Solving and Simulating Models with Heterogeneous Agents and Aggregate Uncertainty

Yann Algana, Olivier Allaisb, Wouter J. Den Haanc, d and Pontus Rendahle, aSciences Po, Paris, France, bINRA, UR1303 ALISS, Ivry-sur-Seine, France, cCentre for Macroeconomics, London School of Economics, London, UK, dCEPR, London, UK, eCentre for Macroeconomics, University of Cambridge, Cambridge, UK, a [email protected], b [email protected], d [email protected], e [email protected]

Abstract

Although almost nonexistent 15 years ago, there are now numerous papers that analyze models with both aggregate uncertainty and a large number—typically a continuum—of heterogeneous agents. These models make it possible to study whether macroeconomic fluctuations affect different agents differently and whether heterogeneity in turn affects macroeconomic fluctuations. This chapter reviews different algorithms to solve and simulate these models. In addition, it highlights problems with popular accuracy tests and discusses more powerful alternatives.

Keywords

Incomplete markets; Numerical solutions; Projection methods; Perturbation methods; Parameterized densities; Accuracy tests

JEL Classification Codes

C63; D52

1 Introduction

The development of computational algorithms to solve economic models with heterogeneous agents and aggregate uncertainty started in the second half of the 1990s. Early examples are Campbell (1998), Den Haan (1996, 1997), and Krusell and Smith (1997, 1998).1 The presence of aggregate uncertainty implies that the cross-sectional distribution of agents’ characteristics is time varying and, thus, has to be included in the set of state variables. This implies that the individual policy rules depend on a large number of arguments, unless the number of agents is small. In particular, under the common assumption that there is a continuum of agents, the set of state variables would be infinite dimensional. A common feature of existing algorithms is to summarize this infinite-dimensional object with a limited set of statistics that summarize the distribution.

Krusell and Smith (1998) consider a model in which employment risk is not fully insurable because of borrowing constraints and missing insurance markets. They show that in this environment the model satisfies the approximate aggregation property, that is, the mean of the capital stock is a sufficient statistic to predict next period’s prices accurately.2 The reason for this important finding is that the marginal propensity to save is very similar across agents with different income and wealth levels—except for the very poor. Since there are not many poor agents and their wealth is small, the similarity of the marginal propensity to save of the other agents implies that redistributions of wealth have no effect on aggregate savings and, thus, not on market prices. This is quite a general result and remains valid if, for example, the amount of idiosyncratic risk is increased. Important is that the amount of aggregate savings is endogenous. This implies that the average agent can build up a wealth level that is so high that the chance of the constraint being binding is small. Den Haan (1997) considers a model in which aggregate savings are zero. In this model, the borrowing constraint is more frequently binding and higher-order moments do matter. Krusell and Smith (2006) say in their conclusion that “we foresee important examples of such phenomena [i.e., quantitatively convincing models with large departures from approximate aggregation] to be discovered in future research.” Such models will, without doubt, be harder to solve, and as we move into solving more complex models, the need for alternative algorithms and careful testing of accuracy becomes more important.

Existing algorithms differ in important aspects from each other. While the first algorithms relied heavily on simulation procedures, the newer attempts try to build algorithms using building blocks proven to be fruitful in the numerical literature such as projection methods and perturbation techniques.

In addition to reviewing solution algorithms, this chapter also reviews different procedures to simulate economies with a continuum of agents. Simulations are an essential ingredient in several of the algorithms and typically are important even when the algorithms themselves do not rely on simulations. The reason is that many properties of the model can only be calculated through simulation. With a continuum of agents, simulation is nontrivial. In the most commonly used procedure, the continuum of agents is approximated with a large but finite number of agents. This introduces unnecessary sampling variation that may be substantial for some groups of the population. We review several alternative procedures that are more accurate and faster.

Another important topic of this chapter is a discussion on how to check for accuracy. The standard procedure to check for accuracy is to use the ![]() or the standard error of the regression, the two accuracy measures that Krusell and Smith (1998) focus on. Den Haan (2010a) shows that these are very weak measures. In particular, it is shown that aggregate laws of motion that differ substantially from each other in important dimensions can all have a very high

or the standard error of the regression, the two accuracy measures that Krusell and Smith (1998) focus on. Den Haan (2010a) shows that these are very weak measures. In particular, it is shown that aggregate laws of motion that differ substantially from each other in important dimensions can all have a very high ![]() and a low regression standard error. Den Haan (2010a) also proposes an alternative accuracy test that is more powerful. Note that Krusell and Smith (1996, 1998) actually consider several alternative accuracy measures. One of them, the maximum forecast error at a long forecast horizon, turns out to be much more powerful in detecting inaccuracies than the

and a low regression standard error. Den Haan (2010a) also proposes an alternative accuracy test that is more powerful. Note that Krusell and Smith (1996, 1998) actually consider several alternative accuracy measures. One of them, the maximum forecast error at a long forecast horizon, turns out to be much more powerful in detecting inaccuracies than the ![]() and the standard error.

and the standard error.

This chapter is organized as follows. In Section 2, we describe the model that we use to illustrate the different algorithms. In Sections 3 and 6, we describe the numerical solution and the numerical simulation procedures, respectively. In Section 4, we discuss the importance of ensuring that the numerical solution satisfies market clearing. In Section 5, we discuss the result from Krusell and Smith (1998) that the mean capital stock is a sufficient statistic, i.e., approximate aggregation. In Section 7, we discuss accuracy tests, and in Section 8, we compare the properties of the different algorithms. The last section concludes.

2 Example Economy

The model described in this section is an extension of Krusell and Smith (1998).3 Its relative simplicity makes it very suitable to illustrate the key features of the different algorithms. Another reason to focus on this model is that its aggregation properties have been quite influential.

