How Much Do You Want to Make?

If you’re an investor who needs income now, I’ve shown you how you can double your yield within ten years by owning stocks that grow their dividends by 10% per year every year.

The increasing yield on cost should stay ahead of the pace of inflation and, if inflation doesn’t get too ugly, put a little extra in your pocket as well.

But where this method of investing really gets exciting is when you reinvest the dividends.

We’d all like more income today. But if you’re an investor who doesn’t need the income right away and can put off instant gratification for long-term benefits, reinvesting your dividends can generate the kinds of returns you probably thought were impossible.

For example, you can triple your money in ten years owning stocks that go up less than the market average.

A stock with a 5% yield that grows its dividend by an average of 10% and whose price rises 6%, below the 7.48% long-term average of the S&P 500, generates a compound annual growth rate of 12.34% over ten years. An investment of $10,000 turns into $32,028.

Just five years later, that $32,028 nearly doubles to $62,754; it more than doubles again five years later to $132,757 for a compound annual growth rate of 13.8% and a total return of 1,227%.

So for those of you who have 20 years, a $100,000 investment today would be worth $1.32 million in 20 years.

The dividend reinvestment strategy gets its power from compounding dividends. The concept of compounding is something that should be taught in elementary schools. We would be a much more financially literate country if our kids understood the idea from a young age.

Perhaps savings would start earlier. Maybe we wouldn’t let our credit card debt get out of hand if we understood how compounding works—that each period’s interest is piled on top of interest, which generates even more interest (or dividends).

Once this concept is grasped and applied early in life, the road to financial independence begins.

When I first got out of school, I learned something about saving for retirement that helped me quite a bit. A 21-year-old who invests $2,000 in an individual retirement account for ten years and then stops investing new money will make more than someone who starts at 31 and continues investing until he’s 60. That’s staggering when you think about it but is accurate due to the power of compounding.

So I did that, investing in mutual funds like you’re supposed to do. I left my financial future up to the professionals. These guys went to the best schools, had well-paying jobs, and were written up in all of the investing magazines. Surely they would secure my retirement for me.

In reality, only 15% of equity fund managers beat the S&P 500. According to Vanguard’s legendary founder John Bogle, from 1984 to 2003, stock mutual funds returned an average annual return of 9.3% versus the S&P 500, which returned 12.2%.

You’d be better off buying the SPDR S&P 500 ETF (NYSE: SPY), which tracks the S&P 500, and leaving it alone for 40 years rather than letting one of these guys get his paws on your money.

It’s not that the fund managers are stupid. They’re not. Beating the market is a very tough game to play. And sometimes fund managers trade too much or have to turn over their portfolio too often. Plus, you’re usually paying at least 1% in expenses just for them to hold and manage your money.

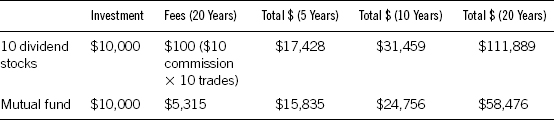

If that money was invested in some dividend-paying stocks held in a discount brokerage, you would pay about $10 to buy each stock and then nothing at all after that. No 1% of your assets each year being siphoned off to a fund manager or financial advisor. How much would that 1% per year add up to if you paid that out for 20 years? More than 20% of your original investment because of the power of compounding.

Assuming you have a $100,000 portfolio that actually beats its peers and tracks the S&P 500, and it has a low 1% expense ratio, after 20 years your portfolio would be worth $346,000 and you would have shelled out over $41,000 in fees. That’s money that should be yours for your retirement. It shouldn’t go to the manager of the Fidelity XYZ Fund or to Dave from Merrill Lynch who set up your portfolio and doesn’t do much else for you other than sending you a Christmas card in December.

