AU 341: The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern

AU-C 570: The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern

AU EFFECTIVE DATE AND APPLICABILITY

| Original Pronouncements | Statements on Auditing Standards (SASs) 59, 64, 77, and 96. |

| Effective Date | These statements are now effective. |

| Applicability | Audits of financial statements in accordance with generally accepted auditing standards (GAAS). |

NOTE: The Statement applies in the audit of any type of entity. It is applicable to both profit-making and not-for-profit organizations. Thus, it would apply, for example, in the audit of a municipality. Also, the Statement applies to both GAAP (generally accepted accounting principles)–basis financial statements and OCBOA (Other Comprehensive Bases of Accounting)–basis financial statements, (e.g., cash or modified cash basis, tax basis, or regulatory basis). However, it does not apply to liquidation-basis financial statements.

|

AU-C EFFECTIVE DATE

SAS No. 126, The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern, is effective for audits of financial statements for periods ending on or after December 15, 2012.

SAS No. 126 does not change or expand SAS No. 59, as amended, in any significant respect. The Auditing Standards Board (ASB) has moved forward with the clarity redraft of SAS No. 59, as amended, so that it is consistent with the format of the other clarified SASs that were recently issued. However, the ASB decided to delay convergence with International Standard on Auditing 570, Going Concern, pending the Financial Accounting Standards Board’s (FASB’s) anticipated development of accounting guidance addressing going concern.

AU-C DEFINITION OF TERM

Source: AU-C 570.07

Reasonable period of time. A period of time not to exceed one year beyond the date of the financial statements being audited.

OBJECTIVES OF AU SECTION 341

The “going concern” concept has long been a tenet of financial accounting. It has been called an assumption, a concept, a basic fixture, and a postulate, and has usually been stated somewhat as follows:

Continuation of entity operations is usually assumed in financial accounting in the absence of evidence to the contrary.

The auditor has an obligation to make an assessment of a client’s ability to continue as a going concern.

Note that the section does not mandate any procedures especially and solely directed to searching for conditions or events that would indicate a going concern problem. The obligation is to assess the information obtained from procedures used for other purposes.

Report modification may result solely from substantial doubt about continued existence regardless of whether there is any uncertainty associated with the recoverability and classification of recorded amounts. Under this section, continued existence has a separate status. There could be substantial doubt about continued existence even when there is no question about recoverability and classification.

When the audit report is modified for a material uncertainty, the opinion is unqualified, but disclosure of the going concern uncertainty is made in an explanatory paragraph that follows the opinion paragraph. This type of uncertainty is the only one that requires a report modification.

The section states that “a reasonable period of time” is a period not to exceed one year beyond the balance sheet date.

OBJECTIVES OF AU-C SECTION 570

AU-C Section 570 states that:

. . . the objectives of the auditor are to

FUNDAMENTAL REQUIREMENTS

Auditor’s Responsibility

The auditor should evaluate whether there is substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time, not to exceed one year beyond the date of the financial statements being audited (i.e., the balance sheet date). However, the auditor is not required to design audit procedures specifically to identify conditions and events that indicate a “going concern” problem.

Procedures Required

The auditor should consider whether the results of his or her usual audit procedures indicate that there could be substantial doubt.

Additional Procedures

If the auditor has substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time, he or she should:

Prospective Financial Information

If prospective financial information is significant to management’s plans, the auditor should obtain that information and should consider the adequacy of support for the significant assumptions. The auditor should pay special attention to those assumptions that are:

Auditor Conclusions—Substantial Doubt Exists

If the auditor concludes that there is substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time, he or she should (1) consider whether the condition is adequately disclosed and (2) modify the auditor’s standard report by including an explanatory paragraph (following the opinion paragraph) or disclaim an opinion. The auditor’s conclusion should be expressed in the report using the terms “substantial doubt” and “going concern.”

Auditor Conclusions—Substantial Doubt Does Not Exist

If the auditor concludes that substantial doubt does not exist about the entity’s ability to continue as a going concern for a reasonable period of time, he or she should consider whether the matter needs to be disclosed.

Inadequate Disclosure

If the auditor concludes that the entity’s disclosures about its ability to continue as a going concern for a reasonable period of time are inadequate, the auditor’s report should be qualified or adverse because of a departure from GAAP.