Problem for the Individual Agent

The economy consists of a continuum of ex ante identical households with unit mass. Each period, agents face an idiosyncratic shock ![]() that determines whether they are employed,

that determines whether they are employed, ![]() , or unemployed,

, or unemployed, ![]() . An employed agent earns an after-tax wage rate of

. An employed agent earns an after-tax wage rate of ![]() and an unemployed agent receives unemployment benefits

and an unemployed agent receives unemployment benefits ![]() .4 Markets are incomplete and agents can only save through capital accumulation. The net rate of return on investment is equal to

.4 Markets are incomplete and agents can only save through capital accumulation. The net rate of return on investment is equal to ![]() , where

, where ![]() is the rental rate and

is the rental rate and ![]() is the depreciation rate. Agent

is the depreciation rate. Agent ![]() ’s maximization problem is as follows:

’s maximization problem is as follows:

(1)

(1)

Here ![]() is the individual level of consumption,

is the individual level of consumption, ![]() is the agent’s beginning-of-period capital, and

is the agent’s beginning-of-period capital, and ![]() is the time endowment. We set

is the time endowment. We set ![]() equal to 1 to simplify the notation.

equal to 1 to simplify the notation.

The Euler equation error, ![]() , is defined as

, is defined as

![]() (2)

(2)

and the first-order conditions of the agent are given by

(3)

(3)

Firm Problem

Markets are competitive and the production technology of the firm is characterized by a constant-returns-to-scale Cobb-Douglas production function. Consequently, firm heterogeneity is not an issue. Let ![]() and

and ![]() stand for the per capita capital stock and the employment rate, respectively. Per capita output is given by

stand for the per capita capital stock and the employment rate, respectively. Per capita output is given by

![]() (4)

(4)

and prices by

![]() (5)

(5)

![]() (6)

(6)

Aggregate productivity, ![]() , is an exogenous stochastic process that can take on two values,

, is an exogenous stochastic process that can take on two values, ![]() and

and ![]() .

.

Government

The only role of the government is to tax employed agents and to redistribute funds to the unemployed. We assume that the government’s budget is balanced each period. This implies that the tax rate is equal to

![]() (7)

(7)

where ![]() denotes the unemployment rate in period

denotes the unemployment rate in period ![]() .

.

Exogenous Driving Processes

There are two stochastic driving processes. The first is aggregate productivity and the second is the employment status. Both are assumed to be first-order Markov processes. We let ![]() stand for the probability that

stand for the probability that ![]() and

and ![]() when

when ![]() and

and ![]() . These transition probabilities are chosen such that the unemployment rate can take on only two values. That is,

. These transition probabilities are chosen such that the unemployment rate can take on only two values. That is, ![]() when

when ![]() and

and ![]() when

when ![]() with

with ![]() .5

.5

Equilibrium

Krusell and Smith (1998) consider recursive equilibria in which the policy functions of the agent depend on his employment status, ![]() , his beginning-of-period capital holdings,

, his beginning-of-period capital holdings, ![]() , aggregate productivity,

, aggregate productivity, ![]() , and the cross-sectional distribution of capital holdings,

, and the cross-sectional distribution of capital holdings, ![]() .6 An equilibrium consists of the following elements:

.6 An equilibrium consists of the following elements:

1. Individual policy functions that solve the agent’s maximization problem for given laws of motion of ![]() and

and ![]() .

.

2. A rental and a wage rate that are determined by Eqs. (5) and (6), respectively.

3. A transition law for the cross-sectional distribution of capital that is consistent with the individual policy function. We let ![]() represent the beginning-of-period cross-sectional distribution of capital and the employment status after the employment status has been realized. The transition law can be written as

represent the beginning-of-period cross-sectional distribution of capital and the employment status after the employment status has been realized. The transition law can be written as

![]() (8)

(8)

This law of motion reveals an advantage of working with a continuum of agents. The idea is to rely on a law of large numbers, so that conditional on ![]() there is no uncertainty about

there is no uncertainty about ![]() .7

.7

3 Algorithms—Overview

There are now several algorithms to solve models with heterogeneous agents and aggregate uncertainty using a wide range of different tools from the numerical solution literature. They include algorithms that use only perturbation techniques like Preston and Roca (2006); algorithms that use only projection methods like Den Haan (1997) and Den Haan and Rendahl (2010); as well as several others that combine different tools such as Den Haan (1996), Krusell and Smith (1998), Algan et al. (2008), Reiter (2009), and Reiter (2010). This section is split in two parts. Section 3.1 discusses procedures that rely on projection approaches, possibly combined with a simulation procedure. These are global procedures in the sense that properties of the model in different parts of the state space affect the numerical solution. Section 3.2 discusses perturbation approaches in which the numerical solution is pinned down by the derivatives at one particular point. The purpose of this section is to explain—hopefully in an intuitive manner—the key aspects of the different algorithms.

3.1 Projection and Simulation Approaches

This section discusses four quite different approaches. It discusses the approach of Krusell and Smith (1998) in which simulations are used to determine the aggregate laws of motion; the approach developed in Den Haan (1996), which is a pure simulation approach; the approach of Algan et al. (2008), which is based mainly on projection methods8; and finally the approach developed in Den Haan and Rendahl (2010), which uses only projection methods. As discussed above, we focus on equilibria in which (i) individual policy functions depend on ![]() and (ii) the next period’s cross-sectional distribution is a time-invariant function of the current distribution and the aggregate shock. All existing algorithms summarize the information of the cross-sectional distribution with a finite set of elements.

and (ii) the next period’s cross-sectional distribution is a time-invariant function of the current distribution and the aggregate shock. All existing algorithms summarize the information of the cross-sectional distribution with a finite set of elements.

