Chapter 21

PROCESS COSTING

CHAPTER LEARNING OBJECTIVES

After studying this chapter, you should be able to:

1. Understand who uses process cost systems.

2. Explain the similarities and differences between job order cost and process cost systems.

3. Explain the flow of costs in a process cost system.

4. Make the journal entries to assign manufacturing costs in a process cost system.

5. Compute equivalent units.

6. Explain the four steps necessary to prepare a production cost report.

7. Prepare a production cost report.

8. Explain just-in-time (JIT) processing.

9. Explain activity-based costing (ABC).

*10. Apply activity-based costing to specific company data.

![]()

*Note: All asterisked (*) items relate to material contained in the Appendix to the chapter.

PREVIEW OF CHAPTER 21

In contrast to job order cost accounting, which focuses on the individual job, process cost accounting focuses on the processes involved in mass-producing products that are identical or very similar in nature. The primary objective of the chapter is to explain and illustrate process cost accounting. At the end of the chapter, two contemporary developments, just-in-time (JIT) processing and activity-based costing (ABC) are considered. The content and organization of this chapter are as follows:

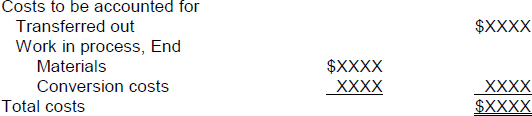

![]()

CHAPTER REVIEW

Process Manufacturing and Accounting

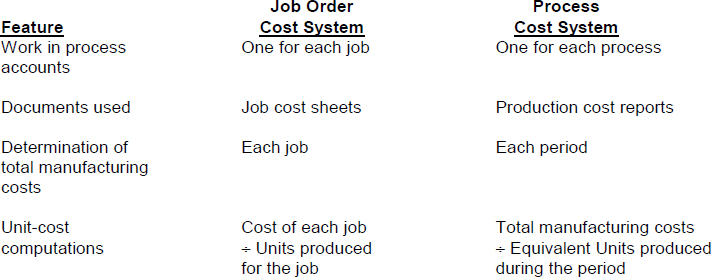

- (L.O. 1) Process cost systems are used to apply costs to similar products that are mass produced in a continuous fashion, such as the production of ice cream, steel or soft drinks. In comparison, costs in a job order cost system are assigned to a specific job, such as the construction of a customized home, the making of a motion picture, or the manufacturing of a specialized machine.

- (L.O. 2) Job order cost and process cost systems are similar in that (a) both use the same three manufacturing cost elements of direct materials, direct labor, and manufacturing overhead; (b) both accumulate costs of raw materials by debiting Raw Materials Inventory, factory labor by debiting Factory Labor, and manufacturing overhead costs by debiting Manufacturing Overhead; and (c) both flow costs to the same accounts of Work in Process, Finished Goods Inventory, and Cost of Goods Sold.

- The major differences between a job order cost system and a process cost system are as follows:

Process Cost Flow

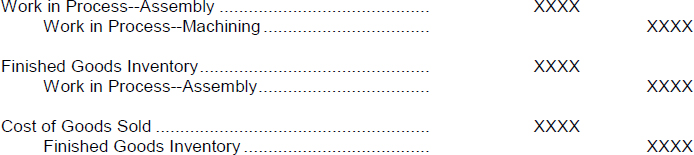

4. (L.O. 3) In the Tyler Company example in the text book, manufacturing consists of two processes: machining and assembly. In the Machining Department, the raw materials are shaped, honed, and drilled. In the Assembly Department, the parts are assembled and packaged.

5. Materials, labor, and manufacturing overhead can be added in both the Machining and Assembly Departments. When the Machining Department finishes its work, the partially completed units are transferred to the Assembly Department. In the Assembly Department, the goods are finished and are then transferred to the finished goods inventory. Upon sale, the goods are removed from the finished goods inventory.

