Chapter 6

Private equity fund accountinga

6.1 WHAT IS HAPPENING IN PRIVATE EQUITY ACCOUNTING?

Private equity as an industry and as an asset class has “grown up” significantly over the last 20 years. This maturing of the industry has pushed private equity and venture capital from a quiet and veiled corner of the room, where it was regarded as a poor relation to the wider asset management family, to center stage. This transformation has brought with it many strains and stresses from public accountability through all areas of governance to reporting.

In essence the private equity and venture capital (“private equity”) business model is relatively simple. It is to invest pooled funds in assets that are typically not liquid to generate returns for the investors.

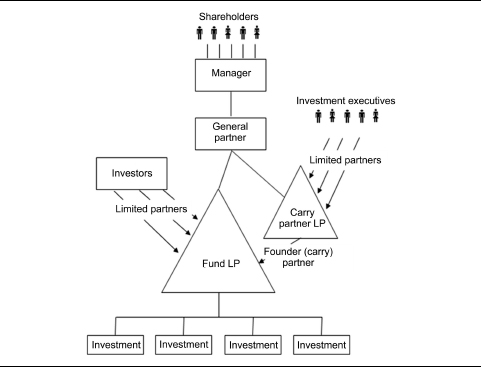

This chapter focuses on the accounting issues encountered in the U.K. private equity environment. Due to the many different detailed business models which fall under this simple business idea, it would be impossible to cover all the potential eventualities which may arise in a business designated as private equity. This chapter focuses on accounting common in the U.K., principally from the point of view of the most commonly used fund structure presented in Exhibit 6.1.

EXHIBIT 6.1 MOST COMMONLY USED FUND STRUCTURE

This chapter sets out the principles of and rationale behind accounting from the perspective of U.K. GAAP and IFRS. On occasion references are made to principles under U.S. GAAP. This chapter is not intended to provide any form of guidance in relation to U.S. GAAP and any references to it are for interest purposes only, particularly when anticipating the future for all accounting standards.

Care must be taken when applying these broad brush principles in practice to any individual situation as relatively small changes in facts can markedly change the consideration of the accounting.

6.1.1 Fund structure

Any fund is structured with two fundamental principles in mind. First, that the fund needs to be able to efficiently acquire, manage, and dispose of investments and, second, that the investor in the fund is not disadvantaged from a tax perspective when compared with investing directly in the underlying asset. This basic structure is then added to, usually to optimize the after tax returns to the individual managers.

Whilst the principles are relatively simple, the complexities of tax laws and the different applicable tax jurisdictions can result in enormously complicated structures. This chapter is based on a simple limited partnership structure set out in Exhibit 6.1. The principles discussed in this chapter are equally applicable to much more complicated structures but, for ease of explanation, this structure is assumed.

6.1.2 Why different GAAPs are used

There are two reasons that any entity prepares accounts for its investors, either because it is required to do so under statute or it has agreed that it would. In the U.K. commonly used GAAPs include:

- U.K. GAAP

- EU-adopted IFRS (“IFRS”)

- U.S. GAAP

- “Other”.

There has been a clear intention for many years for U.K. GAAP and IFRS to merge into a single set of standards. Many of the recent standards issued by the Accounting Standards Board (ASB) in the U.K. are designed to be clones as far as possible of their IFRS counterparts issued by the IASB. Sooner or later U.K. GAAP and IFRS will be deemed to be sufficiently identical for U.K. GAAP to no longer be relevant. In October 2010 the ASB published a Financial Reporting Exposure Draft on the future of financial reporting in the U.K. and the Republic of Ireland. This proposes a three-tier system: listed groups and publicly accountable companies will follow IFRS; medium-sized entities will report under the IFRS for SMEs; and the smallest companies will continue to follow the U.K. GAAP FRSSE.1

It has long been suggested that IFRS and U.S. GAAP would merge and the current publicly stated convergent date is December 2011. There have been significant steps towards convergence; however, there are obstacles remaining. There are still many differences between the principle-based IFRS and the more rule-driven U.S. GAAP (not least in the length, with U.S. GAAP being 15,000 pages long against IFRS at 5,000); however, with the recent issuance of the minutes of their joint meetings on consolidation, there is a clear intention to address the major issues quickly.

Which of the above GAAPs an entity uses will depend on its legal structure, the way it undertakes business, and any agreements with its investors. The common private equity vehicles in the U.K. are:

- Venture capital trusts (“VCTs”)

- Investment trusts

- “Qualifying” limited partnerships

- “Non-qualifying” limited partnerships

- Offshore limited partnerships.

Venture capital trusts

VCTs are vehicles that were established by the U.K. government with a view to encourage individuals to invest in venture capital by providing tax incentives to the investors. To qualify as a VCT there are many rules and regulations that must be followed, one of which is that the entity must be listed on the U.K. stock exchange. This means that the vehicles used are public limited companies. This automatically pushes the VCT into a rigid legislative framework, filing its accounts which have been prepared under U.K. GAAP or IFRS. In the U.K., listed companies are required to prepare their consolidated accounts in accordance with IFRS. As many VCTs do not take controlling stakes in their underlying investments, they can prepare accounts under U.K. GAAP or IFRS. Those that take control stakes are required to prepare consolidated accounts under IFRS. (The issues around consolidation are discussed in Section 6.2.1.)

Investment trusts

Similar to VCTs, this is a listed corporate vehicle and, so, is under a U.K. GAAP or IFRS reporting regime. Investment trusts are generally larger than VCTs and more likely to have invested in control positions. Those with control positions in underlying businesses are required to prepare consolidated accounts and report under IFRS. Those with no control positions may report alternately under U.K. GAAP.

“Qualifying” limited partnerships

From a reporting perspective, these are treated as if they are private limited companies. This means that they are required to prepare and file accounts under either U.K. GAAP or IFRS. Any limited partnership is governed by its limited partnership agreement (LPA). This sets out the contract agreed between the partners as to how the limited partnership will be managed and operated.

For many years, the interpretation by the lawyers of the legislation defining qualifying partnerships has meant that the limited partnership used in a typical private equity structure was determined not to be a qualifying partnership.

The Department for Business Innovation and Skills (BIS) under pressure from the EU has drafted an amendment and clarification to that definition which would result in the majority of limited partnerships being defined as “qualifying” and brought into the statutory reporting and filing regime. The implementation of this amendment, and the extent to which any non-standard structures are included within the definition, remains open. The amendment is expected to apply to accounting periods beginning on or after April 6, 2011.

“Non-qualifying” limited partnerships

A non-qualifying limited partnership has no statutory filing requirement. Accordingly, the only reason that accounts are prepared is because the LPA mentions that they will be. If the LPA states that “the accounts will give a true and fair view”, that statement would immediately push the reporting to be under U.K. GAAP or IFRS. A “true and fair view” is a defined term under the Companies Act and the only way to comply with the LPA requirement is full Companies Act accounting and disclosures.

Many LPAs state that “the accounts will be prepared on the basis of the policies agreed between the Manager and the Auditor”. This allows the manager (within reason) to select those accounting policies which he or she believes are appropriate for the fund, and to ignore those elements of GAAP, either policy or disclosure, which the manager considers unnecessary. These are the policies described as “Other”. A non-qualifying limited partnership can of course adopt any of the recognized GAAPs (U.K., U.S., or IFRS) should it so choose.

