Chapter 24

BUDGETARY CONTROL AND RESPONSIBILITY ACCOUNTING

| The Navigator | |

After studying this chapter, you should be able to:

- Describe the concept of budgetary control.

- Evaluate the usefulness of static budget reports.

- Explain the development of flexible budgets and the usefulness of flexible budget reports.

- Describe the concept of responsibility accounting.

- Indicate the features of responsibility reports for cost centers.

- Identify the content of responsibility reports for profit centers.

- Explain the basis and formula used in evaluating performance in investment centers.

![]()

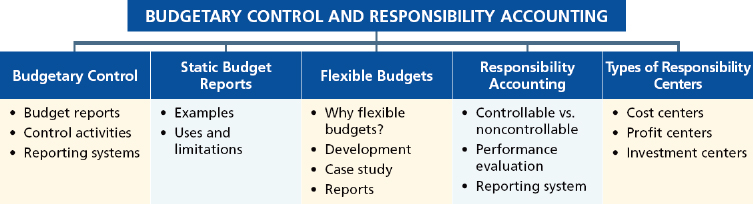

PREVIEW OF CHAPTER 24

In contrast to Chapter 23, we now consider how budgets are used by management to control operations. This chapter focuses on two aspects of management control: (1) budgetary control and (2) responsibility accounting. The content and organization of this chapter are as follows:

![]()

Budgetary Control

- (L.O. 1) The use of budgets in controlling operations is known as budgetary control. Such control takes place by means of budget reports that compare actual results with planned objectives. The budget reports provide management with feedback on operations.

- Budgetary control involves:

- Developing budgets.

- Analyzing the differences between actual and budgeted results.

- Taking corrective action.

- Modifying future plans, if necessary.

- Budgetary control works best when a company has a formalized reporting system. The system should

- Identify the name of the budget report such as the sales budget or the manufacturing overhead budget.

- State the frequency of the report such as weekly, or monthly.

- Specify the purpose of the report.

- Indicate the primary recipient(s) of the report.

Static Budget Reports

4. (L.O. 2) A static budget does not modify or adjust data regardless of changes in activity during the year. As a result, actual results are always compared with the budget data at the activity level used in developing the master budget.

5. A static budget is appropriate in evaluating a manager's effectiveness in controlling costs when (a) the actual level of activity closely approximates the master budget activity level, and/or (b) the behavior of the costs in response to changes in activity is fixed.

Flexible Budgets

6. (L.O. 3) A flexible budget projects budget data for various levels of activity. The flexible budget recognizes that the budgetary process is more useful if it is adaptable to changed operating conditions. This type of budget permits a comparison of actual and planned results at the level of activity actually achieved.

7. To develop the flexible budget, the following steps are taken:

a. Identify the activity index and the relevant range of activity.

b. Identify the variable costs, and determine the budgeted variable cost per unit of activity for each cost.

c. Identify the fixed costs, and determine the budgeted amount for each cost.

d. Prepare the budget for selected increments of activity within the relevant range.

8. For manufacturing overhead costs, the activity index is usually the same as the index used in developing the predetermined overhead rate; that is, direct labor hours or machine hours. For selling and administrative expenses, the activity index usually is sales or net sales.

9. The following formula may be used to determine total budgeted costs at any level of activity:

Total budgeted costs = Fixed costs + (Total variable cost per unit × activity level)

10. Total budgeted costs at each level of activity can be shown graphically.

a. In a graph, the activity index is shown on the horizontal axis and costs are shown on the vertical axis.

b. The total budgeted costs for each level of activity are then identified from the total budgeted cost line.

11. Flexible budget reports are another type of internal report produced by managerial accounting. The flexible budget report consists of two sections: (a) production data such as direct labor hours and (b) cost data for variable and fixed costs. It also shows differences between budget and actual results.

Responsibility Accounting

12. (L.O. 4) Responsibility accounting involves accumulating and reporting costs (and revenues, where relevant) on the basis of the manager who has the authority to make the day-to-day decisions about the items. A manager's performance is evaluated on matters directly under that manager's control.

