Taiwan

Abstract:

This chapter discusses the development and evolution of Taiwan’s ICT industry in the context of a global production network (GPN) and global innovation network (GIN). Particular attention is paid to characteristic features of R&D and offshoring by Taiwan’s ICT industry. The chapter also presents four case studies of firms, showing their significance in ICT R&D and innovation and their representative features of certain aspects of Taiwanese ICT industry. On balance, the globalization of technology has come to a stage in which Taiwan together with some of the developing countries in East Asia has become a source of R&D and innovation – not just a technology recipient and late-adopter as before. As a result of this, Taiwan as well as the peer players in the Asia-Pacific may serve as a partner of collective innovation, with their involvement at the early stage of the product life cycle.

Introduction

Taiwan used to be well known as one of the Asian newly industrializing countries (NICs) in the late 20th century, with its average annual economic growth rates being as high as 8.2% in the 1980s and 6.5% in the 1990s. On the one hand, in terms of GDP structure, Taiwan’s manufacturing sector declined from an all-time peak of 39.4% of GDP in 1986 to a low of 25.0% in 2008. The service sector, by contrast, has followed a constantly rising trend and now accounts for more than 70% of Taiwan’s GDP (73.3% in 2008). On the other hand, in terms of the annual growth rate, the manufacturing sector has still outpaced the service sector; and exports have been a major source of Taiwan’s economic growth.

Taiwan’s economic achievement had much to do with its export-oriented industrialization strategy. Underlying this was a process in which Taiwan’s economic structure was profoundly transformed. Its economic takeoff started with labor-intensive light industries and then heavy and chemical industries before the 1980s. Taiwan’s transition towards high-tech industries began to gather momentum afterwards, giving rise to the fast development of such strategic industries as the ICT hardware, semiconductor, and optoelectronic sectors.

The size of the ICT sector

An overview

Taiwan has been an important player in the global ICT industry for decades, occupying a significant position within the global production network (GPN) and global innovation network (GIN) (Angel and Engstrom, 1995; Borrus and Borrus, 1997; Chen, 2002; Ernst, 2006). “No Jobs, no jobs” was an in-joke among Taiwanese ICT firms, referring to the close relationship between Apple’s late CEO and the company’s Taiwanese partners. On the other side of the coin is the statement written by Ken Belson in the New York Times in 2007, “Etched into the back of every iPhone are the words ‘Designed by Apple in California. Assembled in China’.” Apple might as well have added “Made in Taiwan” (or more precisely, “Designed in Taiwan”). Such a statement can also apply to HP and Dell in notebook computers and Vizio in LCD TVs. Put another way, Taiwan, together with certain parts of Asia, can act as the kingmaker for these U.S. ICT firms.

Underlying the above relationships are some characteristic features of the Taiwanese ICT industry. First of all, major Taiwanese ICT firms tend to be specialized in a vertically separate manner, but are knitted together through social and business connections. Second, Taiwanese ICT firms are generally well known in the industrial community, but most are not famous household names in the final product market, but there are a few exceptions, like HTC, Acer, and Asus. This is because most of them tend to serve as original equipment manufacturing (OEM) or original design manufacturing (ODM) partners for brand marketers (Ernst, 2005; Hilmola et al., 2005), such as Apple, HP, and Dell. As a result, Taiwanese ICT firms have managed to establish strong technological and innovation capabilities through internal R&D, technology transfer from local research institutes, and R&D networking with global leading players, which in turn have made Taiwan a major source of contract work for internationally prominent ICT firms. Third, due to their intensified relationships with international brand marketers, Taiwanese ICT firms have gone global, initially in manufacturing, supply chain management, and logistics, and more recently in R&D. As a result, nowadays, it is far too simplistic to state that Taiwan’s success in the ICT industry is attributable to manufacturing muscle alone; so too is the thesis on Taiwan’s local industrial clustering (Kraemer et al., 1996).

Taiwan is highly specialized in the ICT sector, in terms of manufacturing GDP, exports, and more importantly R&D expenditures. Particularly, Taiwan’s manufacturing R&D is highly concentrated in the ICT sector. In addition, the offshore production of Taiwan-based computing/communications firms right now much outweighs their domestic production. The role played by Taiwan’s ICT industry in the GPN has consequently shifted from a key producer and exporter of end products to that of important components and parts (intermediate goods), especially in terms of domestic production. This development cannot be reduced to the argument that Taiwan-based ICT end product producers have lost their competitive edges to their international competitors; instead, it should be interpreted within the context of the GPN.

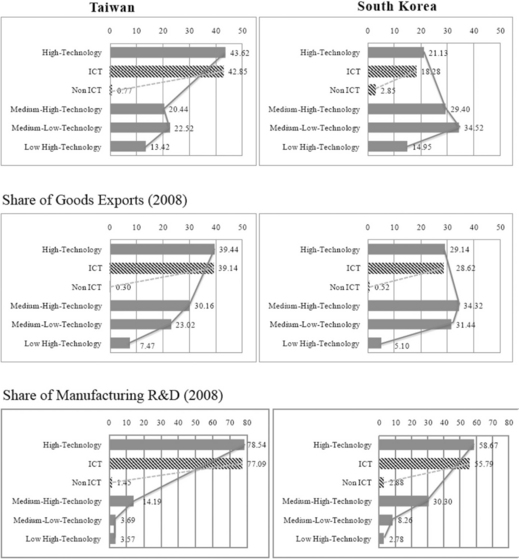

We follow the definition of the OECD and classify the manufacturing sector in four groups: high technology, medium–high technology, medium–low technology, and low-technology sectors. As shown in Figure 4.1, the high-technology sector as a whole accounted for 43.62% of manufacturing GDP in 2008, compared with 20.44% for the medium– high technology sector and 22.52% for the medium–low technology sector. More importantly, the lion’s share of the high-technology sector (42.85% of manufacturing GDP) is associated with the ICT sector. The ICT sector in the high-technology industry also plays a significant role in Taiwan’s manufacturing exports. Of 39.44% of manufacturing exports by the high-technology industry, 39.14% is attributed to the ICT sector. Even more significant is the high concentration of Taiwan’s manufacturing business R&D in the ICT sector. In the high-technology sector, the ICT sector accounted for 77.09% of Taiwan’s manufacturing business R&D, compared with 1.45% for the non-ICT high-technology sector.

