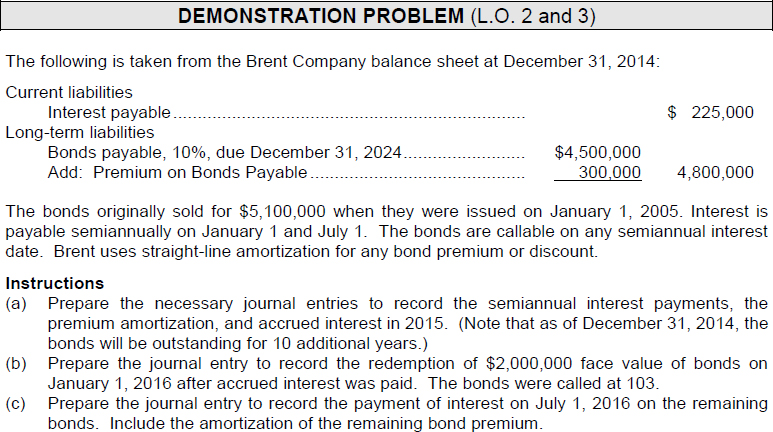

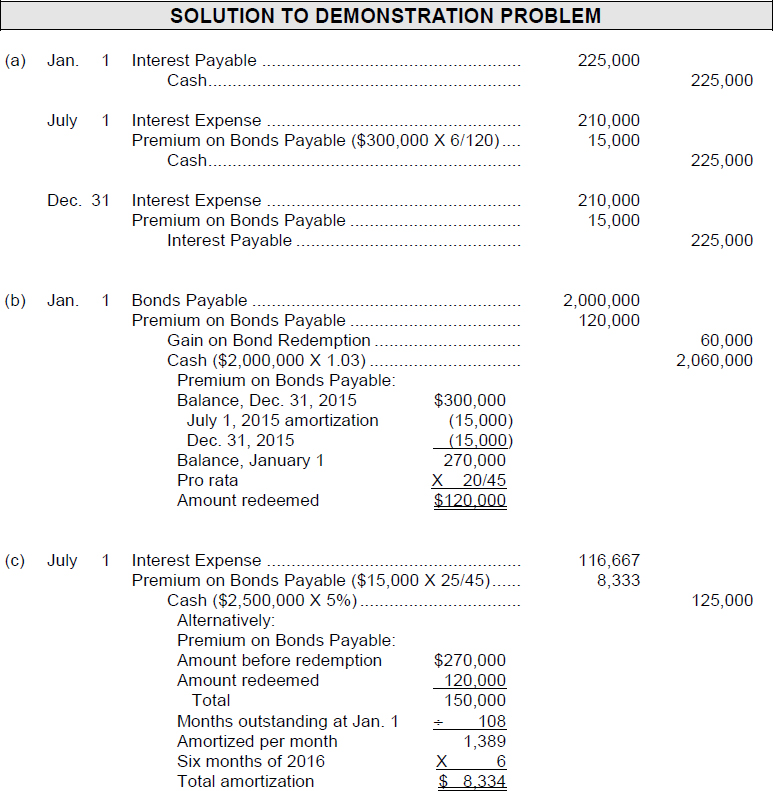

Chapter 15

LONG-TERM LIABILITIES

| The Navigator | |

After studying this chapter, you should be able to:

1. Explain why bonds are issued.

2. Prepare the entries for the issuance of bonds and interest expense.

3. Describe the entries when bonds are redeemed or converted.

4. Describe the accounting for long-term notes payable.

5. Contrast the accounting for operating and capital leases.

6. Identify the methods for the presentation and analysis of long-term liabilities.

*7. Compute the market price of a bond.

*8. Apply the effective-interest method of amortizing bond discount and bond premium.

*9. Apply the straight-line method of amortizing bond discount and bond premium.

*10. Compare the accounting for long-term liabilities under GAAP and IFRS.

![]()

*Note: All asterisked (*) items relate to material contained in the Appendix to the chapter.

