Chapter 25

STANDARD COSTS AND BALANCED SCORECARD

| The Navigator | |

After studying this chapter, you should be able to:

1. Distinguish between a standard and a budget.

2. Identify the advantages of standard costs.

3. Describe how companies set standards.

4. State the formulas for determining direct materials and direct labor variances.

5. State the formula for determining the total manufacturing overhead variance.

6. Discuss the reporting of variances.

7. Prepare an income statement for management under a standard costing system.

8. Describe the balanced scorecard approach to performance evaluation.

*9. Identify the features of a standard cost accounting system.

*10. Compute overhead controllable and volume variance.

![]()

*Note: All asterisked (*) items relate to material contained in the Appendix to the chapter.

PREVIEW OF CHAPTER 25

In this chapter we continue the study of controlling costs by considering additional measures that permit the evaluation of performance. The content and organization of the chapter are as follows:

![]()

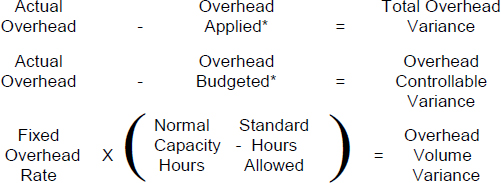

Standards and Budgets

1. (L.O. 1) In concept, standards and budgets are essentially the same. Both are predetermined costs and both contribute significantly to management planning and control.

a. A standard is a unit amount, whereas a budget is a total amount.

b. Standard costs may be incorporated into a cost accounting system.

Why Standard Costs?

2. (L.O. 2) Standard costs offer the following advantages to an organization:

a. They facilitate management planning.

b. They promote greater economy by making employees more “cost conscious.”

c. They are useful in setting selling prices.

d. They contribute to management control by providing a basis for the evaluation of cost control.

e. They are useful in highlighting variances in management by exception.

f. They simplify the costing of inventories and reduce clerical costs.

Setting Standard Costs

3. (L.O. 3) Setting standards requires input from all persons who have responsibility for costs and quantities. Standards may be set at one of two levels. Ideal standards represent optimum levels of performance under perfect operating conditions. Normal standards represent efficient levels of performance that are attainable under expected operating conditions.

4. To establish the standard cost of producing a product, it is necessary to establish standards for each manufacturing cost element—direct materials, direct labor, and manufacturing overhead. The standard for each element is derived from a consideration of the standard price to be paid and the standard quantity to be used.

Direct Materials

5. The direct materials price standard is the cost per unit of direct materials that should be incurred.

a. This standard is based on the purchasing department's best estimate of the cost of raw materials.

b. This standard should include an amount for related costs such as receiving, storing, and handling.

6. The direct materials quantity standard is the quantity of direct materials that should be used per unit of finished goods.

a. This standard is expressed as a physical measure, such as pounds, barrels, or board feet.

b. This standard should include allowances of unavoidable waste and normal storage.

7. The standard direct materials cost per unit is the standard direct materials price times the standard direct materials quantity.

8. The direct labor price standard is the rate per hour that should be incurred for direct labor.

a. This standard is based on current wage rates adjusted for anticipated changes, such as cost of living adjustments included in many union contracts.

b. This standard generally includes employer payroll taxes and fringe benefits.

9. The direct labor quantity standard is the time that should be required to make one unit of the product.

a. This standard is especially critical in labor-intensive companies.

b. In setting this standard, allowances should be made for rest periods, cleanup, machine setup and machine downtime.

10. The standard direct labor cost per unit is the standard direct labor rate times the standard direct labor hours.

Manufacturing Overhead

11. The manufacturing overhead standard is based on a standard predetermined overhead rate.

a. This overhead rate is determined by dividing budgeted overhead costs by an expected standard activity index.

b. The standard manufacturing overhead rate per unit is the predetermined overhead rate times the activity index quantity standard.

Variances

12. (L.O. 4) A variance is the difference between total actual costs and total standard costs. An unfavorable variance suggests that too much was paid for materials, labor, and manufacturing overhead or that there were inefficiencies in using materials, labor, and manufacturing overhead. Favorable variances indicate efficiencies in incurring costs and in using materials, labor, and manufacturing overhead.

