CHAPTER 6

The Payments Niche

The means and methods by which people pay for goods and services has continually evolved throughout history—from commodity‐bartering economies to the proliferation of modern fiat money to checks to credit and debit cards. Today, this evolution continues with mobile apps and online platforms increasingly being used and streamlining payments processes to create a more efficient economy. In this chapter, we take a closer look at emerging payment trends and FinTech innovations, including retailer‐specific mobile apps that allow customers to order and pay from their mobile devices, mobile wallets that hold card and account information to allow mobile payments to be made virtually anywhere, solutions that allow merchants to accept these mobile payments, and mobile apps offering direct peer‐to‐peer payments. Additionally, we take a closer look at blockchain technology, the FinTech innovation behind emerging digital currencies, and identify potential areas where blockchain could impact financial and payment services. While this chapter does not cover all of the emerging FinTech payments solutions, it does address the core competencies of the space and takes into account some of the main players and emerging trends in the industry.

TRENDS TO WATCH

Movement to a Cashless Society

In the United States, according to a recent article, cash remains king as it was used in 32 percent of all transactions, the highest of any payment method.1 Cash was particularly strong in small transactions (payments under $10) where it was used 66 percent of the time. However, we seem to be moving toward a more cashless system as cash's lead over other payment methods has declined from 40 percent in 2012 as usage of both debit and credit cards continues to inch higher. According to the 2016 UPS Pulse of the Online Shopper survey,2 consumers for the first time bought more of their purchases on the web than in stores (51% in 2016 compared to 48% in 2015 and 47% in 2014) with Millennials accounting for the bulk of those online shoppers (54%). In addition, cryptocurrencies such as bitcoin (discussed at length later in this chapter) and mobile payment options like Apple Pay are working hard to become more accepted. Globally, mobile payments are becoming more common. A MasterCard survey found that more than 70 percent of respondents were ready to use their smartphone to make payments in the Middle East and Africa compared to only 38 percent in Europe.3

As a cashless society continues to emerge, banks are increasingly facing competition from upstart FinTech companies that are innovating in the payments niche. While many banks were able to partner with Visa and MasterCard as society transitioned from cash to cards, it remains to be seen whether banks will remain squarely in the payments loop as payments continue to evolve to digital (online and mobile).

To better understand trends in the payments niche, we provide case studies of innovative FinTech companies (Square, Gyft, Check, and Stripe) in the payments niche. The payment innovations discussed are leveraging mobile connectivity to make payments easier for consumers, even for small transactions. Many of the current innovations in payment solutions are not disrupting the existing process, but modifying and refining the existing front‐end process (i.e., interaction between customer and merchant).

FinTech Payment Company Case Studies

Square

Square is a mobile payment solution provider founded in 2009 by Twitter CEO Jack Dorsey and Jim McKelvey. Square has placed itself at the forefront of the point‐of‐sale (POS) segment of the mobile payments industry by offering software and hardware solutions for merchants to accept credit and debit card transactions on their iOS or Android devices. Square's first and flagship product, the Square Reader, plugs into a merchant's mobile device and houses a card reader through which consumers swipe their cards.

Square's other main payments hardware device, Square Stand, was introduced in 2013 and offers a more complete POS system by providing a larger card reader and rotatable mount for various models of iPads to sit on. This allows consumers to tip and sign for purchases through Square Register, the payments software behind the Reader and Stand. Square also offers a peer‐to‐peer money‐transfer service, small business financing service, and payroll support service. Square's fee‐based business model is primarily predicated on a flat fee of 2.75 percent per credit card swipe. A Square Stand can be purchased for $99 while a Square Reader is offered for free on Square.com (however, a contactless Square Reader does cost $49). Square is free of monthly fees and setup costs, and funds deducted off the service fees are deposited into the merchant's bank account within one‐to‐two days. Attracted by this clear pricing and fast deposit model, small businesses and merchants such as food trucks, independent retailers, and salons make up Square's largest customer base.

Square IPO'd at $9 per share in November 2015, in what many considered to be the most high‐profile FinTech IPO of 2015.4 The stock has generally underperformed market expectations since its IPO, as its price had dropped to $8.75 by January 2016.5 Although the stock price has recovered somewhat on the heels of the company's announcement that it is further expanding its operations into European markets (trading at $10.22 as of 8/3/16), it is still being outpaced by broader markets thus far in 2016. The stagnation of Square's stock price reflects a number of underlying issues but two significant obstacles facing the company is that it is not yet profitable and it lost a significant partner in October 2016 when its relationship with Starbucks ended.6 When the partnership was announced in 2013, it was seen as a huge coup for the payments startup to land a corporate whale like Starbucks. With the success of the Starbucks app, the coffee giant and Square parted ways, leaving Square to primarily rely on small businesses in efforts to turn a profit.

