Day 5: The purchase and sale of inventory on credit terms

Key terms and concepts

• Inventory: goods that we purchase for resale. It is the basis of our business and is not something used or consumed within our business itself.

• Credit purchase and credit sale: a purchase or sale of inventory where settlement of the account occurs at a later time. The credit terms are usually stated on the invoice, for example, ‘Net 30 days’.

• Accrual accounting: recording of all business transactions at the time that a legal obligation exists for you to pay or receive money, albeit sometime in the future. You ‘accrue’ or record the right within your accounting system.

• ‘Cash accounting’ principles: under cash accounting rules, credit purchases and credit sales are only recorded in the accounting system on settlement (or part settlement) of the account.

• The Purchase and Sales journals are only for use for the credit purchase or credit sale of inventory.

• The Purchases and Sales entries within the cash book are for cash purchases and cash sales only, but we may have to modify this rule for credit purchases and credit sales that are to be accounted for on a cash basis.

Today we are going to learn how to account for credit sales and credit purchases. We are also going to examine how to account for the return of goods to our supplier or when our customers return goods to us in both cash and credit situations. We will discuss discounts, both at the time of sale or purchase, or at a later date. We will then re-examine all of this from a cash accounting perspective.

Not all accounting procedures apply universally to all businesses. If your business doesn’t involve buying or selling goods or services on credit terms, you can skip this chapter and move on to day 6.

So far, we have looked at the general journal and the cash payments and cash receipts journals. We found that entering transactions through the general journal was a cumber-some process, as was the posting of every transaction to the general ledger.

The cash payments and cash receipts journals made this process easier when the transaction involved cash. By using these journals we could streamline the data entry into one record rather than using multiple lines in the general journal, and we were only required to post the total once per month.

In this chapter we will look at another set of special journals the purchases and sales journals. These journals are used to record the purchase and sale (and returns) of goods purchased on credit for resale at a profit. Goods purchased for resale are called inventory items.

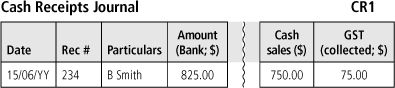

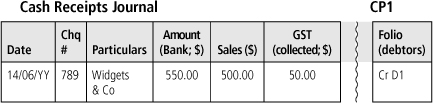

However, you only record in the purchases and sales journals goods purchased on credit for resale — inventory items. Please note the two conditions — inventory and credit terms. Your purchase must relate to inventory and not to other credit purchases, such as a motor vehicle, and the purchase must be on credit terms. Inventory purchased or sold for cash is instead recorded through the cash payments and cash receipts journals respectfully. See example 5.1, which describes purchases and sales for cash.

Example 5.1

On 10 June I make a cash purchase of 10 widgets at $55.00 each from Widgets & Co using cheque number 789.

On 15 June I on sell the widgets to B Smith at a 50 per cent mark-up using receipt number 234.

The purchase and sale has been handled completely within the cash payments and cash receipts journals. For a cash purchase, you credit the Cash at Bank account and debit the Purchases and GST accounts; for a cash sale, you debit the Cash at Bank account and credit the Sales and GST accounts.

Credit purchases and credit sales under accrual accounting

The basic condition for recording any transaction under International Accounting Standards is that all transactions are recorded at the time that the obligation is cast, that is, at the time that the contract is made, when you have a legal obligation to pay or receive monetary value, albeit some time in the future. If you make a purchase or sale on credit terms, you create mutual obligations at the time the contract for the purchase or sale was entered into, but the payment for that inventory item is delayed under the contract. For example, if your invoice reads ‘Net 30 days’, it means that you have 30 days to settle the account in full.

You use the purchases or sales journals to record a purchase or sale transaction entered into on a credit basis.