In practice this usually means that the fund will follow, rather than comply with, U.K. GAAP with certain exceptions, notably consolidation and the accrual of income. The issues arising from a requirement to consolidate are discussed further in Section 6.2.1. If the accounting policies state that the fund will not consolidate control positions, then these issues fall away at the fund level. U.K. GAAP would require that income on instruments that are loans is accrued evenly over the period, even when interest is only expected to be paid at the point of realization of the loan. A common policy adopted is that the fund will recognize income in relation to a particular investment when that investment is realized.

Whilst the accounting framework of “Other” simplifies certain aspects of reporting, it does not remove the requirement for the fund to prepare taxation returns under either U.K. GAAP or IFRS accounting policies.

In addition to any statutory reporting requirements, additional reporting may be required by the terms of the LPA. Due to the drafting in New York State of the regulatory requirements of insurance companies, U.S. investors in a limited partnership will be subject to an additional capital requirement if they do not receive U.S. GAAP accounts for the limited partnership. As a result, it is common for LPAs with U.S. investors to include a requirement to additionally report under U.S. GAAP to the investors.

Offshore limited partnerships

An offshore limited partnership will be governed by the local statutory and regulatory environment. The private equity market has tended to utilize those offshore centers that provide them with the appropriate tax regime, coupled with limited statutory reporting. As a result, any of the GAAPs referred to above may be encountered in offshore structures, depending on jurisdiction.

6.2 CURRENT MAJOR ISSUES AND COMPLEXITIES

In discussing accounting issues, implications, and proposed courses of action to change the accounting, the principles that may be followed are set out in this section. For many of these issues, the preparer of the accounts must use his or her judgment as to how to apply these principles. In any situation it is crucial to assess the individual case on the basis of the available facts and not merely assume that these broad brush principles may be applied automatically in all similar situations without that detailed consideration.

The first rule of accounting for any limited partnership is to read the limited partnership agreement (LPA) to completely understand the contractual relationships between the partners.

6.2.1 Consolidation issues

The case against consolidation

Accounting standards have generally been formulated to fit the majority of business models encountered in a corporate environment. For a shareholder in a conglomerate, it is highly relevant to them to understand the overall financial operations of the group as a whole and the group’s financial position. This consolidated information gives the reader of the accounts a basis upon to make relevant judgments as to the performance and expected future cash flows that they might derive from that business.

This is one clear area where the business model of private equity is not suited to the developed accounting standards. Private equity entities will commonly take control positions in underlying businesses to give them the ability to manage the new investment in the manner that they see fit.

In a conglomerate, the investor can judge the management team and look for their investment return from all the entities that are controlled within the group. In a conglomerate the dividends to the investors are paid from profits generated by the group and, indeed, the earnings of the group and expected dividend stream are important metrics in establishing a price for the shares.

In private equity, this information on the consolidated operations is largely irrelevant to an investor. Their investment returns are generated from the ultimate realization of the underlying entities. The financial position of the fund is not assessed by an investor adding together all the individual underlying asset and liability classes. The performance of the fund is not judged by adding together the turnover, costs, and profits or losses of a collection of disparate businesses. The investor assesses the fund by considering the value of the underlying businesses, and it is this assessment which allows the investor to estimate his or her anticipated investment returns from future realizations. Accounting standards generally agree with this assertion, so long as the fund only holds a small equity position. Accounting standards require that, once you own sufficient equity to control a business, that the accounts should reflect a consolidation of all the businesses so controlled.

For a private equity investor, the value of the investments in the fund, treated in the same way regardless of the size of the equity holding, is highly relevant information—a summation of assets and liabilities is not.

This focus towards value also reflects the way that private equity managers run their businesses. They are closely involved with the strategic direction of the company and board decisions, focusing on deriving value for their investors. Whichever GAAP is used, there are commonly applied processes, practices, and judgments that remove the requirement to prepare consolidated accounts, but each situation must be considered on its own merits and facts.

Consolidation within the fund

As noted above, consolidated accounts do not provide relevant information to the investors. As a result, fund reporting focuses on being able to provide information on the basis of fair value rather than consolidation. To understand how this is achieved in most situations, we need to consider the accounting standards and other pieces of legislation that drive the requirement to consolidate.

Reporting under IFRS

Under IFRS, IAS 27 (“Consolidated and separate financial statements”) requires that an entity consolidates the entities it controls. “Control” is defined as “the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.” In a situation where a single entity owns more than 50% of the equity in an underlying investment, it is difficult to argue that these control conditions are not met. This is one of the major reasons why the private equity community avoids IFRS whenever possible.

If, by careful fund structuring, no single entity “controls” the underlying investment, there is no requirement at fund level to consolidate. So, for a fund proposed to be structured as a limited partnership, if a number of parallel limited partnerships, bound together by a co-investment agreement and ensuring that no single partnership is larger than all the others put together, jointly acquire a controlling interest, then no individual limited partnership can be deemed to control the investment.

The option of splitting the fund vehicle into subscale elements may not be possible in certain situations, such as a standalone investment trust. When an investment trust directly owns a controlling stake in an underlying business, it is likely that the trust will be required to consolidate the results of all its underlying controlled investments. In this situation, the best option may be to accept that consolidated accounts are required and to provide relevant valuation information to the investors alongside the consolidated accounts. Single-entity accounts which include all investments at valuation may be prepared and published together with the consolidated accounts.

In addition IFRS 8 (“Operating segments”) may support the provision of valuation information. Generalizing, IFRS 8 requires that information be reported on the same basis that senior management use to make resource allocation decisions. In that a private equity fund’s acquisition and disposal decisions are made on the basis of investment valuation, the valuation of investments might be expected to be the basis of any IFRS 8 disclosures.

Reporting under U.K. GAAP

U.K. GAAP (FRS 2, “Accounting for subsidiary undertakings”) has the same definition of control as IAS 27. There is, however, an important distinction. U.K. companies reporting under U.K. GAAP report in accordance with the Companies Act 2006. The requirement for an entity to consolidate those other entities it controls is embodied in that Act, not merely in the accounting standards.

Also embodied in the Companies Act is the concept of a “true and fair override”. If those responsible for the accounts of an entity believe that the accounts would not give a true and fair view by following a particular accounting standard, then the override may be invoked and the accounts can be prepared on the alternate basis, disclosing the impact of the departure (where available). It is common for fund accounts to be prepared on the basis of all investments being reported at fair value, invoking the true and fair override. It is usually not possible for the preparers to disclose the impact of the departure, as these amounts are unknown.

It is worth noting that this route is not permitted when reporting in an IFRS environment. Under IFRS, an equivalent of the true and fair override is technically available, but hard to achieve in practice. This is partly because IFRS has no facility for non-consolidation for held-for-sale assets and, second, because IFRS is a global GAAP. At a global level the prevailing view of accountants applying IFRS is far less inclined to see consolidation as not true and fair.

A qualifying partnership is exempt from preparing consolidated accounts if the partnership is dealt with on a consolidated basis in the group accounts of its parent. In the context of a limited partnership with a single general partner (GP) and that GP or its parent prepares consolidated accounts, the limited partnership is permitted to take this exemption. This exemption removes the requirement to prepare consolidated accounts, but moves the issue higher up the control structure. Consolidation within these higher entities is discussed in the section below.

Reporting under U.S. GAAP

U.S. GAAP has anticipated these issues arising from consolidated accounts. For a private equity entity once it has determined that it is an “investment company” (as defined), it may follow the AICPA’s Investment Company Accounting Rules. In essence, these remove the requirement to consolidate and all investments may be included in the balance sheet at fair value.

