Chapter 19

MANAGERIAL ACCOUNTING

| The Navigator | |

After studying this chapter, you should be able to:

- Explain the distinguishing features of managerial accounting.

- Identify the three broad functions of management.

- Define the three classes of manufacturing costs.

- Distinguish between product and period costs.

- Explain the difference between a merchandising and a manufacturing income statement.

- Indicate how cost of goods manufactured is determined.

- Explain the difference between a merchandising and a manufacturing balance sheet.

- Identify trends in managerial accounting.

![]()

PREVIEW OF CHAPTER 19

Beginning with this chapter, we turn our attention to issues such as the costs of material, labor, and overhead and the relationship between costs and profits. The remaining chapters in this textbook focus primarily on the preparation of reports for internal users, such as the managers and officers of a company. These reports are the principal product of managerial accounting. The content and organization of this chapter are as follows:

![]()

Managerial Accounting Basics

1. (L.O. 1) Managerial accounting is a field of accounting that provides economic and financial information for managers and other internal users. Managerial accounting applies to all types of businesses—service, merchandising, and manufacturing—and to all forms of business organizations—proprietorships, partnerships and corporations. Moreover, managerial accounting is needed in not-for-profit entities as well as in profit-oriented enterprises.

Comparing Managerial and Financial Accounting

2. There are both similarities and differences between managerial and financial accounting.

a. Both fields of accounting deal with the economic events of a business and require that the results of that company's economic events be quantified and communicated to interested parties.

b. The principal differences are the (1) primary users of reports, (2) types and frequency of reports, (3) purpose of reports, (4) content of reports, and (5) verification process.

3. The role of the managerial accountant has changed in recent years. Whereas in the past their primary concern used to be collecting and reporting costs to management, today they also evaluate how well the company is using its resources and providing information to cross-functional teams comprised of personnel from production, operations, marketing, engineering, and quality control.

Management Functions

4. (L.O. 2) Managers perform three broad functions within an organization:

a. Planning requires managers to look ahead and to establish objectives.

b. Directing involves coordinating a company's diverse activities and human resources to produce a smooth-running operation.

c. Controlling is the process of keeping the firm's activities on track.

Organizational Structure

5. Most companies prepare organization charts to show the interrelationships of activities and the delegation of authority and responsibility with the company.

Stockholders own the corporation but manage the company through a board of directors. The chief executive officer (CEO) has overall responsibility for managing the business. The chief financial officer (CFO) is responsible for all of the accounting and finance issues the company faces. The CFO is supported by the controller and the treasurer.

Business Ethics

6. All employees are expected to act ethically in their business activities and an increasing number of organizations provide their employees with a code of business ethics.

7. Due to many fraudulent activities, U.S. Congress passed the Sarbanes-Oxley Act of which resulted in many implications for managers and accountants. CEOs and CFOs must certify the fairness of financial statements; top management must certify they maintain an adequate system of internal controls, and other matters.

8. (L.O. 3) Manufacturing consists of activities and processes that convert raw materials into finished goods.

9. Manufacturing costs are typically classified as either (a) direct materials, (b) direct labor or (c) manufacturing overhead.

10. Direct materials are raw materials that can be physically and conveniently associated with the finished product during the manufacturing process. Indirect materials are materials that (a) do not physically become a part of the finished product or (b) cannot be traced because their physical association with the finished product is too small in terms of cost. Indirect materials are accounted for as part of manufacturing overhead.

11. The work of factory employees that can be physically and conveniently associated with converting raw materials into finished goods is considered direct labor. In contrast, the wages of maintenance people, timekeepers, and supervisors are usually identified as indirect labor because their efforts have no physical association with the finished product, or it is impractical to trace the costs to the goods produced. Indirect labor is classified as manufacturing overhead.

12. Manufacturing overhead consists of costs that are indirectly associated with the manufacture of the finished product. Manufacturing overhead includes items such as indirect materials, indirect labor, depreciation on factory buildings and machines, and insurance, taxes, and maintenance on factory facilities. Manufacturing overhead equals all manufacturing costs except direct material and direct labor.