Figure 4.1 Structural characteristics of manufacturing: Taiwan versus South Korea (2008) Source: Compiled by the authors (June 2011).

Though both South Korea and Taiwan are known for their ICT industry, South Korea has comparative strengths in a few medium–high technology sectors, such as the automotive, consumer electronics, and shipping industries. In addition, Taiwan’s industrial R&D is overwhelmingly concentrated in ICT, with this sector alone accounting for more than 70% of Taiwan’s R&D performed by the business sector, as compared with 55.79% in South Korea.

The subsector

In the 1980s, outward investment to Taiwan made by the then dominant vertically integrated firms in advanced countries, such as the U.S. and Japan, triggered Taiwan’s entry into the supply chain of the ICT industry, initially the personal computer (PC) and then the notebook computer subsector. Later on, local firms – Acer and Tatung, for example – were able to take up the vacuum caused by the withdrawal of foreign firms during the mid-1980s due to rising production costs at that time, which then laid the foundation for the formation of local industrial clusters. The Taiwanese PC makers were pioneers in modularizing value chains in the ICT sector and created the OEM and ODM business models. Due credit should also be given to the public sector for its efforts in mobilizing government-sponsored research institutes, such as the Industrial Technology Research Institute (ITRI) and the Institute for Information Industry (III) for technology upgrading and establishing the Hsinchu Science Park, which has developed into the center of gravity for the local ICT industry.

However, an important milestone in the development of the GPNs in Taiwan’s PC industry was the outreach of local firms, starting from the early 1990s. Their outward investment was initially directed towards Southeast Asia, but later towards China and elsewhere in the world. The offshore production of Taiwan-based PC firms has nowadays much outweighed their domestic production. In fact, even such brand-new products as Xbox, iPhone, and iPad are nowadays mostly made/assembled in China and/or Southeast Asia, mainly because of manufacturing offshoring by the Taiwan-based ICT OEM/ODM firms. This has resulted in a substantial change in the structure of Taiwan’s domestic production and exports, moving from ICT final products to intermediate goods, integrated circuits (ICs), and liquid crystal display (LCD) panels in particular.

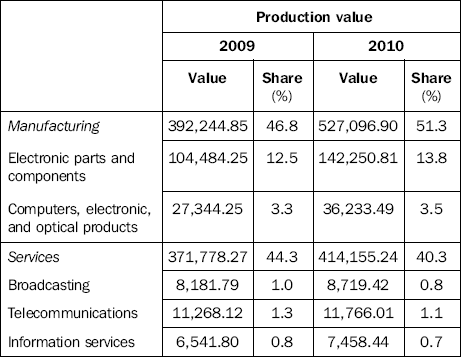

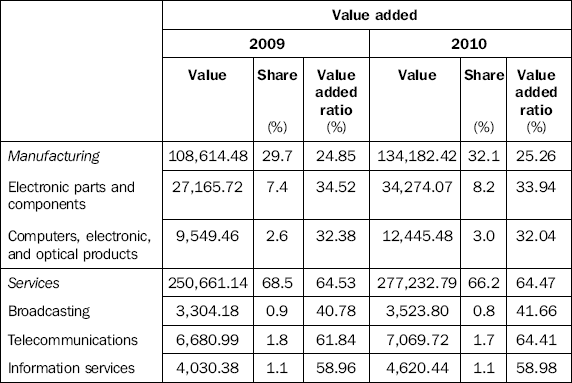

As shown in Table 4.1, electronic parts and components as a field accounted for 13.8% of the production value in the whole manufacturing sector in 2010, compared with 3.5% for the category of computers, electronic, and optical products (final products). With their value added ratios being above 30%, both categories accounted for more than one third of the manufacturing value added in Taiwan. On the other hand, due to its small domestic market and weaknesses in service exports, the major ICT service subsectors, including broadcasting, telecommunications and information services, have relatively small production values in Taiwan.

Table 4.1

The profile of Taiwan’s ICT sector

Source: Data taken from Directorate General of Budget, Accounting, and Statistics (DGBAS) of Executive Yuan, compiled by the authors.

The GPN is a production scheme where various stages of a manufacturing process are undertaken at different geographic locations where they can be carried out most efficiently (UNCTAD, 2005). Along with the trend towards formation of the GPN in the global ICT sector, outsourcing and order-based production adopted by major brand marketers has greatly rationalized their global supply chain (Feenstra, 1998), and hence altered their contractual relationships with their Taiwanese counterparts. As a result, Taiwan’s ICT firms have participated in cross-border supply chain management, logistics operations, and after sales services, by forming a fast-response global production and logistics network. In addition, China has become an overwhelmingly important offshore production site for Taiwan-based PC and notebook computer firms, which has fueled China’s growing significance in the assembly and manufacturing of ICT products. There are even signs that China is playing a growing role in R&D (Chen, 2004). However, for most ICT firms, particularly the IC and LCD manufacturers, their R&D bases remain largely located in Taiwan. This together with the IC design industry has made Taiwan an innovation hub in the GPNs.

