Innovation, Disruption, and the Survival of the Fittest

Stephen Woodhouse

Simon Bradbury Pöyry Management Consulting, Oxford, United Kingdom

Abstract

Energy markets across the world are in the middle of a revolution, triggered by the pursuit of decarbonization and fueled by innovation. History suggests that this is not a safe place to be, not even for the revolutionaries, but especially not for the “old guard.” How many of the existing major energy companies can fully expect to survive in close to their present form for the next 10 years, as the industry transforms away from the conventions of the 20th century into a brave new world? This chapter investigates the key characteristics necessary for a successful future energy company against a backdrop of substantially changing demands from customers and policymakers, as well as the arrival of new competitors and technological advances in IT.

Keywords

decentralized energy

energy business models

consumer engagement

innovation and disruption

utility business strategy

1. Introduction

Customers are used to receiving electricity reliably as if by magic, without wishing to see the means of delivery, either in terms of noticing the infrastructure used to supply power or the impact of consumption on their bank accounts.

But a combination of policy objectives and technological advancements is changing the picture significantly.

Focusing first on policy goals, many countries now have clear policy objectives to decarbonize the electricity sector and their economies more generally. Taking Europe as an example, the European Union has an aspiration to reduce greenhouse gas emissions to 80%–95% below 1990 levels by 2050. Within Europe, national objectives have also been defined by some countries. For example, the United Kingdom has set a legally binding target to reduce greenhouse gas emissions by 80% by 2050, Germany has the target to reduce emissions by 80%–95% by 2050, and Denmark has the target of becoming independent of fossil fuels by 2050.

As an engineering challenge, the scale of change is huge, with heavy reliance on emerging technologies and on major IT projects. Public acceptance of new transmission and (some) generation infrastructure is proving a significant barrier, and without better engagement with customers, this will not improve.

The increased need for coordination across the sector is daunting. This applies to both investment planning, as well as actual market operation. Generation is diversifying and shrinking in scale, and demand must respond to generation not just the other way around. But none of this is insurmountable.

Meanwhile, new actors are entering the energy sector, deploying a series of new technologies, which allow them to understand and meet the needs of customers and small producers in ways, which the existing companies have never done. The decentralized energy system, in which customers can be actively engaged, is becoming a practical possibility.

Activity by consumers, network owners, system operators, and in the wholesale markets must be effectively coordinated, and there will be new roles and interactions supported by distributed intelligence and automation. Conflicts will emerge over who has access to customers, who is in ultimate control, and who captures value and holds risk. Ultimately, it is not clear what services will be offered by which actor and who will hold the relationship with customers.

This tension encapsulates the theme of this book and its focus on the effects of innovation and disruption on the energy sector. A number of strands within this chapter are picked up again in others, including chapters by Cooper, which considers business transformation strategies; by Johnston and Sioshansi, which considers transformations needed to allow engagement of proactive consumers; and by Steiniger, which considers the role of virtual power plants.

The emergence of a decentralized industry, with engaged customers and new remote data and control possibilities has opened up an alternative future for the energy sector. Given the scale and nature of the revolution, the underlying question is: what characteristics will a successful energy company of the future have? This chapter considers this question.

This chapter consists of four sections in addition to the Introduction. Section 2 considers the challenges associated with the energy sector transformation. Section 3 considers the characteristics required for the energy company of the future. Section 4 provides an appraisal of what is needed for the energy companies of today to adjust for the future followed by the chapter’s conclusions.

2. Is delivering this transformation really that much of an issue?

It is fair to question whether the current energy sector transformation can really be thought of as unprecedented. Similar large-scale transformations have previously been achieved in the energy sector, but only within the context of centrally planned vertically integrated monopolies. The option to go back in that direction exists but it seems to be against the tide of history.

The ability for traditional utility business models, which revolve around the existence of large vertically integrated entities, to drive a digital and customer-centric transformation is doubtful.

In today’s market, commercial conditions for large vertically integrated players have deteriorated, signaling a paradigm shift.