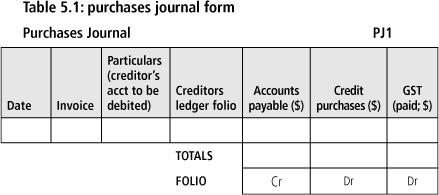

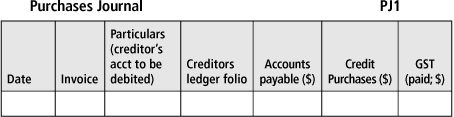

The purchases journal

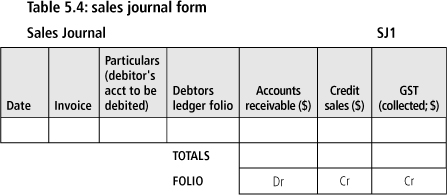

The purchases journal is used to record credit purchases under the accrual accounting system. The format of a purchases journal is shown in table 5.1.

When you make a credit purchase there is no cash transaction, instead you make a promise to pay for these goods at a later date. Therefore you must create a liability account called an Accounts Payable account (Creditors Control or Trade Cred-itors account to use alternative names) to which you credit the amount you will pay in the future rather than crediting the Cash at Bank account direct. Note that the inventory purchased is debited to a Purchases account in the cost of goods sold category and not directly to an inventory account.

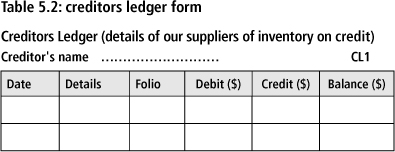

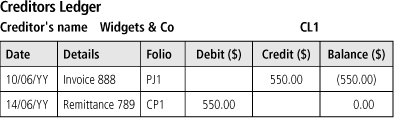

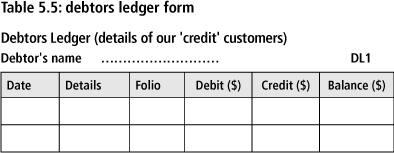

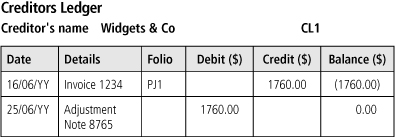

However, the Accounts Payable (Creditors Control) account is only a control account, that is, it only contains total amounts. If our supplier was to query our payment, how could we prove what we owe? The answer is that we also have to keep separate records of our individual supplier’s transactions. These separate records are collectively called the creditors ledger, which is a collection of all of the individual creditors accounts. The total of all of the creditors accounts, the creditors ledger summary, is ‘reconciled’. An example of an individual creditor’s account is shown in table 5.2.

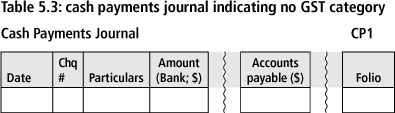

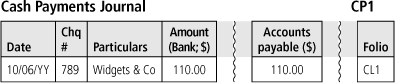

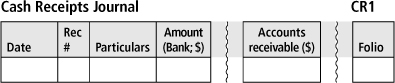

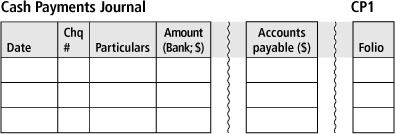

When you finally pay the account, you will debit the Accounts Payable account and credit the Cash at Bank account. This is done through your cash payments journal. You will also debit the individual creditor’s account.

As shown in table 5.3, when you pay the account through your cash payments journal there is no further GST involved. That was already debited along with the Purchases account in the purchases journal at the time that you recorded the original transaction.

See example 5.2, which describes both a purchase and a settlement on credit terms as well as a purchase on credit terms with a deposit paid.

Example 5.2

In the first part of this example we will examine a purchase and settlement on credit terms.

On 10 June I purchase 10 widgets at $55.00 each from Widgets & Co on credit terms to be paid with 14 days. Widget’s invoice number 888 confirms this as follows:

The Accounts Payable account was credited with the amount payable in the future and the Purchases and GST accounts were debited. However, the individual creditor’s account, as shown following, also has to be credited with the amount:

On 14 June we settled the account with cheque number 789. We did this through the cash payments journal, as the following example shows:

This action will credit the Cash at Bank account with the $550.00 (as part of the total posted at the end of the month) and debit the Accounts Payable account with the $550.00 (again in bulk at the end of the month). However, we will also have to credit the individual creditor’s account so that the individual’s amount outstanding is correct and the total of all creditors ledger accounts equals the Accounts Payable account, as indicated following:

Now we will examine a purchase on credit terms with a deposit paid.

