Jay Zarnikau† * The University of Texas at Austin, Austin, TX, United States of America † The University of Texas at Austin and Frontier Associates, Austin, TX, United States of America

Abstract

Retail electricity service can differ with respect to attributes such as reliability of service, environmental impact, value-added services, and payment options. Does a competitive retail sector foster the diverse pricing and service offerings required to satisfy the heterogeneous needs of consumers? This question is explored by comparing product and service offerings in areas of Texas opened to competition to those offered by monopoly providers in areas not opened to retail choice. Competition, supplemented with a state-mandated investment in advanced metering infrastructure (AMI), has led to greater choices of rates and products, consistent with an initial rationale for market reform in Texas.

Keywords

Texas electricity market

retail electricity providers (REPs)

customer choice in electricity

electricity market restructuring

product differentiation

1. Introduction

It is argued throughout this book that the utility business model must change in response to competitive pressures, the growth of distributed self-generation, declining load growth, and the introduction of new technologies providing consumers or their suppliers with greater information and control over energy consumption at the individual household level. New, innovative strategies and operations will be required for financial success, and to meet consumer needs and expectations in tomorrow’s market environment.

A review of the evolving marketing and pricing strategies among retail electric providers (REPs) in the areas of Texas opened to customer choice may provide a glimpse into future business models. These areas of Texas exhibit perhaps the greatest levels of retail competition in North America, and a large investment in AMI infrastructure facilitates many advance technologies for the monitoring and control of energy use. A wide range of competitive strategies have been adopted by these retailers to attract and retain customers, which in turn, impact consumer expectations, environmental goals, load patterns, and demand response capabilities.

This chapter is organized as follows. Section 2 briefly reviews the development of the competitive retail market in Texas. Section 3 discusses pricing. Section 4 provides an overview of product differentiation as a competitive strategy, while Section 5 examines the products and services now offered in areas of Texas opened to competition and draws comparisons to offerings in areas of the state that continue to be served by monopoly providers. Observations are provided in Section 6, followed by the chapter’s conclusions.

2. Background on retail customer choice in texas

A key impetus for the introduction of retail customer choice in Texas was the belief that competition would provide greater pricing and service options to energy consumers and foster the introduction of new, beneficial technologies.1 This section discusses the evolution of the competitive market structure, market concentration among retailers, and key regulatory requirements impacting the market.

2.1. Establishment of a Market Structure

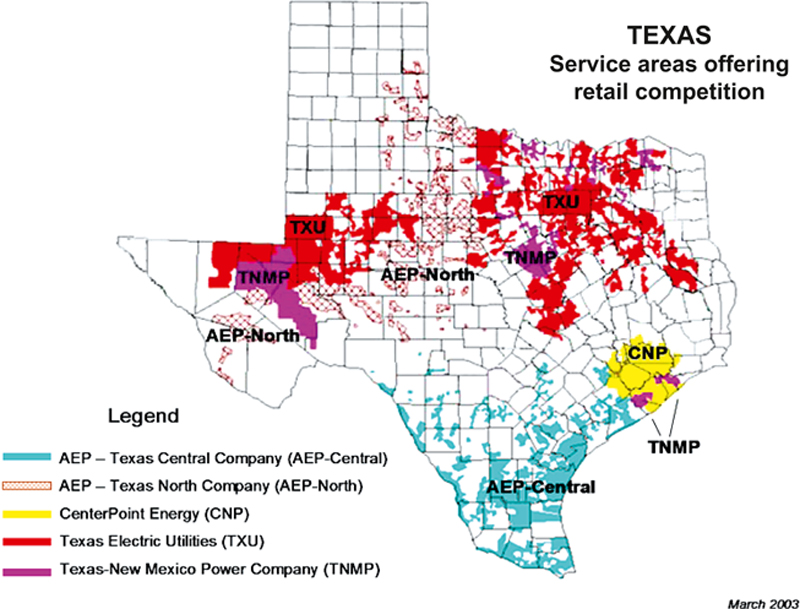

Efforts to introduce competition into the retail sector of the state’s electricity market were launched in Jun. 1999, with the passage of Senate Bill 7 (SB 7) by the Texas Legislature. This act allowed retail competition in the service areas of the investor-owned electric utilities within the Electric Reliability Council of Texas (ERCOT) power region, as identified in Fig. 8.1,2 on a commercial basis beginning Jan. 1, 2002. New entrants were permitted to enter the retail market, and compete with retail arms of five former vertically integrated monopoly utility providers. Efforts to introduce competition into Texas’ retail electricity markets are detailed in Zarnikau (2005), Adib and Zarnikau (2006), and Wood and Gülen (2009).

The introduction of new pricing plans and service options got off to a very slow start. In the early 2000s, consumers were presented with choices among retailers, but much of the competition focused on price and the reputation of the retailer. An exception was green power with higher renewable energy content, as offered by a few retailers.