It is worth noting that with the convergence program, the IASB would appear to be considering a similar principle for IFRS.

Consolidation within the manager or GP

In a typical structure (as set out in Exhibit 6.1), the limited partnership is a subsidiary of the GP, which is in turn a subsidiary of the manager. This would suggest that the manager is the ultimate controller of the limited partnership and, potentially, any controlled underlying portfolio companies. Typically, the manager has a small or even zero interest in the fund with the economic benefit going to the investors and the carried interest partners. In the extreme situation, where that interest is negligible, the manager’s accounts would consolidate the results and financial position of the GP, all the limited partnership and portfolio subsidiaries, with all profits and net assets arising from fund activities being included as a minority interest. Deciphering, from a set of accounts that were prepared on this basis, the results of the financial operations arising from management activities and the financial position of the manager would be very difficult.

Reporting under IFRS

In the structure shown in Exhibit 6.1, the GP is the only entity entitled to manage the operations of the limited partnership, but the question arises as to whether the GP “controls” the limited partnership as defined in IAS 27. The fact that the GP has the ability to govern the financial and operating policies is not open to debate. Questions arise as to whether these policies are controlled “for benefit” or whether there are other restrictions over its ability to govern.

In this context “benefit” may be interpreted as meaning ownership benefits. The question then arises as to whether the GP is managing the limited partnership to derive ownership benefits or remuneration from management activities. For the purposes of interpreting the standard, these functions are considered separately.

In the event that the GP’s interest in the limited partnership is negligible and is only remunerated (in line with market rates) for management services, the inflows received are clearly from its management activities and not from “controlling the policies for benefit”. In this situation, it may be reasonably held that the GP does not “control” the limited partnership.

It is common for GPs (or managers) to be required by the limited partners (LPs) to invest in the limited partnership. In this situation, the GP is acting in a dual role, partly as manager, partly owner. When considering whether the GP, acting in a dual role, is deriving benefit from its ownership or management activities, we need to ascertain for which activity the “benefits” are being received over the expected life of the fund. This question is further complicated where carried interest is also received by the manager, GP, employees, or partners. It is typically argued that carried interest is a benefit of management (regardless of how it is structured for taxation purposes) since it is only available to the management team, does not carry the full downside risk if performance is negative overall, and is linked to the profits generated from the management activity.

The whole question of “for benefit” is highly judgmental and each situation must be carefully considered on its own facts. If it is decided that the manager receives significant benefit from ownership interests, then it might be expected that the limited partnership is consolidated by the manager as the owner of the GP. Conversely, if the majority of the inflows are anticipated from management activities, then it might be reasonably held that the GP, whilst controlling the limited partnership, does not do so for ownership benefits.

The limited partnership agreement (LPA) will establish the rights and responsibilities of the individual partners. Limited partners are excluded from the management of the limited partnership, since involvement in the management imperils their limited liability protection. The LPs can, however, retain rights of removal and appointment over the GP, without damaging this status.

If LPs reserve the right to remove the GP and appoint a successor (commonly referred to as “kick-out rights”), then it may be held that the powers of the GP are restricted. Whether these kick-out rights are sufficient to maintain that the GP does not have control (“substantive kick-out rights”) is a matter of judgment. Typically, to be substantive it must be reasonable that these rights may be exercised. This consideration would include the number or percentage of the LPs who would need to vote for removal, whether specific grounds were required to initiate the process, the overall cost to the LPs by following this course of action, and anything else that might provide a barrier to the rights being exercised.

Where the LPA is structured to ensure that substantive kick-out rights exist, particularly in situations where there is a single LP with a significant interest, the right to eject the GP (and thereby control the limited partnership) may have inadvertently been placed in the hands of a single investor. Should this be the case, the requirement to consolidate the limited partnership has merely moved from the GP to one of the LPs.

Reporting under U.K. GAAP

Much of the U.K. GAAP analysis is similar to that for IFRS, but there are subtle distinctions. As noted in the section above, the requirement to consolidate is enshrined in the Companies Act. FRS 2 then provides guidance as to how you should undertake the consolidation.

In the section above (considering this issue in an IFRS environment), the requirement to consolidate is only present where the control (i.e., governing the policies for “benefit”) test is met. Although FRS 2 has the same definition of control as IAS 27, the analysis—which concludes that there is no benefit to the controller—is less relevant under U.K. GAAP, since the Companies Act has determined that consolidation is required.

Preparing consolidated accounts at the level of the manager allows the exemption from consolidation to be taken by the limited partnership. Rather than prepare fully consolidated accounts with a significant minority interest, we may prepare consolidated accounts that consolidate the underlying subsidiaries on a proportionate basis (“proportional consolidation”). This requires an invoking of a true and fair override of the method of consolidation required by the Act. Under proportional consolidation the accounts of the parent include, on a line-by-line basis, its share of the underlying entity’s results and financial position. Where the interest in the limited partnership is zero, there will be no differences between the entity-only accounts and the consolidated accounts. This way the results arising from the activities of the manager group can be clearly reported.

Where the effective interest of the manager in the limited partnership is small but not negligible, judgment is required. The question arises as to whether the exclusion of accounting entries representing the manager’s small share of each accounting item is materially incorrect, or not. Typically, the manager’s consolidated accounts would show no differences to the entity standalone accounts, so long as the interest is only a few percent.

The analysis under IFRS of restrictions over control equally applies under U.K. GAAP and, in the event that substantive kick-out rights exist, the manager would not be required to consolidate the limited partnership. In this event, however, the available exemption from consolidation through being included in the consolidated accounts of a parent would not be available to the limited partnership.

6.2.2 Priority profit share

In a limited partnership structure, the GP is commonly entitled to receive a priority share of profits in consideration for managing the limited partnership and for having unlimited liability. This may be referred to as management fee, priority profit share (PPS), or GP’s share (GPS). Frequently, this share is around 2% of the committed capital or net cost of investments made.

The LPA is structured such that the GP is entitled to this amount of any profits arising, before any profits are allocated to the LPs. To ensure that the GP has sufficient resources to meet its costs of management, in the event that there are insufficient profits to cover the PPS, an interest-free loan is made by the limited partnership to the GP. This loan is not repayable, it may only be settled by the future allocation of profits.

In the accounts of the fund (U.K. GAAP and IFRS)

From these facts, it is clear that the GP receives an annual amount for taking on its role as GP, which is never repaid. In substance, this is akin to a management fee and it should be recognized in a similar manner in the accounts of the limited partnership.

Commonly, this will be shown as a deduction from profits (or losses) in the income statement. In early years the fund is unlikely to generate profits, and it is important that the PPS is recognized in full in the income statement and allocated fully in the partners’ accounts.

The rationale for this treatment is that:

- The substance of the transaction is an expense payment rather than a loan

- The loan cannot be recognized in the balance sheet as an asset since it does not meet the definition of an asset

- Even if it were recognized as an asset, it should be considered as impaired, since it is not repayable.

In the accounts of the manager (U.K. GAAP and IFRS)

The treatment under the accounting standards and the U.K. taxation rules differ widely for the receipt of PPS for the manager. In the accounts, the receipt is recognized as turnover on the basis that it is in relation to an annual contract and is not repayable.

It is worth noting that, for taxation purposes, the tax nature of the receipt follows the strict legal form rather than the accounting form and, so, only falls to U.K. tax as taxable profits are generated by the limited partnership and allocated to the manager.

