In this chapter we introduce linear regression models for the purpose of prediction. We discuss the differences between fitting and using regression models for the purpose of inference (as in classical statistics) and for prediction. A predictive goal calls for evaluating model performance on a validation set and for using predictive metrics. We then raise the challenges of using many predictors and describe variable selection algorithms that are often implemented in linear regression procedures.

The most popular model for making predictions is the multiple linear regression model encountered in most introductory statistics classes and textbooks. This model is used to fit a linear relationship between a quantitative dependent variable Y (also called the outcome or response variable) and a set of predictors X1, X2, ...,Xp (also referred to as independent variables, input variables, regressors, or covariates). The assumption is that in the population of interest, the following relationship holds:

where β0, ... , βp are coefficients and ε is the noise or unexplained part. The data, which are a sample from this population, are then used to estimate the coefficients and the variability of the noise.

The two popular objectives behind fitting a model that relates a quantitative outcome with predictors are for understanding the relationship between these factors and for predicting the outcomes of new cases. The classical statistical approach has focused on the first objective: fitting the best model to the data in an attempt to learn about the underlying relationship in the population. In data mining, however, the focus is typically on the second goal: predicting new observations. Important differences between the approaches stem from the fact that in the classical statistical world we are interested in drawing conclusions from a limited supply of data and in learning how reliable those conclusions might be. In data mining, by contrast, data are typically plentiful, so the performance and reliability of our model can easily be established by applying it to fresh data.

Multiple linear regression is applicable to numerous data mining situations. Examples are predicting customer activity on credit cards from their demographics and historical activity patterns, predicting the time to failure of equipment based on utilization and environment conditions, predicting expenditures on vacation travel based on historical frequent flyer data, predicting staffing requirements at help desks based on historical data and product and sales information, predicting sales from cross selling of products from historical information, and predicting the impact of discounts on sales in retail outlets. Although a linear regression model is used for both goals, the modeling step and performance assessment differ depending on the goal. Therefore, the choice of model is closely tied to whether the goal is explanatory or predictive.

Both explanatory and predictive modeling involve using a dataset to fit a model (i.e., to estimate coefficients), checking model validity, assessing its performance, and comparing to other models. However, there are several major differences between the two:

A good explanatory model is one that fits the data closely, whereas a good predictive model is one that predicts new cases accurately.

In explanatory models (classical statistical world, scarce data) the entire dataset is used for estimating the best-fit model, to maximize the amount of information that we have about the hypothesized relationship in the population. When the goal is to predict outcomes of new cases (data mining, plentiful data), the data are typically split into a training set and a validation set. The training set is used to estimate the model, and the validation, or holdout, set is used to assess this model's performance on new, unobserved data.

Performance measures for explanatory models measure how close the data fit the model (how well the model approximates the data), whereas in predictive models performance is measured by predictive accuracy (how well the model predicts new cases).

For these reasons it is extremely important to know the goal of the analysis before beginning the modeling process. A good predictive model can have a looser fit to the data on which it is based, and a good explanatory model can have low prediction accuracy In the remainder of this chapter we focus on predictive models because these are more popular in data mining and because most textbooks focus on explanatory modeling.

The coefficients β0, ... , βp and the standard deviation of the noise (σ) determine the relationship in the population of interest. Since we only have a sample from that population, these coefficients are unknown. We therefore estimate them from the data using a method called ordinary least squares (OLS). This method finds values

To predict the value of the dependent value from known values of the predictors, x1, x2...,xp we use sample estimates for β0,..., βp in the linear regression model (6.1) since β0 ,..., βp cannot be observed directly unless we have available the entire population of interest. The predicted value, ŷ, is computed from the equation

An important and interesting fact for the predictive goal is that even if we drop the first assumption and allow the noise to follow an arbitrary distribution, these estimates are very good for prediction, in the sense that among all linear models, as defined by equation (6.1), the model using the least-squares estimates,

A large Toyota car dealership offers purchasers of new Toyota cars the option to buy their used car as part of a trade-in. In particular, a new promotion promises to pay high prices for used Toyota Corolla cars for purchasers of a new car. The dealer then sells the used cars for a small profit. To ensure a reasonable profit, the dealer needs to be able to predict the price that the dealership will get for the used cars. For that reason, data were collected on all previous sales of used Toyota Corollas at the dealership. The data include the sales price and other information on the car, such as its age, mileage, fuel type, and engine size. A description of each of these variables is given in Table 6.1. A sample of this dataset is shown in Table 6.2.

