Appendix B

CITY OF CHARLOTTESVILLE — REQUIRED SUPPLEMENTARY INFORMATION

CITY OF CHARLOTTESVILLE, VIRGINIA

NOTE TO REQUIRED SUPPLEMENTARY INFORMATION

FOR THE YEAR ENDED JUNE 30, 2019

1. BUDGETARY ACCOUNTING

Demonstrating compliance with the adopted budget is an important component of a government’s accountability to the public. Many Citizens participate in the process of establishing the annual operating budgets of state and local governments, and have a keen interest in following the actual financial progress of their governments over the course of the year. The City and many other governments revise their original budgets over the course of the year for a variety of reasons. Accordingly. GAAP requires that governments include the original budget with the comparison of final budget and actual results.

Tbe City’s budget process begins in December with the preparation of estimated revenue forecasts. Departmental budget requests are submitted to the City Manager in early January. By early March the Manager’s proposed budget is presented to City Council. A series of City Council work sessions and public hearings are held. The budget is formally adopted by April 15.

An annual operating budget is adopted for the General Fund and the Social Services Fund. Within the General Fund, budgets are legally adopted at the departmental level. The City Manager is authorized to transfer the budget for personnel cost (salaries and fringe benefits) between departments if necessary; however, any other revisions that alter the total expenditures of any department or agency must be approved by City Council. Unexpended appropriations lapse at the end of the fiscal year unless carried over by Council action.

