5. Banking

The big analytics lesson from banking is its understanding of the capabilities and motivations of its customers to carry through on their obligations.

Introduction

No other industry has dug itself into such a deep hole as banking has. Banks are widely viewed as primarily responsible for precipitating the Great Recession due to shaky lending practices related to subprime mortgages. Retail banking customers are dismayed by hidden costs, new fees, the “small print,” and the difficulty in getting a loan. The public’s confidence in the industry has been shattered...worldwide demonstrations have accused the industry of greed and corruption. Politicians from around the globe have responded with extensive regulatory requirements.

The business climate for banking is dark. The Wall Street Journal reported on the “grim new reality” for the industry characterized by “slow economic growth that tamps down loan demand, low interest rates that pressure investment returns, volatile markets that inhibit risk-taking and tighter regulation that adds to bulging costs.”1 Finally, McKinsey & Company concluded that “without radical action to shrink balance sheets, cut costs, and increase revenues, banks will be unable to attract sufficient new capital from the investment community and to play their critical role in underpinning economic recovery and growth.”2

So what’s an industry to do? How can the resolution of this crisis, driven by tremendous pressures to stabilize and grow the business, deepen its capabilities in analytics? What are the unique analytic sweet spots of the industry? And how can the sweet spots be translated and adapted to healthcare? The bottom line is that it comes down to two solutions with the acronyms HICS (Health Improvement Capability Score) and AMT (All Multichannels Together). This chapter provides the guided tour to understand the industry and its associated analytics and what it means for healthcare.

First, let’s try to understand the industry. For most of us, banking appears to be very complicated. For example, does any layperson really understand what happened when subprime mortgages were split up into multiple securities that Wall Street packaged into investment products? Even investors seemed clueless about the risk associated with these securities and then lost their collective shirts as millions of customers were unable to make payments on mortgages that they should never have been given in the first place, and subsequently defaulted on. And the whole house of financial cards and worldwide economies collapsed. In the unforgettable words of Gordon Gekko in the movie Wall Street, “Greed, for lack of a better word, is good.” That is, unless it makes people do foolish things and goes too far.

At its core, however, banking is really quite straightforward when compared to other industries. Simply put, banking makes money off of money. It needs to secure funds either through its banking customers’ deposits and other money holdings or through other institutions that lend it money (such as commercial banks). Then it turns around and lends money to others and makes profits on the spread between what it paid for the funds and what it can get in return for lending it. It has a relatively narrow range of products to offer its customers, including checking accounts, saving accounts, CDs, mortgages, credit cards, trust services, and perhaps brokerage services. It is narrow when compared to the broad range of products offered by retailers. It is simple when compared to supply-chain issues in manufacturing or the complexity of what constitutes success as in healthcare. There are many performance metrics in banking, but it mostly boils down to using money effectively as measured by returns—return on investment (ROI), return on equity (ROE), return on assets (ROA), and so forth. Compare this to the range of diverse measures in healthcare spanning clinical outcomes, adherence to guidelines, economic outputs, costs, and much more.

The American banking system is large. It consists of 7,513 FDIC-insured banks and savings associations owning 87,873 bank offices and 10,319 savings association offices. Deposits in FDIC-insured organizations totaled $8.85 trillion in June 2011. Additionally, in 2011, there were 7,339 credit unions with assets totaling $914.5 billion.3 Most of the banks are community banks but most of the money is held in larger banks.

Banks have a long history going back to 9000 B.C., starting by making grain loans to farmers and traders. In more modern times, banks became a fixture in almost every community because they provided services that every community needed, just like local schools, fire and police protection, and doctors and hospitals. People went to their local banker to start a business, buy a house or a car, send their children to college, and provide a “monetary home” for their life savings. Bankers were leaders in communities and gave back to help the communities prosper, not just through the money services they provided but also with dedication to the needs of the community in supporting charities and important community initiatives. The 1946 movie It’s a Wonderful Life, directed by Frank Capra, captures the (sentimental) essence of this community obligation. People knew and trusted their banker just as they did their doctor. The doctor took care of their health welfare and the banker took care of their economic welfare.

But the banking experience that most of us have today is quite different. Rather than walking into a bank office and exchanging greetings with the tellers and the manager, the more typical communication now is putting an ATM card into the slot and “greeting” it with a punched-in password. Ditto for Internet banking. Of course, healthcare has changed as well. Doctors do not make house calls anymore and have been “industrialized” into medical groups that produce efficient eight-minute slots for patient consultations with great efficiency in provider-centric complexes.

Nostalgia is warm and fuzzy and might not be relevant for today’s solutions. Community has given way to “what’s best for me.” Consumers want the most convenient and frictionless transactions. Social media communications are the rage but are often more akin to stalking people and extracting information than to building deep relationships. Efficiency has trumped relationships.

So banking has two faces. On the one hand, it was created out of a strong commitment and connection to its primary customer, the people in its communities. On the other, its basic formula to “make money off money” requires a laser focus on the returns on A, E, and I to satisfy its superordinate customer, the investors, in a very turbulent and competitive environment. The balance between these two customers got out of whack, with the former becoming subservient to the needs of the latter. The resultant depersonalization of much of banking today and its associated business failure consequences might be a necessary “hitting bottom,” as with a person overtaken with alcoholism, to motivate it with a sustained will to reinvent itself. Appreciating and servicing customers as a back-to-the-future success strategy might be the hardest, most counterintuitive, and surest way to achieve growth.

The same can be said for the health insurance industry. Its “primary” customers are its members: those who sign up, pay premiums, and receive payment coverage for the care needed to treat illnesses. But the more important customer became employers who actually paid (most of) the premiums out of employee compensation and called the shots about what benefits are provided and what health plan(s) are made available to employees. As employers became more concerned about their escalating insurance costs, they tended to shift costs to employees. For example, many employers offered/required employees to enroll in high-deductible/health savings account plans, which was not necessarily done for the health welfare of employees. Insurance companies were happy to satisfy employers with multiple products and different price points and got out of the business of managing medical costs and real member needs. Members were regarded as a cost to be managed and were often treated by customer service representatives as irritants that needed to comply with business process requirements.