3.1.1 Obtain Aggregate Policy Functions from Simulation

The most popular algorithm used in the literature is the one developed in Krusell and Smith (1998). They approximate the infinite-dimensional cross-sectional distribution with a finite set of moments, ![]() .9 An approximate solution then consists of an individual policy function (as a function of the vector

.9 An approximate solution then consists of an individual policy function (as a function of the vector ![]() ) and a law of motion for

) and a law of motion for ![]() of the form

of the form

![]() (9)

(9)

The idea underlying this algorithm is fairly straightforward. Notice that the problem of solving for the individual policy rules is standard and one can use any of the available algorithms.10 In solving for the individual policy functions, one will run into the problem of evaluating next period’s prices, which depend on next period’s aggregate capital stock, but this can be calculated using the mapping ![]() . The algorithm then proceeds using the following iterative scheme:

. The algorithm then proceeds using the following iterative scheme:

1. Start with an initial guess for ![]() , say

, say ![]() .

.

2. Using this guess, solve for the individual policy rule.

3. Construct a time series for ![]() . That is, using the solution for the individual policy rule, simulate the economy using one of the simulation techniques discussed in Section 6. For each period calculate the elements of

. That is, using the solution for the individual policy rule, simulate the economy using one of the simulation techniques discussed in Section 6. For each period calculate the elements of ![]() from the cross-sectional distribution.

from the cross-sectional distribution.

4. Use least squares to obtain a new estimate for the law of motion ![]() . This is

. This is ![]() .

.

3.1.2 Obtain Aggregate and Individual Policy Functions Through Simulation

As in Krusell and Smith (1998), Den Haan (1996) also assumes that the cross-sectional distribution is characterized by a finite set of moments, ![]() . He solves for the individual policy rules from a simulation procedure, which avoids having to specify an approximating law of motion for the transition of

. He solves for the individual policy rules from a simulation procedure, which avoids having to specify an approximating law of motion for the transition of ![]() .11

.11

Den Haan (1996) parameterizes the conditional expectation, but it is also possible to approximate the consumption or the capital choice. With this approximation, the optimality conditions of the agent can be written as

![]() (10)

(10)

![]() (11)

(11)

(12)

(12)

where ![]() is a flexible functional form of order

is a flexible functional form of order ![]() with coefficient vector

with coefficient vector ![]() .12 The algorithm works as follows:

.12 The algorithm works as follows:

1. Start with an initial guess for the parameterized conditional expectation, characterized by its coefficients, ![]() . Note that this is equivalent to having the individual policy functions for consumption and capital.

. Note that this is equivalent to having the individual policy functions for consumption and capital.

2. Use the individual policy rule to simulate a time series for ![]() and the choices for one agent. That is, we obtain a time series for

and the choices for one agent. That is, we obtain a time series for ![]() . Prices can be calculated using the observed cross-sectional mean capital stock. Let

. Prices can be calculated using the observed cross-sectional mean capital stock. Let ![]() be equal to

be equal to

![]() (13)

(13)

Note that

![]() (14)

(14)

where ![]() is a prediction error that is orthogonal to the variables in the time

is a prediction error that is orthogonal to the variables in the time ![]() information set.13 This means one can use nonlinear least squares to get a new estimate of

information set.13 This means one can use nonlinear least squares to get a new estimate of ![]() .

.

This procedure is similar to the one used by Krusell and Smith (1998), but it does not require specifying an approximation to the law of motion for the moments that are used as state variables. The reason is the following. Krusell and Smith (1998) use the approximation to the aggregate law of motion to describe next period’s prices in terms of next period’s value of ![]() and this period’s moments. If one projects

and this period’s moments. If one projects ![]() on

on ![]() , then this transition law is automatically taken into account without having specified a particular functional form to describe it.

, then this transition law is automatically taken into account without having specified a particular functional form to describe it.

3.1.3 Obtain Aggregates by Integrating over a Parameterized Distribution

Next, we discuss the algorithm of Den Haan (1997) and the improved version developed in Algan et al. (2008). As in Den Haan (1996), the conditional expectation of the individual agent is parameterized and the objective is to solve for the value of ![]() . Moreover, the cross-sectional distribution is characterized with a finite set of moments,

. Moreover, the cross-sectional distribution is characterized with a finite set of moments, ![]() , and the state variables are, thus, again given by

, and the state variables are, thus, again given by ![]() , and

, and ![]() . Nevertheless, these are very different algorithms. Whereas Den Haan (1996) is based on simulations, the algorithm of Den Haan (1997) uses textbook projection methods. A textbook projection procedure consists of (i) a grid in the state variables, (ii) a quadrature procedure to calculate the conditional expectation in Eq. (2), and (iii) an equation solver to find the coefficients of the approximating function for which the errors on the grid are equal to zero.14

. Nevertheless, these are very different algorithms. Whereas Den Haan (1996) is based on simulations, the algorithm of Den Haan (1997) uses textbook projection methods. A textbook projection procedure consists of (i) a grid in the state variables, (ii) a quadrature procedure to calculate the conditional expectation in Eq. (2), and (iii) an equation solver to find the coefficients of the approximating function for which the errors on the grid are equal to zero.14

For the type of problem considered in this paper, it is not straightforward to solve the model using standard projection techniques. Some additional information is required. To understand why, consider a particular grid point, that is, a particular combination of ![]() , and

, and ![]() . Calculation of

. Calculation of

![]()

requires knowing the aggregate capital stock, ![]() . To calculate

. To calculate ![]() at a particular grid point requires not only knowing

at a particular grid point requires not only knowing ![]() (and

(and ![]() ), but typically requires knowing the actual distribution.15 Den Haan (1997) deals with this problem by parameterizing the cross-sectional distribution. Conditional on a particular functional form, say the exponential of an nth-order polynomial, there is a mapping between the

