III

DIVERSIFY

A very sad story illustrates the crucial need for investors to diversify their investment holdings. It concerns a secretary who worked for the Enron Corporation during its heyday in the late 1990s and early 2000s. Enron was one of the new-age companies that formed to revolutionize the market for electric power and mass communications. Two charismatic masterminds, Kenneth Lay and Jeff Skilling, ran Enron and were regularly lionized by the press for their skill and daring. Enron stock was the darling of Wall Street, and it seemed to defy gravity by rising steadily into the stratosphere.

Like most major companies, Enron had established a 401(k) retirement plan for its employees, offering a range of options for the regular savings contributions that would be automatically deducted in each pay period. One of the investment options in the plan was to put those contributions into Enron stock. The chief executive officer, Ken Lay, strongly recommended that employees use Enron stock as their preferred retirement vehicle. Enron was likened to Elvis Presley revolutionizing the music scene. The old power companies were like old fogies dancing to the music of Lawrence Welk. And so the secretary put all of her retirement savings into Enron stock, and how glad she was that she did. As the stock soared, while she had never earned more than a modest secretary's pay, her retirement kitty was worth almost $3 million. During the next year, she looked forward to retirement and a life of leisure and world travel.

Well, she got her wish for more “leisure.” As we now know, Enron had been built on a mosaic of phony accounting and fraudulent trading schemes. Jeff Skilling went to jail, and Ken Lay died while awaiting trial. The stock price collapsed, and the secretary's entire retirement kitty vaporized. She lost not only her job, but also her life savings. She had made the mistake of putting all her investments in one basket. Not only did she fail to diversify her investments, but she put herself in double jeopardy because she took exactly the same risks with her portfolio as she did with her income from employment. She failed to heed one of the few absolute rules of investing: Diversify, Diversify, Diversify.

James Rhodes spent his entire career in the automobile industry casting iron dies that turned sheet metal into fenders, hoods, and roofs. When he left the business, he and his wife decided that they could securely invest their entire accumulated savings in Chrysler bonds, paying an attractive 8 percent interest rate per year. They, like so many autoworkers, had faith in the iconic big three automakers’ ability to survive even in the worst economic times. And the generous interest payments allowed them to continue to enjoy a comfortable middle-class lifestyle—for a while. Now the Rhodeses’ faith in the auto industry and their retirement savings have evaporated. Many individual investors lost almost everything as the bankruptcy of Chrysler and General Motors left the secured bond-holders with no continuing interest payments and only a minimal equity stake in the bankrupt companies.

These very sad stories make all too clear the cardinal rule of investing: Broad diversification is essential.

Enron, Chrysler, and General Motors are not isolated examples. Surprisingly, many large and seemingly stable industrial companies have gone belly up. Even large financial institutions—banks such as Wachovia, investment firms such as Lehman Brothers, insurance companies such as AIG—have gone bankrupt or were forced into mergers or government trusteeship after the value of their stocks cratered. And many financial executives, who should have known better, were wiped out because they had all of their assets invested in the firms where they worked, feeling loyalty and confidence in “their” company. If we had our way, no employee contributions to a 401(k) plan could be invested in their own company. Protect yourself: Every investor should always diversify.

Protect yourself: Every investor should always diversify.

DIVERSIFY ACROSS ASSET CLASSES

What does diversification mean in practice? It means that when you invest in the stock market, you want a broadly diversified portfolio holding hundreds of stocks. For people of modest means, and even quite wealthy people, the way to accomplish that is to buy one or more low-cost equity index mutual funds. The fund pools the money from thousands of investors and buys a portfolio of hundreds of individual common stocks. The mutual fund collects all the dividends, does all the accounting, and lets mutual fund owners reinvest all cash distributions in more shares of the fund if they so wish.

While some mutual funds are specialized, concentrating in a particular market segment such as biotechnology companies or Chinese companies, we recommend that the fund you choose have a mandate of broad diversification and hold securities in a wide spectrum of companies spanning all the major industries. We will give you tips in Chapter 5 on how to select the best, lowest-cost, and most diversified investment funds available.

Diversify across securities, across asset classes, across markets—and across time.

By holding a wide variety of company stocks, the investor tends to reduce risk because most economic events do not affect all companies the same way. A favorable event such as the approval of a new pharmaceutical could be a major boost for the company that discovered the drug. At the same time, it could be damaging to companies making older competing products. Even deep recessions will have different effects on companies catering to different demographic groups. As people tightened their belts, they buy less from Tiffany's and more from Wal-Mart.