Health insurers became the lowest-rated industry in terms of customer engagement.4 (Forrester Research does surveys on customer engagement. The health insurance industry had the lowest average score, at 51%. The average score for banking was 66%. The highest-scoring industries were retail and hotels, at over 80%.) Many business practices of insurers were considered unfair, such as denials for care associated with preexisting conditions, and were subsequently regulated through Obamacare. Other regulations of Obamacare required that insurers become more transparent on the quality and costs of the benefits provided and that they compete in health insurance exchanges to offer their products directly to a potentially large segment of Americans. Additionally, market-driven changes in the way providers are paid—that is, from fee-for-service to global payments—and in the preference for integrated and coordinated care that is measured by outcomes and not by the process of the care, are also changing the perspectives on “customer needs.” And what member customers want will be quite different from what employer customers want.

So the two industries, banking and health insurance, have a lot in common. Both have reached bottom with their customers. Both have been the subject of extensive political and public debates that have spotlighted weaknesses and excesses. Both have been slapped with extensive and onerous regulations. And both need to get back to the future with strategies and practices that give people a reason to do business with them.

Further, they are both increasingly commoditized industries, for example, processing claims and money transactions and issuing insurance or loans, and both need to get a new raison d’être to prosper with profitable business lines. For example, for one major insurer, more than one-third of its $34 billion in revenue comes from noninsurance revenue streams. Its CEO said, “We’re evolving into a ‘Health IT’ company with a health insurance component.”5 For other insurers, they are evolving to become a full-service healthcare company. Cigna has ramped up its customer outreach with 24/7 customer service, mobile applications, social media, decision support tools, and access to health coaches. It is also expanding its engagement with accountable care organizations and partnering with physicians and hospitals more closely.6 But many insurers, perhaps most, dismiss these radical solutions as overkill and think this is basically a public relations problem that can be solved by rebranding and customer communications about how much they care.

Banking knows it must change and agrees with Rahm Emanuel’s immortal words to not let a good crisis go to waste. The industry also understands the “what” more than the “how” in the “back-to-the-future” customer strategy. Many believe that the reinvention and rebirth will be driven by data. When a panel at the 2012 Strata conference on the future of banking was asked, “How pervasive is data analytics and will it provide the competitive edge to transform?” Richie Prager from Blackrock said, “It’s a huge edge.” But Allen Weinberg from McKinsey said that the state of the art of analytics is quite different from the state of the practice.7

And this is at the core of the sweet spot and potential lessons learned from the analytics of banking. Can an industry under more stress than any other (be forced to) make use of analytics in ways to reinvent itself? If not, and if it wastes the crisis, why would any other industry find the guts/purpose/commitment to adopt the best that analytics has to offer? And if it does, how do the analytics mature in unpredictable and totally productive ways?

Industry Challenges

McKinsey’s review of the banking industry in late 2012 painted a dismal picture of its present and future state.8 Revenue growth is down to 3% (compared to 9% in 2007). There were no improvements in costs and there was a deterioration in capital efficiency. This led to a decrease in profits of 2% from 2010 to 2011 and a 15% drop compared to 2007. Global average return on equity (essentially net income after taxes) fell to 7.6% in 2011 (with the U.S. at 7%), down from 13.6% in 2007, which is half its peak value before the financial crisis. The industry as a whole is far from earning its cost of equity, which would require an ROE of 12%. If it does not reach its cost of equity, investors will go elsewhere.

The drivers of these numbers are many. The first is that there are fewer customers demanding loans. Consumers are shying away from debt, paying down balances, and using credit cards less since the boom times ended in 2007. This is seen as a long-term consumer trend toward increased savings, lower consumption, and lower debt. So, paradoxically, there is more funding available for loans through increased savings but poorer use of capital because it is not optimizing returns through profitable lending. In addition to less lending demand, banks are providing less supply of loans because of stricter guidelines about taking on credit risk.

To compensate for this loss in lending revenues and the increased burden of regulations that lead to higher costs (discussed later), banks have looked to new fees to generate income. In fact, one bank official told me that one of the most profitable customer segments consists of people who chalk up lots of fees, such as overdraft fees. Again, paradoxically, these people are more likely to need loans and to provide hugely profitable fees but are not the best risks for loans. However, when banks, most notably Bank of America, announced that they would institute new monthly fees for debit cards, customers left in droves and the backlash caused the banks to reverse the fees. And how about those $39 late-payment fees for credit cards? These are also being tamped down by federal action (see the later discussion).

The pipeline for loans is also eroding because the “shadow banking” system is siphoning off regular banking customers. These shadow companies, including retailers, automobile manufacturers, stock brokers, insurance companies, and others, offer a full spectrum of bank services, including loans and mortgages, credit cards, and money market accounts with checking account features. For example, Walmart has become a financial service giant, offering “Money Centers” within many of its 1,800 U.S. stores where customers can pay bills and cash checks.9 E-trade and Charles Schwab offer free checking accounts with no ATM fees and the convenience to combine cash with stocks in a one-stop-shopping portfolio.

In addition to going after typical banking customers, there is a growing activity from nonbanking entrepreneurs, primarily from the retail industry, to capture the “underbanked” population. This population might not have credit cards or might be perceived as being too risky for traditional loans. For example, Walmart and American Express provide financial services through a prepaid debit card aimed primarily at low-income customers.10 Start-ups also offer prepaid cards. For example, PayNearMe caters to customers without a credit card with the corporate tag line “You can now borrow online and pay offline with cash.”11 Green Dot is a leading provider of reloadable prepaid cards that can be used wherever traditional cards like MasterCard and Visa are used. Their tag line is “Big Banks, No Thanks.”12 And NetSpend Holdings promises “The better way to bank” with prepaid MasterCard and Visa cards.13 In addition to earning revenues from banklike products, these companies are tapping another critical “natural” resource that is highly valued in the retail industry; that is, vast data on how customers are spending their money.14 One of the most important uses of these extensive vaults of data on purchasing patterns and a wide range of personal data is to refine credit risk determinations that can open the funnel on new customer segments for loans. Of course, these data can be used for pinpoint marketing as well. (Both of these issues are discussed in detail later.)