The development of Taiwan’s IC industry benefited a lot from technology transfer and international knowledge networking. Technology transfer from RCA (a U.S. electronics firm) to ITRI initially triggered the emergence of the local IC industry, which was then fueled by the fast development of the local PC industry in the late 1980s because of the industrial linkages between these two sectors. In particular, Taiwan Semiconductor Manufacturing Corporation (TSMC), a successful spin-off from ITRI, pioneered the business model of a “dedicated foundry manufacturing service”, simply carrying out contract fabrication work for global customers ranging from start-up ventures, well-established IC design houses to world-leading integrated device manufacturers (IDMs) (Chen, 2002). As a result, fabless1 IC design houses, as well as specialized IC packaging and testing firms, proliferated in Taiwan because access to external fabrication capacity lowered the barriers to entry into the IC design market. On top of that, the geographical concentration of IC and computer-related firms in Hsinchu Science Park generated agglomeration effects that allowed these firms to exploit the benefits of proximity and outsourcing. Therefore, even though they specialize in one segment of the value chain, IC firms in Taiwan are networked by social and business connections.

It is also evident that Taiwan’s IC industry is organized as an industrial network system with a strong connection to Silicon Valley, the center of the global IC market and of global IC technology. Underlying this exchange were overseas Chinese and Chinese expatriates, who had played an important role in establishing the transpacific social and business networks that had proved crucial in connecting Taiwan’s production system with advanced market knowledge and technology. Apart from the ethnic social network, the similarity in industrial structure made networking between Silicon Valley and Hsinchu Science Park much easier and more intensive (Hsu and Saxenian, 2000; Kim and von Tunzelmann, 1998).

LCD technology began to take root in Taiwan in the early 1990s, thanks to initial technology transfer from the U.S.A. and a government R&D program performed by ITRI, a major nonprofit research institute in Taiwan. However, it was technology transfer from Japan after the Asian Financial Crisis in 1997 and the growing significance of Taiwanese firms in the production of LCD monitors and notebook computers that had provided ammunition to the burgeoning development of the LCD industry in Taiwan. The government took advantage of this trend by promoting the so-called “Two-Trillion Industries”, namely the IC and LCD sectors, from the second half of the 1990s on. A few other science parks were therefore established to accommodate a growing number of industrial players in these high-tech industries. Some of them have become so well established as to have emerged as new industrial clusters in Taiwan. Prominent examples include Southern Taiwan Science Park, Central Taiwan Science Park, and Nankang Software Park.

Right now Taiwan and South Korea are engaged in head-to-head competition to be the global leader in the production of LCD panels. However, both South Korea and Japan are ahead of Taiwan in terms of technology development and production deployment for large-sized LCD panels. In addition, the players in these two countries are diversified conglomerates with global brand names, such as Samsung and LG (LG Display) in South Korea and Sony in Japan, which may facilitate them to exploit economy of scope, especially when it comes to the manufacturing and marketing of LCD TVs. In contrast, the LCD industry in Taiwan is largely featured by vertical disintegration, except for the fact that local leading players, such as AUO and ChiMei, also produce LCD monitors and LCD TVs with their own brands.

R&D expenditure

ICT R&D

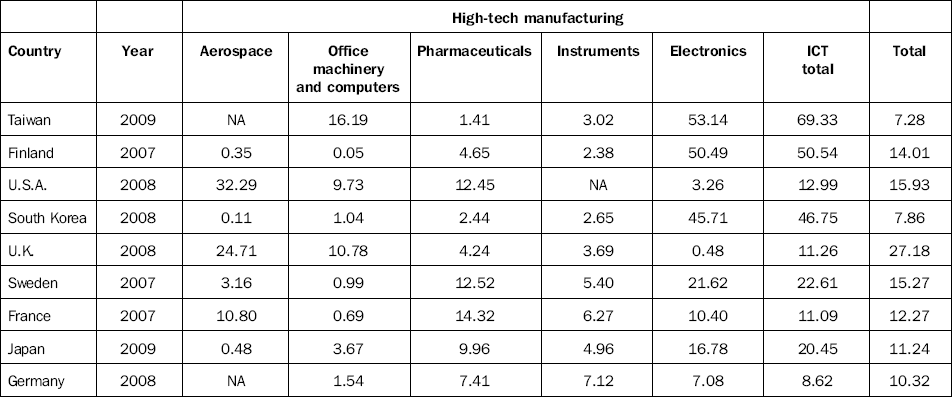

Taiwan has persistently invested in R&D. As a result, Taiwan’s R&D intensity (R&D/GDP) increased from 2.08% in 2001 to 2.90% in 2010, with around 70% of the national R&D expenditure being invested by the private sector. Considering electronics and office machinery and computers as major fields of ICT, about 70% of the national total and BERD can be associated with ICT fields, indicating that Taiwan is highly specialized in ICT R&D (69.33%) even compared with many peer countries, including Finland (50.54%), South Korea (46.75%), and Sweden (22.61%). A closer look at Table 4.2 indicates that the lion’s share of Taiwan’s ICT R&D is related to the electronics field (53.14%), much more than the office machinery and computers field (16.19%). In contrast, service accounted for just about 7.28% of Taiwan’s BERD in 2009 (see Table 4.2 for details).

Table 4.2

Percentage of BERD performed by sector in selected countries (%)

Note: The indicators of high-tech manufacturing follow OECD definitions. The ICT total includes those of electronics and office machinery and computers.

Source: OECD, Main Science and Technology Indicators, Vol. 2011, release 01; compiled by TIER.