Table 5.1 shows the difference between a mutual fund that performs at the market average, with the S&P’s average dividend yield over the past 50 years of 3.16% (about a full percentage point higher than today’s yield), the long-term average dividend growth rate of 5.6%, and takes a 1% management fee each year-versus a portfolio of ten dividend stocks (the kind we use in the 10-11-12 System) with an average 4% yield, 10% dividend growth, average market performance, and no management fee, with dividends reinvested.

Table 5.1 How Much Can You Save?

The expenses of mutual funds are a hidden cost because you don’t actually see the money taken out of your account. Rather, the expense fees hurt performance. So if your fund’s holdings went up 6% in value during the year but the fund has a 1% expense ratio, your return would be only 4.94%. (If the account value started at $100,000, grew by 6% to $106,000, and management took a 1% fee, the portfolio would be left with $104,940.)

Even worse is if you’re paying a financial advisor 1% per year. That’s money that actually does come out of your account and is no longer available to invest.

If you have a $500,000 account, growing at 10% per year, after ten years, you’ve paid over $83,000. Of course, if your advisor is helpful in planning for retirement, your kids’ education, insurance products, asset allocation advice, and the like, and her advice makes you an extra $84,000 over that time or enables you to sleep at night, it will be worth paying the yearly management fee.

But if all your broker does is peddle you stock opportunities, stick you in some funds, or execute your ideas, you’re better off investing with a discount broker and keeping those fees for yourself, so they can compound over the years to make you even more money.

Let’s assume that instead of paying out the $83,000 in fees over ten years, you invested with a discount broker.

Growing at 10% per year, your money would increase to $1,296,871 after ten years and no fees versus $1,172,867 if you paid your advisor 1% per year. That’s a difference of over $124,000. So it’s not just the $83,000 you’re paying to the advisor, it’s also costing you another $40,000 in profits.

I don’t want to make it sound like I’m totally against financial planners. A good one who helps you achieve your financial goals better than you can do it yourself is worth what you’re paying him or her. But there are many who are merely salespeople who happen to sell financial products. Those people are not worth the fees you pay them. In some cases, they’re not even looking out for your best interests. They’re selling you the products that will land them the largest commission. Invested wisely, the money that you pay them, in your pocket instead, can add substantially to your returns.

So how much money do you want to make? Do you want to double your investment? Triple it? It’s up to you. Of course, the higher gains that you shoot for, the more risk you take on, but that risk is relative. We’re not talking about biotech penny stocks that can implode and go to zero on some bad news.

We’re talking about companies that have a long history of paying and raising dividends, whose management teams would like to keep that record intact.

Of course, anything can happen. The markets can swoon, a particular stock can dive on a missed earnings report or scandal. But for the most part, we’re talking solid companies with good track records. And even if the stock does slide, if the dividend continues to be raised, that’s an opportunity to buy more stock.

So let’s take a look at some ways to make boatloads of money without having to do a whole lot of work.

In Table 5.2, you can see various assumptions. We’re going to adjust for initial yield, dividend growth, and stock price growth. We’ll assume the initial investment was $10,000.

Table 5.2 How Much Money Do You Want to Make?

Table 5.2 drives home the point about how powerful compounding dividends is. Notice how the end result after 20 years is higher if the dividend growth rate is higher as opposed to the stock price growth.

For example, if you bought a stock with a 5% yield and 10% dividend growth rate, and the stock price increased just 1% per year, the stock would be worth over $145,000 after 20 years.

However, if the stock price increased 5% per year, you’d wind up with about $128,000, a lower value.

That doesn’t seem like it should make sense, that a stock growing at a faster pace would have a lower value after 20 years.

But you have to consider that for all of those 20 years of reinvesting the dividend, you end up with many more shares of the slower-growth stock. Because the stock price is lower and the dividend is rising, you can buy more shares each quarter. Over time, all of those shares add up.

How many more shares do you get at the lower stock price growth rate?

If the stock increases just 1% per year, you’d have 11,924 shares (after starting with just 1,000). The stock that grows 5% per year results in a total of 4,837 shares, less than half the number of shares than the 1% grower.

