Technical Indicator Wisdom 6

The best time to buy a share is near support levels.

Golden rules are merely old, general rules of thumb. Each rule usually has an exception and often a rule that is the exact opposite. Remember this when creating a personalized set of trading rules.

There is a story about a businessman who had a thriving multimillion dollar business in 2006. He gloated in the media about the book value of his profits, business, and personal investments. He intimated that he could do no wrong. To prove this to his colleagues, he mortgaged his house and borrowed as much as he could and bought only the best performing equities.

To begin with, prices rose steadily, but he did not know, like many thousands other investors, that a market correction was about to hit the market. Had he known this, he would have cut his losses when prices were on the slide. Instead, he tried to rescue his business by mortgaging it to the bank. Things went from bad to worse and he had to sell his investments. He shot himself.

Investor greed is often compounded by a relative time problem.

Without doubt, two years of continuous decline, underperformance, and even sideways movement feels like a lifetime. The temptation to boost growth is powerful by acquiring higher risk—higher return securities. If others can make money, why not me? Perhaps it is time to try something else? The following text looks at general principles in trading.

Please be aware that there is a difference between rules and strategies.

Basic Guiding Principles and Rules

Investment, as distinct from speculation, is a long-term operation. Day trading means to acquire securities for a single day, which implies even more strategy and tighter controls on entry and exits.

This is the essence of this volume, but if traders are to select securities for the long term, how do they go about selecting them? Theory states that you should first set up a portfolio of unit trusts, followed by investing in index stocks. Then, this is followed by selecting specific shares from across different sectors. The following rules and principles are meant as guiding mechanisms and will vary between investors or traders, according to their specific needs and objectives.

General Trading Rules

These age-old rules are used extensively by Wall Street traders and are worth noting.

• Rule 1: The company’s business has to be stable and within an expanding industry.

• Rule 2: Invest in companies with a market capitalization of not less than $10 million.

• Rule 3: Earnings growth (EPS) must be steady for at least a three-year period and dividend payments should be at least half the earnings growth, i.e., the company policy should be at least a two times dividend cover.

• Rule 4: Management must display sound, entrepreneurial flair.

• Rule 5: Buy whenever possible through rights issues as these almost invariably temporarily reduce share prices.

• Rule 6: Buy shares in a market that is liquid and trades regularly.

• Rule 7: There is no mathematical formula for deciding the right price. It is a matter of judgment, but good news can push up a share price and bad news can depress it. Timing a purchase or sale needs patience. There is, however, a formula to calculate a fair price.

Price:Earnings Ratio = Share Price ÷ EPS

Therefore, if the PE ratio and EPS are known factors, then the formula can be adjusted as follows:

Share price = Price:Earnings ratio × EPS

For instance, if Company X is trading at a PE ratio of 10 times and its latest EPS is 50 cents a share, a fair share price is 500 cents. If the market price is less, the share is trading at a discount to its fair value. If the share is higher than the fair value, it is trading at a premium. The formula can also be used as a means of working out a future price. For instance, if the investor believes the current PE ratio is fair, a 15-percent increase in EPS could see the above example achieve the following share price:

Share rice |

= |

Price:Earnings Ratio |

× |

EPS |

|

= |

10 |

× |

(50 cents × 15% growth) |

|

= |

10 |

× |

57.5 |

|

= |

575.50 cents |

|

|

In addition, if you use the average three-year PE and multiply that by the forecasted EPS, you can get a second share price. The two calculated fair values effectively give you a trading range. The share price is fore-casted to be 575.5 cents within a 12-month period.

• Rule 8: Ascertain all the company’s activities as one subsidiary may wreck profits for a few years; that is, you should give each division a value and as such, calculate whether the sum of the parts is greater than the whole.

• Rule 9: Avoid industries with volatile earnings records, such as motor or textiles.

• Rule 10: Choose consumer goods shares in preference to capital goods and shares that are capital rather than labor intensive.

• Rule 11: It rarely pays to buy shares in companies where the directors are selling and, conversely, buy shares where directors are buying.

Time Tested Guiding Principles

If you are new to investing and trading, it is important to recognize one of the truths of investing:

Stock and bond prices will continuously move in a contrary cycle to each other.