6.2.3 Carried interest

The carried interest partner (CIP) (also sometimes known as the founder partner or special LP) is an investor in the limited partnership. Its purpose is to be a vehicle that aligns the interests of the investors and the managers, rewarding those managers with a share of realized profits in a tax-efficient manner. Carried interest schemes typically operate on the basis of realized profits—and not portfolio valuations as for some schemes common in other alternative asset classes.

The CIP will typically have an investment in the limited partnership capital, but no loan commitment. This capital commitment entitles it to a percentage (10% to 25%, but most commonly 20%) of the realized profits generated by the fund. A target rate of return (the “hurdle rate”) may be set for the fund. Hurdle rates vary depending on the type of fund, anticipated market returns in that geography, and the overall carry arrangements. Typically, these are between 5% and 12%.

The timing and share of the profits to which the CIP is entitled are set out in the LPA. In considering the accounting treatment of any carry scheme, the exact terms of the agreement must be considered in detail. To discuss the principles of the accounting, this section focuses on three different types of schemes:

1. Deal by deal with no hurdle or clawback (one end of the range).

2. Deal by deal with a whole fund calculation and clawback.

3. Whole fund with hurdle (the other end of the range).

What do these descriptions mean in terms of the commercial reality in the carry schemes? “Deal by deal with no hurdle or clawback” means that the CIP shares in the profits realized on each deal as it arises, does not need to return a target rate of return to the investors prior to sharing in the profits, and does not share in any realized losses. This type is scheme is rarely seen in Europe any more, since it is generally viewed as being too generous to the CIP at the expense of the investors.

“Whole fund with hurdle” means that the CIP only shares in realized profits after the investors have received all their original investment, plus a target rate of return. This is probably the most common basis agreed in the current market as it ensures that the CIP only benefits from its investment after the managers have fulfilled the fund objectives. This typically results in carry only being paid to the CIP 6 to 10 years after the fund was raised.

“Deal by deal with a whole fund calculation and clawback” is essentially the same commercial term as “whole fund with hurdle”, but the scheme allows payments to be made and subject to reclaim by the fund. Payments may be made to the CIP when profits are realized, so long as the fund remains on course to achieve its objectives and that the amounts can be recovered from the CIP in the event that this proves to be false. The obvious advantage to the CIP of this scheme is that payments may be received earlier in the lifecycle of the fund. Commercially, it is the same as a whole fund scheme allowing for payments on account.

Between the extremes there is an infinite number of quirks and variations that may be introduced through the LPA negotiations. Whatever the quirks and variations, the accounting issues arising should all fall within the same principles as the three schemes set out in this section.

In the accounts of the fund (IFRS)

In considering the treatment of carried interest in the accounts, it is important to appreciate the distinction between profits being allocated and distributions being made. Once the fund has been raised, there are two critical trigger points in the lifecycle of a fund which significantly change the expectations of carry being paid.

The first trigger (Trigger Point A) is when the fair value of the fund’s investments exceeds a value whereby, if all the investments were sold at that value, carry would be due to the CIP. The second (Trigger Point B) is when the conditions are met such that carry is actually due to the CIP.

In considering the accounting for carry in the common limited partnership structure, it is crucial to appreciate that carry can never be an expense of the limited partnership. The carried interest mechanism is merely an allocation of profits between the various partners in the limited partnership.

Typically, in a fund investments are classified as “fair value through profit and loss”. Whilst “available for sale” may appear to be an accurate description of the fund business model, private equity frequently uses complex capital structures and special terms on realization. If the assets are designated as available for sale, detailed consideration and possible separation of any embedded derivatives are required.

The terms of the carried interest arrangement are commonly that the CIP’s entitlement to receive carry is only at the point of realization.

For any type of scheme, typically fair value movements during the asset-holding period are taken to the LPs’ accounts. To simplify the reading of the accounts, many preparers of limited partnership accounts will credit all fair value movements to a separate “fair value” reserve.

Whichever treatment is adopted, after Trigger Point A is passed, a useful disclosure to make is a simple statement that discloses the amount that would be allocated to the CIP in the event that the investments were sold at their carrying value. The different types of scheme determine when profits are allocated to the CIP and distributions made to them.

With a deal-by-deal scheme, since the CIP is entitled to a share of the profits at the point of realization, a share of each realized profit together with a transfer of historic fair value movements is allocated to the CIP. On realization, cash is distributed to the partners in accordance with the LPA. The cash will reduce the balance outstanding on the LPs’ loan accounts and the income accounts of both the LPs and the CIP.

Under a “whole fund with hurdle scheme”, proceeds from realization and other realized profits are distributed to the LPs as repayments of their loan capital and any profits allocated. All profits are allocated to the LPs (or the fair value reserve) until Trigger Point B, when the CIP is due to receive its share (commonly 20%) of all future distributions from the fund. This is reflected in the accounts by transferring an amount equal to the CIP’s share of all remaining net assets from the LPs’ accounts to the CIP. Future profits are allocated in the profit-sharing ratio and cash distributions follow the terms of the LPA.

The terms of the LPA will determine when Trigger Point B is achieved. This may be when the LPs have received back in cash from the fund their loan capital together with the hurdle. If a fund draws more loan capital down from the investors after Trigger Point B (sometimes permitted under the terms of the LPA to provide additional funding to existing investments), the CIP is not entitled to any profits until that further loan and hurdle thereon is repaid. During this period after the trigger being met and undone and before Trigger Point B is re-achieved, the accounting is less clearcut and subject to judgment. It may be held that the subsequent drawdown of loan is of such a size that Trigger Point B will not be reached again, in which case the allocation to the CIP should be reversed. More commonly, it is anticipated that Trigger Point B will be achieved again in a reasonable period of time and allocations to the CIP are merely ceased until that date.

As might be imagined, “deal by deal with a whole fund calculation and clawback” is an amalgam of these accounting treatments. The terms of these types of agreements vary hugely, but a typical commercial agreement would be that the CIP partners may share in the profits arising on realizations, so long as the valuation of the investments in aggregate exceeds the amount of loans and hurdle outstanding. Any amount distributed is paid into an escrow account, under the control of the CIP, which is available to be clawed back by the limited partnership in the event that the fund does not ultimately meet its objectives (clawback). The CIP may withdraw funds from the escrow account subject to a separate set of rules and conditions.

In these situations, calculating Trigger Point B can be a complex calculation depending on the LPA terms. Once it is passed, the CIP may participate in the next realization, so long as it continues to be passed at that time. On realization of an investment, the appropriate share of the profit is allocated to the CIP and an amount is distributed to the escrow account. At this time, although the fund expects to achieve its objectives, this ultimate outcome remains uncertain. Accordingly, it is unlikely that there will be an allocation of unrealized profits to the CIP from the LPs within the partners’ accounts.

So long as the fund continues on track, it is unlikely that the accounts of the limited partnership will reflect any balance held in the escrow account. Typically the fund is excluded from the LP accounts as the CIP, subject to the escrow rules, has control over the funds. If the performance of the fund declines, the amounts distributed to the CIP may be accessed by the limited partnership to distribute to the LPs. The amount required to restore the LPs’ position might then be recognized as a receivable amount in the limited partnership accounts. Whether the full amount of the receivable should be treated as recoverable will depend on the individual circumstances. If the balance resides in the escrow account, recovery is reasonably certain. Once amounts have been distributed to individual managers who participate through the CIP, recovery is likely to be more difficult.

