Impact of Home Office Deductions on Home Sales

Claiming a home office deduction does not impact your ability to claim the home sale exclusion (up to $250,000 of gain; $500,000 on a joint return) if you otherwise qualify for it. In the past it had been reasoned that gain on the portion of the home used as a home office would have to be reported. However, recent regulations make it clear that the exclusion can be applied to the home office portion as well, as long as the office is within the dwelling unit.

However, any depreciation taken on a home office after May 6, 1997, must be recaptured at the rate of 25% (for taxpayers in tax brackets over this amount). This means you must report your total depreciation deductions related to home office use after this date and must pay tax on the total amount at the rate of 25%. You cannot use the exclusion to offset this tax.

You cannot avoid this recapture by choosing not to report depreciation to which you are entitled. Recapture applies to depreciation both allowed (the amount you actually claimed) and allowable (what you were entitled to claim). If you want to avoid depreciation recapture, you must sidestep the home office deduction entirely by disqualifying your home office. You can do this easily by not using the space exclusively for business. By disqualifying your home office, you lose out on depreciation but can still claim many related costs, such as office maintenance and utility costs, as ordinary and necessary business expenses.

Where to Deduct Home Office Expenses

Employees

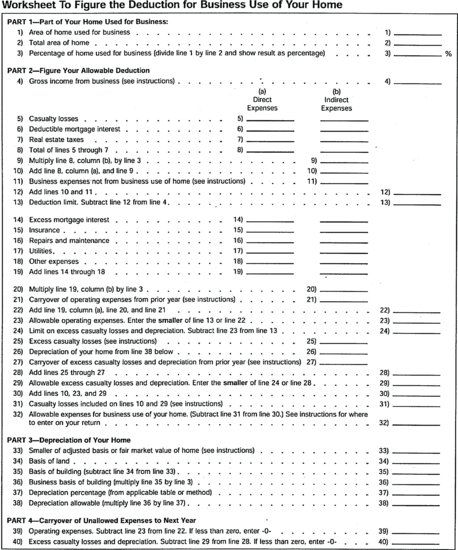

Employees do not compute their home office deduction on Form 8829,

Expenses for Business Use of Your Home. Instead, use the special worksheet in IRS Publication 587, which largely follows Form 8829. You will find this worksheet (

Figure 18.1) on the following page.

Your home office deduction is entered on Form 2106, Employee Business Expenses, or Form 2106-EZ, Unreimbursed Employee Business Expenses, if you are otherwise allowed to use this form. Then the deductions from Form 2106 or 2106-EZ are entered on Schedule A as miscellaneous itemized deductions subject to the 2%-of-AGI rule discussed in Chapter 1.

Remember that if you lease your home to your corporation, you cannot take any home office deductions (other than the mortgage interest, real estate taxes, and casualty and theft losses allowed to all homeowners).

Self-Employed

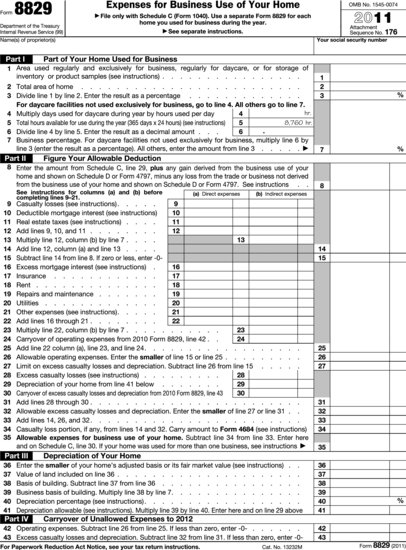

Self-employed individuals compute home office deductions on Form 8829,

Expenses for Business Use of Your Home (

Figure 18.2). This form allows you to calculate the portion of your home used for business. This portion, or percentage, is then used to allocate your home-related expenses. You also use the form to calculate any carryover of unused home office expenses.

If you first begin to use your home office this year and you own your home, you must also complete Form 4562, Depreciation and Amortization, to calculate the depreciation deduction entered on Form 8829.

Depreciation is explained in full in Chapter 14. Note that when you begin to use part of your home for business, it is usually depreciated as nonresidential realty over 39 years (31.5 years if you began home office use before May 13, 1993). You must determine the basis of your home office in order to calculate depreciation. Basis on the conversion of property from personal use to business use is the lesser of the FMV of the office on the date you begin business use or the adjusted basis of the property on that date. If you are not sure about the FMV of your home office, get an appraisal. Ask a local real estate agent to assist you in this task.

Alert

The 2012 form was not available at the time of publication. The 2011 version is for informational purposes and should not be filed with 2012 returns.

The home office deduction calculated on Form 8829 is entered on a specific line on Schedule C for expenses for business use of your home. You cannot use Schedule C-EZ, Net Profit From Business, if you claim a home office deduction.

Farmers

Self-employed farmers who file Schedule F instead of Schedule C do not compute home office deductions on Form 8829. Instead, they should calculate these deductions on the Worksheet (see

Figure 18.1 on page 401) in the same way as employees. Then the home office deduction is entered on Schedule F.

Partners and LLC Members

If you use a home office for your business, you figure your deductions in the same way as an employee. Use the worksheet (

Figure 18.1) on page 401 (do not use Form 8829 to figure your home office deduction).