CHAPTER EIGHT

MANAGING THE STRATEGY

DEVELOPMENT PROCESS

Don’t just tell me that the right strategy is crucial for success. How do I come up with a strategy that works? What process for formulating strategy is most likely to generate a strategy that will lead to success? Is it better to be the pioneer in an emerging market, or to be a follower once the market’s topography is clearer? When should we let innovations bubble up from within the company? When and why should we drive things from the top? Which aspects of strategy formulation do senior executives need to manage most closely?

Most questions about strategy that arise in building a new business concern the substance of the strategy. Managers are anxious that their strategy be the right one. There is an even more important strategy question, however, that most managers forget to ask—and it is the reason many ventures end up with flawed strategies. This crucial question relates to the process of strategy formulation that the venture’s management team will use to develop and implement a winning plan. Although executives are understandably obsessed with finding the right strategy, they can actually wield greater leverage by managing the process used to develop the strategy—by making sure that the right process is used in the right circumstances.

Innovative ideas always emerge in a half-baked, partially formed condition, as we have noted. They subsequently go through a shaping process that transforms them into the fully fleshed-out business plan, complete with strategy, that is required to win funding. This chapter describes two simultaneous but fundamentally different processes of strategy development, and presents a circumstance-based theory that indicates which of these processes management should rely on as the most reliable source of strategic insight at different stages of business development. It then describes the workings of the resource allocation process, which is the filter through which all strategic actions must flow in order to affect the company’s course. The chapter ends by describing some tools and concepts that executives can use to manage the ongoing processes of strategy formulation more effectively.

Two Processes of Strategy Formulation

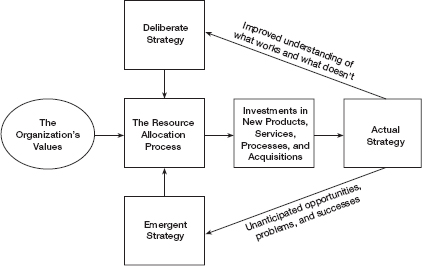

In every company there are two simultaneous processes through which strategy comes to be defined. Figure 8-1 suggests that both of these strategy-making processes—deliberate and emergent—are always operating in every company.1 The deliberate strategy-making process is conscious and analytical. It is often based on rigorous analysis of data on market growth, segment size, customer needs, competitors’ strengths and weaknesses, and technology trajectories. Strategy in this process typically is formulated in a project with a discrete beginning and end, and then implemented “top down.” We hope that the theories discussed in this book can help executives and their advisers devise even better deliberate strategies for creating and sustaining growth than have been possible through traditional methods of data analysis.

Deliberate strategies are the appropriate tool for organizing action if three conditions are met. First, the strategy must encompass and address correctly all of the important details required to succeed, and those responsible for implementation must understand each important detail in management’s deliberate strategy. Second, if the organization is to take collective action, the strategy needs to make as much sense to all employees as they view the world from their own context as it does to top management, so that they will all act appropriately and consistently. Finally, the collective intentions must be realized with little unanticipated influence from outside political, technological, or market forces. Because it is difficult to find a situation in which all three of these conditions apply, the emergent strategy-making process almost always alters the strategy that the company actually implements.2

FIGURE 8 - 1

The Process by Which Strategy Is Defined and Implemented

Emergent strategy, which as depicted in figure 8-1 bubbles up from within the organization, is the cumulative effect of day-to-day prioritization and investment decisions made by middle managers, engineers, salespeople, and financial staff. These tend to be tactical, day-to-day operating decisions that are made by people who are not in a visionary, futuristic, or strategic state of mind. For example, Sam Walton’s decision to build his second store in another small town near his first one in Arkansas for purposes of logistical and managerial efficiency, rather than building it in a large city, led to what became Wal-Mart’s brilliant strategy of building in small towns discount stores that were large enough to preempt competitors’ ability to enter. Emergent strategies result from managers’ responses to problems or opportunities that were unforeseen in the analysis and planning stages of the deliberate strategy-making process. When the efficacy of a strategy that was developed through an emergent process is recognized, it is possible to formalize it, improve it, and exploit it, thus transforming an emergent strategy into a deliberate one.

