations for the government. This analysis explains why the financial position of the government has either increased or decreased for the year. The analysis should also address the financial activities of both governmental and business-type activities as reported in the government-wide statements.

An analysis of the funds. The MD&A addresses any significant changes in the fund balances or fund net position for the year and comments on any significant restrictions or commitments affecting the availability of fund resources at year-end.

An analysis between the budget to the actual statement or schedule. The MD&A should also analyze any significant variation between the original budget and final budget and between the final budget and actual results for the general fund.

Capital asset and debt activities. A description of significant capital asset and long-term debt activities is also included in the MD&A. This discussion should include any significant commitments, changes in credit ratings, debt limitations that may affect the financing of planned facilities or services, and new debt issuances.

Infrastructure, if applicable. If a government is using the modified approach for certain infrastructure capital assets, the MD&A should discuss any significant changes in assessed condition of eligible infrastructure, how the current assessed condition compares with the level set by the government, and any significant differences in the amount spent to maintain infrastructure from the annual amount estimated to maintain those assets.

Economic conditions and outlook. The MD&A also includes a description of any currently known facts, decisions, or conditions that are expected to have a significant financial effect on the government. Currently known facts would include any items that occurred after year-end but before the date of the auditors’ report. Governments are also encouraged to use charts, graphs, and tables in the MD&A to enhance the understandability of the information.

Items to describe could include the following:

- Changes in tax rates, tax base, or population

- Loss of significant employers

- Settlement of significant lawsuits

- New labor contracts

- Deficit reduction measures

Governments also must provide condensed financial information (from the government-wide statements) comparing the current year with the prior year. Governments are required to report the following condensed government-wide financial information:

- Total assets, distinguishing between capital and other assets

- Total liabilities, distinguishing between long-term liabilities and other liabilities

- Total net position, distinguishing between the three components of net position

- Program revenues by major source

- General revenues by major source

- Total revenues

- Program expenses, at a minimum by function

- Total expenses

- Excess (deficiency) of revenues over expenses

- Contributions

- Special and extraordinary items

- Transfers

- Change in net position

- Ending net position

Knowledge check

- Which statement is correct regarding MD&A?

- It is based on currently known facts, decisions, and conditions and must discuss both positive and negative aspects of the current-year activity.

- Any information presented for a component unit should not be distinguished from that of the primary government.

- MD&A should be presented after the basic financial statements.

- Comparative financial information is not reported in the MD&A.

- Which is not required to be included in a government’s general-purpose external financial statements?

- Government-wide financial statements..

- Fund financial statements.

- Certificate of Achievement for Excellence in Financial Reporting.

- Notes to the financial statements.

RSI (Other than MD&A)

RSI (including MD&A) is unaudited information that a government must present as part of its financial presentation. Auditors are required to perform certain limited procedures on RSI; however, the absence of, or deficiencies in, RSI does not affect the auditor’s opinion on the financial statements. In such cases, the auditor adds information to the audit report describing the situation.

As stated earlier, the MD&A is presented before the basic financial statements. Other RSI is presented after the basic financial statements. Governments may be required to report the following additional items as part of RSI:

Budgetary comparison schedule. Governments must present budgetary comparison schedules for the general fund and each major special revenue fund with a legally adopted annual budget. Governments have the option of including these schedules as part of the fund financial statements as opposed to reporting them as part of RSI.

These schedules must contain a minimum of three columns for each governmental fund reported: original budget, final budget, and actual amounts reported using the budgetary basis of accounting. A variance column may be included to facilitate the comparison of budget amounts and actual amounts; this is not required, however. The budget comparison schedule may be prepared using the same format and terminology of the budget document or using the same format as the statement of revenues, expenditures, and changes in fund balances.

Infrastructure assets. When a government uses the modified approach for certain networks or subsystems of infrastructure, certain information must be disclosed as part of RSI. A schedule must be provided that gives the assessed condition of the infrastructure assets over a period of time. Also, a schedule for the last five years must be provided with the estimated annual amount needed to maintain the assets at the condition level established by the government and the actual amount expensed.

Additional information must be provided about the basis for the condition measurement and the scale used to assess and report condition. The condition level at which the government intends to preserve the infrastructure assets must also be disclosed. Factors that significantly affect trends in the information reported in the required schedules must be disclosed.

Pensions and postemployment benefits other than pensions (OPEB). RSI requirements exist related to pensions and OPEB. These requirements are mainly found in the following GASB statements:

- GASB Statement No. 67, Financial Reporting for Pension Plans — An Amendment of GASB Statement No. 25

- GASB Statement No. 68, Accounting and Financial Reporting for Pensions — An Amendment of GASB Statement No. 27

- GASB Statement No. 73, Accounting and Financial Reporting for Pensions and Related Assets That Are Not Within the Scope of GASB Statement 68, and Amendments to Certain Provisions of GASB Statements 67 and 68

- GASB Statement No. 74, Financial Reporting for Postemployment Benefit Plans Other than Pension Plans

- GASB Statement No.75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

- GASB Statement No. 78, Pensions Provided through Certain Multiple-Employer Defined Benefit Pension Plans

- GASB Statement No. 82, Pension Issues — An Amendment of GASB Statements No. 67, No. 68, and No. 73

Knowledge check

- Which statement is correct regarding RSI?