Just as you need to diversify by holding a large number of individual stocks in different industries to moderate your investment risk, so you also need to diversify by holding different asset classes. One asset class that belongs in most portfolios is bonds. Bonds are basically IOUs issued by corporations and government units. (The government units might be foreign, state and local, or government-sponsored enterprises such as the Federal National Mortgage Association, popularly known as Fannie Mae.) And just as you should diversify by holding a broadly diversified stock fund, so should you hold a broadly diversified bond fund.

The U.S. Treasury issues large amounts of bonds. These issues are considered the safest of all and these bonds are the one type of security where diversification is not essential. Unlike common stocks, whose dividends and earnings fluctuate with the ups and downs of the company's business, bonds pay a fixed dollar amount of interest. If the U.S. Treasury offers a $ 1,000 20-year, 5 percent bond, that bond will pay $ 50 per year until it matures, when the principal will be repaid. Corporate bonds are less safe, but widely diversified bond portfolios have provided reasonably stable interest returns over time.

High-quality bonds can moderate the risk of a common stock portfolio by providing offsetting variations to the inevitable ups and downs of the stock market. For example, in 2008, common stock prices fell in both U.S. and foreign markets as investors correctly anticipated a severe worldwide recession. But a U.S. Treasury bond portfolio rose in price as the monetary authorities lowered interest rates to stimulate the economy. If you are confused about how bond prices change as interest rates rise and fall, just remember the “see-saw” rule: When interest rates fall, bond prices rise. When interest rates rise, bond prices fall.

Other asset classes can reduce risk as well. In 2008, all stock markets around the world fell together. There was no place to hide. But during most years, while some national markets zig, others zag. For example, during 2009, when all the major industrial countries were sinking into a deep recession, countries such as China, which was developing its vast central and western regions, continued to grow.

During inflationary periods, real estate and real assets such as timber and oil have usually provided better inflation hedges than ordinary industrial companies whose profit margins are likely to get squeezed when raw material prices rise. Hence, real estate and commodities have proven to be useful diversifiers in many periods. Gold and gold-mining companies have often had a unique role as the commodity of choice for diversification. Gold has historically been the asset to which investors have fled during uncertain and perilous times. It is often called the hedge against Armageddon.

If you purchase the very broad-based index funds we list later in this book, you will achieve some of the benefits of direct real estate and commodities investing. So-called “total stock market” funds will include both real estate companies and commodity products. Broad equity diversification can be achieved with one-stop shopping.

DIVERSIFY ACROSS MARKETS

The stocks of companies in foreign markets such as Europe and Asia also can provide diversification benefits. To be sure, there is some truth to the expression that when the United States catches a cold, the rest of the developed world catches pneumonia; the market meltdowns and painful recessions of 2008–2009 were worldwide. But that does not mean that economic activity and stock markets in different developed nations always move in lockstep. During the 1990s, when the U.S. economy was booming, Japan's economy stagnated for the entire decade. During periods in the 2000s when the U.S. dollar was falling, the euro was rising, giving an added boost to European stocks. And even though globalization has linked our economies more and more closely, there is still good reason not to restrict your holding to U.S. stocks. To the extent that you hold automobile stocks in your portfolio, you should not limit yourself to Detroit. You are likely to be better off including Toyota and Honda in a diversified portfolio.

Does achieving extremely broad diversification seem completely out of reach for ordinary investors? Fear not. There are broadly invested, very low-cost funds that can provide one-stop shopping solutions. We will recommend a broadly diversified United States total stock market index fund that includes real estate companies and commodity producers, including gold miners. We will also show you how a non-U.S. total stock market fund can give you exposure to the entire world economy, including the fast-growing emerging markets. Similarly, a total bond market fund will provide you with a fully diversified bond portfolio. If you will follow the diversification principle here, we will show you, in Chapter 5, the specific funds that will allow you to put together a well-diversified portfolio at low cost.

DIVERSIFY OVER TIME

There is one final diversification lesson that we need to stress. You should diversify over time. Don't make all your investments at a single time. If you did, you might be unlucky enough to have put all of your money into the stock market during a market peak in early 2000. An investor who put everything in the market at the start of 2000 would have experienced a negative return over the entire decade. The 1970s were just as bad. And an investor who put everything in at the 1929 peak, like the father of one of the authors, would not have broken even for more than 20 years.