If we were to purchase 100 widgets at $50 each with a 20 per cent deposit, we would first enter the credit purchase in full through the purchases journal and then enter the cheque made out for the deposit in the cash payments journal. In this way the purchases journal records the full details of the purchase and the cash payments journal simply writes off the debt outstanding, as shown following:

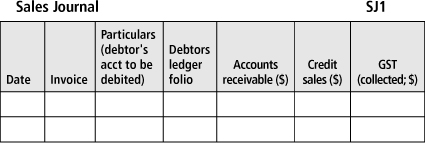

The sales journal

The sales journal is used to record credit sales under the accrual accounting system. The format of a sales journal is shown in table 5.4.

When you make a credit sale there is no cash transaction, instead your customer promises to pay for these goods at a later date. Therefore you must create an asset account called an Accounts Receivable account (or Debtors Control or Trade Debtors account to use alternative names) to which you debit the amount you hope to receive in the future rather than debiting the Cash at Bank account direct. Note that the inventory sold is credited to the Sales account in the revenue category and is not credited directly to an inventory account. Inventory accounting is something that happens after the trial balance stage and is part of the accounting function rather than the transactional recording bookkeeping function.

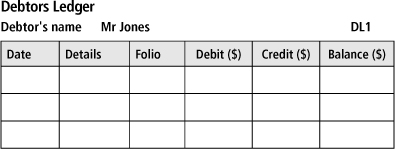

However, as with credit purchases, the Accounts Receivable account is only a ‘control’ account, that is, it only contains total amounts. If our customer was to query our request for payment, how could we prove the debt? The answer is that we also have to keep separate records of our individual customer’s transactions. These separate records are collectively called the debtors ledger, that is, a collection of all of the individual debtor’s accounts. The total of all of the debtors accounts, the debtors ledger summary, is ‘reconciled’ back to the Accounts Receivable (Debtors Control) account at regular intervals.

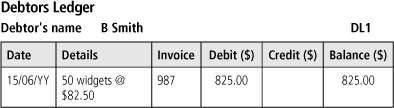

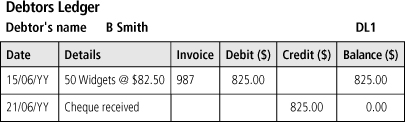

An example of an individual debtor’s account is shown in table 5.5.

When you are finally paid, you will debit the Cash at Bank account and credit the Accounts Receivable account. This is done through your cash receipts journal. You will also be required to credit the individual debtor’s account.

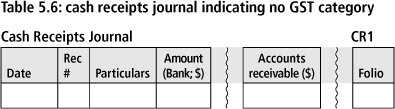

As shown in table 5.6. you will notice once again that when you receive the payment, there is no further GST involved. That was already credited along with the Sales account in the sales journal at the time that you recorded the original credit sale.

See example 5.3, which describes both a sale and a settlement on credit terms as well as a sale on credit terms with a deposit paid.

Example 5.3

In the first part of this example we will examine a sale and settle-ment on credit terms.

The first rule of selling on credit terms is to vet your customers and make sure that they a good credit risk.

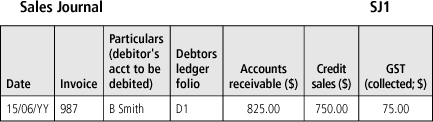

On 15 June I on-sell the widgets to B Smith at a 50 per cent mark-up using invoice number 987, stipulating that the account is to be settled within 14 days:

The Accounts Receivable account was debited with the amount owed and the Sales and GST accounts were credited. However, the individual debtor’s account, as shown following, also has to be debited with the amount:

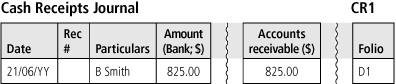

On 21 June B Smith sends us a cheque for $825.00.

