Chapter 1

Pedal to the Metal

While I was launching my startups, I often heard that nine out of ten startups fail. I have seen this statistic challenged, but it is clear to anyone involved with startups that the odds are stacked against the entrepreneur. It has been shown time and time again that entrepreneurs launch startups that have high degrees of uncertainty. With higher degrees of uncertainties come greater risks. With greater risks come greater rewards, along with a greater chance to fail. So, as an entrepreneur you might be tempted to conclude that high failure rates are something you must live with. I disagree and contend that with the proper management techniques you can increase your chances to succeed. Before you start deploying traditional management techniques, let me share a little history on these techniques.

A Little History

Traditional management techniques are based on a 1930s movement focused on helping large corporations manage their firms. Many believe that Peter Drucker, an icon in the world of management, started this movement. Drucker was a fascinating person with a rich history. His view of the world was most definitely shaped by his father, who used to have gatherings that included guests like Sigmund Freud and Joseph Schumpeter. Drucker evolved a strong interest in human behavior, which eventually led to a desire to understand how humans engage in business. This interest led him to write a number of very important management books, at a time when only a handful of books on the subject existed. Go into any bookstore and walk over to the business section and you will find numerous books by Drucker. Do a search on management on Amazon.com and Drucker's books will appear. His contribution to management practices and theory is what led to him being “known widely as the father of management.”1

It's interesting to note that business schools weren't always regarded so highly as today. In fact, when Drucker first began his study of management in the 1930s and 1940s, business schools were poorly regarded.2 What changed? One theory is that the rise of business schools was driven by the rise of business consulting. In his book The Lords of Strategy,3 author Walter Kiechel III writes about the rise of business consulting from its modest roots in the 1930s to the current multibillion-dollar industry. Kiechel discusses how the Boston Consulting Group (BCG) revolutionized the consulting business by introducing frameworks that helped large firms gain competitive advantages. These effective frameworks helped consulting firms like BCG bill millions of dollars.

Traditional Management Tools Fail Entrepreneurs

Unfortunately, the traditional management frameworks developed by consulting firms fail entrepreneurs. Why? One reason that some experts have put forth is that these management frameworks, theories, and principles were developed for and tested on big corporations like General Electric (GE), not startups, and that the vast majority of the literature and case studies were on large, successful firms. This rings true to me, as a search for entrepreneurship on the Harvard Business Review website returns only 40 books, whereas a search for strategy returns 444 books and innovation 224 books. While consulting firms' focus was on corporations, successful startups like Microsoft and Apple were thought to have succeeded on the sheer will and talents of their celebrity founders. Movies on Steve Jobs and Bill Gates further perpetuated the myth that entrepreneurs were born rather than made and that one should not constrain these artistlike entrepreneurs with a structured approach. In the face of overwhelming media hype, entrepreneurs around the world absorbed these myths into their DNA.

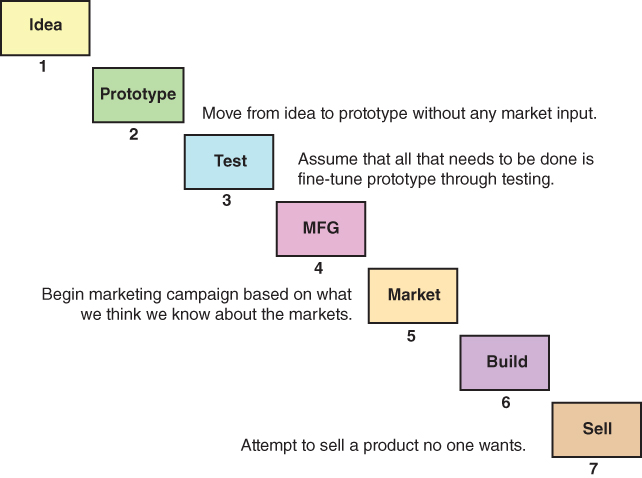

In the early 1990s, I set off to start my first business, which was a digital prepress operation. Like so many other entrepreneurs, I bought into the myth of Jobs and Gates, who at the time were the equivalent of Mark Zuckerberg and Larry Page today. I did so by doing what I saw in the movies—I proceeded to deploy traditional management techniques. The steps I took are consistent with a traditional new product development framework (see Figure 1.1):