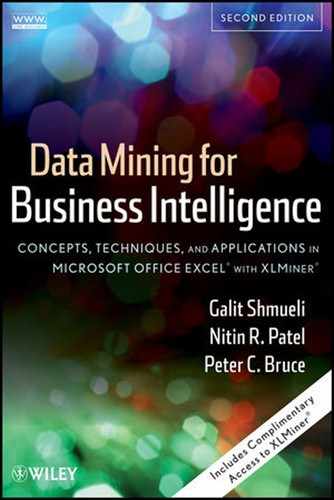

The total number of records in the dataset is 1000 cars (we use the first 1000 cars from the dataset ToyotoCorolla.xls). After partitioning the data into training and validation sets (at a 60% : 40% ratio), we fit a multiple linear regression model between price (the dependent variable) and the other variables (as predictors) using the training set only. Figure 6.1 shows the estimated coefficients (as computed by XLMiner). Notice that the Fuel Type predictor has three categories (Petrol, Diesel, and CNG), and we therefore have two dummy variables in the model [e.g., Petrol (0/1) and Diesel (0/1); the third, CNG (0/1), is redundant given the information on the first two dummies]. These coefficients are then used to predict prices of used Toyota Corolla cars based on their age, mileage, and so on. Figure 6.2 shows a sample of 20 of the predicted prices for cars in the validation set, using the estimated model. It gives the predictions and their errors (relative to the actual prices) for these 20 cars. On the right we get overall measures of predictive accuracy. Note that the average error is $111. A boxplot of the residuals (Figure 6.3) shows that 50% of the errors are approximately between ±$850. This might be small relative to the car price but should be taken into account when considering the profit. Such measures are used to assess the predictive performance of a model and to compare models. We discuss such measures in the next section. This example also illustrates the point about the relaxation of the normality assumption. A histogram or probability plot of prices shows a right-skewed distribution. In a classical modeling case where the goal is to obtain a good fit to the data, the dependent variable would be transformed (e.g., by taking a natural log) to achieve a more "normal" variable. Although the fit of such a model to the training data is expected to be better, it will not necessarily yield a significant predictive improvement. In this example the average error in a model of log(price) is −$160, compared to −$111 in the original model for price.

Table 6.1. VARIABLES IN THE TOYOTA COROLLA EXAMPLEa

Variable | Description |

|---|---|

Price | Offer price in euros |

Age | Age in months as of August 2004 |

Kilometers | Accumulated kilometers on odometer |

Fuel Type | Fuel type (Petrol, Diesel, CNG) |

HP | Horsepower |

Metallic | Metallic color? (Yes = 1, No = 0) |

Automatic | Automatic (Yes = 1, No = 0) |

CC | Cylinder volume in cubic centimeters |

Doors | Number of doors |

QuartTax | Quarterly road tax in euros |

Weight | Weight in kilograms |

Table 6.2. PRICES AND ATTRIBUTES FOR A SAMPLE OF 30 USED TOYOTA COROLLA CARS

Price | Age | Kilometers | Fuel Type | HP | Metallic | Automatic | CC | Doors | Quart Tax | Weight |