Product Versus Period Costs

13. (L.O. 4) Product costs are costs that are a necessary and integral part of producing the finished product. Period costs are costs that are matched with the revenue of a specific time period rather than included as part of the cost of a salable product. These are nonmanufacturing costs. Period costs include selling and administrative expenses.

Manufacturing Income Statement

14. (L.O. 5) The income statements of a merchandising company and a manufacturing company differ in the cost of goods sold section.

15. The cost of goods sold section of the income statement for a manufacturing company shows:

Determining Cost of Goods Manufactured

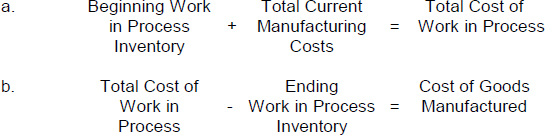

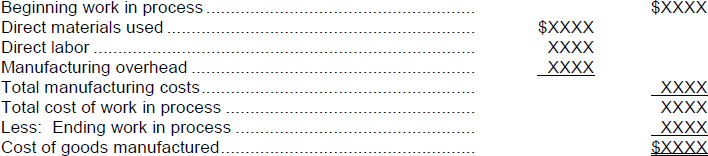

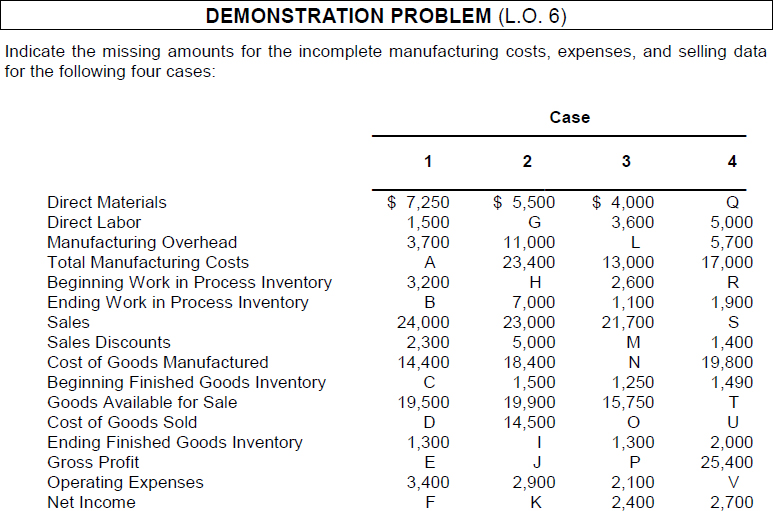

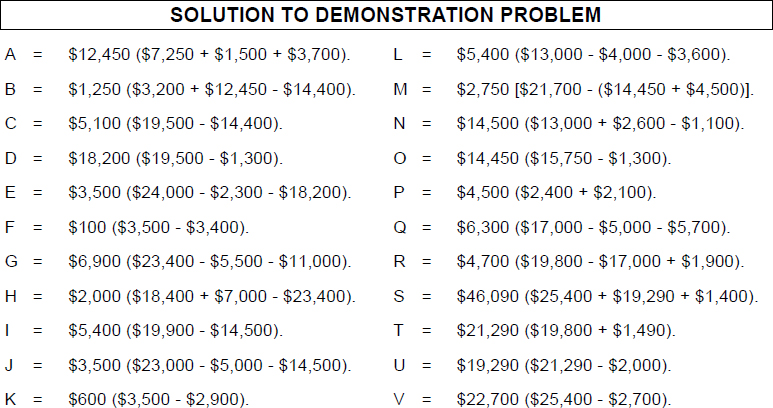

16. (L.O. 6) The determination of the cost of goods manufactured consists of the following:

17. The costs assigned to the beginning work in process inventory are the manufacturing costs incurred in the prior period.

18. Total manufacturing costs is the sum of the direct materials costs, direct labor costs, and manufacturing overhead incurred in the current period.

19. Because a number of accounts are involved, the determination of costs of goods manufactured is presented in a Cost of Goods Manufactured Schedule. The cost of goods manufactured schedule shows each of the cost factors above. The format for the schedule is:

Manufacturing Balance Sheet

20. (L.O. 7) The balance sheet for a manufacturing company may have three inventory accounts: finished goods inventory, work in process inventory, and raw materials inventory.

