The following terms have been used throughout this chapter in connection with retirement plans.

Catch-up contributions Additional employee contributions that can be made only by those who attain age 50 by the end of the year.

Compensation The amount upon which contributions and benefits are calculated. Compensation for employees is taxable wages reported on Form W-2. Compensation for self-employed individuals is net profit from a sole proprietorship or net self-employment income reported to a partner or limited liability member on Schedule K-1.

Coverage Qualified plans must include a certain percentage of rank-and-file employees.

Db(k) Hybrid qualified retirement plans combining an employer-funded pension with a 401(k).

Defined benefit plans Pension plans in which benefits are fixed according to the employee’s compensation, years of participation in the plan, and age upon retirement. Contributions are actuarially determined to provide sufficient funds to cover promised pension amounts.

Defined contribution plans Retirement plans in which benefits are determined by annual contributions on behalf of each participant, the amount these contributions can earn, and the length of time the participant is in the plan.

Elective deferrals A portion of the employee’s salary that is contributed to a retirement plan on a pretax basis. Elective deferrals apply in the case of 401(k) plans, 403(b) annuities, SARSEPs (established before 1997), and SIMPLE plans.

Employee plans corrections resolution system (EPCRS) An IRS program that can be used to correct defects and problems in qualified retirement plans with little or no penalty.

Employee stock ownership plans (ESOPs) An employee benefit plan giving ownership interests in a corporation to employees.

Excess contribution penalty A 6% cumulative penalty imposed on an employer for making contributions in excess of contribution limits.

Funding In the case of defined benefit plans, the amount of assets required to be in the plan in order to meet plan liabilities (current and future pension obligations).

Highly compensated employees Owners and employees earning compensation over certain limits that are adjusted annually for inflation.

Keogh plans A term that had been used to designate qualified retirement plans for self-employed individuals (also called H.R.10 plans). This term is no longer in use.

Master and prototype plans Plans typically designed by banks and other institutions to be used for qualified retirement plans.

Money purchase plans Defined contribution plans in which the annual contribution percentage is fixed without regard to whether the business has profits.

Nondiscrimination Requirements to provide benefits for rank-and-file employees and not simply to favor owners and highly paid employees.

Participation The right of an employee to be a member of the retirement plan and have benefits and contributions made on his or her behalf.

Pension Benefit Guaranty Corporation (PBGC) A federal agency that will pay a minimum pension to participants of defined benefit plans in companies that have not made sufficient contributions to fund their pension liabilities.

Premature distribution penalty A 10% penalty imposed on a participant for receiving benefits before age 59½ or some other qualifying event.

Profit-sharing plan A defined contribution plan with contributions based on a fixed percentage of compensation.

Prohibited transactions Dealings between employers and the plan, such as certain loans, sales, and other transactions between these parties. Prohibited transactions result in penalties and can even result in plan disqualification.

Qualified default investment alternative (QDIA) Permissible 401(k) investments by a plan with automatic enrollment.

Required distributions Plans must begin to distribute benefits to employees at a certain time. Generally, benefits must begin to be paid out no later than April 1 following the year in which a participant attains age 70½. Failure to receive required minimum distributions results in a 50% penalty on the participant.

Roth 401(k)s 401(k) plans funded with after-tax dollars that permit tax-free withdrawals if certain holding period requirements are met. Also called designated Roth accounts.

Roth IRAs Nondeductible IRAs that permit tax-free withdrawals if certain holding period requirements are met.

Salary reduction arrangements Arrangements to make contributions to qualified plans from an employee’s compensation on a pretax basis. In general, salary reduction arrangements relate to 401(k) plans, 403(b) annuities, SARSEPs in existence before 1997, and SIMPLE plans.

Savings incentive match plans of employees (SIMPLEs) IRA- or 401(k)-type plans that permit modest employee contributions via salary reduction and require modest employer contributions. SIMPLE plans are easy to set up and administer.

Simplified employee pensions (SEPs) IRAs set up by employees to which an employer makes contributions based on a percentage of income.

Stock bonus plans Defined contribution plans that give participants shares of stock in the employer rather than cash.

Top-heavy plans Qualified retirement plans that provide more than a certain amount of benefits or contributions to owners and/or highly paid employees. Top-heavy plans have special vesting schedules.

Vesting The right of an employee to own his or her pension benefits. Vesting schedules are set by law, although employers can provide for faster vesting.

Where to Claim Deductions for Retirement Plans

Employees

If you contribute to an IRA and are entitled to a deduction, you claim it on page 1 of Form 1040 as an adjustment to gross income. If you contribute to a salary reduction plan (such as a SIMPLE or a 401(k) plan), you cannot deduct your contribution.

