Preface: Who Is #1?

As you read the second edition of Inside the Mind of the Shopper, consider the various players at retail: shoppers, retailers, brand suppliers, and other supporting businesses. Ask yourself, out of these players, who is the top dog? Who is the most important? Who is #1? The answer(s) to that question will provide insight necessary for understanding many of the concepts we discuss in Inside the Mind of the Shopper.

First of all, #1 is a coveted position in most human endeavors. Clearly, in the world of retail, Walmart is #1, approaching a half trillion in annual sales. Costco is #2, with about a quarter of the sales volume of Walmart. You might consider Amazon a distant competitor, but their outsized annual growth makes clear that it is only a matter of time before they reach #3, globally. You could study just these three global retailers and learn a large share of what you need to know. If we want to add a fourth, it should be Kroger, because of their steady quarter after quarter growth in the United States alone.

Caution should weigh heavily on anyone who considers this through a historical perspective. As British Prime Minister Benjamin Disraeli remarked on ascending to the office: “‘At last I have reached the top of the greasy pole.” One hundred years ago, a new retailer, The Great A&P, with a new business model, quickly became the first retailer in the world to reach a billion dollars of sales. And just recently they filed their final liquidation bankruptcy, after decades of descent, with fruitless reorganization. The caution is that retailing is still a greasy pole.

It is my intention with this book to provide a very new perspective on who is #1. I’m quite confident that the shopper is #1, and I’m not saying that as some kind of feel-good PR fluff. Each of the four retailers first mentioned here, and many others, have all risen to their stature through making some aspect of the shopper #1, at some point in time. Walmart efficiently leveraged price, groceries, and a large selection to achieve their dominance. Costco efficiently leveraged price, groceries, and a limited selection, much of it non-grocery, to drive their growth. Amazon has efficiently leveraged novel technology for all three basic components of retail sales: a meeting of the minds of buyer and seller; close the sale with payment; delivery of the goods to the customer. And as the “Everything Store,” Amazon effectively has an infinite Long Tail. Kroger is in the chase because they have focused on the efficiency of the shopper, without neglecting their own efficiency.

You will see in Mark Heckman’s chapter on the Five Tenets, exactly what we mean about building your own sales through the efficiency of your shoppers. But here I want to put a spotlight on the reality of everyday retail, on what happens behind the screen, unseen by the shoppers. Indeed, many managers within the industry probably haven’t given adequate consideration to these facts.