13. Responsibility accounting can be used at every level of management in which the following conditions exist:

a. Costs and revenues can be directly associated with the specific level of management responsibility.

b. The costs and revenues are controllable at the level of responsibility with which they are associated.

c. Budget data can be developed for evaluating the manager's effectiveness in controlling the costs and revenues.

14. Responsibility accounting is especially valuable in a decentralized company. Decentralization means that the control of operations is delegated to many managers throughout the organization. A segment is an identified area of responsibility in decentralized operations.

15. Responsibility accounting is an essential part of any effective system of budgetary control. It differs from budgeting in two respects:

a. A distinction is made between controllable and noncontrollable items.

b. Performance reports either emphasize or include only items controllable by the individual manager.

16. A cost is considered controllable at a given level of managerial responsibility if that manager has the power to incur it within a given period of time. Costs incurred indirectly and allocated to a responsibility level are considered to be noncontrollable at that level.

17. Performance evaluation is a management function that compares actual results with budget goals. Performance evaluation includes management by exception and behavioral and reporting principles.

18. Management by exception means that top management's review of a budget report is focused either entirely or primarily to differences between actual results and planned objectives. The guidelines for identifying an exception are based on materiality and controllability.

19. Behavioral principles include: (1) managers of responsibility centers should have direct input into the process of establishing budget goals of their area of responsibility; (2) the evaluation of performance should be based entirely on matters that are controllable by the manager being evaluated; (3) top management should support the evaluation process; (4) the evaluation process must allow managers to respond to their evaluations; and (5) the evaluation should identify both good and poor performance.

20. A responsibility reporting system involves the preparation of a report for each level of responsibility shown in the company's organization chart. A responsibility reporting system permits management by exception at each level of responsibility within the organization.

Responsibility Centers and Cost Centers

21. (L.O. 5) Responsibility centers may be classified into one of three types. A cost center incurs costs (and expenses) but does not directly generate revenues. A profit center incurs costs (and expenses) but also generates revenues. An investment center incurs costs (and expenses), generates revenues, and has control over investment funds available for use.

22. A responsibility report for cost centers compares actual controllable costs with flexible budget data. Only controllable costs are included in the report, and no distinction is made between variable and fixed costs.

Profit Centers

23. (L.O. 6) Direct fixed costs or traceable costs are costs that relate specifically to a responsibility center and are incurred for the sole benefit of the center. Indirect fixed costs or common costs pertain to a company's overall operating activities and are incurred for the benefit of more than one profit center.

24. A responsibility report for a profit center shows budgeted and actual controllable revenues and costs. The report is prepared using the cost-volume-profit income statement format.

25. In the responsibility report for a profit center:

a. Controllable fixed costs are deducted from contribution margin.

b. The excess of contribution margin over controllable fixed costs is identified as controllable margin.

c. Noncontrollable fixed costs are not reported.

26. Controllable margin is considered to be the best measure of the manager's performance in controlling revenues and costs.

Investment Centers

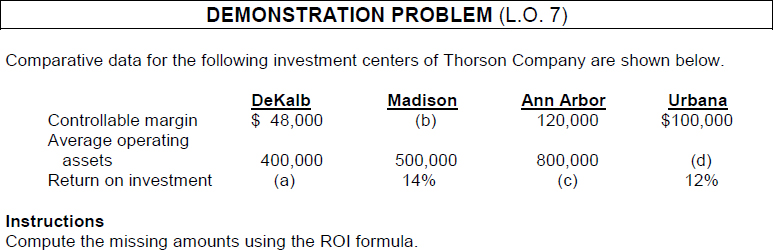

27. (L.O. 7) The primary basis for evaluating the performance of a manger of an investment center is return on investment (ROI). The formula for computing return on investment is: Investment Center Controllable Margin (in dollars) ÷ Average Operating Assets = Return on Investment.

a. Operating assets consist of current assets and plant assets used in operations by the center. Nonoperating assets such as idle plant assets and land held for future use are excluded.

b. Average operating assets are usually based on the beginning and ending cost or book values of the assets.