This action will debit the Cash at Bank account with Mr Smith’s $825.00 (as part of the total posted at the end of the month) and credit the Accounts Receivable account with the $825.00 (again in bulk at the end of the month). However, we will also have to debit the individual debtor’s account so that the individual’s amount outstanding is correct and the total of all the debtors ledgers equals the Accounts Receivable account, as indicated following:

Now we will examine a sale on credit terms with a deposit paid.

If we on-sold the 100 widgets at $75 each with a 20 per cent deposit, we would first enter the credit sale in full through the sales journal and then enter the monies received for the deposit in the cash receipts journal. In this way the sales journal records the full details of the credit sale and the cash receipts journal simply writes off the debt outstanding. This is exactly the same procedure as for purchases on credit terms with a deposit paid, as outlined in example 5.2.

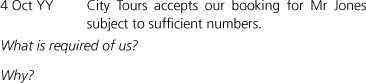

In exercise 5.1 Mr Jones is going to book and pay for a cruise on credit terms. This will demonstrate the complexity of using a manual system for these types of transactions.

Exercise 5.1

Our business is a travel agency called MyTravel. A customer, Mr Jones, wishes to purchase a return ticket for a cruise on the Western Sun leaving Fremantle on 30 October for Bunbury, Albany and Esperance. The ticket will cost Mr Jones $2640 for which he will make a 50 per cent deposit. We will order the ticket from Western Sun Ticketing on a 25 per cent deposit, with the remainder to be paid two weeks before sailing. We mark up the cost by 33.3 per cent to arrive at the price we have charged Mr Jones.

Mr Jones also wishes to book three tours, one in each city visited, from City Tours. The tours can be requested, but not confirmed until 14 days before sailing when 100 per cent payment is required. The tours cost us $600 each, to which we will add a 33.3 per cent mark-up.

Referring to the situation just described, analyse the following circumstances and answer the questions indicated by calculating the amounts involved and creating the appropriate journal entries in the forms drawn up as shown.

![]()

Returns and allowances under accrual accounting

Have you ever bought a pair of shoes and later decided that you didn’t like them and then returned them to the store? This is a classic example of a return, but in business such returns are a little more complex. For example, if a stock line is not selling, instead of returning the goods you may seek a discount from the supplier. This is referred to as an allowance.

Returning goods purchased or sold

At some time we have all purchased an item that we have later returned for one reason or another. Returns of goods purchased, or returns to us of goods sold by us, are readily identified by the average consumer.

If you purchased/sold the goods on cash terms, you would simply receive/pay a cash refund processed through the cash receipts and cash payments journal. The document you would receive/issue is called an adjustment note (credit note) and is in all ways similar to a tax invoice, but with a negative cost indicated rather than a positive one. Since the introduction of the GST, the term ‘adjustment note’ is used rather than the older term ‘credit note’ because the return is handled as an adjustment in your BAS; however, many small companies treat returns as negative purchases/sales and simply show the net amount in the BAS. Either way is acceptable for returns within the BAS period but for out-of-period returns, the adjustment method is preferred.

If you purchased/sold the goods on credit terms, there are two scenarios that we have to cover. If the goods have been paid for and the account settled, the return is usually settled as a cash payment similar to the process just described for goods purchased/sold on cash terms, or alternatively as a credit settlement with the individual creditor’s/debtor’s account going into negative — to be utilised as a credit on the next purchase/sale. Which one you use will depend on whether or not the return relates to a supplier/customer with whom you have regular dealings, or if the transaction is just a one off. Sometimes the terms of trade will also dictate the type of refund given on returned goods.

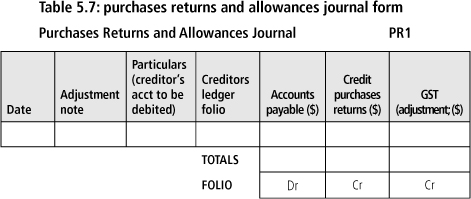

If the purchase or sale return is via an adjustment note, which itself is on credit terms, a purchases (or sales) returns and allowances journal is used, as shown by the forms indicated in tables 5.7 and 5.8.