Despite these issues, Square has continued to grow (as measured by the number of merchants and processing volume) and, as previously mentioned, is gearing up to further expand in European markets. Going forward, it will be interesting to see whether Square will mature into a leader in the payments industry or become another example of a FinTech company with a revolutionary idea that did not have the business model to generate profits sufficient to support it.

Gyft

Gyft is a mobile gift card app that allows customers to buy, store, send, and redeem gift cards conveniently from their mobile device. Gyft's mobile applications allow users to upload and check mobile gift card balances, earn rewards points for using a gift card, purchase with bitcoin or PayPal, and purchase and send gift cards electronically to friends or family.

Table 6.1 provides an overview of Gyft since its founding as well as a timeline related to key milestones achieved.7

TABLE 6.1 Gyft's Significant Corporate Events

| Timeline | Significant Corporate Events |

| 2012 |

Company founded in January and originally focused on developing an iPhone app that allowed users to buy, give, and share gift cards Received first round of seed funding of $1.3M from South African investor in June Announced integration with Apple's Passbook, including over 200 different retail gift cards Received second round of seed funding of $1.3M in September following being a finalist at TechCrunch Disrupt SF |

| 2013 |

Expanded application to web and Android Reported to have around 200,000‐plus gift cards with $10M uploaded to platform and offering over 300 retail cards Received $5M of Series A funding (September) Introduced features like re‐gifting, bitcoin support, and a registry option |

| 2014 |

Tried to expand internationally and introduced a card‐swapping option Announced its new mobile gift card solution (Gyft Cloud) for small‐to‐midsized businesses Partnered with Clover, a First Data subsidiary company that offers an innovative all‐in‐one POS payment and business solution for small‐to‐midsized businesses |

| July 30, 2014 |

First Data, a global leader in payment technology and solutions, announces deal to acquire Gyft Exact details of the transaction have not been disclosed |

Gyft Key Takeaways

- When developing a FinTech innovation, have a clear, validated idea that adds value to both end‐user and partner/provider (in this case retailers).

- Targeted a large sector of the payments segment, gift card industry that totaled approximately $100 billion that could be disrupted technologically.

- Value to consumer—Offered a solution to consumers who often forgot or lost cards with dollars going unused.

- Value to retailer—Offered a solution to retailers who often have unused legacy gift cards and no idea where the cards reside, which is a problem because a 2010 law prevented retailers from booking gift card sales as revenue until the cards are redeemed (value to retailer).

- Value to both—Took concept of managing mobile payments for gift cards for individual companies and developed a multichannel space for consumers and businesses.

- Retailers can target messaging to consumers regarding incentives or promotions and also send reminders to use a forgotten/unused card.

- In a competitive FinTech niche (like payments), attempt to differentiate your strategy from competitors.

- Gyft launched in a very competitive space in 2010 and there were a number of other competitors attempting to disrupt the gift card industry—most notably a few who were attempting to promote social gifting experiences.

- Gyft differentiated itself from those competitors by working with existing retailers and users, and focused on digitizing the existing gift card network/experience on mobile rather than significantly changing user behavior.

- Focus on mobile and digital appeared successful in the FinTech payments niche.

- Gyft was able to grow both consumer and retailer adoption related to digitizing offline gift cards to mobile.

- Will this avenue work in other areas of payments or was the gift card industry unique?

- Disruptive FinTech startups continue to value partnerships and this may lead to acquisitions by partners.

- Gyft joins the list of recent FinTech startups (Check, Simple, Banno, etc.) who were ultimately acquired by those existing companies that they initially sought to disrupt.

- Given the significant amount of capital and resources required to grow the user base of FinTech startups where heavily regulated markets and institutions are common, growing the user/activity base to a level to achieve enough scale to attract more capital or profits to propel future growth may be more difficult than in other sectors.

- Additionally, the importance of partnership in the FinTech sector seems to lend itself to transactions similar to Gyft, where a larger, more established partner acquires the startup as it gains traction.

- Consider the following quote from Gyft's Founder, Vinny Lingham:

We have been building this relationship for a while…. We started the company with a mission to digitize and transform the plastic gift card space…. But as we were going through the process it was a lot more complicated than it seemed. Onboarding merchants was a real grind…. We don't see this as an exit. We see this as a continuation of what we're already doing, but with a lot more resources.8

Check

Check offers a mobile application that provides an efficient and secure way for consumers to access bills and money from their smartphones. The mobile application has more than 10 million users and allows users to monitor bank accounts and credit cards, send reminders regarding bill and low funds, and automatically pay bills.