Emergent processes should dominate in circumstances in which the future is hard to read and in which it is not clear what the right strategy should be. This is almost always the case during the early phases of a company’s life. However, the need for emergent strategy arises whenever a change in circumstances portends that the formula that worked in the past may not be as effective in the future. On the other hand, the deliberate strategy process should be dominant once a winning strategy has become clear, because in those circumstances effective execution often spells the difference between success and failure.3

The Crucial Role of Resource Allocation

in the Strategy Development Process

Figure 8-1 charts the confluence of these deliberate and emergent decision-making processes in defining actual strategy. Ideas and initiatives, whether of deliberate or emergent origin, are filtered through the resource allocation process, as represented by the center-left box in the figure. The resource allocation process determines which of the deliberate and emergent initiatives get funded and implemented, and which are denied resources. Actual strategy is manifest only through the stream of new products, processes, services, and acquisitions to which resources are allocated.

The resource allocation process is typically complex and diffused, operating at every level and all the time. If the values that guide prioritization decisions in resource allocation are not carefully tied to the company’s deliberate strategy (and often they are not), then significant disparities can develop between a company’s deliberate strategy and its actual strategy. Actively monitoring, understanding, and controlling the criteria by which day-to-day resource allocation decisions are made at all levels of the organization are among the highest-impact challenges a manager can tackle in the strategy development process.

Initiatives that receive funding and other resources from the resource allocation process can be called strategic actions, as opposed to strategic intentions. Intel chairman Andrew Grove has counseled, “To understand companies’ actual strategies, pay attention to what they do, rather than what they say.” 4 In our parlance, this means that a company’s strategy is what comes out of the resource allocation process, not what goes into it.

As the company does these things, managers then confront and respond to unexpected crises and opportunities, and their experiences cycle back into the emergent process. As managers learn what works and what doesn’t in the competitive marketplace, their improved understanding flows back into the deliberate strategy process. Each resource allocation decision, no matter how slight, shapes what the company actually does. This creates a new set of opportunities and problems and generates new deliberate and emergent inputs into the process.

How does this critical resource allocation process work? It is powerfully driven by the values of the organization, which, as noted in chapter 7, are the criteria by which managers and employees make prioritization decisions. Most of the ideas for developing new products, services, and businesses bubble up from employees within the organization. Middle managers cannot carry all of these ideas up to senior management for approval and funding, however. The values or criteria that middle managers use to decide which ideas they will promote and which they will allow to languish play a crucial role in determining what comes out of the resource allocation process. We noted in chapter 1 that once middle managers decide an idea has merit, they engage with the innovators in a process of shaping the idea into a fully fleshed-out business plan that can win funding. The values that senior management employ in these funding decisions therefore exert an equally powerful influence on the types of ideas that can and cannot emerge from the resource allocation process.5

Two factors exert a particularly important influence on the values that guide resource allocation decisions. The first is the company’s cost structure, which determines the gross profit margins that it must earn to cover overhead costs and make a profit. Good managers have a very difficult time according priority in the resource allocation process to innovative proposals that will not maintain or improve the organization’s profit margins.6 The second factor is the size threshold that new opportunities must meet in order to get through the resource allocation filter. This threshold grows higher as a company becomes larger. Opportunities that were seen as energizing in a company’s resource allocation process when the company was small get filtered out as “not big enough to be interesting” in the larger company.

In addition to these powerful, direct determinants of the values that guide senior executives’ priorities in resource allocation, other criteria that are subtly embedded in diffused processes throughout the company influence what lower-level employees are able to prioritize. These combine to exert additional influence on which initiatives can pass through the resource allocation filter. An example of these factors is the short tenure in assignment that is typical in the career path of high-potential employees. Management development systems in most organizations move high-potential employees into new positions of responsibility every two to three years in order to help them master management skills in various parts of the business. This practice is critical in management development, but its effect is to influence midlevel managers to accord priority to projects that will pay off within the typical tenure that they expect in their jobs. They want to produce improved results that will merit attractive promotions.

Other factors are embedded within the sales force’s incentive compensation system. Salespeople’s decisions about which customers to focus on and which products to emphasize are critical elements of the diffused resource allocation process and are heavily influenced by how they are compensated. Customers also exert a powerful influence on the sorts of initiatives that survive the resource allocation process. You can’t build a business around a product that your customers don’t want, because the customers pay the bills. Although managers think that they control the resource allocation process, customers often exert even more powerful de facto control over how money can and cannot be spent. Competitors’ actions likewise exert powerful influence. When a competitor’s action threatens to steal customers or growth opportunities away, managers have almost no choice but to push a response through the resource allocation filter.

The resource allocation process, in other words, is a diffused, unruly, and often invisible process. Executives who hope to manage the strategy process effectively need to cultivate a subtle understanding of its workings, because strategy is determined by what comes out of the resource allocation process, not by the intentions and proposals that go into it.