|---|---|---|---|---|---|---|---|---|---|---|

13500 | 23 | 46986 | Diesel | 90 | 1 | 0 | 2000 | 3 | 210 | 1165 |

13750 | 23 | 72937 | Diesel | 90 | 1 | 0 | 2000 | 3 | 210 | 1165 |

13950 | 24 | 41711 | Diesel | 90 | 1 | 0 | 2000 | 3 | 210 | 1165 |

14950 | 26 | 48000 | Diesel | 90 | 0 | 0 | 2000 | 3 | 210 | 1165 |

13750 | 30 | 38500 | Diesel | 90 | 0 | 0 | 2000 | 3 | 210 | 1170 |

12950 | 32 | 61000 | Diesel | 90 | 0 | 0 | 2000 | 3 | 210 | 1170 |

16900 | 27 | 94612 | Diesel | 90 | 1 | 0 | 2000 | 3 | 210 | 1245 |

18600 | 30 | 75889 | Diesel | 90 | 1 | 0 | 2000 | 3 | 210 | 1245 |

21500 | 27 | 19700 | Petrol | 192 | 0 | 0 | 1800 | 3 | 100 | 1185 |

12950 | 23 | 71138 | Diesel | 69 | 0 | 0 | 1900 | 3 | 185 | 1105 |

20950 | 25 | 31461 | Petrol | 192 | 0 | 0 | 1800 | 3 | 100 | 1185 |

19950 | 22 | 43610 | Petrol | 192 | 0 | 0 | 1800 | 3 | 100 | 1185 |

19600 | 25 | 32189 | Petrol | 192 | 0 | 0 | 1800 | 3 | 100 | 1185 |

21500 | 31 | 23000 | Petrol | 192 | 1 | 0 | 1800 | 3 | 100 | 1185 |

22500 | 31 | 34131 | Petrol | 192 | 1 | 0 | 1800 | 3 | 100 | 1185 |

22000 | 28 | 18739 | Petrol | 192 | 0 | 0 | 1800 | 3 | 100 | 1185 |

22750 | 30 | 34000 | Petrol | 192 | 1 | 0 | 1800 | 3 | 100 | 1185 |

17950 | 24 | 21716 | Petrol | 110 | 1 | 0 | 1800 | 3 | 85 | 1105 |

16750 | 24 | 25563 | Petrol | 110 | 0 | 0 | 1600 | 3 | 19 | 1065 |

16950 | 30 | 64359 | Petrol | 110 | 1 | 0 | 1600 | 3 | 85 | 1105 |

15950 | 30 | 6760 | Petrol | 110 | 1 | 0 | 1600 | 3 | 85 | 1105 |

16950 | 29 | 43905 | Petrol | 110 | 1 | 0 | 1600 | 3 | 100 | 1170 |

15950 | 28 | 56349 | Petrol | 110 | 1 | 0 | 1600 | 3 | 85 | 1120 |

16950 | 28 | 32220 | Petrol | 110 | 1 | 0 | 1600 | 3 | 85 | 1120 |

16250 | 29 | 25813 | Petrol | 110 | 1 | 0 | 1600 | 3 | 85 | 1120 |

15950 | 25 | 28450 | Petrol | 110 | 1 | 0 | 1600 | 3 | 85 | 1120 |

17495 | 27 | 34545 | Petrol | 110 | 1 | 0 | 1600 | 3 | 85 | 1120 |

15750 | 29 | 41415 | Petrol | 110 | 1 | 0 | 1600 | 3 | 85 | 1120 |

11950 | 39 | 98823 | CNGl | 110 | 1 | 0 | 1600 | 5 | 197 | 1119 |

A frequent problem in data mining is that of using a regression equation to predict the value of a dependent variable when we have many variables available to choose as predictors in our model. Given the high speed of modern algorithms for multiple linear regression calculations, it is tempting in such a situation to take a kitchen-sink approach: Why bother to select a subset? Just use all the variables in the model. There are several reasons why this could be undesirable.

It may be expensive or not feasible to collect a full complement of predictors for future predictions.

We may be able to measure fewer predictors more accurately (e.g., in surveys).

The more predictors there are, the higher the chance of missing values in the data. If we delete or impute cases with missing values, multiple predictors will lead to a higher rate of case deletion or imputation.

Parsimony is an important property of good models. We obtain more insight into the influence of predictors in models with few parameters.

Estimates of regression coefficients are likely to be unstable, due to multicollinearity in models with many variables. (Multicollinearity is the presence of two or more predictors sharing the same linear relationship with the outcome variable.) Regression coefficients are more stable for parsimonious models. One very rough rule of thumb is to have a number of cases n larger than 5(p+2), where p is the number of predictors.

It can be shown that using predictors that are uncorrelated with the dependent variable increases the variance of predictions.

It can be shown that dropping predictors that are actually correlated with the dependent variable can increase the average error (bias) of predictions.

The last two points mean that there is a trade-off between too few and too many predictors. In general, accepting some bias can reduce the variance in predictions. This bias–variance trade-off is particularly important for large numbers of predictors because in that case it is very likely that there are variables in the model that have small coefficients relative to the standard deviation of the noise and also exhibit at least moderate correlation with other variables. Dropping such variables will improve the predictions, as it will reduce the prediction variance. This type of bias–variance trade-off is a basic aspect of most data mining procedures for prediction and classification. In light of this, methods for reducing the number of predictors p to a smaller set are often used.

