CHAPTER 1

Introduction

A culmination of disruptive forces and evolutionary change in the oil and gas industry have conspired together to make the case for a new, low‐cost operating model. The industry has experienced tremendous evolution in terms of our understanding of the underlying global resource base, the nature of its ownership and principal stakeholders, technologies and methods for resource development, and the economics and business models.

The industry was focused on cost and productivity even before the 2014 collapse in oil prices, but beyond incremental accommodations in response to change there has been little effort to redesign and transform internal enterprise operating models. Unlike other industries that have undertaken operating model transformations in response to disruptive industry forces, upstream companies rarely undertake operating model change on a systematic or enterprisewide basis.

A VITAL INDUSTRY

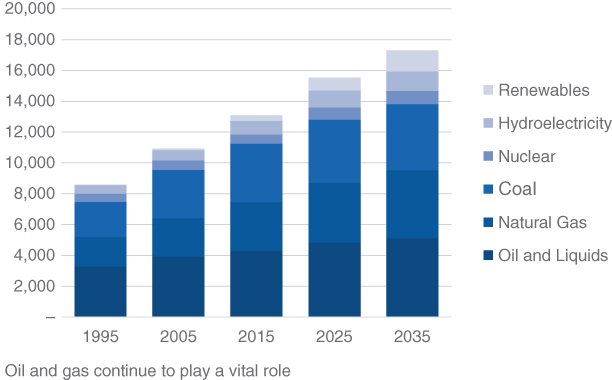

Notwithstanding tremendous advances in renewable energy, hybrids, and electric vehicles (EVs), and agreement among our world leaders to make great strides on behalf of climate change, oil and gas companies are, and will continue to be, an important contributor to the world's energy needs and to the world's economy. Most forecasts, even under aggressive growth trajectories for renewables, still call upon the upstream for one‐half or more of our energy in 20 years.1

In the United States, natural gas and petroleum have played an important role in our energy mix for more than 100 years.2 With the benefit of more than $1.5 trillion over the past 10 years, accounting for about one‐third of all new power generation capacity, renewables now represent a small but important source of energy (see Figure 1.1). Wind and solar provide 5 percent of all electricity consumed in the United States (nuclear power accounts for 63 percent of all non–carbon‐dioxide emitting power sources—the National Review estimates that it will take more than 100 years for solar to replace the electricity currently obtained from nuclear plants).3 Even with the tailwinds of government support at federal, state, and municipal levels, including regulations, tax credits, and direct subsidy, the US Energy Information Administration (EIA) expects “fossil fuels” will provide more than three‐quarters of US primary energy in 2040.

Figure 1.1 World Primary Energy, by Fuel (million tonnes oil equivalent)

Source: BP Energy Outlook 2035

WHAT NOW?

Oil and gas companies have been focused on cost and productivity since before the 2014 collapse in oil prices. Upstream operators have made enormous efforts through massive vendor concessions, capital project deferrals, reductions in force, and “high‐grading” drilling and completion activity to the most productive acreage.

For example, in 2016, one dollar of US onshore capital yielded twice the output (i.e., BOE/D) that it did in 2014, due to lower costs and higher productivity.

The industry has experienced tremendous evolution in terms of our understanding of the underlying global resource base, the nature of its ownership and principal stakeholders, and the methods and technologies for resource development. And business models have evolved considerably with these changes, including the adoption and growth in usage of “drilling promotes” with a carried interest, farm‐outs, and other nonoperated ventures (NOVs), an industry supply chain with a wide array of field services companies, many forms of collaborative ownership and operation through joint ventures (JVs), state ownership and control of natural resources through national oil companies (NOCs), the adoption of corporate shared services models, experimentation with business processes offshoring and/or outsourcing, and much greater use of big‐data analytics and digital solutions within the core operations.

But beyond direct accommodations in response to each of these changes, there has been very little effort to redesign and transform internal enterprise operating models. Moreover, unlike other industries that have undertaken operating model transformations in response to disruptive industry forces (e.g., retail), the upstream rarely undertakes operating model change on a systematic or enterprisewide basis. The notable exception has been event‐driven situations, such as post‐merger integration (PMI) programs where promises of synergies may trigger fundamental reviews of upstream operating models, and major divestitures such as a sale or carve‐out/spin‐off, and initial public offering (IPO) preparation.