), but typically requires knowing the actual distribution.15 Den Haan (1997) deals with this problem by parameterizing the cross-sectional distribution. Conditional on a particular functional form, say the exponential of an nth-order polynomial, there is a mapping between the ![]() values of

values of ![]() and the coefficients of the approximating density,

and the coefficients of the approximating density, ![]() . For example, if one uses a second-order exponential, i.e., a Normal density, then the mean and the variance pin down the two elements of

. For example, if one uses a second-order exponential, i.e., a Normal density, then the mean and the variance pin down the two elements of ![]() .16 Given the parameterization

.16 Given the parameterization ![]() , the conditional expectation can be calculated using standard quadrature techniques and standard projection methods can be used to solve for the coefficients of the individual policy rule,

, the conditional expectation can be calculated using standard quadrature techniques and standard projection methods can be used to solve for the coefficients of the individual policy rule, ![]() .17

.17

Reference Moments/Distribution

The description so far assumes that the order of the approximation of the cross-sectional density is directly related to the moments included. That is, if ![]() moments are used as state variables, then an nth-order approximation is used to approximate the cross-sectional density (and vice versa). But this may be inefficient. For example, it may be the case that only first- and second-order moments are needed as state variables, but that (for the particular class of approximating polynomials chosen) a much higher-order approximation is needed to get the shape of the cross-sectional distribution right.

moments are used as state variables, then an nth-order approximation is used to approximate the cross-sectional density (and vice versa). But this may be inefficient. For example, it may be the case that only first- and second-order moments are needed as state variables, but that (for the particular class of approximating polynomials chosen) a much higher-order approximation is needed to get the shape of the cross-sectional distribution right.

Algan et al. (2008, 2010) improve upon Den Haan (1997) and deal with this inefficiency by introducing “reference” moments that are characteristics of the distribution exploited to pin down its shape, but are not used as state variables.18 Let ![]() , where

, where ![]() consists of (lower-order) moments that serve as state variables and are used to construct the grid and where

consists of (lower-order) moments that serve as state variables and are used to construct the grid and where ![]() consists of higher-order reference moments. On the grid, the values of the reference moments,

consists of higher-order reference moments. On the grid, the values of the reference moments, ![]() , are calculated as a function of

, are calculated as a function of ![]() and

and ![]() using an approximating function

using an approximating function ![]() .19 Algan et al. (2008, 2010) find this mapping by simulating a time series for

.19 Algan et al. (2008, 2010) find this mapping by simulating a time series for ![]() , but this is the only role for simulations in their algorithm. A numerical solution has to be such that the relationship between reference moments and other state variables is consistent with the one that comes out of the simulation.

, but this is the only role for simulations in their algorithm. A numerical solution has to be such that the relationship between reference moments and other state variables is consistent with the one that comes out of the simulation.

Histogram as Reference Distribution

The algorithm of Reiter (2010) is similar to that of Algan et al. (2008, 2010), but differs in its implementation. Reiter (2010) characterizes the cross-sectional distribution using a histogram and obtains a complete reference distribution from the simulation. The reference distribution, together with the values of the moments included as state variables, is then used to construct a new histogram that is consistent with the values of the state variables and “close” to the reference distribution itself. Next period’s values of the cross-sectional moments are calculated by integrating over this histogram.

3.1.4 Obtain Aggregates by Explicit Aggregation

The idea of the algorithm of Den Haan and Rendahl (2010) is to derive the aggregate laws of motion directly from the individual policy rules simply by integrating them without using information about the cross-sectional distribution. Before we describe the algorithm, it will be useful to explain the relationship between the individual policy function and the set of moments that should be included as state variables in the exact solution. Krusell and Smith (2006) show that one often can get an accurate solution by using only first-order moments to characterize the distribution. The fact that individual policy functions of the models considered are close to being linear, except possibly for rare values of the state variables, is important for this result. Here we address the question how many moments one has to include to get the exact solution if the individual policy function is (nearly) linear or nonlinear.

Relationship Between Individual Policy Rule and Aggregate Moments to Include

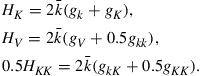

Suppose that the individual policy functions for the employed and the unemployed agent can be written as

(15)

(15)

where ![]() is a vector containing the aggregate state variables

is a vector containing the aggregate state variables ![]() and

and ![]() . Note that (i) the individual policy functions are polynomials in the individual state variables, but the specification allows for more general dependence in the employment status and the aggregate state variables, and (ii) the left-hand side is the level of the capital stock and not, for example, the logarithm.20 Our argument does not rely on the use of polynomials. Other basis functions could be used, including those that generate splines. The logic of the algorithm is easiest understood, however, if the policy function are polynomials in the levels of the individual state variables.

. Note that (i) the individual policy functions are polynomials in the individual state variables, but the specification allows for more general dependence in the employment status and the aggregate state variables, and (ii) the left-hand side is the level of the capital stock and not, for example, the logarithm.20 Our argument does not rely on the use of polynomials. Other basis functions could be used, including those that generate splines. The logic of the algorithm is easiest understood, however, if the policy function are polynomials in the levels of the individual state variables.

The immediate objective is to calculate end-of-period values of the aggregate state, given the beginning-of-period values.21 For the policy function given in Eq. (15), which is linear in the coefficients of the ![]() terms, one can simply integrate across individuals to get

terms, one can simply integrate across individuals to get

(16)

(16)

where ![]()

![]() is the ith uncentered moment of beginning(end)-of-period capital holdings of agents with employment status

is the ith uncentered moment of beginning(end)-of-period capital holdings of agents with employment status ![]() .