28. A manager can improve ROI by (a) increasing controllable margin or (b) reducing average operating assets.

29. The return on investment approach includes two judgmental factors:

a. Valuation of operating assets—cost, book value, appraised value, or market value.

b Margin (income) measure—controllable margin, income from operations, or net income.

![]()

![]()

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

![]()

MULTIPLE CHOICE

Circle the letter that best answers each of the following statements.

- (L.O. 1) Which of the following would not be considered an aspect of budgetary control?

- It assists in the determination of differences between actual and planned results.

- It provides feedback value needed by management to see whether actual operations are on course.

- It assists management in controlling operations.

- It provides a guarantee for favorable results.

- (L.O. 1) Budgetary control involves all but one of the following:

- Modify future plans, if necessary.

- Analyze differences between actual and planned results.

- Take disciplinary action.

- Develop the budget.

- (L.O. 1) Which of the following is not part of a formalized reporting system?

- Identify the name of the budget reports.

- State the corrective action that should be taken.

- Specify the purpose of the report.

- Indicate the primary recipient(s) of the report.

- (L.O. 2) In a static budget,

- data are modified and adjusted according to changes in activity during the year.

- the actual results are always compared with budget data at the original budgeted activity level.

- it is important to select an activity index and a relevant range of activity.

- only budgeted fixed costs are compared with actual fixed costs.

- (L.O. 2) A static budget is usually appropriate in evaluating a manager's effectiveness in controlling:

- fixed manufacturing costs and fixed selling and administrative expenses.

- variable manufacturing costs and variable selling and administrative expenses.

- fixed manufacturing costs and variable selling and administrative expenses.

- variable manufacturing costs and fixed selling and administrative expenses.

- (L.O. 3) In the Johnson Company, indirect labor is budgeted for $24,000 and factory supervision is budgeted for $8,000 at normal capacity of 80,000 direct labor hours. If 90,000 direct labor hours are worked, flexible budget total for these costs is:

- $32,000.

- $36,000.

- $35,000.

- $33,000.

- (L.O. 3) Vidmar Company uses flexible budgets. At normal capacity of 8,000 units, budgeted manufacturing overhead is: $64,000 variable and $180,000 fixed. If Vidmar had actual overhead costs of $250,000 for 9,000 units produced, what is the difference between actual and budgeted costs?

- $2,000 unfavorable.

- $2,000 favorable.

- $6,000 unfavorable.

- $8,000 favorable.

- (L.O. 3) A flexible budget provides a basis for evaluating a manager's performance for:

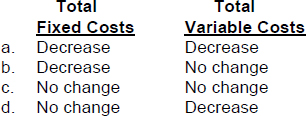

- (L.O. 3) When production levels decline within a relevant range and a flexible budget is used, what effects would be anticipated with respect to each of the following?

- (L.O. 3) A flexible budget is appropriate for:

- (L.O. 3) The criteria used in identifying an exception under management by exception are:

- materiality and frequency.

- controllability and frequency.

- materiality and controllability.

- none of the above.

- (L.O. 4) Responsibility accounting cannot be used effectively when:

- costs are allocated to the responsibility level.

- budget data can be developed for evaluating the manager's effectiveness in controlling costs.

- costs are controllable at the level of responsibility with which they are associated.

- costs can be directly associated with the specific level of responsibility.

- (L.O. 4) Controllable costs for responsibility accounting purposes are those costs that are directly influenced by:

- a given manager within a given period of time.

- a change in activity.

- production volume.

- sales volume.

- (L.O. 4) A responsibility reporting system:

- begins with the highest level of responsibility and moves downward to the lowest level.

- involves the preparation of a report for each level of responsibility shown in the company's organization chart.

- does not permit comparative evaluations of responsibility centers.

- does not permit management by exception at each level of responsibility.

- (L.O. 5) Responsibility reports for cost centers will include:

- (L.O. 6) Which of the following is not a direct fixed cost of a profit center?

