Day 3: Cash receipts and cash payments

Key terms and concepts

• Cash: besides meaning actual money, in business cash usually means cheques as well as direct debits and credit card transactions.

• All cash receipts are accounted for in the cash receipts journal.

• All cash payments are accounted for in the cash payments journal.

• When combined, the cash receipts and the cash payments journals are often referred to as the ‘cash book’.

In days 1 and 2 we categorised our transactions according to a chart of accounts that we created to suit our own business needs and we recorded our business transactions on a ‘one by one’ basis, which can be very time-consuming. In this lesson we will learn about special journals that make the recording of business transactions a little easier.

Source documents

There are many documents produced by a business entity during your normal business activity that provide the source of information you need to enter into your accounting system.

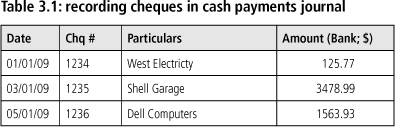

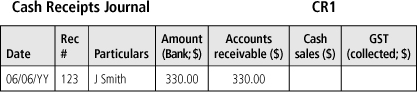

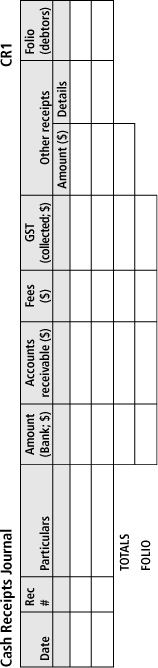

One of the first steps in starting a new business is to open a bank account, usually a cheque account. When you write a cheque to pay an account or make a purchase it is the cheque stub that is the source of information that you need to enter that payment into your accounting records. An example of how this would appear in a cash payments journal is shown in table 3.1.

Other sources of information that emanate from your cheque account include your bank statement, which will indicate any direct debit payments you may have in place, bank charges and so on.

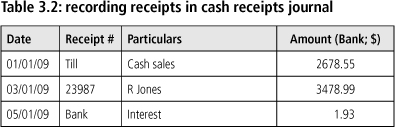

In the normal course of business you will also receive money for which you may issue a receipt, or receive money directly into your cash register or as a direct deposit into your bank account. The copy of the receipt you issued, your daily cash register total and your bank statement are all sources of information that you will use to enter financial information into your cash receipts journal, as shown in table 3.2.

There are also invoices that you receive and invoices that you create for inventory bought and sold on credit terms. These will be entered into the purchases and sales journals, as shown in table 3.3. Adjustments notes, for when goods are returned (previously called credit notes), will be the source of information for your returns journals.

Legal obligations

Only transactions that give rise to a legal obligation are to be entered into your accounting records. If you issue a purchase order to buy some stock, you do not enter the details of that purchase until you receive the invoice from your supplier; in other words until your offer to purchase has been accepted and there is a contract between you.

Cash receipts and cash payments

Originally only the general journal was used to record transactions. It soon became obvious, however, that many transactions were being duplicated time and time again. How many times do you pay wages in a given month? Therefore some special journals were created to handle cash receipts and payments in a more efficient manner. Later in this section we will also examine some special journals that record our credit purchases and sales.

The first stage of the change was to summarise the cash transactions from multiline journal entries into one line in the cash journals, as example 3.1 shows.

Example 3.1

![]()

If we were to use the general journal, the entry would appear as follows:

However, in a cash payments journal the payment could appear like this:

You will notice that we now only need to record the information on one line.

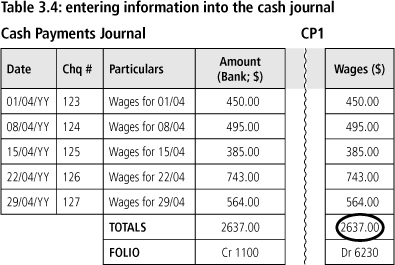

The next innovation was to post the cash journals only once at the end of each month. If we had five wages payments per month, in a general journal we would need 15 lines posted five times to Wages and five times to the Bank account. This would be even more complex if the expense item involved a GST calculation. As table 3.4 shows, in the cash journals we only need the totals of the five lines posted once to Wages and once to the Bank acccount (and if necessary once to the GST).

Table 3.4: entering information into the cash journal

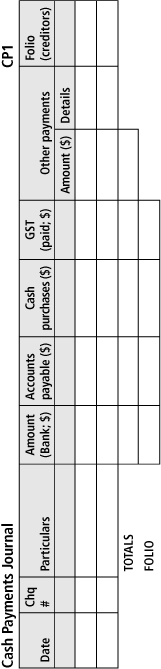

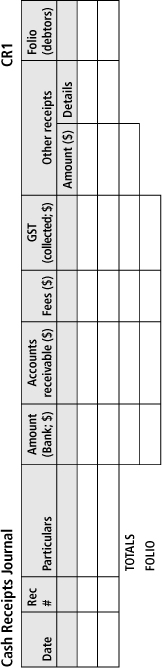

We are now going to expand our cash receipts and cash payments journals, but not fully at this stage. We will only do that once we have discussed returns and allowances. The forms we will use in these exercises are drawn up as shown in example 3.2.