Figure 1.1 Traditional Product Development

I also picked up every business plan book I could find at the bookstore—no Amazon back then. In addition, I spoke to successful business professionals and I looked to my experience at General Motors (GM). I succeeded; however, I didn't realize it at the time, but the steps work rather well when a firm is trying to produce a new iteration of a current product, yet they fail miserably when applied to more breakthrough-type innovation opportunities. It wasn't until my third startup, Ironsilk, that I came to realize that this traditional approach does not work with game-changing, disruptive, or discontinuous types of innovation.

The steps are an overview of the traditional new product development method, and they are by no means comprehensive. There are many tools that big firms use to bring new products to market, including phase gate, surveys, and focus groups, that when applied to startups fail to deliver results. Why? It comes down to the level of uncertainty that surrounds new product development. “New” in most new product development teams means incrementally new. When I was working at General Motors, most of the new product development centered on marketable incremental improvements to existing products. These incrementally improved products have low levels of uncertainties, as the firm has built up a great deal of knowledge in bringing this type of product to market. In most cases the firm will already have resources and capabilities tailored to test, manufacture, market, sell, and support the incrementally improved product. The customers, distribution channels, and partnerships are all essentially the same. That's why the firm is able to focus and execute on the plan. What happens when a firm has no past experience to fall back on? How does it determine the criteria to be used in a phase gate process when it doesn't have the experience to know what's important? In these cases the startup needs to focus on learning about the technical, market, resource, and organization factors that will drive the business.

Why Startups Fail

The topic of startup failure is both complex and important. It's complex because we are dealing with decades of misconceptions as to what startups do, how they do it, and how they succeed. It's important because startups create lots and lots of jobs.

The importance of startup failure has led to millions, if not billions, of dollars invested in trying to get an answer to the question “Why do startups fail?” The effort is driven by the fact that job growth is fueled by startups. A look at the often-referenced statistics from U.S. Census Bureau's 2007 Survey of Small Business Owners reveals that in 2005 small businesses with fewer than five employees accounted for only 163,000 net jobs created. By comparison, firms with five employees or more created over 2.3 million net jobs. The Kaufman Foundation while examining the same statistics delivered good news and bad news. The good news was that recently launched startups created over three million jobs; the bad news was that existing startups lost over one million jobs. The reason for the lost jobs was startup failure. How much failure? Well, the failure rate of startups is open to interpretation. I've seen failure rates vary from 25 to 93 percent depending on who is doing the reporting. According to a Wall Street Journal article, Shikhar Ghosh of the Harvard Business School performed a study that showed that 75 percent of venture capital (VC)-backed firms failed. Yet, the same article points out that the National Venture Capital Association estimates that only 25 percent of VC-backed startups fail.4 The difference in the stats is due to how one defines failure. If you use the most common definition of failure, that investors in a startup are not getting a return on their investment, then according to Ghosh the failure rate is 75 percent. Now, he was researching venture-backed startups, but what about bootstrapped startups that fund themselves through family, friends, savings, credit cards, and mortgages? The numbers can only get worse, as venture-backed startups are considered the most promising startups. What about corporate startups? Are the failure rates any different within the secure walls of a corporation? We will be discussing this further in the chapters to come.