Assignment of Manufacturing Costs

6. (L.O. 4) All raw materials issued for production are a materials cost to the producing department. Materials requisition slips may be used in a process cost system, but fewer requisitions are generally required than in a job order cost system, because the materials are used for processes rather than for specific jobs. The entry to record the materials used is:

7. Time tickets may be used in determining the cost of labor assignable to the production departments. The labor cost chargeable to a process can be obtained from the payroll register or departmental payroll summaries. All labor costs incurred within a producing department are a cost of processing the raw materials. The entry to assign the labor costs is:

8. The basis for allocating the overhead costs to the production departments in an objective and equitable manner is the activity that “drives” or causes the costs. A primary driver of overhead costs in continuous manufacturing operations is machine time used, not direct labor. Thus, machine hours are widely used in allocating manufacturing overhead costs. The entry to allocate overhead is:

9. At the end of the period, the following transfer entries are needed:

Equivalent Units

10. (L.O. 5) A major step in process cost accounting is the calculation of equivalent units. Equivalent units of production measure the work done during the period, expressed in fully completed units. This concept is used to determine the cost per unit of completed product.

11. The formula to compute equivalent units of production under the weighted average method is as follows:

12. The method of computing equivalent units here is referred to as the weighted-average method. It considers the degree of completion (weighting) of the units completed and transferred out and the ending work in process. A lesser used method, called the FIFO method, is discussed in the appendix to this chapter.

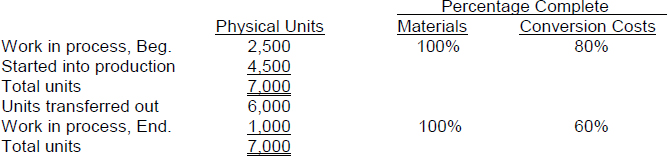

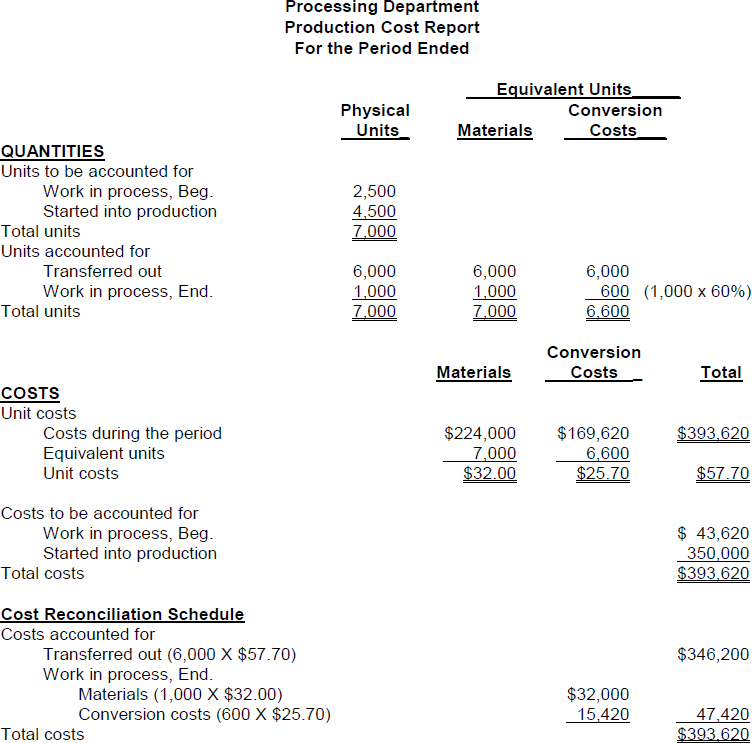

13. To illustrate the computation of equivalent units using the weighted-average method, assume that materials are entered at the beginning of the process and the following information is provided for the Processing Department of the Silva Company:

14. The two equivalent unit computations are as follows:

Production Cost Report

15. (L.O. 6) A production cost report is the key document used by management to understand the activities in a department because it shows the production quantity and cost data related to that department. In order to be ready to complete a production cost report, the company must perform four steps:

a. Compute the physical unit flow.

b. Compute the equivalent units of production.

c. Compute unit production costs.

d. Prepare a cost reconciliation schedule.

16. The computation of physical units involves:

a. adding the units started (or transferred) into production during the period to the units in process at the beginning of the period to determine the total units to be accounted for; and

b. accounting for these units by determining the output for the period—which consists of units transferred out during the period and units in process at the end of the period.

In the example above, the total units to be accounted for and the units accounted for are both equal to 7,000 units for the Silva Company.