The slow introduction to innovative service offerings may be traced to early problems with ERCOT’s implementation of systems to track and disseminate information pertaining to the assignment of account numbers to new premises, customer switching, billing data, and disconnection and reconnection of service. The absence of AMI also posed an impediment to the introduction of certain services. It took some time before retail market rules and systems could stabilize, further slowing innovation. Also, rapid increases in prices in the areas opened to competition from 2005 to 2008 led to uncertainties over the fate of the competitive market structure. Thus during the early years of the retail market, retailers and the market in general, were focused on providing basic services to consumers.

After a very difficult transition period, placing ERCOT into the role of Central Registration Agent succeeded in establishing trust in the retail market and reducing potential barriers to entry for REPs interested in competing in the ERCOT market. On Jan. 1, 2007, price-to-beat (PTB) price constraints3 upon the incumbent utility retail providers expired fully, removing any regulatory oversight over the prices offered by the REPs affiliated with the traditional utility providers, and leading to a reduction in average prices (Kang and Zarnikau, 2009; Swadley and Yucel, 2011). An increase in the production of natural gas through hydraulic fracturing (also known as “fracking”) led to lower prices for the ERCOT market’s marginal fuel source. This led to lower wholesale electricity prices and a perception that the retail market was fulfilling its promise. In recent years, Texas has been ranked as the most successful restructured electricity market in North America (DEFG, 2015).

2.2. Market Share Among Retailers

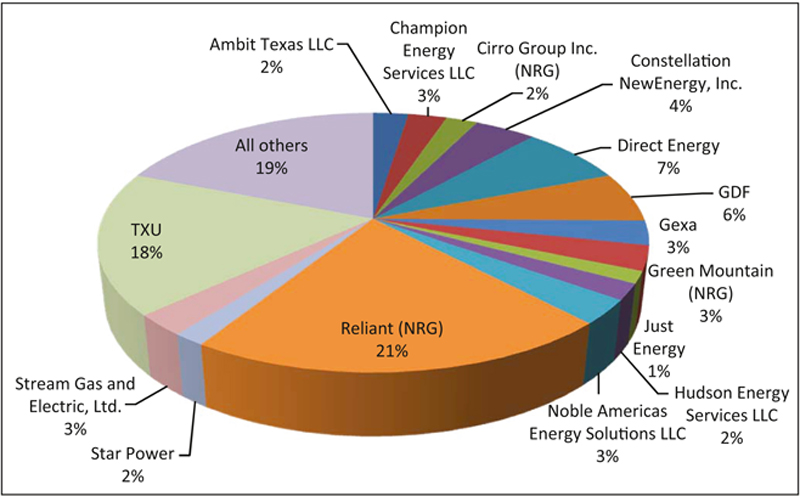

In 2015 over 100 REPs competed to serve 5,955,761 residential customers, 1,034,600 commercial customers, and 3,848 industrial energy consumers (PUCT, 2015). The market share of the largest REPs to residential and commercial energy consumers is reported in Fig. 8.2.4 Reliant Energy (the successor to Houston Lighting and Power Company, and now a subsidiary of NRG) and TXU (the successor to TU Electric) together account for nearly 40% of the market share of sales to residential and commercial energy consumers. NRG’s market share is about 26%, if its sales through Reliant Energy, Green Mountain, and Cirro are combined. Direct Energy’s 7% share of the nonindustrial market is partly the result of its purchase of AEP-Texas’ retail operations.5

Figure 8.2Approximate residential and commercial market share of REPs based on renewable energy credit requirements.(Source: Calculated from PUCT Project No. 27706: ERCOT’s Annual Report on the Texas Renewable Energy Credit Trading Program.)

2.3. Other Regulatory and Market Factors Impacting the Retail Market

Other actions shaping the retail market include the establishment of a renewable energy portfolio standard and credit trading program, establishment of the nation’s first energy efficiency portfolio standard, and investment in AMI systems.

The State’s renewable energy policies affect REPs by setting a minimum “greenness” or renewable energy content to the electricity sold. The restructuring legislation, SB 7, set initial targets. SB 20, in the 2005 legislative session increased Texas’ goal for renewable energy to 5,880 MW in 2015 and set a “voluntary” target of 10,000 MW of wind power for 2025, which Texas has already met. Under the program, each load-serving entity must have Renewable Energy Credits (RECs) equal to its share of the renewable energy goals in effect during a given year (Zarnikau, 2011). ERCOT calculates each load-serving entity’s share of the statewide goal based on each entity’s energy sales. Industrial energy consumers may opt out of the program and have their load excluded from the calculations used to determine REC requirements. As a result of this mandate, all electricity is presumed to possess some minimum renewable energy content of about 5%.6

SB 7 also required each investor-owned electric utility [which, within the areas opened to competition, was a transmission and distribution utility (TDU)] to administer programs designed to reduce the energy demand of the ultimate retail energy consumers in their distribution service areas. Minimum energy efficiency goals have been gradually increased over time (Zarnikau et al., 2015). REPs or energy services companies (ESCOs) provide energy efficiency programs and services to consumers, with funds administered by the TDUs.7 The programs have been extremely successful in meeting the state’s policy goals for energy efficiency, although Texas’ goals are modest, in comparison with those adopted in some other US states.