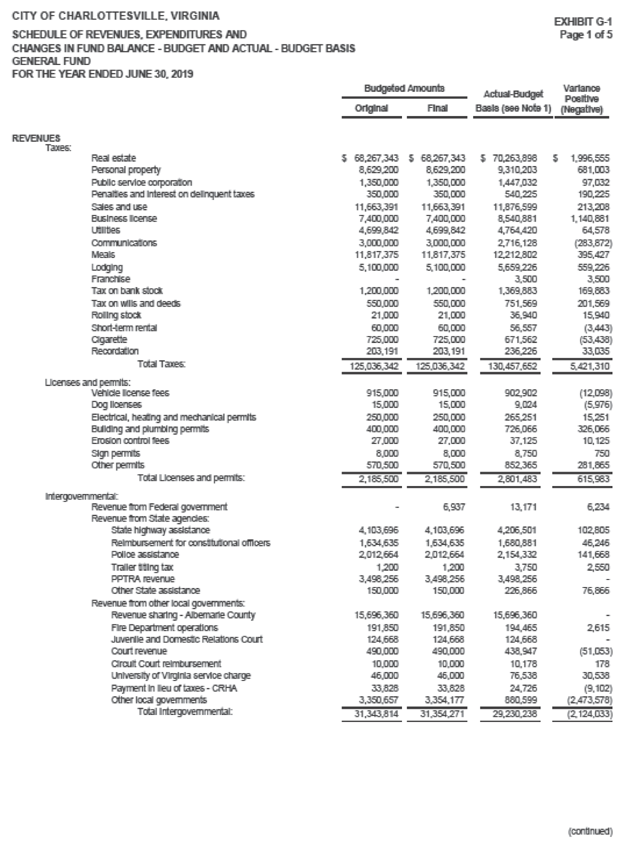

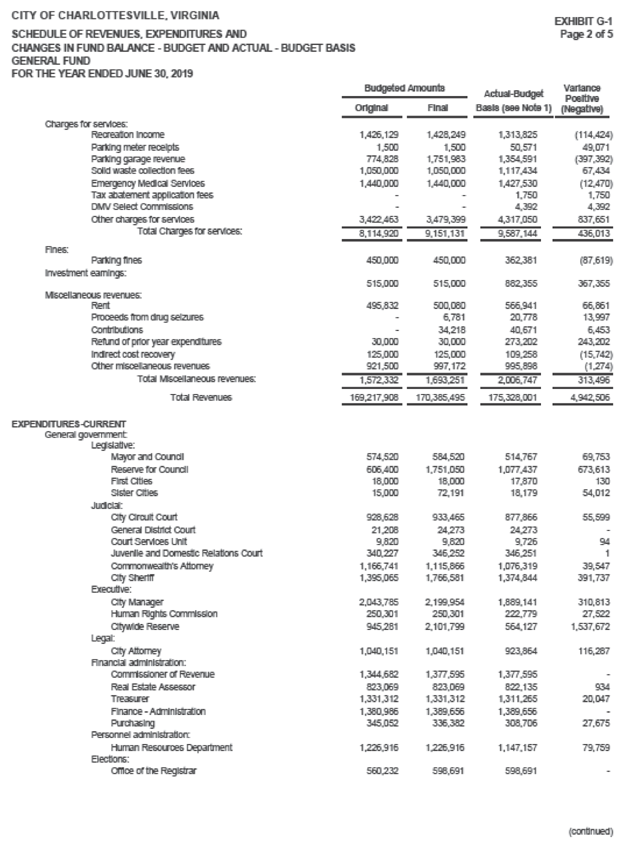

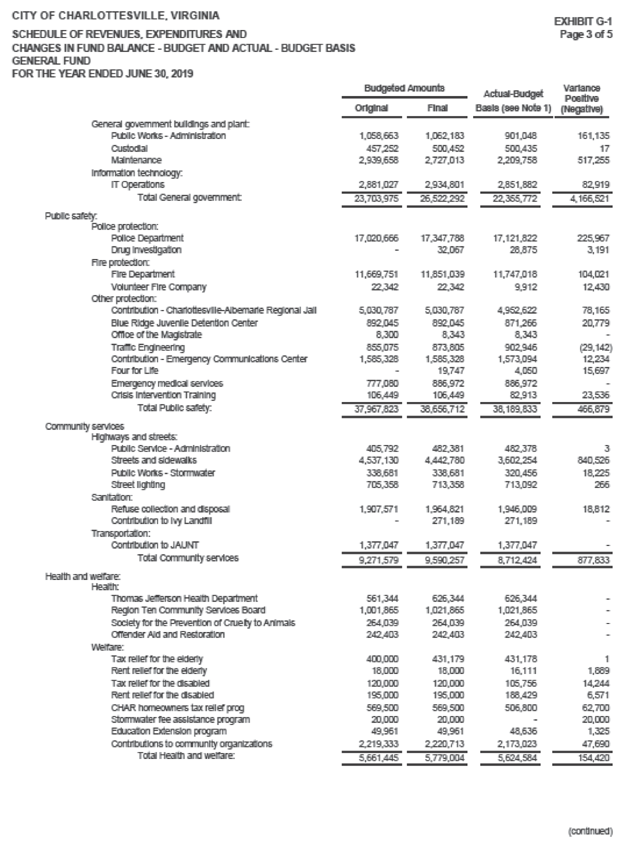

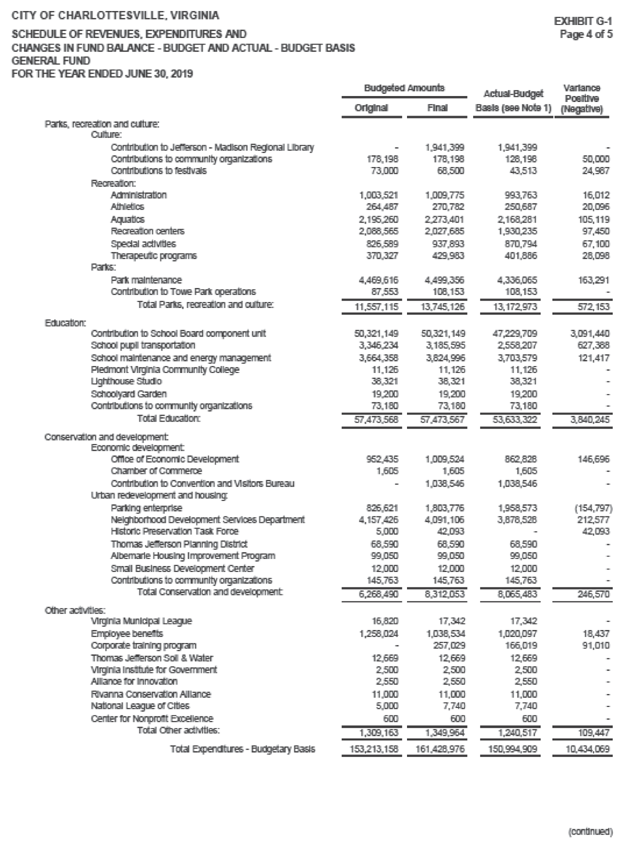

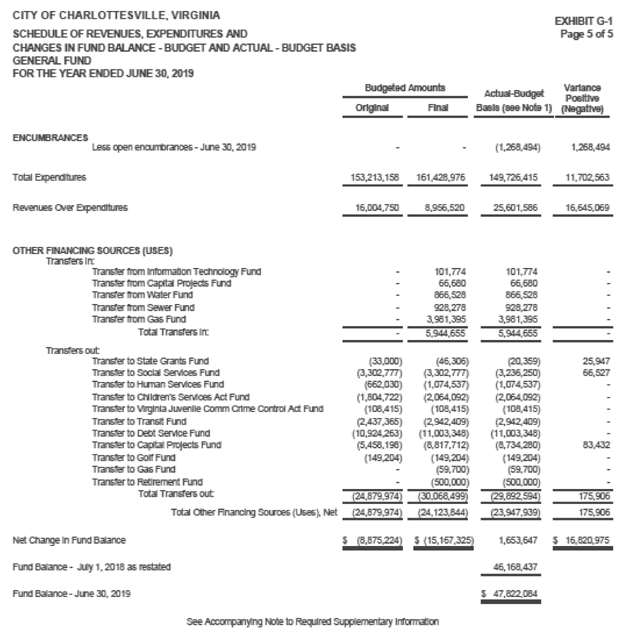

The budgets are integrated into the accounting system and the budgetary data, as presented, in the Required Supplementary Information for all major funds with annual budgets, compares the expenditures with the amended budgets. All budgets are presented on the modified accrual basis of accounting. Accordingly, the Budgetary Comparison Schedules for the General and Social Services Funds present actual expenditures in accordance with GAAP on a basis consistent with legally adopted budgets as amended. Original, final budget and actual revenues and expenditures, including encumbrances, for the General Fund and Social Services Fund are presented on Exhibits G-1 and G-2, respectively. Original budget amounts are the budgets originally adopted by City Council, plus any approved amounts carried over from the previous fiscal year. Final budgets are these amouuts plus any adjustments, through additional appropriations or reductions.