V. APPLICATION TO ECONOMIC HISTORY

How the Gold Standard Worked, 1880–19131

DONALD N. MCCLOSKEY AND J. RICHARD ZECHER

1 THE MONETARY THEORY AND ITS IMPLICATIONS FOR THE GOLD STANDARD

Each intellectual generation since the mercantilists has revised or refined the understanding of how the balance of payments is kept in equilibrium under a system of fixed exchange rates, and all these understandings find a place in the historical literature on the gold standard of the late nineteenth century. It is difficult, therefore, to locate the orthodox view on how the gold standard worked, for it is many views. If one can find historical and economic writings describing the gold standard (and other systems of fixed exchange rates) in the manner of Hume, as a price-specie-flow mechanism, involving changes in the level of prices, one can also find writings describing it in the manner of Marshall, involving changes in the interest rate, or of Taussig, involving changes in the relative price of exportables and importables, or of Ohlin, involving changes in income. The theoretical jumble is made still more confusing by a number of factual anomalies uncovered lately.2 Among other difficulties with the orthodox views, it has been found that the gold standard, even in its heyday, was a standard involving the major currencies as well as gold itself, and that few, if any, central banks followed the putative ‘rules of the game’.

This essay reinterprets the gold standard by applying the monetary theory of the balance of payments to the experience of the two most important countries on it, America and Britain. Before explaining, testing, and using the theory in detail, it will be useful to indicate a few of the ways in which accepting it will change the interpretation of the gold standard of the late nineteenth century. The most direct implication is that central bankers did not have control over the variables over which they and their historians have believed they had control. The theory assumes that interest rates and prices are determined on world markets, and therefore that the central bank of a small country has little influence over them and the central bank of a large country has influence over them only by way of its influence over the world as a whole.

A case in point is the Bank of England. It is often asserted, as Keynes put it, that ‘During the latter half of the nineteenth century the influence of London on credit conditions throughout the world was so predominant that the Bank of England could almost have claimed to be the conductor of the international orchestra. By modifying the terms on which she was prepared to lend, aided by her own readiness to vary the volume of her gold reserves and the unreadiness of other central banks to vary the volume of theirs, she could to a large extent determine the credit conditions prevailing elsewhere.’3 When this musical metaphor is examined in the light of the monetary theory it loses much of its charm. If it is supposed, as in the monetary theory, that the world’s economy was unified by arbitrage, and if it is supposed further that the level of prices in the world market was determined, other things equal, by the amount of money existing in the world, it follows that the Bank’s potential influence on prices (and perhaps through prices on interest rates) depended simply on its power to accumulate or disburse gold and other reserves available to support the world’s supply of money. By raising the interest rate (the bank rate) at which it would lend to brokers of commercial bills, the Bank could induce the brokers or whoever else in the British capital market was caught short of funds to seek loans abroad, bringing gold into the country and eventually into the vaults of the Bank. If it merely issued bank-notes to pay for the gold the reserves available to support the supply of money would be unchanged, for Bank of England notes were used both at home and abroad as reserves. Only by decreasing the securities and increasing the gold it held—an automatic result when it discouraged brokers from selling more bills to the Bank and allowed the bills it already held to come to maturity—could the Bank exert a net effect on the world’s reserves. In other words, a rise in the bank rate was effective only to the extent that it was accompanied by an open market operation, that is, by a shift in the assets of the Bank of England out of securities and into gold. The amounts of these two assets held by the Bank, then, provide extreme limits on the influence of the Bank on the world’s money supply. Had the Bank in 1913 sold off all the securities held in its banking department it would have decreased world reserves by only 0·6 per cent; had it sold off all the gold in its issue department, it would have increased world reserves by only 0·5 per cent.4 Apparently the Bank was no more than the second violinist, not to say the triangle player, in the world’s orchestra. The result hinges on the assumption of the monetary theory that the world’s economy was unified, much as each nation’s economy is assumed to be in any theory of the gold standard. If the assumption is correct the historical inference is that the Bank of England had no more independent influence over the prices and interest rates it faced than, say, the First National Bank of Chicago has over the prices and interest rates it faces, and for the same reason.

A related inference from the monetary theory is that the United Kingdom, the United States, and other countries on the gold standard had little influence over their money supplies. Since money, like other commodities, could be imported and exported, the supply of money in a country could adjust to its demand and the demand would depend on the country’s income and on prices and interest rates determined in the world market. The creation of money in a little country would have little influence on these determinants of demand and in consequence little influence over the amount actually supplied. How ‘little’ America and Britain were depends on how large they were relative to the world market, and in a world of full employment and well-functioning markets the relevant magnitude is simply the share of the nation’s supply of money in the world’s supply. One must depend on an assumption that the money owned by citizens of a country was in rough proportion to its income, for the historical study of the world’s money supply is still in its infancy.5 In 1913 America and Britain together earned about 40 per cent of the world’s income, America alone 27 per cent.6 A rise in the American money supply of 10 per cent, then, would raise the world’s money supply on the order of 2·7 per cent; the comparable British figure is half the American. Clearly, in the jargon of international economics, America and Britain were not literally ‘small countries’. Yet 2·7 per cent is far from the 10 per cent implied by the usual model, that of a closed monetary system, and the British figure is far enough from it to make it unnecessary for most purposes in dealing with the British experience to look closely into the worldwide impact of British policy.

Finally, the monetary theory implies that it matters little whether or not central banks under the gold standard played conscientiously the ‘rules of the game’, that is, the rule that a deficit in the balance of payments should be accompanied by domestic policies to deflate the economy. The theory argues that neither gold flows nor domestic deflation have effects on prevailing prices, interest rates, and incomes. The inconsequentiality of the rules of the game may perhaps explain why they were ignored by most central bankers in the period of the gold standard, in deed if not in words, with no dire effects on the stability of the system.

2 EMPIRICAL ANOMALIES IN THE LITERATURE ON THE GOLD STANDARD

If the orthodox theories of the gold standard are incorrect, it should be possible to observe signs of strain in the literature when they are applied to the experience of the late nineteenth century. This is the case. Indeed, in the midst of their difficulties in applying the theories earlier observers have anticipated most of the elements of the alternative theory proposed here.