Finally, advanced metering systems have been implemented by each of the investor-owned TDUs. These systems can provide a variety of benefits to REPs and consumers in the competitive retail market. ERCOT’s financial settlement system now uses actual hourly consumption data, rather than statistical profiles. Thus the impact on utility or system costs of actions taken by consumers to shape their load patterns, or respond to price signals or curtailment requests, can be recognized in ERCOT’s settlement system. Hourly consumption data can be used to design new programs and services for the mutual benefit of consumers, REPs, and the market in general.

3. Pricing

There are striking differences between pricing in competitive retail markets versus regulated monopoly markets, with respect to the frequency of price changes, the factors affecting prices, and the variety of pricing plans available to consumers.

Utilities subject to regulation or oversight by a city council change prices infrequently. It is not unusual for the same prices to be in effect for many months or years. In contrast, retailers in Texas’ competitive market often change the prices quoted to larger consumers, on a daily basis, and the prices quoted to residential consumers change on a weekly or monthly basis. While components of the price associated with the recovery of regulated transmission and distribution costs and regulatory fees may change infrequently, the generation component is always changing in response to changes in natural gas prices.

Under traditional regulation, the generation charge or fuel factor reflects changes in the utilities’ average cost of a broad mix of fuels in order to ensure that the utility has a reasonable opportunity to recover its reasonable and necessary prudently incurred fuel costs. In contrast, retail prices in the restructured ERCOT market follow marginal wholesale power costs closely. These, in turn, tend to follow natural gas prices (Woo and Zarnikau, 2009).

As discussed further in this chapter, the prices quoted in the competitive market may be fixed over some contract duration or may change in concert with market conditions. Dynamic prices tend to enhance economic efficiency by matching prices better to operating costs on a short-term—sometimes, hourly—basis. The indexed prices available in the competitive market adjust prices for changing market conditions—typically on a monthly basis.

The 1- or 2-year fixed price contracts commonly used to serve residential and small commercial consumers are priced to reflect market conditions at the time the retailer quotes the price. The retailer may hedge a portion of the contracted load via electricity or natural gas futures markets. While lacking any short-run price signals to consumers, the resulting prices may nonetheless yield some improvement in economic efficiency over the fixed-price tariffs designed in ratemaking processes by regulatory agencies, with their regulatory lag and use of average embedded costs.

Arguably, pricing in a competitive market leads to efficiency gains by better matching prices to the short-run marginal cost of generating electricity. Regulatory true-ups are avoided, at least for the generation or fuel component of the final price.

A consumers’ ability to select from a larger menu of prices also represents an efficiency gain. While any individual retailer may offer a limited set of pricing plans, a consumer’s ability to select from a large set of retailers, all offering different prices and pricing plans, provides the consumer with a large set of choices.

4. Product differentiation as a competitive strategy

It is commonly argued that, in a competitive market, product differentiation or value-added services are needed to attract/retain customers, when price competition is limited. For example, see the broader discussion in Makadok and Ross (2013) about how strategic interactions manifested via product differentiation impact industry structure. Furthermore, dynamic pricing or technologies could make the consumers’ load shape more attractive to the retailer, thereby reducing peak generation costs to the mutual benefit of the retailer and consumer.

Previous studies have explored competitive strategies among retailers in electricity markets. Based on survey results from Ontario, Walsh and Sanderson (2008) conclude that a hybrid strategy involving cost, service quality, enhanced communications, and unbundled services, should be adopted when marketing to commercial customers. Stanton et al. (2001) interviewed retailers in Australia and found key elements of their marketing programs to include competitive pricing, price flexibility, price monitoring of competitors, price matching, price leadership, customer service, understanding customer requirements, sales expertise, marketing expertise, and technical assistance. Giulietti et al. (2014) conclude that high search costs (the cost of acquiring information pertaining to offers from competing retailers) inhibit competition. Slim margins and fierce competition among retailers dominate some segments in Norway’s market, while monopolistic behavior can be found in other segments (Fehr and Hansen, 2010).