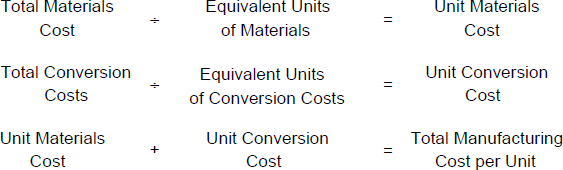

17. In computing unit costs, production costs are expressed in terms of equivalent units of production. When equivalent units are different for materials and conversion costs, the formulas for computing unit costs are as follows:

18. The cost reconciliation schedule shows that the total costs accounted for equal the total costs to be accounted for as follows:

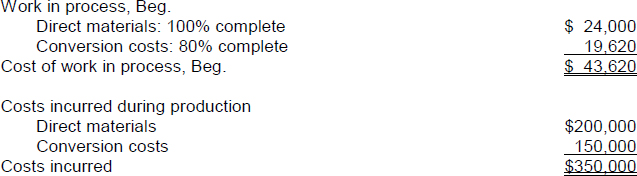

19. (L.O. 7) Assume the Processing Department of the Silva Company has the following additional cost information:

20. The Silva Company's Processing Department Production Cost Report at the end of the period is as follows:

Operations Costing

21. Companies often use a combination of a process cost and a job order cost system, called operations costing. Operations costing is similar to process costing in that standardized methods are used to manufacture the product. At the same time, the product may have some customized, individual features that require the use of a job order cost system.

22. (L.O. 8) Just-in-Time (JIT) processing is dedicated to producing the right products (or parts) at the right time as they are needed. Raw materials are received just in time for use in production, subassembly parts are completed just in time for use in finished goods, and finished goods are completed just in time to be sold.

23. The major benefits of JIT processing are:

a. Manufacturing inventories are significantly reduced or eliminated.

b. Product quality is enhanced.

c. Rework costs and inventory storage costs are reduced or eliminated.

d. Production cost savings are realized from the improved flow of goods through the processes.

24. Under JIT the raw materials and work in process inventory accounts are combined into one Raw and In-Process Inventory account.

Activity-Based Costing

25. (L.O. 10) Activity-based costing (ABC) is a method of product costing that focuses on the activities performed to produce specific products. An ABC system is similar to conventional costing systems in accounting for direct materials and direct labor but differs in regard to manufacturing overhead.

26. In ABC, the cost of a product is equal to the sum of the costs of all activities performed to manufacture it. In selecting a basis, ABC seeks to identify the cost drivers that measure the activities performed on the product. For example, a possible cost driver for ordering raw materials is the number of times an order is placed.

*27. (L.O. 10) ABC involves the following steps:

a. Identify the major activities that pertain to the manufacture of specific products.

b. Accumulate manufacturing overhead costs by activities.

c. Identify the cost driver(s) that accurately measure(s) each activity's contribution to the finished product.

d. Assign manufacturing overhead costs for each activity to products using the cost driver(s).

*28. ABC provides the following benefits:

a. Leads to more cost pools.

b. Enhanced control over overhead costs.

c. Leads to better management decisions.

*29. ABC has the following limitations:

a. Can be expensive to use

b. Some arbitrary allocations continue.

![]()