Check provides an example of the emerging trends toward a cashless and checkless world as it bridged the intersection between personal finance and a disruptive bill pay capability that is basically free for the consumer. Table 6.2 provides an overview of Check since its founding, as well as a timeline related to key milestones achieved by Check.9

TABLE 6.2 Check's Significant Corporate Events

| Timeline | Significant Corporate Events |

| 2007 | Initially founded as a web company named Pageonce to solve a problem that one of the founders found extremely frustrating: remembering usernames and passwords to online accounts |

| 2008 |

Launched “Internet assistant” to help users manage online lives after a private beta period where it collected 20,000 users and built support for more than 60,000 account types. As users began to use product, Check discovered that 50% of users had linked financial accounts. Therefore, they began to focus more on being an aggregator of personal financial data and putting all the information onto one page. As user growth slowed, Check pivoted from focusing on building web platform to focusing on mobile application; Pageonce Personal Assistant Mobile Application was one of original 100 applications available when the iPhone App Store launched Angel round ($1.5 million invested in January 2008) |

| 2009 |

Mobile application hit 1 million users and was in the top 20 in iPhone store for 2009 Revenue model was focused on advertising in free applications and charging for a premium version Series A round ($6.5 million invested in December) |

| 2011 |

Sophistication of application increased to where application could track bank accounts, credit cards, investment and travel plans, monitor bills and manage money; raised capital to become the “wallet of the future”; launched mobile bill pay feature Unknown ($15 million invested in May 2011) |

| 2013 |

Changed name from Pageonce to Check; 8 million users and payments volume of approximately $1.5 million per month Started allowing users to set up mobile person‐to‐person payments Series C round ($24 million in September 2013) |

| 2014 |

10+ million users and $500 million in payments processed per year Check sold to Intuit for $360 million (total funding since inception $47 million) |

Check Key Takeaways

- It is important to maintain flexibility and openness to pivot if needed.

- Check pivoted from desktop “Internet assistant” application to mobile personal financial application and then, more specifically, to mobile payments.

- The pivot grew out of slowing user growth on desktop application, as well as recognition of potential growth in mobile and ultimately mobile payments.

- Even had an unsuccessful attempt at a Facebook application before successfully opening mobile application in iPhone store.

- Check pivoted from desktop “Internet assistant” application to mobile personal financial application and then, more specifically, to mobile payments.

- When developing a FinTech strategy, focus on consumer trends/desires and your core beliefs regarding where the market is headed.

- Check's pivot was consistent with their belief that mobile adoption would increase for financial services.

- This turned out to be consistent with consumer trends and shift from offline to online and mobile.

- For perspective, mobile payments currently represent a fraction of in‐store purchases but the percentage rose 103 percent in the United States between 2010 and 2013.10

- U.S. Consumers were expected to pay more than 14.7 million bills in 2013 with online and mobile payments accounting for more than half.11

- Check's pivot was consistent with their belief that mobile adoption would increase for financial services.

- Check was another successful exit for FinTech venture capital investors and demonstrates the potential for value creation and enhanced returns from investments in FinTech startups.

- Approximately $47 million invested in Check starting with Angel round in 2008. Check ultimately sold for $360 million in 2014, which implies the following:

- Internal rate of return: 88%

- Cash‐on‐cash: 7.7×

- Return on investment: 666%

- Significantly higher than 11.5% median IRR for 2009 Vintage U.S. VC Funds (with asset size between $250 and $500 million) as reported by PitchBook.

- Approximately $47 million invested in Check starting with Angel round in 2008. Check ultimately sold for $360 million in 2014, which implies the following:

Stripe

Stripe attempts to improve Internet commerce by making it easier to process transactions and manage an online business. The company provides fraud prevention and the technical banking infrastructure required to operate online payment systems accounts (Table 6.3).

First, it's really simple for a business to get started using Stripe, and second, it's easy for developers to customize Stripe's technology for their own needs—which is super‐important because not all online businesses have the same needs.