.

The first lesson to learn from these expressions is that if the individual policy rule is an Ith-order polynomial, one has to include at least the first ![]() moments of both types of agents as state variables. Thus,

moments of both types of agents as state variables. Thus,

![]() (17)

(17)

where ![]() is the ith cross-sectional moment of individual capital holdings for agents with employment status

is the ith cross-sectional moment of individual capital holdings for agents with employment status ![]() .

.

We now address the question whether this set of moments is enough. First, consider the case when ![]() , that is, the individual policy rule is linear in

, that is, the individual policy rule is linear in ![]() . Then

. Then ![]() is equal to

is equal to ![]() and the expressions in (16) are—together with the value of

and the expressions in (16) are—together with the value of ![]() —sufficient to calculate

—sufficient to calculate ![]() . Conditional on the individual policy rule being linear, the model with heterogeneous agents and aggregate uncertainty can be solved using standard projection techniques, without relying on simulation procedures or an approximation of the cross-sectional distribution.

. Conditional on the individual policy rule being linear, the model with heterogeneous agents and aggregate uncertainty can be solved using standard projection techniques, without relying on simulation procedures or an approximation of the cross-sectional distribution.

The situation is substantially more complicated if there is just a little bit of nonlinearity. For simplicity, suppose that ![]() . From the discussion above we know that a minimum specification for

. From the discussion above we know that a minimum specification for ![]() would be

would be ![]() . This means that to determine

. This means that to determine ![]() we need expressions for

we need expressions for ![]() and

and ![]() . Using Eq. (15) with

. Using Eq. (15) with ![]() we get

we get

(18)

(18)

Aggregation of this expression gives us the moments we need, but aggregation of the right-hand side implies that we have to include the first four moments instead of the first two as state variables, that is,

![]()

This means that to determine ![]() we need expressions for

we need expressions for ![]() and

and ![]() , which in turn implies that we need even more additional elements in

, which in turn implies that we need even more additional elements in ![]() . The lesson learned is that whenever

. The lesson learned is that whenever ![]() one has to include an infinite set of moments as state variables to get an exact solution, even if there are only minor nonlinearities.

one has to include an infinite set of moments as state variables to get an exact solution, even if there are only minor nonlinearities.

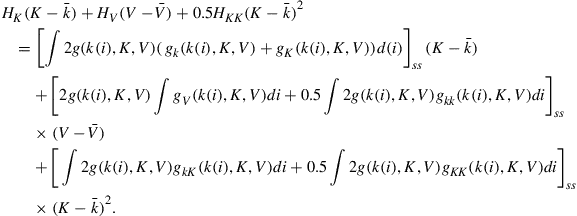

Algorithm of Den Haan and Rendahl (2010)

The key step in the algorithm of Den Haan and Rendahl (2010) is to break the infinite regress problem by approximating the policy rules that are needed to determine next period’s aggregate state using lower-order polynomials. Consider again the case with ![]() . If we break the chain immediately at

. If we break the chain immediately at ![]() , then

, then ![]() is obtained from the approximation

is obtained from the approximation

![]() (19)

(19)

and not from Eq. (18). Note that ![]() in Eq. (19) is not equal to

in Eq. (19) is not equal to ![]() . The

. The ![]() subscript in

subscript in ![]() indicates that the coefficients in the approximating relationship in Eq. (19) are not obtained from the

indicates that the coefficients in the approximating relationship in Eq. (19) are not obtained from the ![]() coefficients as in Eq. (18), but from a separate projection of

coefficients as in Eq. (18), but from a separate projection of ![]() on the space of included terms. The coefficients

on the space of included terms. The coefficients ![]() are chosen to get the best fit for

are chosen to get the best fit for ![]() according to some measure. Given that the excluded terms, i.e.,

according to some measure. Given that the excluded terms, i.e., ![]() and

and ![]() , are correlated with the included terms, these coefficients will also capture some of the explanatory power of the higher-order excluded terms. The key implication of using Eq. (19) instead of Eq. (18) is that aggregation of Eq. (19) does not lead to an increase in the set of aggregate state variables.

, are correlated with the included terms, these coefficients will also capture some of the explanatory power of the higher-order excluded terms. The key implication of using Eq. (19) instead of Eq. (18) is that aggregation of Eq. (19) does not lead to an increase in the set of aggregate state variables.

For ![]() the numerical algorithm consists of the following steps. The variables on the grid are

the numerical algorithm consists of the following steps. The variables on the grid are ![]() . With the use of Eqs. (16) and (19), the error terms defined in Eq. (2) can be calculated given values for

. With the use of Eqs. (16) and (19), the error terms defined in Eq. (2) can be calculated given values for ![]() and

and ![]() . The algorithm chooses those values for the coefficients that minimize some objective function of the errors defined in Eq. (2).

. The algorithm chooses those values for the coefficients that minimize some objective function of the errors defined in Eq. (2).

To get expressions for next period’s aggregate variables using explicit aggregation, one has to break the infinite regress at some point. One could break it at ![]() as in the example above, but one also could break it at some higher level. For example, suppose again that the individual policy rule is approximated well with a second-order polynomial. One possibility would be to set

as in the example above, but one also could break it at some higher level. For example, suppose again that the individual policy rule is approximated well with a second-order polynomial. One possibility would be to set ![]() and approximate

and approximate ![]() ,

, ![]() ,

, ![]() , and

, and ![]() using fourth-order polynomials. But an alternative would be to approximate

using fourth-order polynomials. But an alternative would be to approximate ![]() with a second-order polynomial as above, using Eq. (18)—i.e., the exact expression given the policy rule for

with a second-order polynomial as above, using Eq. (18)—i.e., the exact expression given the policy rule for ![]() , to describe

, to describe ![]() —and construct approximations for

—and construct approximations for ![]() and

and ![]() using fourth-order polynomials.

using fourth-order polynomials.