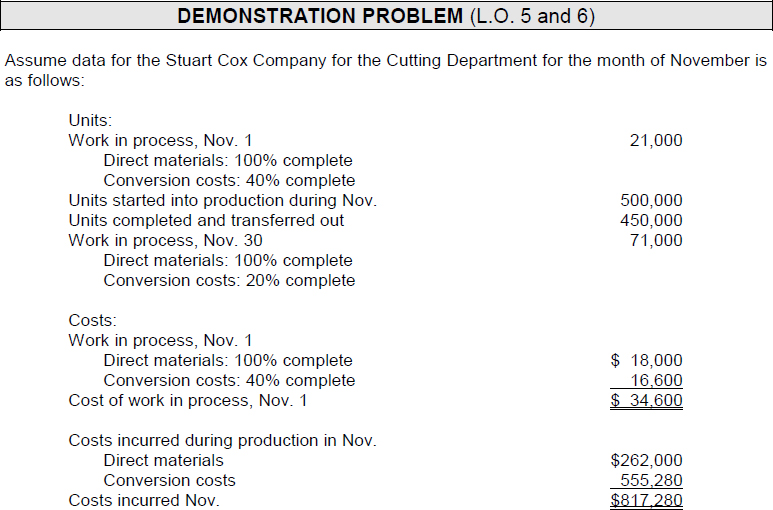

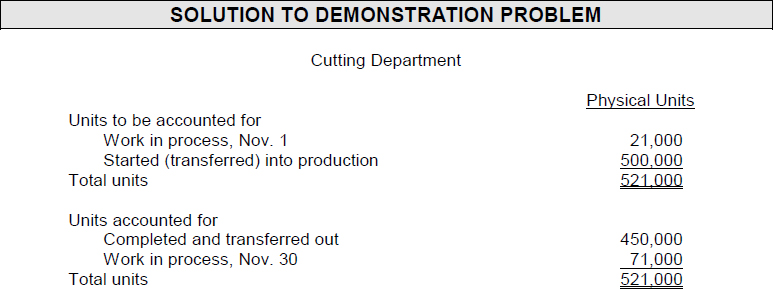

Instructions

Compute the physical unit flow, the equivalent units of production and unit production costs.

![]()

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

![]()

Circle the letter that best answers each of the following statements.

- (L.O. 1) Which of the following is an incorrect statement concerning process cost accounting?

- Individual work in process accounts are maintained for each production department or manufacturing process.

- The summarization of manufacturing costs is performed on production cost reports.

- The focus is on the individual job.

- The system is used by companies that manufacture products through a series of continuous processes or operations.

- (L.O. 2) Which of the following is considered a difference between a job order cost and a process cost system?

- The manufacturing cost elements.

- Documents used to track costs.

- The accumulation of the costs of materials, labor, and overhead.

- The flow of costs.

- (L.O. 2) Which of the following is considered a similarity between a job order cost and a process cost system?

- The flow of costs.

- The number of work in process accounts used.

- The point at which costs are totaled.

- Unit cost computations.

- (L.O. 5) Total physical units to be accounted for are equal to the units:

- started (or transferred) into production.

- started (or transferred) into production plus the units in beginning work in process.

- started (or transferred) into production less the units in beginning work in process.

- completed and transferred out.

- (L.O. 5) Equivalent units of production are a measure of:

- units completed and transferred out.

- units transferred out.

- units in ending work in process.

- the work done during the period expressed in fully completed units.

- (L.O. 6) In Saint-Simon, Inc., the Assembly Department started 6,000 units and completed 7,000 units. If beginning work in process was 3,000 units, how many units are in ending work in process?

- 0.

- 1,000.

- 2,000.

- 4,000.

- (L.O. 6) In the Blanc Company, the Cutting Department had beginning work in process of 4,000 units, transferred out 9,000 units, and had an ending work in process of 2,000 units. How many units were started by Blanc during the month?

- 6,000.

- 7,000.

- 9,000.

- 11,000.

- (L.O. 6) In the Camria Company, materials are entered at the beginning of the process. If there is no beginning work in process, but there is an ending work in process inventory, the number of equivalent units as to material costs will be:

- the same as the units started.

- the same as the units completed.

- less than the units started.

- less than the units completed.

- (L.O. 6) In its first month of operation, the Molding Department started 20,000 units into production. During the month, 18,000 units were transferred out and the 2,000 units in work in process were 100% complete as to materials and 40% complete as to conversion costs. Equivalent units for conversion costs are:

- 20,000.

- 18,000.

- 18,800.

- 19,200.

- (L.O. 6) Equivalent units of production for conversion costs:

- includes all of the beginning work in process units transferred out.

- includes only materials added or conversion costs performed on beginning work in process during the period.

- includes all of the ending work in process units started during the period.

- excludes all of the ending work in process units.

- (L.O. 6) The Cutting Department for Babeuf Company began the period with 4,000 units that were 75% complete, transferred out 14,000 units, and ended with 6,000 units that were 40% complete. The number of equivalent units of conversion costs is:

- 13,400.

- 14,600.

- 15,400.

- 16,400.

- (L.O. 6) The Molding Department of the Smith Company has the following production data: beginning work in process 20,000 units (60% complete), started into production 340,000 units, completed and transferred out 320,000 units, and ending work in process 40,000 units (40% complete). Assuming materials are entered at the beginning of the process, equivalent units for materials are:

- 360,000.

- 300,000.

- 320,000.

- 380,000.

- (L.O. 6) Using the data in question 12 and assuming conversion costs are incurred uniformly during the process, the equivalent units for conversion costs are:

- 320,000.