If we could figure out why startups fail, then we might be able to figure out how to help them succeed. There is no lack of theories as to why they fail. Some experts point to the lack of experienced teams, others believe it has to do with the inherent risk associated with breakthrough innovation, and some believe it has to do with the low barriers to entry. Some recent studies have suggested that startups self-implode by prematurely scaling. I agree with all of them. Startups fail for a variety of reasons, because they are launching high-impact business opportunities with high levels of technical, market, resource, and organization uncertainty. Later in the book we will go into greater depth on uncertainties, but for now let us touch upon a way to think about them. The opposite of uncertainty is certainty. When you accidentally knock a glass off the kitchen table, you know for certain that the glass will fall to the floor. This is certainty. You don't know whether the glass will shatter, crack, or remain intact. This unknown outcome to knocking a glass off the table is considered uncertainty. If the outcome can lead to a loss, then this possibility is considered a risk. When a startup begins with an idea, the number of unknowns and guesses is very large; therefore the degree of uncertainty is high. Since the startup is investing time, money, and reputations, some of the possible outcomes can lead to losses in those areas; therefore the startup is taking risks. If the startup is unaware of the risks and uncertainties, then the likelihood of guessing everything right from day one is probably around the same as the likelihood of winning a major lottery. If the startup is aware of the risks and uncertainties but does not know how to manage them, then it will most likely fail. The key to improving a startup's chances of success lies in the startup's ability to manage uncertainties and correctly determine what risks to assess.

Origins of the Pivot Methodology

Most entrepreneurs will tell you that they had to pivot or change course at least once on the path to success. Groupon stemmed from a do-good website called The Point. PayPal started as cryptography-based libraries for Palm Pilot devices. Hotmail started as browser-readable database software. TiVo started as a home server network. YouTube started as a video-dating platform. Twitter first launched as Odeo, a platform to subscribe to podcasts.5 These startups were hugely successful; unfortunately, as we have discussed, the vast majority of startups fail. Some of these successful startups got lucky stumbling upon a new path, and some experimented with a new path. In all cases, they changed from the path they initially felt was best to a new path to success.

The question for the startups that failed or for the startups that were one pivot away from failure is: “Could you have avoided or reduced all the wasted resources and time that it took to launch your product or service only to fail at attracting enough customers to succeed?” There is now a general consensus among thought leaders in the field of entrepreneurship and innovation that the answer to this question is a resounding yes. I must admit that the corporate startup professionals got there before the individual startup professionals did. A reason for this could be that corporations might have been looking into how to innovate for a very long time and therefore funding a great deal of the effort that went into examining all aspects of innovation. In contrast, movies and books have painted a picture of startup success based on determination, intellect, and hard work against insurmountable odds, and this has led startups astray. This picture was intoxicating to technology geeks like me who grew up watching Star Trek and Star Wars. So, instead of managing startups, entrepreneurs used a seat-of-the-pants, gut-check approach to launching startups that led to one slow failure after another.

There is an effort afoot by experienced startup professionals to question the pedal to the metal mind-set by changing the way startups are managed to a more structured approach based on learning, knowledge construction, and the reduction of uncertainty. Experienced professionals like me have put forth methodologies centered on validated learning loops, which have been used to construct market experiments aimed at getting better answers quicker than before. As I will go into more detail in Chapter 4, this concept first appeared in the mid-1980s. My love for startups drove me to work on this for the past eight years, bringing my experience as an entrepreneur, professional, and mentor together with the latest academic research on best startup practices to work on The Pivot Startup methodology. I believe that the path to success is paved with learning better and quicker than the competition.

My coauthor, Joanne Hyland, has also been teaching the principles of validated learning since she launched her consulting firm in 2001. In Chapters 2 and 3, she will set the stage for why innovation is about bringing discipline to chaos and will introduce the corporate entrepreneur.

Notes

1. Leigh Buchanan, “The Wisdom of Peter Drucker from A to Z,” Inc.com, 2009, www.inc.com/articles/2009/11/drucker.html.

2. “Remembering Drucker,” The Economist, November 19, 2009, www.economist.com/node/14903040?story_id=14903040.

3. Walter Kiechel III, The Lords of Strategy (Boston: Harvard Business School Press, 2010).

4. Deborah Gage, “The Venture Capital Secret: 3 out of 4 Start-Ups Fail,” Wall Street Journal, September 19, 2012, http://online.wsj.com/article/SB10000872396390443720204578004980476429190.html.

5. “Best Pivots in Internet History,” Ranker.com, February 13, 2013, www.ranker.com/list/best-pivots-in-internet-history/ready-to-startup.