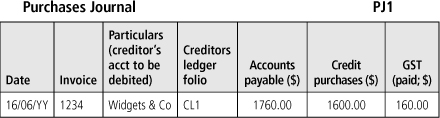

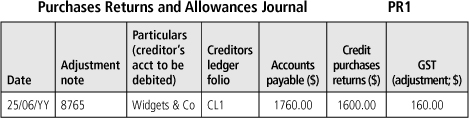

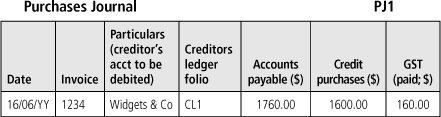

See example 5.4, which outlines a purchase through a purchases journal followed by a purchases return via an adjustment note processed through a purchases returns and allowances journal.

Example 5.4

On 16 June Mr Smith purchased inventory from Widgets & Co for $1760 using invoice number 1234, as indicated following:

On 25 June the goods arrived, but as they were the wrong colour, Mr Smith returned the goods and received an adjustment note numbered 8765:

Applying discounts and allowances

Discounts and allowances received and given is a much misunderstood concept. When you negotiate the original purchase or sale, it doesn’t matter in the slightest how the sale value is arrived at — the price settled is the amount you record. The fact that the amount arrived at may have included an ‘allowance’ — for example, trade, volume or mates’ rates reductions — does not influence the fact that only the final figure is reflected in your original purchases or sales journals. All negotiated allowances built into that figure are ignored, except any allowance that may be triggered after the contract date, such as an early settlement discount.

The only allowance you should record is an allowance that is triggered or negotiated after the contract price has been settled. For example, if we order goods by sample and what is delivered is not of sample quality, we then have the choice of returning the goods and receiving an adjustment note, or renegotiating and paying a lower invoice value.

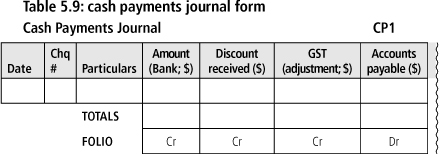

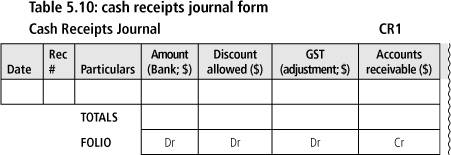

All allowances are recorded through the cash payments and cash receipts journals at the time of settlement of the account, as shown by the forms indicated in tables 5.9 and 5.10.

In example 5.5 a purchase of inventory is followed by a negotiated adjustment to the purchase price.

Example 5.5

On 16 June Mr Smith purchased inventory from Widgets & Co for $1760 using invoice number 1234.

On 25 June the goods arrived but were the wrong colour. Mr Smith negotiated a 25 per cent discount on the original cost and received an adjustment note numbered 8765. He settled the account using cheque number 456.

You will notice that an allowance or discount given after the time of purchase or sale is not only an adjustment to the contract price but also requires a GST adjustment, hence the term ‘adjustment note’ rather than just a ‘credit note’ indicating an adjustment to the price only.

Computerised accounting under accrual accounting

It’s fairly evident that accounting for purchases and sales on credit terms is a very complex process. This is exacerbated even more when we add returns and allowances into the mix and then top it all off with GST considerations.

The complexity of the manual accounting process is in stark contrast to the computerised approach. The source documents involved in the process are the purchase order, invoice and payment advice. The usual computerised approach is to create a separate module that handles credit purchases and sales that is tied in very closely to the inventory management system and processes and records the transactions, both from an inventory management and general ledger perspective, as part of the purchase order, invoice and payment advice creation process.

For example, when you receive a purchase request from a customer, you enter the details into the system, which in turn generates an invoice and a warehouse packing slip and up-dates the inventory record as well as the Accounts Receivable Control account in the general ledger and the individual debtor’s account. If an item is not in stock, the system generates the purchase order to your supplier and marks the customer’s invoice as goods on back order.

When the goods arrive, the system generates a new invoice and warehouse packing slip and again updates the inventory record as well as the Accounts Receivable Control account and the individual debtor’s account.

Similarly, if goods are returned or allowances given, the adjustment note creation processes updates all of the relevant inventory management and general ledger accounts.