- 324,000.

- 336,000.

- 360,000.

- (L.O. 6) Malthus Company has the following equivalent units for July: materials 10,000 and conversion costs 9,000. Production cost data are:

The unit production costs for July are:

- (L.O. 6) For the Assembly Department, unit materials cost is $8 and unit conversion cost is $12. If there are 4,000 units in ending work in process 75% complete as to conversion costs, the costs to be assigned to the inventory are:

- $80,000.

- $68,000.

- $60,000.

- $72,000.

- (L.O. 6) In the Shaping Department of the Hendrix Company, the unit materials cost is $5.00 and the unit conversion cost is $3.00. The department transferred out 8,000 units and had 1,000 units in ending work in process 20% complete. If all materials are added at the beginning of the process, what is the total cost to be assigned to the ending work in process?

- $1,600.

- $5,000.

- $5,600.

- $8,000.

- (L.O. 7) In a production cost report, which one of the following sections is not shown under Costs?

- Unit costs.

- Costs to be accounted for.

- Costs during the period.

- Units accounted for.

- (L.O. 7) Which of the following statements about the production cost report is incorrect?

- Units accounted for must equal units to be accounted for.

- The report only provides a basis for determining whether unit costs and total costs are correct.

- Total costs should reconcile.

- There are four steps in preparing the report.

- (L.O. 6) When materials are added at the beginning of the process and costs are transferred in from another department, unit materials cost is based on the:

- sum of the materials costs in the beginning work in process plus the cost of materials added during the period.

- materials costs added during the period.

- sum of the materials costs in the beginning work in process plus materials costs added during the period plus the costs transferred in.

- costs transferred in.

- (L.O. 6) The Finishing Department of the Monica Company has 27,500 equivalent units of materials in June. An analysis of the work in process account shows: materials cost in beginning work in process $25,000, materials cost added during the period $50,000, and costs transferred in from assembly $200,000. The unit materials cost for June is:

- $10.

- $8.

- $2.

- $3.

- (L.O. 8) Which of the following statements is incorrect concerning just-in-time (JIT) processing?

- U.S. firms are switching to JIT processing in response to foreign competition.

- JIT manufacturing is dedicated to producing the right products at the right time as they are needed.

- JIT strives to eliminate inventories by using a “push” approach in manufacturing.

- JIT accounting creates a Raw and In-Process Inventory account.

- (L.O. 9) Which of the following statements is incorrect concerning activity-based costing (ABC)?

- ABC may be used with either a job order or process cost accounting system.

- ABC assumes all costs related to the activity should respond proportionally to changes in the activity level of the cost driver.

- The primary benefit of ABC is more accurate and meaningful product costing.

- ABC focuses on units of production.

![]()

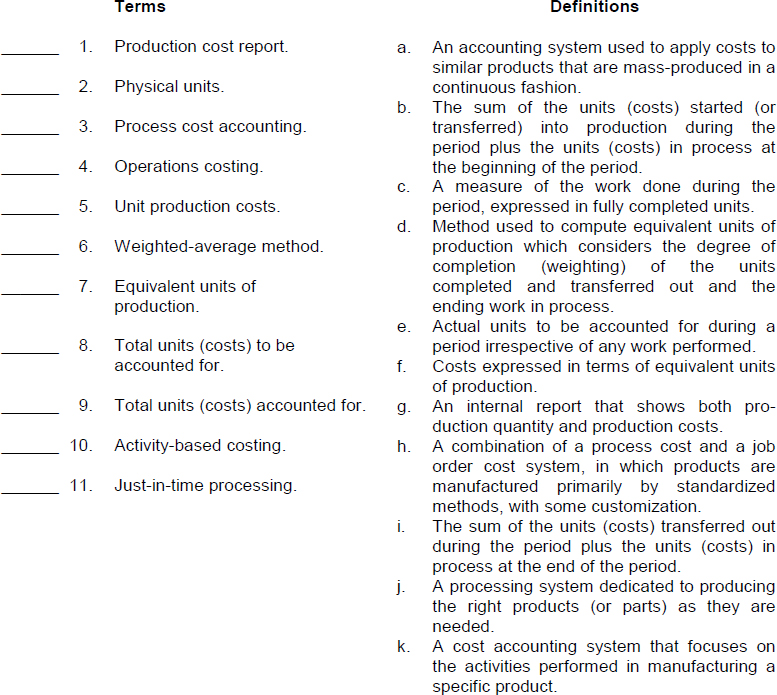

Match each term with its definition by writing the appropriate letter in the space provided.