In the accounts of the fund (U.K. GAAP)

U.K. GAAP still retains a choice of alternate accounting policies for investments. The accounting policy of reporting investments at the “lower of cost or net realizable value” remains valid. It is, however, rarely used since the value of investments is critical to a proper understanding of the affairs of the fund.

FRS 26 (“Financial instruments measurement”) results in accounting treatments similar to reporting under IFRS. FRS 26 is optional for most entities at the present time and is rarely adopted by private equity funds due to the additional standards that are required to be adopted and the extensive disclosures.

As a result, the majority of private equity funds will adopt an accounting convention of “historical cost as amended for the revaluation of fixed asset investments.” This allows the preparer of the accounts to include investments at valuation, without significant additional disclosure. Typically, the fair value movement will be shown underneath the profit and loss account, the balance of which is taken to a revaluation reserve or allocated to the LPs’ accounts. Alternately, the fair value movement is included in a separate statement of total recognized gains and losses.

The accounting principles for recognizing profit allocations and distributions to the CIP under the different schemes are common to those followed under IFRS.

In the accounts of the CIP (IFRS)

In preparing the accounts of the CIP, the main considerations are the recognition of income and the treatment of the investment in the fund.

Carried interest vehicles are commonly limited partnerships, as this can preserve the tax nature of receipts from the fund. These have historically been non-qualifying limited partnerships and may be managed by the GP, the LPs being the individuals involved in the management of the fund. Since the potential recipients of the accounts are themselves closely involved in the management of the fund, they often will believe that they are sufficiently aware of the results and financial position not to need audited financial statements and, accordingly, the reporting requirements of the CIP are minimal. It would be extremely unusual for the managers to prescribe a requirement for IFRS accounts through the LPA.

Carried interest should be recognized by the CIP when it is probable that future economic benefit will flow to the CIP. Under the terms of a typical LPA, these conditions are both met at the point of realization of an underlying asset in the fund. The contractual receipt of realized gains is relatively straightforward. The complications arise in the interaction between the carrying value of the CIP’s investment in the fund, the realization of gains, and any clawback provisions.

Although it may be suggested that the CIP’s interest in the fund is a derivative of sorts, this investment by the CIP in the fund is best regarded as an extremely highly geared investment. Under IAS 39, the investment in the fund is recognized at fair value. Fair value of unquoted private equity assets is discussed in more detail in Chapter 10. In considering the fair value of the CIP’s investment in the fund, there is usually no market for that interest and the preparer has to estimate the fair value based on what a hypothetical third party might pay for that interest.

At the establishment of the limited partnership that will become the fund, following the commitments of LPs, the only asset of the limited partnership is the capital introduced. If there are no further assets or agreements, the cost of the capital introduced is likely to be the most reliable indicator of value on the date when it is introduced. Thereafter, the fair value estimate is subject to significant judgments and opinions.

One cannot set out established rules for estimating the value of the CIP’s interest in the fund. Ultimately, the fair value will be based on the expected timing and quantum of returns generated from that investment. The following points in the life of the fund might reasonably be expected to change an individual’s views of the likelihood or quantum of those returns:

- The LPs making commitments to the limited partnership and the fund closing

- The fund being fully invested

- Trigger Point A when carried interest would be paid if the investments were sold at their carrying value

- Trigger Point B when the CIP is entitled to a share of future realizations

- Actual receipts of carried interest

- Liquidation of the fund.

In the accounts of the CIP (U.K. GAAP)

If the LPA stipulates U.K. GAAP and the manager has adopted FRS 26, then the accounting treatment would be the same as for IFRS above. More usually, FRS 26 is not adopted and the accounting policy for investments is that they are held at the lower of cost and market value. This removes the requirement for the accounts’ preparer to estimate the fair value of the CIP’s interest in the fund. Income from realizations is recognized as it is earned, commonly on realization of the underlying investment assets.

In the accounts of the manager

The CIP may be consolidated into the accounts of the manager under either GAAP. The consideration of whether consolidation is appropriate is similar to that for consolidation of the fund (i.e., is the manager “controlling the CIP for benefit”?). If the carried interest receipts are entirely directed to the individual managers as LPs on the basis of their original personal investment with no carried interest being paid to the manager, it is likely that the CIP will not meet the requirements for consolidation. If the manager receives a significant element of the carried interest in its own right or is able to direct the payments amongst the individuals after the CIP’s establishment, then it is likely that the manager would be held to be “controlling for benefit” and the CIP consolidated.

In practice, the situation is generally less clear than these extremes. The preparer of the accounts needs to consider all the terms by which the individuals invest including vesting rights and the provisions regarding an individual’s rights to the investment on leaving the organization. The more terms that exist putting rights into the hands of the manager over the individuals, then the more likely it is that the CIP should be regarded as a vehicle of the manager and consolidated. If the CIP is consolidated, then the receipts by the CIP would be income in the manager’s consolidated accounts and the payments to the carry recipients treated as minority interests. When the manager does not consolidate the CIP or the fund, there will be no entries in the primary statements relating to the receipts and subsequent payments.

The payment of carried interest through these vehicles is, however, generally held to be a payment from a subsidiary to senior members of management. The existence and the total amount paid or allocated should be disclosed under U.K. GAAP and IFRS in the accounts as a related party transaction.

6.2.4 Partners’ capital

In a typical limited partnership, there are two types of “capital”. All the partners make a capital contribution with the LPs additionally providing loan capital. The ratios of the capital contribution are commonly the same as the carried interest participation by the CIP, so for a 20% carry scheme the ratio for the CIP to the LPs will be 1: 4. The GP will normally only make a nominal contribution to the capital, unless required to make a contribution as a co-investment alongside the LPs. The loan capital provided by the LPs is a significant multiple (up to 100,000 times) their capital contribution. The bulk of the “capital” for investment is provided in the form of subordinated loans, since this allows for the simplest legal processes in terms of drawdown and distribution.

The first question is whether the capital contribution may be regarded as equity or whether, being of a finite life and due to be repaid at the end of that life, this should be regarded as a liability.

Under IAS 32 and FRS 25

The principal feature of this capital contribution is that it entitles the holder to participate in the profits and net assets of the entity on a winding up. The winding-up date is largely predetermined by the LPA. The only feature that would suggest that this is a liability is that it will ultimately be repaid. A reading of the standards can reasonably conclude that, where an equity instrument is redeemable at the end of the expected life of the vehicle, this factor alone would be insufficient to make the instrument a liability. Accordingly, the capital contribution is generally regarded as equity capital.

In a private equity limited partnership, the “loan capital” or “commitment” from the LPs has the following characteristics:

- It is drawn down on demand by the GP

- It is redeemable when the GP deems it appropriate

- It is not subject to any repayment schedule

- It bears no rate of interest

- It is unsecured

- It is only repayable to the extent that funds are available to make the repayment

- To the extent that it has not been redeemed at the conclusion of the limited partnership, it will be written off

- It ranks below any external creditors.

To many, this would appear to have few characteristics or risks associated with a loan and be more akin to an equity risk. However, although subordinated, these “loans” do not entitle the holder to participate in the residual net assets of the entity and the capital contribution of the partners ranks lower than these loans. Hence, these loans should properly be shown as a liability of the limited partnership.

