AU 508: Reports on Audited Financial Statements

AU-C 700: Forming an Opinion and Reporting on Financial Statements

AU-C 705: Modifications to the Opinion in the Independent Auditor’s Report

AU-C 706: Emphasis-of-Matter Paragraphs and Other-Matter Paragraphs in the Independent Auditor’s Report

AU-C 600: Special Considerations—Audits of Group Financial Statements (Including the Work of Component Auditors)

AU-C 708: Consistency of Financial Statements

AU-C 805: Special Considerations—Audits of Single Financial Statements and Specific Elements, Accounts, or Items of a Financial Statement

AU-C 560: Subsequent Events and Subsequently Discovered Facts

IMPORTANT NOTE: The guidance in this section applies to audits of nonissuers. Auditors of issuers and public entities subject to Securities and Exchange Commission (SEC) rules should refer to the guidance in Public Company Accounting Oversight Board’s PCAOB No. 1, References in Auditors’ Reports to the Standards of the Public Company Accounting Oversight Board, for changes made to the guidance in this section.

AU EFFECTIVE DATE AND APPLICABILITY

| Original Pronouncements |

Statements on Auditing Standards (SASs) 58, 64, 79, 85, 93, and 98. |

| Effective Date |

These statements currently are effective. |

| Applicability |

Auditor’s reports issued in connection with audits of historical financial statements that are intended to present financial position, results of operations, and cash flows in conformity with generally accepted accounting principles (GAAP). |

|

The Statement does not apply to unaudited financial statements as described in Section 504, Association with Financial Statements. It also does not apply to reports on incomplete financial information or other special presentations as described in Section 623, Special Reports. |

AU-C EFFECTIVE DATE AND SUMMARY OF CHANGES

SAS No. 122, Codification of Auditing Standards and Procedures, is effective for audits of financial statements with periods ending on or after December 15, 2012.

AU-C Sections 700, 705, and 706 include auditor report changes and are closely integrated with AU-C sections 210, Terms of Engagement, and 580, Written Representations.

AU-C Sections 700, 705, and 706 supersede:

- AU Section 410, Adherence to Generally Accepted Accounting Principles

- AU Section 508, Reports on Audited Financial Statements, paragraphs .01–.11, .14–.15, .19–.32, .35–.52, .58–.70, and .74–.76

- AU Section 530, Dating of the Independent Auditor’s Report (as amended), paragraphs .01–.02

The primary changes pertain more to appearance and presentation than substance; however, they are significant. The clarified standards include auditor report changes:

- The description of management’s responsibility,

- The use of headings, and

- The introduction of two new terms—emphasis-of-matter and other-matter paragraphs—replacing the term explanatory paragraph.

The introduction paragraph will no longer reference either management’s or the auditor’s responsibility. The clarified SAS requires a new section titled “Management’s Responsibility for the Financial Statements.” This new section is required to describe management’s responsibility for the preparation and fair presentation of the financial statements in more detail than what was required in AU Section 508. The description includes an explanation that management is responsible for the preparation and fair presentation of the financial statements in accordance with the applicable financial reporting framework, and that this responsibility includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

The clarified SAS also requires a section headed “Auditor’s Responsibility.” This section requires a statement related to the auditor’s responsibility to express an opinion on the financial statements based on an audit and another statement that the audit was conducted in accordance with US GAAP or other standards, if applicable. This section replaces the “scope” paragraph.

The opinion paragraph will have the heading “Opinion.” The use of the heading clearly differentiates the opinion from the report. If the opinion is qualified, the opinion paragraph must be followed by a paragraph with the appropriate heading:

- Basis for Qualified Opinion

- Basis for Adverse Opinion

- Basis for Disclaimer of Opinion

If the auditor has other responsibilities, such as reporting on legal or regulatory requirements, additional guidance is provided.

Signature and dating of report remain essentially the same.

AU-C Section 706 introduces and describes two paragraphs in the auditor’s report:

1. An

emphasis-of-matter paragraph refers to a matter appropriately presented or disclosed in the financial statements. An emphasis-of-matter paragraph is any paragraph added to the auditor’s report that relates to a matter that is appropriately presented or disclosed in the financial statements.

Certain standards require an emphasis-of-matter paragraph, whereas other emphasis-of-matter paragraphs are added at the discretion of the auditor, consistent with current practice. However, all such paragraphs are to be considered emphasis-of-matter paragraphs, because they are intended to draw the users’ attention to a particular matter.

2. An other-matter as a paragraph included in the auditor’s report refers to a matter other than those presented or disclosed in the financial statements that, in the auditor’s judgment, is relevant to the users’ understanding of the audit, the auditor’s responsibilities, or the auditor’s report.

AU DEFINITIONS OF TERMS

Adverse opinion. An adverse opinion states that the financial statements do not present fairly the financial position, results of operations, and cash flows of the entity in conformity with GAAP. An adverse opinion is an opinion, even though negative, and cannot be expressed unless an audit in accordance with GAAS has been performed.

Audit. An audit, as referred to in the standard report, is an audit of historical financial statements performed in accordance with GAAS in effect at the time the audit is performed. GAAS includes the ten standards as well as Statements on Auditing Standards (SASs) that interpret those standards and, when relevant, the American Institute of Certified Public Accountants (AICPA) Audit and Accounting Guides.

Auditor’s standard report. The auditor’s standard report states that the financial statements present fairly, in all material respects, an entity’s financial position, results of operations, and cash flows in conformity with GAAP. It has a title that includes the word independent, and three paragraphs—an introductory paragraph that identifies the financial statements audited and the division of responsibility between the auditor and management, a scope paragraph that describes the nature of an audit, and an opinion paragraph that expresses the auditor’s opinion on the financial statements audited.

Continuing auditor. An auditor who has audited the financial statements of the current period and of one or more consecutive periods immediately prior to the current period.

Disclaimer of opinion. A disclaimer of opinion means that the auditor is unable to and does not express an opinion on the financial statements.

Explanatory language added to the auditor’s standard report. Certain circumstances, while not affecting the auditor’s unqualified opinion on the financial statements, may require that the auditor add an explanatory paragraph (or other explanatory language) to the report.

Qualified opinion. A qualified opinion states that, except for the effects of the matter(s) to which the qualification relates, the financial statements present fairly, in all material respects, the financial position, results of operations, and cash flows of the entity in conformity with GAAP.

Unqualified opinion. An unqualified opinion states that the financial statements present fairly, in all material respects, the financial position, results of operations, and cash flows of the entity in conformity with GAAP. This is the opinion expressed in the auditor’s standard report.

Updated report. A report issued in conjunction with the report on current period financial statements by a continuing auditor that takes into consideration information that the auditor has become aware of during the audit of the current period financial statements.

AU-C DEFINITIONS OF TERMS

Source: AU-C 700.11

Comparative financial statements. A complete set of financial statements for one or more prior periods included for comparison with the financial statements of the current period.

Comparative information. Prior period information presented for purposes of comparison with current period amounts or disclosures that is not in the form of a complete set of financial statements. Comparative information includes prior period information presented as condensed financial statements or summarized financial information.