At the higher growth rate, you’d have 4,837 shares of stock at a price of $26.53, whereas the 1% grower gives you 11,924 shares at $12.20.

As the price of the stock experiences higher levels of growth, the price does in fact make an important contribution to the end value.

But, as you can see, if you’re in a long-term dividend reinvestment program, the starting yield and dividend growth rate are just as important, if not more so, than the growth rate of the stock itself.

In fact, the best thing that could happen to you would be for the stock to languish for a long time while you continue to buy cheap shares. Then at some point in the distant future (preferably when you’re getting ready to sell), the stock takes off and achieves some measure of growth.

Even if your stock doesn’t move much over the years but continues to raise the dividend at a healthy clip and run a successful business, you shouldn’t worry about it.

It could wind up being the best thing that ever happened to you as you grow the number of shares you own significantly, which will generate more dividends to be reinvested or spent as income.

Keep in mind that you don’t have to sell your shares to reap the benefits. Let’s say you’ve successfully reinvested your dividends for 20 years in the stock with the 5% initial yield, 10% dividend growth, but just 1% price growth.

After the 20-year period, you need the income from the stock and stop reinvesting the dividends in order to collect them. At that point, the stock is paying a yield of 30.6% per year on your original cost, and your $10,000 investment generates $8,578 per quarter in dividend income, or $34,312 per year for an annual yield of over 343% on your original investment.

If, instead, the stock price grew 5% per year, it still yields 30.6% on your original cost, but because you were able to buy fewer shares all those years (because the price was higher), your quarterly income is $3,594—or $14,376 per year. Still not bad at all on a $10,000 investment, particularly one that is now worth 13 times what you originally paid for it.

Now, I’m not suggesting you try to find stocks that are going to be duds in order to be able to accumulate more shares. As you can see, there is a point where the increase in the stock price does make a difference to your total return.

But I wanted to point out that huge things can happen even if your stock is a disappointment as far as price, as long as it grows the dividend by a meaningful amount every year.

As I stated at the beginning of this book, the way we approach stocks seems to have changed over the past 15 years. We’ve become a society of stock traders who agonize over every tick rather than investors in good companies that are in them for the long term.

And the fact that your stock may be as boring as a high school trigonometry class could be a good thing. According to a study by Harvard Business School’s Malcolm Baker, Acadian Asset Management’s Brendan Bradley, and New York University’s Jeffrey Wurgler, between 1968 and 2002, “Low volatility and low beta portfolios offered an enviable combination of high average returns and small drawdowns.”1

Beta: A measure of volatility or risk. It is the correlation of a stock or portfolio’s change in value in response to a move by the overall market. A stock with a beta of 1 moves exactly the way the broad market moves. A stock with a beta of 0.5 results in a price change that is half of the market’s. A stock with a beta of 2 doubles the market’s move.

Example: Stock A has a beta of 1, Stock B has a beta of 0.5, and Stock C has a beta of 2. They all trade at $10. If the stock market rises 10%, Stock A should climb 10% and trade at $11. Stock B only goes up 5% to trade at $10.50. Stock C jumps 20% to trade at $12.

According to the study, $1 invested in 1968 in the quintile of lowest-volatility stocks was worth $59.55 in 2002. This contrasts with a result of just $0.58 for stocks with the highest volatility.

This concept runs counter to what we’ve always been led to believe—that in order to reap outsized gains we need to take on additional risk. And that boring stocks produce boring returns.

Dividend-paying stocks are often considered boring stocks. Insurance companies, Real Estate Investment Trusts (REITs), big consumer products companies, and utilities don’t have the sizzle of the hottest new technology or biotech stocks. And, of course, everyone can point to the companies that were enormously successful, such as Google (Nasdaq: GOOG) and Apple (Nasdaq: AAPL). But for every one of those, there are many many companies like Real Networks (Nasdaq: RNWK) that has never consistently made money and whose shareholders have taken a beating.