—Business Insider Research Analyst John Heggestuen12

TABLE 6.3 Stripe's Significant Corporate Events

| Timeline | Significant Corporate Events |

| 2010–2011 |

Two seed rounds, one undisclosed and another at $2M (Y Combinator alum) Stripe launched in 2011 Software allows companies to take online payments securely and is noted for being relatively easy to use and customizable |

| 2012 |

Raised $18M in a Series A in February (reported $100M valuation) and $20M in a Series B in July (reported $500M valuation) Acquired chat and task‐management application kickoff |

| 2014 |

Raised $80M in January (reported $1.75B valuation) and $70M in December (reported $3.5B valuation) Announced support for bitcoin transactions |

| 2015 |

Raised $90M in a Series C (reported $5BN valuation) in July Announced Visa partnership to help expand further internationally Unveiled Stripe Relay, tools for retailers to help them build native buying experiences within other apps like Twitter; intended to improve the buying experience by not requiring users to jump through multiple websites |

Stripe Key Takeaways

- Despite larger and mature incumbents in the payments space, niches still exist to exploit.

- Payments is an industry that has existed in some form for thousands of years, but evolving customer expectations and preferences (transitioning to more mobile and online commerce) continue to create opportunities for savvy companies and entrepreneurs.

- Focus on the headaches when considering FinTech innovations.

- Stripe's Relay product clearly targets the elimination of certain headaches that customers and retailers have with trying to sell items online.

- For example, Stripe's “buy” buttons reduce headaches experienced by both retailers (who advertise products on social media) and consumers (who have to click through to multiple sites to buy).

- Stripe's Relay product clearly targets the elimination of certain headaches that customers and retailers have with trying to sell items online.

- When developing an innovation in certain FinTech niches, ease of use and ability to customize may require flexibility and fading into the background.

- Building “buy” buttons that work in other apps/sites and allowing companies to customize their payment options are examples of ways Stripe competes by allowing the user (i.e., retailer) to have tremendous flexibility.

- Again, FinTech partnerships prove to be vital.

- Stripe has partnered with a number of companies, including traditional financial services companies (such as AmEx, Visa), as well as nonfinancials (such as developing “buy” buttons for Pinterest, Facebook, and Twitter).

Retailer‐Specific Mobile Payment Apps and Loyalty Programs

One potential result of a more cashless world is banks losing greater control over the customer experience. As banks increasingly fight to remain relevant in payments, banks may begin partnering with merchants to drive usage of merchant‐specific cards and other solutions to gain their share of the digital wallet. To better understand merchant‐specific wallets, loyalty programs, and emerging trends in this area, we discuss two of the more prominent examples—the offerings of Starbucks and Walmart.

The Starbucks App

The Starbucks app, available on iPhone and Android operating systems, has emerged as one of the most functional and well‐regarded mobile payments systems in the retail industry. This status has been achieved through the app's consumer‐friendly interface, as well as the capability of each Starbucks location to efficiently process in‐store orders and mobile orders from the app. When setting up the mobile app, customers link their debit or credit card to the app and add funds to create a balance in the app. Upon arrival at the store, customers who have ordered their coffee via the app are automatically given a unique barcode through their device to scan at the register when they pick up their order. With the scan, the funds are transferred out of the app and to the store, rendering the transaction complete. The app also links any purchases made to the customer's loyalty rewards account, in which points can be accumulated and put toward free refills, drinks, and sandwiches.

Much of the success and widespread adoption of the Starbucks app can be attributed to the efficient infrastructure of Starbucks' locations that allows baristas to fill mobile orders quickly and consistently without sacrificing a quality in‐store experience for the traditional customer. The app served as a key driver of a 9 percent increase in sales for the company in fiscal 2015 in its Americas division, with more than 1 million users leveraging the app in December 2015 alone.13 Perhaps the most impressive metric stemming from the app lies in the fact that 10 percent of all orders come from the app in Starbucks' most high‐volume locations.14 As one of the most well‐established and user‐friendly mobile payment apps in the retail industry, the Starbucks app should continue to turn rising levels of mobile usage among consumers into tangible growth for its company.

Walmart Pay

As one of the bellwethers of the retail industry, Walmart's move into the mobile payments space should come as no surprise. However, despite its status as a retail juggernaut worldwide, Walmart's expansion into mobile payments came somewhat late when compared to other retail leaders that have adopted Apple Pay or developed their own mobile payment systems.

In June 2016, Walmart rolled out “Walmart Pay” in all of its stores, giving its customers the ability to pay for items at checkout by simply taking a picture of a barcode with their mobile device. Walmart Pay is available on any phone that can download the Walmart app and is only accessible through the Walmart app. It entails a fairly simple setup process. Users enter credit or debit card information into the app to begin the process and from there may begin to make purchases. At checkout, the user indicates to the cashier or self‐checkout kiosk that he or she would like to use Walmart Pay. A QR code (barcode) is then generated at the point of sale terminal and the user takes a picture of this barcode on a code‐reading camera accessed through the app. The user then confirms his purchase through the app, the transaction is completed, and a receipt is sent to the user via email.