Patents

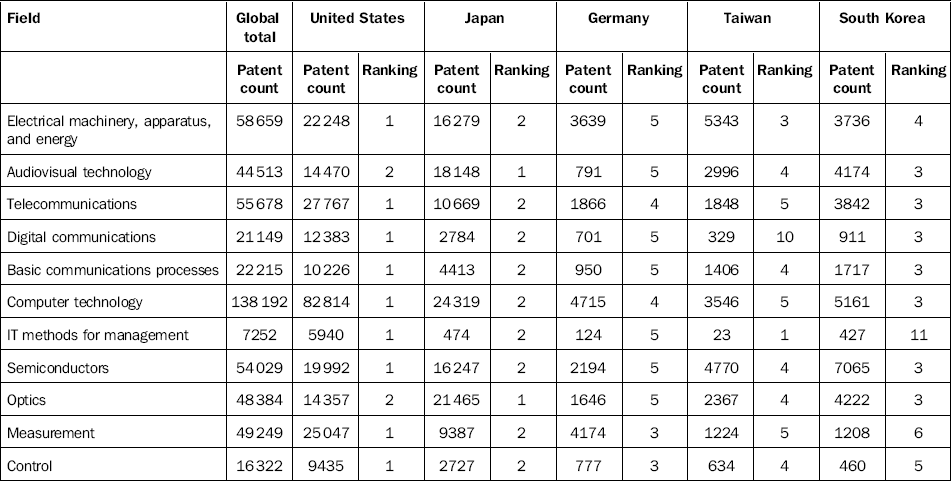

Taiwan has been very active in U.S. patenting. It should be noted that international patenting of firms can be a location or country-specific decision. Because Taiwanese ICT firms as a whole have a strong connection with the U.S.A. in terms of market and value chain relationships, they tend to file international patents in the U.S.A. Taiwan ranked 4 for eight years in a row (1999–2006), after only the U.S., Japan and Germany. Taiwan was overtaken by South Korea in 2007, but remained the fifth largest holder of U.S. patents afterwards. In addition, ICT-related fields have been the major part of Taiwanese patenting in the U.S.A. In terms of the ranking of accumulated U.S. patent counts over the period 2006–10, Taiwan performs particularly well in such fields as electrical machinery, apparatus and energy, semiconductors, computer technology and optics (see Table 4.3 for details). Ironically, even with so many U.S. patents, Taiwan has faced a huge deficit in technological trade. For example, in recent years, the value of Taiwan’s technology exports each year has been around a quarter that of technology imports, registering a substantial deficit of USD2.317 billion in 2009. In other words, Taiwan’s achievement in international patenting is not proportional to its trade balances in technology, a phenomenon termed the “innovation paradox”.

Table 4.3

U.S. patenting performance in ICT fields by selected countries, 2006–10

Source: USPTO Weekly Data; adapted from 2011 White Book on Taiwan Industrial Technology.

Chen (2007) discussed some reasons underlying the Taiwanese “innovation paradox” by referring to some characteristic features of Taiwan’s national innovation system. In short, Taiwanese ICT firms, on the one hand, are generally characterized by vertical disintegration and are deeply involved in OEM/ODM contacts for brand marketers; thus, individual firms specialize in a specific industrial and technological segment and may tend to focus their R&D efforts on incremental technological change in relation to a specific technological trajectory, leading to rapid proliferation of patents. On the other hand, following on closely from this, Taiwan’s ICT firms tend to pursue technological innovation on the pathway led by the architectural design created by leading architecture and/or industrial standard setters. As a result, the more their production volume expands, both domestically and overseas, the more royalties they pay to the architecture and/or industrial standard setters.

The role of FDI and offshoring in ICT R&D

Taiwan’s economic takeoff benefitted to quite an extent from foreign direct investment, but since the mid-1980s Taiwanese firms have gone international via outward investment. Before 1986, Taiwan’s international economic relations were connected mainly with Japan and the U.S.A. Japan’s technologies, machines, and key parts were imported to produce goods, and from its home base Taiwan exported to the U.S.A. and, to a lesser degree, Europe. After 1986, Taiwan’s outward investment started to take off, initially to Southeast Asia and more recently to China. Indeed, from the 1990s on, China has become the biggest host country for Taiwan’s outward investment, with China’s share of Taiwan’s outward investment reaching 60–70% in the second half of the 2000s. Taking 2008 as an example, Taiwan’s approved outward investment amounted approximately to USD15.16 billion, with 70.53% (USD10.69 billion) being directed to China.

In particular, both electronic parts and components manufacturing and computers as well as electronic and optical products manufacturing, which are mainly ICT related, have recently accounted for more than 40% of Taiwan’s annual outward manufacturing investment to China. As a result, China has become an important offshore production site for Taiwan-based PC and notebook computer firms, having significantly outweighed the latter’s domestic production since 2002. Along with this development, not only has China’s coverage of the ICT value chain at the mass production level become more comprehensive, but China is playing an increasingly important role in ICT GINs, resulting in part from the relocation of Taiwan-based ICT firms’ R&D functions (Chen, 2004; Ernst, 2006).

Since then, the local players, in many cases backed up by government R&D initiatives, have steadily become partners to international brand marketers. As a result, even though the electronic and electrical field has been the major area of FDI to Taiwan for decades, MNC operations in Taiwan have shifted towards international procurement offices and suppliers of key components and materials (e.g., electronic chemicals) for local ICT manufacturing. With regard to manufacturing, the local sectors supported by FDI have moved from the PC and notebook computer subsectors to the IC and LCD subsectors. In particular, both the U.S.A. and Japan have been important sources of key components and parts as well as manufacturing equipment for local ICT manufacturing. For example, ASML, the global second largest semiconductor equipment manufacturer has recently established in Taiwan a production plant and an R&D center for lithography, the first of its kind in Asia, in order to take advantage of the booming IC sector in Taiwan. Together with ASML, some other global leading players in semiconductor equipment, such as Lam Research and Tokyo Electron Limited (TEL) also set up international training centers in Taiwan. Even for IC design, local industrial clustering has also lured other foreign networked firms, such as EDA tool providers to set up operations in Taiwan.

Apart from FDI in production, some MNCs in Taiwan have also invested in R&D. Based on the dataset provided the Ministry of Economic Affairs (MOEA), Liu and Chen (2005) have managed to characterize, with statistical robustness, those foreign R&D subsidiaries with a higher R&D intensity in Taiwan. Among other findings, they found that those foreign-owned firms in Taiwan with a higher export propensity tended to be more R&D intensive, especially those of branded ICT firms. As an economy featured by international competitiveness and export orientation, Taiwan may be able to act as a host for some MNCs in order to capitalize on its comparative advantages to serve the international market.