To compound the disruption, other groups are questioning the need for intermediaries like banks at all, especially when plentiful information on buyers and sellers is transparent and risk can be determined forthrightly. These groups facilitate direct peer-to-peer lending through lending clubs, between friends and families, and through crowdsourcing. For example, Prosper.com “connects people who want to invest money with people who want to borrow money, offering “seasoned returns” to investors of 9.69%.15

Last, but not least, new regulations are a big challenge for the banking industry in terms of the cost associated with compliance and the risks associated with not anticipating regulators’ needs. The Dodd-Frank Wall Street Reform and Consumer Protection Act was signed by President Obama in July 2010. This followed European finance ministers’ approval of similar regulations for much of Europe a few months earlier. However, the Dodd-Frank bill has not yet been fully defined (as of the end of 2012) in terms of the specific requirements, causing banks to be ever vigilant to the potential need for requirements. In general, the bill includes broad powers for the government to monitor systemic financial risk and to intervene where it deems necessary. Banks will be required to hold much higher levels of equity capital, and their ability to earn profits will be restrained by changes in the regulatory environment. In addition, commercial banks’ ability to take investment risks will be restrained. And the government can require banks to get smaller and even to liquidate if the bank is posing financial risks and approaching bankruptcy.

An example of the management challenges in achieving compliance is described by Julie Wooding, a consultant at FICO.16 In the example, a CEO says the new formula required by Dodd-Frank and Basel III for calculating deposit-insurance premiums takes 18 employees working on four committees to gather 60 different numbers, which are plugged into 20 separate equations to derive the bank’s “performance score.” Later we will discuss how these new work processes can be managed in the most efficient way through perfected enterprise analytics.

Another regulatory concern for banks is the creation of a Bureau of Consumer Financial Protection that will oversee and regulate the issuance of mortgages, credit cards, personal loans, and retirement plans. The bureau has a $500 million budget that does not require Congressional approval. The new agency has the authority to enforce its rules on banks with more than $10 million in assets. As of the end of 2012, the bureau was also still a work in progress. In general, banks will be required to maintain much larger levels of capital. Credit card issuers will be required to operate under modified rules that are much more consumer-friendly than in the past. Debit card processors will be required to charge lower fees on transactions.17

Key Business Drivers and Strengths

In all industries, the key business approaches to improved profitability are to cut costs, improve the balance sheet, and increase revenues. These are heightened in the banking industry because of all the challenges discussed, which force a renewed effort to make the business work much better.

Cut Costs

Improving banking productivity through cost cutting is necessary but not sufficient to achieve the ROE benchmark. McKinsey notes that banks would have to reduce their expenses by up to 6% a year between now and 2015 to achieve it. But, according to their survey data, only 2.5% of banks achieved annual cost reductions of 4% or more in the years from 2000 to 2010.18 Clearly, there might be greater routes to profitability through revenue enhancement; there are, however, clear steps for improving efficiency, and these have to do with changing infrastructure and optimizing channels.

The first infrastructure issue is a move away from bricks and mortar (bank offices and branches) for the delivery of many banking functions. Indeed, almost all typical transactions could be handled digitally19 through online channels that include self-service approaches. Branches are very expensive and are used less and less for usual retail banking transactions. The branches could be repurposed for more revenue-producing purposes. For example, some have suggested an ultra-makeover, to a cool and friendly Apple store–like place where customers can come and experience new ways to manage their money in a comfortable, low-pressure environment. Financial coaches might suggest ways to satisfy their personal needs by considering compelling financial products from the bank.

This movement away from the physical space should also happen in healthcare. I do not look forward to my visits to the medical megaplexes where much care is delivered. Clearly, some “hospitality” functions of hospitals have improved, including pianos in the lobby, single rooms, and better menus. And certainly very sick patients need to be treated in environments that aggregate resources, such as the many specialists who seem to be needed. But most care is pretty routine and can be handled virtually, which would please a large segment of customers. But it seems that one has to have an appointment for almost anything, and this can be very inefficient for the customer. Perhaps the physical space requirement exists more to satisfy the fee-for-service system and the self-serving doctrine that it is better to be safe than sorry than to get the job done on the customers’ terms. More on this in a bit in the “Strengthening the Multichannel Platform” section.

The second infrastructure issue is the need to modernize IT systems to meet regulatory demand. If all regulations in the pipeline were applied with immediate effect, the top-13 banking global players’ ROE would fall from 20% to 7% due to the increased effort required to comply.20 After the regulations are known, or predicted, many of these can be automated to dramatically reduce operating costs. An example of the complexity of regulatory demands is in the area of rules on money laundering. Simple tasks like checking the names of clients against those on a sanctions blacklist can be very complicated for banks, which might have thousands of customers with the same names as those on the blacklist. Each becomes a false positive that could embarrass the bank and ruin a client relationship. So banks turn to computers that can aggregate data from a variety of sources, including the customer’s nationality and address, the names of family members, and whether they have travelled to or received money from countries on sanctions lists.21 Additionally, upgrading legacy systems and applying advanced analytics could cut the time for many business processes; for example, cutting the cycle time for a mortgage decision to minutes rather than days.

A valuable byproduct of upgrading IT infrastructure for regulatory compliance and improved business processes is the use of new data and system capabilities to provide new insights for other banking functions such as serving customers better. This comes from full integration of all data from its various business lines and channels. Indeed, the upgrade can enable a full digitization of the business. One way of picturing how digitization can help customer service is the ability to make decisions in real time with decision rules and machine learning that lead to the right offer, to the right customer, at the right time.22

The third infrastructure issue is full enablement of multichannel capability, especially to “go mobile” and “go social.”23 Mobile becomes the new hub of transactions and communications. It is the channel preference for consumers in many industries, supplanting more fixed devices such as computers, land lines, call centers, and (soon to be archaic) ATMs across town. It provides new ways for paying and borrowing “on the go.” And most important, it is totally available to the customer to receive information and messages at the right time.