While it may be difficult to accept these fluctuations, the tougher part for many traders is coming to terms with yet another investment truth:

There is little you or anyone else can do to predict with any degree of accuracy when, how fast, and how much prices will decline—or bounce back.

Since market volatility is always present in stock and bond trading, it is the sensible trader whose program is always prepared to deal with market movements. Once you’ve developed an investment mix that suits your personal goals, time horizon, and risk tolerance, you should stick with it. In other words, find what works for you and “stay the course,” even though the most trying conditions.

Easier said than done, right? To assist traders, here are simple guiding principles to consider prior to investment actions. Investment in equities does not have to be difficult, especially if you follow a few simple time-tested practices and avoid a few common trading emotions.

Some Common Trading Emotions

• Panic. It is human nature to panic at the first sign of trouble in the market. The natural reaction is to become nervous and want to revise the investment portfolio. Bear trends can cause even the most experienced investor to have second thoughts. I stress again, any losses incurred are only “on paper” until you actually sell your shares. Getting caught up in market fever might encourage you to buy when the market is high and to sell when markets are low which the reverse of a common sense approach is.

• Market fever. Whether up or down, market direction must never dictate a portfolio mix. When creating a sound long-term investment program, rely on factors outlined in this volume, including investment goals, time horizon, risk tolerance, and personal financial situation.

• Abandoning strategy. It is enticing to sell an investment that falls in value without warning. Resist the temptation. Over time, shares have offered the highest returns and the greatest protection against inflation. Bonds offer higher income, but are subject to changes in interest rates. Cash reserves (such as money market funds and CDs) may protect your savings against daily price declines, but do little in the long run to preserve the spending power of savings.

• Churning your portfolio. As a general rule, do not make sudden shifts in a portfolio if the market is falling. Most experts will state that moving money from shares and bonds to more conservative investments in the hope of avoiding a loss or finding a gain is seldom successful.

• Invest regularly. It is often better to invest gradually, making necessary changes over time in the allocation of assets to shares, bonds, and cash reserves. If the investment continues to be a worry and is keeping the investor awake at night, “sell to the sleeping point.” Gradual moves should be limited to 15 percentage point increments, i.e., an investor with a portfolio consisting of 80 percent shares and 20 percent gilts, can move (if equities are worrying him) to a 65 percent share, 20 percent bonds, and the remainder in cash. This practice is called cost averaging and allows investors to buy more fund shares when prices are low and fewer shares when prices are high.

• Be diversified. Maintaining an investment mix of shares (for growth), bonds (for income), and short-term reserves (for stability) is a sensible way to hedge against many of the risks associated with investing. Today’s topsy-turvy markets serve to emphasize the benefits of a diversified investment mix. Without doubt, when diversification is used, the rewards associated with one asset class (for instance, income from bonds) can help to offset the risks from another (such as a decline in the price of shares).

• A key benefit of unit trusts is its diversification, which enables investors to have a stake in many shares and/or bonds through a single fund; locally and overseas.

![]() However, it is also wise to diversify among different types of assets by including shares, bonds, and money market funds in a portfolio. This lowers your risk of losing money because of poor performance by one market.

However, it is also wise to diversify among different types of assets by including shares, bonds, and money market funds in a portfolio. This lowers your risk of losing money because of poor performance by one market.

• Look before you leap. Every listed company is required to send potential investors a prospectus. Read it carefully, checking the fund’s objective, costs, and long-term performance in comparison to its competitors. Call the company and speak to the directors (the company secretary is usually available) and ask questions about any issues that are not obvious or understood.

• Reinvest earnings. When the investor buys shares, he or she can have earnings (dividends) sent to him or automatically reinvested. By electing the latter, earnings are turned into equity which can then generate more earnings. Reinvestment is an effective way to help investments grow faster.

• Be realistic. The returns achieved by the three classes of financial assets (shares, bonds, and cash) over the past 10 years have provided investors with substantial capital gains. Looking ahead, however, it is important to have realistic expectations and not to assume the high returns of the past decade will be repeated in the next decade.

• Remember “no pain, no gain.” The pursuit of higher returns is always accompanied by higher risk. When investing in shares or gilts, expect losses in some years. However, over the long haul, past results have proven that short-term risks have been worth taking when aiming for higher long-term gains.