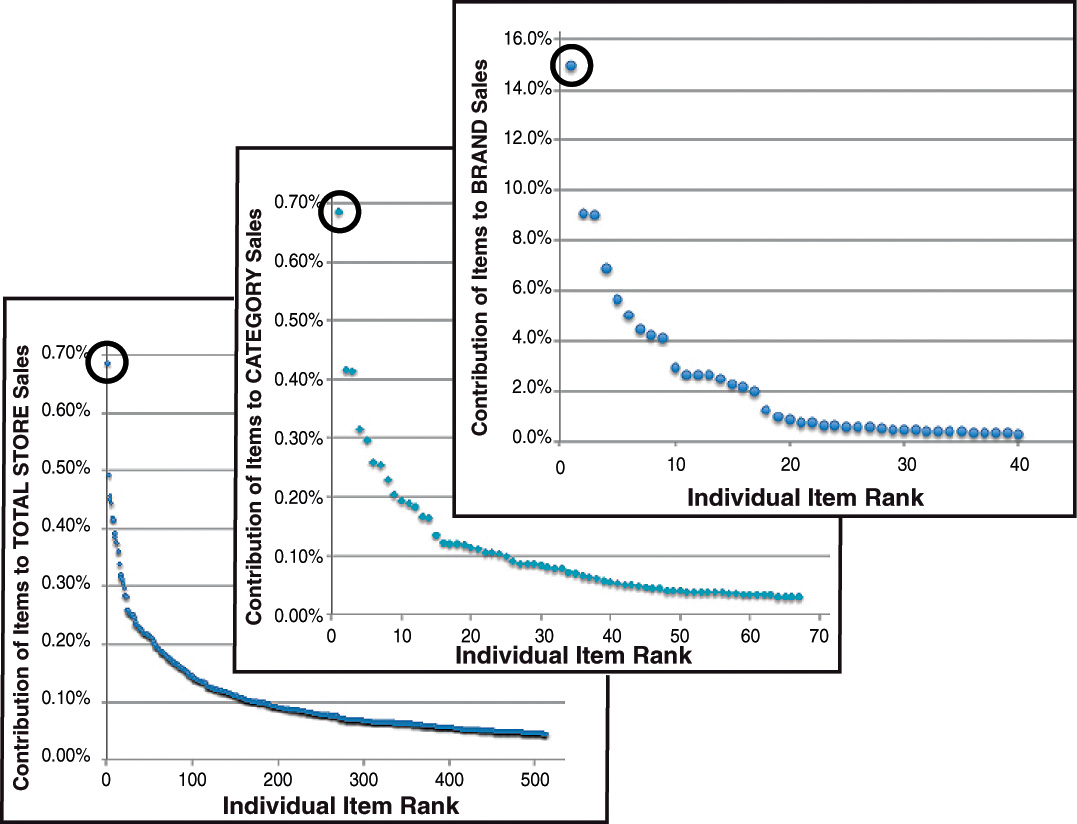

These three graphs (Figure P.1) show some solid illustrative data on who is #1. From these, it is important to see how the views of shoppers are related to, but radically different than, those of the typical bricks-and-mortar retailer. In the first graph on the left, the share of the store’s sales contributed by single items is displayed. The circled high point is in fact the #1 selling product in that store. In the second, middle graph, we see only the contribution of items in a single category to sales of that particular category. And the circled high point is the #1 selling item in that category. The third graph, in the upper-right, is the same type of graph, but in this case it includes data for only a single brand in the category. As with the other graphs, the circled high point is the #1 selling item for that brand manufacturer.

Each one of these #1s has a special significance for one of the three major manager categories at retailers around the world. The first major manager type is management representing the retail store itself. The stark fact is that many of these managers may not know just what that #1 selling item is. The reason is simple: That item is probably one of anywhere from a few thousand to hundreds of thousands of items in one of possibly hundreds or thousands of stores under their purview. Management is focused on a massive undertaking that scarcely makes allowance for focus on any one item.

The second type of manager we want to notice is the one associated with the manufacturers brand, the brand manager, whose product suite is illustrated in the upper-right graph. Brand managers have a greater opportunity for focus, with possibly anywhere from dozens to hundreds of items managed across a wide variety of retailers. The relatively tiny brand catalog—tiny in comparison to the retailer catalog—means that no retailer can be expected to have the knowledge of individual brand items that the brand manager does.

Now comes a major complicating factor. No one can reasonably manage 50,000 items. This can be thought of in terms of management span-of-control theory. Basically, supervisors work most effectively with 3–10 employees. As the number of employees increases, span-of-control increases—supervision becomes more problematic. Products are not people, but the general principle applies there also. In the interests of managing 40,000 different items in a store, retailers have been grouping them together into a couple hundred different categories. This reduces the problem from one of a totally unmanageable 40,000 items to one of maybe 200 categories with more like 500 to a few thousand items. For the past 30 years, the science of category management has come a long way.

However, there are still embedded serious conflicts that keep anyone from focusing on the shoppers. Please recognize that if you were buried under 40,000 items, or even a couple thousand items in a category, as a category manager, you would be overwhelmed from a span-of-control point of view. And this is exacerbated by the fact that all those different brands in the category are competitors. Competitors are not your friends, even if you are all polite. I don’t want to overemphasize the angst, but I have actually seen a grown man cry in a store because of what he believed his competitor was doing to him—through his “little children,” the brand products he was responsible for managing, on behalf of his manufacturer employer.

This is to give meaning to my statement that what is going on in the aisles of the stores is brand-on-brand mayhem, a gladiatorial contest with civilizing rules. Now, the interesting thing is that the retailer has someone assigned to each category, who ultimately has responsibility for what happens in that category. But every brand knows that only a certain amount of shelf space is allotted to the category, and to put it simply, every slot Brand A doesn’t fill, Brand X, Y, or Z will.

Note too that federal law forbids, under the threat of severe punishment, any collusion among the brands that might be disadvantageous to the shoppers. Another possibly shocking fact: Retailers do not want any one supplier to be too successful in selling their products to the shoppers. The reason for this is obvious when you realize that most of the retailer’s profits come from what are basically advertising fees paid by the brands supplying products to the retailer. These fees are totally legitimate, but they have to be negotiated independently with each supplier. This leads to the retailer essentially managing a serial blind auction in which each supplier comes in and makes a deal for his products with the retailer armed with no knowledge of the deals the retailer is making with others (as specified by law).

The result is that each supplier is essentially a “customer” for the retailer’s services: store, shelves, shoppers, and displays. And the retailer does best with a good number of healthy suppliers, with no one being dominant.

Now, obviously, this is not as neat as I have outlined here, but it reasonably accurately explains why no one is paying much attention to the shopper, other than being polite and pleasant and operating a store that is reasonably convenient to the shopper. After all, the retailer is essentially a merchant warehouseman who makes his money on that basis. And for self-service retailers, the shopper is an unpaid stock-picker who picks the products she wants and takes them to the exit to make payment. (All this means that the retailer mantra of 100 years ago, “Pile it high, and let it fly!” is still deeply embedded yet today in an industry that’s poorly understood, even by the global hordes employed in the industry.)

With all this in mind, you should see that any item that is #1 (or #2, #3, #4, and so on) actually got that way because the shopper, the true #1, gave that product the sales and rank it has. The shopper is always the real #1, and it is their innermost feelings and desires that are manifested in the total sales occurring in the store.

As you read this second edition of Inside the Mind of the Shopper and consider the concepts and ideas, the history and trajectory of global retail that we explore, remember: With all the power, money, and products at retail, it is the shopper that is #1!