Upstream operators were already struggling to earn adequate returns before prices fell, but now face difficulties generating sufficient cash flow even to cover their basic needs—they do not generate enough cash flow to cover operating costs, capital projects, overhead expenses, debt service, dividends, and so on. With oil and gas prices remaining low, hedges rolling off, and sources of cash falling short of uses for cash, the upstream requires fundamental gains in cost and productivity. Many of the largest (and easiest) cuts, like vendor concessions, will not be sustainable over a full cycle. Furthermore, some of the biggest gains thus far are not scalable. And the future supply gap beyond 2020 requires a significant investment to find, develop, and produce resources that are very likely to be relatively expensive barrels.

There must be considerably more work, and more difficult work, to reduce upstream costs. The industry has made great strides for sure, but now the more difficult (but more valuable) task is to sort through:

- What different to do (i.e., setting the strategic agenda)

- What to do differently (i.e., defining the operating model)

The first question (i.e., the “what”) establishes a strategic agenda, and relates to choices in terms of the corporate and business unit strategies, asset portfolios, and business models. Setting the strategic agenda demands choices about what businesses to be in and what assets to own. Perhaps more importantly, the strategic agenda must establish in which “key capabilities” to invest and which activities to “in‐source.” It is impossible to be “world‐class” in every capability—every aspect of activity of the business and therefore critical choices must be made.

The choices about what not to do are often more important than the choices about what to do. Most upstream oil and gas enterprises have a portfolio of too many businesses, too many assets, too many geographies, too many resource types, and too many opportunities, all of which are competing for too little capital, not enough expertise, and too limited a talent pool. Therefore, the most important strategic choices are what not to do. Moreover, these choices require an iterative process to “reconcile” between the following three critical elements of the upstream enterprise:

- Aspirations, goals, and objectives for the business

- Opportunities and needs of the underlying resource portfolio

- Organizational capabilities of the enterprise internal operating model and talent pool

The second question (i.e., the “how”) sets the enterprise operating model, and relates to the internal architecture of the company, its operation, and its governance. Defining the operating model—choices regarding the internal architecture, performance metrics, systems, processes, and culture has a profound impact on the performance of an enterprise. An operating model is effectively the “blueprint” for the internal architecture of an enterprise, its operation, and oversight.

Now, most research and experience with low‐cost operations tends to focus on innovation in business models (rather than enterprise internal operating models) to lower the costs of acquiring and serving customers and enhance the customer experience, often with digital platforms.4–6 Where there is research and experience with low‐cost operating models, it tends to be in consumer‐facing industries, with examples such as Costco, Dell, Southwest Airlines, Walgreens, Wal‐Mart, E*Trade, and IKEA rather than “B2B” industries, or specifically, the upstream oil and gas industry.7,8

INDUSTRY EVOLUTION

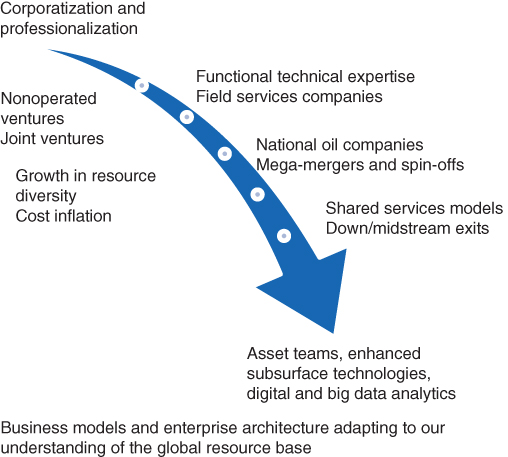

Over the past century, the oil and gas industry has experienced a significant evolution in terms of our understanding of the underlying global resource base, the methods and technologies involved in its development, and the nature of its ownership and principal stakeholders. In conjunction with this change, there has been considerable evolution in business models—but so far, the accommodations made to enterprise internal operating models have been largely incremental (see Figure 1.2).