The columns that you decide to use in your cash payments or cash receipts journals are completely up to you, depending upon the business that you are in. There is really no defined structure for the cash journals. For the purposes of this book the number of columns we indicate is limited by its page width. If you use a spreadsheet program to create your cash journals, you can create as many columns as you require. For an example of a spreadsheet cash journal, see my website www.tpabusiness.com.au.

Columns in the cash payments and cash receipts journals are meant to hold details of payments that are made regularly during the month, such as wages paid every week. Where a payment is only made occasionally, such as your quarterly electricity bill, then you would use the Other Payments column to record this. This applies equally to both the cash payments and cash receipts journals. In example 3.2 we will examine a cash payment that only occurs occasionally and therefore doesn’t require its own column but is subject to GST. For this we will refer to our Electricity account.

You will notice that the total credit of $770 to the Bank account equals the total debit of the GST and Other Payments accounts, but the Other Payments amounts are all posted separately.

You should also note the dates used. The date of entry into the ledger of the totals is the last day of the month, such as the Bank and GST accounts, whereas the Other Payments, such as the Electricity and Gas accounts used in this example, are posted using the actual date of the payment.

Let’s now try an exercise.

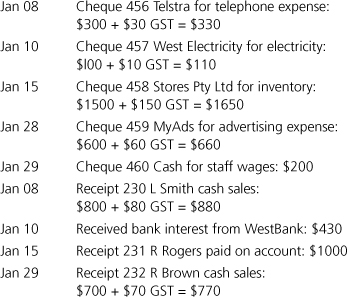

Exercise 3.1

Post the following transactions to the cash payments and cash receipts journals using the forms drawn up as shown. They can also be downloaded from my website www.tpabusiness.com.au.

Purchases of assets on deposit using part cash, part credit

All cash payments must be accounted for through the cash payments journal, but how do we record a transaction if we purchase an item partly with cash and partly with credit? In this case we’ll use the example of the purchase of a Ford Falcon motor vehicle for $36 000 on 20 per cent deposit and the remainder on credit terms from Little Motors.

Firstly we will account for the motor vehicle and GST in full using the general journal, as is shown in table 3.5. Little Motors will be opened as a liability account in its own right — a sundry creditor. It is not considered under Creditors (Accounts Payable) as the purchase did not relate to the credit purchase of inventory.

Next we will draw the cheque on Little Motors and enter the cheque details into the cash payments journal, as shown in table 3.6.

Accounts payable and accounts receivable

When you make credit purchases or credit sales of inventory, in other words goods for resale, you will make your final settlement payment through the cash payments journal and receive payment for goods sold through the cash receipts journal. These credit purchases and sales are made via the purchases and sales journals where the actual purchase or sale and GST have been accounted for. Therefore, as shown in example 3.3 (overleaf), when you settle your accounts, or receive payment, the amount will go into the Bank and the Accounts Payable or Receivable accounts only — there is no additional GST required.

Example 3.3

![]()

Cash sales and cash purchases

Only credit sales and purchases of inventory are accounted for through the sales and purchases journals. All cash sales and purchase of inventory are accounted for through the sash receipts and cash payments journals. In the case of cash sales and cash purchases, you account for both the sale and the GST through the cash receipts and cash payments journals, as shown in example 3.4.

Example 3.4

![]()

Business rules regarding the cash book

All cash payments and all cash receipts will be accounted for through the cash books. There are no exceptions. Any amount that is debited or credited to the Bank account will come via the cash book.

It should also be noted that all payments should be via cheque (or EFTPOS or direct debit) and that the use of hard currency should be discouraged. For minor purchases, such as staffroom tea and coffee, a petty cash book should be used.

All receipts should be deposited in full. There should be no deductions or amounts taken from the cash received, irrespec-tive of the reason.

Computerised accounting: spend money/receive money

In a computerised accounting program, the cash amounts are entered through Cash Payments (Spend Money in MYOB) or Cash Receipts (Receive Money in MYOB) modules that, in practice, are very similar to the cash payments and cash receipts journals. However, there are two types of computerised accounting packages. Those named a ‘cash book’ generally have a data entry screen that mimics the manual cash book, while ‘accounting’ programs such as MYOB have a ‘header’ that often looks like a cheque or receipt and has a grid similar to a spreadsheet where you enter in the details, as indicated by the screenshot in figure 3.1 (overleaf).

Figure 3.1: MYOB ‘spend money’ page

The amounts and details are entered to the correct classifications, a screen of data at a time, similar to a row of data at a time in a manual system, but then like the journal, the posting to the general ledger and the trial balance are automated processes, with the GST calculation also automated. There is no need to post the totals at the end of the month; however, computerised systems still retain the monthly rollover concept as a method of internal control.

The dual use of the cash payments and cash receipts journals and the general journal for some transactions, such as the purchase of a motor vehicle on credit terms with a deposit, is handled the same whether you are using a manual or computerised system.

Revision exercise for day 3

Post the following entries to the appropriate cash payments or cash receipts journals using the same headings as the forms shown overleaf, using as many lines as you require. They can also be downloaded from my website www.tpabusiness.com.au.

Now post the amounts that you have entered into your cash book into the appropriate general ledger accounts (using as many as you require) and then prove the posting through a trial balance. You are to allocate names and numbers to the accounts as you deem appropriate.

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.