Condensed financial statements. Historical financial information that is presented in less detail than a complete set of financial statements, in accordance with an appropriate financial reporting framework. Condensed financial statements may be separately presented as unaudited financial information or may be presented as comparative information.

General purpose financial statements. Financial statements prepared in accordance with a general purpose framework.

General purpose framework. A financial reporting framework designed to meet the common financial information needs of a wide range of users.

Unmodified opinion. The opinion expressed by the auditor when the auditor concludes that the financial statements are presented fairly, in all material respects, in accordance with the applicable financial reporting framework.

AU-C 705 Definitions

Source: 705.07

Modified opinion. A qualified opinion, an adverse opinion, or a disclaimer of opinion.

Pervasive. A term used in the context of misstatements to describe the effects or possible effects, on the financial statements of misstatements, if any, that are undetected due to an inability to obtain sufficient appropriate audit evidence. Pervasive effects on the financial statements are those that, in the auditor’s professional judgment:

- Are not confined to specific elements, accounts, or items of the financial statements;

- If so confined, represent or could represent a substantial proportion of the financial statements; or

- With regard to disclosures, are fundamental to users’ understanding of the financial statements.

AU-C 706 Definitions

Source: 706.05

Emphasis-of-matter paragraph. A paragraph included in the auditor’s report that is required by GAAS, or is included at the auditor’s discretion, and that refers to a matter appropriately presented or disclosed in the financial statements that, in the auditor’s professional judgment, is of such importance that it is fundamental to users’ understanding of the financial statements.

Other-matter paragraph. A paragraph included in the auditor’s report that is required by GAAS, or is included at the auditor’s discretion, and that refers to a matter other than those presented or disclosed in the financial statements that, in the auditor’s professional judgment, is relevant to users’ understanding of the audit, the auditor’s responsibilities, or the auditor’s report.

OBJECTIVES OF AU SECTION 508

The primary objective of this section is to help ensure the public’s understanding of the auditor’s role by requiring the auditor’s report to more explicitly address in nontechnical language the following matters: (1) responsibility assumed, (2) procedures performed, and (3) degree of assurance provided.

SAS 58 prescribed a new form of standard report for auditors and deleted all reference to “consistency,” eliminated “subject to” qualifications, and substituted “audited” for “examined.” It required all auditors’ reports to have a title that includes the word independent (for example, Independent Auditor’s Report).

In conjunction with deleting the routine reference to “consistency” in the auditor’s standard report, SAS 58 revised the second standard of reporting in the ten generally accepted auditing standards, as follows:

The report shall identify those circumstances in which such principles (GAAP) have not been consistently observed in the current period in relation to the preceding period.

Thus, the auditor does not include an explicit opinion on consistency in normal circumstances, but adds an explanatory paragraph to highlight an inconsistency.

SAS 79 eliminated the reporting requirement to add an explanatory paragraph for all uncertainties, except substantial doubt about ability to continue as a going concern (see Section 341, The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern).

The removal of the uncertainties reporting requirement culminated a long debate about the relevance of this form of reporting that was set in motion by the Financial Accounting Standards Board’s (FASB) Statement 5 on loss contingencies. Under GAAP, when an uncertainty is properly disclosed, the financial statements are not deficient and no audit report modification is warranted.

SAS 93, Omnibus Statement on Auditing Standards—2000, amends SAS 58 to include a reference to the United States of America as the country of origin of the accounting principles used to prepare the financial statements and the auditing standards that the auditor follows in performing the audit. This change was made because financial statements in conformity with US GAAP and audited according to US GAAS are increasingly available beyond US borders.

OBJECTIVES OF AU-C SECTIONS

AU-C 700 states that:

. . . the objectives of the auditor are to

a. form an opinion on the financial statements based on an evaluation of the audit evidence obtained, including evidence obtained about comparative financial statements or comparative financial information, and

b. express clearly that opinion on the financial statements through a written report that also describes the basis for that opinion.

AU-C 705 states that:

. . . the objective of the auditor is to express clearly an appropriately modified opinion on the financial statements that is necessary when

a. the auditor concludes, based on the audit evidence obtained, that the financial statements as a whole are materially misstated or

b. the auditor is unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement

AU-C 706 states that:

. . . the objective of the auditor, having formed an opinion on the financial statements, is to draw users’ attention, when in the auditor’s judgment it is necessary to do so, by way of clear additional communication in the auditor’s report, to

a. a matter, although appropriately presented or disclosed in the financial statements, that is of such importance that it is fundamental to users’ understanding of the financial statements or

b. as appropriate, any other matter that is relevant to users’ understanding of the audit, the auditor’s responsibilities, or the auditor’s report.

FUNDAMENTAL REQUIREMENTS: AUDITOR’S STANDARD REPORT

Components of Auditor’s Standard Report

The auditor’s standard report should include the following:

1. A title that includes the word independent (for example, Independent Auditor’s Report). A title is not required for an auditor’s report if the auditor is not independent. (Section 504, Association with Financial Statements, provides guidance on reporting when an auditor is not independent.)

2. An introductory paragraph with statements that:

a. The financial statements explicitly identified in the report as to title and date were audited.

b. The financial statements are the responsibility of the entity’s management.

c. The auditor’s responsibility is to express an opinion on the financial statements based on the audit.

3. A scope paragraph with statements that:

a. The audit was conducted in accordance with GAAS and an identification of the United States of America as the country of origin of those standards (e.g., auditing standards generally accepted in the United States of America, or US GAAS).

b. Those standards require that the auditor plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

c. An audit includes:

(1) Examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements

(2) Assessing the accounting principles used and significant estimates made by management

(3) Evaluating the overall financial statement presentation

d. The auditor believes that the audit provides a reasonable basis for the opinion.

4. An opinion paragraph that presents the auditor’s opinion as to whether the financial statements present fairly, in all material respects, the financial position of the entity as of the balance sheet date and the result of its operations and its cash flows for the period then ended in conformity with GAAP. The opinion should identify the United States of America as the country of origin of those accounting principles (e.g., accounting principles generally accepted in the United States of America, or US GAAP).

5. The manual or printed signature of the auditing firm and the date of the audit report, which is normally the date of completion of fieldwork.

The “AU Illustrations” section at the end of this chapter contains examples of the auditor’s standard report on financial statements covering a single year (Illustration 1) and on comparative financial statements (Illustration 2). The illustrations also contain examples of audit reports on comparative financial statements when the opinions differ between years (Illustrations 14 and 15).

Addressee

The auditor’s report may be addressed to the entity whose financial statements are being audited, its board of directors, or its shareholders. For an unincorporated entity, the report should be addressed as circumstances dictate. For example:

- Unincorporated entity. The report should be addressed to the partners, or to the general partner of a limited partnership, to joint venturers, or to the proprietor of a sole proprietorship.

- Audit of entity not the client of the auditor. When an auditor is retained to audit the financial statements of an entity that is not the auditor’s client, the report should be addressed to the one who retained the auditor and not to the directors or shareholders of the entity whose financial statements were audited.