The first step in trying to reduce the number of predictors should always be to use domain knowledge. It is important to understand what the various predictors are measuring and why they are relevant for predicting the response. With this knowledge the set of predictors should be reduced to a sensible set that reflects the problem at hand. Some practical reasons for predictor elimination are expense of collecting this information in the future, inaccuracy, high correlation with another predictor, many missing values, or simply irrelevance. Also helpful in examining potential predictors are summary statistics and graphs, such as frequency and correlation tables, predictor-specific summary statistics and plots, and missing value counts.

The next step makes use of computational power and statistical significance. In general, there are two types of methods for reducing the number of predictors in a model. The first is an exhaustive search for the "best" subset of predictors by fitting regression models with all the possible combinations of predictors. The second is to search through a partial set of models. We describe these two approaches next.

Exhaustive Search The idea here is to evaluate all subsets. Since the number of subsets for even moderate values of p is very large, we need some way to examine the most promising subsets and to select from them. Criteria for evaluating and comparing models are based on the fit to the training data. One popular criterion is the adjusted R2, which is defined as

where R2, is the proportion of explained variability in the model (in a model with a single predictor, this is the squared correlation). Like R2, higher values of adjusted R2 indicate better fit. Unlike R2, which does not account for the number of predictors used, adjusted R2 uses a penalty on the number of predictors. This avoids the artificial increase in R2 that can result from simply increasing the number of predictors but not the amount of information. It can be shown that using R2adj to choose a subset is equivalent to picking the subset that minimizes σ2.

Another criterion that is often used for subset selection is known as Mallow's Cp. This criterion assumes that the full model (with all predictors) is unbiased, although it may have predictors that if dropped would reduce prediction variability. With this assumption we can show that if a subset model is unbiased, the average Cp value equals the number of parameters p+1 (= number of predictors +1), the size of the subset. So a reasonable approach to identifying subset models with small bias is to examine those with values of Cp that are near p+ 1. Cp is also an estimate of the error[9] for predictions at the x values observed in the training set. Thus, good models are those that have values of Cp near p+ 1 and that have small p (i.e., are of small size). Cp is computed from the formula

where σ2full is the estimated value of σ in the full model that includes all predictors, and SSR is the sum of squares of Regression given in the ANOVA table. It is important to remember that the usefulness of this approach depends heavily on the reliability of the estimate of σ2for the full model. This requires that the training set contain a large number of observations relative to the number of predictors. Finally, a useful point to note is that for a fixed size of subset, R2, Radj2 and Cp all select the same subset. In fact, there is no difference between them in the order of merit they ascribe to subsets of a fixed size.

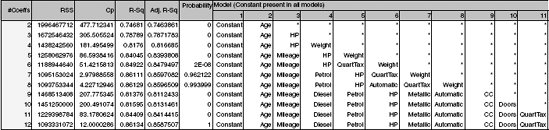

Figure 6.4 gives the results of applying an exhaustive search on the Toyota Corolla price data (with the 11 predictors). It reports the best model with a single predictor, 2 predictors, and so on. It can be seen that the R2adj increases until 6 predictors are used (number of coefficients = 7) and then stabilizes. The Cp indicates that a model with 9–11 predictors is good. The dominant predictor in all models is the age of the car, with horsepower and mileage playing important roles as well.

Popular Subset Selection Algorithms The second method of finding the best subset of predictors relies on a partial, iterative search through the space of all possible regression models. The end product is one best subset of predictors (although there do exist variations of these methods that identify several close-to-best choices for different sizes of predictor subsets). This approach is computationally cheaper, but it has the potential of missing "good" combinations of predictors. None of the methods guarantee that they yield the best subset for any criterion, such as adjusted R2. They are reasonable methods for situations with large numbers of predictors, but for moderate numbers of predictors the exhaustive search is preferable.