Goett et al. (2000) report the retail service attributes of most value to commercial energy consumers and found that consumers favored local providers and free energy audits, distrusted sign-up bonuses, preferred retailers to make charitable contributions, generally preferred time-of-use rates to real-time pricing, would rather deal with a human customer service person than a voice message system, and had a diversity of preferences regarding generation mix. Woo et al. (2014) describe common rate and service offerings, with a particular focus on exploring the meaning and implications of product differentiation, in the context of electricity supply. They conclude that “applying product differentiation to electricity can greatly induce end-users to more effectively and efficiently satisfy their demand, and to do so in an environmentally friendly way” (Woo et al., 2014).

Many prior studies have focused on the marketing of green energy in restructured markets. Rundle-Thiele et al. (2008) provide an extensive literature survey of strategies involving the marketing of renewable energy. Using focus groups and interviews, Paladino and Pandit (2012) explore the challenges in marketing renewable energy in Australia’s competitive market. The role of consumer preferences in the German market, with its high FiT, was explored by Menges (2003). Fuchs and Arentsen (2002) discuss options for breaking consumer trajectories favoring nonrenewable energy. Kim (2013) finds that incumbent utilities exposed to retail competition are less likely to compete effectively on a “green” dimension.

In the ERCOT market, many of same competitive strategies adopted in other competitive electricity markets are emerging, including product differentiation, the introduction of broad pricing options, and a focus on value-added services. Slim margins in a competitive retail market lead to a need for product differentiation, in order to capture higher margins associated with a differentiated and more unique product. There are limits to price competition because of the small margins and many costs (eg, transmission and distribution delivery charges and, to some degree, market-based generation costs) are outside the control of the REP. Such costs are likely to be common across all REPs, so the differentiation based on products or value-added services, discussed in the following section, starts past this “common base.”

5. Product and service differentiation in the competitive ERCOT retail market

It has taken the competitive retailers in the Texas market a while to find their role and develop their marketing strategies. But, product differentiation seems to be picking up, particularly following the completion of AMI deployments in the competitive areas. The first wave of product differentiation through green pricing programs with renewable energy content above that required by the state’s goal for renewable energy, may have run its course. The retail sector is now in a second wave of product differentiation, featuring AMI-enabled dynamic pricing, free nights/free weekend time-of-use rate programs, dashboards and other software to provide consumers with information pertaining to their energy use, prepay electricity programs, smart thermostats, assistance with other utilities (eg, telephone service) and trades (eg, HVAC, plumbing, and home security), and links to charities.

5.1. Programs, Plans, and Technologies Offered by REPs

The PUCT’s Power to Choose website8 provides the pricing plans offered in competitive areas, which can be compared with the tariffs of the state’s regulated utilities. Inspection of the Power to Choose website for a zip code in Houston (within the CenterPoint service area) suggests availability of the following service options:

• Overall, 322 rate options with a purported range of prices from 5.6 to 14.5 cents/kWh, at a usage level of 1000 kWh/month.

• 52 REPs are offering residential service (although many of the REPs have affiliate relationships with other REPs).

• 23 Prepay plans from 6 REPs (Direct Energy, Frontier Utilities, Penstar Power, Zip Energy, Hino Electric, and Breeze Energy)

• Time-of-Use plans: seven from four REPs (Direct Energy, Champion Energy Services, TruSmart Energy, Clearview Energy). These do not apparently include the “free nights” or “free weekend” plans.

• Fixed rate plans: 268 plans. Available from nearly all of the REPs.

• Variable rate plans: 47 plans from 27 REPs.

• Indexed (market rate) plans: seven plans from three REPs.

• 100% renewable plans: 81 offerings by 28 REPs.

How many plans are offered by the largest REPs? TXU offers 5, Reliant offers 10, and Direct Energy lists 11 plans.

The number and range of plans offered in the competitive market clearly exceeds what is available in areas not exposed to retail competition. Table 8.1 suggests that the residential consumers in the Xcel and Southwestern Electric Power Company service areas within Texas are offered no rate choices. Rate options from the other two investor-owned utilities serving parts of Texas are limited. As suggested in Table 8.2, more rate choices are offered by the state’s two largest municipal systems, yet the numbers and diversity of choices continue to pale, in comparison to those offered in the competitive market.

Table 8.1

Residential Rate Offerings by Vertically Integrated Investor-Owned Utilities Not Exposed to Retail Competition

Utility

Rates offered

Structure and notes

Entergy, Texas

Residential Service (RS)

Residential Service Time-of-Day (RS-TOD)

Time of day price differences

El Paso Electric Company, Texas

Schedule No. 1 Residential Service

Seasonally differentiated energy charge

Alternative Time-of-Use rate

Time of day price differences

Low Income Rider

Customer charge is removed from Schedule No. 1 rate

Qualified Water Conservation Air Cooling Rider

Not available to new customers

Off-Peak Water Heating Rider

Not available to new customers

Xcel, Texas (Southwestern Public Service Company)

Residential Service

Seasonal price differences

Southwestern Electric Power Company (AEP)

Residential Service (RS)

Seasonal price differences

Source: Compiled by the authors.