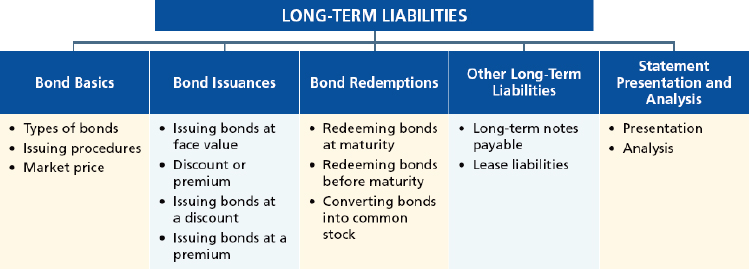

PREVIEW OF CHAPTER 15

In this chapter we will explain the accounting for the major types of long-term liabilities reported on the balance sheet. These liabilities may be bonds, long-term notes, or lease obligations. The content and organization of the chapter are as follows:

![]()

Bonds

- (L.O. 1) Long-term liabilities are obligations that are expected to be paid more than one year in the future. Long-term liabilities include bonds, long-term notes, and lease obligations.

- Bonds offer the following advantages over common stock:

- Stockholder control is not affected.

- Tax savings result.

- Earnings per share of common stock may be higher.

- The major disadvantages resulting from the use of bonds are that interest must be paid on a periodic basis, and the principal (face value) of the bonds must be paid at maturity.

Types of Bonds

4. Secured bonds have specific assets of the issuer pledged as collateral for the bonds. A mortgage bond is secured by real estate. Unsecured bonds are issued against the general credit of the borrower; they are also called debenture bonds.

5. Bonds that mature at a single specified future date are called term bonds. In contrast, bonds that mature in installments are called serial bonds.

6. Registered bonds are issued in the name of the owner and have interest payments made by check to bondholders of record. Bearer or coupon bonds are not registered; thus bondholders must send in coupons to receive interest payments.

7. Convertible bonds permit bondholders to convert the bonds into common stock at their option. Callable bonds are subject to call and retirement at a stated dollar amount prior to maturity at the option of the issuer.

8. State laws grant corporations the power to issue bonds.

a. Within the corporation, formal approval by both the board of directors and stockholders is usually required before bonds can be issued.

b. In authorizing a bond issue, the board of directors must stipulate the total number of bonds to be authorized, total face value, and the contractual interest rate.

c. The terms of the bond issue are set forth in a formal legal document called a bond indenture.

Market Price of Bonds

9. The market value (present value) of a bond is a function of three factors: (a) the dollar amounts to be received, (b) the length of time until the amounts are received, and (c) the market rate of interest.

10. (L.O. 2) The issuance of bonds at face value results in a debit to Cash and a credit to Bonds Payable.

a. Over the term of the bonds, entries are required for bond interest.

b. At the maturity date, it is necessary to record the final payment of interest and payment of the face value of the bonds.

11. Bonds may be issued below or above face value.

a. If the market (effective) rate of interest is higher than the contractual (stated) rate, the bonds will sell at less than face value, or at a discount.

b. If the market rate of interest is less than the contractual rate on the bonds, the bonds will sell above face value, or at a premium.

Bond Issues at Discount

12. When bonds are issued at a discount,

a. The discount is debited to a contra account, Discount on Bonds Payable, and it is deducted from Bonds Payable in the balance sheet to show the carrying (or book) value of the bonds.

b. Bond discount is an additional cost of borrowing that should be recorded as interest expense over the life of the bonds.

Bond Issues at Premium

13. When bonds are issued at a premium,

a. The premium is credited to the account, Premium on Bonds Payable, and it is added to Bonds Payable in the balance sheet.

b. Bond premium is a reduction in the cost of borrowing that should be credited to Interest Expense over the life of the bonds.

Bond Redemptions

14. (L.O. 3) When bonds are redemeed before maturity it is necessary to (a) eliminate the carrying value of the bonds at the redemption date, (b) record the cash paid, and (c) recognize the gain or loss on redemption.

15. In recording the conversion of bonds into common stock the current market prices of the bonds and the stock are ignored. Instead, the carrying value of the bonds is transferred to paid-in capital accounts and no gain or loss is recognized.

Long-term Notes Payable

16. (L.O. 4) A long-term note payable may be secured by a document called a mortgage that pledges title to specific assets as security for a loan.

a. Typically, the terms require the borrower to make installment payments consisting of (1) interest on the unpaid balance of the loan and (2) a reduction of loan principal.

b. Mortgage payable is recorded initially at face value; each installment payment results in a debit to Interest Expense, a debit to Mortgage Payable, and a credit to Cash.

17. (L.O. 5) A lease is a contractual agreement between a lessor (owner) and a lessee (renter) that grants the right to use specific property for a period of time in return for cash payments.