Figure 1.2 Upstream Evolution

Source: IHS Energy

What began in the early days of the twentieth century as a largely entrepreneurial effort quickly evolved into big business, in part due to the scale of its requirements, in terms of capital and expertise—in the 1960s, oil supply was safe and abundant and not a constraint on economic growth, with excess capacity exceeding demand by about 20 percent of the free world's consumption.9 This fueled the corporatization and professionalization of the industry and facilitated tremendous growth in functional expertise, especially geological and geophysical roles, engineering, and other technical functions. The growth era of 1972–1981 drove large‐scale expansion. While the 1980s were characterized by low prices, layoffs, and consolidation, they also gave rise to innovations in 3D seismic, commercial beginnings for both horizontal and logging while drilling, and many new technologies and service companies.10

While the breadth and depth of technical capabilities flourished, so, too, did the opportunity for specialized field services companies to provide such expertise on an intermittent or as‐needed basis. Similarly, business model adaptations such as nonoperated ventures (NOVs) and joint ventures (JVs) enabled companies to participate in resource development and production activities beyond the reach of their core ownership holdings or core capabilities. These vehicles also facilitated a pooling of financial capital and technical expertise, which were often in short supply, while also syndicating the project risk—which was often considerable.

As oil and gas became big business, many host countries recognized the opportunity to retain a greater share of their resource sector's bounty and control through the adoption of state‐led national oil companies (NOCs)—another variation in the sector's business models. Consolidation among the largest integrated players (mega‐mergers) facilitated consolidation—affording large economic gains in the downstream refining and retail segments of the industry and a consolidation of conventional upstream business. Many companies adopted corporate shared services models for centralized procurement and other business roles.

Consolidation of the world's lowest‐cost conventional resources under NOCs and state ownership caused international oil companies (IOCs) and independent operators to venture further afield into new international frontiers and a growing array of resource types—including ultra‐deep‐water, the arctic, shale gas, tight oil, and the Canadian oil sands. These ventures generally represent much higher cost resources and require even more specialized expertise.

In the aftermath of the collapse in oil and gas prices, efforts to offset the effects of cost inflation and capital constraints have included the sale of many midstream and downstream assets, with many upstream operators exiting these parts of the value chain to focus their efforts (and limited resources) on the needs and opportunities of the upstream. Within the enterprise, this has generally included a migration toward asset team organizations, and investments in key capabilities such as enhanced subsurface capabilities, with improved data processing for 3D seismic, greater use of geomechanical modeling and reservoir engineering, enhanced recovery (EOR), and new applications for digital and big data analytics.

Despite this evolution—our understanding of the resource base, methods and technologies for its development, ownership and stakeholders, business models—there has been little effort to redesign and transform enterprise operating models beyond incremental accommodations. Unlike industries that have undertaken operating model transformations in response to disruptive industry forces (e.g., retail), the upstream rarely undertakes operating model change on a systematic or enterprisewide basis. The notable exception is post‐merger integration (PMI) programs, where promises of synergies often trigger fundamental reviews of operating models.

TEN REASONS TO UPDATE YOUR OPERATING MODEL

Many factors have conspired together to make the case for change—reasons to adopt a low‐cost operating model. A culmination of disruptive forces—including supply gluts in US shale gas and tight oil and growing consensus among world leaders to curb fossil fuel emissions—is reshaping the global energy landscape. Despite several years of relatively high prices, upstream returns had been low, both by historical standards and relative to the cost of capital. And it has been difficult for the majors to maintain, let alone grow, production or replenish reserves. Nor can we rely on high prices. Furthermore, research indicates a major shift in how capital markets value oil and gas companies, with multiyear income, cash flow, and operational measures (including reserves) playing a much more important role in stock prices.11,12