21. The manufacturing inventories are reported in the current asset section of the balance sheet.

a. The inventories are generally listed in the order of their expected realization in cash.

b. Thus, finished goods inventory is listed first followed by work in process and direct materials.

22. Each step in the accounting cycle for a merchandising company is applicable to a manufacturing company.

a. For example, prior to preparing financial statements, adjusting entries are required.

b. Adjusting entries are essentially the same as those of a merchandising company.

c. The closing entries for a manufacturing company are also similar to those of a merchandising company.

23. (L.O. 8) Contemporary developments in managerial accounting involve: (a) a U.S. economy that has in general shifted toward an emphasis on providing services, rather than goods; and (b) efforts to manage the value chain and technological changes.

24. The value chain refers to all business processes associated with providing a product or service. Many companies have significantly lowered inventory levels and costs using just-in-time (JIT) inventory methods. Under a just-in-time method, goods are manufactured or purchased just in time for use. In addition, many companies have installed total quality management (TQM) systems to reduce defects in finished products.

25. The theory of constraints is a specific approach used to identify and manage constraints or bottlenecks in order to achieve the company goals. Activity-based costing (ABC) is a popular method for allocating overhead that obtains more accurate product costs. The balanced scorecard is a performance-measurement approach that uses both financial and nonfinancial measures to evaluate all aspects of a company's operations in an integrated fashion. In addition, many companies have begun to evaluate not just corporate profitability but also corporate social responsibility.

![]()

![]()

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

![]()

MULTIPLE CHOICE

Circle the letter that best answers each of the following statements.

- (L.O. 1) Which of the following would not describe managerial accounting reports?

- They are internal reports.

- They provide general purpose information for all users.

- They are issued as frequently as the need arises.

- The reporting standard is relevance to the decision to be made.

- (L.O. 1) Financial and managerial accounting are similar in that both:

- have the same primary users.

- produce general-purpose reports.

- have reports that are prepared quarterly and annually.

- deal with the economic events of an enterprise.

- (L.O. 2) The function of coordinating the diverse activities and human resources of a company to produce a smooth running operation is:

- planning.

- directing.

- controlling.

- accounting.

- (L.O. 2) The function that pertains to keeping the activities of the enterprise on track is:

- planning.

- directing.

- controlling.

- accounting.

- (L.O. 2) The function that involves looking ahead and establishing objectives by management is:

- planning.

- directing.

- controlling.

- accounting.

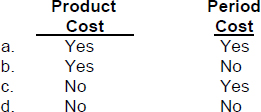

- (L.O. 4) Direct materials are a:

- (L.O. 4) Direct labor is a(n):

- nonmanufacturing cost.

- indirect cost.

- product cost.

- period cost.

- (L.O. 4) For a manufacturing company, which of the following is an example of a period cost rather than a product cost?

- Depreciation on factory equipment.

- Wages of salespersons.

- Wages of machine operators.

- Insurance on factory equipment.

- (L.O. 4) Property taxes on a manufacturing plant are an element of:

- (L.O. 4) The salary of a plant manager would be considered a:

- (L.O. 5) For the year, Mahatma Company has cost of goods manufactured $325,000, beginning finished goods inventory $150,000, and ending finished goods inventory $175,000. The cost of goods sold is:

- $275,000.

- $300,000.

- $325,000.

- $350,000.

- (L.O. 5) If the cost of goods manufactured is less than the cost of goods sold, which of the following is correct?

- Finished Goods Inventory has increased.

- Work in Process Inventory has increased.

- Finished Goods Inventory has decreased.

- Work in Process Inventory has decreased.

- (L.O. 6) The account that shows the cost of production for those units that have been started in the manufacturing process, but that are not complete at the end of the accounting period is:

- Raw Materials Inventory.

- Work in Process Inventory.

- Finished Goods Inventory.

- Cost of Goods Sold.