Three popular iterative search algorithms are forward selection, backward elimination, and stepwise regression. In forward selection we start with no predictors and then add predictors one by one. Each predictor added is the one (among all predictors) that has the largest contribution to R2 on top of the predictors that are already in it. The algorithm stops when the contribution of additional predictors is not statistically significant. The main disadvantage of this method is that the algorithm will miss pairs or groups of predictors that perform very well together but perform poorly as single predictors. This is similar to interviewing job candidates for a team project one by one, thereby missing groups of candidates who perform superiorly together, but poorly on their own.

In backward elimination we start with all predictors and then at each step eliminate the least useful predictor (according to statistical significance). The algorithm stops when all the remaining predictors have significant contributions. The weakness of this algorithm is that computing the initial model with all predictors can be time consuming and unstable. Stepwise regression is like forward selection except that at each step we consider dropping predictors that are not statistically significant, as in backward elimination.

Note: In XLMiner, unlike other popular software packages (SAS, Minitab, etc.), these three algorithms yield a table similar to the one that the exhaustive search yields rather than a single model. This allows the user to decide on the subset size after reviewing all possible sizes based on criteria such as Radj2 and Cp.

For the Toyota Corolla price example, forward selection yields exactly the same results as those found in an exhaustive search: For each number of predictors the same subset is chosen (it therefore gives a table identical to the one in Figure 6.4). Notice that this will not always be the case. In comparison, backward elimination starts with the full model and then drops predictors one by one in this order: Doors, CC, Diesel, Metallic, Automatic, QuartTax, Petrol, Weight, and Age (see Figure 6.5). The Radj2 and Cp measures indicate exactly the same subsets as those suggested by the exhaustive search. In other words, it correctly identifies Doors, CC, Diesel, Metallic, and Automatic as the least useful predictors. Backward elimination would yield a different model than that of the exhaustive search only if we decided to use fewer than six predictors. For instance, if we were limited to two predictors, backward elimination would choose Age and Weight, whereas an exhaustive search shows that the best pair of predictors is actually Age and HP.

The results for stepwise regression can be seen in Figure 6.6. It chooses the same subsets as forward selection for subset sizes of 1–7 predictors. However, for 8–10 predictors, it chooses a different subset than that chosen using the other methods: It decides to drop Doors, Quart Tax, and Weight. This means that it fails to detect the best subsets for 8–10 predictors. Radj2 is largest at 6 predictors (the same 6 as were selected by the other models), but Cp indicates that the full model with 11 predictors is the best fit.

This example shows that the search algorithms yield fairly good solutions, but we need to carefully determine the number of predictors to retain. It also shows the merits of running a few searches and using the combined results to determine the subset to choose. There is a popular (but false) notion that stepwise regression is superior to backward elimination and forward selection because of its ability to add and to drop predictors. This example shows clearly that it is not always so.

Finally, additional ways to reduce the dimension of the data are by using principal components (Chapter 4) and regression trees (Chapter 9).

6.1 Predicting Boston Housing Prices. The file BostonHousing.xls contains information collected by the U.S. Bureau of the Census concerning housing in the area of Boston, Massachusetts. The dataset includes information on 506 census housing tracts in the Boston area. The goal is to predict the median house price in new tracts based on information such as crime rate, pollution, and number of rooms. The dataset contains 14 predictors, and the response is the median house price (MEDV). Table 6.3 describes each of the predictors and the response.

Table 6.3. DESCRIPTION OF VARIABLES FOR BOSTON HOUSING EXAMPLE

CRIM

Per capita crime rate by town

ZN

Proportion of residential land zoned for lots over 25,000 ft2

INDUS

Proportion of nonretail business acres per town

CHAS

Charles River dummy variable (= 1 if tract bounds river; = 0 otherwise)

NOX

Nitric oxide concentration (parts per 10 million)

RM

Average number of rooms per dwelling

AGE

Proportion of owner-occupied units built prior to 1940

DIS

Weighted distances to five Boston employment centers

RAD

Index of accessibility to radial highways

TAX

Full-value property tax rate per $10,000

PTRATIO

Pupil/teacher ratio by town

B

1000(Bk – 0.63)2 where Bk is the proportion of blacks by town

LSTAT

% Lower status of the population

MEDV

Median value of owner-occupied homes in $1000s

Why should the data be partitioned into training and validation sets? For what will the training set be used? For what will the validation set be used?

Fit a multiple linear regression model to the median house price (MEDV) as a function of CRIM, CHAS, and RM.