Separate Individual Policy Rule for Aggregation

It is possible that a high-order polynomial is needed to accurately describe individual behavior for all possible values of ![]() . Using this algorithm would then require a lot of aggregate state variables, since every monomial in the approximating function corresponds to an additional aggregate state variable. However, one can use a complex approximation to describe individual behavior and one can use a simpler individual policy rule just to aggregate and obtain the aggregate laws of motion. In fact, Den Haan and Rendahl (2010) approximate individual policy rule with a spline,22 but obtain the aggregate law of motion by aggregating a simple linear approximation of the individual policy rule, and show that they can get an accurate solution with this approach.

. Using this algorithm would then require a lot of aggregate state variables, since every monomial in the approximating function corresponds to an additional aggregate state variable. However, one can use a complex approximation to describe individual behavior and one can use a simpler individual policy rule just to aggregate and obtain the aggregate laws of motion. In fact, Den Haan and Rendahl (2010) approximate individual policy rule with a spline,22 but obtain the aggregate law of motion by aggregating a simple linear approximation of the individual policy rule, and show that they can get an accurate solution with this approach.

3.2 Perturbation Approaches

In this section, we discuss two perturbation procedures. The procedure developed by Preston and Roca (2006) is a “pure” implementation of the perturbation procedure. We will see that the order of the implementation used implies which moments of the cross-sectional distribution should be included. For the perturbation procedure of Preston and Roca (2006), the nonstochastic steady state, around which the solution is perturbed, corresponds to the model solution when both aggregate and idiosyncratic uncertainty are equal to zero. The algorithm of Reiter (2009) combines a perturbation procedure with projection elements, which makes it possible to perturb the model around the solution of the model without aggregate uncertainty but with individual uncertainty.

Perturbation methods have the advantage of being fast and since they do not require the specification of a grid allow for many state variables. Also, projection methods require several choices of the programmer, especially in the construction of the grid, whereas implementation with perturbation techniques is more standard. Perturbation methods also have disadvantages. Since they are based on a Taylor series expansion around the steady state, the policy functions are required to be sufficiently smooth. Den Haan and De Wind (2009) discuss another disadvantage. Perturbation approximations are polynomials and, thus, display oscillations.23 As argued in Den Haan and De Wind (2009), the problem of perturbation procedures is that one cannot control where the oscillations occur.24 They could occur close to the steady state and lead to explosive solutions.

3.2.1 Perturbation Around Scalar Steady State Values

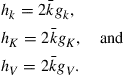

Preston and Roca (2006) show how to solve models with aggregate uncertainty and heterogeneous agents with a perturbation procedure. The steady state they consider is the solution of the model when there is no aggregate uncertainty and when there is no idiosyncratic uncertainty.

There are some particular features of the model described above that makes it less suited for perturbation procedures. So we will modify the problem slightly. The idea of perturbation procedures is to take a local approximation around the point where there is no uncertainty and then introduce the amount of uncertainty as an explicit variable in the policy function of the agent. Since perturbation techniques rely on the implicit function theorem, uncertainty should affect the problem in a smooth way. In the problem described in Section 2, one can characterize the amount of uncertainty with the probability of becoming unemployed. But even an increase in the probability of becoming unemployed from zero to a slightly positive number introduces sudden discontinuous jumps in the budget set if the individual employment status, ![]() , switches from 0 to 1. If one wants to use a perturbation technique, it is safer to let the support of

, switches from 0 to 1. If one wants to use a perturbation technique, it is safer to let the support of ![]() increase continuously with the perturbation parameter that controls uncertainty.25 Preston and Roca (2006) assume that the law of motion for

increase continuously with the perturbation parameter that controls uncertainty.25 Preston and Roca (2006) assume that the law of motion for ![]() is given by

is given by

![]() (20)

(20)

where ![]() has variance

has variance ![]() .26,27 Similarly, let the law of motion for

.26,27 Similarly, let the law of motion for ![]() be given by

be given by

![]() (21)

(21)

Perturbation techniques cannot deal with inequality constraints, because they could never be captured with the derivatives at the steady state. The inequality constraint is, therefore, replaced by a smooth penalty function that makes it costly to have low capital levels. In particular, Preston and Roca (2006) assume that there is a utility cost of holding ![]() equal to

equal to ![]() .28 The first-order conditions of the agents can then be written as

.28 The first-order conditions of the agents can then be written as

(22)

(22)

![]() (23)

(23)

The order of the perturbation approximation and the set of state variables are related to each other. If a second-order approximation is used then—as will be explained below—the state variables for the agent are ![]() with

with

![]() (24)

(24)

where

![]() (25)

(25)

![]() (26)

(26)

![]() (27)

(27)

![]() (28)

(28)

That is, first- and second-order moments of the cross-sectional distribution are included. If a first-order approximation is used, then only first-order moments are included.