Mobile banking might not be profitable for usual banking transactions, but it is “sticky” in terms of retaining customers largely because it satisfies customers’ need for convenience, which is very important. And it might become the new table stakes on providing banking services. However, it could be a powerful platform for creating new revenues if banks turn their focus to achieving good financial outcomes for customers, thereby broadening the scope of services provided.

Related to mobile is social media in terms of capitalizing on customer preferences for peer communications. In one way, social media is a way to create “mass” intimacy in a digital age. For example, social media can be used to elicit feedback about bank initiatives and to spread messages. In another way, social media is a surveillance tool to monitor news channels, blogs, forums, Facebook, and Twitter, to monitor whether sentiment is positive or negative and to then counter the bad and reinforce the good. Social-media data can also be used to understand customers’ characteristics and predilections for supplementing marketing data by mining personal data.

Finally, a common way to attempt to reduce costs is through mergers and acquisitions. The regulatory burdens are especially difficult for small banks, and an M&A might be the surest route to (a form of) survival. Other reasons espoused for mergers and acquisitions include other ways to consolidate expense reduction, increase market power, reduce earnings volatility, and improve scale and scope economies. However, there is no compelling evidence to support the proposition that mergers and acquisitions provide a gain in value or performance, although acquired firm shareholders tend to gain a lot at the expense of the acquiring firm.24

Improve the Balance Sheet

Banks need to work with less capital and use what they have more efficiently. According to the McKinsey report, banks have made significant efforts to stabilize their balance sheets. For example, the industry Tier 1* ratios increased 11.7% in 2011, compared to 8.2% in 2007. Tier 1 capital has increased sharply 57% since 2007.25 The percentage of risky assets to total assets declined by one percentage point. These improvements show relatively good progress, largely spurred by government requirements.

* Regulators use the Tier 1 capital ratio to grade a firm’s capital adequacy as one of the following rankings: well-capitalized, adequately capitalized, undercapitalized, significantly undercapitalized, and critically undercapitalized. A firm must have a Tier 1 capital ratio of 6% or greater, and not pay any dividends or distributions that would affect its capital, to be classified as well-capitalized. Firms that are ranked undercapitalized or below are prohibited from paying any dividends or management fees. In addition, they are required to file a capital restoration plan.

In order to do more with less capital, banks are working on improving credit performance; that is, reducing the number and impact of underperforming loans and reducing credit costs. Assessing credit worthiness is at the core of the analytics that banking usually does very well. But it was stunned by the subprime mortgage crisis that neglected the core rating principles of understanding credit histories and the ability to repay. To be fair, much of the subprime mortgage activity was not done by traditional banks but by nonbank independent mortgage originators such as Countrywide. These “shadow banks” were able to mask credit issues from investors and regulators through the use of complex, off-balance sheet derivatives and securitizations.26 In fact, about 50% of the growth in mortgages in the early 2000s was attributed to nonbanks.27 This is a case of the few bad apples causing the whole bushel to rotten. However, the result, growing out of the crisis, is a refined approach to establishing credit risk. We see this as the unique banking sweet spot and will discuss it shortly.

Grow the Top Line

The biggest opportunity for banks to improve their profitability might be to become much more customer-centric. McKinsey states that a customer-centric view leads to greater loyalty, higher cross-selling, less attrition, and ultimately higher sales and profits.28 It is largely a marketing and sales function and includes cross-selling and up-selling existing customers, attracting new customers, and opening new markets for even more customer segments. The strategy, well known in the retail industry, is that by knowing customers better, with ever-increasing breadth and volume of data, and then segmenting them into useful marketing clusters, the retailer can pitch the right product, at the right time, through the right media to the customers and increase sales. In the retail chapter, we discussed how Target homes in on women in their second trimester of pregnancy and uses this “opportunity for habit change” to sell a host of products related to baby and family.

Additionally, this type of targeted sales based on segmentation can indicate those individuals who can be most profitable through a high-touch approach and those who are less profitable and can be managed adequately with high-tech approaches. The potential for granular microsegmentation to approach the realization of a virtual “market of one” can improve relationships and offers in other ways as well.

Wells Fargo Bank is known for its commitment to customers. Its vision statement reads, “We want to satisfy all our customers’ financial needs and help them succeed financially.” It also states, “Our vision has nothing to do with transactions, pushing products or getting bigger for the sake of bigness. It’s about building lifelong relationships one customer at a time.”29

In healthcare, health plans are changing their tune with customers. It’s not just about instructions to members on how to submit claims. For example, the tag line for Tufts Health Plan is “No one does more to keep you healthy.” WellPoint’s mission is to “improve the lives of the people we serve and the health of our communities.” Kaiser Permanente focuses on “Thrive...Find your groove...Wake up smiling.” The question is whether the new tune will lead to good customer experiences and outcomes and better business outcomes.

There is a good deal of vendor hype on how big data will help marketers. For example, one vendor says that big data will provide the “opportunity to understand customers at a depth that harkens back to the past of neighborhood stores and local banks” and to develop “deep, relevant and constantly improving dialogue with these customers”—and to do so at an immense scale. This proponent provides an example of pitching a product at the right time. For example, the bank knows that a customer frequently accesses her checking account via her mobile device; she also uses Web banking and handles all her banking communications electronically. Put this information together with the fact that she most often accesses her accounts in the evening at 8:00 p.m., and the data might suggest that the offer would best be sent via e-mail or text at 8:05 p.m.30 But, you know, I am not sure it matters when and how an offer is presented for a new and improved checking account. The e-mail might go directly to the trash bin if the recipient knows that it comes from the bank.