Table 8.2

Residential Rate and Service Offerings by Vertically Integrated Municipal Utilities Not Exposed to Retail Competition

Utility

Rates/services offered

Structure and notes

Austin Energy

Residential Inside City Limits

Five inclining blocks

Residential Outside City Limits

Three inclining blocks

Time-of-Use Option

Three time-of-day periods, two seasons

Green Choice Option

Residential Solar

Bill credit for solar energy generation

Payment Assistance

Energy Efficiency Rebates

Extensive set of programs

Green Building

Promotes resource conservation in new construction

Plug-In Electric Vehicles

Provides incentives for charging stations

CPS Energy, San Antonio

Residential Service Tariff

Two-tier inclining block rate

Energy Efficiency Rebates

Extensive set of programs

Energy Portal

Weatherization Assistance

Affordability Discounts

Payment Options

Residential Demand Response Programs

Source: Compiled by the authors.

ERCOT’s annual survey of load-serving entities may additionally be used to provide insights into the popularity of various types of programs and technologies, in both the competitive and noncompetitive areas served by ERCOT. Between Jun. 2013 and Sep. 2014, there was a dramatic increase in the number of consumers reported to be enrolled in peak rebate programs (ie, programs offering a rebate for demand reduction during high price periods announced by the REP). Yet, due to a dearth of price spikes in 2014, it is unclear how many consumers will actively agree to curtail during a spike in wholesale prices. Participation in time-of-use rate programs is similarly strong. Perhaps surprisingly, over 1000 residential consumers are on real-time pricing, a pricing structure more commonly applied to large industrial energy consumers (Table 8.3).

Table 8.3

Summary of Results From ERCOT’s Demand Response Surveys

The value-added services offered by the largest REPs were inspected by visiting each REP’s website. As suggested by Table 8.4, a large variety of services are offered, including home security, frequent flier miles, energy information and feedback, carbon offset credits, and opportunities to make charitable donations. Nonetheless, some of the larger REPs appear to be focused on basic electricity service, that is, a no-frills commodity price.

Table 8.4

Value-Added Services Offered by Largest REPs in Texas

REP

Product/service

Description from website

TXU Energy

MyEnergy Dashboard

Graphs and tools show how and when energy is used to facilitate lifestyle changes and lower costs

iThermostat

Allows management of a home’s energy usage anywhere, anytime

Personal Energy Advisor

Creates a personalized checklist of tools, tips, projects, and videos to help a customer save energy and money

Energy Management Alerts

Sends timely email alerts to help manage electricity usage and costs

TXU Complete ConnectSM

Assistance in finding cable, Internet, and phone service providers

MyHome ProtectSM

Warranty service covering common home repairs and replacements

Surge ProtectSM

Two surge protection products with guaranteed warranty service for repairs or replacements due to lightning strikes or power surges

Direct Energy

Benjamin Franklin Plumbers

Plumbing services

Home Warranty of America

Whole home warranty protection

One Hour Air Conditioning and Heating

Mister Sparky

Electricians

Nest thermostats

Get a Nest Learning Thermostat™ at no additional charge (a $249 value) with a Comfort & Control plan

Gexa Energy

Frequent flier miles

American Airlines AAdvantage members get a low fixed electricity charge, as well as 15,000 bonus miles for signing up; 2 miles for every dollar spent on the energy charge portion of electricity bill

MD Anderson Children’s Art Project

The MD Anderson Children’s Art Project receives $25 when customer selects a Gexa Energy electricity plan

Green Mountain Energy

SolarSPARC™ (Smart People Accelerating Renewable Change)

Green Mountain makes a monthly contribution for each customer to build new solar projects. Plus, customer gets an annual solar credit that grows over time

Nest thermostats

Pollution Free™ Electric Vehicle

Special rate for EV drivers

Renewable Rewards buy-back program

Receive a credit for any excess energy a customer’s distributed energy system exports to the grid

Carbon Offsets

Calculates carbon footprint, and facilitates purchase of carbon credits

Cirro Energy

All that is mentioned is smart money-saving plans, online and mobile account management, convenient payment options, local customer service, plus some of the lowest fixed rates available

Champion Energy

Smart Track™

Detailed usage information, giving consumer the power to track and manage electricity usage

Get Connected

Connect electricity, phone, cable, Internet, and security packages all with one phone call

Home security

Partnership with Alliance Security

Discount on LED light bulbs

Constellation NewEnergy, Inc (StarTexPower, a Constellation Company serves Texas Area)

myAccount Dashboard

Manage electricity account by viewing current balance and bill history from a computer or smart phone

Community grant programs

Investing energy dollars back into the communities StarTex serve through charitable donations and volunteerism

Rewarding loyalty programs

Ambit Texas LLC

Ambit Home Services

Two forms of coverage: (1) Ambit AC/Heat Shield for heating and cooling systems; (2) Ambit Surge Protection for lightning or power surge protection