- Timekeeping for center's employees.

- Depreciation on center's equipment.

- Profit center manager's salary.

- General office administrative costs.

- (L.O. 7) In the return on investment (ROI) formula:

- sales are divided by average investment center operating assets.

- controllable margin is divided by sales.

- controllable margin is divided by average investment center operating assets.

- sales are divided by net income.

- (L.O. 7) Which of the following will cause an increase in ROI?

- An increase in variable costs.

- An increase in average operating assets.

- An increase in sales.

- An increase in controllable fixed costs.

- (L.O. 7) Which of the following is incorrect about average operating assets?

- Both current assets and plant assets are included.

- Nonoperating assets are excluded.

- The assets are valued at fair market values.

- The average may be based on beginning and ending recorded balances.

- (L.O. 7) If controllable margin is $300,000 and the average investment center operating assets are $1,000,000, the return on investment is:

- .33%.

- 3.33%.

- 10%.

- 30%.

![]()

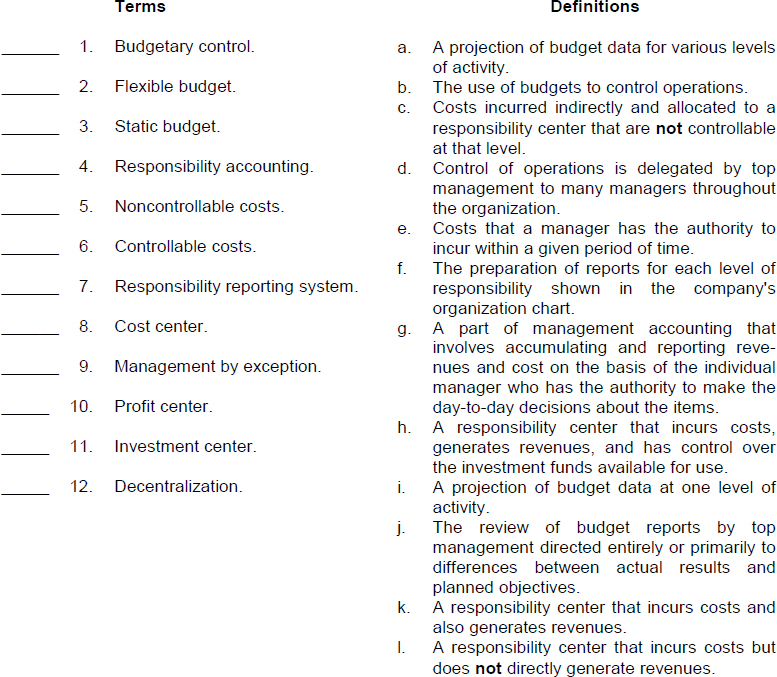

MATCHING

Match each term with its definition by writing the appropriate letter in the space provided.

![]()