Foreign-owned subsidiaries with higher R&D intensity are also found to be characterized by a greater degree of localization in terms of their sourcing of both production materials and capital goods. This is particularly true for ICT brand marketers, which have relied substantially on local sourcing in Taiwan. In addition, where Taiwan’s industrial sectors have a larger pool of R&D employees, their constituent foreign affiliates tend to be more R&D intensive. On the one hand, this seems to imply that the R&D efforts of foreign affiliates in Taiwan are driven by a local technology pool. On the other hand, assuming that a larger pool of R&D employees in a sector implies that its local firms are more technology aggressive, one can argue that indigenous R&D efforts serve as a complement to, rather than a substitute for, the R&D activities of foreign affiliates.

On top of that, the government in Taiwan has orchestrated a plan to encourage MNCs to establish R&D centers on the island, which since its implementation in 2002 has met with some success. Up to September 2010, sponsored by that program, there were some 46 R&D centers, established by 34 different MNCs. Of note is the fact that these R&D centers are related mainly to the current strength of Taiwan’s industrial development, with the lion’s share (65%) being focused on the broadly defined ICT area and showing a strong intention of collaborating with local firms. This may have something to do with the position of Taiwan’s ICT industry within GPNs and GINs. In the case of HP, IBM, and Motorola, the major players in Taiwan’s ICT industry can be regarded as these companies’ first-tier suppliers and/or ODM partners, especially with regard to components and barebones. As brand marketers have become hollowed-out, collaborative research and design between brand marketers and first-tier suppliers have increasingly come to the fore, which may be facilitated by the geographical proximity between the two parties’ knowledge bases. As for the Microsoft Technology Center, Microsoft provides essential platform technologies to the local ICT industry, based on which the latter may develop new products for the international as well as domestic markets. However, the role played by offshore R&D facilities in this case has gone beyond the traditional technology transfer units, which tend to perform adaptive R&D to meet local needs, but is by nature in line with the prevailing collaborative research and design model. In fact, some of their intelligent property outputs have been adopted by the R&D headquarters (Chen et al., 2009).

In addition, with some of Taiwan’s ICT firms having scaled down, or even having hollowed out their manufacturing operations in Taiwan, shifting them towards China and elsewhere, it may in fact become necessary for them to increasingly rely on their Chinese subsidiaries in order to engage in manufacturing-related R&D (Liu and Chen, 2007). This seems more likely in the case where the de-linking of R&D and manufacturing is feasible (Chen, 2004). As a matter of fact, the majority of Taiwanese ICT OEM/ODM vendors tend to conduct R&D, product design, and pilot runs mainly in Taiwan, while leaving mass production jobs to be undertaken at their overseas plants.

Such innovation offshoring is different from the familiar notion of R&D internationalization which tends to take a position that individual MNCs are the unit of analysis and MNCs’ offshore R&D is perceived as part of their own international R&D networks, facilitating them to exploit or explore both internal and external resources. However, our version of R&D internationalization has something to do with current restructuring in the ICT sector on the global scale. Within this process, different layers of industrial players are increasingly required to closely interact with one another for innovation. As part of this restructuring, this externalization of innovation no longer stops at the national border, but involves the reconfiguration of MNCs’ international R&D networks (Chen, 2007).

On balance, GPNs in the ICT industry have come to the fore. Characteristic features of GPNs include cross-border modularized production and speedy patchy production, instead of production under one roof and mass production as before. Therefore, from the standpoint of Taiwan’s ICT producers, the triangular linkages involving Taiwan (Hsinchu), China (the Yangtze River Delta), and the U.S.A. (Silicon Valley) may mean much more to their prosperity than does the local industrial cluster in Taiwan.

The Taiwanese ICT sector: company-level perspective

This section presents four case studies of firms.Selection of the cases for intensive study is based on their significance in ICT R&D and innovation and their representative features of certain aspects of Taiwanese ICT industry.

TSMC

TSMC has been regarded as a major catalyst in the evolution of the global IC industry. The company was created in 1987 to function as a dedicated foundry service provider, simply carrying out contract fabrication work for global customers, ranging from IC design houses to world-leading IDMs. Therefore, customer relationship management, as well as fabrication capacity and capability, were always central to TSMC’s operations, in which technological development and e-commerce have come to play an increasingly important role.

TSMC was a spin-off from ITRI, which had managed to master the technology transferred from RCA. As the global leader in foundry, TSMC has approached the technological frontiers, almost on a par with the global IC leader, Intel. Underlying this is the company’s commitment to R&D, leading to a substantial number of U.S. patents each year. In 2008, TSMC’s R&D expenditure (USD629.35 million) amounted to 6.16% of its sales. In addition, TSMC has been a member of Sematech, an international consortium of the semiconductor industry, and is currently working closely with the major members of Sematech on the 450 mm (the latest generation of technologies) project.

In the arm’s-length relationship between foundries and fabless design houses, it is essential to manage the flow of knowledge so as to facilitate a smooth and efficient transfer of new designs into production. This has been made possible by the design firm’s adherence to “design rules” laid out by the foundry; namely, restrictions on the type of designs that will be manufactured in the foundry on a specific delivery schedule. These design rules are determined by the foundry’s manufacturing capacity and capability. In light of this, foundries such as TSMC have become an essential node of the innovation network of new IC designs, which entails close interactions of knowledge and information between foundries and their customers. As a result, in 1996 TSMC initiated the concept of the “virtual fab” in order to promote virtual integration with its customers by means of business-to-business (B2B) applications, thus rendering TSMC the facilitator of its customers’ supply chain management.

