Cracking the Code of Change

by Michael Beer and Nitin Nohria

THE NEW ECONOMY HAS ushered in great business opportunities—and great turmoil. Not since the Industrial Revolution have the stakes of dealing with change been so high. Most traditional organizations have accepted, in theory at least, that they must either change or die. And even Internet companies such as eBay, Amazon.com, and America Online recognize that they need to manage the changes associated with rapid entrepreneurial growth. Despite some individual successes, however, change remains difficult to pull off, and few companies manage the process as well as they would like. Most of their initiatives—installing new technology, downsizing, restructuring, or trying to change corporate culture—have had low success rates. The brutal fact is that about 70% of all change initiatives fail.

In our experience, the reason for most of those failures is that in their rush to change their organizations, managers end up immersing themselves in an alphabet soup of initiatives. They lose focus and become mesmerized by all the advice available in print and online about why companies should change, what they should try to accomplish, and how they should do it. This proliferation of recommendations often leads to muddle when change is attempted. The result is that most change efforts exert a heavy toll, both human and economic. To improve the odds of success, and to reduce the human carnage, it is imperative that executives understand the nature and process of corporate change much better. But even that is not enough. Leaders need to crack the code of change.

For more than 40 years now, we’ve been studying the nature of corporate change. And although every business’s change initiative is unique, our research suggests there are two archetypes, or theories, of change. These archetypes are based on very different and often unconscious assumptions by senior executives—and the consultants and academics who advise them—about why and how changes should be made. Theory E is change based on economic value. Theory O is change based on organizational capability. Both are valid models; each theory of change achieves some of management’s goals, either explicitly or implicitly. But each theory also has its costs—often unexpected ones.

Theory E change strategies are the ones that make all the headlines. In this “hard” approach to change, shareholder value is the only legitimate measure of corporate success. Change usually involves heavy use of economic incentives, drastic layoffs, downsizing, and restructuring. E change strategies are more common than O change strategies among companies in the United States, where financial markets push corporate boards for rapid turnarounds. For instance, when William A. Anders was brought in as CEO of General Dynamics in 1991, his goal was to maximize economic value—how-ever painful the remedies might be. Over the next three years, Anders reduced the workforce by 71,000 people—44,000 through the divestiture of seven businesses and 27,000 through layoffs and attrition. Anders employed common E strategies.

Managers who subscribe to Theory O believe that if they were to focus exclusively on the price of their stock, they might harm their organizations. In this “soft” approach to change, the goal is to develop corporate culture and human capability through individual and organizational learning—the process of changing, obtaining feedback, reflecting, and making further changes. U.S. companies that adopt O strategies, as Hewlett-Packard did when its performance flagged in the 1980s, typically have strong, long-held, commitment-based psychological contracts with their employees.

Managers at these companies are likely to see the risks in breaking those contracts. Because they place a high value on employee commitment, Asian and European businesses are also more likely to adopt an O strategy to change.

Few companies subscribe to just one theory. Most companies we have studied have used a mix of both. But all too often, managers try to apply theories E and O in tandem without resolving the inherent tensions between them. This impulse to combine the strategies is directionally correct, but theories E and O are so different that it’s hard to manage them simultaneously—employees distrust leaders who alternate between nurturing and cutthroat corporate behavior. Our research suggests, however, that there is a way to resolve the tension so that businesses can satisfy their shareholders while building viable institutions. Companies that effectively combine hard and soft approaches to change can reap big payoffs in profitability and productivity. Those companies are more likely to achieve a sustainable competitive advantage. They can also reduce the anxiety that grips whole societies in the face of corporate restructuring.

Idea in Practice

The UK grocery chain, ASDA, teetered on bankruptcy in 1991. Here’s how CEO Archie Norman combined change Theories E and O with spectacular results: a culture of trust and openness—and an eightfold increase in shareholder value.

In this article, we will explore how one company successfully resolved the tensions between E and O strategies. But before we do that, we need to look at just how different the two theories are.

A Tale of Two Theories

To understand how sharply theories E and O differ, we can compare them along several key dimensions of corporate change: goals, leadership, focus, process, reward system, and use of consultants. (For a side-by-side comparison, see the table “Comparing theories of change.”) We’ll look at two companies in similar businesses that adopted almost pure forms of each archetype. Scott Paper successfully used Theory E to enhance shareholder value, while Champion International used Theory O to achieve a complete cultural transformation that increased its productivity and employee commitment. But as we will soon observe, both paper producers also discovered the limitations of sticking with only one theory of change. Let’s compare the two companies’ initiatives.