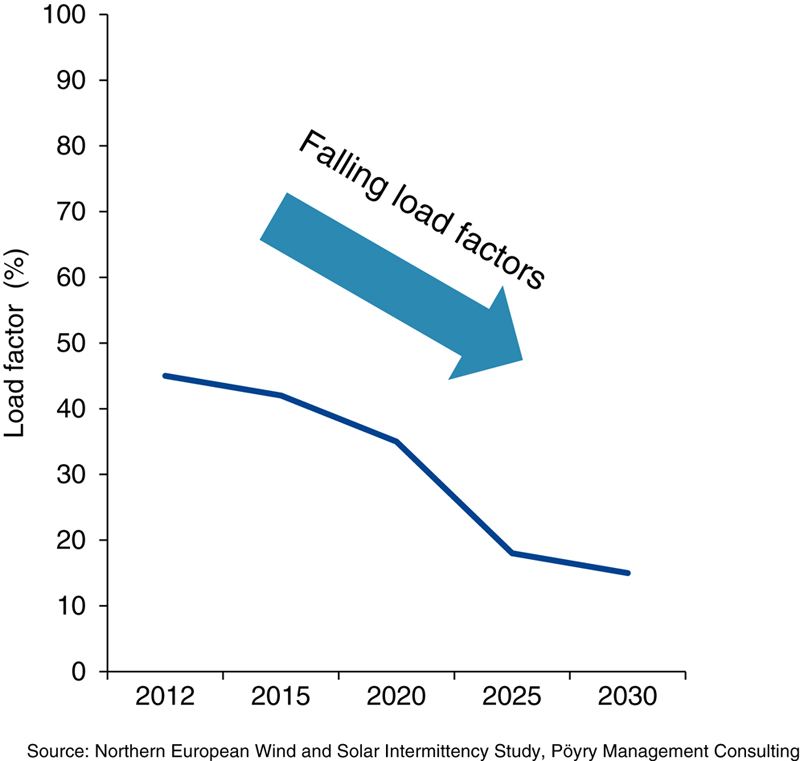

The first change is that utilities are suffering from major profitability issues, especially with their thermal generation assets. Running hours and ability to capture revenue are being curtailed as the volume of renewable generation on the system increases. Studies have highlighted further anticipated reductions in load factor for thermal plant, as the penetration of renewables continues to grow. This is illustrated in Fig. 2.1, which presents anticipated falling load factors for CCGTs, based on a Pöyry study in relation to the implications of intermittency in Northern Europe.1

Figure 2.1Projected load factors for thermal plant.

The second shift relates to the effectiveness of the “vertically integrated” utility model at dealing with both political and market risk. Over recent years, the model has increasingly proved to be poor at dealing with such risks, and its ability to effectively manage risk in a rapidly evolving environment looks unlikely.

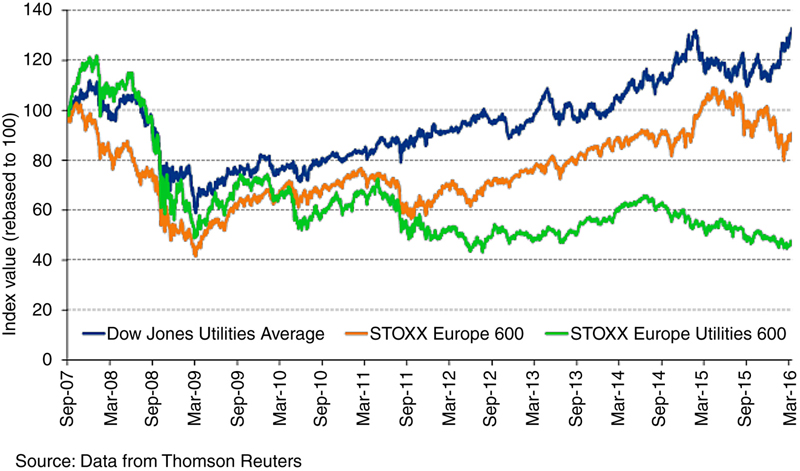

The performance of listed utilities’ share prices provides an indication of the challenging times that these companies have found themselves in, over recent years, as a result of these shifts. Prior to and during the economic downturn that began in 2008, European utility stocks outperformed the market. All stocks suffered as a result of the downturn, but the recovery of European utility stocks has fallen far short of the wider market. Importantly, in a reverse of the precrash relationship, utilities are now underperforming relative to the market. This provides a clear indicator of the changing fortunes of the utilities. These trends are illustrated in Fig. 2.2.2

Figure 2.2Performance of EU utility stocks versus EU stocks more generally.