![]()

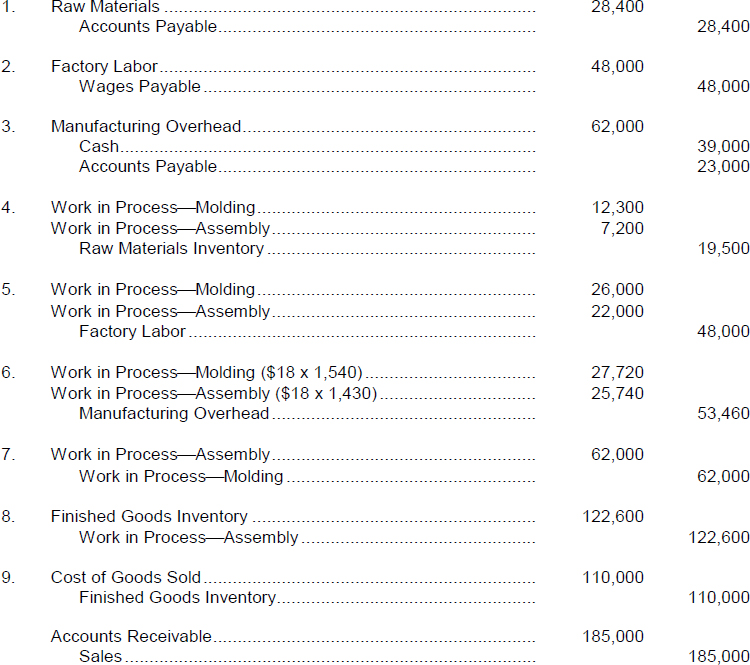

EX. 21-1 Avanti Manufacturing Company has two production departments: Molding and Assembly. March 1 inventories are Raw Materials $3,600, Work in Process—Molding $2,200, Work in Process—Assembly $8,800 and Finished Goods $26,000. During March, the following transactions occurred:

1. Purchased $28,400 of raw materials on account.

2. Incurred $48,000 of factory labor. (Credit Wages Payable.)

3. Incurred $62,000 of manufacturing overhead; $39,000 was paid and the remainder is unpaid.

4. Requisitioned materials for Molding $12,300 and Assembly $7,200.

5. Used Factory labor for Molding $26,000 and Assembly $22,000.

6. Applied overhead at the rate of $18 per machine hour. Machine hours were Molding 1,540 and Assembly 1,430.

7. Transferred goods costing $62,000 from the Molding Department to the Assembly Department.

8. Transferred goods costing $122,600 from Assembly to Finished Goods.

9. Sold goods costing $110,000 for $185,000 on account.

Instructions

Journalize the transactions. (Omit explanations.)

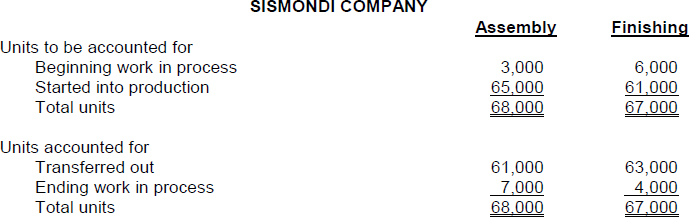

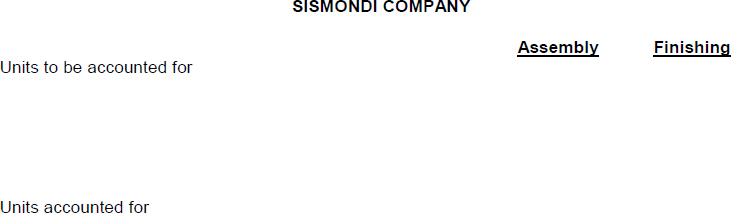

EX. 21-2 (L.O. 5 and 6) Sismondi Company has a process cost accounting system. During May, the Assembly and Finishing Departments had the following data concerning physical units:

Assembly:

| Work in process, May 1 | 3,000 |

| Started into process during the month | 65,000 |

| Work in process, May 31 | 7,000 |

Finishing:

| Work in process, May 1 | 6,000 |

| Transferred in from Assembly Department during the month | ? |

| Work in process, May 31 | 4,000 |

Instructions

Compute the physical units transferred out and in process for each department.