13. Analyzing variances begins with a determination of the cost elements that comprise the variance. For each manufacturing cost element, a total dollar variance is computed. Then this variance is analyzed into a price variance and a quantity variance.

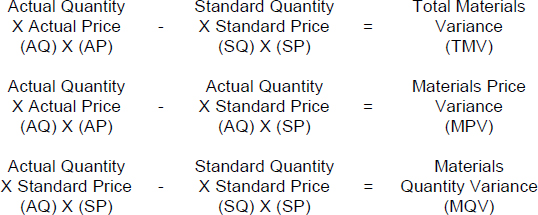

Direct Materials Variances

14. The formulas for the direct materials variances are:

15. A variance matrix can be used in analyzing variances. In such cases, the formulas for each cost element are computed first and then the variances.

16. Materials price variances are usually the responsibility of the purchasing department, whereas materials quantity variances are usually attributable to the production department.

Direct Labor Variances

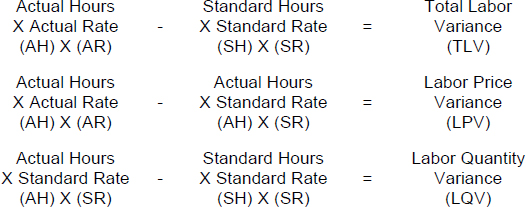

17. The formulas for the direct labor variances are:

18. Labor price variances usually result from paying workers higher wages than expected and/or misallocation of workers. Labor quantity variances relate to the efficiency of the workers and are the responsibility of the production department.

Manufacturing Overhead Variance

19. (L.O. 5) The total overhead variance is the difference between the actual overhead costs and overhead costs applied based on standard hours allowed.

20. To find the total overhead variance in a standard costing system, we determine the overhead costs applied based on standard hours allowed. Standard hours allowed are the hours that should have been worked for the units produced. The total overhead variance formula is as follows:

![]()

21. One reason for an overhead variance relates to over- or under-spending on overhead items. Generally the responsibility for these variances rests with the production department. The overhead variance can also result from inefficient use of overhead. The responsibility for these variances rests on either the production or sales departments.

Reporting of Variances

22. (L.O. 6) All variances should be reported to appropriate levels of management as soon as possible. Variance reports facilitate the principle of “management by exception.” Rather than analyze every variance, top management will normally look for significant variances.

Statement Presentation of Variances

23. (L.O. 7) In income statements prepared for management under a standard cost accounting system, cost of goods sold is stated at standard cost and the variances are separately disclosed. In financial statements prepared for stockholders and other external users, standard costs may be used.

Balanced Scorecard

24. (L.O. 8) Many companies use both financial and nonfinancial measures to evaluate performance. This approach is known as the balanced scorecard. The four most commonly employed perspectives are as follows:

a. The financial perspective employs financial measures of performance.

b. The customer perspective evaluates how well the company is performing from the viewpoint of those people who buy and use its product.

c. The internal process perspective evaluates the internal operating processes critical to success.

d. The earning and growth perspective evaluates how well the company develops and retains its employees.

The different perspectives are linked together so a company can better understand how to achieve its goals and what measures to use to evaluate performance.

Standard Cost Accounting System

*25. (L.O. 9) A standard cost accounting system is a double-entry system of accounting in which standard costs are used in making entries and variances are formally recognized in the accounts. A standard cost system may be used with either job order or process costing.

*26. As an example, the purchase of raw materials inventory for $5,000 when the standard cost is $6,000 would be recorded as follows:

a. A debit balance in a variance account indicates an unfavorable variance.

b. A credit balance in a variance account indicates a favorable variance.

Overhead Variances

*27. (L.O. 10) The computation of the manufacturing overhead variances is conceptually the same as the computation of the materials and labor variances. For manufacturing overhead, however, both variable and fixed overhead must be considered. The formulas are:

*28. The overhead controllable variance shows whether overhead costs were effectively controlled.

a. Budgeted costs are determined from the flexible manufacturing overhead budget for standard hours allowed.

b. Most controllable variances are associated with variable costs which are controllable costs.

*29. The overhead volume variance indicates whether plant facilities were efficiently used during the period.

a. This variance relates solely to fixed costs.

b. It measures the amount that fixed overhead costs are under- or overapplied.