Any small business that does any of its transactions on credit terms and uses accrual accounting would be well advised to consider computerised accounting. If you deal primarily with cash, the difference between a computerised and manual approach is not that significant.

Credit purchases and credit sales under cash accounting

If we are a small business entity that has elected to account for our GST liability and our income tax on a cash basis but we also have credit transactions, that is, we purchase and sell inventory on a credit basis, how do we account for credit transactions in cash-based accounting records?

This is a dilemma! There are three ways that we can record our credit transactions. We already know that we can record them when they occur, as is required using the accrual accounting method, or when the account is settled using the cash accounting rules permitted by the Tax Office (ATo). But we can also record the transactions as they take place and then adjust our records to reflect the Tax Office’s cash accounting rules for BAS and end-of-year income tax requirements; however, this requires a lot of unnecessary duplication and effort.

The answer to our dilemma lies in the International Accounting Standards themselves (actual title being ‘International Finan-cial Reporting Standards’). So who do we report to? In financial accounting terms we report to ourselves, as the owners of the business. So if we are reporting to ourselves and not to an outside independent owner (shareholder), it is my opinion that we can safely ignore the standards and adopt the Tax Office’s cash accounting rules.

A word of caution: we can adopt the Tax Office’s cash accounting rules if the business concerned is a small business entity with a turnover under $2 million and no overseas (hedging) transactions. If you are involved in overseas transactions, you may be required to follow International Accounting Standards in order to comply with the Tax Office requirements.

Credit purchases accounted for under cash accounting

When we make a credit purchase — that is, we receive goods with an invoice to be paid sometime in the future — we will update the individual creditor’s account with the details of the purchase, but we will not include any details of the purchase or GST in our accounting records; in other words, we will not update the Accounts Payable (Creditors Control) account with the total of our creditors ledger. In fact, we do not even have an account called Accounts Payable in our general ledger accounts.

Example 5.6 outlines a purchase on credit terms using cash accounting (example 5.2 revisited).

Example 5.6

On 10 June I purchased 10 widgets at $55.00 each from Widgets & Co on credit terms to be paid with 14 days.

In this case we don’t enter the details in the purchases journal but rather we enter the details directly into our individual creditor’s account:

The summary of all creditors outstanding is normally reconciled to the Accounts Payable account; however, in this case we do not have such an account and therefore the only record of our total outstanding creditor liabilities is the creditors ledger summary.

On 14 June we settled the account with cheque number 789. We did this through the cash payments journal, as the following example shows:

In this example you will notice that we have recorded the payment in the Purchases and GST accounts, and not the Accounts Payable account as previously. We are in fact treating the settlement of our credit purchase as a cash purchase at the time of payment of the account, not at date of invoice or when we received the goods.

The cash payment is then posted to the individual creditor’s account to write off the outstanding debt, as shown following:

Credit sales accounted for on a cash basis under cash accounting

When we make a credit sale, that is, we sell goods with an invoice to be paid sometime in the future, we will update the individual debtor’s account with the details of the sale, but we will not include any details of the sale or GST in our accounting records.

Example 5.7 outlines a sale and settlement on credit terms using cash accounting (example 5.3 revisited).

Example 5.7

On 15 June I on-sell the widgets to B Smith at a 50 per cent mark-up using invoice number 987, stipulating that the account is to be settled within 14 days.

In this case, as we are accounting for our sale and GST on a cash basis, we do not enter anything into our accounting records at the time of the actual sale. We will, however, note the sale in our individual debtor’s account. The summary of the debtors ledger would normally be reconciled to the Accounts Receivable account; however, in this case, as there is no Accounts Receivable account in our accounting records, the summary total will represent the actual amount that is outstanding to us.

On 21 June B Smith sends us a cheque for $825.00

We enter the cheque in settlement of the account in the normal way through the cash receipts journal, but record it in the Sales and GST accounts, as indicated following. We treat the cash settlement as if it were a cash sale.