• Be patient. As an investor, the greatest ally is time. Once a personal strategy has been chosen, stick to it, even when markets decline. The exception is when circumstances demand some readjustments. Over time, risk of losing money declines and the potential for profit increases.

• Reassess periodically. Market movements change the value of an investment. It is important to maintain the portfolio percentage mix by regularly rebalancing the portfolio. Do this at least once a year.

General Stock Strategies

Investment Process

The following four steps provide a basic overview.

Stock Selection

The key to profitable trading is to select companies that meet your criteria. For instance, if you want to buy quality stocks, you would have to conduct research focusing on quality stocks. In a nutshell, research is always the starting point in share selection. This includes analysis of financial strength, the company’s products, services and other variables that may affect the company’s earnings growth. For example, Coca-Cola’s product is a household brand name and recognized worldwide. Because it has consistently generated 15 to 20 percent growth in earnings in the past 20 years, it is very likely that Coke will be profitable in the next 20 years. In general, as a company’s profit grows, so do the share prices.

There are three processes in picking shares for a portfolio:

• Identification: Identify stocks from sectors that you are interested in.

• Research: Conduct research on these companies to narrow the list to a manageable size—not more than 10 stocks at a time.

• Selection: Select each of the stocks from different industries for diversification.

Identifying Stocks

To get the trader started, there are three recommended ways to identify stocks.

• Identify companies that manufacture the favorite things in your daily life, such as soft drinks, shoes, clothes, or computers and make sure they are publicly traded companies by checking the labels and packaging of the products.

• Get company names from work places where you, your friends, relatives, and neighbors have firsthand experience about the quality of the company.

• Use stockbrokers’ research as a reference library to start share selections. From the top 10 stocks recommended, choose those that you feel most comfortable with.

Researching Stocks

• After identifying the stocks you are interested in, it is crucial to conduct extensive research on these companies. To meet investing objectives, it is important to set up criteria to narrow the long list of companies. Here are some factors to consider:

![]() Narrow down your stock selections to the companies in the top 20 industries.

Narrow down your stock selections to the companies in the top 20 industries.

![]() Select those companies with a projected annual sales and earnings growth of 15 percent or higher over the next five years; then, the share price will be likely to double in about five years.

Select those companies with a projected annual sales and earnings growth of 15 percent or higher over the next five years; then, the share price will be likely to double in about five years.

![]() Choose stocks with return on equity of 15 percent or higher, which is slightly above the historical market average.

Choose stocks with return on equity of 15 percent or higher, which is slightly above the historical market average.

![]() Avoid stocks with PE’s higher than its growth rate. Too high of a PE means that the share price is overvalued.

Avoid stocks with PE’s higher than its growth rate. Too high of a PE means that the share price is overvalued.

Diversification

How many stocks should the investor have in his portfolio? I believe that only stocks that the investor knows and has researched should be good enough to become part of his long-term strategic portfolio. Therefore, start with a manageable five shares, each in a different industry.

Later, the investor can work his way up to 10 stocks. In the long term, the amount of shares in the portfolio should be limited to the time that the investor has to keep track of.

Owning lots of stocks will not significantly reduce risk.

Buying Stocks

There are three main methods of buying stocks from the exchange.

• Market order: Buy a stock at the current market price. This method is the most common.

• Limit order: Buy a stock when it reaches a target price, which is normally below the current market price.

• Stop order: Buy a stock when it rises to a target price above the current price. This is used to protect gains in a short stock position.

Keeping track of company news, earnings reports, and economic conditions are essential for profitable investing. Any new development of news can dramatically change the price of shares.

Monitoring the news will give the investor indications of the health of the industry he or she is invested in. They may want to lighten their stocks if the ratios become less attractive, such as supply becoming more than demand. To monitor stock investments, I believe that financial websites are the only answer.

Selling Stocks

When is a good time to sell other than when you need the money? U.S. Investment Guru Warren Buffett’s answer is “almost never.” He once said, “If you don’t want to own a stock for 20 years, why even own it for 2 minutes.”

Develop Specific Strategies

Have a clear, concise and well-defined investment planning process. Many investment advisors divide the entire planning process into clearly defined steps, which cannot be separated. Instead of a straight line, it must be understood that the process is a continuous loop, but that each step must have its own set of prerequisites. However, these steps do provide a framework for decision making as an investment strategy is developed.