Another example comes from Singapore. Citigroup keeps an eye on customers’ credit card transactions for opportunities to offer them discounts in stores and restaurants. (Say what, from a bank?) The customer swipes a credit card; the analytics checks the time of day, the location, and previous shopping or eating habits and then recommends, through a text message, an Italian restaurant just down the street that meets the customer’s profile. It could result in the bank getting a second card transaction and a cut from the restaurant. The model for this is Amazon’s online store, which recommends items that a customer might like based on previous purchases and on what similar customers have bought.31

Another approach to knowing the customer well is to go beyond product pitching and restaurant referrals and give them useful information products. For example, Britain’s Lloyds Banking Group wants to go beyond answering “what’s left in my balance” to advise customers on a prediction of how much they will have available after all their usual bills are paid. And products like Quicken and Yodlee sell software to banks that they can provide to customers to help them manage their money.32

Finally, new revenues can be grown by repurposing the branch office as alluded to earlier. An example of this is OCBC, which “aims to convey honesty, sincerity, and simplicity,” and according to them “may be the coolest bank Gen-Y has ever seen.” They use retail stores modeled after a shopping experience and create credit cards with customized designs to express their personality. Also, SNS Bank has storelike outlets, tablets that customers can use, and extended hours.

Quite frankly, however, financial products like checking accounts and CDs are pretty stodgy and do not have the pizazz of iPads or the broad array of the latest and sexiest products from Target and Apple. And I am not sure how many profitable customers would be attracted to the bank by having their dog’s picture on their credit card. Certainly, high-end retailers attempt to turn their showrooms into a living room, including a piano player, to make the customer comfortable and also primed for buying. And wealth management services from banks can have very tony physical environments for its richest customers. The question is whether this radical bricks-and-mortar reinvention will attract more than this upper slice of customers, and perhaps the cool Gen-Y’ers, and deliver more revenues. This transformation would require much more than a reuse of physical assets as well. It would also require the staffing of branches to change from bank tellers to financial friends and advisors.

Culture intrudes. We have talked a lot about possibilities for growth so far and some concrete examples. But, as mentioned at the outset of this chapter, the state of the art in banking is quite different from the state of the practice. There are examples of best practice, for sure, but for many banks the journey to sustainable growth has just begun and it has more to do with the sociology than the technology. Sean Rowles, EVP for Citizens Bank, formulates a “banking hierarchy of needs,” ranging from the base of the pyramid on what he calls survival mode to apathy mode in the middle and to advocacy mode at the apex. Many banks are in survival mode and focus on regaining trust and being safe in terms of taking on risk and complying with regulations. But this strategy does not lead to more revenues and might actually increase costs. The second level is apathy and is marked by being convenient, as with multiple channels, and by being competent in the usual banking initiatives. This can produce modest increases in revenues. At the top of the pyramid is customer advocacy where the customer is king and queen and the approach is to “meet my needs, be approachable, and know me.”33 Clearly, a bank’s success in achieving sustainable growth will be how fast and well it can get up the curve.

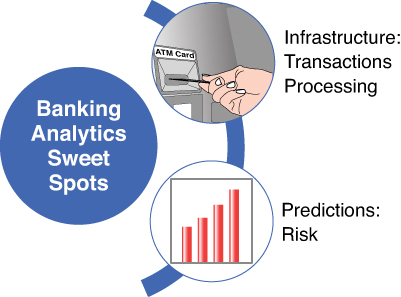

Analytics Sweet Spots

Relative to the key business drivers just described, this section turns to selected analytic sweet spots that support a few business solutions that are unique to banking and offer promise for healthcare (see Figure 5.1).

It boils down to two sweet spots: (1) infrastructure: transactions processing and (2) predictions: risk.

Infrastructure: Transactions and Processing

The banking industry has been a pioneer in new technologies for handling transactions. It started with ATMs, automated teller machines. ATMs were a significant advance in service and convenience for customers and were no small miracle of technology. No longer did customers have to enter the bank, stand in line, and wait for human tellers to cash checks, receive cash, and make deposits. The success of the self-service approach was picked up by other industries, most notably energy, in which people could pump and pay for their own gas at stations. Today, people can get medicines and DVDs and much more from self-service machines.

The first ATM was put into use over 50 years ago in a shopping center in Ohio. Today, ATMs are everywhere. In fact, there are 370,000 automated teller machines across the United States, or about 1 for every 296 people. Compare this to the number of doctors per person in the U.S. (2.3/1000)34 and you can see that people “demand” about 50% more ATMs than MDs. Perhaps if the provision of medical care were more virtual and as efficient as banking with ATMs, the demand would increase, prices would fall, and outcomes would improve.

The driving force for ATMs was most certainly cost reduction. But consumers grew to love them even though they harbored worrisome concerns about being robbed at the machine. Similarly, would anybody in their right mind want to handle extremely flammable liquids to save a few cents on a gallon of gasoline? People were willing to accept these risks in order to lower the friction costs of being served by slower humans. And beyond that, the industry developed the “new normal” through mere force of presence, convenience, and rewards.

ATM usage is on the decline. The preferred banking method now is Internet banking, with more than 50% of customers using it. But it too is being eclipsed. Just as ATMs reduced the demand for branch office visits and the Internet supplanted the need for field trips to the ATM, mobile is clearly the emerging channel of choice today. Mobile combines higher levels of convenience with new paperless technologies. For example, mobile apps allow one to take a picture of a check with a smartphone and to deposit it on the fly.

Banks are also looking to technology to improve customer (self) service through natural language processing. Citigroup is working with IBM on how to advance “customer interactions” by using IBM’s supercomputer “Watson.”35 Recall that Watson was the computer contestant that beat the best-performing humans at Jeopardy. The Watson system is powered by its DeepQA software, which is able to ingest large quantities of information and respond to questions with a series of options and related probabilities. For example, it could “know” the customer’s financial situation thoroughly and be able to answer customer questions as well as or better than humans and to offer financial advice and products. It is not clear how well robots will contribute to improving customer centricity, although they certainly will reduce costs.

Healthcare is the other industry where Watson is looking for opportunities. IBM is working with WellPoint and Cedars Sinai Cancer Institute to train a new generation of robotic physician assistants. These could inform doctors of the pertinent points on the vast medical research on cancer, as well as a patient’s medical and genomic history, to help with differential diagnosis.36

What banks need now are AMTs, or All Multichannels Together, to allow for seamless transactions through many channels, especially with mobile at the hub. With all channels integrated, the amount of information about a customer multiplies and can be harvested for other business needs. However, the information system infrastructure needed to support the multichannel environment and to wring out insights from all the emitted data is more complex and costly than most existing core systems.