- When a government uses the modified approach for certain networks or subsystems of infrastructure, certain information must be disclosed as part of RSI.

- RSI requirements do not exist related to pensions and OPEB.

- All RSI is presented before the basic financial statements.

- Budgetary comparison schedules are reported for all governmental funds.

The CAFR

The preceding sections discussed the minimum requirements for general-purpose external financial statements for governments. However, to meet the key financial reporting objectives of accountability, governments are encouraged to go beyond the minimum requirements by preparing a CAFR. The CAFR provides a variety of additional information outside the audited financial statements that is useful in assessing a government’s performance and financial condition.

The Government Finance Officers Association (GFOA) provides guidance on what information should be included in the CAFR. The GFOA also administers an award program (the Certificate of Achievement for Excellence in Financial Reporting) for governments that meet their requirements.

A CAFR consists of at least three sections: introductory, financial, and statistical.

Each section requires certain information and tables. Governments need to present only the information and tables applicable to them. The requirements of the three sections follow.

The introductory section

The introductory section provides an overview of the government’s financial position and results of operations. The following items are included in the introductory section:

- Report cover

- Title page

- Table of contents

- Certificate of Achievement for Excellence in Financial Reporting, if applicable

- List of principal officials

- Organizational chart

- Audit committee letter

- Letter of transmittal

The financial section

The financial section provides the financial statements, RSI, and related notes. The following items are included in the financial section:

- Independent auditor’s report

- MD&A

- Basic financial statements

- RSI (other than MD&A)

- Combining and individual fund presentation and supplementary information

One of the goals of the CAFR is to present information about each individual fund and component unit. Because the basic financial statements present information only on major funds and major component units, the combining statements are where information is reported for funds and component units not reported individually in the basic financial statements. Separate combining statements are needed for any nonmajor governmental funds, nonmajor enterprise funds, internal service funds, fiduciary funds, and nonmajor component units. The combining statements should include a total column that agrees with the related column in the fund financial statements.

The statistical section

The statistical section of the CAFR provides information that is useful in evaluating the economic condition of a government.

GASB Statement No. 44, Economic Condition Reporting: The Statistical Section — An Amendment of NCGA Statement 1, as amended, requires governments to report five categories of statistical information as follows:

- Financial trends

- Net position

- Change in net position

- Fund balances for governmental funds

- Changes in fund balances for governmental funds

- Revenue capacity (This is information about the most significant own-source revenue. If a government has other own-source revenues that are nearly as significant as its largest source, it should consider presenting revenue capacity information for those own-source revenues as well.)

- Revenue base

- Revenue rates

- Principal revenue payers

- Property tax levies and collections (If a government presents revenue capacity information about a property tax.)

- Debt capacity

- Ratios of outstanding debt

- Ratios of general bonded debt

- Direct and overlapping debt

- Debt limits

- Pledged-revenue coverage

- Demographic and economic

- Demographic and economic indicators

- Principal employers

- Operating

- Government employees

- Operating indicators (demand or level of service)

- Capital asset indicators (volume, usage, or nature)

- GASB Statement No. 44 also contains requirements related to operating information reported by pension and OPEB plans in separately issued reports.

Knowledge check

- Which statement is correct regarding the CAFR?

- The IASB provides guidance on what information should be included in the CAFR.

- The statistical section of the CAFR provides information that is useful in evaluating the social condition of a government.

- The CAFR provides a variety of additional information outside the audited financial statements that is useful in assessing a government’s performance and financial condition.

- GASB Statement No. 44 requires governments to report six categories of statistical information.

Other sections

In addition to the three sections included in the CAFR, governments are free to include additional sections. For example, a government might include a single audit section or investment section.

The relationship between the minimum requirements for external financial statements and the CAFR is summarized in the following table.

Summary

Governments are required to include certain minimum information in their external financial reports. The requirements are designed to meet the basic needs of a broad group of external users. At minimum, a government’s general-purpose external financial statements contain MD&A, basic financial statements, and RSI.

Governments are encouraged to go beyond the minimum requirements by preparing a CAFR. The CAFR provides a variety of additional information outside the audited financial statements that is useful in assessing a government’s performance and financial condition. The CAFR has three sections: introductory, financial, and statistical.

Practice questions

Please note that the following practice questions are not required reading material.

- Choose the correct statement concerning a government.

- A government can issue only a CAFR.

- A government can issue its basic financial statements, MD&A, and other RSI without its CAFR.

- Both (a) and (b) are permitted.

- Neither (a) nor (b) is permitted.

- Which is not part of the introductory section of a CAFR?

- Transmittal letter.

- Organizational chart.

- RSI.

- Table of contents.

- Which is part of the financial section of a CAFR?

- Transmittal letter.

- Auditor’s report.

- Computation of overlapping debt.

- Demographic statistics.

- Which is not part of the statistical section of a CAFR?

- List of principal officials.

- Debt capacity information.

- Demographic and economic information.

- Financial trends information.

- Combining financial statements are required in the CAFR when there is more than one fund of which type or category of funds?

- Nonmajor governmental funds.

- Internal service funds.

- Private-purpose trust funds.

- All the above.

- Explain the difference between the minimum requirements for general-purpose external financial reporting and the CAFR. Must a government issue both?

- What should be the focus of the MD&A? Is comparative information required in the MD&A?

- Explain how information about individual funds is presented in the financial reports of a government.