Day 4: End-of-month reconciliations - proving our transactions

Key terms and concepts

• Bank reconciliation statement: the form we use in the process of reconciling your bank statement to your Cash at Bank account.

• You must reconcile your bank statement to your Cash at Bank account on a monthly basis. Before you complete your quarterly BAS, you must ensure that all three months of that quarter have been reconciled. This is a crucial aspect of your bookkeeping process.

So far we have learned how to classify using our chart of accounts, record our transactions into journals and post them to the general ledger accounts, and shortcut that process by using special journals to summarise that data before it is posted to the ledger.

Now we must prove our work. This is done in two ways. Firstly our trial balance will prove that all of our debits equal all of our credits, but, as discussed in this chapter, these amounts will not necessarily all be correct. Secondly, we will prove the bank account data through a process known as the bank reconciliation.

Bank reconciliations

Accounting involves continual cross-checking. When you posted the cash book to the general ledger accounts in the revision exercise in day 3, you double-checked your posting through a trial balance. In the case of a bank reconciliation, we cross-check the details in our ledger’s Cash at Bank account to ensure they are correct by comparing them with our bank statement and explaining (reconciling) any differences. We do this before we total off and post to the cash book. The ‘cash book’ is the term we use when referring to the cash payments and cash receipts journals when viewed together.

When you first set up your business cheque account, arrange to receive a bank statement on a regular monthly basis, either electronically or by mail. Your monthly accounts cycle should consist of the following tasks:

• entering cash amounts received or disbursed into your cash book

• checking your bank statement for any amounts not already included in your cash book, such as bank fees and direct debit amounts, and entering them into your cash book

• reconciling your bank account to ‘prove’ your figures

• totalling your cash book

• posting the totals to your ledger

• double-checking your ledger postings with a trial balance.

You may question why we are attempting to ‘reconcile’ and not ‘equal’ our bank account figures. The reason is that it’s unlikely your ledger’s Cash at Bank account will equal your bank statement balance, even after you have taken into account all of the amounts that were added to your bank statement without your knowledge, such as bank fees and direct debits. The main reasons for this are:

• unpresented cheques. When you write a cheque you often use the post to deliver it. The recipient of your cheque then has to deposit it in their bank account. It can then take 15 or more days before the cheque is presented on your bank statement, even though you recorded the cheque in your ledger on the day it was written.

• outstanding deposits. The golden rule is that you must deposit all monies received on the day you actually receive them. However, if you use your bank’s night safe facility, it is possible that your funds won’t be processed until the next working day, which could be the first working day of the following month and hence the possibility of an outstanding deposit appearing on your bank statement.

Reconciling your bank account

After you have recorded all of your receipts and payments for the month in your cash book, ensure you have completed the following steps before you total off.

Step 1: compare your most recent bank reconciliation statement with your bank statement

This bank reconciliation statement will undoubtedly contain unrecorded deposits and unpresented cheques. It is hoped that over the course of the months those amounts will have found their way onto your latest bank statement. Tick off last month’s outstanding amounts against this month’s bank statement and note any amounts that remain outstanding.

Step 2: cross-check your cash book amounts against your bank statement

Tick off each amount listed in your cash book against the relevant amount on your bank statement. If your cash receipts book doesn’t contain a ‘Deposited’ column, you may have to do some calculations to come up with the bank statement deposits.

Step 3: cross-check your bank statement against your cash book

Examine your bank statement for any amounts that have not been included in your cash book to date, such as bank fees, interest earned or paid, direct debit payments and receipts. Write these amounts into your cash book with the date of entry into the bank statement and the word BANK as the receipt or cheque number. All amounts in your bank statement should now be accounted for in your cash book.