The fallout has been pronounced. For example, in 2014 GDF Suez wrote off €14.9 billion as the value of its power plants fell,3 while both RWE and E.On posted significant losses linked to the decline of their fossil fuel businesses.4

Pinpointing the issues and the magnitude of their effect from the perspective of his company, Rolf Martin Schmitz, the COO of RWE, noted that “the massive erosion of wholesale prices caused by the growth of German photovoltaics constitutes a serious problem for RWE which may even affect the company’s survival.”5

The third development is that new technology providers—some of them very well-funded—are entering the energy space and have the potential to undermine the link between existing companies and customers. As an example, while traditional utilities are feeling pain, Eric Schmidt, former CEO of Google, encapsulated the potential but also the uncertainty for the future, commenting that “the Energy Transition in Europe will provide a lot of opportunities for many companies—but nobody knows exactly today where and how to make money in the future.” The interest and arrival of new players is changing the competitive landscape of the markets and the mindset of consumers.

There are lessons from other industries that suggest that existing companies with traditional business models are not best placed to adapt to opportunities that new technologies bring.

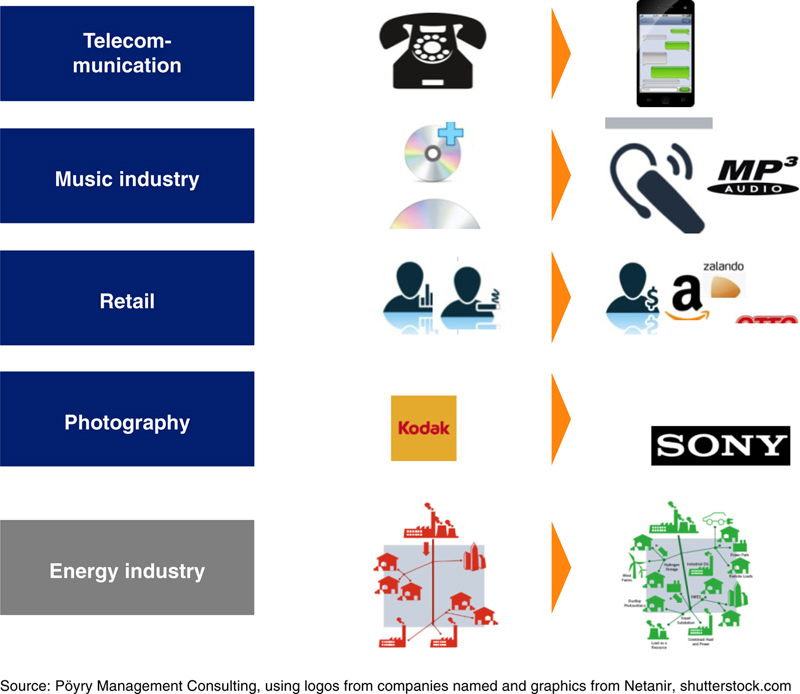

In telecoms, the invention of a range of mobile technologies forced a major change in the services which traditional players deliver. More recently there has been a second seismic shift with the introduction of smartphones, in many cases, moving potential revenue away from network operators to the phone hardware providers themselves. The rise of digital downloads has substantially changed the music business value chain, allowing new entrants to go straight to customers. Digital photography left its creator—Kodak—in bankruptcy (Chapter 11), as they failed to ride the crest of the technological wave. Airbnb built a portfolio of 1 million rooms—which it does not own—in 6 years, while it took the Hilton Group 100 years to achieve 700,000.

Fig. 2.3 provides an illustration of the transformations seen in these industries. Such lessons provide a stark warning to those still in traditional utility business model mode—ignore change at your peril.

Figure 2.3Industry transformations.