*30. In computing the overhead variances,

a. Standard hours allowed are used in each of the variances.

b. Budgeted costs are derived from the flexible budget.

c. The controllable variance generally pertains to variable costs.

d. The volume variance pertains solely to fixed costs.

![]()

![]()

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

![]()

MULTIPLE CHOICE

Circle the letter that best answers each of the following statements.

- (L.O. 3) A standard that represents the optimum level of performance under perfect operating conditions is called a(n):

- normal standard.

- controllable standard.

- ideal standard.

- materials price standard.

- (L.O. 4) The standard unit cost is used in the calculation of which of the following variances?

- (L.O. 4) In the Norton Company, each unit of finished goods requires one pound of direct materials at $2 per pound. In producing 50,000 units, 45,000 pounds of materials are used at $2.10 per pound. The materials price variance is:

- $4,500 unfavorable.

- $5,000 favorable.

- $5,000 unfavorable.

- $10,000 favorable.

- (L.O. 4) Using the data in question 3 above, the materials quantity variance is:

- $10,500 favorable.

- $10,000 favorable.

- $10,500 unfavorable.

- $4,500 unfavorable.

- (L.O. 4) In the Delaney Company, the standard material cost for the silk used in making a dress is $27.00 based on three square feet of silk at a cost of $9.00 per square foot. The production of 1,000 dresses resulted in the use of 3,400 square feet of silk at a cost of $9.20 per square foot. The materials quantity variance is:

- $600 unfavorable.

- $680 unfavorable.

- $3,600 unfavorable.

- $3,680 unfavorable.

- (L.O. 4) The difference between the actual labor rate multiplied by the actual labor hours worked and the standard labor rate multiplied by the standard labor hours is the:

- total labor variance.

- labor price variance.

- labor quantity variance.

- labor efficiency variance.

- (L.O. 4) The labor price variance is the difference between the:

- standard and actual rate multiplied by actual hours.

- standard and actual rate multiplied by standard hours.

- standard and actual hours multiplied by actual rate.

- standard and actual hours multiplied by the difference between standard and actual rate.

- (L.O. 4) In the Wetzel Company 20,000 direct labor hours were worked when standard hours were 21,000 and the actual pay rate was $6.30 when the standard rate was $6.50. The labor quantity variance is:

- $6,300 favorable.

- $6,300 unfavorable.

- $6,500 favorable.

- $6,500 unfavorable.

- (L.O. 4) Using the data in question 8, the labor price variance is:

- $4,000 unfavorable.

- $4,000 favorable.

- $4,200 unfavorable.

- $4,200 favorable.

- (L.O. 4) An unfavorable labor quantity variance means that:

- the actual rate was higher than the standard rate.

- the total labor variance must also be unfavorable.

- actual hours exceeded standard hours.

- actual hours were less than standard hours.

- (L.O. 4) Information on Engstrom's direct labor costs for the month of August is as follows:

Actual rate $7.50 Standard hours 11,000 Actual hours 10,000 Direct labor price variance—unfavorable $5,000 What was the standard rate for August?

- $6.95.

- $7.00.

- $8.00.

- $8.05.

- (L.O. 4) An unfavorable material price variance generally is the responsibility of the following department:

- Quality control.

- Purchasing.

- Engineering.

- Production.

- (L.O. 4) Which department is usually responsible for a labor price variance attributable to misallocation of workers?

- Quality control.

- Purchasing.

- Engineering.

- Production.

- (L.O. 5) The total overhead variance is:

- the difference between actual overhead costs and overhead applied.

- based on actual hours worked for the units produced.

- the difference between overhead budgeted and overhead applied.

- the difference between actual overhead costs and overhead budgeted.

- (L.O. 5) The overhead controllable variance is the difference between the:

- budgeted overhead based on standard hours allowed and the overhead applied to production.

- budgeted overhead based on standard hours allowed and budgeted overhead based on actual hours worked.

- actual overhead and the overhead applied to production.

- actual overhead and budgeted overhead based on standard hours allowed.

- (L.O. 6) In reporting variances,

- promptness is relatively unimportant.

- management normally investigates all variances.