Evolving Global Resource Base

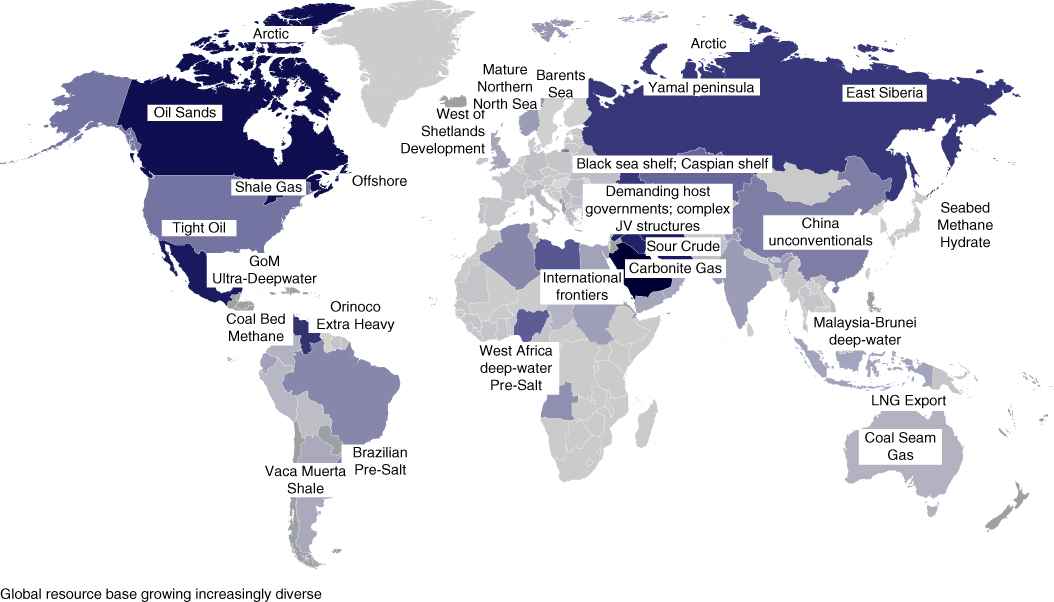

Enterprise operating models require a much broader set of key capabilities, some new, to accommodate our evolving understanding of the global resource base (see Figure 1.3). Furthermore, the replacement challenge facing the industry is formidable—the world needs ∼60 million barrels per day of new production by 2040 to offset declining fields and net demand growth. This must be sourced from an increasingly diverse, and expensive, resource base amidst choices between enhanced recovery from mature fields, new frontiers, deep‐water and ultra‐deep‐water, unconventional resources such as tight oil, shale gas, oil sands, and coal bed methane, and emerging but largely unproven sources, like the arctic, seabed methane hydrate, and carbonite reservoirs.13 The industry is pursuing higher‐cost resources, more technical/lower quality reservoirs, heavy oil, or harder to commercialize gas, and with more above‐ground risk.

Figure 1.3 World Resource Plays

Source: IHS Energy

Disruption from the “Ripple Effect” of Unconventionals

Rapid growth in US onshore unconventional liquids production and high levels of natural gas production (despite falling rig count and new well spuds) have contributed to keeping liquids, gas, power, and industrial feedstock prices low. This has fueled disruptive change throughout the economy and altered the competitive landscape for refiners, petrochemicals companies, and energy infrastructure. In the upstream, shorter cycle times and very different subsurface risk and cash flow profiles have challenged strategies with disruptive impact along several dimensions:

- Increased short‐cycle supply, reduced prices, increased price volatility, and challenged the role of OPEC; there was a westward migration in the balance of power and a reorientation of crude and product flows and trade patterns.

- Shifted capital inflows toward US onshore; private capital dove headfirst into the upstream sector; many exploration and production (E&P) companies created separate organizations for unconventionals investment and/or operation.

- Provided operational blueprint for developing lower permeability oil and gas reservoirs internationally.

- Challenges to pricing mechanisms, market liquidity, and competitiveness of global gas/LNG projects.

- Increased cost‐competitiveness of US petrochemicals; capacity shifted away from foreign naphtha‐based markets toward US ethane‐based conversion capacity and downstream manufacturing.

- Reduced US carbon footprint and increased cost‐competitiveness of US power‐intensive industry; there was more displacement of coal‐fired (and even some nuclear) power generation.

Discovery Challenges

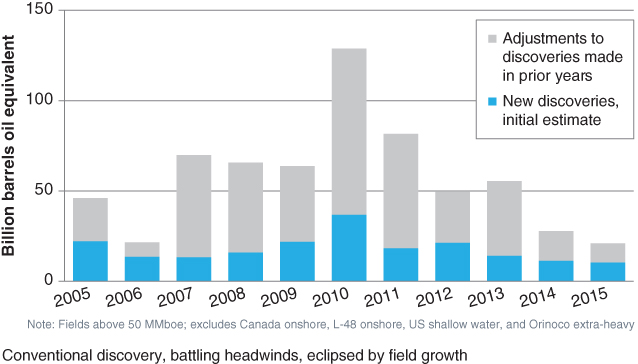

The challenges of our evolving resource base are accentuated by a decline in conventional exploration—conventional oil and gas exploration is yielding lower volumes of higher‐cost, lower‐value reservoirs. We are replacing cheaper, high‐quality barrels with high‐cost/lower‐quality barrels (see Figure 1.4). Accounting for the rise of unconventionals—a relatively high‐cost resource—only makes this picture worse.