It is the scale of the ongoing energy sector transformation, the rate of IT advancements, and the difficulties being faced by the traditional utility, in combination, which make the current challenge so significant. If the utilities of today are to survive, successful transformation requires evolution on all fronts—technological, commercial, and cultural. For those that can adapt, there are opportunities. Not adapting looks set to be a short-lived strategy.

In such an environment, what features are needed to create a successful integrated energy company for the future? The alternative is perhaps for new companies to take over the customer relationship, and for the existing companies to be pushed upstream. These themes are explored further by Johnston & Sioshansi, who consider models for engagement of proactive consumers and by Steiniger & Sioshansi, who focus on the role of virtual power plants to aggregate consumers.

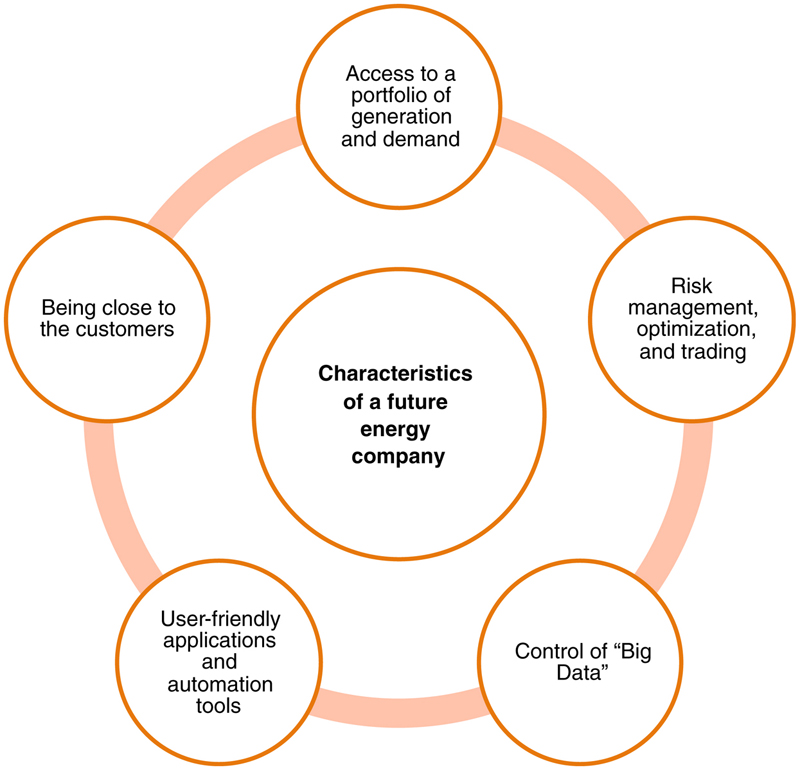

3. The five key characteristics of a future energy company

The emergence of a decentralized industry, with engaged customers and new remote data and control possibilities has opened up an alternative possible future for the energy sector. The sections below set out a possible recipe for a future integrated energy company, structured around five key characteristics. These are as follows (and as displayed in Fig. 2.4):

• Characteristic 1: access to a portfolio of generation, storage, and flexible demand will remain important in the future, but with less emphasis on asset ownership.

Figure 2.4Five characteristics of future integrated energy company.

• Characteristic 2: risk management, optimization, and trading are essential parts of the operation of a utility and will continue to be core business.

• Characteristic 3: control of “Big Data” will give leverage for competitive advantage.

• Characteristic 4: user-friendly applications and automation tools will enhance customer propositions and unlock demand response.

• Characteristic 5: being close to the customers and retaining their trust as their needs change will be important to unlock new sources of value.

3.1. Characteristic 1: Access to a Portfolio of Generation, Storage, and Flexible Demand Will Remain Important in the Future

Any future portfolio will require access to a diverse portfolio. This will need to span generation, demand, and storage or other technologies that can deliver flexibility. Circumstances differ and not everyone needs the same portfolio of generation or the same types of customer. But having access to an appropriate blend of resources will allow for value to be realized through trading activities and for risks to be managed.