The process of actually using the app to pay for purchases has received mixed reviews from consumers, as some find it to be cumbersome and less streamlined than simply paying with a card. Nonetheless, Walmart Pay fills a need for many Walmart customers who either don't own a completely payment capable smartphone or would be more inclined to share payment information with Walmart than Apple or Google.

DIGITAL CURRENCIES AND BLOCKCHAIN TECHNOLOGY

Blockchain originated as the underlying technology that powered bitcoin, the most prolific worldwide cryptocurrency system. While bitcoin's future remains uncertain and difficult to predict, it is possible that blockchain technology becomes the most valuable contribution to emerge from bitcoin. The use of blockchain allows bitcoin users to exchange the currency through a decentralized system that lends itself to digital integrity and previously unseen levels of openness. Despite bitcoin's perhaps undeserved reputation as the chief facilitator of the online black market as a result of being the currency used by illegal online bazaar Silk Road, blockchain has emerged as a legitimate tech solution for financial institutions that could potentially change the entire landscape of the industry.15 Banks, insurers, and other traditional incumbents have begun exploring the possibilities of the use of blockchain as it pertains to making their processes faster and more efficient. Essentially, traditional incumbents are trying to test the ability of the blockchain and a distributed ledger to enhance efficiency in a variety of processes.

To sum, blockchain technology is viewed by many as the most applicable component of bitcoin to the traditional financial system and has created a view among traditional players that while bitcoin has been a revolutionary cultural concept and has some application to the system, the real value of bitcoin lies in its proliferation of blockchain as a feasible tech solution that could disrupt and improve the financial ecosystem.

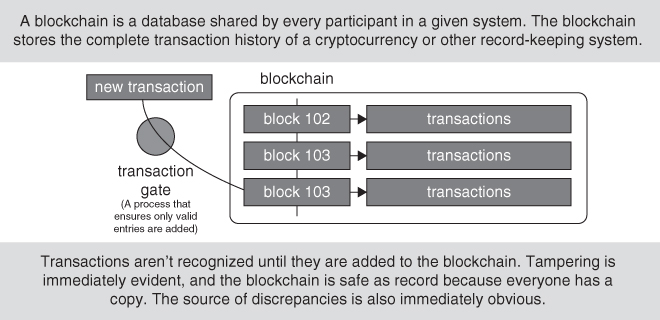

What Is Blockchain?

Blockchain is a digital, distributed transaction ledger that continuously updates its extensive list of data records by holding data in chronological blocks and adding these blocks to an existing chain of blocks with the anonymous approval of the other members of the chain through timestamping and corresponding information. Once entered into a blockchain, information can never be altered or erased, ensuring a transparent and accurate record of transactions and information available to many. Given the fact that every node (computer) in the system has a copy of the blockchain, users can quickly detect any discrepancy that may be a sign of potential fraud or hacking attempts. Figure 6.1 presents a visual picture of how blockchain works.

FIGURE 6.1 How Blockchain Works

Source: ZD Net | Used with permission of ZDNET.com. Copyright © 2017. All rights reserved

The key characteristics of blockchain are listed here.

- Reliability. Given that blockchain operates through a wide circle of participants without a single centralized location, there is no one point of failure. This allows the system to continuously run without fear of a shutdown or interruption.

- Transparency. All transactions are visible to all members of the blockchain, increasing trust and auditability.

- Immutability. It is more difficult to make changes to the blockchain without detection than traditional payment systems, increasing confidence in transactions.

- Irrevocability. The permanent and fixed nature of the blockchain makes it possible for transactions to become binding and final.

Consistent with the potential applications and excitement around blockchain technology, venture capital investment into companies providing blockchain services has soared from only $3 million in 2011 to nearly $475 million in 2015. In total, investors have poured nearly a billion dollars into over 120 startups operating on every continent except Antarctica. Before 2015, investors focused mainly on the digital payments through the bitcoin side of blockchain investment, but have recently shifted toward a preference for startups that provide blockchain software and infrastructure.

In terms of investment by functionality, funders have segmented the industry into three distinct groups: applications and solutions, middleware, and infrastructure. The segment that has received the most funding from investors has been applications and solutions. These companies provide and operate bitcoin wallets as alternative payment solutions utilizing blockchain and include startups such as ribbit.me, Circle, and Shocard.