Similarly, banks are under great pressure to anticipate and respond to regulatory requirements. The risks of noncompliance are huge. And as they venture up the curve to be truly customer-centric, they will need to gather and integrate all the information from a variety of sources to know customers better in order to offer tailored products and keep them away from savvy upstart competitors.

To master all these demands, banks need to perfect two fundamental pieces of analytics: Get the business basics right and strengthen the platform for the digital future.

Getting the Business Basics Right through Analytics

Banking needs to make the business work better. It requires a commitment to industrialize its processes. This involves improving its core administrative IT systems and, perhaps, modernizing legacy systems. It has to do the basics right and then reap the rewards in efficiency gains.

Perhaps the most fundamental improvement is to organize the data around the customer. Banks, like other industries, operated in silos related to business units, product teams, or acquisitions, and the information systems were centered on each business’s needs. There was little coordination among the different groups with the whole enterprise in mind, and customers might have received duplicative offers. The enterprise was simply not able to get a full picture of its customers across the various parts of the business.

What does this full picture, or 360-degree view of the customer, provide? It can inform the business about (1) the products the customer uses and her interactions with customer service, (2) how she responds to incentives and conducts banking business, (3) what she buys from other banks, and (4) how she uses different channels.

Now, this vision of a 360 view of the customer has been discussed for decades. A number of banks have taken the leap, but most have chosen not to. After all, it is a big and expensive deal and usually is associated with large-scale legacy system improvements. The ROI for a 360-degree view is more a vision than an evidence-based assurance. Indeed, a lot of the push for a customer-centric view and its associated IT requirements comes from vendors marketing the “art of the possible.”

An example is a report from IDC Financial Insights on “Banking for Success: Using Analytics to Grow Wallet Share.”37 IDC is a provider of research-based advisory and consulting services for the finance industry. The white paper advocates the value of customer relationships and the analytics that support it (customer analytics) to increase profits. Its primary business case is that customer analytics leads to improved marketing success. It gives a scenario, based on client data, of the potential benefits. The scenario is for a retail bank with ten million customers and $2.75 billion in revenue. The total estimated benefits amount to $43 million from the following categories:

• Reduce customer churn $21M

• Increase revenue per customer $16M

• Increase revenue from loan activity $5M

• Reduce cost of marketing $1M

The benefits, or $43 million, represent about 1.5% of revenues. But the cost of producing the benefits is not included such that an ROI cannot be calculated. Upgrading a legacy platform can easily take tens of millions of dollars. So if this is the state of the art in making the case for customer analytics to improve marketing results, it is incomplete. And it is understandable why there might be a reticence to invest in it.

The other fly in the ointment about moving to a 360 view might have more to do with the sociology than the technology. The sociology has to do with the reservations that banks might harbor about being fully customer-centric. They might sense that customers will not be receptive for a variety of reasons; for example, the trust issue, the limited portfolio of products, and the culture of moving from tellers to advisors.

While the sociology ripens and the evidence accumulates on the eventual need for moving toward a customer-centric platform, there are other analytics that demand quick action. The biggest one is that regulations are overbearing and modernizing core systems to comply is a survival issue. Legacy systems might not be flexible enough to adapt well to the changes. For example, rules might be hard coded into legacy systems, requiring extensive software modifications. So the need for flexibility and scalability often spells the need to retool or replace legacy systems. The good news is that software and hardware are getting much better to accommodate real-time decision making, including the use of in-memory databases to work with large sets of data with minimal time delays, cloud computing, service-oriented architecture, and capacity to manage big data from old and new sources such as unstructured data and social media.

A healthcare example of the benefits of modernizing core administrative systems comes from the IBM publication “The Value of Building Sustainable Health Systems.”38 This white paper offers quantitative estimates of the benefits for health plans in adopting a tiered transformation road map based on analytics development and related competencies. The first tier of the model is to improve core administrative systems, and the second is to address proactive regulatory management. Later stages include innovations in market offerings and business transformation and agility. The research estimates that with a “fully deployed” analytics program as specified, a mid-size health plan could net a potential $644 million annually in economic benefits.

The first stage involves simplifying IT systems, data, and infrastructure, as well as modernizing claims, benefits, and enrollment processes. The estimated annual benefits are $129 million, which is derived mostly by reducing IT costs and harvesting the data to reduce medical costs. In the second stage of regulatory management, most of the overall benefit of $61 million comes from reducing the administrative cost of compliance and by subsequently using the new data capability to reduce medical costs.

Again, as with the IDC example, the investment cost to achieve the benefits is not stated. Also, the benefits represent capturing the fully matured opportunity, that is, what is possible if everything is accomplished and if all the stages in the implementation proceed without a snag.

Strengthening the Multichannel Platform

In addition to strengthening the basics, banks must build new capacity in the areas of mobile and social media. Mobile is the answer to a strong customer demand for convenience, but it also provides business opportunities for marketing and strengthening customer loyalty. And social media is a consumer force not to be ignored. It is an opportunity area to build customer intimacy by being socially engaging. And it can aid marketing and mitigate reputation risks.

Today, many banks have projects underway to pull together customer data from all channels—branch, ATM, online banking, mobile banking, call center, social media sites—in one place as an “intelligent multichannel bank.” The payoff is to mine the data in real time and use it to cross-sell, up-sell, detect fraud, and keep customers in the right products.39 Additionally, the multichannel integration produces new data to facilitate pervasive analytics as with predictive modeling and including microsegmentation. And the platform can make the data available in near real time to service all aspects of the business.