This does not necessarily mean continued ownership of the assets by the energy companies, however. In future, a more asset-neutral approach may be expected to emerge.6 Indeed, this trend is already in evidence, as ownership of generation is diversifying. Initially, this was seen with a wave of independently owned wind farms. More recently, the trend has continued as millions of consumers have invested in solar generation. Looking forward, a similar pattern looks set to emerge with growing installation of domestic scale batteries. Asset ownership is becoming more diversified and decentralized to the extent that, increasingly, each house/business or, with aggregation, cluster of houses/businesses could be considered as an asset.

As an example of a possible model for the future, Statkraft has built a successful business in Germany based on aggregating renewable generation plants from smaller developers, and offering trading and risk management services. They have over 9.5 GW of wind and solar energy from more than 1300 sites under contract, which dwarfs its small portfolio of hydro and gas generation in Germany. As a result, Statkraft is the largest direct selling company in Germany and one of the biggest traders in the German day-ahead and intraday markets, without owning any wind assets there. It is notable that their “asset-light” approach is concentrated on portfolio management and trading and risk management, rather than a full focus on retail and the needs of household customers.

Ongoing market design changes in Europe are increasing the potential for this model to be applied more broadly. Now that renewable energy has a significant role in many markets, the emphasis is increasingly on integrating renewables into the market rather than insulating them from it. In the European Commission’s recent Clean Energy Package,7 for example, we are seeing proposals for balance responsibility and, prospectively, removal of priority dispatch for all but the smallest renewable installations. In addition, there is emphasis on future support regimes for renewables structuring payments around their revenues from the wholesale market. Entering into arrangements with an aggregator to provide trading and risk management services in the vein described above is one option available for dealing with greater market exposure.

Therefore, having access to a portfolio of resource across generation and demand, integrating commercial arrangements with the assets of others into this portfolio, will be an important feature of the future energy company, as well as a valuable service to others in the market.

3.2. Characteristic 2: Risk Management, Optimization, and Trading are Essential Parts in the Operation of a Utility

Electricity is the world’s most volatile traded commodity. The true strength of traditional energy companies is their ability to invest in assets with a 20–40 year lifetime on the back of a series of short-term contracts. The series of trading, risk management, optimization, and financial and collateral management tools, which support this is world class. The complexity and volatility of the wholesale market is a barrier to entry for new players, and existing energy companies will retain a competitive advantage over new players for some time to come in this regard.

But the nature of risks within the market is changing. The growth of renewables has increased price risk but has also brought volume risk to the fore. Thermal plants now have real uncertainty over when and how much they will operate, as running patterns flex around renewable generation output with near-zero short run marginal costs. The challenge lies in that the industry broadly continues to trade the same products as 10 years ago, which suited the risks faced at that time, but are not geared toward the risks of the future.

For example, a decade ago, most CCGTs would be able to predict reasonably well their likely running patterns for the coming weeks, months, and even beyond, based on expectations of typical demand patterns and fuel prices relative to coal generators. But today, a CCGT’s output is dependent on wind and solar levels, which are only known in the nearer-term, and so it does not know its likely hourly production profile significantly ahead of real time. Unlike the situation 10 years ago, the CCGT now has volume risk, as well as price risk, changing the basis for forward energy trading. The spark spread relates to a profile of generation that has not been seen in most of Europe for 5 years. A negative spread just means that the market is trading the wrong products.

New trading instruments are available, though, in the form of options. This is a natural product to complement trading of firm energy. Generation capacity can essentially be considered an “option” to produce energy. While all production capacity represents such an option, some resources offer greater flexibility than others in how the option can be exercised and how frequently. In an increasingly decarbonized system with high levels of low carbon generation, energy market volatility could be significantly greater, increasing the value of such options.

The appropriate response is to ensure that market participants are able to trade energy “options” in the form of a sufficiently broad range of products mirroring the various types of services the market requires. Multiple option variants could be developed to reflect different requirements, such as deliverability and flexibility, and to suit the capabilities of different types of capacity. Our own suggested approach develops the concept of capacity as an energy option and proposes a bilateral model for the trading of energy “options.”8 Under a bilateral approach, options for use of a resource can be sold by the provider to other parties who may require flexibility to balance their own positions (e.g., as a complement to variable generation resources or to help manage retail positions).