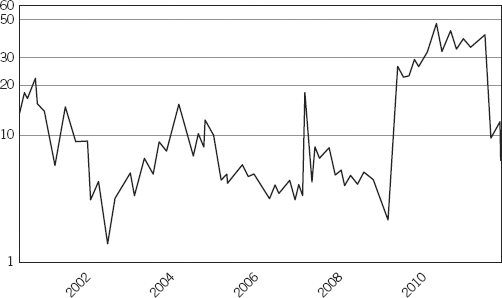

Consider a high-beta company like Dendreon (Nasdaq: DND) with a beta of over 5.5 (see Figure 5.1). Over the past ten years, Dendreon’s stock price has been all over the place, possibly making fortunes for investors or traders lucky enough to be on the right side of the trade but also losing gobs of money for those who got it wrong.

In comparison, the S&P 500 Dividend Aristocrats Index has a beta of 0.93, which means its price change should be only 93% of that of the S&P 500.

Table 5.3 shows a list of some “boring” Aristocrats/Champions and their betas.

Table 5.3 Aristocrats/Champions and Their Betas

Source: Yahoo! Finance

| Company | Beta |

| Coca-Cola (NYSE: KO) | 0.42 |

| Consolidated Edison (NYSE: ED) | 0.27 |

| Exxon Mobil (NYSE: XOM) | 0.53 |

| Illinois Toolworks (NYSE: ITW) | 1.10 |

| Kimberly Clark (NYSE: KMB) | 0.34 |

| McDonald’s (NYSE: MCD) | 0.34 |

| Procter & Gamble (NYSE: PG) | 0.47 |

| Wal-Mart (NYSE: WMT) | 0.43 |

| S&P 500 | 1.00 |

Now let’s look at Table 5.4, which shows these same boring stocks and how they have performed over the past ten years. Note that this list is price only, not including dividends.

Table 5.4 But Low Beta Doesn’t Mean Boring Returns

Source: Yahoo! Finance

| Company | Beta | Performance |

| Coca-Cola (NYSE: KO) | 0.42 | 48% |

| Consolidated Edison (NYSE: ED) | 0.27 | 54% |

| Exxon Mobil (NYSE: XOM) | 0.53 | 116% |

| Illinois Toolworks (NYSE: ITW) | 1.10 | 38% |

| Kimberly Clark (NYSE: KMB) | 0.34 | 25% |

| McDonald’s (NYSE: MCD) | 0.34 | 279% |

| Procter & Gamble (NYSE: PG) | 0.47 | 69% |

| Wal-Mart (NYSE: WMT) | 0.43 | 4% |

| S&P 500 | 1.00 | 10% |

As you can see, most of these boring stocks outperformed the S&P 500, of which they’re a part.

Now, when we include reinvested dividends, look what happens (see Table 5.5).

Table 5.5 Reinvesting Dividends in Low Beta Stocks Amps Up Returns Even More

Source: Yahoo! Finance

| Company | Beta | Total Return |

| Coca-Cola (NYSE: KO) | 0.42 | 92% |

| Consolidated Edison (NYSE: ED) | 0.27 | 159% |

| Exxon Mobil (NYSE: XOM) | 0.53 | 169% |

| Illinois Toolworks (NYSE: ITW) | 1.10 | 69% |

| Kimberly Clark (NYSE: KMB) | 0.34 | 73% |

| McDonald’s (NYSE: MCD) | 0.34 | 381% |

| Procter & Gamble (NYSE: PG) | 0.47 | 115% |

| Wal-Mart (NYSE: WMT) | 0.43 | 21% |

| S&P 500 | 1.00 | 30% |

Going back to my earlier idea that investors became traders in the late 1990s and seemed to have forgotten how to invest for the long haul, somehow the notion of a 10% to 15% annual return isn’t sexy anymore. They want to double or triple their money on the next great stock.

Believe me, I like a good speculation as much as the next guy. And I absolutely love researching tiny biotech companies that could be the next five or ten bagger (a stock that goes up five or ten times the original investment).