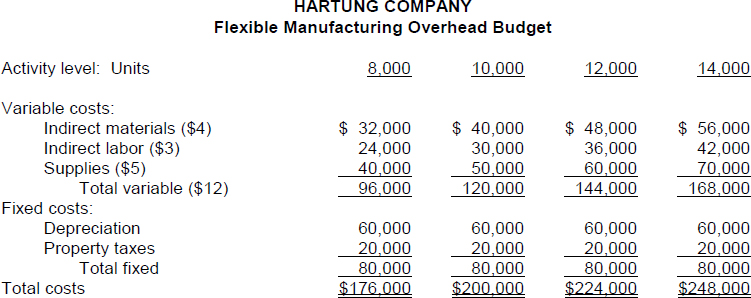

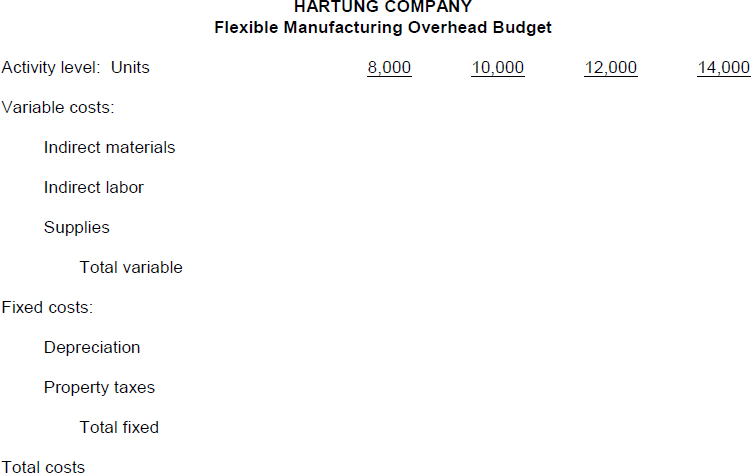

EX. 24-1 (L.O. 3) Hartung Company is in the midst of preparing its flexible budget for manufacturing overhead. At a production level of 10,000 units, unit costs are: Indirect materials $4, Indirect labor $3, Supplies $5, Depreciation $6, and Property taxes $2. Depreciation and property taxes are fixed costs.

Instructions

Complete the following four-column flexible budget for the manufacturing costs for the Hartung Company.

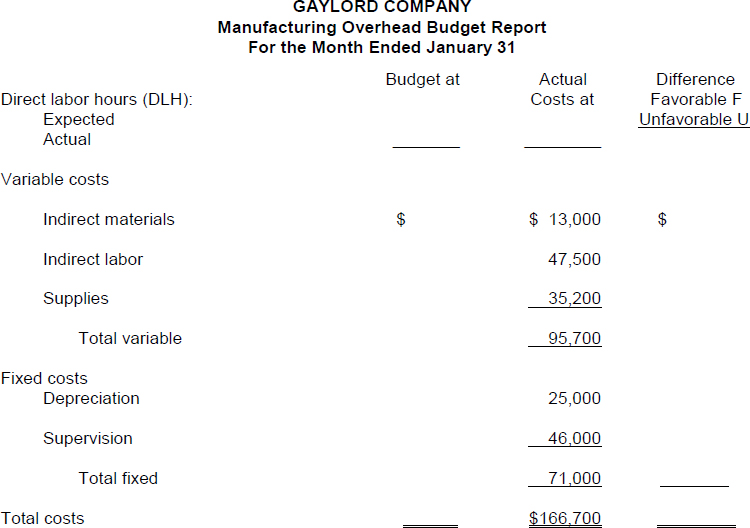

EX. 24-2 (L.O. 3) Gaylord Company has the following flexible budget for manufacturing overhead:

![]()

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

TRUE-FALSE

| 1. (T) | |

| 2. (T) | |

| 3. (F) | A static budget is an effective means to evaluate a manager's ability to control costs provided (1) the actual level of activity closely approximates the master budget activity level, or (2) the behavior of the costs in response to changes in activity is fixed. |

| 4. (T) | |

| 5. (F) | To develop the flexible budget, the following steps are taken:

|

| 6. (T) | |

| 7. (F) | Management by exception does not mean that top management will investigate every difference. Exceptions are identified by materiality and controllability of the item. |

| 8. (T) | |

| 9. (F) | Responsibility accounting is especially valuable in a decentralized company. |

| 10. (T) | |

| 11. (F) | A controllable cost can be variable or fixed, and a noncontrollable cost can also be variable or fixed. |

| 12. (T) | |

| 13. (T) | |

| 14. (T) | |

| 15. (F) | There is usually no distinction between variable and fixed costs in a responsibility report for cost centers. |

| 16. (F) | Most direct fixed costs are controllable by the profit center manager. |

| 17. (F) | The basic formula for computing return on investment is controllable margin (in dollars) divided by average operating assets. |

| 18. (T) | |

| 19. (F) | A number of judgmental factors are involved such as the proper valuation of operating assets and selection of the income measure to be used. |

| 20. (T) |

MULTIPLE CHOICE

MATCHING

- b

- a

- i

- g

- c

- e

- f

- l

- j

- k

- h

- d

EXERCISES

EX. 24-1