On the broadest level it has always been puzzling that the gold standard in its prime worked so smoothly. After all, the mechanism described by Hume, in which an initial divergence in price levels was to be corrected by flows of gold inducing a return to parity, might be expected to work fairly slowly, requiring alterations in the money supply and, more important, in expectations concerning the level and rate of change of prices which would have been difficult to achieve. The actual flows of gold in the late nineteenth century, furthermore, appear to be too small to play the large role assigned to them.7 Of course, one should ask, ‘Too small relative to what?’ Gold was a substantial part of the monetary base, and one could rescue the argument by positing, as Milton Friedman and Anna Schwartz have done in their classic study of American monetary history, a close causal connection between the monetary base (‘high-powered money’ in their terminology) on the one hand and money and the price level on the other. This is an attractive argument for the United Kingdom, as might be expected for a country with nearly 100 per cent gold reserves against its currency and with no gold mines. For the United States, however, it is considerably less attractive. Only half of the variations in the American stock of high-powered money from 1880 to 1913 can be explained directly by gold flows, and other national monies with a less mechanical connection to external flows of gold than the British, such as the French and German, could be expected to have a similar record.8 Most observers, perhaps anticipating these results, have emphasised the function of gold flows as a mere signal to central bankers to contract or expand their economies. If central bankers did play the rules of the game, reacting to a small outflow of gold by reducing the monetary base still further, a small flow of gold could, of course, have large effects, at any rate if one believes the orthodox theories. To repeat, however, central bankers often did not play the rules: the Bank of France and the National Bank of Belgium, for example, kept their discount rates low regardless of gold flows.9 An alternative indicator of the extent to which central bankers played the rules is the extent to which the relationship between inflows of gold and increases in domestic credit (that is, increases in the portion of the money supply determined by factors other than the inflow of gold) was positive. Once again, the indications are that in the late nineteenth century the monetary authorities, in this case American and British, cheated: the correlation between gold flows and annual changes in domestic credit was –0·07 in the United States and –0·74 in the United Kingdom.10

Yet the gold standard, it is said, worked quickly and well. The exchange rate between sterling and dollars, among many other rates, remained virtually unchanged from January 1879, when the United States put itself back on gold, to August 1914, when the war put the United Kingdom effectively off it. Nobody ran out of gold. And over this third of a century the restrictions on flows of gold, commodities, immigrants, and capital that were in the eighteenth century and have become again in the twentieth such popular instruments of government policy either were not used (for gold, immigrants, and capital) or were used for purposes other than correcting deficits in the balance of payments (for commodities). In view of its strange efficacy central bankers may be forgiven for looking back on the gold standard of the late nineteenth century with the pious awe usually reserved for religious mysteries.

The mystery of the smooth working of the gold standard fades if the central postulate of the monetary theory, the unity of commodity and capital markets, is an adequate characterisation of the world’s economy in the late nineteenth century. If the postulate is accepted, it implies that the wrenching adjustments of prices, interest rates, and incomes that the orthodox theory in its many forms holds necessary for re-establishing equilibrium in the balance of payments were in fact not necessary. The world’s economy determined the prices and interest rates prevailing in each nation’s economy and it was the flow of gold itself that re-established equilibrium in the money market by satisfying the demand for money that prompted the flow in the first place.

Whether the postulate of unified markets is acceptable or not is an empirical matter to be examined below. What is relevant here is that writers on the history of the gold standard, even as they have passed by its implications, have accepted it in part. The postulate is most easily defended (in fact, nearly universally accepted) for goods that enter international trade. Hume himself emphasised that the prices of such goods could differ only by transport or tariff costs, and Jacob Viner, in his survey in 1937 of the development of the theory of the gold standard, quoting Hume to this effect, was emphatic that all important subsequent writers agreed.11 Frank Taussig certainly did. He wrote in 1906: ‘Those commodities that enter into international trade have a common price the world over. The extraordinary cheapening of transportation during the last half-century, the perfected organisation of markets and exchanges, contribute to make this assumption a safe one for all the great staples.’12 Taussig, like many others before and since, went on to emphasise that non-traded goods existed, arguing that the gold standard re-established equilibrium in a nation’s balance of payments by altering the price of non-traded relative to traded goods. It is worth remarking here that it is not enough to reject the postulate of unified markets that non-traded goods merely exist: as will be argued in detail below, there must be low substitutability between traded and non-traded goods in both consumption and production. In any case, later writers have made larger concessions to the force of arbitrage in commodity markets. In his massive study of the interwar gold standard published in 1940, W. A. Brown, for example, asserted that ‘the international influence of the London or Liverpool price of many important commodities was a factor tending to prevent substantial divergence in the movements of general prices of countries adhering to the international gold standard’.13 And in 1964, Robert Triffin, in an important piece of iconoclasm on the gold standard, was still more explicit:

‘Under these conditions, national price and wage levels remained closely linked together internationally, even in the face of divergent rates of monetary and credit expansion, as import and export competition constituted a powerful brake on the emergence of any large disparity between internal and external price and cost levels. Inflationary pressures could not be contained within the domestic market, but spilled out directly to a considerable extent, into balance-of-payments deficits rather than into uncontrolled rises of internal prices, costs, and wage levels.’14

A flow of gold is by no means a necessary part of this process of arbitrage. In fact, the mere threat of arbitrage may be sufficient to bring a nation’s prices and interest rates into line with the world’s, without flows of anything. The usual justification for seizing on the flow of gold as the central mechanism of adjustment in prices and interest rates among countries on the gold standard is that gold is cheap to ship: slight variations in the exchange rate between two currencies caused by disturbances in the balance of payments and correctable by changes in prices and interest rates will cause gold to flow if the two currencies are both attached to gold at fixed rates. As Marshall put it in the early 1920s, when the exchange rate between French and Belgian money is favourable to France, ‘really it is favourable to those who bring goods to France from Belgium and it is unfavourable to all who send goods in the opposite direction. One of the goods, which may be sent, is gold.’15 Marshall was choosing his words carefully, as he usually did, for he realised that other commodities could and did serve this function as well. Gold, being cheap to transport, was always close to the price at which it would be exported (if foreign means of payments were especially desired by, say, Englishmen) or imported (if English means of payment were especially desired by foreigners); but a large number of commodities or securities would also at any one time be at their export or import price if arbitrage, allowing for transport costs and tariffs, were effective. At the end of the same chapter, in a section entitled, in Marshall’s descriptive manner, ‘So long as national currencies are effectively based on gold, the wholesale price of each commodity tends to equality everywhere’, he agrees, speaking by analogy with the gold points of the ‘leadpoint’ and the ‘Egyptian bond-point’ without drawing explicitly the inference that gold does not in that case play the central role in forcing parallel movements of prices and interest rates in different nations assigned to it in the orthodox theories.16 The firm belief of the classical and neo-classical economists in the unity of world markets under modern conditions did not fit well with their views on the gold standard.

The behaviour of prices in the late nineteenth century has suggested to some observers that the view that it was gold flows that were transmitting price changes from one country to another is indeed flawed. Over a short period, perhaps a year or so, the simple price-specie-flow mechanism predicts an inverse correlation in the price levels of two countries interacting with each other on the gold standard. A monetary expansion in Britain, the story goes, would raise the British price level, making British exports less competitive. This would produce a deficit in Britain’s payments, equivalent to an outflow of gold. The outflow of gold would reduce the supply of money in Britain and raise it elsewhere, driving prices in Britain down and prices in, say, America up. Yet, as Triffin has noted and as we shall demonstrate presently, even over a period as brief as a single year, what is impressive is ‘the overall parallelism—rather than divergence—of price movements, expressed in the same unit of measurement, between the various trading countries maintaining a minimum degree of freedom of trade and exchange in their international transactions’.17