An Illustration of Resource Allocation in

Strategy Making: The Case of Intel

Intel began as a manufacturer of semiconductor memories, and its founding engineers developed the world’s first commercially viable dynamic random access memory (DRAM) chips.7 In 1971 an Intel engineer serendipitously invented the microprocessor during a funded development project for a Japanese calculator company, Busicom. Although DRAMs continued to account for the lion’s share of company sales through the 1970s, Intel’s sales of microprocessors grew gradually in a host of small, emerging applications.

Every month Intel’s production schedulers met to allocate the available production capacity across their products, which ranged from DRAMs to EPROMs and microprocessors.8 The sales department would bring to this meeting its forecast shipments by product, and accounting would bring a rank ordering of those products by gross margins per wafer start. The highest-margin product would then be allocated the production capacity needed to meet its forecast shipments. The next-highest-margin product would then get the capacity it needed in order to meet its forecast shipments, and so on, until the product line with the lowest gross margins was allocated whatever residual capacity remained. Gross margins per wafer start, in other words, constituted the values of the organization that were used in this critical resource allocation decision.

Japanese DRAM makers attacked the U.S. market in the early 1980s, causing pricing levels to drop precipitously and relegating DRAMs to the lowest ranking by gross margin of Intel’s products. Because there was less intense competition, microprocessors consistently earned among the most attractive gross margins in Intel’s product portfolio. The resource allocation process therefore systematically diverted manufacturing capacity away from DRAMs and into microprocessors. This occurred without any explicit management decision to change strategy. Senior management, in fact, continued to invest two-thirds of R&D dollars into the DRAM business even as the resource allocation process was executing a systematic exit from DRAMs.9

Finally, by 1984, when the company had plunged into financial crisis and DRAMs had contracted to just a fraction of Intel’s volume, senior management recognized that Intel had become a microprocessor company. They stopped DRAM R&D spending, and Gordon Moore and Andy Grove made their storied exit through the company’s revolving lobby door as managers of the old company, and reentered as managers of the new company.10 But it was the resource allocation process that transformed Intel from a DRAM company into a microprocessor company. Intel’s remarkable strategy shift was not the result of an intended strategy articulated within the executive ranks; rather, it emerged through the daily decisions made by middle managers as they allocated resources.11

Once this new business opportunity had become clear, then it was time to manage strategy in an assertive, deliberate mode—which Intel management did masterfully. By keeping a strong and sometimes ruthless hand on the resource allocation filter, management screened out bubbling-up initiatives that did not directly support the microprocessor business. Both strategy processes were crucial. A viable strategic direction had to coalesce from the emergent side of the process, because nobody could foresee clearly enough the future of microprocessor-based desktop computers. But once the winning strategy became apparent, it was just as critical to Intel’s ultimate success that the senior management then seized control of the resource allocation process and deliberately drove the strategy from the top.

Match the Strategy-Making Process to

the Stage of Business Development

Intel’s history illustrates that strategies rarely follow a simple sequence from formulation to implementation. Furthermore, strategy is never static. Most companies must at the outset chart their course in a deliberate direction because they need to start going somewhere. We hope that the theories in this book will help those who create new businesses to deliberately target a viable strategy with much more accuracy than was possible in the past. But even with this guidance, there will be much to be discovered.

Research suggests that in over 90 percent of all successful new businesses, historically, the strategy that the founders had deliberately decided to pursue was not the strategy that ultimately led to the business’s success.12 Entrepreneurs rarely get their strategies exactly right the first time. The successful ones make it because they have money left over to try again after they learn that their initial strategy was flawed, whereas the failed ones typically have spent their resources implementing a deliberate strategy before its viability could be known. One of the most important roles of senior management during a venture’s early years is to learn from emergent sources what is working and what is not, and then to cycle that learning back into the process through the deliberate channel. As Mintzberg and Waters advise, “Openness to emergent strategy enables management to act before everything is fully understood—to respond to an evolving reality rather than having to focus on a stable fantasy. . . . Emergent strategy itself implies learning what works—taking one action at a time in a search for that viable pattern or consistency.” 13

Effective managers eventually recognize the viable pattern that constitutes a successful strategy. At this point, with a firm hand on the criteria used as filters in the resource allocation process, managers need to make strategy formulation much more deliberate. Rather than continuing to feel their way into the marketplace, they need to boldly execute the strategy that they have learned will work. Intel, Wal-Mart, and a host of other companies each saw a viable strategy emerge that was substantially different than their founders had envisioned. But once the model was clear, they executed that strategy aggressively.