You can reduce risk by building up your investments slowly with regular, periodic investments over time. Investing regular amounts monthly or quarterly will ensure that you put some of your money to work during favorable periods, when prices are relatively low. Investment advisers call this technique “dollar-cost averaging.” With equal dollar investments over time, the investor buys fewer shares when prices are high and more shares when prices are low. It won't eliminate risk but it will ensure that you don't buy your entire portfolio at temporarily inflated prices. The experience of putting your entire investment in the stock market at a wrong time could sour you on common stocks for an entire lifetime, sadly compounding the problem.

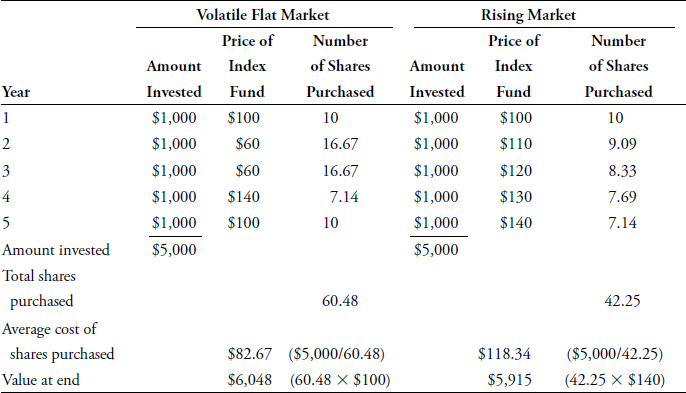

With dollar-cost averaging, investors can actually come out better in a market where prices are volatile and end up exactly where they started than in a market where prices rise steadily year after year. Suppose that all investments are made in a broad stock market index fund and that $ 1,000 is invested each year over a five-year period. Now let's consider two scenarios: In the first scenario, the stock market is very volatile, declining sharply after the program is commenced and ending exactly where it started. In the second scenario, the stock market rises each year after the program begins. Before we look at the numbers, ask yourself under which scenario the investor is likely to do better. We bet that almost everybody would expect to have better investment results in the situation when the market goes straight up. Now let's look at the numbers.

The table on page 63 assumes that $ 1,000 is invested each year. In scenario one, the market falls immediately after the investment program begins; then it rises sharply and finally falls again, ending, in year five, exactly where it began. In scenario two, the market rises continuously and ends up 40 percent higher at the end of the period. While a total of exactly $ 5,000 is invested in both cases, the investor in the volatile market ends up with $6,048—a nice return of $1,048—even though the stock market ended exactly where it started. In the scenario where the market rose each year and ended up 40 percent from where it began, the investor's final stake is only $5,915.

Warren Buffett presents a lucid rationale for the investment principle illustrated above. In one of his published essays he says:

A short quiz: If you plan to eat hamburgers throughout your life and are not a cattle producer, should you wish for higher or lower prices for beef? Likewise, if you are going to buy a car from time to time but are not an auto manufacturer, should you prefer higher or lower car prices? These questions, of course, answer themselves.

Dollar-Cost Averaging

But now for the final exam: If you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period? Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall. In effect, they rejoice because prices have risen for the “hamburgers” they will soon be buying. This reaction makes no sense. Only those who will be sellers of equities in the near future should be happy at seeing stocks rise. Prospective purchasers should much prefer sinking prices.

Dollar-cost averaging is not a panacea that eliminates the risk of investing in common stocks. It will not save your 401(k) plan from a devastating fall in value during a year such as 2008, because no plan can protect you from a punishing bear market. And you must have both the cash and the confidence to continue making the periodic investments even when the sky is the darkest. No matter how scary the financial news, no matter how difficult it is to see any signs of optimism, you must not interrupt the automatic-pilot nature of the program. Because if you do, you will lose the benefit of buying at least some of your shares after a sharp market decline when they are for sale at low-end prices. Dollar-cost averaging will give you this bargain: Your average price per share will be lower than the average price at which you bought shares. Why? Because you'll buy more shares at low prices and fewer at high prices.

Some investment advisors are not fans of dollar-cost averaging because the strategy is not optimal if the market does go straight up. (You would have been better off putting all $ 5,000 into the market at the beginning of the period.) But it does provide a reasonable insurance policy against poor future stock markets. And it does minimize the regret that inevitably follows if you were unlucky enough to have put all your money into the stock market during a peak period such as March of 2000 or October of 2007.

REBALANCE

Rebalancing is the technique used by professional investors to ensure that a portfolio remains efficiently diversified. It is not complicated, and we believe that individual investors should rebalance their portfolios as well. Since market prices change over time, so will the share of your portfolio that is in stocks or bonds. Rebalancing simply involves periodically checking the allocation of the different types of investments in your portfolio and bringing them back to your desired percentages if they get out of line. Rebalancing reduces the volatility and riskiness of your investment portfolio and can often enhance your returns.