Goals

When Al Dunlap assumed leadership of Scott Paper in May 1994, he immediately fired 11,000 employees and sold off several businesses. His determination to restructure the beleaguered company was almost monomaniacal. As he said in one of his speeches: “Shareholders are the number one constituency. Show me an annual report that lists six or seven constituencies, and I’ll show you a mismanaged company.” From a shareholder’s perspective, the results of Dunlap’s actions were stunning. In just 20 months, he managed to triple shareholder returns as Scott Paper’s market value rose from about $3 billion in 1994 to about $9 billion by the end of 1995. The financial community applauded his efforts and hailed Scott Paper’s approach to change as a model for improving shareholder returns.

Champion’s reform effort couldn’t have been more different. CEO Andrew Sigler acknowledged that enhanced economic value was an appropriate target for management, but he believed that goal would be best achieved by transforming the behaviors of management, unions, and workers alike. In 1981, Sigler and other managers launched a long-term effort to restructure corporate culture around a new vision called the Champion Way, a set of values and principles designed to build up the competencies of the workforce. By improving the organization’s capabilities in areas such as teamwork and communication, Sigler believed he could best increase employee productivity and thereby improve the bottom line.

Leadership

Leaders who subscribe to Theory E manage change the old-fashioned way: from the top down. They set goals with little involvement from their management teams and certainly without input from lower levels or unions. Dunlap was clearly the commander in chief at Scott Paper. The executives who survived his purges, for example, had to agree with his philosophy that shareholder value was now the company’s primary objective. Nothing made clear Dunlap’s leadership style better than the nickname he gloried in: “Chainsaw Al.”

By contrast, participation (a Theory O trait) was the hallmark of change at Champion. Every effort was made to get all its employees emotionally committed to improving the company’s performance. Teams drafted value statements, and even the industry’s unions were brought into the dialogue. Employees were encouraged to identify and solve problems themselves. Change at Champion sprouted from the bottom up.

Focus

In E-type change, leaders typically focus immediately on streamlining the “hardware” of the organization—the structures and systems. These are the elements that can most easily be changed from the top down, yielding swift financial results. For instance, Dunlap quickly decided to outsource many of Scott Paper’s corporate functions—benefits and payroll administration, almost all of its management information systems, some of its technology research, medical services, telemarketing, and security functions. An executive manager of a global merger explained the E rationale: “I have a [profit] goal of $176 million this year, and there’s no time to involve others or develop organizational capability.”

By contrast, Theory O’s initial focus is on building up the “software” of an organization—the culture, behavior, and attitudes of employees. Throughout a decade of reforms, no employees were laid off at Champion. Rather, managers and employees were encouraged to collectively reexamine their work practices and behaviors with a goal of increasing productivity and quality. Managers were replaced if they did not conform to the new philosophy, but the overall firing freeze helped to create a culture of trust and commitment. Structural change followed once the culture changed. Indeed, by the mid-1990s, Champion had completely reorganized all its corporate functions. Once a hierarchical, functionally organized company, Champion adopted a matrix structure that empowered employee teams to focus more on customers.

Comparing theories of change

Our research has shown that all corporate transformations can be compared along the six dimensions shown here. The table outlines the differences between the E and O archetypes and illustrates what an integrated approach might look like.