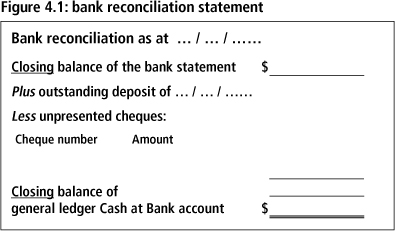

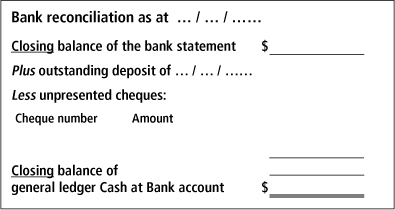

Step 4: complete your bank reconciliation statement

Firstly, take note of any amounts in your cash book that have not been ticked off. These are the outstanding deposits and unpresented cheques that will appear on your bank reconciliation statement. You are now in a position to write up your bank reconciliation statement in the format as shown in figure 4.1 (overleaf).

If the closing balance of your bank statement equals your ‘calculated’ Cash at Bank account balance, you can go ahead and total off and post your cash book. If not, you start again.

The step-by-step process described in this section to reconcile your bank account is shown in example 4.1.

Example 4.1

Our bank statement for May is as follows:

Step 1 is to check that the outstanding amounts from last month’s bank reconciliation statement are shown on this month’s bank statement.

Step 2 is to tick off our cash book amounts against our bank statement, noting any amounts included in our cash book that are not indicated on the bank statement.

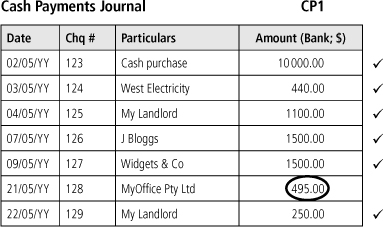

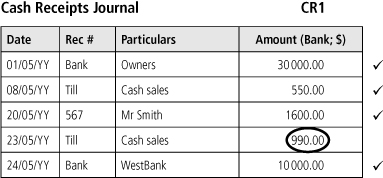

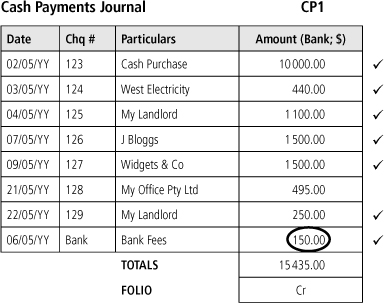

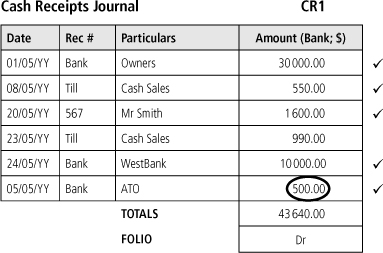

Our cash book written up with known amounts for May appears as follows:

Step 3 is to insert any amounts from our bank statement that have not yet been included in our cash book, such as bank interest or charges and direct debits. Next total off the cash book, which will be presented as follows:

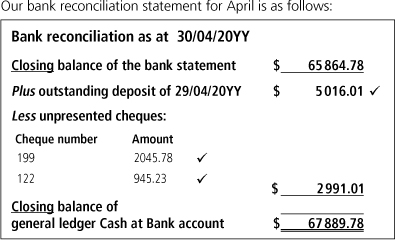

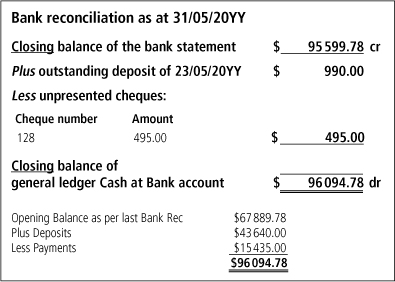

Step 4 is to write up our bank reconciliation statement, which will look like the figure overleaf:

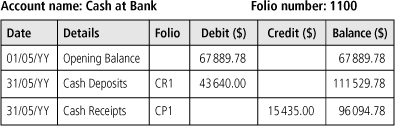

As the bank reconciliation now balances, we can total off our cash book and post the totals to our general ledger accounts and verify our posting through a trial balance. At the end of this process our Cash at Bank account will look like the following:

For an opportunity to complete a bank reconciliation yourself, try exercise 4.1.