Similar to the growing excitement for FinTech applications in the payments area that we discussed earlier in this chapter, there has also been increased interest in startups that provide blockchain services to companies, whether it be software for companies to build their own blockchain applications or the blockchain infrastructure itself. Providers of software to build blockchain‐capable applications have become known as middleware companies. Some of the most prominent middleware startups are Blockcypher and Factom. The infrastructure segment includes companies that provide a blockchain infrastructure to build secure platforms for their clients, such as successful startup Ripple.

Table 6.4 provides an overview of the largest recent venture fundings in both blockchain and payments companies.

TABLE 6.4 Largest Payments, Bitcoin, and Blockchain Funding in 2015–2016

Source: Mercer Capital Quarterly FinTech Newsletters from Q1 2015 through Q2 2016

| Period | Company | Amount ($M) | Company Description |

| Q3 2015 | AvidXchange | $225 | Payment solutions (Automated Billpay & A/P) |

| Q1 2015 | 21 Inc. | $116 | Stealth bitcoin startup |

| Q1 2015 | Zuora | $115 | Cloud‐based subscription billing services |

| Q1 2015 | Coinbase | $75 | Cryptocurrency wallet and exchange |

| Q2 2015 | Yapstone | $60 | Online electronic payments processing platform for online marketplaces |

| Q2 2015 | ZenPayroll | $60 | Cloud‐based comprehensive payroll service making processing payroll for business simple |

| Q1 2015 | Raise Marketplace | $56 | Marketplace for buying and selling giftcards |

| Q1 2015 | Bill.com | $50 | Small and Medium Business invoicing and payments platform |

| Q2 2015 | Circle | $50 | Bitcoin‐based digital service to store, send, and receive money |

| Q3 2015 | Shift Payments | $50 | Debit card with universal currency access |

| Q3 2015 | Payoneer | $50 | International money transfers |

| Q2 2015 | WePay | $40 | Provides marketplaces, crowdfunding sites, and other platform businesses a payments platform |

| Q2 2016 | Remitly | $39 | International payment service allowing customers to make international transfers from United States |

| Q2 2016 | Simplee | $38 | Software platform for health‐care payments and billing |

| Q1 2015 | Ripple Labs | $30 | Open source payment network |

Potential Applications of Blockchain Moving Forward

Payment Solutions

The payment solutions industry is ripe for potential applications of blockchain to increase efficiency, transparency, and accuracy. Blockchain could facilitate low‐cost micropayments processed without fees, which may open up new business models such as a newspaper website charging by articles read rather than a monthly subscription. Electronic signature and digital transaction management could remove barriers in the car buying and leasing processes by integrating proof of concept with blockchain to record contracts. Furthermore, the settlement process in travel, retail, and hospitality loyalty programs could be vastly improved, as blockchain could handle a more organized and efficient treatment of loyalty points and update these points in real time. BTC Smart Meters, a South African utilities company, is already integrating blockchain into the way its customers pay for utilities by accepting bitcoin as a form of digital payment supported by blockchain capabilities.

Financial Services

Beyond payments applications, blockchain technology has a number of far‐reaching and potentially disruptive applications for financial institutions if adopted. Not only are massive public blockchain companies being discussed as possibilities for transaction support, but permissioned (private) blockchain companies could give institutions the capability to run a blockchain within only their organization. Blockchain could also eliminate the need for central authorities to certify ownership and clear transactions, as the information would be widely available on a massive securities exchange blockchain. Nearly instantaneous settlement of securities transactions would be made possible by blockchain and the traditional t + 3 settlement window could be reduced to t + “whatever regulatory bodies deem acceptable,” which would lower the cost to trade as less capital will be tied up in the settlement process. NASDAQ is already testing the use of blockchain in its NASDAQ Private Market, a marketplace for pre‐IPO trading of private companies. NASDAQ Linq, as the blockchain product has been named, has already drawn praise for the way it has increased efficiency and speed in the clearance and settlement of trades. With the introduction of Linq, NASDAQ is on the leading of edge of what could become a widespread introduction of blockchain into the financial services industry.16

Blockchain technology also has a number of horizontal applications that could impact all industries, not just financial services. While not all‐inclusive, a few primary potential applications of blockchain in other industries include the following:

- Smart Contracts. Blockchain will be able to create agreements represented as software that can automatically trigger an action under certain conditions, such as when a payment is made or missed.

- Automated Auditing. Blockchain can allow for automated third‐party verification by a distributed network to ensure that transactions are accurate and complete.

- Cybersecurity. The nature of blockchain enables the immediate detection of data manipulation and verifies the integrity of IT systems.