Figure 1.4 Conventional Oil and Gas Discoveries and Field Growth, by Year

Source: IHS Energy

The year 2015 marked the lowest point for conventional oil and gas discovery in many years—the absolute number of wells drilled generally has not been in decline as much as the volumes being discovered—a smaller number of large fields. Nor have there been many billion‐barrel discoveries—the Piri gas field in Tanzania was 1.9 Tcf (i.e., 318 million boe), accounting for 16 percent of total volumes. A growing proportion of discoveries are in the higher‐cost deep‐water (i.e., 1000 to 5000 ft) and ultra‐deep‐water (i.e., >5000 ft); discoveries in shallow water (i.e., <1000 ft) and onshore are in decline. And more gas than oil is being discovered, which are lower economic value resources.

The rise of unconventionals, plus successful openings in places like Mexico and Iran, bring great promise but do not address all of our replacement needs. Nor will growth in renewables. The global resource potential remains enormous but appraisal and development is costly and technologically complex. Many new plays still require economically viable fiscal terms, operating structures, and costs. We must replace “cheap barrels” in the context of an evolving and increasingly expensive resource base, disappointing conventional exploration results, project delays, and rising costs and capital intensity.

One bright spot has been the offsetting effect of “field growth”—upward adjustments made to the volumetric resource estimates of prior year discoveries—which now often exceeds new discoveries. Roughly 2000 conventional fields have their technical resources revised upward every year based on factors such as more/better data, de‐risking milestones, and enhanced interpretation. Therefore, some companies might opt to focus on existing basins and fields over traditional frontier exploration in order to reduce costs and mitigate declining exploration success rates. Others might opt to focus on unconventionals, which carry a very different subsurface risk (and cost) profile than conventional frontier exploration.

Fading Production

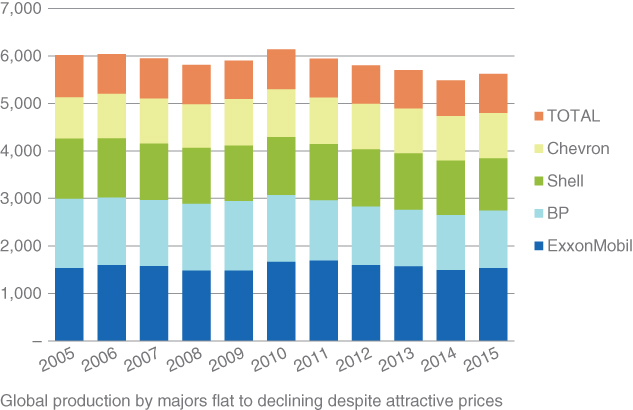

Upstream operating cash flow is both inadequate and in decline. Despite a period of high prices, returns in the upstream oil and gas sector were already down (i.e., both relative to historical returns on capital and relative to the cost of capital) well before the 2014 collapse in oil prices. Moreover, as illustrated in Figure 1.5, major producers struggled to grow their production (and to replenish reserves). Production is fading, operating margins have shrunk, the supply chain of services companies has telegraphed that its prices must rise, and the amount of invested capital has soared.

Figure 1.5 Worldwide Oil and Gas Production by Majors (MM boe)

Source: IHS Energy

Many large NOCs, such as Mexico's PEMEX and Venezuela's PDVSA, also face fading production. Over the past 10 years PEMEX's total annual production of gas and liquids declined 35 percent, from 1580 million barrels of oil equivalent (MM boe) in 2006 to only 1159 million boe in 2015. Host governments and state‐owned national oil companies had grown reliant in their expectations for high returns and a steady stream of cash flow from royalties or dividends to fund public programs and other state initiatives. The oil and gas sector had become the proverbial cash cow.

But with fading production and massive investment requirements, host governments and national oil companies must take action. For example, liquids production from PDVSA has gone from 3.3 million barrels per day in 2008 (the year before the nationalization of its oil service companies) to only 2.7 million barrels per day (bpd) in 2015, an 18 percent decline. Venezuela's Maracaibo‐Falcon basin declined 35 percent from producing 1 million bpd in 2008 to 0.7 million bpd in 2015. Production from the enormous El Furrial field declined an extraordinary 51 percent in seven years from 408,000 bpd in 2008 to just 198,000 bpd in 2015. While production does typically decline in mature fields, this rate of decline is unusually severe.