- (L.O. 6) Nehru Company has beginning and ending raw materials inventories of $32,000 and $40,000, respectively. If direct materials used were $130,000, what was the cost of raw materials purchased?

- $130,000.

- $140,000.

- $122,000.

- $138,000.

- (L.O. 6) Ghindia Company has beginning and ending work in process inventories of $52,000 and $58,000 respectively. If total current manufacturing costs are $248,000, what is the total cost of work in process?

- $300,000.

- $306,000.

- $242,000.

- $254,000.

- (L.O. 6) Mura Company has beginning work in process inventory of $72,000 and total current manufacturing costs of $318,000. If cost of goods manufactured is $320,000, what is the cost of the ending work in process inventory?

- $60,000.

- $74,000.

- $80,000.

- $70,000.

- (L.O. 6) If the total manufacturing costs are greater than the cost of goods manufactured, which of the following is correct?

- Work in Process Inventory has increased.

- Finished Goods Inventory has increased.

- Work in Process Inventory has decreased.

- Finished Goods Inventory has decreased.

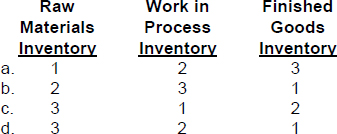

- (L.O. 7) The inventory accounts that show the cost of completed goods on hand and the costs applicable to production that is only partially completed are, respectively

- Work in Process Inventory and Raw Materials Inventory.

- Finished Goods Inventory and Raw Materials Inventory.

- Finished Goods Inventory and Work in Process Inventory.

- Raw Materials Inventory and Work in Process Inventory.

- (L.O. 7) In the current asset section of a balance sheet, manufacturing inventories are listed in the following sequence:

- (L.O. 8) When companies allocate overhead based on each product's use of activities in making the product, this is known as:

- Just-in-time (JIT) inventory.

- Value chain allocation.

- Activity-based costing.

- total quality management.

![]()

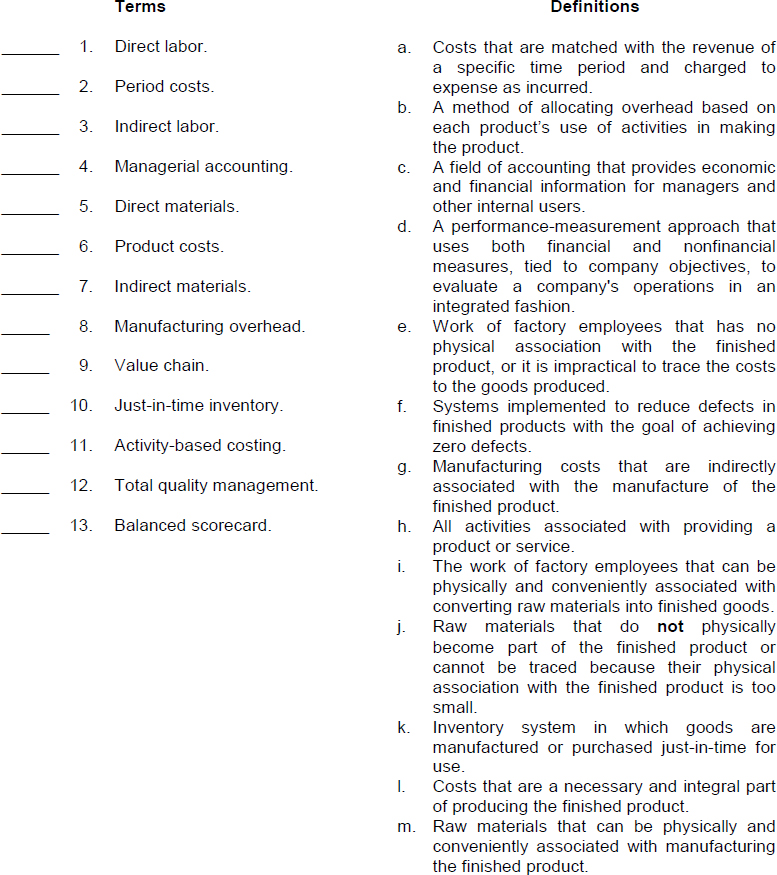

Match each term with its definition by writing the appropriate letter in the space provided.