Write the equation for predicting the median house price from the predictors in the model.

What median house price is predicted for a tract in the Boston area that does not bound the Charles River, has a crime rate of 0.1, and where the average number of rooms per house is 6? What is the prediction error?

Reduce the number of predictors:

Which predictors are likely to be measuring the same thing among the 14 predictors? Discuss the relationships among INDUS, NOX, and TAX.

Compute the correlation table for the 13 numerical predictors and search for highly correlated pairs. These have potential redundancy and can cause multicollinearity. Choose which ones to remove based on this table.

Use an exhaustive search to reduce the remaining predictors as follows: First, choose the top three models. Then run each of these models separately on the training set, and compare their predictive accuracy for the validation set. Compare RMSE and average error, as well as lift charts. Finally, describe the best model.

6.2 Predicting Software Reselling Profits. Tayko Software is a software catalog firm that sells games and educational software. It started out as a software manufacturer and then added third-party titles to its offerings. It recently revised its collection of items in a new catalog, which it mailed out to its customers. This mailing yielded 1000 purchases. Based on these data, Tayko wants to devise a model for predicting the spending amount that a purchasing customer will yield. The file Tayko.xls contains information on 1000 purchases. Table 6.4 describes the variables to be used in the problem (the Excel file contains additional variables).

Table 6.4. DESCRIPTION OF VARIABLES FOR TAYKO SOFTWARE EXAMPLE

FREQ

Number of transactions in the preceding year

LAST_UPDATE

Number of days since last update to customer record

WEB

Whether customer purchased by Web order at least once

GENDER

Male or female

ADDRESS_RES

Whether it is a residential address

ADDRESS_US

Whether it is a U.S. address

SPENDING (response)

Amount spent by customer in test mailing (in dollars)

Explore the spending amount by creating a pivot table for the categorical variables and computing the average and standard deviation of spending in each category.

Explore the relationship between spending and each of the two continuous predictors by creating two scatterplots (SPENDING vs. FREQ, and SPENDING vs. LAST_UPDATE). Does there seem to be a linear relationship?

To fit a predictive model for SPENDING:

Partition the 1000 records into training and validation sets.

Run a multiple linear regression model for SPENDING versus all six predictors. Give the estimated predictive equation.

Based on this model, what type of purchaser is most likely to spend a large amount of money?

If we used backward elimination to reduce the number of predictors, which predictor would be dropped first from the model?

Show how the prediction and the prediction error are computed for the first purchase in the validation set.

Evaluate the predictive accuracy of the model by examining its performance on the validation set.

Create a histogram of the model residuals. Do they appear to follow a normal distribution? How does this affect the predictive performance of the model?

6.3 Predicting Airfares on New Routes. Several new airports have opened in major cities, opening the market for new routes (a route refers to a pair of airports), and Southwest has not announced whether it will cover routes to/from these cities. In order to price flights on these routes, a major airline collected information on 638 air routes in the United States. Some factors are known about these new routes: the distance traveled, demographics of the city where the new airport is located, and whether this city is a vacation destination. Other factors are yet unknown (e.g., the number of passengers who will travel this route). A major unknown factor is whether Southwest or another discount airline will travel on these new routes. Southwest's strategy (point-to-point routes covering only major cities, use of secondary airports, standardized fleet, low fares) has been very different from the model followed by the older and bigger airlines (hub-and-spoke model extending to even smaller cities, presence in primary airports, variety in fleet, pursuit of high-end business travelers). The presence of discount airlines is therefore believed to reduce the fares greatly.

The file Airfares.xls contains real data that were collected for the third quarter of 1996. They consist of the predictors and response listed in Table 6.5. Note that some cities are served by more than one airport, and in those cases the airports are distinguished by their three-letter code.