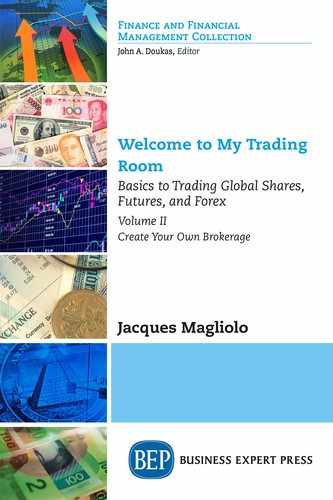

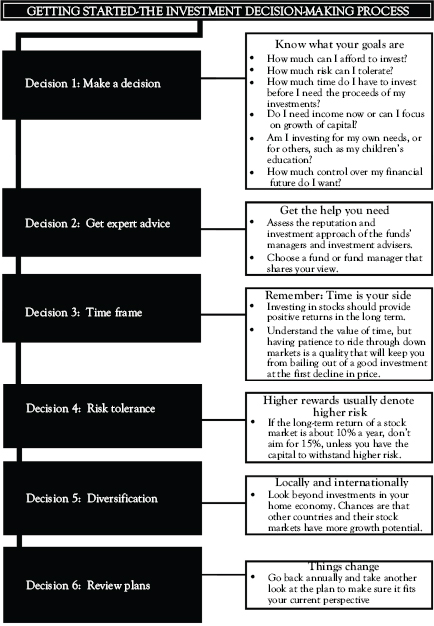

Another way to look at the investment decision-making process is as follows:

• A clear definition of objectives, time horizon, and risk tolerance goes a long way toward suggesting the appropriate investment strategy. The better that an objective can be defined, the better the plan that can be drafted to meet these objectives.

Of course, in real life everyone will have different and distinct financial goals, each with different parameters. For instance, a young person just starting out in a career is likely to have very different goals than an older couple who may be focused on retirement. Each objective is bound to have different time horizons and risk parameters.

The monetary goal must be a straightforward process.

• The investor must understand what he or she has before he or she can plan for the future. Therefore, as a first step, an inventory should be made of all resources, including pension plans, social security, and immovable property. Add in any other planned investments.

• This is followed by an estimation of a projection of the investor’s future income and capital needs. This must be done in today’s dollar value. In other words, estimate the average inflation rate in 30 years’ time.

• Add an appropriate inflation adjustment. This will give you an inflation-related dollar target.

• From this information an investor can determine his minimum required rate of return on his current assets and planned investments.

• This required rate of return must be feasible and attainable and within the investor’s risk tolerance.

• If the rate of return is not feasible, this indicates that the investor is living beyond his or her means and he or she has to go back and make adjustments in his or her lifestyle or, alternatively, increase planned investments. Above all, the investor must be realistic when he or she writes down his or her long-term requirements.

Often investors feel driven to take excessive risk when they are unable or unwilling to invest enough to meet their goals. The elderly often become victims of fraud when they see that their existing assets will not be enough to support their lifestyle. Then they often lose everything.

Age and financial situations will impact on how investors set their goals. It’s silly for 25-year-olds to attempt to exactly forecast their retirement budget. At that age, few of us know how our lives and careers will develop. In addition, the very long timeframes mean that if our estimates of rate of return, inflation, or expenses are off just a little, the resulting error will be enormous. While our future may be a blank sheet, the need to provide for it is not.

Take heart, it is possible to design a portfolio that has an expected rate of return adequate for the investor’s required needs. However, know this from the outset—an investment return has to be higher than both the inflation rate and that achieved by the relatively low risk yield achieved on bonds. For instance, if a bond rate is 10 percent, invest in equities if a rate of return of less than that is required?

The next question is: Can the investor live with the risk required to meet those goals? If he or she cannot, there is no other alternative but to go back and adjust his or her lifestyle or increase planned investments.

Get Expert Help

If this sounds like a complicated exercise, do not panic. There are dozens of software packages to do these calculations and the main selection process for stock selection.