Costs and Capital Efficiency

Most of the world's conventional fields are “mature” and the operational complexities of mature fields grow over time—this puts pressure on costs. We also see cost escalation driven by a rising tide of local content requirements, falling yard productivity (e.g., more rework), and in some cases, other factors such as regulatory requirements and higher complexity.

The case of UK offshore operators is not unusual—they experienced more than a threefold increase in development costs on a per barrel of oil equivalent (boe) over 10 years, while unit operating costs rose nearly fourfold. Meanwhile, production efficiency—how much is actually produced from production facilities compared to what would be produced if they operate without problems—has dropped over the same period from around 80 percent to less than 70 percent.14 The industry was able to withstand this decline in productivity and escalation in costs because oil prices nearly tripled over the same period. But now the economics of North Sea production are very challenging, with negative free cash flow in some fields, and often reliant on the benefits of a large installed base of infrastructure.

Project delays and overruns have damaged IOC reputations for operational excellence, and much of this comes from the way IOCs have managed uncertainty as projects have become more complex. The real project cost baselines and their uncertainties and risks are neither well estimated nor well managed. In the United Kingdom, five large projects accounted for about 30 percent of total spend, while smaller fields accounted for the rest. As field sizes become smaller, unit costs rise. Oil & Gas UK cited the average unit development cost for fields under consideration at £13.50/boe ($21.75), up from £4.00/boe ($6.44) on an inflation‐adjusted basis from 10 years earlier; the average unit operating cost year was £17.00/boe ($27.39), up from £4.50/boe ($7.25) 10 years earlier.15 As the unit cost rises, the economic life of many fields is shortened; more reserves are stranded as infrastructure is decommissioned earlier.

Technology and Expertise

Enterprise operating models now require a much wider set of critical capabilities to accommodate the growth and evolution of the industry's requisite capabilities—combinations of assets, technology, and expertise. For example, recent industry‐changing innovations include deep‐water and ultra‐deep‐water technologies, production technologies in the oil sands, 3D seismic acquisition and data processing, rotary steerable drilling, geo‐steering with logging‐while‐drilling, horizontal drilling coupled with multistage hydraulic fracturing, and a host of completions techniques for unconventionals involving greater use of water, proppant, and pressure (aka superfrac), longer laterals and more stages, sequencing variations (e.g., zipper frac), different proppants (e.g., ceramic), and more. Greater capabilities are required to enhance primary and tertiary recovery in shale gas and tight oil. Artificial lift for horizontal wells is an evolving science, and recovery is also managed through reservoir contact, in‐fill drilling, trade‐offs between lateral length frac height, stage spacing, and downspacing, and opportunities for refracturing.

Supply Chain and Services

Enterprise operating models also might be reoptimized to acknowledge the massive growth and evolution of the upstream supply chain for outsourced services—its size, potential roles, and available capabilities. The upstream supply chain has transformed the industry through functional and geographical unbundling. One fundamental trade‐off in this fractionalization is between the gains of capabilities specialization (and their utilization), versus the costs of coordination and oversight. Growth in the externalization of services has enabled greater utilization of specialized capabilities—combinations of assets, technology, and expertise—in novel ways. The future of the supply chain will be influenced by: (1) improvements in coordination technology that lower the cost of functional and geographical unbundling, (2) improvements in production technology that affect the benefits of specialization, (3) narrowing of wage gaps that reduces the benefit of offshoring, and (4) the price of oil.16

Fiscal and Regulatory Terms

We have seen a significant evolution in the structure, calibration, and fluidity of host government fiscal and regulatory regimes for natural resources, with immediate implications for enterprise operating models. Government receipts may include royalties, local and state taxes, corporate and special taxes, and direct participation or participation through an NOC. One result of all the competing objectives for fiscal and regulatory terms is that this has become an increasingly complex and specialized area, demanding specialized expertise both to navigate strategic choices and also to influence the competitive landscape.