Over a longer period of time, of course, the parallelism is consistent with the theory of price–specie–flow. In fact, one is free to assume that the lags in its mechanism are shorter than a year, attributing the close correlations among national price levels within the same year to a speedy flow of gold and a speedy price change resulting from the flow rather than to direct and rapid arbitrage. One is not free, however, to assume that there were no lags at all; in the price-specie-flow theory inflows of gold must precede increases in prices by at least the number of months necessary for the money supply to adjust to the new gold and for the increased amount of money to have its inflationary effect. The American inflation following the resumption of specie payments in January 1879 is a good example. After examining the annual statistics on gold flows and price levels for the period, Friedman and Schwartz concluded that ‘It would be hard to find a much neater example in history of the classical gold-standard mechanism in operation.’18 Gold flowed in during 1879, 1880, and 1881 and American prices rose each year. Yet the monthly statistics on American gold flows and price changes tell a very different story. Changes in the Warren and Pearson wholesale price index during 1879–81 run closely parallel month by month with gold flows, rising prices corresponding to net inflows of gold. There is no tendency for prices to lag behind a gold flow and some tendency for them to lead it, suggesting not only that the episode is an especially poor example of the price-specie-flow theory in operation, but also that it might well be a reasonably good one of the monetary theory.19

The strain of interpreting the gold standard of the late nineteenth century in terms of the available theories shows most clearly in the relations uncovered in empirical work between gold flows and income. After World War I economists put increasing emphasis on variations in income induced by deficits or surpluses in the balance of payments as the critical element in re-establishing equilibrium. As the matter was put in one historical survey of the gold standard, ‘What is important to note … is that the adjustment attributed to price changes and gold flows in the nineteenth century was swift and smooth, not because of the power of price changes to effect adjustment, but because income changes were always acting in the same direction to reinforce the price change.’20 Yet the negative correlation between income and gold inflows over the course of the business cycle predicted by such assertions did not hold, at any rate not during the late nineteenth century in the United Kingdom and the United States, and this uncomfortable fact has long been known. To a first approximation (the succeeding approximations will be presented in Section 4 below), the monetary theory predicts the opposite correlation, which is the correlation in fact observed: as incomes rise in a country the demand for money of its citizens will rise as well, and the demand can be satisfied, if it is not satisfied by the domestic monetary authorities, by an importation of gold, that is to say, by a surplus—not a deficit—in the balance of payments.21

A. P. Andrew observed as early as 1907 that this was the case for the United States in the late nineteenth century, and W. E. Beach in 1935 and Alec Ford in 1962 that it was the case for the United Kingdom as well.22 In a book on the American balance of payments during the nineteenth century published in 1964, and in a set of related articles, Jeffrey Williamson went further, arguing explicitly that a rise in income in the United States, when not accompanied by a rise in the internal supply of money (as it was, for example, during the period of intensive exploitation of the Californian gold discoveries), produced an excess demand for real money balances and, therefore, a surplus in the balance of payments.23 And an article by P. B. Whale in 1937 is a still earlier anticipation of this point in the monetary theory. Citing Andrew and Beach, he wrote:

‘[T]he suggestion is that in a regime of fixed exchange rates the monetary requirements of a particular country may be altered by changes in prices or trade activity independent of any prior change in the supply of money…. evidence of concomitant [domestic] movements of gold into and out of circulation [concomitant, that is, with evidence of inward and outward movements of gold internationally, which was correlated positively with the business cycle] confirms the view that it was the monetary requirements determined by a given price level which provided the underlying cause of the international gold movements.’24

At another point he refers approvingly to a contemporary German writer who treated ‘gold flows somewhat similarly as a result of an excess of money balances at the equilibrium level of incomes’, that is to say, in precisely the manner of the monetary theory.25 Evidently, it would be grossly unfair to earlier work on the gold standard of the nineteenth century to claim that the elements drawn together in this essay are novel with us. They are all in the earlier work, however uncomfortably they fit with the successive versions of the orthodox theory.

3 DID INTERNATIONAL MARKETS WORK WELL?

If arbitrage—or, more precisely, a close correlation among national price levels brought about by the ordinary working of markets—can be shown to characterise the international economy of the late nineteenth century many of the conclusions of the monetary theory will follow directly and the rest will gain in plausibility. In the monetary theory, the international market short-circuits the effects of domestic policy on American prices, and the expansion of the domestic supply of money spills directly into a deficit in the balance of payments.

It is essential, therefore, to examine the evidence for this short-circuiting. As a criterion of its effectiveness, we use the size of the contemporaneous correlations among changes in the prices of the same commodities in different countries. We have chosen a sample of the voluminous information on prices for examination here.26 The statistical power of the tests is not as high as one might wish, for even if two nations shared no markets they could none the less exhibit common movements in prices if they shared similar experiences of climate, technological change, income growth, or any of the other determinants of prices. In the long run, indeed, the other theories of the balance of payments imply some degree of correlation among national prices. For this reason we have resisted the temptation to improve the correlations by elaborate experimentation with lags and have concentrated on contemporaneous correlations, that is, on correlations among prices in the same year. If international markets worked as sluggishly as the other theories assume, there would be little reason to expect contemporaneous correlations to be high.

The simplest way to think about arbitrage is in terms of a single market. Given fixed exchange rates and the vigorous pursuit of profit through arbitrage, the correlation between price changes for a homogeneous commodity in two countries, say America and Britain, separated by transportation costs and tariffs, would be zero within the limits of the export and import points and unity at those points. A regression of British on American prices would test simultaneously for the lowness of the commodity’s cost of transportation, including tariffs, relative to its price and the vigour with which prices were arbitraged. The good would not actually have to be traded between the two countries for the correlation to be high: the mere threat of arbitrage, or a common source of supply or demand, would be sufficient for goods with low transport costs. For goods actually flowing in trade in a uniform direction over the period 1880 to 1913, such as wheat from America to Britain, one would expect the correlation to be perfect and the slope of the corresponding regression to be unity, no matter what the cost of transport or the level of tariffs, so long as these did not change. They both did change, of course, as exemplified by the failure of the German price of wheat to fall as far as the British or American during the 1880s, as the Germans imposed protective duties on wheat imports.27 None the less, the average correlation among the changes in American, British, and German prices of wheat is high, about 0·78. A regression of the annual change in British prices on the change in American prices (Britain had no tariffs on wheat, but the cost of ocean transport was falling sharply in the period) yields the following result (all the variables here and elsewhere in this section are measured as annual absolute changes; the figures below the coefficients in parentheses are standard errors; the levels of the variables have been converted to an index in which the average levels are equal to one):28

![]()

One would expect errors in the independent variable to affect this and the later regressions, biasing the slope towards zero (there were changes in the source of the American wheat price, for example, and after 1890 it is a New York price alone). The value of 0·646 would be a lower bound on the true slope and the value implied by a regression of the American on the British price (1·124) an upper bound. The two bounds bracket reasonably closely the value to be expected theoretically, namely, 1·0, and the constants in both regressions (which represent the trend in the dependent price over time) are insignificantly different from zero. Not surprisingly, in short, wheat appears to have had a unified world market in the late nineteenth century; a fortiori, so did gold, silver, copper, diamonds, racehorses, and fine art.