Moving forward, traders need to find means of packaging risk and managing complexity in ways that will continue to bring in capital for new projects. The new risks need new market instruments, such as the energy options discussed above, to manage volume risk and complement the markets for delivered energy. With a system of energy options, parties with flexible assets could sell options for access to their flexibility to others, such as retailers who are then able to exercise the options when needed to access energy and help manage price volatility. This gives:

1. the flexible assets revenue that is not tied solely to production and

2. the counterparty with a type of insurance that helps to protect them against price fluctuations.

As an alternative to trading hedges, another possible route for risk mitigation is offered through physical hedges. Tesla provides an example of an integrated model, which now spans electric vehicle, solar PV panels (since the acquisition of SolarCity9), and electricity storage through its Powerwall product. Through its Supercharger network, Tesla (for now) offers free fast charging for its EV owners; and the addition of solar and storage to the mix offers the possibility for customers to break links with traditional utilities and instead rely on Tesla for all their energy needs. Importantly, this is all under the banner of a well-recognized and established brand. Customers buying into the Tesla product range will have a long-term relationship with the company, given the lifetime of the underlying products themselves. Tesla has the ability to define these relationships such that it can access the flexibility offered by the fleet of EV charging activities, storage, and generation assets of its customers. It also has a way in to become the energy supplier for its customers and their Tesla products. Therefore, through its brand and products, Tesla hopes to make big waves in the energy market.10

3.3. Characteristic 3: Control of “Big Data” Will Give Leverage for Competitive Advantage

Put simplistically, utilities have tended to know their customers as deemed profiles, only obtaining details on actual consumption in aggregate across a period of months significantly after the event and with very little understanding of their needs or desires. The advent of smart meters and other data processing technologies/businesses offer the opportunity to change this. The dawn of readily available “Big Data” (i.e., the ability to integrate with data from other sources, such as social media) provides access to much more granular and timely information concerning consumer behavior and the underlying reasons.

This is a powerful new resource. It allows utilities to obtain a much clearer understanding of consumer preferences and behavioral patterns and, therefore, the needs and requirements of their customers. To make the most of this opportunity, utilities need the ability to effectively access, analyze, and process the new sources of data to harness the valuable information that they contain concerning consumer behavior. Based on this, utilities will have the ability to develop propositions that are suited to the needs of the consumer and so capture value. This, in turn, may open opportunities to bundle energy with other services. This theme is picked up further as part of characteristic 5 below.

Energyworx provides an example of a company harnessing big data for use in utility sector applications.11 Energyworx converts data delivered through smart meters and sensors into propositions that its clients can act on. Utility clients benefit from Energyworx’s high granularity information about individual consumers’ energy consumption through faster and more accurate billing to consumers, more precise demand forecasting for planning generation, or better targeted pricing and marketing depending on their customers’ installed energy equipment. Equally, prosumers benefit, for instance, by being better able to judge whether they should consume or redistribute their energy or by being able to compare their energy efficiency against other users from the community.

Big Data methodologies and enhanced connectivity of devices will also revolutionize day-to-day operation of the system. With the increased complexity of a decentralized system, the challenge of efficient operation will multiply. Efficient optimization requires better data on the state of different devices and their ability/willingness to respond. Additionally, more powerful tools are needed to allow data to be turned into intelligence and control. But in many regards, data are not available today in timescales that support such optimization. For example, it is remarkable that the settlement timetable for domestic customers has barely changed since the time when urgency in data transfer meant using first class instead of second class postage.

The modernization process in energy has begun. Domestic “smart metering” is gathering pace. However, it is rudimentary and far from being universally applicable. There are beacons of positive development, though. For example:

• Estonia has rolled out a centralized data hub which supports applications from third-party developers. Eesti Energia in its role as a retailer now has around one-third of its domestic customers facing hourly spot pass through tariffs.