Table 6.5. DESCRIPTION OF VARIABLES FOR AIRFARE EXAMPLE

S_CODE

Starting airport's code

S_CITY

Starting city

E_CODE

Ending airport's code

E_CITY

Ending city

COUPON

Average number of coupons (a one-coupon flight is a nonstop flight, a two-coupon flight is a one-stop flight, etc.) for that route

NEW

Number of new carriers entering that route between Q3-96 and Q2-97

VACATION

Whether (Yes) or not (No) a vacation route

SW

Whether (Yes) or not (No) Southwest Airlines serves that route

HI

Herfindahl index: measure of market concentration

S_INCOME

Whether (Yes) or not (No) a vacation route

VACATION

Starting city's average personal income

E_INCOME

Ending city's average personal income

S_POP

Starting city's population

E_POP

Ending city's population

SLOT

Whether or not either endpoint airport is slot controlled (this is a measure of airport congestion)

GATE

Whether or not either endpoint airport has gate constraints (this is another measure of airport congestion)

DISTANCE

Distance between two endpoint airports in miles

PAX

Number of passengers on that route during period of data collection

FARE

Average fare on that route

Explore the numerical predictors and response (FARE) by creating a correlation table and examining some scatterplots between FARE and those predictors. What seems to be the best single predictor of FARE?

Explore the categorical predictors (excluding the first four) by computing the percentage of flights in each category. Create a pivot table with the average fare in each category. Which categorical predictor seems best for predicting FARE?

Find a model for predicting the average fare on a new route:

Convert categorical variables (e.g., SW) into dummy variables. Then, partition the data into training and validation sets. The model will be fit to the training data and evaluated on the validation set.

Use stepwise regression to reduce the number of predictors. You can ignore the first four predictors (S_CODE, S_CITY, E_CODE, E_CITY). Report the estimated model selected.

Repeat (ii) using exhaustive search instead of stepwise regression. Compare the resulting best model to the one you obtained in (ii) in terms of the predictors that are in the model.

Compare the predictive accuracy of both models (ii) and (iii) using measures such as RMSE and average error and lift charts.

Using model (iii), predict the average fare on a route with the following characteristics: COUPON = 1.202, NEW = 3, VACATION = No, SW = No, HI = 4442.141, S_INCOME = $28,760, E_INCOME = $27,664, S_POP = 4,557,004, E_POP = 3,195,503, SLOT = Free, GATE = Free, PAX = 12782, DISTANCE = 1976 miles.

Predict the reduction in average fare on the route if in (b) Southwest decides to cover this route [using model (iii)].

Predict the reduction in average fare on the route if in (b) Southwest decides to cover this route [using model (iii)].

In reality, which of the factors will not be available for predicting the average fare from a new airport (i.e., before flights start operating on those routes)? Which ones can be estimated? How?

Select a model that includes only factors that are available before flights begin to operate on the new route. Use an exhaustive search to find such a model.

Use the model in (viii) to predict the average fare on a route with characteristics COUPON=1.202, NEW=3, VACATION=No, SW=No, HI=4442.141, S_INCOME = $28,760, E_INCOME = $27,664, S_POP = 4,557,004, E_POP = 3,195,503, SLOT = Free, GATE = Free, PAX = 12782, DISTANCE = 1976 miles.

Compare the predictive accuracy of this model with model (iii). Is this model good enough, or is it worthwhile reevaluating the model once flights begin on the new route?

In competitive industries, a new entrant with a novel business plan can have a disruptive effect on existing firms. If a new entrant's business model is sustainable, other players are forced to respond by changing their business practices. If the goal of the analysis was to evaluate the effect of Southwest Airlines' presence on the airline industry rather than predicting fares on new routes, how would the analysis be different? Describe technical and conceptual aspects.

6.4 Predicting Prices of Used Cars. The file ToyotaCorolla.xls contains data on used cars (Toyota Corolla) on sale during late summer of 2004 in The Netherlands. It has 1436 records containing details on 38 attributes, including Price, Age, Kilometers, HP, and other specifications. The goal is to predict the price of a used Toyota Corolla based on its specifications. (The example in Section 4.2.1 is a subset of this dataset.)

Data Preprocessing. Create dummy variables for the categorical predictors (Fuel Type and Metallic). Split the data into training (50%), validation (30%), and test (20%) datasets. Run a multiple linear regression using the Prediction menu in XLMiner with the output variable Price and input variables Age_08_04, KM, Fuel Type, HP, Automatic, Doors, Quarterly_Tax, Mfg_Guarantee, Guarantee_Period, Airco, Automatic_Airco, CD_Player, Powered_Windows, Sport_Model, and Tow_Bar.

What appear to be the three or four most important car specifications for predicting the car's price?

Using metrics you consider useful, assess the performance of the model in predicting prices.