As the allocation of profits and losses are predetermined by the LPA, amounts allocated to the partners are similarly shown as liabilities of the partnership. This results in a balance sheet adding down to a small figure, being the capital contribution of the partners. In order to assist the LPs in interpreting the accounts, all the amounts due to and from the partners are usually included at the foot of the balance sheet.

6.2.5 Responsibility shift

The fund accounts are a critical element of the reporting that a fund makes to its investors. It is likely to be an annual part of a range of regular investor reports covering portfolio companies and fund progress.

Investor reporting has advanced significantly as the private equity market has matured and continues to develop further each year. Much of the current drive behind the enhancement in investor reporting has been driven by changes in accounting by the investors. Prior to 1999, most investors would report their private equity interests in their own accounts at (impaired) cost. Accordingly, investor reports were treated as a reassuring signpost that the fund was heading in the right direction, but little use was made of the accounting data in the reports.

Now, the majority of investors will be required to include their private equity interests in their own accounts at fair value. This has resulted in an important shift in responsibilities from the GP to the LPs. If a LP is to use the valuation of the fund reported to it by the GP, it must satisfy itself that the valuation is free from material error. In effect, the GP’s reported number becomes the LP’s number the moment that the LP includes it in its accounts. An LP needs to have processes in place to allow it appropriately to assess and challenge the limited partnership accounts.

6.3 INTERPRETING FUND ACCOUNTS

The fund accounts can provide the investor with a large amount of information, but for this case study we shall focus on a number of questions that are fundamental to the LP’s understanding of the accounts. These questions are:

- What GAAP is used?

- How much did the LP put in?

- How much more might the LP be called upon to invest?

- How much has the LP received back?

- What is this costing the LP?

- How much will the LP get back and when?

- What value should the LP put in his/her accounts?

Appendix 6.A to this chapter contains the financial statements of Zebra Fund LP for the year ended December 31, 2009. Zebra Fund is an English limited partnership, established by an LPA dated June 4, 2004 as restated and amended on May 12, 2007. The fund commitments at final close amounted to USD130mn.

We consider the questions above for the LP entitled Employees Fund in the subsections below.

Which GAAP is used?

Confirming the GAAP used and the basis of preparation is the first step in interpreting the accounts. The GAAP provides the broader background within which the accounts are prepared.

Note 2 “Accounting policies” includes the reference to the accounting convention as: “These financial statements have been prepared in accordance with the applicable accounting standards and in accordance with the historical cost accounting convention as modified by the revaluation of investments.” There is no clear reference to which GAAP these have been prepared under.

Throughout Note 2 there are references to financial reporting standards. These are U.K. GAAP terms, but there is no reference to U.K. GAAP. This would indicate that the accounts are prepared under the GAAP referred to in Section 6.1.2 as “Other” and, whilst it has adopted many U.K. GAAP standards, the basis of preparation is not fully in compliance with U.K. GAAP.

This is confirmed by the report of the auditors which gives as the opinion, “In our opinion the financial statements for the year ended 31 December 2009 have been properly prepared in accordance with the accounting policies set out in note 2 to the financial statements and in accordance with the LPA.”

The key identifiers in this report are the absence of the term “a true and fair view” and no reference to a particular GAAP in the audit report. It is the report of the auditor which confirms the GAAP used. This means that all that the reader of the accounts can assume in relation to the accounting policies adopted will be set out in the notes to the accounts.

How much did the LP put in?

This should be a question to which the LP already knows the answer, and Zebra Fund’s financial statements provide a confirmation or reconciliation to that amount. Note 9 “Total Partners’ Funds” gives details of the transactions between the fund and the LPs. The size and format of partners’ notes varies widely. If a fund has a large number of LPs, disclosing in the notes the movement for the year on each partner’s account, together with the cumulative movements since inception, will lead to a note of many pages in length. This example is typical in format whereby the movement in the year is shown for the LPs as a whole and the cumulative movement by individual partner. The final table in Note 9 shows that the Employees Fund has provided cumulative loan drawdowns of USD14.65mn.

Lack of symmetry

There are a number of factors—which stand out when considering this note—that should alert the reader that this fund has an unusual allocation structure. In a typical limited partnership all transactions with the LPs take place symmetrically across all LPs. If an LP provides 20% of the total LPs’ commitment, the LP would expect 20% of the drawdowns, distributions, and income allocations. Maintaining symmetry is preferable from an administrative point of view, but is not always possible. This asymmetry complicates any interpretation of the accounts.

Clearly the Zebra Fund is asymmetric as we have loans drawn down from the investors and income allocations which are not in proportion to their individual commitments. The fund has made distributions to only two of the LPs and the CIP, whilst the other LPs have received nothing.

There are several ways that asymmetry may be introduced into the limited partnership. Certain investors may be excused from investments in certain jurisdictions or industries. In the situation of Zebra Fund LP, there is a long period from commencement (June 4, 2004) to final closing (May 12, 2007). The fund is established within the single limited partnership as two separate pockets in which individual investors (including the CIP) have invested, depending on when they joined the limited partnership. The fund was originally set up with a commitment of USD60.00mn. Drawdowns were made from the first two investors (Employees Fund and Pension Fund) of USD22.00mn in the ratio of their commitments 20:40. These investments were realized prior to the other partners being admitted, generating gains of USD55.00mn. These realizations triggered an allocation to the CIP under the terms of the original LPA since all loans that had been drawn down at that date, together with the hurdle, had been repaid. This information was all included in prior period accounts.

When additional partners were admitted at the final closing and the Pension Fund increased its commitment, for accounting and carry purposes two pockets were effectively created, being these original investments and all subsequent investments.

Whilst it is clear that in the early period the partners had asymmetric allocations and returns, the important factor going forward is the knowledge that all LPs now participate in existing investments in accordance with their capital contributions. This piece of crucial information is not set out in the accounts, but it would already be known to the LPs.

How much more might the LP be called upon to invest?

To date USD14.65mn has been drawn down in loans. This would also suggest that there is a further USD5.35mn that may be drawn down (being the Employees Fund share of the LPs’ combined capital contribution multiplied by the overall fund size, less drawdowns to date). That is the obvious calculation, but without checking the LPA, it is not possible to conclusively state that it is correct. Many LPAs allow for additional amounts to be drawn in excess of the agreed commitment, if required to fund GPs’ share or to redraw amounts that related to investments that were realized within a relatively short timeframe and distributed back to the LPs. The accounts only show the outstanding commitment by derivation. If there was an amount that could be recalled by the GP in excess of the amount calculated, this would probably be disclosed.

How much has the LP received back?

Again this should be a known number by the Employees Fund. Note 9 clearly shows that the Employees Fund has received back USD21.11mn since the inception of the Zebra Fund.

What is this costing the LP?

There are several elements to the question of what this management service costs, principally the management fee and the carried interest.

Note 2 sets out in full the basis of calculation of the management fee. For the year ended December 31, 2009, this amounts to 2% of the total commitments, plus expenses incurred by the manager in investigating deals that did not proceed (“abort costs”) and deducting any fees received by the manager from the portfolio (“monitoring, directors’, or transaction fees”).

In 2009, the total commitment amounted to USD130.00mn, so simple mathematics suggests a management fee of USD2.60mn, against USD2.23mn in the Profit and Loss Account. The difference being the net amount by which fees charged into the portfolio companies exceeded abort costs on transactions. The gross amount of abort costs and fees are not disclosed in these accounts.