This conclusion can be reinforced from another direction. For wheat the reinforcement is unnecessary, for few would doubt the international character of the wheat market, but it is useful to develop here the line of argument. Because of transport costs, information costs, and other impediments to a perfect correlation among changes in national prices, any use of the notion of a perfectly unified market must be an approximation, within one country as well as between two countries. For purposes of explaining the balance of payments economists have been willing to accept the approximation that within each country there is one price for each product, setting aside as a second-order matter the indisputable lack of perfect correlation between price changes in California and Massachusetts or between price changes in Cornwall and Midlothian. It is reasonable, therefore, to use the level of the contemporaneous correlation between the prices of a good in different regions within a country as a standard against which to judge the unity of the market for that good between different countries. If the correlations between the prices of wheat in America, Britain, and Germany were no lower than those between the prices of wheat in, say, different parts of Germany, there would be no grounds for distinguishing between the degree of unity in the national German market and in the international market for wheat. This was in fact the case. The average correlation between changes in the prices of wheat in pairs of German cities (Berlin, Breslau, Frankfurt, Konigsberg, Leipzig, Lindau, and Mannheim) from 1881 to 1912 was 0·85, quite close to the average correlation for the three countries over the same period of 0·78.

One could proceed in this fashion through all individual prices, but a shorter route to the same objective is to examine correlations across countries between pairs of aggregate price indexes. Contrary to the intuition embodied in this thought, however, there is no guarantee, at any rate none that we have been able to discover, that the correlation of the indexes is an unbiased estimator of the average degree of correlation among the individual prices or, for that matter, that it is biased in any particular direction.29 In other words, barriers to trade could be high or low in each individual market without the aggregate correlation necessarily registering these truths. None the less, putting these doubts to one side, we will trust henceforth to the intuition.

The pioneers of the method of index numbers, Laspeyres, Jevons, and others writing in the middle of the nineteenth century, produced indexes of wholesale prices—believable indexes of retail prices began to be produced only in the 1890s and implicit GNP deflators, of course, much later—and in consequence wholesale price indexes dominated empirical work on the balance of payments in the formative years of the theory. The contemporaneous correlation between annual changes in British and American wholesale prices 1880–1913 is 0·66, high enough in view of the differences in weights in the indexes and in view of the low correlation of annual changes implied by the lags operating in the orthodox theories to lend support to the postulate of a unified world market.

It is at this point, however, that supporters of the orthodox theory begin to quarrel with the argument, as did Taussig with those bold enough to suggest that world markets in more than merely traded goods were integrated in the late nineteenth century, or as did the many doubters of the theory of purchasing power parity with those who used wholesale prices to indicate the appropriate rates of exchange after World War I. The standard objection has been that wholesale price indexes are biased samples from the distribution of correlations because they consist largely of easily traded goods, ignoring non-traded services and under-representing non-traded goods. A large lower tail of the distribution, it is said, is left off, leading to a false impression that national price levels are closely correlated.

A point that must be made at once, however, is that traded goods, in the sense of goods actually traded and goods identical to those actually traded, were not a small proportion of national income. Historians and economists have usually thought of the openness of economies in terms of the ratio of actual exports or imports to national income, and have inferred that the United States, with a ratio of exports to national income of about 0·07 in the late nineteenth century, was relatively isolated from the influence of international prices and that the United Kingdom, with a ratio of 0·28, was relatively open to it. Yet in both countries consumption of tradeable goods, defined as all goods that figured in the import and export lists, was on the order of half of national income.30 If any substantial part of the national consumption or production of wheat, coal, or cloth entered international markets in which the country in question was a small supplier or demander, the prices of these items at home would be determined exogenously by prices abroad. Wholesale indexes, if they do indeed consist chiefly of traded goods, are not so unrepresentative of all of national income as might be supposed.

But what of the other, non-tradeable half of national income? Surely, as James Angell wrote in 1926, ‘for non-traded articles there is of course no direct equalisation [of price] at all’.31 The operative word in this assertion is ‘direct’, for without it the assertion is incorrect. The price of a good in one country is constrained not only by the direct limits of transport costs to and from world markets but by the indirect constraints arising from the good’s substitutability for other goods in consumption or production. This was clear to Bertil Ohlin, who asked, ‘To what extent are interregional discreppancies in home market prices kept within narrow limits not only through the potential trade in these goods that would come into existence if interregional price differences exceeded the costs of transfer, but also through the actual trade in other goods?’32 It is not surprising to find Ohlin asking such a question, for the analytical issue is identical to the one that gave birth to that errant child of the Hecksoher-Ohlin theory, factor-price equalisation. The price of the milk used as much as the wage of the labour used is affected by the international price of butter and cheese. A rise in the price of a traded good will cause substitutions in production and consumption that will raise the prices of non-traded goods. To put the point more extremely than is necessary for present purposes, in a general equilibrium of prices the fixing of any one price by trade determines all the rest. The adjustment to the real equilibrium of relative prices, which must be achieved eventually, can be slow or quick. The monetary theory assumes that it is quick.

If it were in fact slow, one would expect the contemporaneous correlation between prices for countries on the gold standard to fall sharply as more comprehensive price indexes, embodying non-traded goods, are compared. This is not the case. The correlation between the annual changes in the GNP deflators 1880–1912 for America and Britain is 0·60, to be compared with the correlation for wholesale prices alone of 0·66. The regressions of the annual changes of American on British deflators and British on American were (standard errors in parentheses; levels of the price variables converted to indexes with their averages as the base):

AP |

= |

0·0002 + 0·961 BP |

R2 = 0·35, D.–W. = 1·98 Standard error of the regression as a percentage of the average level of the American price = 2·5% |

BP |

= |

0·0017 + 0·33 AP |

R2 = 0·34, D.–W. = 1·92 Standard error of the regression as a percentage of the average level of the British price = 1·4% |

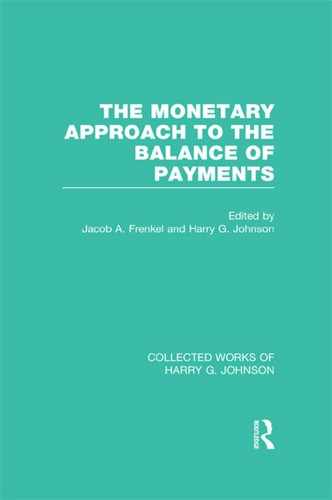

The correlations of the German GNP deflator with the American (0·40) and the British (0·45) are considerably lower, but this may be simply a reflection of the inevitable frailties of Walther Hoffman’s pioneering effort to produce such a deflator, or, perhaps, a reflection of the sharp rises in German tariffs. More countries have retail price indexes (generally with weights from working-class budgets) than have reliable GNP deflators, and these statistics tell a story that is equally encouraging for the postulate of arbitrage. The correlation matrix of annual changes in retail prices for the United States, the United Kingdom, Germany, France, and Sweden is shown in Table 16.1. The British–American correlation (0·57) is again not markedly below the correlation of the wholesale indexes, despite the importance of such non-traded goods as housing in the retail indexes.33

Table 16.1 Simple Correlations between Annual Changes in Retail Prices, 1880–1912

The correlation of American with British retail prices is probably not attributable to the trade in food offsetting a lower correlation between non-traded goods, for the simple correlation between American and British food prices in the years for which it is available (1894–1913) is lower, 0·49 compared with 0·57. Against this encouraging finding, however, must be put a less encouraging one. The average correlation between the changes in food prices in five regions of the United States (North Atlantic, South Atlantic, North Central, South Central, and the West) for 1891–1913 is very high, 0·87, contrasted with the British–American correlation of only 0·49. If food prices were as well arbitraged between as inside countries the British–American correlation would have to be much higher than it is. Still, even with perfect unity in the market for each item of food, one would not expect countries with substantially different budget shares to exhibit close correlations in the aggregate indexes. The lower correlation between Britain and the United States than between regions of the United States, then, may well reflect international differences of tastes and income rather than lower arbitrage.