Operating Leases

18. In an operating lease the intent is temporary use of the property by the lessee with continued ownership of the property by the lessor. The lease (or rental) payments are recorded as an expense by the lessee and as revenue by the lessor.

Capital Leases

19. A capital lease transfers substantially all the benefits and risks of ownership from the lessor to the lessee.

a. The lessee is required to record an asset and the related obligation at the present value of the future lease payments.

b. The leased asset is reported on the balance sheet under plant assets.

c. The portion of the lease liability to be paid in the next year is a current liability, and the remainder is classified as a long-term liability.

Presentation and Analysis

20. (L.O. 6) Long-term liabilities are reported in a separate section of the balance sheet immediately following current liabilities.

21. The debt to total assets ratio measures the percentage of the total assets provided by creditors. It is computed by dividing total debt by total assets.

22. The times interest earned ratio provides an indication of the company's ability to meet interest payments as they become due. It is computed by dividing income before interest expense and income taxes by interest expense.

Effective-Interest Method

*23. (L.O. 8) The effective interest method of amortization is an alternative to the straight-line method. Under this method,

a. Interest Expense is computed first by multiplying the carrying value of the bonds at the beginning of the period by the effective interest rate.

b. The credit to Cash (or Interest Payable) is computed by multiplying the face value of the bonds by the contractual interest rate.

c. The bond discount or premium amortization amount is then determined by comparing bond interest expense with the interest paid or accrued.

*24. The effective interest method produces a periodic interest expense equal to a constant percentage of the carrying value of the bonds. When the amount of interest expense is materially different under the two methods, the effective interest method is required under generally accepted accounting principles.

*25. (L.O. 9) The straight-line method of amortization allocates the same amount of bond discount (premium) each interest period. The formula is:

Bond Discount (Premium) ÷ Number of Interest Periods = Bond Discount (Premium) Amortization

Bond discount amortization is recorded by debiting Interest Expense and crediting Discount on Bonds Payable. Bond premium amortization is recorded by crediting Interest Expense and debiting Premium on Bonds Payable.

A Look at IFRS

*26. (L.O. 10) IFRS requires use of the effective-interest method for amortization of bond discounts and premiums. GAAP also requires the effective-interest method, except that it allows use of the straight-line method where the difference is not material.

*27. The accounting for convertible bonds differs between IFRS and GAAP. Unlike GAAP, IFRS splits the proceeds from the convertible bond between an equity component and a debt component. The equity conversion rights are reported in equity.

![]()

![]()

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

![]()

MULTIPLE CHOICE

Circle the letter that best answers each of the following statements.

- (L.O. 1) The market price of a bond is the:

- Present value of its principal amount at maturity plus the present value of all future interest payments.

- Principal amount plus the present value of all future interest payments.

- Principal amount plus all future interest payments.

- Present value of its principal amount only.

- (L.O. 2) When bonds are sold at face value on the issue date, Bonds Payable is credited for:

- maturity value plus interest payable.

- face value.

- call price.

- conversion price.

- (L.O. 3) On the maturity date, January 1, Livingston Corporation pays the accrued interest recorded on December 31 and the face value of the bonds. The entry to record the payment will result in a credit to Cash and a debit to:

- Bonds Payable for the total payment.

- Bonds Payable for the face amount and a debit to Interest Expense for the interest due.

- Bonds Payable for the face amount and a debit to Interest Payable for the interest due.

- none of the above.

- (L.O. 2) On the date of issue, Jagielo Corporation sells $2 million of 5-year bonds at 97. The entry to record the sale will include the following debits and credits:

- (L.O. 2) On the issue date, Wellington Corporation sells $1,000,000 bonds at 103. The entry to record the sale will include a credit to Premium on Bonds Payable of:

- (L.O. 2) How does the amortization of discount on bonds payable affect each of the following?

- (L.O. 2) The market rate of interest for a bond issue which sells for more than its par value is:

- Independent of the interest rate stated on the bond.

- Higher than the interest rate stated on the bond.

- Equal to the interest rate stated on the bond.

- Less than the interest rate stated on the bond.

- (L.O. 2) How does the amortization of premium on bonds payable affect each of the following?