NOTE: Under Section 301, Public Company Audit Committees, and the SEC’s related implementing Rule No. 33-8138, “Strengthening the Commission’s Requirements Regarding Auditor Independence,” the audit committee is “directly responsible for the appointment, compensation, and oversight of the work of any registered public accounting firm employed by that issuer . . . for the purpose of preparing or issuing an audit report or related work, and each such registered public accounting firm shall report directly to the audit committee.” Therefore, audit reports of listed companies should be addressed to the audit committee. It is acceptable to also address the report to the stockholders and boards of directors.

FUNDAMENTAL REQUIREMENTS: EXPLANATORY LANGUAGE ADDED TO THE AUDITOR’S STANDARD REPORT

General

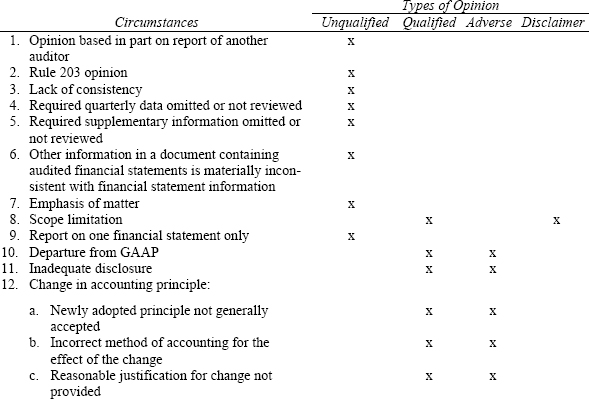

Circumstances may require the auditor to add an explanatory paragraph or explanatory language to the standard report, even though the circumstances do not affect the auditor’s unqualified opinion. Unless specifically stated otherwise, the explanatory paragraph may either precede or follow the opinion paragraph. AU 508.11 lists the following circumstances that may require explanatory language:

1. The auditor’s opinion is based in part on the report of another auditor (see Illustrations and Section 543, Part of Audit Performed by Other Independent Auditors).

2. The financial statements contain a departure from a promulgated accounting principle to prevent them from being misleading. (These situations are covered by Rule 203 of the AICPA Code of Professional Ethics. Also, see Section 410/411.)

3. There is substantial doubt about the entity’s ability to continue as a going concern (see Section 341, The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern).

4. There has been a material change between periods in accounting principles or in the method of their application.

5. Certain circumstances relating to reports on comparative financial statements exist (e.g., prior year audited by another accountant whose report is not presented).

6. Selected quarterly financial data required by SEC Regulation S-K has been omitted or has not been reviewed (see Section 722, Review of Interim Financial Information).

7. The following circumstances pertaining to supplementary information required by the FASB, the Governmental Accounting Standards Board (GASB), or the Federal Accounting Standards Advisory Board (FASAB) exist:

a. The information has been omitted.

b. The information presented departs materially from FASB, GASB, or FASAB guidelines.

c. The auditor is unable to complete prescribed procedures on the information.

d. The auditor has doubts about whether the information conforms to FASB, GASB, or FASAB guidelines.

8. Other information in a document containing audited financial statements is materially inconsistent with information appearing in the financial statements (see Section 550, Other Information in Documents Containing Audited Financial Statements).

9. The auditor may, but is not required to, add an explanatory paragraph when he or she wishes to emphasize a matter concerning the financial statements.

Opinion Based in Part on Report of Another Auditor

When the auditor decides to refer to another auditor’s report as a basis, in part, for the opinion on the financial statements, he or she should disclose this fact in the introductory paragraph of the report and should refer to the other auditor’s report in the opinion paragraph (see Illustration 4 and Section 543, Part of Audit Performed by Other Independent Auditors).

Departure from a Promulgated Principle

Rule 203 of the AICPA Code of Professional Conduct states that the auditor should not express an unqualified opinion if the financial statements contain a material departure from an accounting principle promulgated by the bodies designated by Council of the AICPA to establish such principles. Rule 203, however, provides for the possibility that literal application of a principle may, in unusual circumstances, result in misleading financial statements. In those unusual circumstances, the auditor’s report should include a separate paragraph or paragraphs containing the following:

1. A description of the departure

2. The approximate effects of the departure, if practicable

3. Reasons why compliance with the principle would result in misleading financial statements

The explanatory paragraph(s) may either precede or follow the opinion paragraph. In these circumstances, the auditor may express an unqualified opinion with respect to the conformity of the financial statements with GAAP. Illustration 10 presents an example of an auditor’s report in these circumstances.

NOTE: The financial statements conform with GAAP because the departure from a promulgated principle (pronouncement) is necessary to keep the financial statements from being misleading.

Lack of Consistency

If there has been a change in accounting principles or in the method of their application that has a material effect on the comparability of financial statements, the auditor should add an explanatory paragraph following the opinion paragraph which (1) notes the change, (2) identifies the nature of the change, and (3) refers to the note in the financial statements that discusses the change.

The auditor does not indicate concurrence with the change. If he or she does not concur, the opinion should be qualified because of the GAAP departure or be an adverse opinion (see “Fundamental Requirements: Departures from Unqualified Opinions”).

Explanatory Paragraph

The following is an example of an appropriate explanatory paragraph (following the opinion paragraph) for a change in accounting principle or the method of application:

Reports on Financial Statements of Subsequent Years

The explanatory paragraph described above is required in the auditor’s report of financial statements of subsequent years as long as the year of change is presented and reported on. An exception to this requirement occurs when a change in accounting principle that does not require a cumulative effect adjustment is made at the beginning of the earliest year presented and reported on (for example, a change from FIFO to LIFO).

If the accounting change is accounted for by retroactive restatement of the financial statements affected, the explanatory paragraph is required only in the year of change.

Emphasis of a Matter

The auditor may add an explanatory paragraph, either preceding or following the opinion paragraph, to emphasize a matter regarding the financial statements, but nonetheless express an unqualified opinion on these statements. The auditor should not refer to this type of explanatory paragraph in the opinion paragraph.

FUNDAMENTAL REQUIREMENTS: DEPARTURES FROM UNQUALIFIED OPINIONS

General

Circumstances may require that the auditor not express an unqualified opinion on the financial statements. Depending on the circumstances, the auditor should express a qualified opinion (“except for”) or an adverse opinion or disclaim an opinion.

Qualified Opinions

When the auditor expresses a qualified opinion, he or she should

1. Add one or more separate explanatory paragraph(s) preceding the opinion paragraph of the report that disclose(s) all of the substantive reasons for the qualified opinion.

2. Add appropriate qualifying language to the opinion paragraph, including the word except or exception in a phrase such as except for or with the exception of.

3. Add a reference in the opinion paragraph to the explanatory paragraph(s).

Qualified opinions are expressed when there is a scope limitation or a departure from GAAP, and the auditor has decided not to disclaim an opinion or express an adverse opinion, respectively.

The illustrations contain examples of auditors’ reports qualified because of a scope limitation (Illustration 5) and qualified because of a departure from GAAP (Illustrations 7 and 8).