If one proceeds in this fashion further in the direction of less traded goods the results continue to be mixed, although on balance giving support to the postulate of unity in world markets. The most obvious non-traded good is labour. The correlation between changes in wages of British and American coal-miners 1891–1913 is 0·42 but the correlation between those of British and American farm labourers is only 0·26. Both are lower than the correlations between changes in the wages of the two employments in each country, 0·65 in Britain and 0·53 in America. The correlation between the annual changes in Paul Douglas’ index of hourly earnings of union men in American building and the changes in A. L. Bowley’s index of wages in British building from 1891 to 1901 is negligible, only 0·10. On the other hand, the average correlation among bricklayers’ hourly wages in four cities (Boston, Cincinnati, Cleveland, and Philadelphia) selected from the mass of data for 1890–1903 in the 19th Annual Report of the U.S. Commissioner of Labor is only 0·14. The correlations for changes in wages between countries are low, in other words, but there is reason to believe that they are nearly as low within a geographically large country like the United States as well.

The same is true for an unambiguously non-traded commodity, common brick. That it is non-traded, that is a poor substitute for traded goods, and that it enters into the production of non-traded commodities is evident from the negligible correlation between changes in its average price in Britain and America. Yet from 1894, when the statistics first become available, to 1913, the average correlation between prices of common brick at the plant in seven scattered states of the United States (California, Georgia, Illinois, New York, Ohio, Pennsylvania, and Texas) was only 0·11, and even between three states in the same region (New York, Ohio, and Pennsylvania) it was only 0·13. This degree of correlation may be taken as an indicator of the correlation between regions of the United States attributable to a common experience of general inflation, technological change, and growth of income rather than to the unity of markets. It is small. In any case, common brick is a good at the lower end of the distribution of goods by their correlations, and there is little evidence of greater integration of markets within than between countries.

All these tests can be much expanded and improved, and we plan to do so in later work.34 What has been established here is that there is a reasonable case, if not at this stage an overwhelming one, for the postulate of integrated commodity markets between the British and American economies in the late nineteenth century, vindicating the monetary theory. There appears to be little reason to treat these two countries on the gold standard differently in their monetary transactions from any two regions within each country.

4 MONEY, GOLD, AND THE BALANCE OF PAYMENTS

If international arbitrage of prices and interest rates was thoroughgoing and if the growth of real income in a country was exogenous to its supply of money, then the country’s demand for money can be estimated by relatively straightforward econometric techniques. The balance of payments—identified here with flows of gold—predicted by the monetary theory can then be estimated as the difference between the growth in the country’s total predicted demand for money and the growth in its actual domestic supply. If, further, the actual flow of gold closely approximates the flow implied by the estimated change in the demand for money minus the actual change in the domestic supply of money, the monetary theory of the gold standard warrants serious consideration. In fact, to a remarkable degree the monetary theory for the United States and the United Kingdom from 1880 to 1913 passes this final test.

In Table 16.2 are presented the average movements of the British and American variables to be explained (the movements, that is, in money supplies and in that part of the money supply attributable to international flows of gold) and the average movements of the variables with which the monetary theory would explain them (the movements in prices, interest rates, and incomes affecting the demand for money and the movements in that part of the money supply attributable to domestic forces). The average percentage change in the money supply was decomposed in a merely arithmetical way (described in the footnote to the table) into a part reflecting how the money supply would have behaved if all gold flows into or out of the country had been allowed to affect it (by way of the multiple effects of reserves on the money supply) and a residual reflecting all other influences. Arithmetically speaking, the causes of changes in British and American money supplies differed sharply; virtually all the change in Britain was attributable to international flows of gold while virtually all the change in America was attributable to other, domestic sources of new money. Economically speaking, the differences are less sharp. Although over these three decades on average the rate of change of the money supply was far larger in America than in Britain, the difference is adequately explained in terms of the monetary theory by the faster growth of American income, given the similarity (in accord with the findings of the last section) in the behaviour of prices and given the relative fall in American interest rates.

Table 16.2 Average Annual Rates of Change 1882–1913 of American and British Money Supplies (Domestic and International), Incomes, Prices, and Interest Rates. (percentages; standard errors in parentheses)

Sources:

Line 1. The rate of change of the money supply attributable to gold flows was calculated as:

![]()

where M is the total money supply, H is ‘high-powered money’ (Mt/Ht, therefore, is the so-called ‘money multiplier’) and R is the annual net flow of gold. The figures on money supply and high-powered money for the United Kingdom were taken from D. K. Sheppard, ‘Asset Preferences and the Money Supply in the United Kingdom 1880–1962’, University of Birmingham Discussion Papers, Ser. A, No. 111 (November 1969), p. 16; and for the United States from Friedman and Schwartz, op. cit., pp. 704–7. The figures on gold flows for the United Kingdom were compiled from Beach, op. cit., p. 46f. These are for England alone, excluding Scotland and Ireland, but there is little doubt that they cover the great bulk of flows into and out of the United Kingdom. Gold flows for the United States are given in U.S. Bureau of the Census, Historical Statistics of the United States (Washington, D.C.: 1960), series U6.

Line 2 = Line 3 – Line 1.

Line 3. Source as in Line 1.

Line 4. U.S. real gross national product is from Simon Kuznets’ worksheets, reported in R. E. Lipsey, Price and Quantity Trends in the Foreign Trade of the United States (New York: National Bureau of Economic Research, 1963), p. 423; for years before 1889, the Kuznets figure Lipsey used was inferred from Lipsey’s ratio of GNP to farm income and his estimate of farm income (pp. 423–4). U.K. real gross domestic product is from C. H. Feinstein, National Income, Expenditure and Output of the United Kingdom, 1855–1965 (Cambridge: Cambridge University Press, 1971), Appendix Table 6, col. 4.

Line 5. For the U.S. the figure is from Lipsey, as in Line 4. For the U.K. the figure is from Feinstein, Appendix Table 61, col. 7.

Line 6. The U.S. interest rate is Macauley’s unadjusted index number of yields of American railway bonds (Historical Statistics of the U.S., as cited, series X332). The U.K. rate is the yield of consolidated government bonds (consols) in Mitchell, Abstract of British Historical Statistics (Cambridge, Cambridge University Press, 1962), p. 455.

So much is apparent from the arithmetic of the British and American experience. To go further one needs a behavioural model explaining the annual balance of payments in terms of the monetary theory. The model is simplicity itself. It begins with a demand function for money, the only behavioural function in the model, asserting that the annual rate of change in the demand for money balances depends on the rates of change of the price level and of real income and on the absolute change in interest rates (asterisks signify rates of change):

![]()

And it ends with a domestic money supply function (literally, an identity using the observed money multiplier, as explained in the footnote to Table 16.2) and the statement that the money not supplied domestically was supplied through the balance of payments. It is evident that the monetary theory is simply a comparative statics theory of money’s supply and demand, in which the balance of payments satisfies demands for money not satisfied by domestic sources.