As for the determination of an investor’s lifestyle, again—there are many available programs that allow for instant comparisons of alternative scenarios. These enable the investor to see instantly if his assets will support his desired lifestyle and what rate of return will be necessary to keep him from running out of funds. These can also determine how much risk he or she will have to assume to get the desired rate of return.

These programs make quick work of budgeting, pension forecasts, inflation adjustments, assets available, time to go to objective, rates of return required to meet objectives, and risk required to meet rate-of-return requirements. These also enable the investor to build in known expenses like replenishment of household goods (depreciation of current assets) and expected future receipts like sale of property or inheritance. The investor can also plan for changes in tax rates and conduct his own scenario planning.

In addition, these programs do a great job of pulling together many elements of the problem and graphically illustrating the possibilities. Getting expert help is a starting point, but, ultimately, it is important for the investor to do these planning exercises himself.

Set a Timeframe

Obviously, the sooner one starts investing for the future, the better. Time is, therefore, only on an investor’s side for a period, after which it becomes another constraint. Regular, small savings early in an investor’s career will grow to meaningful balances given the magic of compounding. So, 25-year-olds may be content with a goal of saving 20 percent of their gross income, obtaining a rate of return of at least five percentage points over inflation, and avoiding taxes on their investments. If they continue this discipline throughout their careers, they may reasonably expect to attain financial independence and security.

The idea of saving 20 percent of gross salary may seem a little revolutionary to many of today’s consumers.

When an investor is in his or her 20s, retirement may seem far off and almost impossible to forecast financial needs, determine where he or she would like to live, in what style, what size house he or she may want, how many children he or she think they will have to put through university, and other needs. However, as he or she get closer to 50 it gets easier to forecast retirement requirements, as he or she will already have some assets to inventory.

Putting numbers to requirements, including assets available, extent of needs, past investment success, time remaining to retirement, future investment levels, and required rates of return become easier. However, the more assets the investor has by the time he or she is 50, the easier it is to plan for the retirement. So, effectively, invest during the 20s to make it easier to plan in the 50s.

There is still some hope for those with retirement plans. It is not too late to begin a serious investment program. All along the way the investor will need to adjust constantly, particularly under a globalized world and increasingly merging stock markets. Undoubtedly, new requirements will develop and a stronger need will emerge for better research to take place into the investment planning process. A good plan is flexible, but focused and disciplined at the same time.

Time horizon is a critical factor in investment planning, but often not properly understood. Time horizon ends when you plan to liquidate an entire portfolio to meet a goal. For instance, if one is saving for a down payment on a house in two years, the time horizon left is two years. However, if one is investing for retirement, the time horizon is the rest of your life.

One of the most insane ideas regularly foisted upon investors is the idea that retirees should invest only for income and become more conservative. In other words, invest in blue chips for the dividend income and safety. Under a globalized world, this often does not apply.

The following is clear.

A horizon under three years becomes a speculative one in the stock market. In the short term, risk to one’s retirement plan is too high.

Rule of thumb: Remember that market risk falls as the time horizon increases and analysis shows that risk actually falls as the square root of the time horizon. That means that the difference between the best case or worst case expectations for a 1-year time horizon is only one-third as large after nine years, or one-fourth as large after 16 years. With a very long time horizon, the worst case expectation in the stock market may be better than the best case with “safe” assets.

Investors who anticipate living off their capital after retirement should consider that they have two time horizons.

• In the short run they will need income.

• In the long run they will need a growth of capital and income.

They should arrange their asset allocation accordingly.

Risk tolerance is the final dimension of the goal-setting process. Investors do face a far greater risk of outliving their capital than losing it in a properly designed, equity-based, global asset-allocation plan.

On the other hand, excessive risk at the portfolio level can lead to real and permanent losses. Where a risk is extremely high (speculative shares), an investor will need to achieve the highest rate of return per unit of risk. Thus, even if an investor has a high tolerance for risk, he or she should aim to get rich, or at least achieve financial independence.

What often happens when the inevitable market decline occurs, investors begin to feel betrayed and frightened. In this frame of mind, investors are ready to do the worst possible thing: sell and retreat to the “safety” of cash.

Don’t Abandon Long-Term Plans

The investor locks in losses and paper losses become real. The recovery will come and he or she will have lost their long-term objectives.