There are broad potential future applications of blockchain, including:

- Digital asset management

- eVoting

- Smart contracts and self‐executing wills

- Digital notary

- Registration and title of goods beyond cars and homes

- Money tracking for government tax‐funded projects

- Secure cloud storage across multiple platforms

Government Regulation of Blockchain

Given that blockchain technology is still rapidly evolving, governments worldwide have been left in somewhat of a holding pattern as it pertains to the regulation of blockchain companies. Perhaps the biggest obstacle facing governmental agencies and other regulatory bodies is that given the global nature of the technology and the sheer volume of regulation it could be subject to, the capabilities and potential uses of blockchain could be greatly constrained if it were to come under excess regulation by a vast cross‐section of international agencies. Still, conversations about regulation among governments and regulatory bodies are becoming more prevalent as blockchain penetrates the financial industry, although the outcomes of these conversations are often inconclusive.

The European Securities and Market Authority (ESMA) released a paper in June 2016 stating that it had still not established a concrete opinion on the regulation of blockchains or their potential to disrupt the financial industry.17 Their position argues that it is still too early to tell whether governments will be able to regulate blockchain in an efficient way that has minimal effect on the use of the technology. The ESMA does concede that blockchain could boost efficiency, reduce intermediation, and foster transparency in securities transactions, but states that scaling, international governance, and security issues still make the future of blockchain too uncertain to have a regulatory or legal opinion.

Regulation of blockchain in the United States is in an even more juvenile stage as the government is just beginning to recognize it as a legitimate disruptor. Members of Congress recently met with representatives from the industry to discuss its potential and gain a better understanding of blockchain.18 This meeting was meant to serve as a briefing for members of Congress and showed that the United States is becoming more proactive in taking steps toward regulating blockchain. However, there is still a great deal of debate as to whether this regulation should take place at the state or federal level, as some states have taken the lead in regulation while others are waiting to see if the federal government will handle the arduous process. At The Blockchain and Distributed Ledger Technology Conference in April 2016, a panel made up of FDIC regulators and state securities commission representatives reasoned that regulation would remain at the state level, as most of the companies interested in blockchain technology are small, heavily localized companies.19 Thus, while governments and regulatory agencies both domestic and abroad are making some headway in figuring out a strategy to regulate blockchains, concrete pieces of legislation seriously affecting the industry are still a long ways off.

Digital Currency Case Study

In order to provide perspective on FinTech companies emerging in the digital currency space, let's take a look at Coinbase, a mobile bitcoin wallet provider that allows customers to buy, store, and accept bitcoin currency from the web or their mobile device.

Coinbase

Coinbase's mobile application allows users to store bitcoins in customer's wallets or vaults for zero fees, purchase/sell bitcoins, and check and manage accounts. For better perspective on Coinbase's operations, consider the following quotes related to Coinbase:

Coinbase, headquartered in San Francisco, has become one of the most prominent businesses, allowing people to buy and store bitcoins and developing deals with merchants to help them carry out bitcoin transactions.

—Time20

Finally, bitcoin is being recognized as a great vehicle for banking. It is clear that not only can bitcoin be used for remittances and stored value, but also for banking efficiency and credit‐card transactions.

—Tim Draper of DFJ21

A lot of these companies, they want to invest in category leaders, and we made a convincing case that that was us.

—Brian Armstrong, CEO of Coinbase22

Table 6.5 provides an overview of Coinbase since its founding as well as a timeline related to key milestones achieved by the company.23

TABLE 6.5 Coinbase's Significant Corporate Events

| Timeline | Significant Corporate Events |

| 2012 |

June: company founded by Brian Armstrong and Fred Eshram September: received $600,000 in seed funding from Y Combinator, Funders Club, and other individual investors |

| 2013 |

May: raised Series A funding of $6.1 million from Ribbit Capital, Union Square Ventures, Red Swan Ventures, among other investors December: raised Series B funding of $25 million from Andreessen Horowitz, Union Square Ventures, QueensBridge Venture Partners, Ribbit Capital, and other individual investors |

| 2014 |

May: acquired Kippt, a collaborative bookmarking system for professional networks that allows users to collect and share content August: acquired Blockr.io, a popular explorer for the blockchain, or the distributed public ledger that keeps track of all bitcoin transactions September: Coinbase expands into Europe |

| 2015 |

January: raised Series C funding of $75 million from New York Stock Exchange, Valor Capital Group, DFJ, BBVA Ventures, and other investors January: Coinbase becomes first regulated bitcoin exchange in the United States |

Coinbase Key Takeaways

- Bitcoin and blockchain have implications beyond payment processing.