Let ![]() be the policy function for variable

be the policy function for variable ![]() with

with ![]() . To get the perturbation solution, we write the model as follows:

. To get the perturbation solution, we write the model as follows:

![]() (29a)

(29a)

![]() (29b)

(29b)

![]() (29c)

(29c)

![]() (29d)

(29d)

![]() (29e)

(29e)

Here, ![]() is the steady-state value of capital and

is the steady-state value of capital and ![]() is a scalar parameter that scales both types of uncertainty,

is a scalar parameter that scales both types of uncertainty, ![]() and

and ![]() . The variables

. The variables ![]() ,

, ![]() , and

, and ![]() are given by

are given by

![]() (30)

(30)

![]() (31)

(31)

(32)

(32)

Because of the aggregation constraints, i.e., Eqs. (29c), (29d), and (29e), it is important that the solution is specified in the nontransformed level of the variables and not, for example, in logs.29 If not, then the functional forms of ![]() , and

, and ![]() would not be consistent with the functional forms of

would not be consistent with the functional forms of ![]() and

and ![]() . The aggregation constraint makes clear what the list of state variables should be for the particular approximation order chosen. That is, a particular approximation implies a particular law of motion for the cross-sectional income and wealth distribution, which in turn implies what the relevant state variables are.

. The aggregation constraint makes clear what the list of state variables should be for the particular approximation order chosen. That is, a particular approximation implies a particular law of motion for the cross-sectional income and wealth distribution, which in turn implies what the relevant state variables are.

Suppose that one uses a first-order approximation. Clearly, ![]() and

and ![]() matter for the individual policy functions. The agent also cares about prices and, thus, about

matter for the individual policy functions. The agent also cares about prices and, thus, about ![]() , and future values of

, and future values of ![]() . When the savings function is linear in

. When the savings function is linear in ![]() , and

, and ![]() , then the aggregation restriction (together with the linearity of the policy function) implies that

, then the aggregation restriction (together with the linearity of the policy function) implies that ![]() is linear in these variables as well, and that other moments of the cross-sectional distribution, thus, should not be included.

is linear in these variables as well, and that other moments of the cross-sectional distribution, thus, should not be included.

If the individual policy functions are second order and in particular include ![]() and

and ![]() , then the aggregation constraint implies that next period’s capital stock depends on

, then the aggregation constraint implies that next period’s capital stock depends on ![]() and

and ![]() , which means that these should be included as state variables as well.30

, which means that these should be included as state variables as well.30

When Eqs. (30)–(32) are used to substitute out ![]() , and

, and ![]() , then Eq. (29) specifies a set of five equations in five functions:

, then Eq. (29) specifies a set of five equations in five functions: ![]() ,

, ![]() , and

, and ![]() . Sequentially differentiating the five equations and evaluating the expressions at the steady state gives the equations with which to solve for the coefficients of the Taylor expansions of the five policy functions. In the appendix, we give an example.

. Sequentially differentiating the five equations and evaluating the expressions at the steady state gives the equations with which to solve for the coefficients of the Taylor expansions of the five policy functions. In the appendix, we give an example.

Perturbation approximations specify complete polynomials.31 This means that the term ![]() is not combined with any other state variables in a second-order approximation, because it is itself a second-order term. Similarly,

is not combined with any other state variables in a second-order approximation, because it is itself a second-order term. Similarly, ![]() and

and ![]() only appear by themselves since they are also second-order terms.

only appear by themselves since they are also second-order terms.

Comparison with Explicit Aggregation

The explicit aggregation algorithm of Den Haan and Rendahl (2010) and the perturbation algorithm of Preston and Roca (2006) seem to be at the opposite sides of the spectrum of solution algorithms. The algorithm of Den Haan and Rendahl (2010) is a “pure” implementation of projection methods and the algorithm of Preston and Roca (2006) is a “pure” implementation of perturbation techniques.32 There also seem to be nontrivial differences in terms of the structure of the algorithms. To be able to explicitly aggregate the individual policy functions, Den Haan and Rendahl (2010) have to derive additional approximations for the higher-order terms of the individual choices. No such step is present in the algorithm of Preston and Roca (2006).

But there is also a striking similarity between the algorithms: Both Preston and Roca (2006) and Den Haan and Rendahl (2010) derive the law of motion for the aggregate variables directly from the individual policy rules without relying on simulations or numerical integration techniques.

The algorithm of Den Haan and Rendahl (2010) does not take a stand on how to solve for the individual policy rules and these could, in principle, be solved for using perturbation techniques. To understand the connection between the two algorithms, consider the following implementation of the explicit aggregation algorithm. First, suppose the solution to the individual policy rule, ![]() , is obtained using perturbation techniques taking the aggregate policy rule as given. If nth-order perturbation is used, then one has to solve simultaneously for the higher-order policy rules,

, is obtained using perturbation techniques taking the aggregate policy rule as given. If nth-order perturbation is used, then one has to solve simultaneously for the higher-order policy rules, ![]() for

for ![]() . In perturbation software one would simply add

. In perturbation software one would simply add ![]() as additional equations and the

as additional equations and the ![]() variables would appear as additional variables. This would result in a solution for the

variables would appear as additional variables. This would result in a solution for the ![]() variables as a function of

variables as a function of ![]() , that is,

, that is, ![]() . When the aggregate policy rule is given, then this is typically a straightforward simple implementation of perturbation techniques and could be solved using standard software such as Dynare. Second, the solution for the aggregate policy rule is obtained by explicitly aggregating policy rules for

. When the aggregate policy rule is given, then this is typically a straightforward simple implementation of perturbation techniques and could be solved using standard software such as Dynare. Second, the solution for the aggregate policy rule is obtained by explicitly aggregating policy rules for ![]() and

and ![]() . Finally, one would iterate until convergence is achieved. In the appendix, we work out an example to show that the solution obtained with explicit aggregation is in this case identical to the one obtained with the algorithm of Preston and Roca (2006).

. Finally, one would iterate until convergence is achieved. In the appendix, we work out an example to show that the solution obtained with explicit aggregation is in this case identical to the one obtained with the algorithm of Preston and Roca (2006).