• Next Kraftwerke—further described in chapter by Steiniger in this volume—bundles around 3000 small- to medium-scale generators and consumers into a virtual power plant, using a digital platform to connect and optimize flows between producers and consumers.12

• Open Utility—further described in chapter by Johnston in this volume—uses its peer-to-peer energy matching platform to allow consumers to select their own supply source based on current supply and demand from measured smart meter data.13

The full “Internet of Things” vision may be overkill for the energy system for now, as electricity costs for most applications are low and transaction costs are material in that context. However, it is clear that existing information gathering and monitoring tools in many markets are not yet fit for the decentralized future. Capitalizing upon the functionality offered by rapid advances in IT and communications technologies offers the chance to forge a model for the future focused around the customer.

3.4. Characteristic 4: User-Friendly Applications and Automation Tools Will Enhance Customer Propositions and Unlock Demand Response

Many customers now expect instant information and feedback via smartphone or Internet. Customer service in most industries has moved away from call centers to sophisticated applications and Internet-based solutions. Energy companies are adapting to this service model and there has been a proliferation of smart apps in recent years.

However, for the demand side to become truly active by changing consumption patterns in response to system conditions, users will not want continuous active involvement. For most domestic consumers, the potential saving even from very sophisticated decision-making is low. Typically, households in Europe pay around €2 per day for electricity in total, and the saving from optimal consumption patterns is a fraction of that. With (flexible) electric heating or vehicle charging the value increases. For example, to charge a 30 kWh electric vehicle battery, the saving based on typical day–night tariffs in United Kingdom could be €5 or more per charge. But these decisions will still need to be automated if users are expected to take optimal decisions everyday. This requires energy companies to offer excellent, user-friendly, and robust automation tools, which allow users to retain control.

Therefore, decentralized decision-making must become automated, and the customers’ experience should not be affected. In this vein, in the United Kingdom, npower has partnered with Nest Labs,14 who specialize in smart thermostats and smoke/CO detectors.15 The Nest Thermostat learns from the user and programs itself based on this, while also allowing remote control via smartphone. This provides the consumers with energy for heating based on learning from observed patterns of behavior, while also offering control where desired.

German company beegy16 offers another example where consumers enjoy automated integration of a suite of smart energy technologies behind a streamlined interface. Their service consists of managing a home’s PV panels, Tesla Powerwalls, and EV charging points through a single beegyHUB, whose activities the homeowner can track through a web portal or smartphone app. The company consolidates all beegyHUBs Germany-wide into a single beegy Community. Algorithms allow users to store their energy or feed it into the Community when their consumption dips below their generation capacity. Alternatively, when their consumption exceeds their domestic generation and stored energy, users can also draw on the Community for electricity—at a flat rate that beegy locks in for 20 years. The company also offers its clients constant monitoring of their equipment, providing a 20-year warrantee for all products. Alongside this specific German example, the chapter by Löbbe & Hackbarth describes examples of innovative companies in Germany.

Heating represents another area where smart technologies could enable demand-side response. Glen Dimplex, the world’s largest manufacturer of electrical heating equipment, has been focusing since 2015 on this issue through the RealValue project, in collaboration with partners from Ireland, Germany, and Latvia. This 3-year project, funded through the EU’s Horizon 2020 program, aims to demonstrate how Smart Electrical Thermal Storage (SETS) can, along with a management platform and interface for end users, meet domestic heating needs while also acting as energy storage capacity for the electricity industry.

The trend of twinning automation and user-friendly apps with energy applications is clearly on the rise, with early movers seeing and benefiting from the access to and engagement with consumers that it offers.

3.5. Characteristic 5: Being Close to the Customers as Their Demands Change

The needs of customers do not always align with the plans of vertically integrated energy companies. The most obvious conflict is over incentives for energy efficiency, which causes customers to consume less energy and, hence, companies to produce and sell less of their basic product. This dilemma sheds light on how a truly customer-focused energy company might approach its customer offering.

Ultimately, most successful mass-market business models involve a combination of high volume and low margin sales accompanied by opportunistic niche sales with higher value. To be sustainable, the higher value sales need to be based on predicting and then meeting customer wishes. The bundling of services may be within the energy sector or extend beyond. For example, cars or appliances may come with an energy supply agreement.