New customer advantage

Travel voucher gift for new customers

Power Payback™

Ambit gives advanced notice of an approaching period of extreme demand by email or phone. If customers reduce usage during designated time, Ambit offers a bill credit of $1.00 for every kilowatt-hour saved

Free Energy

Opportunity to earn Free Energy if one refers 15 customers to Ambit Energy

Travel Rewards

Earn one travel point for every kilowatt-hour used, or 10 points for every therm/ccf used. Referring friends can earn up to 45,000 points. Points can be redeemed for travel packages listed in the website

Just Energy

SmartStat

A high tech thermostat has Wi-Fi, mobile apps, easy web portal, live weather, and color screen. And SmartStat’s Home IQ™ lets you see your monthly estimated energy savings, monthly heating and cooling summaries, details on performance influencing factors such as the weather and average set point, HVAC runtime reports, and more

Hudson Energy Services LLC

All that is mentioned are fixed or variable or mixed rates

Noble Americas Energy Solutions

Nothing noteworthy

All that is mentioned is different pricing options, including different fixed price and index price options. Green energy is also available

Reliant (an NRG company)

Home Solutions®

Services include home generators installation, AC/Heat Protect, AC Tune-Up, Surge Protect, plumbing service, electric line with surge protect, and air filter delivery services

BabyPower 12 plan

$100 donation to March of Dimes, $100 bill credit, a low price for 12 months, and customer service and support

15,000 airline miles for signing up and 500 bonus miles each month for the next 24 months; a low electricity price, and innovative tools to manage electricity usage

Heart Power plan

A $100 donation to the American Heart Association. Plus, a $100 bill credit, 12 month contract, and customer service and support

The Reliant Texans plan

A J.J. Watt jersey, a $25 donation split between the Justin J. Watt Foundation and the Houston Texans Foundation, and an invitation to a Houston Texans autograph session

Reliant Rockets Secure Advantage 12

An autographed Patrick Beverley jersey; invitation to a Rockets autograph session; electricity plan for 12 months; and customer service and support

The Reliant Cowboys Secure Advantage plan

A term electricity plan, plus: a football autographed by Jason Witten; an invitation to a Cowboys autograph session and customer service and support

Reliant Rangers Secure Advantage 12 plan

Provides an autographed Texas Rangers baseball

Reliant Learn & Conserve 24 plan

Free Nest Learning Thermostat™

Reliant Sweet Deal plan

13 months of electricity for the price of 12

Stream Gas and Electric Ltd

Free Energy Program

Enroll 15 friends and earn free energy credits

GDF (ThinkEnergy)

Energy Education

ThinkEnergy provides energy saving education with blogs and tips online

Source: Compiled by the authors.

A review of the websites of the four investor-owned utilities serving parts of Texas not opened to competition suggest limited availability of value-added services, other than energy information programs. Regulation by the PUCT may make it difficult for these utilities to offer “creative” services.

Residential consumers served by CPS Energy and Austin Energy—the state’s two largest municipal utility systems—enjoy a fairly wide range of value-added services to foster their sustainability goals. CPS Energy offers Nest thermostats and an energy portal. Austin Energy established the nation’s first green building program. Both utilities offer extensive energy efficiency programs. However, the range of choices and the flexibility of differentially targeted attributes built in those choices is still quite limited in these monopoly municipal utility service areas, compared to the competitive retail parts in the ERCOT market served by multiple competitive retailers.

The net impact of all these pricing strategies, marketing programs, and technologies promoted by the REPs upon the ERCOT market is unclear. As noted in chapter by Levin and Cavanagh and in the Introduction by Sioshansi, many of the contracts offered by REPs have minimum-usage charges which might discourage consumers from undertaking energy efficiency measures (Levin, 2015). With minimum usage charges, consumers cannot achieve cost savings by undertaking measures, which would reduce their consumption below the minimum usage threshold. It would be interesting for future research to explore the implications of such pricing strategies for environmental impacts and for investments in distributed renewable energy systems. On the other hand, the prepay electricity programs offered in the competitive market can have a very large conservation impact (Zarnikau, 2014). Many REPs offer technologies designed to enable consumers to save energy. Programs facilitating consumer response to price signals in the competitive areas have led to a significant reduction in peak demand (Frontier Associates LLC, 2014).

6. Competitive pressures and the response by the retail sector

Even though it has been over a decade since the introduction of retail choice in ERCOT, the transformation of the ERCOT retail market is still in its early phases. The marketplace is vigorous, with many old and new suppliers and customers switching between them. But the market structure has yet to gel in any sort of equilibrium. New firms are entering the market routinely, even as existing players merge and consolidate. New products are being introduced rapidly, even though positioning (of firms) on existing products has not been established. It is not clear how long this level of flux can be sustained before the market structure crystallizes somewhat.