What the management service is costing the Employees Fund will depend on its view of costs. The manager receives 2% of the aggregated commitments, plus any abort costs incurred. A proportion of this is being charged directly to the portfolio companies, the balance is received by them from the Zebra Fund. Whether the fees that are charged to the portfolio companies should be regarded by the LPs as a cost to them is clearly a matter of debate.

The CIP has been allocated USD8.35mn of gains realized in a prior period. So, for the Employees Fund, we can either consider our annual costs to be:

- USD0.40mn (being the Employees Fund’s share of USD2.60mn)

- An amount in excess of USD0.40mn to reflect abort costs and fees

- USD0.34mn (being the Employees Fund’s share of USD2.23mn)

- USD0.87mn.

USD0.87mn is calculated as the sum of the Employees Fund’s share of the management fee since inception of the Zebra Fund (USD2.00mn) and the share of the carried interest allocation (USD2.78mn), divided by the period since inception of over ![]() years.

years.

Whilst this gives a more comprehensive figure of the cost by including the carried interest previously allocated, this is not necessarily the only or indeed the “right” answer. This calculation includes the annual charge to the fund for management fee, excluding costs borne by the portfolio companies and including carried interest paid to the CIP on a cash basis.

It would not be sensible to compare the annual returns received against the calculated annual cost. A comprehensive assessment of costs can only be reasonably calculated when the fund is approaching the end of its life and the performance of the fund as a whole on the basis of an annual rate of return can be calculated.

How much will the LP get back and when?

This is one of the questions that no set of accounts can answer. What the accounts can answer is: “What is the amount that is disclosed as being due to the LP at the year-end?” Note 9 to the accounts shows that the amount allocated to the Employees Fund at December 31, 2009 is USD7.45mn.

In the Partners’ Accounts note, the Unrealized Fair Value reserve is held as a single balance and is not allocated to the individual partners (loss USD40.80mn). In the event that the fund was wound up and this loss realized, the Employees Fund would suffer its share of the loss. Again, with the asymmetric allocations, the accounts do not show precisely what the Employees Fund’s share of that loss would be. When allocating the fair value reserve, it is likely that an allocation might be made to the CIP. Note 9 discloses the fact that there is no amount of the unrealized fair value reserve due to the CIP. As noted above, the Employees Fund’s allocation is 2/13ths of the total, so the share is a loss of USD6.28mn.

Overall, these accounts show that the balance due to the Employees Fund at December 31, 2009 is USD1.17mn. There may be an additional amount potentially available though a clawback of the prior year payments made to the CIP, but again this is not disclosed in these accounts.

What value should the LP put in his/her accounts?

The techniques used in estimating the fair value of private equity investments and the International Private Equity and Venture Capital Valuation Guidelines (IPEV Guidelines) are discussed in detail in Chapter 10.

The Employees Fund accounts are being prepared under a GAAP that requires that investments are reported at fair value. The Board of the Employees Fund is required to prepare accounts that are free from material misstatement and error. The fair value of the interest in Zebra Fund LP, included in the accounts of the Employees Fund, is solely the responsibility of that Board. It is likely to use information from the accounts of Zebra Fund LP, but the fact that it is extracted from these underlying accounts does not reduce the Board’s responsibilities. Accordingly, the Board needs to establish processes to enable it to ascertain that the information it is using is free from material error.

The fund accounts disclose that the Employees Fund’s share of the net assets at December 31, 2009 is USD1.17mn.

Fair value is defined in different words depending on which GAAP and standard is being followed, although the concept remains constant. Fair value is the price at which a transaction would take place at the reporting date. In considering the fair value of an interest in a fund, the expected cash flows arising from a realization of the assets at the reporting date would appear to be a good starting point. When estimating the fair value of the interest in the fund, the valuer should consider whether adjustments should be made to his or her share of the net assets. For the purposes of this section, let us assume that the processes over the underlying investment valuations have indicated that the fair values of the underlying investments are “right” at the reporting date.

The valuer should then consider from the point of view of a prospective purchaser what factors he or she might take into account when entering into a transaction. Any matter that might affect the views of an external acquirer should be included in the consideration. These might include changes that have arisen in the period since the accounts of Zebra Fund were prepared, either internally with acquisitions and disposals; an issue arising in an underlying investment which would impact valuation; or, externally, such as the market dislocation that impacted almost all investment valuations in October 2008. There may be terms in the LPA that might impact the attributable share of net assets. As noted in the sections above, allocations of profit to the CIP are generally made when contractually due. An adjustment may be required to reflect potential future allocations to the CIP.

The strongest evidence supporting fair value is that from a transaction that actually takes place in the market. There are situations when interests in funds are sold. Whilst a price determined by a secondary transaction can provide good evidence of fair value, these prices need to be treated with caution. Generally, secondary prices are negotiated based on factors and assumptions pertinent to the individual parties and considerably wider than simply a view of underlying assets at fair value. If the Employees Fund has decided to sell its interest, then any secondary prices would be of primary importance. In most situations secondary prices provide a useful reference point, but of limited value without a clear understanding of the pricing assumptions and motivations of the parties.

So, the original question cannot be answered in the absence of additional information; however, the consideration of value should commence with the attributable share of net assets of USD1.17mn.

APPENDIX 6.A

ZEBRA FUND LP FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2009

6.A.1 Contents

| 6.A.1 The manager, the general partners, and advisors | 132 |

| 6.A.2 Report of the manager, Zebra LLP | 133 |

| 6.A.3 Report of the independent auditors to the partners | 134 |

| 6.A.4 Profit and loss account | 135 |

| 6.A.5 Statement of total recognized gains and losses | 134 |

| 6.A.6 Balance sheet | 136 |

| 6.A.7 Cash flow statement | 137 |

| 6.A.8 Notes to the financial statements | 138 |

6.A.2 The manager, the general partner, and advisors

| Manager: | Zebra LLP |

| General Partner: | Zebra GP Limited |

| Advisors: | Licus LLP |

| Bankers: | Warthogs Plc |

| Auditors to the Partnership: | Auditors LLP |

6.A.3 Report of the manager, Zebra LLP

We are pleased to present the financial statements of Zebra Fund LP (the Partnership) for the year ended December 31, 2009.

Zebra Fund LP is an English limited partnership, established by a limited partnership agreement dated June 4, 2004 as restated and amended on May 12, 2007. The limited partnership agreement states that the limited partnership shall continue until the expiration of 10 years from the initial closing date, namely June 4, 2014. The limited partnership may be extended for a further 2 years in order to permit the orderly liquidation of investments, pursuant to limited partner consent.

The primary purpose of the partnership is to make investments in medium-sized European and North American businesses, which will typically be medium to long term in nature with the principal objective of generating capital growth.

The following closings occurred bringing the total commitments to USD130,000,000. Drawdowns to date are USD87,402,930 representing 67.23% of the committed capital to date. Distributions of USD71,682,933 have been made to date (including USD8,346,979 to the Carried Interest Partner escrow account). The general partner of the partnership is Zebra GP Limited.

During the year, the partnership made the following investments:

- USD0.90mn in the Book Club LP, primarily operating in South East England.

The financial statements of the partnership are set out together with detailed notes on pp. 135 to 146.

Statement of manager’s responsibilities

The limited partnership agreement requires the manager to prepare financial statements for each financial period in accordance with the accounting policies set out in Note 2. In preparing those financial statements, the manager is required to:

- Select suitable accounting policies and then apply them consistently

- Make judgments and estimates that are reasonable and prudent

- State whether applicable accounting standards have been followed, subject to any material departures disclosed and explained in the financial statements

- Prepare the financial statements on a going concern basis unless it is inappropriate to presume that the partnership will continue in business.