Apart from regular online business transactions, TSMC’s B2B operations, under the total package called “eFoundry”, cover three major aspects: logistics, engineering, and design collaborations. TSMC’s eFoundry consists of a suite of Internet-based applications providing its customers with real-time support in wafer design, engineering, and logistics, functioning as the master tool for the concept of the virtual fab. It currently supports a few online services, including TSMC-Online, TSMC-Direct, TSMC-YES (Yield Enhancement System), TSMC-ILV (Internet Layout Viewer), and eJobView.

In terms of collaboration in logistics, TSMC-Online provides access to real-time production and logistics information updates in such areas as the status of wafer fabrication, assembly, and testing, as well as order handling and shipping. As for engineering collaboration, TSMC-Online provides a variety of engineering capabilities, including interactive views of prototyping, lot status, yield analysis, and quality reliability data. It is also empowered with design collaboration capabilities in support of customer access to important information needed during the design process. Aided by Design Service Alliance, as discussed below, TSMC-Online provides selected blocks of IP owned by third parties – these are robust design solutions that conform to TSMC’s production technologies – which are then made available to designers.

In order to facilitate design collaboration, TSMC also formed the Design Service Alliance with third parties. The emergence of system on a chip (SOC) has highlighted the importance of SIPs, and as a result IC design has come to resemble the assembly of SIPs, from both internal and external sources. Design houses also face the challenge of choosing from among a variety of library suppliers and electronic design aid (EDA) tools. TSMC previously functioned as a pure-play foundry with limited design service capacity, but with the Design Service Alliance, the company can now mobilize external resources to facilitate the design processes of its customers.

Through the Design Center Alliance, TSMC helps its customers to connect to a global network of qualified and experienced IC design centers in order to gain the necessary design expertise. Similarly, through the EDA Alliance, TSMC’s design service engineers work with EDA Alliance members in order to deliver TSMC-specific technology files and design kits that may simplify its customers’ design experience. In essence, the Design Service Alliance as a whole aims to provide TSMC’s customers with total IC design solutions to accelerate the cycle time from specification, through tape-out, to finished wafers. Both TSMC’s customers and the key testing and packaging firms can gain access to the Design Service Alliance using TSMC-Online as the platform.

To summarize, while starting out as a standalone OEM foundry, TSMC has come to resemble a provider of integrated service packages covering a wide range of value chain management activities thanks to its extensive application of e-commerce as well as capabilities. For SOC to go through the entire value chain, wafer foundries hold a unique position in verifying as well as producing silicon-proven IPs. Therefore, the technological complexity of SOC may induce foundry firms to tighten networking relationships with the other types of industrial players. For example, in advancing the concept of virtual foundry, TSMC is championing a collegial win–win–win model, instead of the win–win customer/supplier relationship that currently prevails, which in turn, according to TSMC, may entail a “pay-for-performance” business model. As a result, the industrial network in the IC industry will probably go further “internationalized”, highlighting the escalating importance of crossborder technological linkages of the IC industrial clusters around the globe.

Mediatek

Mediatek, created in 1997, is a leading fabless IC company for wireless communications and digital multimedia solutions in Taiwan and even globally, with its annual revenues reaching about USD2159 million in 2008, up from USD1198 million in 2004. The company’s R&D intensity was as high as 22.24% in 2008. Mediatek holds a unique position as a major catalyst in proliferation of variety and fast expansion in the quantity of Shanzhai2 (also known as guerilla) handsets in China. Mediatek started its operations by designing and marketing chips for CD-ROM drives and further expanded its operations to many sorts of consumer devices. Right now, the firm has a chipset inside 50% of DVD players worldwide.

In 2004 Mediatek expanded into the territory of mobile phones by making chipsets, a total solution incorporating processor, radio, and other sorts of chips together with the necessary software. It is now widely perceived that Mediatek’s solutions and business model have revolutionized the handset industry,3 at least in China. Before Mediatek’s entry, leading handset chip makers, such as Texas Instruments (TI), Broadcom, and Qualcomm worked closely with global oligopolistic brand marketers of handsets. Mediatek’s total solutions, which have shortened the lead time to market from 9 months to about three months, make it much easier for handset makers to design and produce a wide variety of mobile phones. Together with its extensive technical supports in China, Mediatek has facilitated the explosive development of Shanzhai handsets in China. It was estimated that about 150 million Shanzhai handsets were produced in 2007, with 40% of them “exported” to such countries as India, Russia, and Brazil. In spite of the notorious reputation of “bandit” phones, many of the Shanzhai handsets in China are incorporated with local innovative ingredients and/or features, based mainly on Mediatek’s total solutions.

In a sense, Mediatek’s chipsets are in line with the trend of SOC in the IC industry, but the company’s success also lies in its extensive technical support network in China. Prior to Mediatek’s entry, there were precedents, such as Wavecom, a spinoff from Ericsson and Bellwave, a Korean total solution provider, and even Infineon and TI had chipsets catering to low-cost handset makers, but none of them have gone as far as Mediatek. Not only was the timing ripe for Mediatek, but the company has built its strength on its extensive technical support network in China, proximity to customers, and serving as the local point of contact for everything relating to using its parts and chips from other vendors.

Thanks mainly to Mediatek’s integrated solutions catering to low-cost and Shanzhai handset makers, the technological barriers for designing and making handsets have been lowered, enabling Chinese Shanzhai handset makers to rapidly and frequently launch new products that fit well with the diverse needs of the lower tiers of the market, overlooked by the incumbents. Therefore, while entering at a point somewhere between the growth and maturity stages, Mediatek has helped to create a massive market space which used to be underserved or underexplored (Chen and Wen, 2010).

Mediatek’s ambition is not just providing chipset solutions for low-end handsets, instead the company has aimed at the smartphones market and even handsets for the Chinese indigenous 3G standard, TD-SCDMA (Time-Division Synchronous Code Division Multiple Access). Recently Mediatek’s solutions have been adopted by LG, a well-known Korean handset brand. Ming-Kai Tsai, the Chairman of Mediatek, always emphasizes that “low cost does not necessarily mean low technology because to achieve low cost may require integration of many functions together; hence high technology can be a means to achieve low cost.” In addition, Mediatek opts to focus on the so-called “good-enough market”, trying to differentiate the company from the leading firms’ practices of “overshooting” of functions.