- Bitcoin is more than just a new way to make purchases. It is a protocol for exchanging value over the Internet without an intermediary.

- Anywhere a transaction between two parties has traditionally required third‐party validation, bitcoin or blockchain may be applicable, including the execution of contracts, the transfer of property, and identity management.

- Wall Street is beginning to take bitcoin seriously.

- NYSE's entrance into the bitcoin space through its investment in Coinbase is a signal that more moderate consumers and investors may be warming to the idea of a decentralized currency.

- With further adoption, businesses and individuals are seeing the opportunities for increased ease and greater accessibility within international financial markets.

- The cost of transacting, through avoiding typical banking channels and other payment processing middlemen, is significantly lower.

- Focus on mobile and digital appears successful in this segment of the payments industry.

- Coinbase intends to use its new capital to grow its employee base while focusing on improving its mobile product as it eyes entry into developing markets.

- Mobile use may be even more critical in emerging markets, especially where computer access is limited.

CONCLUSION

With society continuing to move toward a more cashless system, banks will increasingly face competition from upstart FinTech companies such as the companies profiled in this chapter. Additionally, banks will increasingly have customers who use retailer‐specific applications and loyalty programs, which may ultimately threaten many banks' present role within the payments loop. As these trends continue to emerge, banks need to determine how they can best partner and innovate in order to stay relevant and maintain revenue from facilitating payments.

In addition to the continued transition to a more cashless society and the emergence of retailer‐specific apps, blockchain technology could have a significant impact the financial services industry. Banks, exchanges, and other intermediaries are beginning to explore various uses of blockchain to improve speed, efficiency, and transparency in an increasingly complex and dense financial environment. While the use of blockchain is starting to proliferate across the financial landscape, some looming questions in the short and long term remain that will determine whether blockchain truly does restructure the entire system or become an afterthought fondly looked back upon as a peculiar fad 20 years in the future.

The most immediate crux regarding the adoption of blockchain by financial institutions is the question of whether to acquire software that enables the incumbents to build their own blockchain in house, or outsource this task to a startup with expertise and create a strategic partnership moving forward. Some institutions are already taking the lead in answering this question, the most notable being the partnership between digital distributed ledger provider R3 and over 40 of the world's leading financial institutions, including BNP Paribas, Barclays, Goldman Sachs, Credit Suisse, JP Morgan, UBS, and Wells Fargo, in what has become known as the R3 Consortium.24 These partnerships have edged the financial landscape closer to total global interconnectivity between institutions, exchanges, brokers, custodial entities, and all other parties in a transaction. This will greatly reduce intermediation in the financial landscape and cut down on the cost of doing business for providers of financial services. On the other hand, some institutions are attempting to build their own blockchain system in‐house, such as NASDAQ's Linq. In the short term, this question of whether to partner with providers of blockchain infrastructure or attempt to design a blockchain infrastructure looms the largest over financial institutions just beginning to dip their toes into the deep pool of blockchain technology.

The most pressing long‐term issue for blockchain adoption is the treatment of the technology by governments and regulatory bodies, which at present is unclear. As mentioned earlier, the global nature of blockchain could create an environment of undue regulatory restraint on the capabilities of the technology, as legislation and regulation could close in on blockchain from multiple governments and regulatory agencies spanning the globe with little coordination between the agencies. Despite the potential for this adverse environment, governments and regulatory agencies appear to be behind the curve in regard to blockchain, although it could improve their operations through innovations such as eVoting and improved recordkeeping. Most governing bodies are still grappling with key questions such as what exactly is blockchain and should it be regulated at a federal or local level. As officials and regulators work through these initial queries, blockchain will continue to evolve, leading to more headaches for those attempting to dictate what companies can and cannot do with blockchain and, as a result, to an even longer period of time before widespread legislation is seen in regard to the technology.

In closing, with large institutions rapidly adopting blockchain technology and regulatory bodies scratching their heads and dragging their feet, an environment ripe for innovation and change within the financial landscape has been created. Blockchain startups and financial institutions have been able to get out in front of legislation and basically operate with limited oversight as they attempt to increase speed, efficiency, and transparency within the financial ecosystem. While it is still far too early to make an observation on any widespread effect of blockchain on the financial landscape, the recognition and early adoption by institutions of blockchain as a legitimate technological solution coupled with an evolving regulatory environment has created the potential for blockchain to act as a highly disruptive technology that could enact seismic change in the entire financial ecosystem.