Managing Two Fundamentally Different

Strategy Processes: A Rare and Tricky Skill

In most waves of disruptive growth, a host of competitors are drawn to the opportunity. Firms that do not emerge from the pack as leaders fail in one of two places. First, many of the initial entrants fail because they spend their money aggressively implementing a deliberate strategy in the nascent stages when the right strategy cannot be known. The second point of failure occurs after the market and its applications become clear to the firms that have managed the emergent strategy process most effectively. The firms that then get left in the dust are those whose executives do not seize deliberate control of resource allocation and focus all investments in executing the race up-market.

The switch from an emergent to a deliberate strategy mode is crucial to success in a corporation’s initial disruptive business. But the CEO’s job in managing this process does not end there, because the deliberate strategy process often becomes a subsequent impediment to a company’s efforts to launch new waves of successful disruptive growth. This happens in two ways. First, the filters in the resource allocation process of successful companies become so well attuned to the successful strategy that they filter out all but the initiatives that sustain the existing business—causing them to ignore the disruptive innovations that create the next waves of growth. Just as important, once deliberate strategy processes have become embedded within organizations, they find it difficult to employ emergent processes again when launching new businesses.

A company’s efforts to catch new waves of disruptive growth need to be guided through emergent processes. Simultaneously, however, because the corporation’s established businesses typically have many years of profitability remaining even while the disruptive new-growth business is getting underway, the mainstream business needs to be driven by deliberate strategy processes to guide the sustaining innovations that will keep it competitive and profitable.

In our studies we have found a good number of companies whose executives have perceived the need to allocate resources to create new disruptive growth businesses before it is too late. But very, very rarely have we seen executives who have consistently demonstrated the ability to manage the strategy development process appropriately across a range of businesses in various stages of maturity. After they have entered a deliberate strategy mode they find it very difficult to let new businesses be guided through an emergent process.

For example, Prodigy Communications, a joint venture between Sears and IBM, was a pioneer in online services in the early 1990s. The managers of Sears and IBM were extraordinarily bold in resource allocation: They invested over a billion dollars in what was a very uncertain, potentially disruptive innovation. But they weren’t as successful in managing the strategy process—in helping Prodigy define a viable strategy through emergent processes even while the parent companies were managing their mainstream businesses deliberately.

Prodigy’s original business plan envisioned that consumers would use online services primarily to access information and make online purchases. In 1992, management realized that Prodigy’s two million subscribers were spending more time sending e-mail than downloading information or making purchases online. The architecture of Prodigy’s computer and communications infrastructure had been designed to optimize transactions processing and information delivery, and Prodigy consequently began charging extra fees to subscribers who sent more than thirty e-mail messages per month. Rather than seeing e-mail as an emergent strategy signal, the company tried to filter it out, because in a deliberate mode, management’s job was to implement the original strategy.

America Online (AOL) luckily entered the market later, after customers had discovered that e-mail was a primary reason for subscribing to an online service. With a technology infrastructure tailored to messaging and its “You’ve got mail” signature, AOL became much more successful.

In light of our model, Prodigy’s mistake was not that it entered the market early. Nor was it a mistake that management targeted online information retrieval and shopping as the primary attraction of an online service. Nobody could know at the outset precisely how online services would be used.14 The executives’ mistake was to employ a deliberate strategy process before the strategy’s viability could be known. Had Prodigy kept strategic and technological flexibility to respond to emergent strategic evidence, the company could have had a huge lead over AOL and CompuServe (the third major online service provider). A similar challenge confronted the set of companies that responded in the early 1990s to the widely held view that a large market for handheld personal digital assistants was about to emerge. Many of the leading computer makers—including NCR, Apple, Motorola, IBM, and Hewlett-Packard—targeted this market, along with a few start-up firms such as Palm. All sensed that the market wanted a handheld computing device. Apple was one of the most aggressive of the innovators in this space. Its Newton cost $350 million to develop because of the technologies, such as handwriting recognition, that were required to build as much functionality into the product as possible. Hewlett-Packard also invested aggressively to design and build its tiny Kittyhawk disk drive for this market.

In the end, the products just weren’t good enough to be a substitute for notebook computers, and each of the companies scrapped its effort—except Palm. Palm’s original strategy was to provide an operating system for these personal digital assistants.15 When its customers’ strategies failed, Palm searched around for another application and came up with the concept of an electronic personal organizer.

What were the strategic mistakes here? The computer companies employed deliberate strategy processes from the beginning to the end. They invested massively to implement their strategies, and then wrote the projects off when the strategies proved wrong. Palm was the only firm that shifted to an emergent strategy process when its original deliberate strategy failed. When a viable strategy emerged, Palm shifted back toward a deliberate process as it migrated up-market.