By virtue of the unity of world markets and the assumed exogeneity of the growth of real income to the supply of money (which is itself a consequence of market unity and the availability of an elastic supply of money abroad), there is no simultaneous equation bias in estimating the demand for money by ordinary least squares. It is convenient to estimate the demand in real terms. The result for the United States 1884–1913 of regressing the rate of change of real balances on the rate of change in real income and the absolute change in the interest rate is (t-statistics in parentheses):

![]()

And for the United Kingdom:35

![]()

These appear to be reasonable demand equations, although the income elasticity in the equation for the United Kingdom is low, perhaps an artefact of errors in the series for income, which, given the low variability of British income, would reduce the fitted regression coefficient. Another explanation might be the substantial ownership of British money by foreigners, which would reduce the relevance of movements in British income to the ‘British’ money supply. Still, both demand equations accord reasonably well with other work on the demand for money.

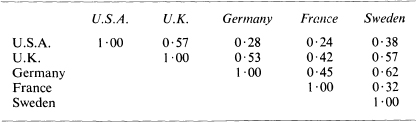

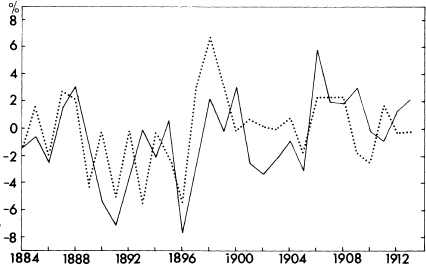

The acid test of the model, of course, is its performance in predicting the balance of payments as a residual from the predicted demand for money and the actual domestically determined supply. Its performance is startlingly good. The good fit of the American demand equation offsets the relative unimportance of gold flows to the American supply, while the relative importance of gold flows to the British supply offsets the poor fit of the British demand equation. Figures 16.1 and 16.2 exhibit the results, comparing the actual effect of gold flows on the American and British money supplies with the predicted effect. The actual effect is calculated annually by applying the observed ratio of money to reserves (including gold) to the actual flow of gold, the predicted effect by subtracting the domestic sources of money from the demand for money predicted by the regressions. In other words, the predicted effect is the excess demand for money predicted by the regressions in conjunction with the actual changes in the money supply due to domestic sources. One could just as well make the comparison of predicted with actual flows of gold, translating the predicted excess demand for money in each country into an equivalent demand for gold imports. The result would be the same, namely, a close correspondence between the predictions of the theory and the observed behaviour of the British and American stock of money and balance of payments.

Graph 1. Predicted (——) and Actual (- - -) Effects of Gold Flows on the U.S. Money Stock, Annual Rates of Change, 1884–1913.

Graph 2. Predicted (——) and Actual (- - -) Effects of Gold Flows on the U.K. Money Stock, Annual Rates of Change, 1884–1913.

No doubt the tests could be refined and more evidence could be examined. We believe, however, that we have established at least a prima facie case for viewing the world of the nineteenth-century gold standard as a world of unified markets, in which flows of gold represented the routine satisfaction of demands for money. We do not claim to have rejected decisively the view of the gold standard that depends on poor arbitrage between national markets or the view that predicts an inverse rather than a positive correlation between gold inflows and income or any of the other variants of the orthodox theories. Indeed, it is perfectly possible that these variants are partly true, perhaps true in the very short run, or under special circumstances, such as mass unemployment—the monetary theory is, in the sense described earlier, an equilibrium theory, which could be consistent with any number of theories about how the British and American economies behaved out of equilibrium. But a balance-of-payments surplus or deficit is not in itself, as has often been assumed, evidence that the economy in question is in fact out of equilibrium. The monetary theory’s central message is that a growing, open economy, buffeted by external variations in prices and interest rates, will have a varying demand for money, which would only fortuitously be supplied exactly from domestic sources. A country’s balance of payments, in other words, could be positive or negative over the course of a year even if all asset and commodity markets in the country were continuously in equilibrium, for the flow of money into the country during the year could exactly meet the year’s change in the demand for money. The source of the simplicity of the monetary theory of the gold standard is clear: the monetary theory is an equilibrium model, whereas the alternative theories are to a greater or lesser extent dynamic, disequilibrium models. We believe (as must be evident by now) that the simpler model yields a persuasive interpretation of how the gold standard worked, 1880–1913.

1 An earlier and longer version of this essay (available on request) was presented to the Workshop in Economic History at the University of Chicago and to the Cliometrics Conference at the University of Wisconsin. We wish to thank the participants in these meetings for their comments. The friendly scepticism of Moses Abramovitz, C. K. Harley, Hugh Rockoff, Jeffrey Williamson, and our colleagues at the University of Chicago, among them Stanley Fischer, Robert J. Gordon, A. C. Harberger, Harry G. Johnson, Arthur Laffer, and H. Gregg Lewis, contributed to a sharpening of the argument.

2 Many of these have been published in the Princeton Studies in International Finance. For example, Arthur I. Bloomfield, Short-term Capital Movements under the Pre-1914 Gold Standard (1963); the work cited below; and Peter H. Lindert, Key Currencies and Gold, 1900–1913 (1969). Bloomfield’s Monetary Policy under the International Gold Standard (New York, Federal Reserve Bank of New York, 1959) is seminal to this literature.

3 J. M. Keynes, Treatise on Money (London, Macmillan, 1930), vol. II, 306–7.

4 World official reserves at the end of 1913 of $7,100 million (16 per cent of which was foreign exchange, a good part of it sterling) are estimated by Lindert, op. cit., 10–12.

5 In 1964 Robert Triffin undertook to act as midwife, but as he concedes, the infant is still in poor health (see his The Evolution of the International Monetary System: Historical Reappraisal and Future Perspectives, Princeton Studies in International Finance, no. 12 [Princeton, Department of Economics, 1964] appendix I).

6 Needless to say, these are crude estimates: to continue the metaphor above, the historical study of world income is barely into its adolescence. The estimate of $362 billion for 1913 world income in 1955 prices begins with Alfred Maizels’s compilation of figures on gross domestic product at factor cost for twenty-one countries, given in his Industrial Growth and World Trade (Cambridge, Cambridge University Press, 1965), appendix E, p. 531. Czech and Hungarian income was estimated from Austrian income (post-1919 boundaries) on the basis of Colin Clark’s ratios among the three (in The Conditions of Economic Progress, 2nd edn [London, Macmillan, 1951] p. 155). Russian income was estimated by extrapolating Simon Kuznets’ estimate for 1958 back to 1913 on the basis of his figure for the decennial rate of growth, 1913–58 (in Modern Economic Growth [New Haven, Yale University Press, 1966] 65 and 360), yielding a figure of $207 per capita in 1958 prices, which appears to be a reasonable order of magnitude. The Russian per capita figure was then applied to the population of Bulgaria, Greece, Poland, Romania, and Spain, completing the coverage of Europe (boundary changes during the decade of war, 1910 to 1920, were especially important for these countries, except Spain; estimates of the relevant populations are given in R. R. Palmer, Atlas of World History [Chicago, Rand McNally, 1957] p. 193). Maizels gives estimates of national income for Canada, Australia, New Zealand, South Africa, Argentina, and Japan in 1913. Income per head in 1955 dollars was taken to be $50 in Africa except South Africa, $100 in Latin America except Argentina, $50 in India, and $60 in Asia except India and Japan, all on the basis of Maizels’ estimates for 1929 and an assumption of little growth. Population figures for these groups of countries around 1910 were taken from D. V. Glass and E. Grebenik, ‘World Population, 1800–1950’, in H. J. Habakkuk and M. Postan, Cambridge Economic History of Europe, Vol. VI, part 1 (Cambridge, Cambridge University Press, 1965) p. 58, with adjustments for the countries included in Maizels’ estimates, from his population figures (op. cit., p. 540).