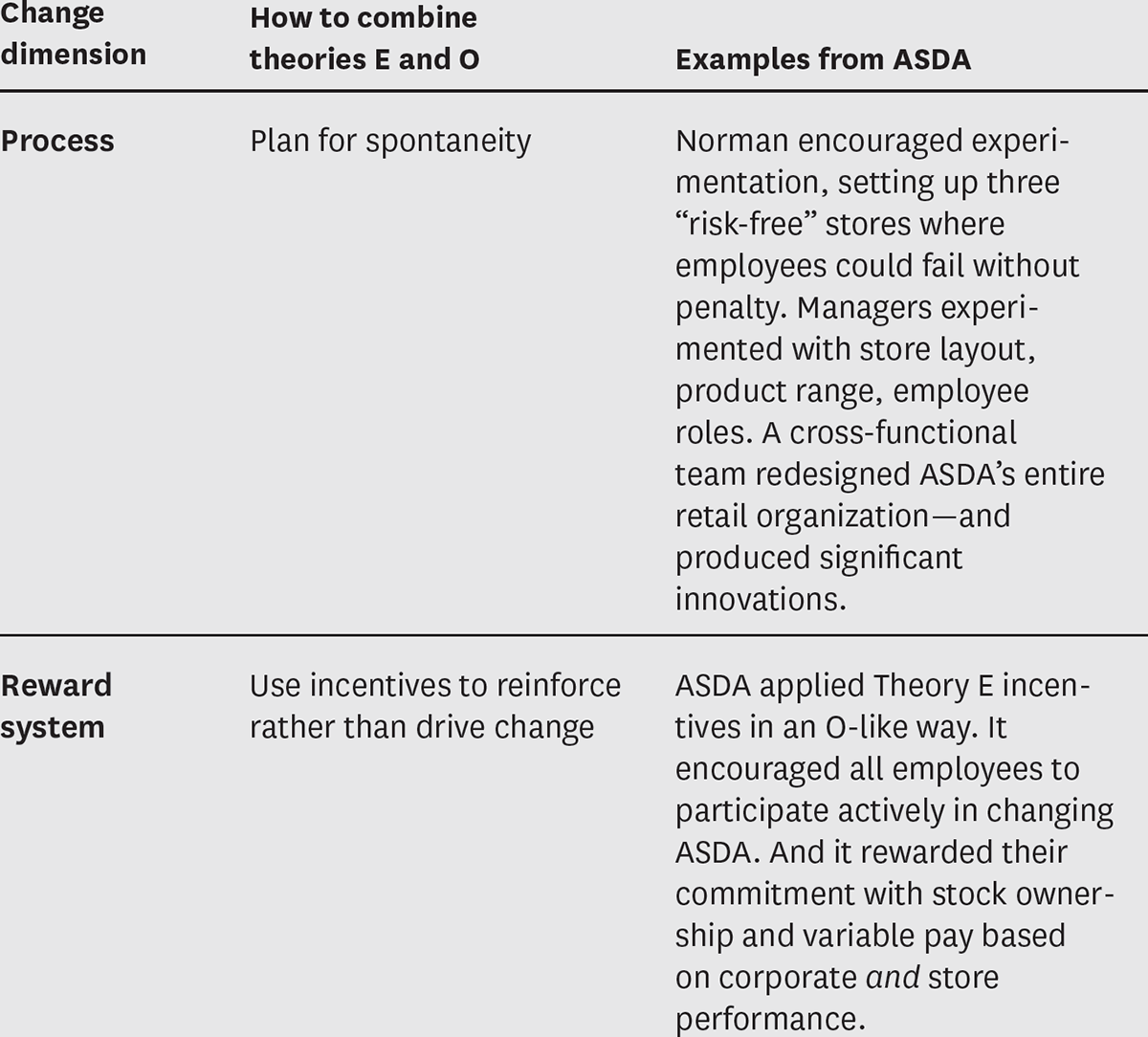

Process

Theory E is predicated on the view that no battle can be won without a clear, comprehensive, common plan of action that encourages internal coordination and inspires confidence among customers, suppliers, and investors. The plan lets leaders quickly motivate and mobilize their businesses; it compels them to take tough, decisive actions they presumably haven’t taken in the past. The changes at Scott Paper unfolded like a military battle plan. Managers were instructed to achieve specific targets by specific dates. If they didn’t adhere to Dunlap’s tightly choreographed marching orders, they risked being fired.

Meanwhile, the changes at Champion were more evolutionary and emergent than planned and programmatic. When the company’s decade-long reform began in 1981, there was no master blueprint. The idea was that innovative work processes, values, and culture changes in one plant would be adapted and used by other plants on their way through the corporate system. No single person, not even Sigler, was seen as the driver of change. Instead, local leaders took responsibility. Top management simply encouraged experimentation from the ground up, spread new ideas to other workers, and transferred managers of innovative units to lagging ones.

Reward System

The rewards for managers in E-type change programs are primarily financial. Employee compensation, for example, is linked with financial incentives, mainly stock options. Dunlap’s own compensation package—which ultimately netted him more than $100 million—was tightly linked to shareholders’ interests. Proponents of this system argue that financial incentives guarantee that employees’ interests match stockholders’ interests. Financial rewards also help top executives feel compensated for a difficult job—one in which they are often reviled by their onetime colleagues and the larger community.