Two competing factors push in different directions: (1) demand growth and changing demographics in the ERCOT market provide opportunities for retailers to build position continuously, but (2) a relatively high rate of customer switching creates costs and uncertainties for retailers, affording little time to establish position. Technological change, in particular the advent of distributed generation and home energy management systems, further magnifies the challenges faced by retailers in establishing a market position, in the face of a growing market and competition.

Amid this apparent tumult, though, some intended benefits from retail competition in the ERCOT market seem to have been served already clearly. These include: (1) more product choice for customers and (2) higher competition, at least as indicated by the simplistic metric of the number of firms operating, in comparison to the regulated parts of the ERCOT market.

The picture is not clear with respect to competitive pricing. When competition in commodity markets heats up, focus on market segmentation and differentiation starts to take over, leading to product and service diversity and muddling of the price waters. This is a rich area for empirical research, requiring careful control for not only resource factors (such as fuel price or congestion) affecting prices, but also for strategic factors, such as how the features of the offered products and services impact prices. The diversity in the offerings takes away the pure commodity nature of the offering, potentially allowing for long term firm-level strategies geared toward commanding higher margins. While empirical proof is weak, it appears as though price competitiveness has improved in the parts of ERCOT opened to retail choice. Perhaps this is because the vigorous nature of firm-level competition that has put customers at the center of value creation in the retail business.

There are early signs of both proactive and reactive innovation by retailers in the ERCOT market. This is encouraging, as innovation is central to value creation, for both suppliers and customers. Incentives for proactive innovation are driven by shifting (and growing) the customer base and by technological change, inducing retailers to introduce new products and services, in anticipation of demand.

Reactive innovation—or to put bluntly, imitation—involves observing the behavior of competitors and that of customers, in order to mold product offerings and firm strategy. It is widely recognized in the innovation literature that imitation is the quintessential mechanism for reaping and spreading the benefits of innovation.

Transparency in the overall market is critical in fueling both proactive and reactive innovation. In ERCOT’s retail market, www.powertochoose.org has been the central lynchpin for creating and enhancing transparency.

A related but less appreciated aspect outside the REP circles is the role that advanced data analytics is beginning to play in helping firms chart their product strategy. Such analytics range from tracking customer switching behavior, to analyzing product offerings of competitors, to predicting the impact of weather on load to manage wholesale supply.

These stylistic observations about REPs’ strategic behavior are in line with the remark of Steil et al. (2002) on Schumpeter’s deep insights around the interlinks between competition and innovation: “…competition under capitalism is…competition through innovation and then trial by actual experience.”

The deepest impacts of Texas’s retail market transformation are yet to be seen, although some recent events offer some insights into what may be coming. In particular, the conditions ripe for the introduction of disruptive market constructs, products, and services in the ERCOT market may be forming. This aspect adds an entirely new dimension to the more common but narrow focus around price competitiveness, when analyzing the benefits retail competition.

Two examples illustrate this point. First, there have been discussions within ERCOT about creating market incentives for aggregating distributed energy resources (DERs). Under the initial concepts being discussed, DERs would be allowed to earn a broad, (locationally) averaged wholesale price (GTM 2015). This could be a significant incentive for DERs, especially in locations with high wholesale prices. This development is interesting, given that, unlike many other markets in the United States, Texas has not had a strong policy support for distributed generation. Examined from that backdrop, it is impressive that largely market-driven forces are increasingly engendering broader structural changes within the market.9

This is especially noteworthy, given that low natural gas prices have put downward pressure on incentives to build more capacity in Texas, even though the peak supply situation is expected to be quite difficult over the next decade or so (ERCOT, 2014). Here, Texas has benefited by being on the sidelines, as the solar story has played out over the last decade elsewhere in the United States (especially, California, New Jersey, and Arizona) and the world (Germany, Japan, China, among others). Price and quality for solar products have reached very compelling points—these are precisely the most critical ingredients needed for rapid take up in market-driven retail areas like Texas.

Second, there are indications about the entry of disruptive retail products. An example of that is the recent product launch by a partnership between MP2 Energy and SolarCity. This product, initially targeted toward solar homeowners in the Dallas-Fort Worth area, effectively offers net metering to solar customers (SolarCity 2015). It is too early to comment on how good the product will be for the customers, or the companies offering them, but this product essentially solves a hitherto major barrier for solar customers in Texas, namely the lack of statewide net metering, and it does so based on purely market incentives (as perceived by MP2 Energy and SolarCity). Nearly all other US solar markets have required some form of ongoing legislative and/or regulatory intervention to resolve this issue, often engendering acrimonious mudslinging among utilities, solar companies, and consumer groups. That seems to have been avoided in the ERCOT market, at least for the moment, thanks to the underlying incentives in the fiercely competitive retail market in ERCOT.