Clearly, this is not simple stuff.

Points of Executive Leverage in the Strategy-Making Process

The resource allocation process is the filter through which all strategic actions must flow. Because it is so complex and diffused throughout a company, it is rare that senior executives can simply devise a new strategy and “implement” it. Rather, defining and implementing strategy entails managing the conditions under which the strategy and resource allocation processes operate so that the strategy process can work efficiently, given the circumstances that each of the company’s organizations is in. Effective, appropriate processes will generate the needed strategic insights. The remainder of this chapter focuses on three points of executive leverage on the strategy process. Managers must:

- Carefully control the initial cost structure of a new-growth business, because this quickly will determine the values that will drive the critical resource allocation decisions in that business.

- Actively accelerate the process by which a viable strategy emerges by ensuring that business plans are designed to test and confirm critical assumptions using tools such as discovery-driven planning.

- Personally and repeatedly intervene, business by business, exercising judgment about whether the circumstance is such that the business needs to follow an emergent or deliberate strategy-making process. CEOs must not leave the choice about strategy process to policy, habit, or culture.

Create a Cost Structure that Finds the Right Customers Attractive

Note that we didn’t identify “memos from the executive office” as a way of influencing the organization’s values. That is because the power of a venture’s cost structure overwhelms “being strategically important” as a criterion that drives resource allocation decisions.16 Executives must pay very careful initial attention to creating a cost structure and business model within which orders from the kinds of ideal customers we described in chapter 4 will appear to be profitable. Otherwise, it will be impossible to build a business with those customers as a foundation.17

Let us illustrate by bringing things close to home, recounting Clayton Christensen’s own experience in running a venture capital–backed company that he founded with several MIT professors in the early 1980s, before he retreated to academia. The company was formed to exploit exciting technology to make products with a class of remarkable materials called advanced ceramics, and the history is recounted in a set of cases under the disguised name Materials Technology Corporation (MTC).18

MTC’s strategy was to become a major manufacturer of products made from these advanced ceramic materials. Because the materials business is capital intensive, Christensen and his colleagues knew from the beginning that MTC would need lots of capital to carry the company to break-even—they estimated about $60 million. In the early 1980s this was a lot of money to raise. What drove the amount needed was not just the cost of the physical facilities, but also the length of the product development cycle. Because of MTC’s position at the beginning of the value chain, it needed to win contracts to develop new components for its customers, who would then use those advanced components to make next-generation products of their own. Developing and testing the components easily took one to two years. When MTC succeeded, then and only then could the customers initiate their own cycle to design and test the new products that MTC’s advanced materials had enabled. The customers’ development processes typically took two to four additional years. In other words, MTC’s strategy entailed enduring a lot of expense before the revenue could begin rolling in.19

Christensen decided to cover the cost of MTC’s research and development staff by negotiating multimillion dollar joint development contracts from major corporate partners, in much the same way that many biotechnology companies have funded their protracted development processes. When MTC sold a major development contract to create the technology required to manufacture the products that its strategy envisioned, it then had to hire the scientists and engineers to do the work.

The strategy worked well for a couple of years. Then MTC’s first major development contract was completed, and the funding that had covered the salaries of three Ph.D. scientists and five engineers came to an end. Given the slow ramp to volume production inherent in MTC’s product development cycle, how could the company cover their salaries? These were some of the best materials scientists in the world, and they just couldn’t be sent packing. So the company had to sell another development contract to whomever would pay MTC enough money to cover their salaries and overhead. When the next funded project reached its end, the firm had to sell another funded program to cover the company’s high fixed costs, and so on. The company started with a strategy to be a volume product manufacturer. But very quickly and without intention, management began implementing a strategy to become a contract research house. There just wasn’t any way that the gross margins generated by initial volumes of manufactured products could cover the overheads that had to be put in place to deliver what MTC sold to its first customers.

MTC’s long development cycle and huge funding need represent an extreme example, but every new corporate venture experiences its own version of this challenge. It is the habit of large, established companies to ramp up expenses ahead of revenues, because in a world of deliberate strategy and sustaining innovation, these are safe bets. But these outlays define a cost structure very quickly, and before you know it you’ve got yourself a business model that defines the kind of business that does or does not look attractive. Ultimately MTC did become a manufacturing company, but only through wrenching layoffs and by restructuring the nature of its costs. It was only by creating a new cost structure that a new type of customer order could appear to be attractive and could thereby be accorded priority in resource allocation.