Exercise 4.1

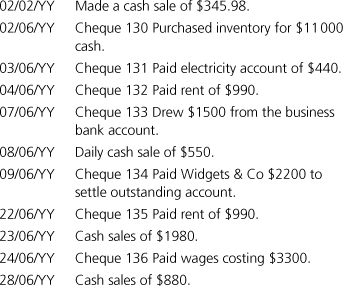

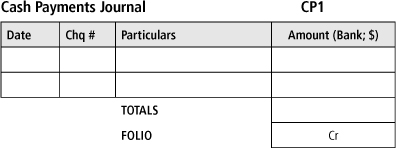

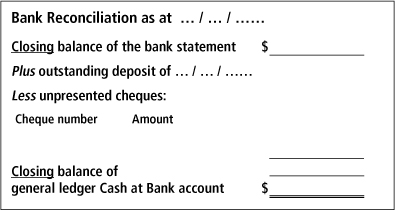

Enter the following transactions into the appropriate abbreviated cash payments or cash receipts journals for June using the same headings as in the forms shown, using as many lines as you require. Next post the bank totals to the Cash at Bank account and finally write up a bank reconciliation statement.

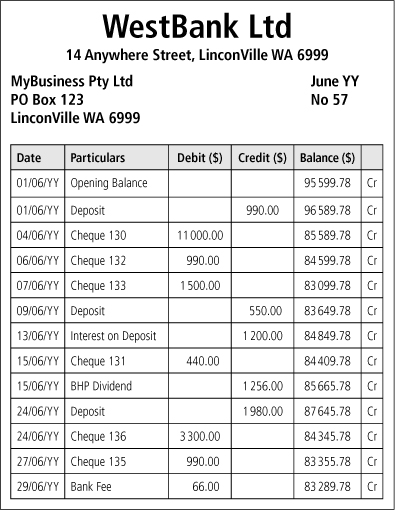

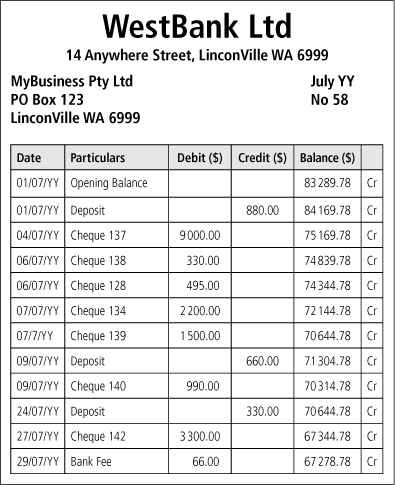

Our bank statement for June appears as follows:

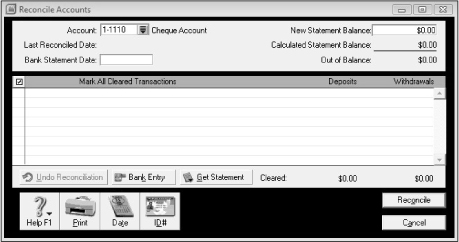

Computerised accounting

Performing a bank reconciliation in a computerised accounting program is very similar to the manual process. It still requires you to ‘tick off’ the cash entries against your bank statement and to input any information contained in your bank statement that is not included in your records. The actual process to complete the bank reconciliation is a little easier, but on the whole it’s still a fairly labour-intensive manual process. The screenshot in figure 4.2 shows a default bank reconciliation form.

Figure 4.2: computerised accounting program bank reconciliation form

Some accounting packages allow you to download your bank statement into your accounting system to make the process a little easier. This can be useful, but it’s still important that you familiarise yourself with the manual process first so that you fully understand what your computerised accounting program is trying to do.

Revision exercise for day 4

Using the forms as shown, post the following transactions to the appropriate abbreviated cash payments or cash receipts journals for July. Next post the bank totals to the Cash at Bank account and then finally write up a bank reconciliation statement.

Our bank statement for July appears as follows:

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.