The O-style compensation systems at Champion reinforced the goals of culture change, but they didn’t drive those goals. A skills-based pay system and a corporatewide gains-sharing plan were installed to draw union workers and management into a community of purpose. Financial incentives were used only as a supplement to those systems and not to push particular reforms. While Champion did offer a companywide bonus to achieve business goals in two separate years, this came late in the change process and played a minor role in actually fulfilling those goals.

Use of Consultants

Theory E change strategies often rely heavily on external consultants. A SWAT team of Ivy League–educated MBAs, armed with an arsenal of state-of-the-art ideas, is brought in to find new ways to look at the business and manage it. The consultants can help CEOs get a fix on urgent issues and priorities. They also offer much-needed political and psychological support for CEOs who are under fire from financial markets. At Scott Paper, Dunlap engaged consultants to identify many of the painful cost-savings initiatives that he subsequently implemented.

Theory O change programs rely far less on consultants. The handful of consultants who were introduced at Champion helped managers and workers make their own business analyses and craft their own solutions. And while the consultants had their own ideas, they did not recommend any corporate program, dictate any solutions, or whip anyone into line. They simply led a process of discovery and learning that was intended to change the corporate culture in a way that could not be foreseen at the outset.

In their purest forms, both change theories clearly have their limitations. CEOs who must make difficult E-style choices understandably distance themselves from their employees to ease their own pain and guilt. Once removed from their people, these CEOs begin to see their employees as part of the problem. As time goes on, these leaders become less and less inclined to adopt O-style change strategies. They fail to invest in building the company’s human resources, which inevitably hollows out the company and saps its capacity for sustained performance. At Scott Paper, for example, Dunlap trebled shareholder returns but failed to build the capabilities needed for sustained competitive advantage—commitment, coordination, communication, and creativity. In 1995, Dunlap sold Scott Paper to its longtime competitor Kimberly-Clark.

CEOs who embrace Theory O find that their loyalty and commitment to their employees can prevent them from making tough decisions. The temptation is to postpone the bitter medicine in the hopes that rising productivity will improve the business situation. But productivity gains aren’t enough when fundamental structural change is required. That reality is underscored by today’s global financial system, which makes corporate performance instantly transparent to large institutional shareholders whose fund managers are under enormous pressure to show good results. Consider Champion. By 1997, it had become one of the leaders in its industry based on most performance measures. Still, newly instated CEO Richard Olsen was forced to admit a tough reality: Champion shareholders had not seen a significant increase in the economic value of the company in more than a decade. Indeed, when Champion was sold recently to Finland-based UPM-Kymmene, it was acquired for a mere 1.5 times its original share value.

Managing the Contradictions

Clearly, if the objective is to build a company that can adapt, survive, and prosper over the years, Theory E strategies must somehow be combined with Theory O strategies. But unless they’re carefully handled, melding E and O is likely to bring the worst of both theories and the benefits of neither. Indeed, the corporate changes we’ve studied that arbitrarily and haphazardly mixed E and O techniques proved destabilizing to the organizations in which they were imposed. Managers in those companies would certainly have been better off to pick either pure E or pure O strategies—with all their costs. At least one set of stakeholders would have benefited.

The obvious way to combine E and O is to sequence them. Some companies, notably General Electric, have done this quite successfully. At GE, CEO Jack Welch began his sequenced change by imposing an E-type restructuring. He demanded that all GE businesses be first or second in their industries. Any unit that failed that test would be fixed, sold off, or closed. Welch followed that up with a massive downsizing of the GE bureaucracy. Between 1981 and 1985, total employment at the corporation dropped from 412,000 to 299,000. Sixty percent of the corporate staff, mostly in planning and finance, was laid off. In this phase, GE people began to call Welch “Neutron Jack,” after the fabled bomb that was designed to destroy people but leave buildings intact. Once he had wrung out the redundancies, however, Welch adopted an O strategy. In 1985, he started a series of organizational initiatives to change GE culture. He declared that the company had to become “boundaryless,” and unit leaders across the corporation had to submit to being challenged by their subordinates in open forum. Feedback and open communication eventually eroded the hierarchy. Soon Welch applied the new order to GE’s global businesses.