![]()

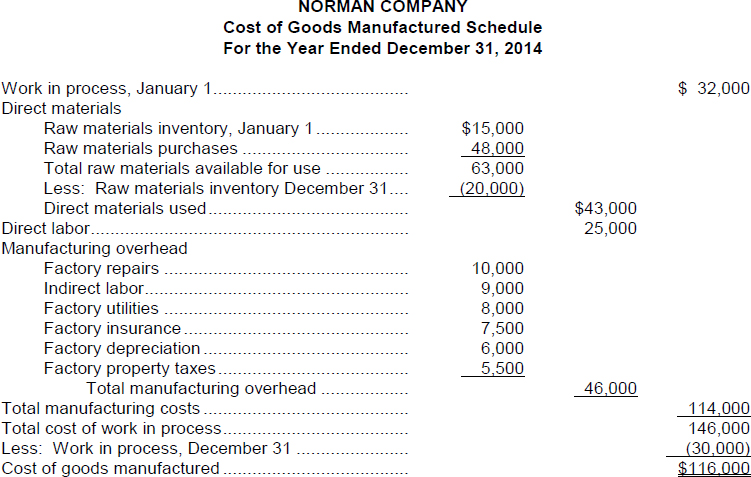

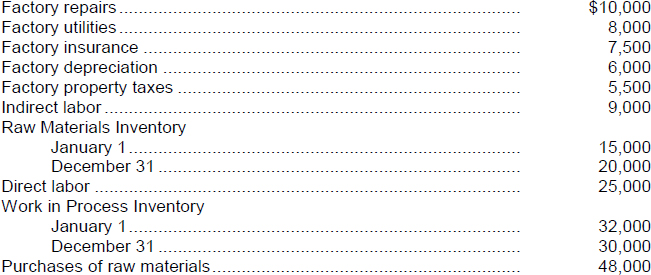

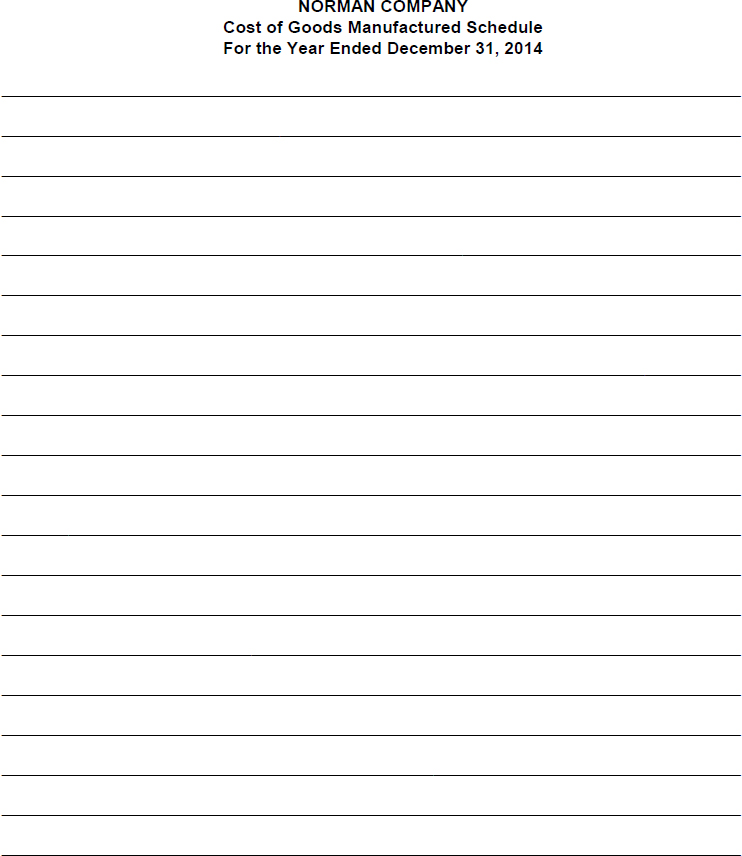

EX. 19-1 (L.O. 6) At the end of 2014, the following information pertains to Norman Company:

Instructions

Prepare a Cost of Goods Manufactured Schedule for Norman Company.