These two examples suggest that the competitive market design offers tremendous incentives for rapid deployment of disruptive products and services, once certain technical and price points are met.

7. Conclusions

If electric utilities are subjected to greater competitive pressures in the future, retail business of utilities might look more like the REPs operating in the areas of Texas opened to competition. Energy charges would reflect better the cost of the marginal generation fuel and would change as market conditions changed. Peak rebate programs and other forms of dynamic pricing would become more widespread. Electricity retailers would expand price and service options to meet diverse consumer needs better.

While competition leads retailers to introduce new products and services to attract and retain customers, it is instructive to note that the market structure and environment in Texas has been shaped by government regulation, to a large degree. A Central Registration function was assigned to the system operator. Rules and protocols were developed by the PUCT and ERCOT. Goals for renewable energy and energy efficiency were established by the state government, which also ordered the deployment of AMI and competitive renewable energy zones (CREZ) infrastructure.

Some concluding thoughts on the overall desirability of retail choice in electricity markets, in particular in the presence of externalities (such as harmful emissions), are in order. Specifically, should it not be expected that in retail choice markets, over time, both suppliers and consumers will focus largely on lowest cost products (in dollars per kilowatt-hour), thereby precluding the opportunity to deploy environmentally friendly generation and consumption of electricity? Indeed, there are analysts who, in anticipation of such “race to the bottom” outcomes in retail choice environments, suggest that a better option is to retain the conventional regulated rate-of-return (ROR) model with a strong interventionist regulator that can mandate the level of “greenness” in the mix of electricity sold. Such arguments are tenuous for the following reasons:

• First, as is now well established, the conventional ROR model creates a number of perverse incentives for the regulated utilities that might oppose and scuttle socially desirable efforts to change the electricity generation–consumption system, if such changes would hurt the utilities’ business interests. Strong regulators may well be able to deal with such utilities. However, from time to time, regulators themselves are prone to regulatory capture. Maintaining a strong independent regulatory regime that constantly works only in the public interest requires constant public participation, vigilance, and due diligence.

• Second, as argued earlier, there is no reason to expect that retail-choice electricity markets will necessarily degenerate into markets where the sole focus is on lowest prices.10 Several examples of how REPs in Texas are trying to position and differentiate themselves from the rest were provided earlier. Fundamental forces will continue to drive such brand positioning, refinement, and differentiation. The suite of customer-oriented technologies (solar PV, electric vehicles, smart thermostats, home energy management systems, etc.) that are deepening market reach will only help accelerate that process of differentiation. Price competitiveness will still be important, but the main point here is that, in addition to just focus on prices, the market will afford a number of variations in how electricity is sold to customers by catering to their attribute-specific preferences on items such as reliability, customer service, simplicity, innovation, trustworthiness, etc. If environmental protection is one of those salient attributes, then undoubtedly some products will arise to serve those preferences (100% renewable electricity plans are partly an example of this.) However, there is no reason to believe that retail-choice will automatically serve the purpose of improving our environment, unless environmental protection is a clear preference of a segment of the customers (and it is), or is built into the market as an underlying condition of generation and consumption.

• Third, this position presumes that the lowest cost generating units are more polluting, which is increasingly untrue.

• Fourth, and most importantly, regulating at the retail level is not always necessary (or even desirable, for example, due to heightened complexity) to internalize externalities in the electricity supply chain. For example, emissions could be regulated at the generation level, and then all REPs in a given market have to procure from the generation mix that emerges to meet such regulations. In this sense, the retail portion of the market can simply be a taker of whatever mix is provided for by the generation side. An example is the recently finalized US EPA Clean Power Plan (CPP). The CPP has set state-wise reductions targets for the power sector as a whole, with the most direct and significant impacts on generation technologies. In markets with retail choice, REPs will “work with” the resulting generating mix to develop and sell their electricity products. Thus while they are clearly impacted by the CPP, there is no direct regulation of REPs involved here.

Nonetheless, the effects of minimum-usage charges, as discussed in the following chapter and in the Introduction by Sioshansi, could certainly have an offsetting impact on progress toward environmental goals for some customer segments.

Retail choice can provide an efficient mechanism to leverage competitive dynamics to serve customer demand. In this sense retail choice is best seen at the mediating mechanism between supply and demand. Given the supply mix and customer preferences, the retail choice mechanism can coordinate an efficient outcome. The nature of the supply and demand themselves, however, may change, owing to changes in regulation, technology, or social norms. Retail choice may allow those changes to be reflected in an efficient manner.

ERCOT’s unique retail market structure might not be appropriate for markets of smaller size, inadequate competition at the wholesale level, and lesser faith in market forces. Yet, even in regions where this degree of retail competition is not introduced, dealing with distributed generation and new metering and control technologies will require a customer-centric approach, as discussed in chapter by Gimon.