Unfortunately for companies like Champion, sequenced change is far easier if you begin, as Welch did, with Theory E. Indeed, it is highly unlikely that E would successfully follow O because of the sense of betrayal that would involve. It is hard to imagine how a draconian program of layoffs and downsizing can leave intact the psychological contract and culture a company has so patiently built up over the years. But whatever the order, one sure problem with sequencing is that it can take a very long time; at GE it has taken almost two decades. A sequenced change may also require two CEOs, carefully chosen for their contrasting styles and philosophies, which may create its own set of problems. Most turnaround managers don’t survive restructuring—partly because of their own inflexibility and partly because they can’t live down the distrust that their ruthlessness has earned them. In most cases, even the best-intentioned effort to rebuild trust and commitment rarely overcomes a bloody past. Welch is the exception that proves the rule.

So what should you do? How can you achieve rapid improvements in economic value while simultaneously developing an open, trusting corporate culture? Paradoxical as those goals may appear, our research shows that it is possible to apply theories E and O together. It requires great will, skill—and wisdom. But precisely because it is more difficult than mere sequencing, the simultaneous use of O and E strategies is more likely to be a source of sustainable competitive advantage.

One company that exemplifies the reconciliation of the hard and soft approaches is ASDA, the UK grocery chain that CEO Archie Norman took over in December 1991, when the retailer was nearly bankrupt. Norman laid off employees, flattened the organization, and sold off losing businesses—acts that usually spawn distrust among employees and distance executives from their people. Yet during Norman’s eight-year tenure as CEO, ASDA also became famous for its atmosphere of trust and openness. It has been described by executives at Wal-Mart—itself famous for its corporate culture—as being “more like Wal-Mart than we are.” Let’s look at how ASDA resolved the conflicts of E and O along the six main dimensions of change.

Explicitly confront the tension between E and O goals

With his opening speech to ASDA’s executive team—none of whom he had met—Norman indicated clearly that he intended to apply both E and O strategies in his change effort. It is doubtful that any of his listeners fully understood him at the time, but it was important that he had no conflicts about recognizing the paradox between the two strategies for change. He said as much in his maiden speech: “Our number one objective is to secure value for our shareholders and secure the trading future of the business. I am not coming in with any magical solutions. I intend to spend the next few weeks listening and forming ideas for our precise direction. . . . We need a culture built around common ideas and goals that include listening, learning, and speed of response, from the stores upwards. [But] there will be management reorganization. My objective is to establish a clear focus on the stores, shorten lines of communication, and build one team.” If there is a contradiction between building a high-involvement organization and restructuring to enhance shareholder value, Norman embraced it.

Set direction from the top and engage people below

From day one, Norman set strategy without expecting any participation from below. He said ASDA would adopt an everyday-low-pricing strategy, and Norman unilaterally determined that change would begin by having two experimental store formats up and running within six months. He decided to shift power from the headquarters to the stores, declaring: “I want everyone to be close to the stores. We must love the stores to death; that is our business.” But even from the start, there was an O quality to Norman’s leadership style. As he put it in his first speech: “First, I am forthright, and I like to argue. Second, I want to discuss issues as colleagues. I am looking for your advice and your disagreement.” Norman encouraged dialogue with employees and customers through colleague and customer circles. He set up a “Tell Archie” program so that people could voice their concerns and ideas.

Making way for opposite leadership styles was also an essential ingredient to Norman’s—and ASDA’s—success. This was most clear in Norman’s willingness to hire Allan Leighton shortly after he took over. Leighton eventually became deputy chief executive. Norman and Leighton shared the same E and O values, but they had completely different personalities and styles. Norman, cool and reserved, impressed people with the power of his mind—his intelligence and business acumen. Leighton, who is warmer and more people oriented, worked on employees’ emotions with the power of his personality. As one employee told us, “People respect Archie, but they love Allan.” Norman was the first to credit Leighton with having helped to create emotional commitment to the new ASDA. While it might be possible for a single individual to embrace opposite leadership styles, accepting an equal partner with a very different personality makes it easier to capitalize on those styles. Leighton certainly helped Norman reach out to the organization. Together they held quarterly meetings with store managers to hear their ideas, and they supplemented those meetings with impromptu talks.