Market risk means that sometimes equities will go down. No one can really determine when that will happen. In essence, if the investor is in the market, he or she must get used to the idea that there will be future declines. Alternatively, if he or she cannot get used to this idea, do not invest in shares. It is therefore better to have not been in the market at all than to panic and sell when the market slumps.

Investors should decide in advance how much risk they are willing to tolerate. Meanwhile, this can be defined in many different ways.

For instance:

• An investor could say that he or she wants to be 95 percent certain that he or she will never have a loss exceeding a given amount.

• The global investor could accept a risk level that is mid-way between the S&P 500 and local short-term bonds.

• He could also tolerate whatever risk is required to achieve a long-term result of 3 percent better than the S&P 500.

Comment on Risk-Reward Relationship

A clear statement of objectives, risk tolerance, and time horizon should be written down and form the first portion of a policy statement for an investment strategy.

• Every plan should have a policy statement, which should be reviewed regularly (at least once a year). This statement will help the investor to focus on achieving goals, which will in turn help him keep a clear head in times of panic selling.

• If investors think they can administer long-term investment plans without stressful days, they are simply not ready to enter the world of stock exchanges.

• The next step in developing a strategy is to begin to formulate an asset-allocation plan that will satisfy the requirements we have just laid down.

Diversify

This is a process of taking a portfolio and reducing risk of exposure through a number of technical and fundamental processes. These are discussed in greater length throughout these volumes, but it is sufficient to state that a portfolio should match both where the investor is now and where he or she wants to be when he or she retires.

The challenge is to find the proper mix of investments with just the right amount of his or her money in a variety of investments.

To find the investment mix that’s right for the investor, start by understanding investment essentials. The focus of these volumes is to expand on each of these issues, in detail and mathematically. Meanwhile, learn the following basic principles about diversification:

• The key step in managing risk is to decide how to allocate investment funds among the three primary classes of financial assets, namely cash reserves, bonds, or shares—or a combination of these.

• The first step should always be to assess asset classes briefly before investigating potential risks and rewards. Once this has been completed undertake an asset allocation. Keep in mind that risk is always present in investing. Risk cannot be eliminated, but it can be managed. There are three basic pointers to keep in mind:

![]() Diversification can protect the investor against risks from a single stock or bond, but not against market and inflation risks.

Diversification can protect the investor against risks from a single stock or bond, but not against market and inflation risks.

![]() Shares have historically offered the highest annual returns, but with substantial short-term market risk.

Shares have historically offered the highest annual returns, but with substantial short-term market risk.

![]() Time has a moderating influence on stock and bond market risk. The longer one holds an investment, the more likely it will earn a positive return.

Time has a moderating influence on stock and bond market risk. The longer one holds an investment, the more likely it will earn a positive return.

• Cash reserves: Offer stability and provide income that rises and falls with short-term interest rate movements. These include treasury bills, bank deposits, convertible debentures, or money market instruments.

• Bonds (also called gilts): Interest-bearing debt obligations issued by corporations, government (central to local), and utilities. Bonds represent a loan to the issuer and provide income during their lifetime, plus a promise to repay principal upon maturity. Although bonds generally offer higher and steadier income than cash reserves, their principal value fluctuates as interest rates change. In general, when interest rates rise, bond prices decline, and when interest rates decline, bond prices rise.

• Shares: These represent ownership interest in a corporation. Stocks offer the potential for current income (from dividends) and capital growth (from an increase in value). However, stocks are more susceptible to short-term price risks (i.e., stock prices fluctuate sometimes sharply—over shorter periods of time).

While this section concentrates on the equity market, it does not suggest that investors ignore these alternative markets in a diversification strategy.

• While shares and bonds may offer higher returns than cash reserves, they also expose you to higher levels of risk. This risk-reward trade-off is a key consideration in investing: in order to pursue higher returns, investors must be willing to assume additional risk.

• Individual shares and bonds expose investors to specific risk, i.e., the risk that problems with an individual company or bond issuer will reduce the value of your investment dramatically. Specific risk can be eliminated through diversification using unit trusts or mutual funds.

• Diversification among many stocks and bonds will greatly diminish the impact of a single stock or bond. However, diversification does not remove risk from market movement caused by investor perceptions.

Chapter 7 is an assessment into how market experts conduct research.