NOTE: Disclosing all the substantive reasons for an opinion means that all GAAP departures and scope limitations that are material and known to the auditor should be disclosed. For example, the auditor should disclose a known misapplication of the lower of cost or market method in inventory evaluation, even though the opinion has been qualified for a scope limitation related to inventory.

Scope Limitation

Restrictions on the audit’s scope, whether imposed by the client or by circumstances, may require the auditor to qualify the opinion or to disclaim an opinion. Ordinarily, the auditor should disclaim an opinion on the financial statements when restrictions that significantly limit the scope of the audit are imposed by the client.

Uncertainties and scope limitations. If the auditor has not obtained sufficient evidential matter concerning an uncertainty, he or she should consider the need to express a qualified opinion (“except for”) or to disclaim an opinion. Qualifying or disclaiming an opinion because of a scope limitation is appropriate when sufficient evidential matter does or did exist but was not available to the auditor (for example, management did not retain certain records, or management imposed a scope restriction). If it is expected that evidence concerning the resolution of the uncertainty will become available in the future, an unqualified opinion with an explanatory paragraph is appropriate.

Notes to financial statements. Notes to financial statements may contain unaudited information that should be subjected to auditing procedures. If the auditor is not able to apply necessary auditing procedures to these disclosures, he or she should qualify the opinion or disclaim an opinion because of the scope limitation. However, some disclosures, such as the pro forma effects of a business combination or a subsequent event, are not necessary to fairly present the financial statements in accordance with GAAP and, therefore, may be identified as unaudited or as not covered by the auditor’s report.

Reporting on one basic financial statement. The auditor may audit and express an unqualified opinion on one of the basic financial statements if the scope of the audit is not restricted. Illustration 3 contains an example of an auditor’s report on the audit of a balance sheet.

Departure from GAAP

When financial statements are materially affected by a departure from GAAP, the auditor should issue a qualified opinion or an adverse opinion.

When the auditor expresses a qualified opinion, he or she should include a separate explanatory paragraph or paragraphs before the opinion paragraph disclosing (1) all substantive reasons that led to the conclusion that there was a departure from GAAP and (2) the principal effects of the departure on the financial statements, if practicable (see Section 431, Adequacy of Disclosure in the Financial Statements). If the effects of the departure are not reasonably determinable, the auditor’s report should state that fact.

The opinion paragraph of a report qualified because of a departure from GAAP should include appropriate qualifying language and refer to the explanatory paragraph(s).

Illustrations 7 and 8 contain an example of an auditor’s report qualified because of a departure from GAAP.

NOTE: Disclosing all substantive reasons for a GAAP departure means that all known instances of violation of GAAP involved should be mentioned. For example, the auditor should not disclose that a building is stated at appraised value and fail to mention that the increase to appraised value was made to capitalize a realized loss on the sale of another asset.

Inadequate disclosure. If the financial statements, including the notes to the financial statements, do not disclose information required by GAAP, the auditor should issue a qualified or adverse opinion because of this departure from GAAP and should provide the information in the auditor’s report, if practicable (see Section 431, Adequacy of Disclosure in the Financial Statements). Illustration 13 contains an example of an auditor’s report qualified because of inadequate disclosure.

NOTE: At times, current-year financial statements are prepared on the basis of accounting principles that are acceptable at the financial statement date but will have to be restated in the following year because of the issuance of a statement of financial accounting standards whose effective date is after the date of the current year’s financial statements. In those circumstances, if the auditor decides that the matter should be disclosed in the current year’s financial statements and it is not, the auditor should express a qualified or adverse opinion as to conformity with GAAP.

Omission of statement of cash flows. If an entity issues a balance sheet and an income statement but fails to present a statement of cash flows, the auditor normally should qualify the opinion. The auditor is not required to prepare a basic financial statement and include it in the auditor’s report if the entity’s management does not present the statement.

Illustration 11 contains an example of an auditor’s report qualified because of the omission of the statement of cash flows.

Uncertainties and departures from GAAP. Matters involving risks or uncertainties may cause a departure from GAAP because of the following:

1. Inadequate disclosure

2. Inappropriate accounting principles

3. Unreasonable accounting estimates

The auditor should qualify the opinion or express an adverse opinion if he or she concludes that a matter involving a risk or an uncertainty is not adequately disclosed in the financial statements (see FASB Accounting Standards Codification [ASC] 450, Contingencies, for the required disclosures of some uncertainties).

The auditor should qualify the opinion or express an adverse opinion if he or she concludes that the accounting principle used to report a transaction involving an uncertainty causes the financial statements to be materially misstated. An example is a sale on account where collection is uncertain that is reported under the accrual method instead of under the installment or cost recovery method as required by GAAP.

The auditor should qualify the opinion or express an adverse opinion if he or she concludes that management has made an unreasonable estimate of the future outcome of an uncertainty and that its effect is to cause the financial statements to be materially misstated (see Section 312, Audit Risk and Materiality in Conducting an Audit and Section 342, Auditing Accounting Estimates).

Accounting changes—general. The auditor should express a qualified opinion if (1) a newly adopted accounting principle is not an accounting principle that is generally accepted, (2) the method of accounting for the effect of the change is not in conformity with GAAP, or (3) management has not provided reasonable justification for the change in accounting principle. If the effects of the change are sufficiently material, the auditor should express an adverse opinion on the financial statements.

If management has not provided reasonable justification for a change in accounting principle, the auditor should, in subsequent years, continue to qualify the opinion on the financial statements of the year of change as long as those financial statements are presented and reported on. The auditor’s opinion on financial statements of subsequent years need not be qualified.

Illustration 12 contains an example of an auditor’s report qualified because management did not provide reasonable justification for a change in accounting principle.

Accounting changes—subsequent years. Whenever the auditor expresses a qualified or an adverse opinion on the conformity of financial statements with GAAP for the year of change, the auditor should do the following when reporting on subsequent year’s financial statements:

1. Disclose the reservations with respect to the financial statements for the year of change if those financial statements are presented and reported on with the subsequent year’s financial statements.

2. If an entity has adopted an accounting principle that is not generally accepted, the auditor should express a qualified or an adverse opinion on the subsequent year’s financial statements, depending on the materiality of the departure of those financial statements.

3. If an entity accounts for the effects of a change in accounting principle prospectively when it should have reported the cumulative effects of the change in the year of change, the auditor should express a qualified or an adverse opinion on the subsequent year’s financial statements, depending on the materiality of the effect of the departure from GAAP on those financial statements.

Adverse Opinions

An adverse opinion is expressed when the auditor believes the financial statements taken as a whole are not presented fairly in conformity with GAAP.

When the auditor expresses an adverse opinion, he or she should do the following:

1. Disclose in a separate explanatory paragraph before the opinion paragraph of the report all substantive reasons for the opinion.

2. State the principal effects of the subject matter that caused the adverse opinion on financial position, results of operations, and cash flows, if practicable (see Section 431, Adequacy of Disclosure in the Financial Statements). If the effects are not reasonably determinable, the auditor’s report should state this fact.

3. Include in the opinion paragraph a direct reference to the separate explanatory paragraph.

Illustration 9 contains an example for an auditor’s report expressing an adverse opinion.