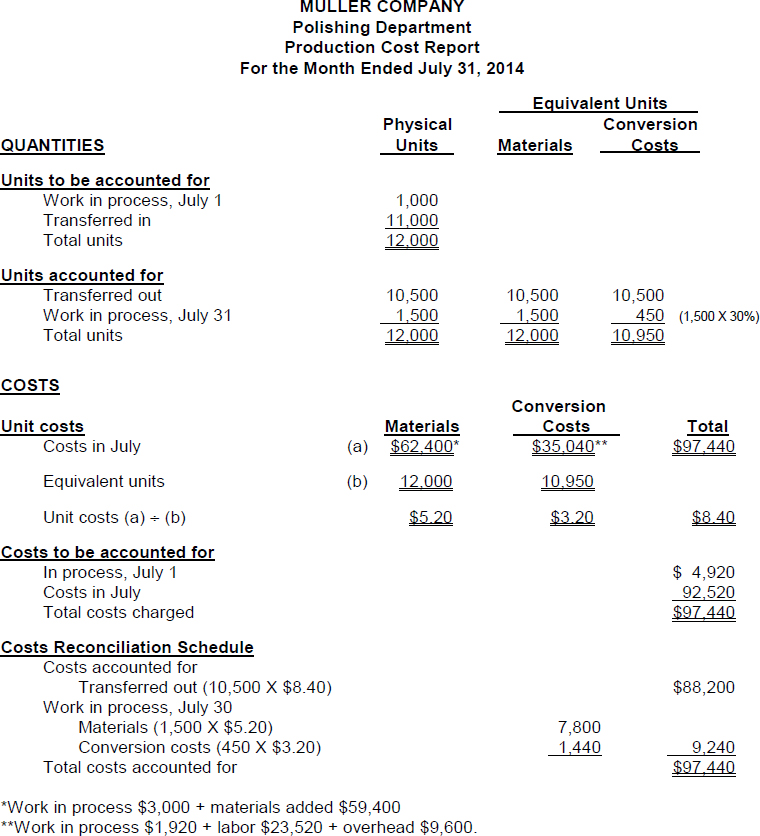

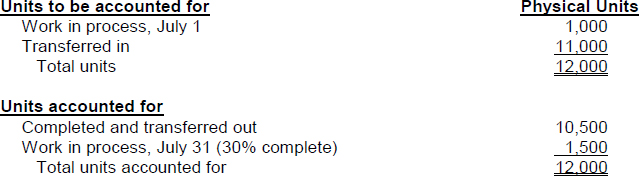

EX. 21-3 (L.O. 2 through 8) The Muller Company reports the following physical units for its Polishing Department for the month ended July 31, 2014.

Work in process July 1 was $3,000 for direct materials and $1,920 for conversion costs. Costs incurred in July were: materials $59,400, labor $23,520, and overhead $9,600. The percentage complete refers to conversion costs. Materials and transferred in units are added at the beginning of the process.

Instructions

Prepare the production cost report.