All Employers

To claim the credit for plan start-up costs of small employers, file Form 8881, Credit for Small Employer Pension Plan Startup Costs. The credit is part of the general business credit and so must be entered on Form 3800, General Business Credit, if you have another credit that is part of the general business credit.

Self-Employed

Contributions you make to self-employed qualified retirement plans, SEPs, or SIMPLEs on behalf of your employees are entered on Schedule C (or Schedule F for farming operations) on the specific line provided on the form, called pension and profit-sharing plans. Contributions you make on your own behalf are claimed on page 1 of Form 1040 as an adjustment to gross income. Contributions you make to an IRA are also claimed on page 1 of Form 1040 as an adjustment to gross income.

Partnerships and LLCs

Deductions for contributions to qualified plans on behalf of employees are part of the partnership’s or LLC’s ordinary trade or business income on Form 1065. The deductions are entered on the line provided for retirement plans.

The entity does not make contributions on behalf of partners or members. Partners and members can set up their own retirement plans based on their self-employment income. Thus, if partners and members set up qualified retirement plans, they claim deductions for their contributions on page 1 of Form 1040.

As a practical matter, small partnerships and LLCs generally do not establish qualified plans for employees, since the partners and members do not get any direct benefit.

S Corporations

Deductions for contributions to qualified plans are taken by the corporation as part of its ordinary trade or business income on Form 1120S. Enter the deduction on the line provided for pension plans, profit-sharing plans, and so on. This line includes contributions to nonqualified plans if the corporation is entitled to claim a current deduction for such contributions.

C Corporations

C corporations deduct contributions to retirement plans on Form 1120. The deduction is entered on the line provided for pension plans, profit-sharing plans, and so on. This line includes contributions to nonqualified plans if the corporation is entitled to claim a current deduction for such contributions.

Other Reporting Requirements for All Taxpayers

Qualified plans entail annual reporting requirements. If you maintain a qualified plan, you must file certain information returns each year to report on the amount of plan assets, contributions, number of employees, and such (unless you are exempt from reporting). Information returns in the 5500 series are

not filed with the IRS. Instead, these rules are filed with the Department of Labor’s Pension and Welfare Benefits Administration (PWBA) at

www.efast.dol.gov. These returns must be filed electronically in most cases. There are penalties for failure to file these returns on time and for overstating the pension plan deduction.

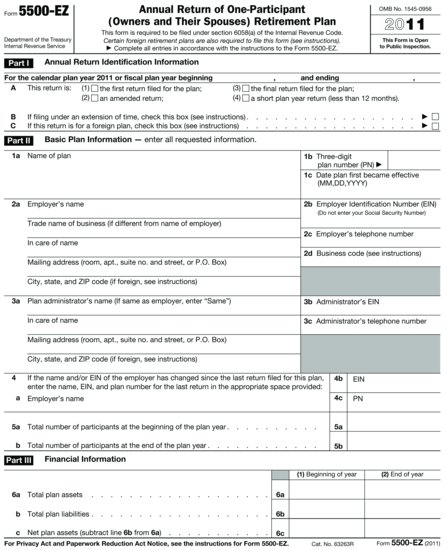

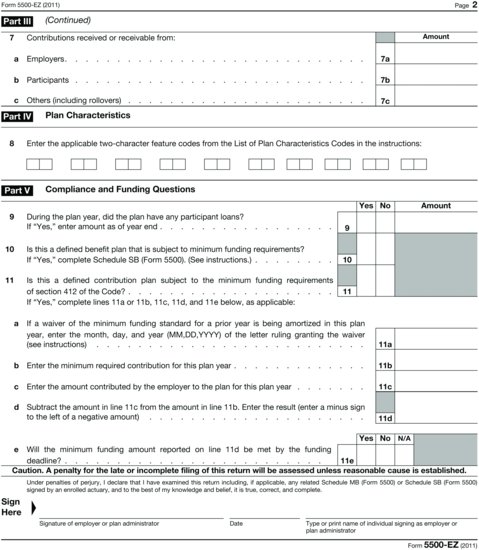

The return is due by the last day of the seventh month following the close of the plan year. Thus, if the plan is on a calendar year, the return is due no later than July 31 of the following year. Obtaining an extension to file an income tax return generally does not extend the time for filing these returns. However, if you are self-employed and obtain a filing extension for your individual return to October 15, you have until the extended due date to file Form 5500-EZ (Figure 16.3). If you do not have a filing extension for your personal return, you can request an extension of time to file Form 5500-EZ by filing Form 5558, Application for Extension of Time to File Certain Employee Plan Returns, to obtain an automatic 2½ month extension (to October 15).