But those trades are for the money that you’d take to Vegas. That’s not investing unless you really know something about the company that Wall Street does not. And even then, it’s a big risk.

If you don’t think that an annual return of 10% to 15% is solid, you’ll never be satisfied. You’re the guy who goes out to a great meal and complains that the valet took too long to get your car. You’re the woman who’s married to the handsome prince and complains about his mother.

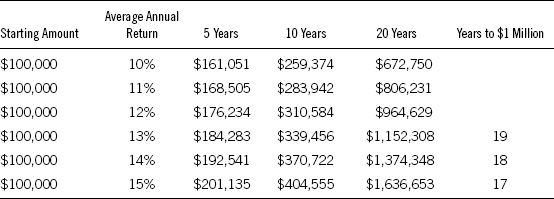

Look at Table 5.6 and see what you can do with an average return of 10% to 15% per year.

Table 5.6 $100,000 Turns into . . .

Impressive numbers, right? As Tom Petty sang, “The waiting is the hardest part.”

It’s tough to get those double-digit returns, particularly the ones north of 13%, after just five years. For example, if you buy a stock with a 5% dividend that has 10% annual dividend growth and 5% stock price appreciation, after five years your average compounded annual growth rate will be 10.82%. Because of the power of compounding, that average annual growth rate rises to 11.60% over 10 years and 13.61% over 20.

In this scenario, your $100,000 would turn into $1 million after 18.75 years.

That may sound like a long time, but if you’re in your forties, fifties, or sixties, think about where you were 19 years ago. The time sure flies, doesn’t it?

Wouldn’t it have been nice to have put away a sum of money back then and forgotten about it, only to see it worth more than ten times what you invested?

Nineteen years ago, I was working my first job out of college at a credit union. I wasn’t making much money, but I had worked since I was 12 years old and was always a good saver, so I had some money to invest.

If I had put away $25,000 into a quality dividend stock back then, today I’d likely have my fifth grader’s college paid for.

If everyone did this when their child was born, rather than handing it over to some mutual fund manager who will underperform the market or trying to pick hot stocks, chances are when those kids are ready for college, most if not all of the needed funds will be there.

Many events two decades away seem impossible to fathom now but will get here sooner than you think.

College, a wedding, retirement, traveling around the world, setting up a new business—these are all things that can be achieved by starting this kind of program today and not touching the money for 18 to 20 years.

Admittedly, that’s not easy for most of us. When things are that far away and that expensive, they are daunting.

When my son was born, I was told it would cost roughly $80,000 per year for him to go to college. We started saving immediately, but still, the idea that we would have to come up with $320,000 and then another $320,000 (and likely more) for my daughter a few years later made us want to not even think about it.

And keep in mind that what I’ve shown you are the results of just investing once and letting the dividends compound. If, occasionally, you had some spare cash to invest and bought more stock, the results would be even greater. You don’t need to have a huge amount to make a difference.

If your starting purchase was $2,500 and every few months you bought $200 more worth of stock, or whatever you can afford, that money will also compound over the years and turn into significantly more.

So although this chapter is all about the ease of the system, you can step on the gas once in a while with any extra funds that you can afford to invest. I strongly encourage you to do so when you’re able.

Our consumer culture has turned us into instant-gratification hogs. We want it all and we want it now. The idea of putting off enjoyment or letting our money sit and work for us for 19 years or so is a foreign concept for many of us.

Particularly when we are being bombarded all day by marketing messages telling us we have to have the latest car, TV, and gadget.

I’ve already told you that I’m not going to try to turn you into a saver if you’re not. That’s above my pay grade. It’s all on you.

What I hope I’ve been able to show you in this chapter is what you can accomplish if you do save and invest.

Essentially, your financial dreams can come true. All it takes is to put some money away and invest it in quality companies that pay a decent yield and grow the dividend every year by a meaningful amount.