Suppose you have decided that the portfolio balance that is most appropriate for your age and your comfort level has 60 percent in stocks and 40 percent in bonds. As you add to your retirement accounts, you put 60 percent of the new money into a stock fund and the remainder into a bond fund.

Movements in the bond and stock markets will tend to shift your allocation over time. Small changes (plus or minus 10 percent) should probably be ignored. But what if the stock market doubles in a short period and bond values stay constant? All of a sudden you would find that three-quarters of your portfolio is now invested in stocks and only one-quarter is allocated to bonds. That would change the overall market risk of your portfolio away from the balance you chose as best for you. Or what if the stock market falls sharply and bonds rise in price, as was the experience of investors in 2008? What do you do then?

The correct response is to make corrective changes in the mix of your portfolio. This is what we mean by “rebalancing.” It involves not letting the asset proportions in your portfolio stray too far from the ideal mix you have chosen as best for you. Suppose the equity portion of your portfolio is too high. You could direct all new allocations, as well as the dividends paid from your equity investments, into bond investments. (If the balance is severely out of whack, you can shift some of your money from the equity fund you hold into bond investments.) If the proportion of your investments in bonds has risen so that it exceeds your desired allocation, you can move money into equities.

The right response to a fall in the price of one asset class is never to panic and sell out. Rather, you need the long-term discipline and personal fortitude to buy more. Remember: The lower stock prices go, the better the bargains if you are truly a long-term investor. Sharp market declines may make rebalancing appear a frustrating “way to lose even more money.” But in the long run, investors who rebalance their portfolios in a disciplined way are well rewarded.

When markets are very volatile, rebalancing can actually increase your rate of return and, at the same time, decrease your risk by reducing the volatility of your portfolio.

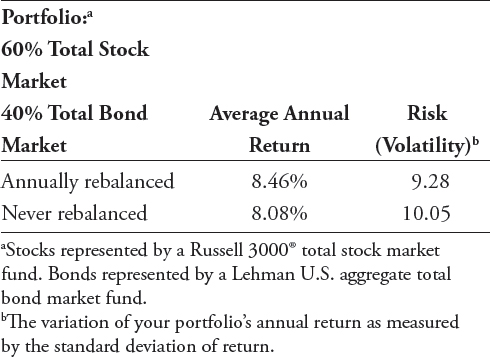

The decade from 1996 through 2005 provides an excellent example. Suppose an investor's chosen allocation is 60 percent in stocks and 40 percent in bonds. Let's use a broad-based U.S. total stock market index fund for the equity portion of the portfolio and a total bond market index fund for the bonds to illustrate the advantages of rebalancing. The table on page 69 shows how rebalancing was able to increase the investor's return while reducing risk, as measured by the quarterly volatility of return.

If an investor had simply bought such a 60/40 portfolio at the start of the period and held on for 10 years, she would have earned an average rate of return of 8.08 percent per year. But if each year she rebalanced the portfolio to preserve the 60/40 mix, the return would have increased to almost 8½ percent. Moreover, the quarterly results would have been more stable, allowing the investor to sleep better at night.

During the decade January 1996 through December 2005, an annually rebalanced portfolio provided lower volatility and higher return.

The Importance of Rebalancing

Why did rebalancing work so well? Suppose the investor rebalanced once a year at the beginning of January. (Don't be trigger-happy: Rebalance once a year.) During January 2000, near the top of the Internet craze, the stock portion of the portfolio rose well above 60 percent, so some stocks were sold and the proceeds put into bonds that had been falling in price as interest rates rose. The investor did not know we were near a stock market peak (the actual peak was in March 2000). But she was able to lighten up on stocks when they were selling at very high prices. When the rebalancing was done in January 2003, the situation was different. Stocks had fallen sharply (the low of the market occurred in October 2002) and bonds had risen in price as interest rates were reduced by the Federal Reserve. So money was taken from the bond part of the portfolio and invested in equities at what turned out to be quite favorable prices.

Rebalancing will not always increase returns. But it will always reduce the riskiness of the portfolio and it will always ensure that your actual allocation stays consistent with the right allocation for your needs and temperament.

Rebalancing will not always increase returns. But it will always reduce the riskiness of the portfolio and it will always ensure that your actual allocation stays consistent with the right allocation for your needs and temperament.

Investors will also want to consider rebalancing to change their portfolio's asset mix as they age. For most people, a more and more conservative asset mix that has a deliberately reduced equity component will provide less stress as they approach and then enter retirement.