Documentation Requirements

If, after considering the aggregate of events and conditions identified during the audit, the auditor believes that there is substantial doubt about the ability of the entity to continue as a going concern for a reasonable period of time, the auditor should document all of the following:

- If substantial doubt exists, document the possible effects of the conditions or events on the financial statements and the adequacy of the related disclosures.

- If substantial doubt is alleviated, document the conclusion about whether disclosure of the principal conditions and events that led the auditor to believe there was substantial doubt is needed.

INTERPRETATIONS

Eliminating a Going Concern Explanatory Paragraph from a Reissued Report (August 1995)

An auditor may be asked by the client to reissue the audit report and eliminate the going concern paragraph. Such requests usually occur after the going concern matter has been resolved. The auditor has no obligation to reissue the audit report. However, if the auditor decides to reissue the report, he or she should

TECHNIQUES FOR APPLICATION

Procedures

The auditor’s evaluation of whether there is a substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time (not to exceed one year beyond the balance sheet date) is based on his or her knowledge of relevant conditions and events that exist at, or occurred before, completion of fieldwork. It is not necessary for the auditor to design audit procedures specifically to identify conditions and events that indicate a going concern problem. Regular auditing procedures are sufficient.

Regular auditing procedures that may identify conditions and events that indicate a going concern problem include the following:

Indications of Going Concern Problems

Regular audit procedures such as those described above may reveal conditions and events that indicate there could be substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time. Examples of these conditions and events (going concern warning signs or red flags) are as follows:

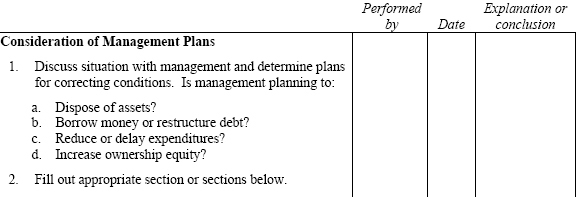

Consideration of Management’s Plans

If, after considering the conditions and events described above, the auditor believes there is substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time, he or she should consider management’s plans for addressing these conditions and events.

Management’s plans may be classified as follows:

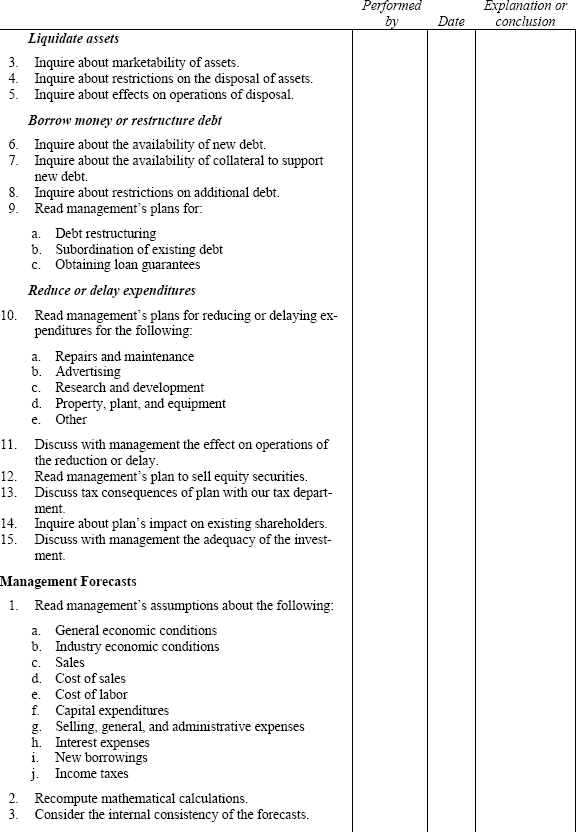

Plans to Dispose of Assets

If management plans to dispose of assets, the auditor should consider the following:

Marketability of Assets

The auditor should do the following:

Restrictions on Disposal of Assets

Under certain circumstances, the entity may be prohibited from disposing of assets. If management contemplates disposal, the auditor should do the following:

Effects of Disposal

The auditor should consider possible adverse effects of the proposed disposal of assets. He or she should do the following:

Plans to Borrow Money or Restructure Debt

If management plans to borrow money or restructure debt, the auditor should consider the following:

Availability of Debt Financing

The auditor should do the following:

Availability and Sufficiency of Collateral

If there is a question about an entity’s continued existence, it is probable that it will not be able to borrow funds without collateral. The auditor should consider the availability and sufficiency of assets as collateral. Assets to be considered are the following:

Restrictions on Additional Borrowing

Existing loan agreements may prohibit the entity from borrowing additional funds. To determine this, the auditor should do the following:

Existing or Committed Arrangements

If there are existing plans or commitments to modify existing loans or to guarantee existing or new loans, the auditor should do the following:

Plans to Reduce or Delay Expenditures

When a question arises about the continued existence of an entity, it is not uncommon for the entity to reduce or delay expenditures, such as the following:

If management plans to reduce or delay these expenditures, the auditor should do the following:

Plans to Increase Ownership Equity

When a question arises about the continued existence, it is not uncommon for the entity to offer equity capital to an investor. Also, it is not uncommon for investors to search for entities in need of additional capital.

Ordinarily, in these circumstances, the entity will sell its stock to the investor at a discount from market value. In certain circumstances, the investor may have plans to bring profitable businesses into the troubled entity to use the troubled entity’s net operating loss carryforward. In these situations, the auditor should do the following:

The auditor’s concern is that the funds will be sufficient to ease the liquidity problem and to provide sufficient working capital.

Consideration of Management Forecasts

The auditor is not required to examine management forecasts; however, he or she should read these forecasts and apply his or her knowledge of the client. The auditor should pay special attention to cash flows and the implementation of management plans. The auditor is interested in whether the forecasts provide a reasonable basis for the belief that the entity will be in business a year from the current balance sheet date.

Obtain Management Assumptions

The auditor should ask management for its assumptions, especially assumptions about the following:

Sources of Management Assumptions

The auditor should ask management for sources for its assumptions in developing the prospective data, especially the following:

Possible sources for assumptions are the following:

When the auditor reads management’s assumptions, he or she may want to consider the following:

Internal Consistency of Assumptions

Management assumptions should be internally consistent. Examples of this internal consistency are the following:

Financial Statement Effects

Substantial Doubt Exists

If the auditor concludes, after considering management’s plans, that there is substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time, he or she should consider possible effects on the financial statements and the adequacy of the related disclosure. Disclosure might include the following:

Substantial Doubt Does Not Exist

After considering management’s plans, the auditor may conclude that substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time does not exist. In these circumstances, the auditor should nonetheless consider the need to disclose the conditions and events responsible for the initial doubt and any mitigating factors, including management’s plans.

Effects on the Auditor’s Report

If the auditor concludes that substantial doubt exists about the entity’s ability to continue as a going concern for a reasonable period of time, the auditor’s standard report should include an explanatory paragraph, following the opinion paragraph, to reflect that conclusion. In these circumstances, the auditor ordinarily expresses an unqualified opinion (see the next section, “Disclaimer of Opinion”). The auditor may no longer express a “subject to” opinion for any uncertainty (see Section 508, Reports on Audited Financial Statements). The auditor’s conclusion should be expressed using a phrase such as “substantial doubt about its (the entity’s) ability to continue as a going concern.” The report wording must include the terms “substantial doubt” and “going concern” and should be stated unconditionally.

The following (from AU 341.13) is an example of an explanatory paragraph:

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note X to the financial statements, the Company has suffered recurring losses from operations and has a net capital deficiency that raise substantial doubt about its ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note X. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Disclaimer of Opinion

Instead of issuing an unqualified opinion with an explanatory paragraph following the opinion paragraph, the auditor may disclaim an opinion if he or she concludes that there is substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time. A disclaimer of opinion is permitted at the auditor’s discretion, but never required.

Inadequate Disclosure

If the auditor concludes that the entity’s disclosures about its ability to continue as a going concern for a reasonable period of time are not adequate, the auditor’s report should be modified for a departure from generally accepted accounting principles. This may result in either a qualified (except for) or adverse opinion (see Section 508).

Prior Period Audit Report

The fact that the auditor is issuing a “going concern” report on the current period financial statements does not imply that a going concern problem existed in the prior period. Therefore, the auditor’s report on prior period financial statements presented for comparative purposes with the current period financial statements need not be changed.

Subsequent Period Audit Report

The auditor may have issued a “going concern” report on the prior period financial statements that are presented for comparative purposes with the current period financial statements. If the going concern problem has been resolved during the current period, the explanatory paragraph included in the auditor’s report on those prior period financial statements should not be repeated.

AU ILLUSTRATION

The following checklist may be used by the auditor to assess his or her doubt about a client’s ability to continue as a going concern and to evaluate management’s plans for addressing the issue.