NOTE: Because an adverse opinion is an opinion, it should not be expressed unless the auditor has performed an audit of sufficient scope to be able to express an opinion.

Disclaimer of Opinion

The auditor disclaims an opinion when he or she has not performed an audit sufficient in scope to enable him or her to form an opinion on the financial statements. Ordinarily, the auditor should disclaim an opinion on the financial statements when significant scope restrictions are imposed by the client.

The auditor should not disclaim an opinion because he or she believes there are material departures from GAAP.

The auditor should do the following when disclaiming an opinion because of a scope limitation:

1. Indicate in a separate explanatory paragraph the reasons why the audit did not comply with GAAS.

2. State in the disclaimer of opinion paragraph that the scope of the audit was not sufficient to warrant the expression of opinion.

3. The auditor’s report should not include a scope paragraph.

Illustration 6 contains an example of an auditor’s report disclaiming an opinion because of a scope limitation.

NOTE: Even though the auditor disclaims an opinion, the auditor should disclose any known GAAP departures.

FUNDAMENTAL REQUIREMENTS: REPORTS ON COMPARATIVE FINANCIAL STATEMENTS

General

A continuing auditor should update his or her report on the prior period financial statements presented on a comparative basis with the current period financial statements. When updating his or her report, the auditor should consider the effects of circumstances or events coming to his or her attention during the audit of the current period financial statements that may affect the prior period financial statements (see below, “Change of Opinion”).

The auditor’s report on comparative financial statements should be dated as of the date of completion of fieldwork for the most recent audit.

Change of Opinion

In an updated report, if the auditor expresses an opinion different from the one previously expressed on prior period financial statements, he or she should do the following:

1. Disclose all substantive reasons for the different opinion in a separate explanatory paragraph before the opinion paragraph of the report.

2. The explanatory paragraph should disclose the following:

a. The date of the auditor’s previous report

b. The kind of opinion previously expressed

c. The circumstances or events that caused the auditor to express a different opinion

d. The updated opinion on the prior period financial statements is different from the opinion previously expressed on those financial statements

Illustration 16 contains an example of an auditor’s report with an opinion different from the one previously expressed on prior period financial statements.

Reissuance of Predecessor Auditor’s Report

Predecessor’s Procedures

Before reissuing or consenting to the reuse of a report previously issued on financial statements of a prior period, when those financial statements are to be presented on a comparative basis with audited financial statements of a subsequent period, a predecessor auditor should consider whether the previous report on those statements is still appropriate. The predecessor should do the following:

1. Read the current period financial statements.

2. Compare the prior period financial statements that the predecessor reported on with the financial statements to be presented on a comparative basis.

3. Obtain letters of representation from:

a. The successor auditor, stating whether the successor’s audit revealed matters that might have a material effect on, or require disclosure in, the financial statements reported on by the predecessor auditor, and

b. Management of the former client, stating:

(1) Whether any information has come to management’s attention that would cause them to believe that any previous representations should be modified, and

(2) Whether any events have occurred subsequent to the balance sheet date of the latest prior period financial statements reported on by the predecessor auditor that would require adjustment to, or disclosure in, those financial statements. (Illustration 17D contains an example of a letter of representation from a successor auditor and from management.)

Based on the above procedures, if the predecessor auditor believes the previously issued report must be revised, he or she should make inquiries about the matter and perform other procedures considered necessary.

Revision of Previously Issued Report

If the predecessor auditor concludes that the previously issued report should be revised, the updated report should disclose all substantive reasons for the different opinion in a separate explanatory paragraph preceding the opinion paragraph of the report. The explanatory paragraph should disclose the following:

1. The auditor’s previous report date

2. The kind of opinion previously expressed

3. The circumstances or events that caused the auditor to express a different opinion

4. The updated opinion on the prior period financial statements is different from the opinion previously expressed on those financial statements

Dating of Reissued Report

When reissuing the auditor’s report on prior period financial statements, the predecessor auditor should use the date of the previous report.

If the predecessor revises the report or the previously reported-on financial statements are restated, the predecessor auditor should dual date the report.

Predecessor Auditor’s Report Not Presented

General

When the predecessor auditor’s report on prior period financial statements is not presented, the successor auditor should disclose in the introductory paragraph of his or her report the following:

1. The prior period financial statements were audited by another auditor

2. The predecessor auditor’s report date

3. The type of report issued by the predecessor auditor

4. The substantive reasons for a report other than the standard report

Illustration 17 contains examples of successor auditor reports when the predecessor auditor’s report is not presented.

Prior Period Financial Statements Restated

When the prior period financial statements have been restated, the introductory paragraph of the successor auditor’s report should state that a predecessor auditor reported on the prior period financial statements before restatement. If the successor auditor is able to satisfy himself or herself as to the appropriateness of the restatement, he or she may also include the following paragraph from AU 508.74 in the report:

INTERPRETATIONS

Report of an Outside Inventory-Taking Firm as an Alternative Procedure for Observing Inventories (Issued July 1975; Revised October 2000: Revised March 2006)

Some companies, such as retail stores or automobile dealers, use outside specialists in the taking of physical inventories to count, list, price, and subsequently compute the dollar amount of inventory on hand. The fact that inventory is counted by outside specialists is not by itself a satisfactory substitute for the auditor’s own observation or taking of some physical counts.

The auditor would ordinarily apply the following procedures:

1. Examine the outside specialist’s work program.

2. Observe its counting procedures.

3. Make or observe some physical counts.

4. Recompute calculations of submitted inventory on a test basis.

5. If appropriate, apply tests to intervening transactions.

The independent auditor might, as a matter of professional judgment, decide to reduce the extent of work because of the work of outside specialists, but any restrictions imposed by management or others would be a scope limitation. If the inventory is counted by an outside firm of nonaccountants, this is not a satisfactory substitute for the auditor’s own observation.

Reporting on Financial Statements Prepared on a Liquidation Basis of Accounting (Issued December 1984; Revised June 1993 and February 1997; Revised October 2000; Revised June 2009; Revised October 2011 Effective for Audits of Financial Statements for Periods Ending on or After December 15, 2012)

An entity is not viewed as a going concern if liquidation is imminent. In these circumstances, the liquidation basis of accounting is GAAP. If the liquidation basis has been properly applied and adequate disclosures are made, the auditor should issue an unqualified opinion.

If financial statements on the liquidation basis are presented in comparative form with a prior period’s going-concern basis financial statements, the auditor’s report should include an explanatory paragraph that describes the change in basis of accounting. (Illustrations 19 and 20 present examples of auditor’s reports on financial statements on the liquidation basis of accounting.)

(The above terminology has been revised to reflect the clarified standards and is effective for audits of financial statements for periods ending on or after December 15, 2012:

Reference in Auditor’s Standard Report to Management’s Report (January 1989)

The auditor’s standard report on financial statements should not refer to a separate report by management, if management chooses to present one, that describes management’s financial reporting responsibilities. The standard auditor’s report should still state that management is responsible for the financial statements, but a cross-reference to a report by management might be misinterpreted by users.