Finally, the cash receipt is posted, as totals at the end of the month, to the Cash at Bank, Sales and GST accounts and on an individual basis to the individual debtor’s account:

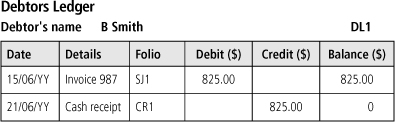

Debtors Ledger

Debtor's name B Smith DL1

Returns and allowances under cash accounting

If you purchased/sold goods on cash terms, you would simply receive/pay a cash refund processed through the cash receipts and cash payments journals. In the case of credit purchases and sales accounted for under the cash system, there is no record made in the accounts until the amount is settled. Therefore, any allowances and returns are recorded in the individual creditor’s or debtor’s accounts but not in the accounting system itself. There is no need for the sales returns and purchases returns journals.

In exercise 5.2 we will revisit Mr Jones. This time he is still going to book and pay for a cruise on credit terms, but we are going to account for these transactions under cash accounting rules.

Exercise 5.2

Redo exercise 5.1 as if you were accounting for your credit purchases and credit sales on a cash accounting basis but remember you only update your general ledger Sales, Cash at Bank and GST accounts when the account is actually settled, not when the transactions are entered into. Use the forms drawn up as shown following, with as many lines as you require. A full set of blank forms is available on my website www.tpabusiness.com.au.

Computerised accounting under cash accounting

As with computerised accounting under the accruals method, we must look at the two types of computerised accounting programs. ‘Cash book’ accounting programs usually work on a cash basis. You can prepare a quote, convert it into an invoice and when the invoice is paid the relevant general ledger accounts — the Cash at Bank, Sales and GST accounts — are updated.

On the other hand, most computerised ‘accounting’ programs work under the accruals method. If you wish to create a cash report, they will ‘back out’ the noncash items, or credit amounts not yet settled, and report the ‘cash’ position. This means that even if you are using cash accounting, under most computerised ‘accounting’ systems (as distinct from ‘cash book’ systems) you will still use the sales and purchases journals, albeit an automated process through the invoice generation and inventory control module.

Some accrual accounting programs also allow you to detach your Purchase and Sales modules and then double-count your cash transactions, once to write off the individual debtor or creditor accounts and again to update the general ledger accounts. This is not really a satisfactory solution.

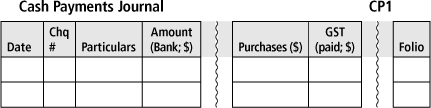

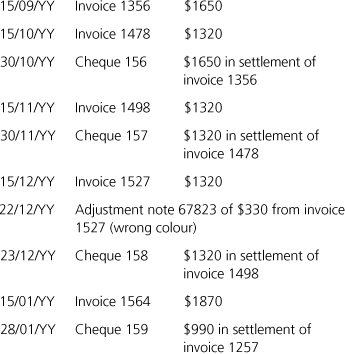

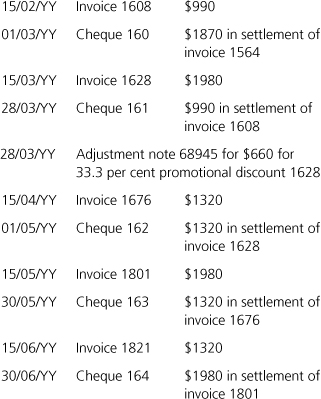

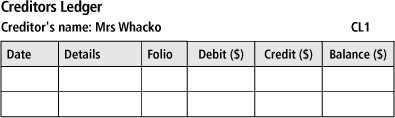

Revision exercise for day 5

We are a company that purchases essentially the same quantity of goods using credit terms once per month from the one supplier, Mrs Whacko. The goods are to be paid for within 45 days. We commenced purchasing with an order on 1 September that was supplied with an invoice on 15 September. It is now 30 June and our supplier’s auditors have asked for a verification of the amount outstanding. Are our records up to the task?

The transactions for the last nine months have been as follows:

Please enter the ‘credit’ purchases into Mrs Whacko’s individual creditor’s account and the payments made into the cash payments journal. Please post the cash payment amounts individually to Mrs Whacko’s account and also to the general ledger Purchases and GST accounts.

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.