The Future of Utility Customers and the Utility Customer of the Future

Abstract

Focusing on residential customers, the chapter examines how the electricity utility industry’s model as a monopoly provider of a “universal” essential public good is being challenged by changing customer options, including self-generation, energy efficiency, “enabled” appliances, local energy storage, and electric vehicles. Against a background of falling peak demand and energy usage, the chapter explores the electricity grid’s place in the hierarchy of needs, when faced with the coexistence, competition and coopetition of multiple energy sources and emerging technologies. It considers what electricity customers want, the choices they will face, and how these choices will shape the utility of the future.

Keywords

1. Introduction

2. Where next for the grid—fate and its drivers

2.1. Mostly Business-as-Usual

2.2. The Distributed Grid

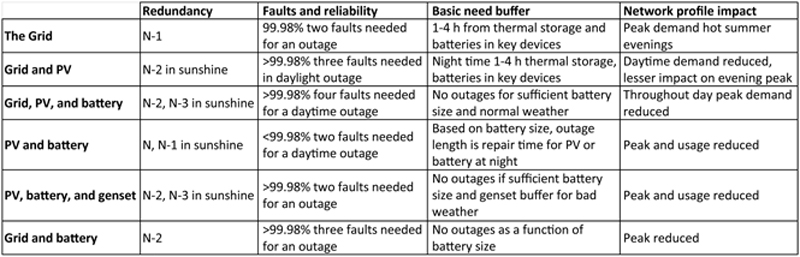

2.3. Grid Defection

In the 100+ year history of the electricity utility industry, there has never been a truly cost-competitive substitute available for grid power. We believe the solar + storage could reconfigure the organization and regulation of the electricity power business over the coming decade.10

Over time, many U.S. customers could partially or completely eliminate their usage of the power grid.11

Our view is that the “we have done it like this for a century” value chain in developed electricity markets will be turned upside down within the next 10–20 years, driven by solar and batteries.12

3. Preferences—Maslow’s basement, coopetition, and energy ecosystems

4. Grid parity in prices and product

A small PV-battery system has the highest NPV, but also the highest amount of unserved energy… The results of the study imply that leaving the grid is not a feasible option even at low PV and battery installation costs.21

5. S-curves, S-bends, and can EV’s save the grid?

The electric vehicle is coming! It is an integral part of man’s future and survival on this planet. Today we are observing the stepping stones that will bring technology and imagination together to create truly efficient vehicles and energy systems worthy of the 21st century… The threshold of a new age is upon us. It is ours to behold.

The Complete Book of Electric Vehicles, 2nd edition, 1981 (Shacket, 1981)

A very poor man may be said in some sense to have a demand for a coach and six; he might like to have it; but his demand is not an effectual demand, as the commodity can never be brought to market in order to satisfy it.24

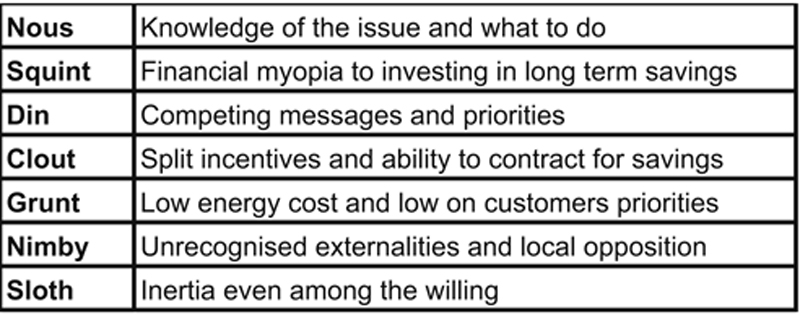

In behavioral economic terms: Nous is imperfect information; Squint is hyperbolic discounting; Din is cognitive overload and attention constraints; Clout is principle agent problems and split incentives; Grunt is satisficing behaviour for basic needs; Nimby is unpriced externalities; and Sloth is endowment effects, status quo effects and non-optimising behavior. See Gillingham and Palmer (2013) on this and the energy efficiency gap.

Consumer engagement with their electricity supply has recently increased, but it is uncertain how much consumers will want to engage in the future… up until recent price events and solar uptake, electricity use was invisible to the residential consumer.

Despite saying they are willing to change their behaviour to reduce their energy bills, many residential consumers continue to behave in ways that are contradictory to their intent (for example, they increase their use of energy-intensive appliances). Research suggests that motivations (for example, to help the environment) do not necessarily translate into behaviour (such as turning off lights or installing solar panels) and other factors also come into play (for example, social norms, ingrained habits, and the extent to which the person believes it is easy or difficult to take action).