The manager is responsible for maintaining proper accounting records which disclose with reasonable accuracy the financial position at any time of the partnership. The manager has general responsibility for taking such steps as are reasonably open to it to safeguard the assets of the partnership and, hence, for taking reasonable steps for the prevention and detection of fraud and other irregularities.

Disclosure of information to auditors

The manager confirms that, so far as it is aware, there is no relevant audit information of which the partnership auditors are unaware, and the manager has taken all the steps that ought to have been taken as manager to make itself aware of any relevant audit information and to establish that the partnership’s auditors are aware of this information.

For and on behalf of Zebra LLP

February 28, 2010

6.A.4 Report of the independent auditors to the partners of Zebra Fund LP

We have audited the financial statements of Zebra Fund LP for the year ended December 31, 2009 which comprise the profit and loss account, the balance sheet, the cash flow statement, the statement of total recognized gains and losses and the related notes. These financial statements have been prepared under the accounting policies set out therein.

This report is made solely to the partners, as a body, in accordance with the terms of our engagement. Our audit work has been undertaken so that we might state to the partners those matters we have been engaged to state to them in this report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the partners, as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of partners and auditors

As described in the statement of manager’s responsibilities on p. 133, the manager is responsible for the preparation of the financial statements in accordance with the limited partnership agreement dated June 4, 2004 as amended and restated on May 12, 2007 (the LPA).

Our responsibility under the terms of our engagement letter dated December 18, 2008 is to audit the financial statements having regard to International Standards on Auditing (U.K. and Ireland).

We report to you our opinion as to whether the financial statements have been properly prepared in accordance with the accounting policies set out in Note 2 to the financial statements and in accordance with the LPA.

We also report to you if, in our opinion, the manager’s report is not consistent with the financial statements, if the partnership has not kept proper accounting records, if we have not received all the information and explanations we require for our audit, or if information specified by the LPA regarding other transactions is not disclosed.

Basis of audit opinion

We conducted our audit having regard to International Standards on Auditing (U.K. and Ireland) issued by the Auditing Practices Board. An audit includes examination, on a test basis, of evidence relevant to the amounts and disclosures in the financial statements. It also includes an assessment of the significant estimates and judgments made by the partners in the preparation of the financial statements, and of whether the accounting policies are appropriate to the partnership’s circumstances, consistently applied, and adequately disclosed.

We planned and performed our audit so as to obtain all the information and explanations which we considered necessary in order to provide us with sufficient evidence to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or other irregularity or error. In forming our opinion we also evaluated the overall adequacy of the presentation of information in the financial statements.

Opinion

In our opinion the financial statements for the year ended December 31, 2009 have been properly prepared in accordance with the accounting policies set out in Note 2 to the financial statements and in accordance with the LPA.

Anthony Cecil

for and on behalf of Auditors LLP

Chartered Accountants

6.A.5 Profit and loss account

6.A.6 Balance sheet

6.A.7 Cash flow statement

6.A.8 Notes to the financial statements

1. The partnership

Establishment of the partnership

Zebra Fund LP (the partnership) is a United Kingdom limited partnership, established by a limited partnership agreement dated June 4, 2004 as restated and amended on May 12, 2007:

- The carried interest partner is Zebra Executive LP

- The general partner of the partnership is Zebra GP Ltd.

The manager of the partnership is Zebra LLP, and is responsible for the management, operation, and administration of the affairs of the partnership in accordance with the limited partnership agreement.

Business of the partnership

The primary purpose of the partnership is to carry on the business of making investments with the principal objective of achieving a high rate of return from income and capital gains.

Duration of the partnership

The limited partnership agreement states that the partnership shall continue until the 10th anniversary of the initial closing date, namely June 4, 2014. The partnership may be extended by up to 2 years in order to permit the orderly liquidation of investments, pursuant to consent of the limited partner.

2. Accounting policies

The following accounting policies have been applied consistently in dealing with items which are considered to be material in relation to the financial statements.

Accounting convention

These financial statements have been prepared in accordance with the applicable accounting standards and in accordance with the historical cost accounting convention as modified by the revaluation of investments.

The manager has a reasonable expectation that the partnership has adequate resources to continue in operational existence for the foreseeable future, including recourse to loan commitments. Accordingly, the manager continues to adopt the going concern basis in preparing the financial statements.

Income

Bank interest and loan interest income are accounted for on an accruals basis. If there is doubt over the recoverability of dividends or interest income, a provision will be made. Dividend income is recognized when the right to receive payment is established.

General partner share

The general partner, Zebra GP Ltd., is entitled to receive a priority profit share. Until the earliest of the end of the investment period or the stepdown date, this is calculated as 2% per annum of total commitments. Thereafter, this is 2% per annum of the aggregate acquisition cost of investments which have not been realized. The stepdown date will occur on May 12, 2010 and 3 years after the final closing of Zebra Fund LP. The general partner’s share is increased by an amount equal to the aggregate abort costs incurred by the manager, general partner, or any of their associates (including any irrecoverable VAT or similar tax thereon) in the immediately preceding accounting period to the extent such abort costs have not already been recovered by the manager, general partner, or associate either from the partnership or third parties.

The share will be reduced in accordance with the LPA where the aggregate of fees earned and retained by the general partner, manager, or any of their associates in connection with the management of the fund’s portfolio exceeds the retained fees level.

Such share ranks as a first charge on capital gains of the partnerships in any accounting period. Where the gains of the fund exceed the amount to be allocated to the general partner, the general partner may elect which items of capital gain form part of the share taken.

If there are insufficient capital gains in any one accounting period, the general partner may take an interest-free loan in respect of the balance of the general partner’s share entitlement. Drawings are taken annually in advance through 2006, and sem–annually thereafter. In no circumstances shall such interest-free loans be repaid by the general partner other than by set-off of allocations of capital gains. As the general partner is entitled to draw the amount even if profits are not made, and such drawings are not repayable in the event that there are no profits, Financial Reporting Standard 5 “Reporting the substance of transactions” has been adopted and the priority profit share for the relevant period is accounted for as an expense of the limited partnerships.

Transaction and funding costs

All ancillary costs associated with the making of investments are recognized on an accruals basis and expensed in the relevant accounting period.

Foreign exchange

Monetary transactions denominated in foreign currencies are recorded at actual exchange rates prevailing at the date of the transaction. Assets and liabilities in currencies other than U.S. dollars are translated into U.S. dollars at the rates of exchange prevailing at the balance sheet date. Exchange differences are taken to the profit and loss account or the statement of total recognized gains and losses, as appropriate.

Distributions

All capital and income receipts shall be distributed among the partners based on allocations made in accordance with the limited partnership agreement. Any other income of the partnership shall be distributed to the investors pro rata to their commitments.

The carried interest partner is not entitled to payment in respect of any carried interest until the limited partners have received an amount equal to the aggregate commitments previously drawn down by the partnership, plus an amount representing an annualized internal rate of return of 8%, calculated in accordance with the provisions of the limited partnership agreement.

Taxation

Taxation has not been recorded in these financial statements as any tax liabilities that may arise, on income or capital, are borne by the individual partners comprising the limited partnership. Accordingly, no provision for taxation is made in these financial statements. Capital losses are allocated to the partners in accordance with the LPA.

Investments