Reporting on Audits Conducted in Accordance with Auditing Standards Generally Accepted in the United States of America and in Accordance with International Standards on Auditing (March 2002; Revised May 2008)

As discussed in this section, the auditor is required to (1) indicate in his or her report that the audit was conducted in accordance with GAAS and (2) identify the United States of America as the country of origin of those standards. However, nothing in this section prohibits an auditor from stating that the audit was conducted in accordance with another set of auditing standards. If the audit was also conducted in accordance with International Standards on Auditing in their entirety, the auditor may indicate this in his or her report.

When reporting on an audit performed in accordance with US GAAS and International Standards on Auditing, the auditor should comply with US reporting standards.

The following is an example from the interpretation (AU 9508.59) of a paragraph in a report for an audit performed in accordance with US GAAS and International Standards on Auditing:

Reporting as Successor Auditor When Prior-Period Audited Financial Statements Were Audited by a Predecessor Auditor Who Has Ceased Operations (November 2002; Revised June 2009)

If prior period financial statements were audited by a predecessor auditor who has ceased operations, and such statements are presented for comparative purposes with the current financial statements, the successor auditor should indicate in the introductory paragraph of his or her report that the financial statements of the prior period were audited by another auditor and should indicate the date and type of report. (If the report was not unqualified, the auditor should also indicate the substantive reasons for the report qualifications.) The successor auditor also should state that the other auditor has ceased operations, but should not name the other auditor.

The interpretation presents the following example of such a report (AU 9508.61):

For SEC engagements, the SEC staff has stated that in annual reports, the predecessor’s latest prior period report should be reprinted with a legend indicating that the report is a copy of the previously issued report and that the report has not been reissued.

If the prior period financial statements are subsequently restated, the successor auditor cannot report on the restated adjustments until the audit of the current period financial statements is complete. If the successor auditor is asked to report on the restated financial statements without also reporting on the current period audited financial statements, the successor auditor would need to reaudit the prior period statements.

Effect on Auditor’s Report of Omission of Schedule of Investments by Investment Partnerships That Are Exempt from Securities and Exchange Commission Registration under the Investment Company Act of 1940 (April 2003; Revised June 2009)

When an auditor is reporting on financial statements of an investment partnership that is exempt from SEC registration and that does not include required Schedule of Investments information, the auditor is required to include the missing information in a qualified or an adverse report, if practicable. The auditor should not describe “the nature of the omitted disclosures” in the qualified or adverse report.

Clarification in the Audit Report of the Extent of Testing of Internal Control Over Financial Reporting in Accordance with Gaas (June 2004; Revised March 2006)

Nonissuers, as defined in the Summary of Key Changes that immediately precedes Section 100-230, are required to perform audits under GAAS as established by the Auditing Standards Board of the AICPA. An auditor of a nonissuer may want to clarify that an audit performed under GAAS does not require the same level of testing and reporting on internal control over financial reporting as required for an audit by Section 404(b) of the Sarbanes–Oxley Act for entities subject to the rules of the SEC. (See the summary of PCAOB Standard No. 5, An Audit of Internal Control Over Financial Reporting That Is Integrated with an Audit of Financial Statements, presented later in this publication.) The interpretation suggests that the following language can be inserted as the third sentence in the scope paragraph:

An audit includes consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

The interpretation notes that this additional language should not be used when a nonissuer voluntarily engages its auditor to audit and report on the effectiveness of internal control over financial reporting, or does so to comply with regulatory requirements.

Reference to PCAOB Standards in an Audit Report on a Nonissuer (June 2004)

PCAOB Standard No. 1, Reference in Auditors’ Reports to the Standards of the Public Company Accounting Oversight Board, requires that audit reports for engagements performed in accordance with PCAOB standards include a statement that the engagement was conducted in accordance with the standards of the PCAOB. A company that is not subject to the rules of PCAOB standards (a nonissuer) is not precluded from conducting the audit in accordance with the standards of the PCAOB and including a statement about this in the audit report. (Issuers and nonissuers are defined in the Summary of Key Changes immediately preceding Section 100-230.) Therefore, if an auditor is engaged to perform an audit of a nonissuer under PCAOB standards, the auditor would state in the report that the audit was conducted in accordance with both US GAAS (as required by Section 508, Reports on Audited Financial Statements) and with PCAOB standards. The scope paragraph would state that “We conducted our audit in accordance with generally accepted auditing standards as established by the Auditing Standards Board (United States) and in accordance with the auditing standards of the Public Company Accounting Oversight Board (United States).” (The auditor may use the reference to the Auditing Standards Board to clarify the source of GAAS in this type of reporting situation.)

NOTE: The PCAOB has issued a series of staff questions and answers titled Audits of Financial Statements of Nonissuers Performed Pursuant to the Standards of the Public Company Accounting Oversight Board.

Among other things, these questions clarify that a firm does not need to be registered with the PCAOB in order to audit a nonissuer under PCAOB standards. The PCAOB also clarifies what standards apply when the report refers to the standards of the PCAOB. The authors strongly recommend that auditors read these questions and answers if they are considering performing an audit of a nonissuer under PCAOB standards. The questions and answers can be found on the PCAOB’s website at www.pcaobus.org.

This interpretation notes that an audit report of a subsidiary, investee, or other type of affiliate of an issuer that is not itself an issuer should refer to the audit as having been performed according to GAAS if the report will not be filed with the SEC. For example, an issuer’s subsidiary may be subject to certain regulations that require an audit performed according to Government Auditing Standards (the “Yellow Book”). In this case the audit report on the subsidiary would refer to GAAS and generally accepted government auditing standards.

Finally, the interpretation suggests in AU 9508.92 that the following language be used to clarify that the purpose and extent of the auditor’s testing of internal control over financial reporting was to determine the auditor’s procedures and was not sufficient to express an opinion on the effectiveness of internal control. This language is suggested because an audit of a nonissuer performed under PCAOB auditing standards does not require an audit of internal control as required by PCAOB Auditing Standard 5, An Audit of Internal Control over Financial Reporting That Is Integrated with an Audit of Financial Statements, unless otherwise required by a regulator with jurisdiction over the nonissuer. The language can be inserted as the third sentence in the scope paragraph.

The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly we express no such opinion.

This additional language should not be used when a nonissuer voluntarily engages its auditor to audit and report on the effectiveness of internal control over financial reporting, or does so to comply with regulatory requirements.

NOTE: Practitioners should be aware that the AICPA’s Center for Public Audit Firms, which replaced the SEC Practice Section, has notified its member firms of certain requirements that apply to employee stock purchase, savings, and similar plans that are required to file Form 11-K pursuant to Section 15(d) of the Securities Exchange Act of 1934. Such plans are considered issuers and must submit an audit report to the SEC in accordance with PCAOB standards. However, these 11-K plans also may be subject to the Employee Retirement Income Security Act (ERISA) and, therefore, may be required to submit an audit to the US Department of Labor in accordance with GAAS. Because PCAOB Auditing Standard 1 does not allow reference to GAAS, and because the Center believes that the Department of Labor will not accept audit reports not referencing GAAS, firms need to conduct audits of these 11-K plans according to two sets of standards. They also must prepare two separate audit reports to meet these requirements.