7 Scepticism on this point has long been widespread. Consider, for example, J. W. Angell, The Theory of International Prices (Cambridge, Harvard University Press, 1926), p. 400: ‘It is perfectly obvious that neither the magnitudes nor the directions of the international flows of gold were adequate to explain those close and comparatively rapid adjustments of payments-disequilibria, and of price relationships, which were witnessed before the war.’

8 The American and British record is examined later in Table 16.2 below. Bruce Brittain of the Research Department, First National City Bank of New York, is currently engaged in examining the French experience in the light of the monetary theory.

9 P. Barrett Whale, ‘The Working of the Pre-War Gold Standard’, Economica, N.S., 4: 18–32, February 1937; reprinted in T. S. Ashton and R. S. Sayers, eds., Papers in English Monetary History (Oxford University Press, 1953), to which subsequent reference is made, p. 153. Compare R. H. I. Palgrave, ed., Dictionary of Political Economy (London, Macmillan, 1901), article on Banks, France: ‘The Bank of France endeavours to keep an even rate of discount. Thus for about five years, between 1883 and 1888, its rate of discount remained at 3%, while there were no fewer than 36 changes varying from 2% to 5% at the Bank of England during the same time.’

10 The sources for this calculation are given in Table 16.2 below.

11 Jacob Viner, Studies in the Theory of International Trade (1937; reprinted New York, A. M. Kelley, 1965), pp. 314–18.

12 Frank Taussig, ‘Wages and Prices in Relation to International Trade’, Quarterly Journal of Economics, 20: 497–522, August 1906, p. 499.

13 William A. Brown, The International Gold Standard Reinterpreted, 1914–1934 (New York, National Bureau of Economic Research, 1940), p. 775, italics added.

14 Robert Triffin, The Evolution of the International Monetary System, Princeton Studies in International Finance, no. 12 (Princeton, Department of Economics, 1964), p. 10 (his italics). P. B. Whale’s article of 1937, cited above, is a startlingly complete anticipation of this and other elements in the monetary theory.

15 Alfred Marshall, Money, Credit and Commerce (London, Macmillan, 1923), p. 145 (italics added). Compare p. 228, where he argues that a duty placed on some of a country’s imports will increase duty-free imports and that ‘Gold and silver will generally find a place among these’ (italics added).

16 Marshall, op. cit., pp. 152–4.

17 Triffin, op. cit., p. 4. He used export unit values. One could object that for many of the eleven countries he examined over the period 1870–1960 export unit values could be similar (namely, world wholesale prices for manufactures) without a corresponding similarity in the prices of domestic goods. Section 3 below overcomes this objection.

18 Milton Friedman and Anna J. Schwartz, A Monetary History of the United States, 1867–1960 (Princeton, Princeton University Press, 1963), p. 99.

19 The price index is given in George F. Warren and Frank Pearson, Prices (New York, Wiley, 1933, pp. 11–13). The statistics on gold flows (silver flows do not disturb the pattern) are from the U.S. Commerce Department, Census Bureau, Monthly Summary of Foreign Commerce, for January 1879 through December 1882. In 1882 the association between gold and prices reported in the text breaks down: prices rose in the first half of 1882 yet gold flowed out. This change, however, is consistent with the monetary theory, for in early 1882, according to the dating of the National Bureau of Economic Research, the business expansion that had begun in early 1879 came to an end. As the next few paragraphs in the text will emphasise, a fall in income reduces the demand for money and, other things equal, releases money for export.

20 W. M. Scammel, ‘The Working of the Gold Standard’, Yorkshire Bulletin of Economic and Social Research, 17: 32–45, May 1965.

21 The incorrect predictions of the orthodox theory on this point arise in part from a confusion between the balance of trade and the balance of payments. The working model is that the balance of payments is equal to the balance of trade plus a random error term (the balance on capital account). See, for example, Viner, Studies, cited above, and J. E. Meade, The Balance of Payments (London, Oxford University Press, 1951) p. 80. George Macesich used just such a model to explain the behaviour of the American economy in an early period of the gold standard (‘Sources of Monetary Disturbances in the United States, 1834–1845’, Journal of Economic History 20:407–34, September 1960). He asserted (p. 414) that ‘The heavy and varied capital flows thus had implications for the required behavior of exchange rates, specie flows, money supply, relative prices and the balance of trade.’ The exogeneity and randomness of the capital account in the American experience during the nineteenth century was asserted still more explicitly by J. Ernest Tanner and Vittorio Bonomo, in a criticism of the book by Williamson cited below (Tanner and Bonomo, ‘Gold, Capital Flows and Long Swings in American Business Activity’, Journal of Political Economy 76: 44–52, Jan./Feb. 1968). Williamson, however, in an attack on Macesich’s argument (J. G. Williamson, ‘International Trade and United States Economic Development, 1827–1843’, Journal of Economic History 21: 372–83, September 1961) made the decisive point (p. 377): ‘concomitant with real growth, there is a tendency to generate excess demands for real money balances, reflected, under a gold standard system, by an increasing inflow of gold. The solution is a general equilibrium one…. demands for money (gold), goods and securities must be solved simultaneously in a general equilibrium context’. This is a clear anticipation of the foundations of the monetary theory.

22 A. P. Andrew, ‘The Treasury and the Banks under Secretary Shaw’, Quarterly Journal of Economics, 21: 519–68, August 1907. W. E. Beach, British International Gold Movements and Banking Policy, 1881–1913 (Cambridge, Harvard University Press, 1935; see especially Charts xvii, xviii, and xix, and p. 77: ‘In general gold imports became important during the latter stages of the periods of business expansion, and at the same time the volume of currency in the hands of the public was expanding. In recession the flows were reversed’). A. G. Ford, The Gold Standard 1880–1914, Britain and Argentina (Oxford, Clarendon Press, 1962); see especially p. 36: ‘international gold movements, instead of being the determinants of the supply of money in Britain in this period, were probably determined by domestic monetary needs to some extent’.