Focus simultaneously on the hard and soft sides of the organization

Norman’s immediate actions followed both the E goal of increasing economic value and the O goal of transforming culture. On the E side, Norman focused on structure. He removed layers of hierarchy at the top of the organization, fired the financial officer who had been part of ASDA’s disastrous policies, and decreed a wage freeze for everyone—management and workers alike. But from the start, the O strategy was an equal part of Norman’s plan. He bought time for all this change by warning the markets that financial recovery would take three years. Norman later said that he spent 75% of his early months at ASDA as the company’s human resource director, making the organization less hierarchical, more egalitarian, and more transparent. Both Norman and Leighton were keenly aware that they had to win hearts and minds. As Norman put it to workers: “We need to make ASDA a great place for everyone to work.”

Plan for spontaneity

Training programs, total-quality programs, and top-driven culture change programs played little part in ASDA’s transformation. From the start, the ASDA change effort was set up to encourage experimentation and evolution. To promote learning, for example, ASDA set up an experimental store that was later expanded to three stores. It was declared a risk-free zone, meaning there would be no penalties for failure. A cross-functional task force “renewed,” or redesigned, ASDA’s entire retail proposition, its organization, and its managerial structure. Store managers were encouraged to experiment with store layout, employee roles, ranges of products offered, and so on. The experiments produced significant innovations in all aspects of store operations. ASDA’s managers learned, for example, that they couldn’t renew a store unless that store’s management team was ready for new ideas. This led to an innovation called the Driving Test, which assessed whether store managers’ skills in leading the change process were aligned with the intended changes. The test perfectly illustrates how E and O can come together: it bubbled up O-style from the bottom of the company, yet it bound managers in an E-type contract. Managers who failed the test were replaced.

Let incentives reinforce change, not drive it

Any synthesis of E and O must recognize that compensation is a double-edged sword. Money can focus and motivate managers, but it can also hamper teamwork, commitment, and learning. The way to resolve this dilemma is to apply Theory E incentives in an O way. Employees’ high involvement is encouraged to develop their commitment to change, and variable pay is used to reward that commitment. ASDA’s senior executives were compensated with stock options that were tied to the company’s value. These helped attract key executives to ASDA. Unlike most E-strategy companies, however, ASDA had a stock-ownership plan for all employees. In addition, store-level employees got variable pay based on both corporate performance and their stores’ records. In the end, compensation represented a fair exchange of value between the company and its individual employees. But Norman believed that compensation had not played a major role in motivating change at the company.

Use consultants as expert resources who empower employees

Consultants can provide specialized knowledge and technical skills that the company doesn’t have, particularly in the early stages of organizational change. Management’s task is figuring out how to use those resources without abdicating leadership of the change effort. ASDA followed the middle ground between Theory E and Theory O. It made limited use of four consulting firms in the early stages of its transformation. The consulting firms always worked alongside management and supported its leadership of change. However, their engagement was intentionally cut short by Norman to prevent ASDA and its managers from becoming dependent on the consultants. For example, an expert in store organization was hired to support the task force assigned to renew ASDA’s first few experimental stores, but later stores were renewed without his involvement.

By embracing the paradox inherent in simultaneously employing E and O change theories, Norman and Leighton transformed ASDA to the advantage of its shareholders and employees. The organization went through personnel changes, unit sell-offs, and hierarchical upheaval. Yet these potentially destructive actions did not prevent ASDA’s employees from committing to change and the new corporate culture because Norman and Leighton had won employees’ trust by constantly listening, debating, and being willing to learn. Candid about their intentions from the outset, they balanced the tension between the two change theories.

By 1999, the company had multiplied shareholder value eightfold. The organizational capabilities built by Norman and Leighton also gave ASDA the sustainable competitive advantage that Dunlap had been unable to build at Scott Paper and that Sigler had been unable to build at Champion. While Dunlap was forced to sell a demoralized and ineffective organization to Kimberly-Clark, and while a languishing Champion was sold to UPM-Kymmene, Norman and Leighton in June 1999 found a friendly and culturally compatible suitor in Wal-Mart, which was willing to pay a substantial premium for the organizational capabilities that ASDA had so painstakingly developed.

In the end, the integration of theories E and O created major change—and major payoffs—for ASDA. Such payoffs are possible for other organizations that want to develop a sustained advantage in today’s economy. But that advantage can come only from a constant willingness and ability to develop organizations for the long term combined with a constant monitoring of shareholder value—E dancing with O, in an unending minuet.

Originally published in May 2000. Reprint R00301