Financial Statements Prepared in Conformity with International Financial Reporting Standards as Issued by the International Accounting Standards Board (May 2008)

When an auditor reports on financial statements prepared in conformity with International Financial Reporting Standards (IFRS), the auditor would refer, in the auditor’s report, to IFRS rather than to US GAAP. A sample opinion paragraph is:

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 20X2 and 20X1, and the results of its operations, comprehensive income, changes in equity, and its cash flows for the years then ended, in conformity with International Financial Reporting Standards as issued by the International Accounting Standards Board.

PROFESSIONAL ISSUES TASK FORCE PRACTICE ALERTS

97-3 Changes in Auditors and Related Topics

This practice alert discusses appropriate procedures for successor auditors, such as:

- Requesting that the client authorize the predecessor auditor to permit a review of the predecessor audit documentation after the successor auditor has accepted the engagement

- Remembering that, since the client and successor auditor are responsible for the opening balances on the current year financial statements and consistency of accounting principles, the successor must obtain sufficient competent evidential matter to provide a reasonable basis for expressing an opinion.

In addition, predecessor auditors must consider relevant matters when asked by a former client to reissue their audit reports. Matters include deciding whether to reestablish a client relationship and evaluating the former client’s intended use of the predecessor auditor’s report.

This practice alert states that before consenting to include his or her report on previously audited financial statements, a predecessor auditor should perform procedures similar to its client acceptance and continuation procedures as required by Statement on Quality Control Standards (SQCS) 2, System of Quality Control for a CPA Firm’s Accounting and Auditing Practice, and may wish to consider the guidance in Practice Alert 2003-3, Acceptance and Continuance of Clients and Engagements.

The auditor typically would evaluate whether specific events have occurred, such as a major change in:

- Management

- Directors

- Ownership

- Legal counsel

- Financial condition

- Litigation status

- Nature of the entity’s business

- Scope of the engagement

Consideration of:

- Whether the client has selected an underwriter that has been the subject of adverse publicity

- The professional reputation and experience of both the successor auditor and legal counsel associated with subsequent years’ financial statements

After consideration of these factors, the predecessor auditor should then consider whether his or her report is still appropriate under the circumstances, using guidance provided in this section under “Fundamental Requirements: Reports on Comparative Financial Statements.” If, after performing the appropriate procedures, a predecessor becomes aware of subsequent events or transactions that require adjustment, additional disclosure or reclassification, the predecessor auditor should make inquiries and perform any other necessary procedures.

An auditor may decide not to consent to the use of his or her previously issued report and is not required to subsequently sign a consent for inclusion of that report in a registration statement or for any other reason. The auditor does not need to disclose or communicate the reasons for not issuing the report to either the entity or its audit committee. If the predecessor does not reissue his or her report, the successor may be engaged to audit the financial statements previously reported on and should follow the guidance in “Fundamental Requirements” of Section 315, Communications between Predecessor and Successor Auditors.

Finally, the alert discusses the use of indemnification clauses when reissuing reports. SEC independence rules prohibit indemnification agreements between auditors and current publicly held clients. However, the SEC staff has agreed not to question a predecessor auditor’s independence with respect to a former client for indemnification agreements, provided that:

1. The indemnification letter would be void and any advanced funds would be returned to a client if a former auditor is found liable for malpractice, and

2. The indemnification provision is entered into after a successor auditor has issued an audit report on the former client’s most recent financial statements included in the client’s registration statement.

TECHNIQUES FOR APPLICATION

The following table lists the circumstances requiring modification of the auditor’s standard report and the effect of the modification on the auditor’s standard report.

Scope Limitation

General

The decision to qualify the opinion or to disclaim an opinion depends on the auditor’s assessment of the importance of the omitted procedure to his or her ability to form an opinion on the financial statements being audited. The auditor’s assessment is affected by the following:

1. Nature and magnitude of the potential effects

2. Significance to financial statements of item to scope limitation

3. Pervasiveness of the item

Pervasiveness generally relates to the number of items in the financial statement; that is, is the matter isolated to a few items or does it affect many? For example, ending inventory affects many items—current assets, current ratio, gross profit, income taxes, and net income—whereas an investment accounted for by the equity method affects few line items in the financial statements.

Common Restrictions on Scope

Common restrictions on the scope of the audit involve (1) observation of physical inventories, (2) confirmation of accounts receivable, and (3) long-term investments accounted for by the equity method when the auditor is unable to obtain audited financial statements of the investee.

If the auditor did not observe the ending inventory because of circumstances such as appointment after year-end, he or she should apply alternative procedures. Alternative procedures may include observing all or part of the physical inventory after year-end and rolling it back to year-end by adjusting for additions and sales between year-end and the date the physical inventory was observed. Whatever alternative procedures are used, the auditor should always make, or observe, some physical counts of the inventory and apply appropriate tests to the transactions between year-end and the date of the observation. (See Section 331, Inventories.)

If the auditor did not confirm accounts receivable at year-end because of circumstances such as appointment after year-end, he or she might do either of the following at the time of appointment:

1. Try to confirm year-end balances or individual sales and cash receipts.

2. Confirm balances at a date subsequent to year-end and apply appropriate tests to transactions between year-end and the confirmation date.

Some debtors are unable to confirm balances at any time. In these circumstances, the auditor should consider examining subsequent cash receipts or specific sales invoices. In all instances in which accounts receivable are not substantiated by confirmation, the auditor has to document how the presumption that receivables will be confirmed was overcome (see Section 330, The Confirmation Process).

If the auditor is unable to obtain audited financial statements of the investee for investments accounted for by the equity method, he or she should examine other types of financial statements (compiled, reviewed, internal) and, depending on the materiality of the investment, apply appropriate auditing procedures to these statements.

If there is a scope limitation and the auditor satisfies himself or herself as to the account balance by applying alternate procedures, the auditor’s report should not make reference to these circumstances.

Restrictions Imposed by Client

As noted under “Fundamental Requirements,” when scope limitations are imposed by the client, the auditor should ordinarily disclaim an opinion on the financial statements. The rationale for a disclaimer in these circumstances is that the client is in a position to avoid the limitation and the auditor cannot know what would be found by release of the restriction.

Departure from GAAP

The decision to express a qualified or an adverse opinion because of a departure from GAAP depends on the degree of materiality of the departure. Criteria for determining the degree of materiality of a departure from GAAP are:

1. Dollar magnitude of the effects

2. Significance of the item to the entity (for example, inventories to a manufacturing company)

3. Pervasiveness of the misstatements

4. Impact of the misstatement on the financial statements taken as a whole

In practice, auditors also consider the likely purpose of management in departing from GAAP. A judgment that management intended to mislead users would ordinarily cause the auditor to express an adverse opinion.

Litigation Services

A practitioner engaged to provide expert consulting or witness services is not subject to the requirements of GAAS, including the reporting standards. However, an expert engaged by plaintiffs or defendants in an auditor malpractice matter may testify about the application of GAAS to the circumstances.