Again, Tesla is an example here. Its branding is an essential part of its proposition and its customers feel that they are buying into the brand. Strong brands from the nontraditional, newer entrants into the energy sector may hasten the demise of traditional integrated energy companies, whose own brands have, in some cases, been tarnished by concerns regarding misselling to or profiteering at the expense of their customers. Trust in conventional utilities has been negatively affected, as a result.17

A successful energy business must build a strong relationship with its customers, including trust on both sides, and has to build a good understanding of its customers’ needs. It must come to think of its relationship with customers as part of its asset base, noting that, in a long-term business, assets must be carefully managed to not be exploited.

4. The new energy company

Taking the above characteristics into consideration, who in the energy sector has this combination of skills today? Arguably, no one.

The existing energy companies excel at characteristics 1 and 2: portfolio management and trading/risk management. But how do they defend their businesses from left-field entrants already skilled in Big Data, user-friendly applications, and automation tools? They must focus on their existing strengths while covering the gaps—and improve their relationships with their customers while doing so.

What appears to be central to a successful strategy for the future is to focus on the consumer and to place the customer at the heart of the offering. While the sector has always focused on providing energy to meet consumers’ needs, the traditional approach has been for consumers to be passive and for there to be a one-way flow down the supply chain from utilities to consumers. Energy needs have been met, but the consumers and their wider preferences have been largely extraneous to the workings of the markets.

With Big Data providing insights into consumer behavior and needs, IT providing scope for greater consumer interaction and increased ownership of energy assets at smaller scale, the scope for more mutually beneficial engagement between energy company and consumer is vastly increased. In this context, companies which dwell on their existing skills and focus on their own technologies and assets at the expense of their customers run a high risk of failure, especially in a fast-changing industry.

Some of Europe’s utilities are seeking to reinvent themselves. RWE has restructured, choosing to bundle renewables, networks, and retail into a new subsidiary, Innogy, separate from the conventional generation business (although still under the RWE banner18). E.On has also restructured, but has elected to retain renewables, networks, and retail under the E.On brand, with the conventional generation business now operating as Uniper.19

Whether such steps will prove effective in improving their fortunes remains to be seen. But it seems unlikely that the newer potential entrants to the energy sector, such as Tesla or Google, will withdraw, having made effective forays and gained traction. The drive toward decentralized energy, with a growing role for demand-side response, aggregation, and engaged customers has also irrevocably changed the game.

In the current environment, our advice to the utilities contains the following messages:

• hesitate before taking big decisions on conventional generation investments;

• invest in trading and risk management tools, such as options, and trading capabilities that are appropriate for the future market context;

• understand the customer base and the requirements and perspectives of the consumer; and

• take a strategic view on customer propositions that will work for your customers and on the branding and partnership models that will allow you to achieve them at scale.

5. Conclusions

The energy industry is ripe for revolution toward a system which uses new technologies to put its customers first. The set of characteristics above set out one possible recipe for a future integrated energy company, which retains its connection with customers and enshrines these relationships as the crux of its business. Other futures are available, including ones in which new companies take over the relationship with customers and force the energy companies to retreat upstream toward production and trading.

Utilities need to find new ways to engage with their customers to drive value propositions through the combination of smart apps, appliances, and Big Data capabilities. In short, focusing on the customer side of the business will not be an alternative business model—it will be the lead.

Changes are being seen in the utility–customer relationship and new propositions are being developed for electricity consumers. For example, in Australia, Sumo Power is borrowing from concepts in other sectors by offering an “all you can eat” energy contracts,20 which gives the customer cost certainty and avoids the prospect of unexpectedly high bills. But there is scope for further developments and innovation in this relationship.

Electricity will not be going out of fashion anytime soon. As a whole, its value to society is growing as electrification increases. The question is whether the existing companies will retain their customer-facing role, or become someone else’s outsourcing partner for top-up kWh. To remain viable, companies within the sector today need to adapt to keep ahead. That means changing the way business is conducted and focusing on the needs and wishes of customers before someone else does.

This theme is the focus of many of the accompanying chapters, which explore specific examples of innovation and disruption on future business models.