This example illustrates why executives need to pay careful attention to getting the initial conditions right. The only way that a new venture’s managers can compete against nonconsumption with a simple product is to put in place a cost structure that makes such customers and products financially attractive. Minimizing major cost commitments enables a venture to enthusiastically pursue the small orders that are the initial lifeblood of disruptive businesses in their emergent years.

Accelerating the Emergent Strategy Process

Executives whose ventures are in a discovery mode need not passively watch what evolves in the emergent strategy process. They can employ a rigorous method called discovery-driven planning to help a viable strategy emerge much more quickly and purposefully than is likely to happen through less-structured trial and error.20

Most deliberate strategic planning processes go through four steps, as suggested in table 8-1. First, innovators make assumptions about the future and about the success that a new business idea will enjoy. These assumptions might be grounded in good predictive theory, but often they are grounded in the way things worked in the past. In the second step, the innovators make financial projections based on those assumptions, and third, senior executives approve the proposal based on the financial projections. Fourth, the team responsible for the new venture goes off to implement the strategy. There frequently is a loop from the second step back to the first in this deliberate process. Because the innovators and middle managers typically know how good the numbers have to look in order for the proposal to get funded, they often will cycle back and revise the assumptions that they are making in order to make the numbers work.

This process does not work badly in a world of sustaining improvements and deliberate strategy. But when it is used for decision making in the emergent world of disruption, this process causes bad decisions to be made because the assumptions upon which the projections and decisions are built often prove wrong.

Discovery-driven planning is a way to actively manage the emergent strategy process. As depicted in table 8-1, it involves reordering the four steps. The first step is to make the financial projections—the targeted or required financial performance of the venture. The logic behind this is quite compelling. If everybody knows how good the numbers must look in order to win funding, why go through the cyclical charade of making and revising assumptions in order to make the numbers look good enough? The required income statement and return on investment should just be the standard first slide in every presentation. The second step, where the real work begins, is to compile an assumptions checklist. It answers the question, “We all know how good the numbers need to be. So what assumptions need to prove true in order for us to realistically expect that these numbers will materialize?” The assumptions on this list should be rank-ordered from most to least crucial. The list must include assumptions related to each of the theories in this book: that low-end or new-market disruptions are possible, that the targeted customers will use the new product for the jobs they are trying to get done, that the new venture will lead the company to the point in the value chain where the money will be in the future, and so on.

TABLE 8 - 1

| A Discovery-Driven Method for Managing the Emergent Strategy Process | |

| Sustaining Innovations: Deliberate Planning |

Disruptive Innovations: Discovery-Driven Planning |

| (Note: decisions to initiate these projects can be grounded on numbers and rules.) | (Note: decisions to initiate these projects should be based on pattern recognition.) |

| 1. Make assumptions about the future. | 1. Make the targeted financial projections. |

| 2. Define a strategy based on those assumptions, and build financial projections based on that strategy. |

2. What assumptions must prove true in order for these projections to materialize? |

| 3. Make decisions to invest based on those financial projections. | 3. Implement a plan to learn—to test whether the critical assumptions are reasonable. |

| 4. Implement the strategy in order to achieve the projected financial results. | 4. Invest to implement the strategy. |

The third and fourth steps in discovery-driven planning also reverse the order of the deliberate strategy process. The third step is to implement a plan. This is not a deliberate strategic plan, but rather a plan to test the validity of the most important assumptions. This plan needs to generate quickly, and with as little expense as possible, validating or invalidating information about the most critical assumptions. This enables innovators to revise the strategy prior to the fourth step—the decision to implement through significant investment. This can be done after the viability of various assumptions becomes more evident.

Innovators who are using the discovery-driven process frequently learn quite early that there just isn’t a reasonable set of assumptions to support a plan that will achieve the numbers the organization requires. This might imply that the idea simply can’t be shaped into a viable strategy at all. Or it might mean that the idea needs to be placed within a smaller business unit, whose values might not demand that it get prohibitively big prohibitively fast.

Managing the Mix of Emergent and Deliberate Strategies

Many processes in an organization can become so refined and effective that they simply keep chugging along with little top-management attention, freeing managers to worry about more nonstandard dimensions of the business. It is dangerous, however, to allow the strategy development process to operate on autopilot. At any given point in time, some businesses under a manager’s care may need to be managed through aggressive, deliberate strategy processes, while others need emergent processes.