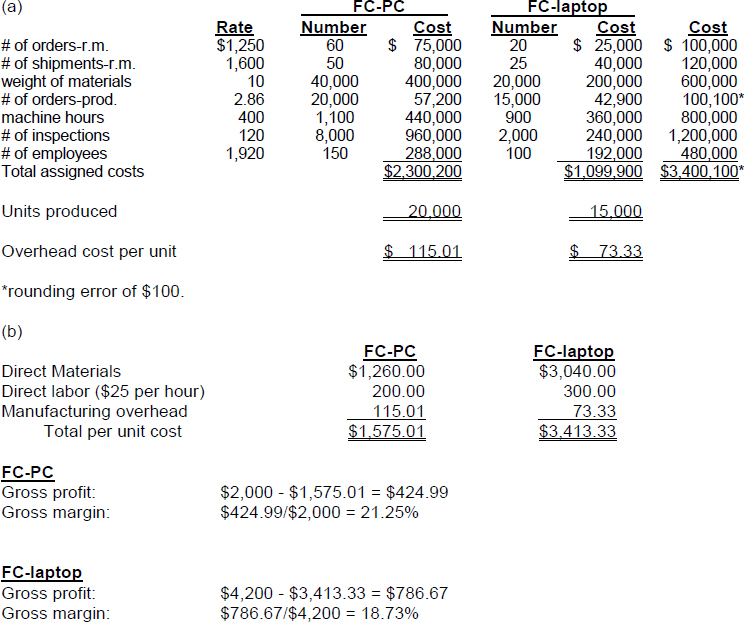

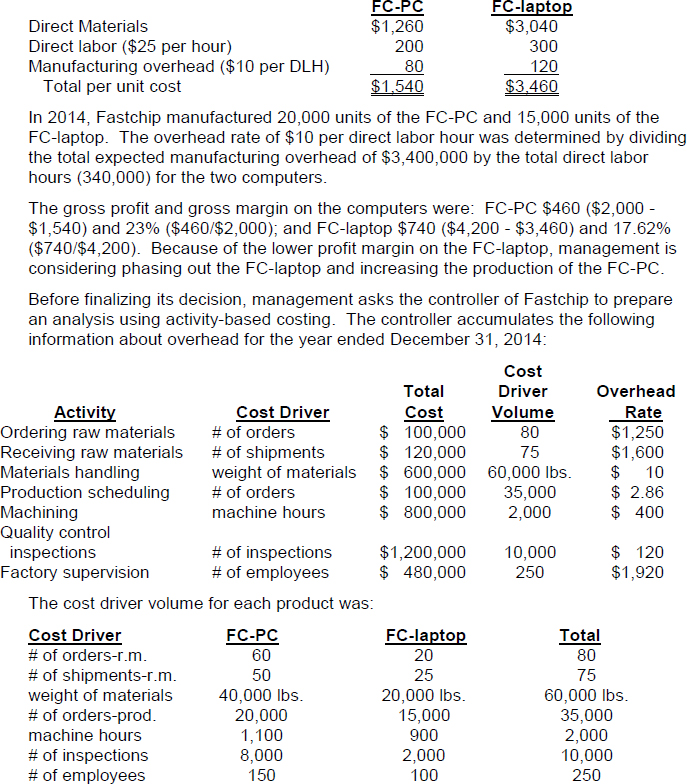

*EX. 21-4 (L.O. 11) Fastchip, Inc. manufactures two computers: the FC-PC which sells for $2,000, and the FC-laptop, which sells for $4,200. The production cost per unit for each computer in 2014 was as follows:

Instructions

(a) Assign the total 2014 manufacturing overhead costs to the two products using activity-based costing (ABC).

(b) What was the cost per unit, gross profit and gross margin of each model using ABC costing?

![]()

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

| 1. (F) | Job order costing focuses on the individual job, while process cost accounting focuses on the processes involved in producing homogeneous products. |

| 2. (T) | |

| 3. (F) | A distinctive feature of process cost accounting is that individual work in process accounts are maintained for each production department or manufacturing process. |

| 4. (F) | Under process cost accounting, the determination of total manufacturing costs is made for each accounting period. |

| 5. (F) | Both job order costing and process costing track the same three manufacturing cost elements—direct materials, direct labor, and manufacturing overhead. |

| 6. (F) | The flow of costs indicates that materials, labor, and manufacturing overhead can be added in any or all departments. |

| 7. (T) | |

| 8. (T) | |

| 9. (F) | Fewer requisitions are generally required because the materials are used for processes rather than jobs. |

| 10. (T) | |

| 11. (F) | When finished goods are sold, the entry to record the cost of goods sold is a debit to Cost of Goods Sold and a credit to Finished Goods Inventory. |

| 12. (T) | |

| 13. (T) | |

| 14. (T) | |

| 15. (T) | |

| 16. (T) | |

| 17. (F) | The unit conversion cost is equal to the total conversion costs divided by equivalent units of conversion costs. |

| 18. (T) | |

| 19. (F) | The order of calculation in a production cost report requires that the computation of the physical unit flow come before the computation of the unit production costs. |

| 20. (T) | |

| 21. (F) | A primary objective of just-in-time manufacturing is to eliminate all manufacturing inventories. |

| 22. (T) | |

| 23. (T) |

MULTIPLE CHOICE

MATCHING

- g

- e

- a

- h

- f

- d

- c

- b

- i

- k

- j

EX. 21-1

EX. 21-2