HTC

Since its inception in 1997, HTC has pioneered the smartphone market through partnerships with Microsoft, Intel, TI, Qualcomm as well as some of the leading mobile operators in advanced countries, including Orange, O2, T-Mobile, Vodafone, Cingular, Verizon, Sprint, and NTT DoCoMo. The company is currently the world’s largest producer of Windows Mobile smartphones and pocket PCs. Business Week ranked HTC as the second best performing technology company in Asia in 2007 and ranked the firm 3 in its global listing in 2006.

HTC is committed to driving the growth and capabilities of smartphone technology. Since its establishment, the company has developed strong R&D capabilities and pioneered first-of-a-kind products in the market. It has invested in a strong R&D team, accounting for 25% of the total headcount. In 2008, HTC’s R&D expenditure (USD305.16 million) amounted to 6.30% of its sales. In terms of internationalization, part of HTC’s development team is based in Seattle, together with the acquisition of One & Co, a noted design firm based in San Francisco. However, unlike other Taiwan-based ICT device firms, which rely much on offshore production, HTC maintains a world-class high-volume manufacturing facility in Taiwan.

Another factor that differentiates HTC from most of its peers in Taiwan is branding. In 2006 HTC started to promote its own brand. For this, among many other things, HTC has been engaged in transforming its innovation culture and capabilities from “design to order” with efficiency to value creation based jointly on cutting-edge technologies, creativity, software intelligence,and services. Apart from its partnership with leading Western mobile operators, HTC intends to eventually become a household name alongside Apple and Nokia.

To achieve this aim, HTC was the first handset maker to launch smartphones powered by Android, the open-source operating system (OS) developed by Google. In doing so, the company has developed a new operating system based on Google’s Android OS. In addition, in collaboration with China Mobile, HTC will launch some smartphones that support China Mobile’s TD-SCDMA standard. It is even coworking with the Chinese operator to promote TD-LTE (TD Long Term Evolution; 4G). For HTC, all of these efforts amount to a strategic attempt to establish new competencies and competitive advantages in order to withstand shrinking margins in the handset industry and its Chinese rivals’ flocking in with cost advantages.

Quanta

Equipped with its well-established ODM capabilities and business model, Quanta Computer, founded in 1988, has been the largest and most specialized notebook computer producer in the world for a decade. For this, Quanta has established operation centers across Asia, America, and Europe to manufacture, configure, and service products as well as provide logistics support to deliver products and services in a competitive and efficient way in the world. It is estimated that Quanta’s worldwide market share of laptop computers had increased from 10% in 1990 to a peak of 30% in 2005, and then down to 22.5% in 2009. However, since its profit margin had fallen steadily from 12.7% in 2001 to 3.68% in 2007, Quanta is seeking diversification. To keep competitive, Quanta is looking to cloud computing as fertile ground for future development, and services as an important source of value creation.

Quanta’s journey of diversification started in 2002, when the company expanded beyond the razor-thin-margin notebook computer market and into the higher margin market segment of displays, giving birth to Quanta Display as a TFT-LCD maker. In 2005, Quanta won the right to build an ultra-low-cost machine for One Laptop per Child (OLPC), a U.S. nonprofit program launched by Nicholas Negroponte of the Media Lab at the Massachusetts Institute of Technology (MIT). This kind of laptop costs no more than USD100, which is about one fifth the price of even the cheapest notebook computers on the market. The aim of OLPC is to sell these machines to millions of students and others in the developing world. Though Quanta eventually managed to meet the target of mininotebook computers, Eee PC launched by Asustek eventually became more popular and profitable. Right now Quanta has extended its businesses into enterprise network systems, home entertainment, mobile communications, automotive electronics, and digital home markets. As a result of its efforts of diversification, 30% of Quanta’s revenue came from products other than notebook computers in 2009, but its aim was to reach a 50–50 ratio in the future.

Quanta has been recognized by Fortune Magazine as a Fortune Global 500 enterprise. Underlying this achievement as well as some others is the company’s commitment to R&D. Quanta has over 30 000 employees worldwide of which more than 3500 people are working in R&D and engineering development. In particular, the Quanta Research Institute (QRI) was inaugurated in 2005, comprising advance R&D, corporate R&D, and business unit R&D functions within the Quanta R&D Complex (QRDC), its global headquarters, near Taipei.

To ensure Quanta’s long-term prospect of retaining technological leadership, the QRI has collaborated with leading institutions around the globe in a few cutting-edge research fields, including high-performance computing algorithms, large-bandwidth mobile communications, and a more intuitive human interface. Working with the likes of MIT, the National Taiwan University, the Computing Center of Academia Sinica, and the National Center for High-Performance Computing, the QRI has tried to outreach to external sources of state-of-the-art technologies. In particular, the QRI sponsored a project conducted by MIT’s Computer Science and Artificial Intelligence Laboratory (CSAIL) to develop next-generation computing and communication platforms. In 2009, Quanta also formed an alliance with the University of California at Berkeley to explore medical technology and cloud computing.

Based on its existing ODM advantages, Quanta is trying to mobilize its resources to implement a new type of total solution strategy, called “SSDMM” (System Solution Design and Manufacturing Move). This SSDMM calls for the integration of downstream business offerings, including end product solutions in the automobile, wireless (smartphones and 3G handsets), entertainment (LCD TVs and consumer electronics products), enterprise (storage units and servers), and digital home sectors. As a result, Quanta is transforming itself from a manufacturer of notebook computers to a provider of a set of comprehensive total solutions, termed “service by integration”. Quanta intends eventually to progress further toward the direction of “service by innovation”, with an aim to create value and profits with services. Barry Lam, the Chairman of Quanta, emphasizes that the company intends to “pursue the goal of ‘me first, me only’, going beyond vertical disintegration or scale economies.”