- (L.O. 3) Hoffman Corporation retires its bonds at 106 on January 1, following the payment of semiannual interest. The face value of the bonds is $100,000. The carrying value of the bonds at the redemption date is $104,950. The entry to record the redemption will include a:

- credit of $4,950 to Loss on Bond Redemption.

- debit of $6,000 to Premium on Bonds Payable.

- credit of $1,050 to Gain on Bond Redemption.

- debit of $4,950 to Premium on Bonds Payable.

- (L.O. 3) Ray Corporation's $100,000 convertible bonds are converted into 3,000 shares of $20 par value common stock when the market price of the stock is $40 per share. Using the book value method, the entry to record the conversion will include a:

- credit to Paid-in Capital in Excess of Par –Common Stockof $40,000.

- debit to Loss on Bond Conversion of $20,000.

- credit to Paid-in Capital in Excess of Par – Common Stockof $20,000.

- debit to Loss on Bond Conversion of $60,000.

- (L.O. 4) Buffon Electronics Company issues a $300,000, 10%, 20-year mortgage note on January 1. The terms provide for semiannual installment payments, exclusive of real estate taxes and insurance, of $17,483. After the first installment payment, the principal balance is:

- $300,000.

- $294,910.

- $297,517.

- $292,172.

- (L.O. 4) Portly Cihla, Inc. issues a $1,000,000, 10%, 20-year mortgage note on January 1, 2014. The note will be paid in annual installments of $140,000 each payable at the end of the year. What is the amount of interest expense that should be recognized by Portly Cihla, Inc. in the second year?

- $36,000.

- $86,000.

- $96,000.

- $100,000.

- (L.O. 5) Which of the following is not a condition under which the lessee must record the lease as an asset?

- The lease contains a bargain purchase option.

- The lease transfers ownership of the property to the lessee.

- The lease term is equal to 60% of the economic life of the lease property.

- The present value of the lease payments is 95% of the fair market value of the leased property.

*14. (L.O. 8) Under the effective interest method of amortization, interest expense is computed by multiplying:

a. the face value of the bonds by the contractual interest rate.

b. the carrying value of the bonds at the beginning of the period by the effective interest rate.

c. the carrying value of the bonds at the beginning of the period by the contractual interest rate.

d. the carrying value of the bonds at the end of the period by the effective interest rate.

*15. (L.O. 8) On January 1, Arawak, Inc. issued $2,000,000 of 9% bonds for $1,900,000. The bonds were issued to yield 10%. Interest is payable annually on December 31. Arawak uses the effective interest method of amortizing bond discount. At the end of the first year. Arawak should report unamortized bond discount of:

a. $90,000.

b. $71,000.

c. $51,610.

d. $51,000.

*16. (L.O. 8) On January 1, when the market interest rate was 14%, Santorio Corporation issued bonds in the face amount of $500,000, with interest at 12% payable semiannually. The bonds were issued at a discount of $53,180. How much of the discount should be amortized by the effective interest method for the first interest period?

a. $1,277.

b. $2,659.

c. $3,191.

d. $3,723.

*17. (L.O. 8) On January 1, Abbie Corporation issued $500,000 of 12%, six-year bonds with interest payable on July 1 and January 1. The bonds sold for $549,300 at an effective interest rate of 10%. On the first interest date, using the effective interest method, the debit entry to Bond Interest Expense is for:

a. $25,000.

b. $27,465.

c. $32,958.

d. $50,000.

*18. (L.O. 9) The effects of the straight-line method of amortization on the following in each interest period (assuming discount or premium amortization) are:

*19. (L.O. 9) On January 1, the Montesque Corporation sells $300,000 of 5-year, 10% bonds at 98 with interest payable on July 1 and January 1. The entry on July 1 to record payment of bond interest and the amortization of bond discount using the straight-line method will include a:

a. debit to Interest Expense, $15,000.

b. debit to Interest Expense, $30,000.

c. credit to Discount on Bonds Payable, $600.

d. credit to Discount on Bonds Payable, $1,200.

*20. (L.O. 9) For the bonds issued in question 19, above, what is the carrying value of the bonds at the end of the fourth interest period?

a. $297,600.

b. $296,400.

c. $294,000.

d. $291,600.

![]()

Match each term with its definition by writing the appropriate letter in the space provided.

![]()

EX. 15-1 (L.O. 2 and *8) On January 1, Gutenberg Printers Inc. issues $400,000 of 10-year 12% bonds at 98 with interest payable on July 1 and January 1.