In healthcare, the emphasis and excitement are less on building and mining multichannelintelligence and more on using mobile health (mHealth) applications to improve care. The number of health-centric apps on Apple devices has more than quadrupled since 2010 to about 19,000, with more than a quarter for health professionals.40 The doctor’s black bag has given way to digital tools. Smartphones have amazing capabilities, including the camera, GPS tracking, and call history, which can help with medical treatments. And social media is becoming an important channel of communication, especially with younger patients, such that the phrase that the “doctor will see you now” is supplanted with “the doctor will Tweet you now.” The GPS feature of smartphones has enabled interesting applications for monitoring patient progress. For example, pain and depression can result in less activity. An app that tracks how often a patient sends text messages and places calls, and how often he moves and where he goes, when compared to previous behavior, can provide an early indicator that the patient is withdrawing or becoming less active and could indicate a flare-up of illness.41 Similarly, the camera feature can be used to take pictures of skin lesions that might be indicative of melanoma and send it for analysis and advice about whether to consult a dermatologist.42 And because iPhones are what teenagers live and die for, the perfect channel to send health messages is through Twitter, including hyperlinks to cool Web sites with teenager-friendly materials, rather than the usual stodgy medical handouts.43

Predictions: Risk

The cashier swipes your card and smiles. Before she hands it back, complex mathematical models hundreds of miles away crunch the data: If you’ve hit your credit limit, should it be extended? Is it really you using the card?44

We are all familiar with filling out the forms to get a credit card, car loan, and mortgage. We know the importance of our FICO score, which is the primary metric that determines whether we will get a loan and at a good rate. We also know about how the lending threshold for home loans was lowered such that subprime loans were issued on a mass scale, which contributed mightily to the meltdown. Subsequently, capital dried up and one had to have a stratospheric FICO number to get a loan. All this, and disruptive innovators entering the space, spurred a refinement in thinking about how to assess the likelihood that a customer will follow through with the obligation to repay a loan.

What is FICO and why is it so important to banking...and to healthcare? FICO is an acronym for Fair Isaac Corporation, the creators of the score. (One might have imagined that the acronym would have stood for something really momentous, like the Financial Index that Controls Outcomes.) It is a summary score of an individual’s past performance in paying off debt and a prediction of future behavior to make good on a loan. It is derived from data on payment history, current level of indebtedness, types of credit used, length of credit history, and new credit. People receive scores between 300 and 850. Above 650 indicates a very good history. FICO is usually the most important indicator of the person’s credit trustworthiness to follow through and pay off a loan. Often it is the only number a lender really looks at.

In healthcare, there is no clear analogue to a FICO score. But there should be. We propose the HICS, the Health Improvement Capabilities Score. This would be an overall indicator of an individual’s capability to do their part in getting better. The HICS value would appear on each patient’s chart and would guide treatment decisions just like diagnostic values from laboratory tests do. It is very important because much of the untapped resource for health improvement lies with the individual. In fact, as discussed previously, healthcare accounts for only 10% of improvements in health functioning, whereas personal behavior accounts for 40%.

Doctors lament the fact that patients do not “comply” with “prescribed” medications or treatment “orders.” Yet there are many reasons why the HICS might be low, and caregivers should be fully cognizant of them if their goal is improved patient outcomes. More on this later after we learn more about the specifics that banking can teach us about making judgments on capabilities.

What’s clear is that lending practices are changing and a broad swath of new data is being used in predictive modeling to understand risk better. The first response to the crisis might have been to not lend because of fear of loan defaults, which were high on the list of oversight metrics. Some banks reasoned that they should just wait until the smoke clears. On the other hand, if banks do not lend, new competitors outside the banking industry are more than willing to step into the gap and gain the business.

So the reality is that banks must lend, but must do it differently. In an address to the FICO World 2012 Conference, PNC Executive Vice President and Credit Executive Gordon Cameron said that banks need to lend and with a new approach:

“We need to change the way we measure risk, understand consumers, and make credit decisions. As the recession showed, the systems most banks use today simply aren’t ready for the new lending environment.”45

He said that banks must move away from static measures of consumer risk and customer behavior, and develop adaptive systems that identify changes in behavior more rapidly, estimate likely future changes, and change decisions as a result.

The underlying analytics for measuring risk is predictive analytics. It provides insight on future behavior that can help identify the best action to take on every customer and transaction. For example, in fraud detection, the modeling can detect subtle aberrations from the norm/expected in applications, purchases, claims, transactions, and more. It can detect whether the right person is using a credit card and, if not, indicate to not approve the purchase. Or if the credit limit is reached, it can decide to extend the limit to achieve more purchasing, leading to more lending. It can make loan decisions in seconds through a series of algorithms. It can match personal characteristics with sales campaigns to offer the right product at the right time. And it can do these calculations with reliable precision, embedded in processes in the back office. It can predict whether a customer is likely to switch to a competitor. It creates customer segments based on patterns of similarity and relationship to a specific product or outcome. It can predict customers’ future behavior in relation to spending. And much more.

The fuel for predictive engines is data, lots of it, and different kinds of it.

The amount of publicly available data about each and every one of us grows all the time, to the point where an organization with the will, the patience, and the right software can analyze in detail our financial transactions, our habits, our political leanings, our preferences, and our geographic location, among other things.46

Perhaps the most instructive view on the new uses of predictive analytics comes from new banking competitors and their disruptive ways to know customers better and steal them away from banks. For example, ZestCash47 provides loans to people with bad or no credit histories. One of its tag lines is “All data is credit data...and we should be using it all to make better underwriting decisions.” It was started by Douglas Merrill, a former chief information officer and head of engineering at Google. It goes beyond a reliance on FICO credit scores, thought to be based on 15 to 20 variables, and looks at thousands of indicators. For example, if a customer calls to say she will miss a payment, most banks ding the customer as a poor risk. But ZestCash has found through its data mining that such customers are actually more likely to repay in full. Another useful signal is the length of time customers spend on ZestCash’s Web site before applying for a loan. It is not clear what this might be indicative of but it is a variable in their predictive models.

Wonga48 is a British start-up that offers loans for very short periods. On its Web site it says that it can “deposit up to £400 in your bank account by 22:31 today,” or five hours away. It also looks at a huge range of data such as e-mail address and social-network sites, to make credit decisions practically in real time.

Another firm, Cignifi,49 mines mobile-phone records. It says that “anyone with a mobile phone can be credit scored.” It looks at variables such as the time when calls were made, their frequency, and the whereabouts of the callers for clues about their likelihood to repay loans.