- the reports should facilitate management by exception.

- the reports are not departmentalized.

*17. (L.O. 9) A standard cost system may be used in:

*18. (L.O. 10) Budgeted overhead for the Henderson Company at normal capacity of 30,000 direct labor hours is $6 per hour variable and $4 per hour fixed. In May, $310,000 of overhead was incurred in working 31,500 hours when 32,000 standard hours were allowed. The overhead controllable variance is:

a. $5,000 favorable.

b. $2,000 favorable.

c. $10,000 favorable.

d. $10,000 unfavorable.

*19. (L.O. 10) Using the data in question 18, the overhead volume variance is:

a. $8,000 favorable.

b. $11,000 favorable.

c. $5,000 favorable.

d. $10,000 favorable.

*20. (L.O. 10) The overhead volume variance is the difference between the:

a. overhead budget based on standard hours allowed and overhead budget based on actual hours worked.

b. normal capacity hours and standard hours allowed times the fixed overhead rate.

c. actual overhead and the overhead budget based on standard hours allowed.

d. actual overhead and the overhead applied.

![]()

Match each term with its definition by writing the appropriate letter in the space provided.

![]()

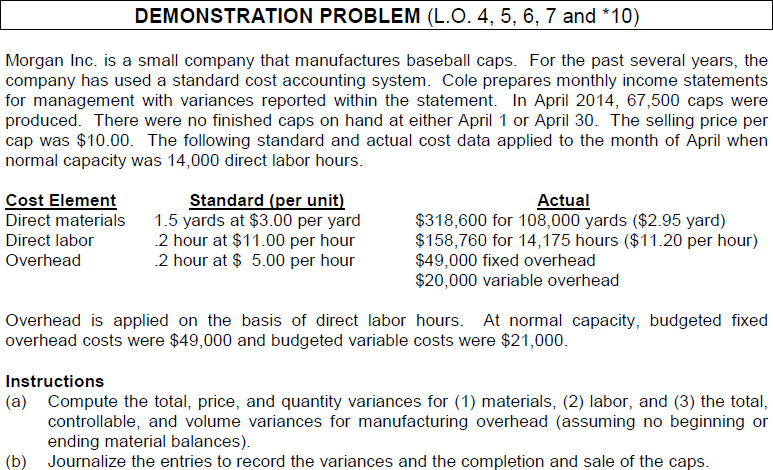

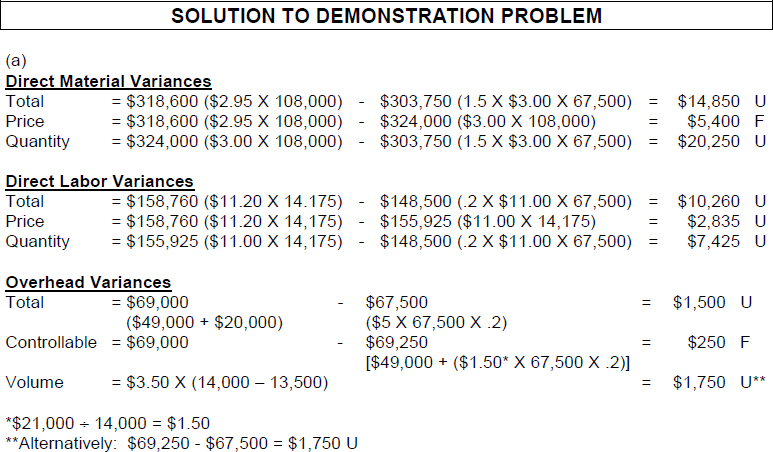

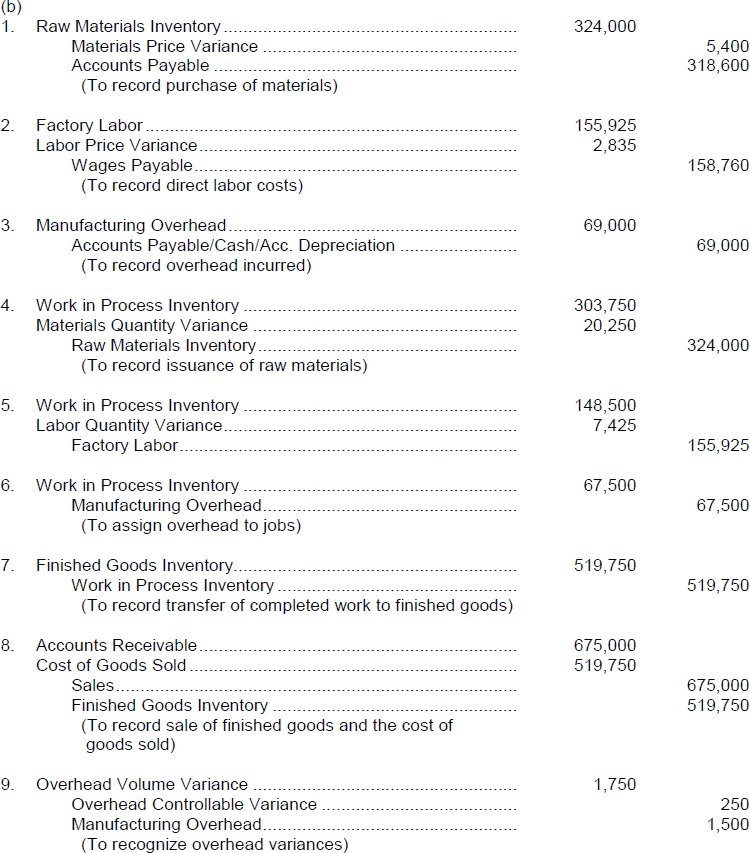

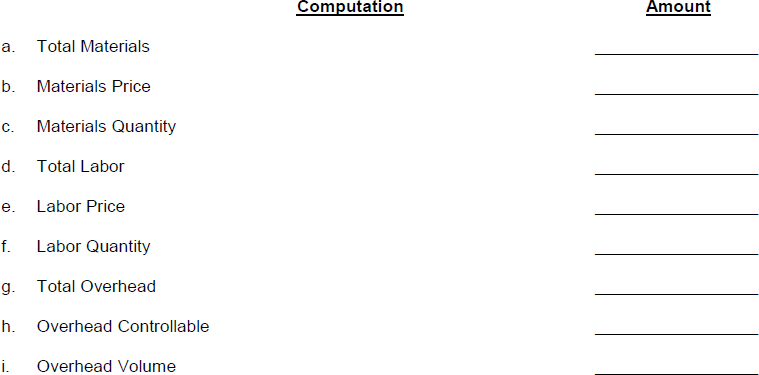

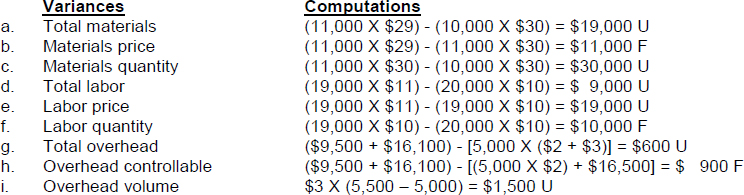

EX. 25-1 (L.O. 4, 5, *10) Lindsey Company manufactures coats with fur-lined hoods. The following information pertains to the standard costs of manufacturing the hood of one coat:

| Direct Material | 1 yard at $30 per yard |

| Direct Labor | 2 hours at $10 per hour |

| Variable Overhead | 1/2 hour at $2 per hour |

| Fixed Overhead | 1/2 hour at $3 per hour |

Other data:

1. Coats produced during June—10,000.

2. 11,000 yards were purchased and used at $29 per yard.

3. Actual direct labor costs were $209,000 for 19,000 hours worked.

4. Normal capacity was 5,500 direct labor hours.

5. Actual variable overhead costs were $9,500.

6. Actual fixed overhead costs were $16,100.

Instructions

Compute the following variances for Lindsey Company:

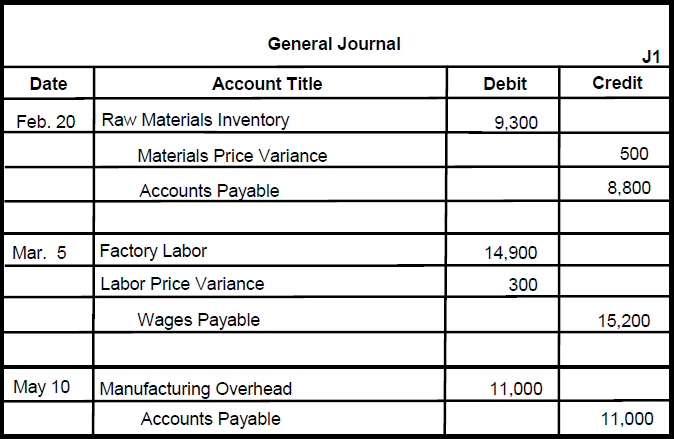

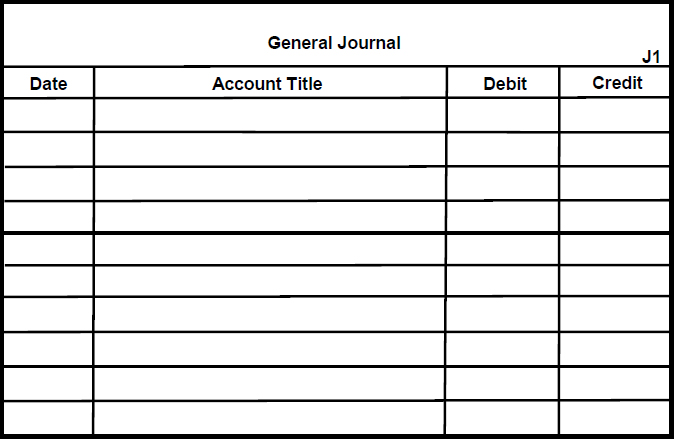

*EX. 25-2 (L.O. 8) A. Carlson uses a standard cost accounting system. The following transactions occurred during the year:

| Feb. 20 | Purchased raw materials on account, $8,800 when the standard cost was $9,300. |

| Mar. 5 | Incurred direct labor costs, $15,200 when the standard labor cost was $14,900. |

| May 10 | Incurred manufacturing overhead costs, $11,000 (credit Accounts Payable). |

| June 18 | Issued raw materials for production, $8,200 when the standard cost was $9,000. |

| Aug. 3 | Assigned factory labor to production, $14,900 when the standard cost was $14,500. |

| Sept. 10 | Applied manufacturing overhead to production, $10,150. |

| Oct. 2 | Transferred completed work to finished goods, $29,700. |

| Nov. 22 | Sold the finished goods for $42,000. |

| Dec. 31 | Recognized unfavorable overhead variances: controllable $550 and volume $300. |

Instructions

Prepare the entries for A. Carlson in the following general journal.

![]()

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

TRUE-FALSE

| 1. (T) | |

| 2. (T) | |

| 3. (F) | Ideal standards represent the optimum level of performance under perfect operating conditions. Normal standards represent an efficient level of performance under normal operating conditions. |

| 4. (T) | |

| 5. (F) | It is the direct labor price standard that is based on current wage rates adjusted for anticipated changes such as cost of living adjustments. |

| 6. (T) | |

| 7. (F) | An unfavorable variance has a negative connotation. It suggests that too much was paid for materials and labor or that there were inefficiencies in using materials and labor. |

| 8. (F) | The materials price variance is the difference between the actual quantity of materials purchased times the actual cost and the actual quantity times the standard cost. |

| 9. (T) | |

| 10. (F) | The materials price variance is normally the responsibility of the purchasing department. |

| 11. (T) | |

| 12. (F) | The labor quantity variance is the difference between the actual hours times the standard rate and the standard hours times the standard rate. |

| 13. (T) | |

| 14. (T) | |

| 15. (T) | |

| 16. (F) | In using variance reports, top management normally looks for significant variances. The variance reports facilitate the principle of “management by exception.” |

| 17. (T) | |

| 18. (T) | |

| 19. (F) | The use of standard costs in inventory costing is in accordance with generally accepted accounting principles when there are no significant differences between actual and standard costs. |

| *20. (T) |

MULTIPLE CHOICE

- l

- c

- n

- a

- j

- p

- h

- d

- m

- e

- i

- o

- k

- g

- f

- b

EXERCISES

EX. 25-1

EX. 25-2