Instructions

(a) Journalize the issuance of the bonds and the entries on July 1 and December 31 for interest and the amortization of bond discount using the straight-line method. (Omit explanations.)

(b) Journalize the July 1 and December 31 entries assuming the effective interest rate on the bonds is 12.4% and the effective interest method is used. (Omit explanations.)

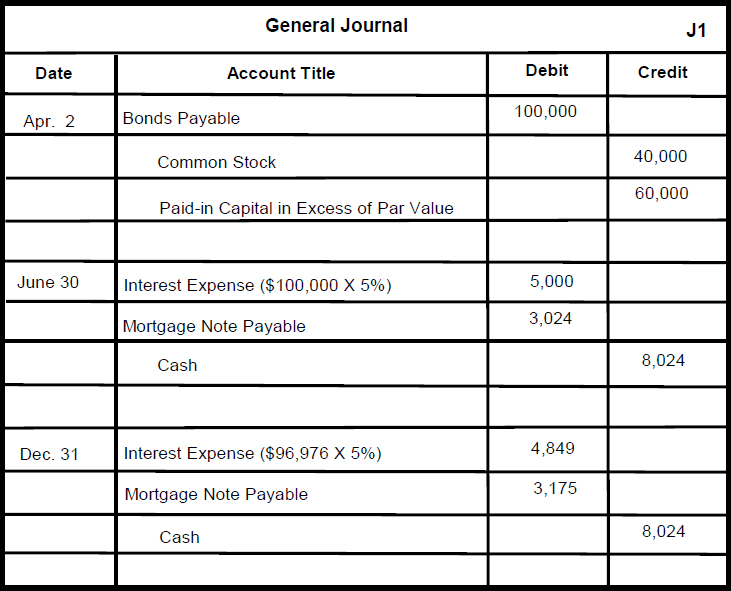

EX. 15-2 (L.O. 3, 5 and *9) Sonoda Computers Inc. has the following transactions concerning long-term liabilities during the current year.

| Apr. 2 | Convertible bonds issued by Sonoda at face value are converted into common stock. The $100,000 bond issue has a conversion price of $25 per share of common stock with one $1,000 bond convertible into 40 shares of stock. The common stock has a par value of $10 and a fair market price of $30 at the time of conversion. |

| June 30 | The first installment payment on a $100,000, 10%, 10-year mortgage note is made by Sonoda. The terms of the mortgage contract provided for semiannual installment payments, exclusive of real estate taxes and insurance of $8,024. |

| Dec. 31 | The second installment payment is made on the mortgage note. |

Instructions

Journalize the transactions. (Omit explanations.)

![]()

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

TRUE-FALSE

| 1. (T) | |

| 2. (F) | The fact that bondholders do not have voting rights is an advantage for common stockholders because their control is not affected. |

| 3. (T) | |

| 4. (T) | |

| 5. (F) | Bonds that permit bondholders to convert the bonds into common stock at their option are known as convertible bonds. |

| 6. (T) | |

| 7. (F) | The market price of a bond is equal to the present value of the principal and interest payments. |

| 8. (F) | Because interest on bonds is usually payable annually or semiannually, the interest is expected to be paid within the following year and thus is a current liability. |

| 9. (T) | |

| 10. (T) | |

| 11. (F) | The premium account is added to Bonds Payable on the balance sheet. |

| 12. (T) | |

| 13. (F) | The redemption of bonds results in an ordinary gain or loss in the income statement. |

| 14. (T) | |

| 15. (F) | For operating leases the lessee simply records the lease payments as an expense in the income statement. No asset is recorded. |

| 16. (T) | |

| 17. (T) | |

| 18. (T) | |

| *19. (F) | When the amounts are materially different, the effective-interest method is required under generally accepted accounting principles. |

| *20. (T) |

MULTIPLE CHOICE

MATCHING

- f

- b

- g

- h

- i

- j

- d

- k

- e

- c

- a

EX. 15-1 Note : I am not able to change the account titles in these journal entries because the journal is an image pasted into the Word file.

The account title Bond Interest Expense should be changed to Interest Expense.

The account title Bond Interest Payable should be changed to Interest Payable.

The account title Paid-in Capital in excess of Par Value should be modified by deleting the word « Value » and replacing it with – Common Stock.

The account title Mortgage Note Payable should be changed to Mortgage Payable.