Tesco,50 a large British retailer, like other retailers described in the retail chapter, uses its customers’ purchasing data to send targeted coupons. For example, “when a household starts buying nappies, signaling the arrival of a new baby, Tesco usually sends discount vouchers for beer, knowing that the new father will have less opportunity to go to the pub.” The firm has banking ambitions. It offers credit cards and loans and plans to introduce full bank accounts. Given the depth of its databases, it might well assess the creditworthiness of its customers on the basis of their grocery shopping.51

CoreLogic is a full-service financial information company that provides information on personal characteristics related to risk assessment, as with credit applications and collection procedures. They maintain 215 million consumer credit records representing more than 35 million unique customers.52 What’s most intriguing is the breadth and depth of the information they collect and synthesize. They collect more than 100 credit variables. They derive information from traditional sources, including credit bureaus, public records, and bank accounts. And they collect it from nontraditional sources, including payday loan companies, rental purchase stores, credit card companies, consumer finance businesses, nonprime auto lenders and credit unions, eviction notices, bankruptcy proceedings, criminal history, mortgage deeds, and many more. These data are all provided to client companies to help them cover risks more accurately.

There is also a push from credit raters in getting data for a “secondary underwriting screen for credit” that includes data on paying consistently over a substantial period (as with rental payments), buying life insurance, education attainment, employee effectiveness, parent effectiveness, and sticking with an exercise program. And the way to get the data is through “meaningful dialogues and listening.”53 Whoa. Meaningful dialogues? What has come over bankers? Isn’t the readily available big data enough? How are they going to find out about their customers stick-to-itiveness with exercise programs? Well, they are going to ask them. And they need the data to recruit, retain, please, and optimize their customers. They know that if they do not know their customers well, competitors will steal the space. And they do this despite stringent privacy concerns related to consumer protection. They must ensure that they are using fair and consistent lending practices, sharing information appropriately, and securing personally identifiable data.54

Getting back to the HICS. Banks are very clear on what their primary outcomes are: profitable loans. They have honed analytics to determine the capabilities of their customers to follow through on their obligations. And they are interested in extending the period of assessment from a static determination to one that is more dynamic and continuous over time. They even understand the correlates of successful outcomes beyond the traditional confines of financial metrics. In so doing, both the bank and its customers can be partners in the success that both want. And this will require, perhaps, a good deal more sharing of personal information, which might be possible only through a trusting relationship. And this might be the fly in the ointment for banks, but not necessarily for healthcare.

Banking can teach healthcare that it is important to understand and manage the capabilities and obligations of its customers. In healthcare, these obligations and capabilities are hardly taken into account. What if the composite HICS score were listed on the patient’s medical record? A low score would indicate to the caregiver that the patient was unlikely to follow through with recommendations on how to get healthier. The score could be decomposed into its component parts such as these:

• Inability to engage in care due to finances such as underinsurance and low income

• Lack of family support

• Previous noncompliance with treatment plans and medication regimens

• Poor education

• Cultural issues

• Lack of transportation

• Lack of availability of nutritious food

• Restrictive health-plan benefits

It is understandable why such a score does not exist in healthcare. Care is fragmented. Achieving health is not always the goal. Payment policies support individual rather than coordinated approaches to care, and focus on how many things were done rather than how well. There is industry fuzziness about defining outcomes and using these in performance measurement of systems. Accountable care organizations can address these concerns. But, for now, let’s put the HICS score on the chart and in the values statement for the organization to put a spotlight on the need to attend to people’s capabilities and supports, or lack thereof, to improve their health. And then to do something about it.

An example is the organization Health Leads.55 It strives to ensure that one day all doctors will be able to prescribe solutions that improve health, not just manage disease. These prescriptions include the need for food, housing, health insurance, job training, fuel assistance, and more, which are often more influential in producing health than “traditional” healthcare. Health Leads “connects the dots” between the healthcare system and social systems and achieves improved health results through an innovative business model. For example, they note that “every day in America, doctors prescribe antibiotics to patients who have no food at home or are living in a car.” It is not the doctor’s job to improve the social determinants of health for society, and they don’t have the time or knowledge to address patients’ basic resource needs. The HICS can help in this assessment and provide information to caregivers and then coordinate the provision of enablers for better health attainment through organizations like Health Leads.

Conclusions

The unique analytic sweet spots in banking are efficient transaction processing, self-service channels, and risk prediction. The challenges facing the industry are daunting. Analytics can help it lift out of doldrums and to new heights. And the shape that analytics takes in the pressure cooker of reform and business survival should produce analytic resources that other industries can learn from.

The business demands of banking are not unlike those of the healthcare industry, especially health plans. The Affordable Care Act imposed sweeping changes on the health insurance industry on a par with the reforms in the banking industry. Health insurers face a good deal of oversight, changes to basic coverage, and a reorientation toward the “real” customer. Both industries face commodification and an assault from disruptive innovators. The IT challenges and opportunities to support the business are significant. For both industries, a major challenge will be (re)establishing a mutually satisfying relationship with its customers after a long period of relative disregard.

The need to make the business basics work better through analytics is the first order of business in both industries. Both need to respond to a huge list of compliance requirements, and both need to adapt to the changing preferences of their customers in terms of business channels. Mobile applications appear to be the epicenter of transactions and communications.

Both industries seem to be traveling on a similar journey and at about the same point. Banking has a bit of a head start in making the business run better through analytics, but the lessons are not complete at this point.

The real lesson from banking is its depth of experience and techniques to understand risk. The risk has to do with the capabilities and motivation of its customers to carry through on their obligations in the partnership with the bank; that is, to repay a loan commitment. It is acquiring more and varied information to understand its customers better, which will improve loan risk assessment and might improve relationships if it does not breach basic privacy rights. But what is so starkly different in healthcare is the industry’s blind spot in understanding people’s capabilities and constraints to follow through with treatment “orders” and then to do something about the situation. Rather, healthcare prescribes its solutions to patients and moves on to the next prescription without considering the overwhelming importance of other determinants of health. The one big, unique solution from banking for healthcare is to have an analogue to banking’s FICO score, called the Health Improvement Capabilities Score, which should be considered as much as lab values and other findings in guiding the course of care.