The way forward

Without denying its significance to the GIN, there are concerns in Taiwan that the ICT industry, particularly concerning the ODM business, is subject to some bottlenecks. First, the industry is facing razor-thin profit. Second, the Taiwanese ICT industry is short of capabilities to define and create the dominant architecture design for new generations of ICT products, which in turn may lock it into the trajectory of OEM/ODM manufacturing. Third, due to its overconcentration in the ICT sector, especially its intermediate goods in terms of domestic production, Taiwan may become particularly vulnerable to the downturn of the global economy. This has proven to be the case during the recent global financial crisis, when Taiwan’s ICT industry, particularly the DRAM and LCD subsectors, was severely harmed because of the “bullwhip effect”.

To overcome the above-mentioned bottlenecks, the government has formulated a few policies to facilitate the transformation of Taiwan’s ICT industry. First, in line with the trend toward blurred boundaries between manufacturing and services, the “servitization of manufacturing” (also known as industrial services) has surged as an important thrust in the transformation for an increasing number of manufacturers. The Taiwanese government is actively promoting such a transformation in the manufacturing sector, particularly the ICT sector. An important aspect of this transformation is taking advantage of the current strengths of the Taiwanese ICT supply chain, to create new service opportunities for manufacturing, and eventually provide the global market with the offering of “one-stop-shopping services”. In fact, as discussed earlier, like some other firms, Quanta is transforming itself from a manufacturer of notebook computers to a provider of a set of comprehensive total solutions. Eventually it plans to progress further toward the direction of “service by innovation”, with an aim to create value and profits with services. Second, the government is also promoting new fields, such as cloud computing and car electronics, with an aim to facilitate diversification of the ICT industry. With particular regard to cloud computing, the MOEA has reached agreements with a couple of MNCs – Microsoft and IBM – to develop the technologies and applications needed, in cooperation with some local universities and research institutes.

Conclusions

The development of Taiwan’s ICT industry as a whole has gone beyond the paradigm of local clustering thanks to the formation of the GPN and GIN. Along with this trend, Taiwan’s computing-related industry has outreached in terms of production and more recently even R&D. As a result, in terms of domestic production and exports, the role played by Taiwan’s ICT industry in the GPN has shifted from a key producer of end products to that of important components and parts (intermediate goods). This development cannot be reduced to the argument that Taiwanese ICT end product producers have lost their competitive edges to their international competitors, instead it should be interpreted within the context of the GPN.

A hot debate on the prosperity of Taiwan’s ICT industry is about branding versus OEM/ODM manufacturing. Chu (2009) threw out this issue: “Can Taiwan’s second movers upgrade via branding (in a natural way)?” In the end, she reached the conclusion: “The evolution of the (ODM) firms’ organizational capabilities led to path dependence in further development. As the second mover builds up organizational capabilities as a subcontractor, these capabilities become the guiding and limiting factors influencing the firm’s strategic choices in further expansion” (p. 1064). Given the bottlenecks mentioned above, it is obvious that Taiwanese ICT firms need to change. However, it makes little sense for all of them to go for branding, especially given the fact that even leading countries in the ICT industry, like the U.S.A., Japan, and South Korea, each have a limited number of brands. On the other hand, a few of the Taiwanese ICT players have increasingly shown some features different from the stereotype of their image. For example, Acer’s unique Channel Business Model has been instrumental in the company’s latest success. Even Compal, an ODM vendor, has positioned itself to know the end customers better than do its counterparts of brand marketers in order to better serve the latter and get itself closer to the end market.

More importantly, Taiwanese ICT players can be regarded as an important catalyst for the introduction of brand-new generations of ICT products to the global market. Indeed, underlying Apple’s success in iPhones are various supports from a number of Taiwanese ICT firms’ efforts in R&D as well as the deployment of production and logistics networks. Therefore, it can be argued that, from the perspective of the ICT industry, Taiwan’s national innovation system is closely linked with the global innovation system. Such cases are not limited to existing ICT subsectors and/or technologies. With its current strengths, Taiwan’s ICT industry is also collaborating with leading foreign players in emerging technologies and fields. For example, Microsoft has joined force with Taiwan to conduct R&D in cloud computing and new related generations of devices, as a result of which Taiwan may participate in the development of the cloud computing servers, new chips, software and applications that will be required. Likewise, Dell has also expanded its R&D center in Taiwan after having been given R&D mandates for cloud computing.

The 2011 Report on R&D in ICT in the European Union (EU)4 indicated a widening gap between the EU and the U.S.A. in ICT R&D investments, a disparity of nearly EUR38 billion, as of 2008. In fact, the gap may be wider than statistics suggest because U.S. firms seem to have done a better job in leveraging R&D and design capabilities, as well as manufacturing, both in Taiwan and elsewhere in Asia (including India). In other words, the U.S.–EU ICT R&D gap can be better understood in a multilateral rather than bilateral context. Indeed, the globalization of technology has reached a stage at which Taiwan together with some developing countries in East Asia have become a source of R&D and innovation, not just a technology recipient and late-adopter as before. As a result of this, Taiwan and the peer players in the Asia-Pacific may serve as partners of collective innovation, with their involvement at the early stage of the product life cycle.

1.Fabless manufacturing relates to the design and sale of hardware and semiconductor chips while outsourcing fabrication (fab) to a specialist manufacturer – a so-called “semiconductor foundry”.

2.Some refer to Shanzhai handsets as copycats or “bandit” phones, but this is not necessarily true.

3.Before Shanzhai handsets and Mediatek’s total solutions, the global giants of mobile phones and such chip makers as TI, Broadcom, and Qualcomm not only controlled the technology of the phone chip, the heart of a handset, but also owned the know-how of supporting software.

4.This report was published by the Institute for Perspective Technological Studies, a joint research center under the aegis of the European Commission.