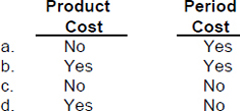

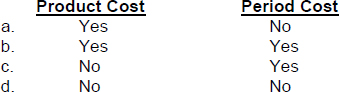

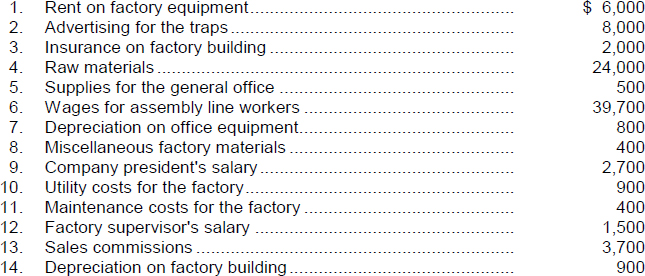

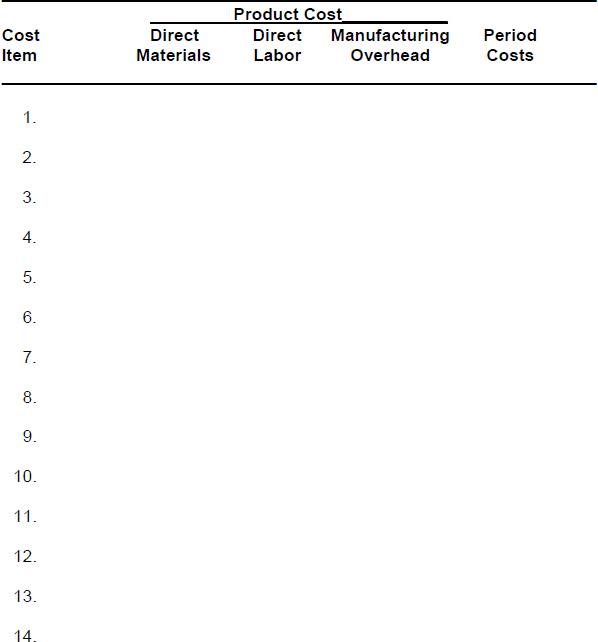

EX. 19-2 (L.O. 3 and 4) The Svengooli Company specializes in manufacturing woodchuck traps. The company has a large number of orders to keep the factory production at 10,000 per month. Svengooli's monthly manufacturing costs and other expense data are as follows:

Instructions

Enter each item and place an “X” mark under each of the following column headings.

![]()

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

TRUE-FALSE

| 1. (F) | Managerial accounting relates primarily to managers and other internal users. |

| 2. (T) | |

| 3. (F) | The reporting standard for internal reports is relevance to the decision being made. |

| 4. (F) | Planning requires management to look ahead and to establish objectives. The statement given relates to the function of directing. |

| 5. (T) | |

| 6. (T) | |

| 7. (T) | |

| 8. (F) | The wages of these employees are usually identified as indirect labor because their efforts either have no physical association with the finished product or it is impractical to trace the costs to the goods produced. |

| 9. (F) | Manufacturing overhead consists of costs that are indirectly associated with the manufacture of the finished product. |

| 10. (T) | |

| 11. (T) | |

| 12. (F) | Period costs include selling and administrative expenses. |

| 13. (T) | |

| 14. (F) | Direct materials become a cost of the finished goods manufactured when they are used, not when they are acquired. |

| 15. (T) | |

| 16. (F) | The sum of the direct materials costs, direct labor costs, and manufacturing overhead incurred is the total manufacturing costs for the year. |

| 17. (T) | |

| 18. (T) | |

| 19. (F) | Raw Materials Inventory shows the cost of raw materials on hand. Finished Goods Inventory shows the cost of completed goods on hand. |

| 20. (F) | Manufacturing inventories are reported in the current asset section in order of their expected realization in cash. |

MULTIPLE CHOICE

MATCHING

- i

- a

- e

- c

- m

- l

- j

- g

- h

- k

- b

- f

- d

EXERCISES

EX. 19-1