23 J. G. Williamson, American Growth and the Balance of Payments (Chapel Hill: University of North Carolina Press, 1964), especially Chapter V; Williamson, ‘Real Growth, Monetary Disturbances and the Transfer Process: the United States, 1879–1900’, Southern Economic Journal, 29: 167–80, January 1963; and his article cited in the footnote above. It is testimony to the staying power of the tradition that Williamson is attacking that most of his work concerns the influences on the commodity and capital account separately. As was noted above, this procedure is otiose if it is indeed the balance of payments that is at issue. Williamson himself makes this point, in the chapter of his book (V) that presents the germ of the monetary theory: ‘in previous chapters we have exaggerated the independence of the movements in net capital flows and the trade balance.… the main point seems to be that gold flows cannot be treated simply as residuals’ from the trade and capital accounts together (pp. 163–4).

24 Whale, op. cit., pp. 158–9.

25 Whale, op. cit., p. 156. He was referring to K. F. Maier, Goldwanderungen: ein Beitrag zur Theorie des Geldes [Migration of Gold: A Contribution to the Theory of Money], 1935.

26 The sample is described in the appendix of the longer paper, available from the authors on request.

27 From 1880–2 to 1889–91 the ratio of the Berlin to the British price of wheat increased 30 per cent and remained at the higher ratio thereafter.

28 This and all subsequent regressions were subjected to the Cochrane-Orcutt iterative technique, removing in all cases understatement of the standard errors of the coefficients resulting from any auto-correlation of the residuals.

29 We have received a good deal of enlightenment on this point from H. Gregg Lewis of the University of Chicago and Hugh Rockoff of Rutgers University. The issue is as follows. Suppose, to simplify at the outset, that one chooses the same set of weights (w1, w2, …, wN) to form the two indexes of prices (IA and IB) in the two countries (A and B). What is the relationship between the weighted average of the individual correlations,

![]()

and the correlation of the weighted averages, corr (IA, IB) (where ![]()

![]() For the case of two prices we have written out both correlations in terms of the relevant covariances (expressing the prices in standardised form, thereby eliminating variances of the individual prices and making the corresponding covariances identical to correlation coefficients), with no very illuminating results. If no restrictions are placed on the covariances we can generate counter-examples to the proposition that the two are equal. But we suspect that we are neglecting true restrictions among the covariances (one set implying values for another set) and, further, that the case of large N would give more useful results.

For the case of two prices we have written out both correlations in terms of the relevant covariances (expressing the prices in standardised form, thereby eliminating variances of the individual prices and making the corresponding covariances identical to correlation coefficients), with no very illuminating results. If no restrictions are placed on the covariances we can generate counter-examples to the proposition that the two are equal. But we suspect that we are neglecting true restrictions among the covariances (one set implying values for another set) and, further, that the case of large N would give more useful results.

30 For the calculation for the U.K. in 1913, see D. N. McCloskey, Markets Abroad and British Economic Growth, 1820–1913, ch. 1 (MS available on request) p. 18.

31 J. W. Angell, The Theory of International Prices (Cambridge, Harvard University Press, 1926) p. 381. Later Angell conceded in part the point made below, although he believed (p. 392) that ‘it cannot be adequate to explain the comparatively quick adjustments [of domestic to international prices] that actually take place’.

32 Bertil Ohlin, Interregional and International Trade, rev. edn. (Cambridge: Harvard University Press, 1967) p. 104. His italics, question mark added; first edn., 1933. Contrast Jacob Viner’s Canada’s Balance of International Indebtedness 1900–1913 (Cambridge, Harvard University Press, 1924) p. 210: ‘The prices of services and what may be termed “domestic commodities”, commodities which are too perishable or too bulky to enter regularly and substantially into foreign trade, are wholly or largely independent of direct relationship with foreign prices. World price-factors influence them only through their influence on the prices of international commodities, with which the prices of domestic commodities, as part of a common price-system, must retain a somewhat flexible relationship’ (his italics). Although this is an improvement on the earlier formulation by Cairnes (quoted by Viner on the next page) that ‘with regard to these, there is nothing to prevent the widest divergence in their gold prices’, it falls short of a full analysis of what is meant by ‘direct’ and ‘somewhat flexible’, an analysis provided by Ohlin. In long-run equilibrium the distinction between direct and indirect is beside the point and the relationship of domestic to international prices is not even somewhat flexible. Viner’s work incidentally, is one of a series of books on the balance of payments published in the Harvard Economic Studies in the 1920s and 1930s under the influence, direct or indirect, of Taussig: J. H. Williams, Argentine International Trade under Inconvertible Paper Money: 1880–1900 (1920); Viner (1924); Angell (1926); Ohlin (1933); Harry D. White, The French International Accounts, 1880–1913 (1933); and Beach (1935). Students of the history of economic thought will find it significant that of these Ohlin, who acknowledges explicitly his debt to the Stockholm School (among them Cassel, Heckscher, and Wicksell, all of whom emphasised the intimate relationship between domestic and international prices), broke most sharply with Taussig on this issue.

33 The notion of an ‘Atlantic Economy’, incidentally, receives support from these figures: the average correlation of French with other retail price indexes, a crude measure of the appropriateness of including a country in the Atlantic economy, is 0·36, while the same statistic for the United States is 0·37; on this reading, it would be as appropriate to exclude France from the economy of Western Europe as to exclude the United States.

34 We have passed by, for example, the issue of how unified were the markets for assets. The correlation between the annual changes in the British and American long-term interest rates 1882 to 1913 used in the model fitted below was 0·36, and could no doubt be improved by a closer attention to gathering homogeneous data than we have thought necessary for now. Michael Edelstein, for example, reports in his ‘The Determinants of U.K. Investment Abroad: The U.S. Case’ (unpublished MS, p. 10n) a correlation coefficient of 0·77 between annual changes in the levels of yields on first-class American railway bonds offered in London and in New York from 1871 to 1913, a period including years before the refixing of the sterling–dollar exchange rate in 1879. The discount rates of central banks may be taken as a rough measure of the short-term interest rate. The recent revisionist literature on the gold standard has emphasised the close correlations between these rates in different countries. Triffin (op. cit., p. 9), for example, quotes Bloomfield, approvingly, to the effect that ‘the annual averages of the discount rates of twelve [European] central banks reveal the … interesting fact that, in their larger movements at least, the discount rates of virtually all the banks tended to rise and fall together’ (A. I. Bloomfield, Monetary Policy under the International Gold Standard, as cited, p. 35). Bloomfield and Triffin attribute the parallelism to a corresponding parallelism in the business cycles of the nations involved, but the finding can also be interpreted as evidence of direct or indirect arbitrage in the international capital market. Lance E. Davis’ finding that the internal American capital market was poorly arbitraged in this period, suggests that for America at least arbitrage was little better within than between countries (Davis’ work is summarised in his contribution to R. W. Fogel and S. L. Engerman, The Reinterpretation of American Economic History [New York, Harper and Row, 1971], ‘Capital Mobility and American Economic Growth’, pp. 285–300). The widely-believed assertion that domestic British industry was starved of funds in favour of British investment in Argentine railways and Indian government bonds can be given a similar interpretation.

35 The evidence is described in the footnote to Table 16.2. The interest rate on three-month bankers’ bills (Mitchell, Abstract of British Historical Statistics (Cambridge University Press, 1962), p. 460) performed better than the consol rate, and was used here.