AU ILLUSTRATIONS

The following are illustrations of auditors’ reports, explanatory paragraphs, a letter from successor auditor to predecessor auditor, and a letter from management to the predecessor auditor.

1. Auditor’s Standard Report: Financial Statements Covering a Single Year (Adapted from AU 508.08)

2. Auditor’s Standard Report on Comparative Financial Statements (Adapted from AU 508.08)

3. Auditor’s Report on One Basic Financial Statement (Adapted from AU 508.34)

4. Auditor’s Report: Opinion Based in Part on Report of Another Auditor (Adapted from AU 508.13)

5. Auditor’s Report: Qualified Opinion—scope Limitation (Adapted from AU 508.26)

6. Auditor’s Report: Disclaimer of Opinion—scope Limitation (Adapted from AU 508.63)

7. Auditor’s Report: Qualified Opinion—Departure from GAAP Explained in Report (Adapted from AU 508.39)

8. Auditor’s Report: Qualified Opinion—Departure from GAAP Explained in a Note (Adapted from AU 508.40)

9. Auditor’s Report: Adverse Opinion—Departure from GAAP (Adapted from AU 508.60)

10. Auditor’s Report: Rule 203 Opinion

11. Auditor’s Report: Omission of Statement of Cash Flows (Adapted from AU 508.44)

12. Auditor’s Report: Management Has Not Provided Reasonable Justification for Change in Accounting Principle (Adapted from AU 508.17)

13. Auditor’s Report: Inadequate Disclosure (Adapted from AU 508.42)

14. Auditor’s Standard Report on the Prior Year Financial Statements and a Qualified Opinion on the Current Year Financial Statements (Adapted from AU 508.67)

15. Auditor’s Standard Report on the Current Year Financial Statements with a Disclaimer of Opinion on the Prior Year Statements of Income, Retained Earnings, and Cash Flows (Adapted from AU 508.67)

16. Auditor’s Report: Opinion Different from Opinion Previously Expressed (Adapted from AU 508.69)

17. Auditor’s Report: Predecessor Auditor’s Report Not Presented (Adapted from AU 508.74)

18. Illustrative Updating Management Representation Letter (Adapted from AU 333.18)

19. Auditor’s Report on Single-Year Financial Statements in Year of Adoption of Liquidation Basis (Adapted from AU 9508.36)

20. Auditor’s Report on Comparative Financial Statements in Year of Adoption of Liquidation Basis (Adapted from AU 9508.36)

Illustration 1. Auditor’s Standard Report: Financial Statements Covering a Single Year (Adapted from AU 508.08)

To the Board of Directors

Widget Company

Main City, USA

Independent Auditor’s Report

We have audited the accompanying balance sheet of Widget Company as of December 31, 20X6, and the related statements of income, retained earnings, and cash flows for the year then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Widget Company as of [at] December 31, 20X6, and the results of its operations and its cash flows for the year then ended in conformity with accounting principles generally accepted in the United States of America.

Smith and Jones

February 15, 20X7

Illustration 2. Auditor’s Standard Report on Comparative Financial Statements (Adapted from AU 508.08)

To the Board of Directors

Widget Company

Main City, USA

Independent Auditor’s Report

We have audited the accompanying balance sheets of Widget Company as of December 31, 20X6 and 20X5, and the related statements of income, retained earnings, and cash flows for the years then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Widget Company as of [at] December 31, 20X6 and 20X5, and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

Smith and Jones

February 15, 20X7

Illustration 3. Auditor’s Report on One Basic Financial Statement (Adapted from AU 508.34)

To the Board of Directors

Widget Company

Main City, USA

Independent Auditor’s Report

We have audited the accompanying balance sheet of Widget Company as of December 31, 20X6. This financial statement is the responsibility of the Company’s management. Our responsibility is to express an opinion on this financial statement based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the balance sheet referred to above presents fairly, in all material respects, the financial position of Widget Company as of December 31, 20X6, in conformity with accounting principles generally accepted in the United States of America.

Smith and Jones

February 15, 20X7

Illustration 4. Auditor’s Report: Opinion Based in Part on Report of Another Auditor (Adapted from AU 508.13)

To the Board of Directors

Widget Company

Main City, USA

Independent Auditor’s Report

We have audited the consolidated balance sheets of Widget Company and subsidiaries as of December 31, 20X6 and 20X5, and the related consolidated statements of income, retained earnings, and cash flows for the years then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We did not audit the financial statements of B Company, a wholly owned subsidiary, which statements reflect total assets of $_____ and $_____ as of December 31, 20X6 and 20X5, respectively, and total revenues of $_____ and $_____ for the years then ended. Those statements were audited by other auditors whose report has been furnished to us, and our opinion, insofar as it relates to the amounts included for B Company, is based solely on the report of the other auditors.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits and the report of other auditors provide a reasonable basis for our opinion.

In our opinion, based on our audits and the report of other auditors, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Widget Company as of December 31, 20X6 and 20X5, and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

Smith and Jones

February 15, 20X7

Illustration 5. Auditor’s Report:

Qualified Opinion—scope Limitation (Adapted from AU 508.26)

To the Board of Directors

Widget Company

Main City, USA

Independent Auditor’s Report

[Same first paragraph as the standard report]

Except as discussed in the following paragraph, we conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

We were unable to obtain audited financial statements supporting the Company’s investment in a foreign affiliate stated at $_____ and $_____ at December 31, 20X6 and 20X5, respectively, or its equity in earnings of the affiliate of $_____ and $_____, which is included in net income for the years then ended as described in Note X to the financial statements; nor were we able to satisfy ourselves as to the carrying value of the investment in the foreign affiliate or the equity in its earnings by other auditing procedures.

In our opinion, except for the effects of such adjustment, if any, as might have been determined to be necessary had we been able to examine evidence regarding the foreign affiliate investment and earnings, the financial statements referred to in the first paragraph above present fairly, in all material respects, the financial position of Widget Company as of December 31, 20X6 and 20X5, and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

Smith and Jones

February 15, 20X7

Illustration 6. Auditor’s Report: Disclaimer of Opinion—scope Limitation (Adapted from AU 508.63)

To the Board of Directors

Widget Company

Main City, USA

Independent Auditor’s Report

We were engaged to audit the accompanying balance sheets of Widget Company as of December 31, 20X6 and 20X5, and the related statements of income, retained earnings, and cash flows for the years then ended. These financial statements are the responsibility of the Company’s management.

[Second paragraph of standard report should be omitted]

The Company did not make a count of its physical inventory in 20X6 or 20X5, stated in the accompanying financial statements at $_____ as of December 31, 20X6, and at $_____ as of December 31, 20X5. Further, evidence supporting the cost of property and equipment acquired prior to December 31, 20X5, is no longer available. The Company’s records and circumstances do not permit the application of other auditing procedures to inventories or property and equipment.

Since the Company did not take physical inventories, and we were not able to apply other auditing procedures to satisfy ourselves as to inventory quantities and the cost of property and equipment, the scope of our work was not sufficient to enable us to express, and we do not express, an opinion on these financial statements.

Smith and Jones

February 15, 20X7