Fiscal regime types fall into two broad categories: (1) concessions, which involve royalties and taxes (R/T), and (2) contracts, such as production sharing contracts (PSCs) or service contracts (SCs). However, some R/T regimes are based on contracts, and some SCs look very much like PSCs. R/T structures prevail in much of the Americas, Western Europe, and Australia. PSCs prevail in much of Africa and Asia. SCs prevail in Mexico, Saudi Arabia, and Iran. Structures in Algeria, Iraq, Russia, and Kazakhstan might be described as a mix. Norway has long held an R/T regime that captures a relatively high take in terms of its economic rent from the oil and gas sector while other advanced, industrialized states with R/T regimes capture less.17 Malaysia and Indonesia are two of many countries that have adopted PSC structures within the last 30 decades. However, the Indonesian fiscal regime tends to be less investor‐friendly than Malaysia, which attracts much more foreign investment in its oil and gas sector. After a disappointing bid round in 2009, Indonesia proposed changes to its fiscal and regulatory regime in 2010 to attract more investment.18

Neither R/T nor PSC regimes necessarily dictate a high or low government take, but PSCs tend to be more progressive, and progressive terms are especially important in a low‐price environment—progressive structures are those that vary with prices or profits, such as taxes and profit sharing. Regressive structures are those that are fixed and not linked to prices or profitability, such as royalties, export duties, and domestic market obligations (DMOs). Fiscal regimes (and resource bid rounds) seek to strike a balance between encouraging direct investment and the need for an attractive and politically saleable government take, and a growing interest in methods to promote local economic development.19 Similarly, regulatory frameworks seek to increase innovation and competition while also ensuring safety and environmental concerns, but must avoid becoming overly burdensome or expensive.

Social License and Environmental Costs

Upstream companies today require an enterprise operating model that involves a much greater investment in capabilities that support and promote their social license to operate than ever before. Regardless of one's views on climate change and the host of other environmental issues and concerns that can affect the industry, the inarguable truth is that environmental issues have grown to become an extraordinary force for the E&P sector, manifesting in an extremely wide range of business costs and challenges. These include increased capital expenditures and higher operating costs to meet the rise of regulatory requirements, major project delays, and lower wellhead prices due to constraints in take‐away capacity, restricted access to federal lands and waters, and outright bans on some practices such as hydraulic fracturing or working in certain environmentally protected areas. One study by the Fraser Institute estimates that delays in pipeline projects cost several billion dollars per year.20 Barriers to building pipelines that restrict Canadian take‐away capacity result in prices that are 20 to 30 percent below Brent, costing Canada's economy and governments billions in forgone revenues. “Without adequate pipelines to Canada's coasts, Canadian oil producers are forced to sell their products at dramatically discounted prices,” said Kenneth Green, senior director of Natural Resource Studies at the Fraser Institute and co‐author of The Costs of Pipeline Obstructionism.21

Weak Oil and Gas Prices

Under even the most optimistic outlook for oil and gas prices over the next several years, upstream oil and gas companies need a new low‐cost operating model now more than ever. North American natural gas prices had been low since 2009, under surging supply from the boom in domestic shale gas production. But now we see the same story playing out in global liquids, from US tight oil production as well as both OPEC and non‐OPEC production. According to Oil & Gas UK, even at $80, one‐third of the UK's offshore developments are uneconomic.22

E&P NEEDS A NEW AGENDA

The E&P context has changed and while on their own any one of these changes might be quite manageable, in aggregate, the change in context demands a bold new approach for a low‐cost operating model. The industry has experienced tremendous evolution in terms of our understanding of the underlying global resource base, the nature of its ownership and principal stakeholders, technologies and methods for resource development, and the economics and business models. Yet beyond incremental changes, we have not seen efforts to redesign and transform operating models on a systematic or enterprisewide basis.

The upstream has been focused on cost and productivity for several years and has made significant gains since the collapse in oil prices. However, operating cash flows remain generally insufficient to cover operating costs plus the needs for future investment, let alone provide an adequate return on the capital that is already employed. And many of the cost gains that have been made will not be sustainable over a full cycle. The “low‐hanging fruit” has been taken, but still there is much work to be done.

Operating models and operational excellence must now be on everyone's agenda—changes can yield profound cost savings and operating efficiencies. However, change is much easier to plan than to implement. Furthermore, operating model redesign is rarely executed on an organization‐wide basis (notable exceptions include post‐merger integration programs, large‐scale cost‐transformation programs, and other event‐driven programs that are charged with significant cost targets).

Operating model redesign is a time to cut costs while growing stronger—by investing in the most important capabilities, while leveraging the capabilities of others where it makes sense to do so. Operating model redesign is also a time to harness the entrepreneurial spirit of the talent pool—to align, empower, and enable employees to drive enterprise improvement, balancing between quick wins that build momentum and longer‐term efforts that require major change or investment.