Executives cannot twist an on/off valve to start and stop the flow of opportunities and problems from deliberate and emergent directions. These are always flowing in, and the CEO’s job is to manage constantly which direction should predominantly influence strategic thinking. The valve, which is the resource allocation process, can get really sticky—which is why CEOs need to keep their hands on the control constantly and consciously. When a viable strategy has emerged and it is time for execution, the CEO needs aggressively to switch to a deliberate strategy mode and stop funding emergent opportunities that might divert the company from its focus on the winning plan.

Once this has been done, however, executives often suffer amnesia and selectively remember only their success in deliberately implementing the successful strategy. They lose memory of the emergent process through which the successful strategy was discovered, and therefore forget to reset the strategy process to an emergent mode in those new organizations that are attempting to build the next growth businesses. Nearly all companies, as a result, employ one-size-fits-all deliberate strategy systems. This is a very common reason why new ventures launched by corporations and by many venture capital firms fail.21 Managing the strategy process in ways that are appropriate to the circumstance can greatly improve the odds that a venture can succeed.

Simply seeking to have the right strategy doesn’t go deep enough. The key is to manage the process by which strategy is developed. Strategic initiatives enter the resource allocation process from two sources—deliberate and emergent. In circumstances of sustaining innovation and certain low-end disruptions, the competitive landscape is clear enough that strategy can be deliberately conceived and implemented. In the nascent stages of a new-market disruption, however, it is almost impossible to get the details of strategy right. Rather than executing a strategy, managers in this circumstance need to implement a process through which a viable strategy can emerge.

There are three points of executive leverage in strategy making. The first is to manage the cost structure, or values of the organization, so that orders of disruptive products from ideal customers can be prioritized. The second is discovery-driven planning—a disciplined process that accelerates learning what will and won’t work. The third is to vigilantly ensure that deliberate and emergent strategy processes are being followed in the appropriate circumstances for each business in the corporation. This is a challenge that few executives have mastered, and is one of the most important contributors to innovative failure in established companies.

Notes

1. The notion that these two different processes coexist was articulated by Henry Mintzberg and James Waters in their classic paper “Of Strategies, Deliberate and Emergent,” Strategic Management Journal 6 (1985): 257. Stanford Professor Robert Burgelman is probably the preeminent scholar in this field, and many of his papers are cited in this chapter. Two important papers of his are “Intraorganizational Ecology of Strategy Making and Organizational Adaptation: Theory and Field Research,” Organization Science 2, no. 3 (August 1991): 239–262; and “Strategy as Vector and the Inertia of Coevolutionary Lock-in,” Administrative Science Quarterly 47 (2002): 325–357. Burgelman’s recent book, Strategy Is Destiny (New York: Free Press, 2002), summarizes many of his findings. Professors Rita McGrath and Ian MacMillan of the Columbia and Wharton Business Schools, respectively, have also studied these issues. We have found their article “Discovery-Driven Planning” (Harvard Business Review, July–August 1995) to be particularly helpful in understanding what processes of strategy development are appropriate in what circumstances. Finally, we have also drawn heavily on the work of Professor Amar Bhide, The Origin and Evolution of New Business (Oxford and New York: Oxford University Press, 2000).

2. Mintzberg and Waters, “Of Strategies,” 258.

3. This, too, is a departure from the traditional approach to thinking about the “right” way to set strategy. Typically, business scholars have adopted an “either-or” approach to the process of strategy formulation, as (in)famously demonstrated in the highly visible arm wrestle between Henry Mintzberg (“bottom-up”) and Igor Ansoff (“top-down”) in the pages of the Strategic Management Journal (vol. 11, 1990, and vol. 12, 1991).

4. Andrew Grove, Only the Paranoid Survive (New York: Doubleday, 1996), 146.

5. Professors Joseph L. Bower of the Harvard Business School and Robert Burgelman of Stanford are the leading scholars who have described how resources get allocated across competing alternative investments at all levels of the organization. See Joseph L. Bower, Managing the Resource Allocation Process (Boston: Harvard Business School Press, 1970); and Robert A. Burgelman and Leonard Sayles, Inside Corporate Innovation (New York: Free Press, 1986).

6. The effect that such a filtering mechanism can have on a company’s strategy possibilities can be profound. 3M Corporation, for example, is one of the most innovative companies in modern history, in terms of its abilities to apply its core technological platforms to an array of market applications. Its insistence that all new products meet relatively high gross margin targets, however, has focused the company on a vast array of small, premium product niches and has prevented all but a few of its new products from becoming large mass-market businesses.

7. This history has been chronicled in Robert A. Burgelman, “Fading Memories: A Process Study of Strategic Business Exit in Dynamic Environments,” Administrative Science Quarterly 29 (1994): 24–56; and in Grove, Only the Paranoid Survive.

8. EPROMs are erasable, programmable, read-only memory circuits. Like its microprocessors, Intel’s EPROM product line also resulted from the emergent, rather than deliberate, process. See Burgelman, “Fading Memories.”

9. There were strong reasons why senior management continued to invest in DRAMs. For example, management believed that DRAMs were the “technology driver” and that remaining competitive in DRAMs was essential in order to be competitive in other product lines.

10. Grove, Only the Paranoid Survive.

11. Microprocessors were a new-market disruptive technology in that they brought logic to applications where it previously had not been feasible, given the size and cost of the large printed wiring board logic circuitry that was used in the mainframe computers and minicomputers of the day. Relative to Intel’s business model, however, microprocessors were a sustaining innovation. The product helped Intel make more money in the way that it was structured to make money, and therefore resources were readily allocated to it. This illustrates a very important principle—that disruptiveness can only be expressed relative to the business model of a company and its competitors.

12. Strong evidence for this is discussed in Amar Bhide, The Origin and Evolution of New Businesses (New York: Oxford University Press, 2000).

13. Mintzberg and Waters, “Of Strategies,” 271.

14. In a number of speeches and articles, Dr. John Seeley Brown has made this point—that it is very hard to predict in advance how people will end up using the disruptive technologies that change the way we live and work. We recommend all of Dr. Brown’s writings to our readers. He has influenced our own thinking in profound ways. See, for example, J. S. Brown, ed., Seeing Differently: Insights on Innovation (Boston: Harvard Business School Publishing, 1997); J. S. Brown, “Changing the Game of Corporate Research: Learning to Thrive in the Fog of Reality,” in Technological Innovation: Oversights and Foresights, eds. Raghu Garud, Praveen Rattan Nayyar, and Zur Baruch Shapira (New York: Cambridge University Press, 1997), 95–110; and J. S. Brown and Paul Duguid, The Social Life of Information (Boston: Harvard Business School Press, 2000).

15. In the parlance of chapter 4, most of these firms were trying to cram the disruptive innovation—handheld devices—into the large, obvious mainstream market, notebook computers. True to form, this strategy proved to be very expensive, and they all failed.

16. An important theoretical perspective called “resource dependence” asserts that it is the entities external to the organization that control what the organization can and cannot do. These entities—customers and investors—provide to the organization the resources that it needs to thrive. Managers cannot do things that are not in the interests of these external providers of resources, or they will withhold their resources and the company will die. See Jeffrey Pfeffer and Gerald R. Salancik, The External Control of Organizations: A Resource Dependence Perspective (New York: Harper & Row, 1978). The Innovator’s Dilemma devoted significant space to this issue, noting that the mechanism for managing change in the face of resource dependence is to create independent organizations that can be dependent on other providers of resources, who value the disruptive products.

17. The distinguished sociologist Arthur Stinchcombe has written extensively on the importance of initial conditions in determining the subsequent chain of decisions and events.

18. Clayton Christensen, “Materials Technology Corp.,” Case 9-694-075 (Boston: Harvard Business School, 1994); and Clayton Christensen, “Linking Strategy and Innovation: Materials Technology Corp.,” Case 9-696-082 (Boston: Harvard Business School, 1996).

19. For Christensen, studying these problems as an academic has made it clear that MTC’s technology was a breakthrough sustaining innovation: The company was trying to bring better products into established markets, and the breakthrough technology entailed extensive interdependencies in development and design. MTC made many of the choices described in this book incorrectly—and as a result, although the company has survived and is profitable, the path was absolutely tortuous.

20. See Rita Gunther McGrath and Ian C. MacMillan, “Discovery-Driven Planning,” Harvard Business Review, July–August 1995, 44–56. Professors McGrath and MacMillan have written a number of very useful things about managing the creation of new businesses, of which this article is representative. We encourage you to badger them in their offices at Columbia and Wharton, respectively, for more good ideas. In their article, they use the term “platform-based planning.” We have instead called this process “deliberate strategic planning” to be consistent with the language used elsewhere in this chapter.

21. We are concerned that as venture capital firms have gradually become populated by less-experienced analysts who learned only about deliberate strategy in their MBA courses, they are subtly demanding more and more rigor, and data and evidence that the strategy of a business is right. They then pressure the management teams of their portfolio companies to “execute.” They only revert to an emergent mode when the initial investment has been squandered and the founding managers sacked, and there is no alternative but to seek a viable strategy through emergent processes.