The explicit aggregation algorithm of Den Haan and Rendahl (2010) can, thus, be viewed as a general procedure that boils down to the algorithm of Preston and Roca (2006) if the individual policy rules are solved for using perturbation techniques. Moreover, if the individual policy rules are indeed solved with perturbation techniques, then—as was outlined above—the explicit aggregation algorithm suggests a simple way to solve the model using standard perturbation software such as Dynare.

3.2.2 Perturbation Around the Steady State Cross-Sectional Distribution

The procedure of Preston and Roca (2006) perturbs around the point where there is neither aggregate nor idiosyncratic uncertainty. The idea of the procedure in Reiter (2009) is to take a perturbation around the model solution with no aggregate uncertainty.33 This solution consists of a cross-sectional distribution for income and capital levels that is not time varying. We describe the algorithm as a general perturbation problem and in doing so deviate somewhat from the description in Reiter (2009), but the underlying idea is the same.

Consider a numerical solution to the model of Section 2,

![]() (33)

(33)

where ![]() is a vector with the coefficients of the numerical solution for the capital policy function.

is a vector with the coefficients of the numerical solution for the capital policy function. ![]() is an approximating (but fixed) functional form, say an nth-order polynomial. Let the law of motion for

is an approximating (but fixed) functional form, say an nth-order polynomial. Let the law of motion for ![]() be given by

be given by

![]() (34)

(34)

The subscript ![]() makes clear that this law of motion depends on the solution of the individual policy function. That is, a different individual policy rule will imply a different law of motion for the cross-sectional distribution. It is assumed that

makes clear that this law of motion depends on the solution of the individual policy function. That is, a different individual policy rule will imply a different law of motion for the cross-sectional distribution. It is assumed that ![]() is more than a limited set of moments, but pins down—possibly with additional assumptions—the complete cross-sectional distribution. For example,

is more than a limited set of moments, but pins down—possibly with additional assumptions—the complete cross-sectional distribution. For example, ![]() could be the values of a histogram defined on a fine grid.34 This assumption implies that—conditional on the individual policy function—the mapping

could be the values of a histogram defined on a fine grid.34 This assumption implies that—conditional on the individual policy function—the mapping ![]() is known, although implementing it may require some numerical procedures like quadrature integration. In other words, given the choice to approximate the savings function with

is known, although implementing it may require some numerical procedures like quadrature integration. In other words, given the choice to approximate the savings function with ![]() and given the choice to characterize the cross-sectional distribution in a particular way, the only unknown is

and given the choice to characterize the cross-sectional distribution in a particular way, the only unknown is ![]() . As soon as

. As soon as ![]() is known, then all variables, including

is known, then all variables, including ![]() , can be calculated for a given set of initial values and realizations of the shock.

, can be calculated for a given set of initial values and realizations of the shock.

The individual policy function in Eq. (33) can be written without the aggregate state variables, but with time-varying coefficients. That is,

![]() (35)

(35)

with

![]() (36)

(36)

Let ![]() , let the dimension of

, let the dimension of ![]() be given by

be given by ![]() , and let

, and let ![]() be an

be an ![]() vector with nodes for the employment status and capital levels.35 Evaluated at the nodes for the individual state variables,

vector with nodes for the employment status and capital levels.35 Evaluated at the nodes for the individual state variables, ![]() , the first-order conditions of the agent can be written as follows36:

, the first-order conditions of the agent can be written as follows36:

(37)

(37)

In equilibrium, the endogenous part of ![]() , i.e.,

, i.e., ![]() , is determined by

, is determined by

![]() (38)

(38)

where, as mentioned above, ![]() is—conditional on knowing

is—conditional on knowing ![]() —a known function. Suppose that

—a known function. Suppose that ![]() is constant and that

is constant and that ![]() characterizes the corresponding cross-sectional distribution. Evaluated at these constant values for

characterizes the corresponding cross-sectional distribution. Evaluated at these constant values for ![]() and

and ![]() , Eq. (37) is then a standard set of

, Eq. (37) is then a standard set of ![]() equations to solve for the

equations to solve for the ![]() (constant) elements of

(constant) elements of ![]() . But to understand the procedure considered here, it is important to think of Eq. (37), with

. But to understand the procedure considered here, it is important to think of Eq. (37), with ![]() determined by Eq. (38), as a system that defines the vector-valued function

determined by Eq. (38), as a system that defines the vector-valued function ![]() .

.

It is important to understand what is fixed and what we are solving for in this system. First, ![]() has a known functional form, namely, the one chosen as a numerical approximation. In the example considered in Section 2, the stochastic variables

has a known functional form, namely, the one chosen as a numerical approximation. In the example considered in Section 2, the stochastic variables ![]() and

and ![]() have discrete support, so there is an analytical expression for the conditional expectation in Eq. (37). If this is not the case, then a numerical integration procedure has to be used. But for every quadrature procedure chosen, Eq. (37) represents a fixed set of equations. The same is true for Eq. (38). It may be possible that

have discrete support, so there is an analytical expression for the conditional expectation in Eq. (37). If this is not the case, then a numerical integration procedure has to be used. But for every quadrature procedure chosen, Eq. (37) represents a fixed set of equations. The same is true for Eq. (38). It may be possible that ![]() is only implicitly defined by a set of equations. This does not matter. Essential is that there is a fixed set of equations that in principle determines

is only implicitly defined by a set of equations. This does not matter. Essential is that there is a fixed set of equations that in principle determines ![]() .

.

Thus, Eq. (37), with ![]() determined by Eq. (38), is a system in which the coefficients of the approximating individual policy function,

determined by Eq. (38), is a system in which the coefficients of the approximating individual policy function, ![]() , are the variables. That is, instead of consumption and capital being variables, the coefficients of the policy function have become the variables. The idea is now to solve for these functions using the perturbation approach. That is, we write

, are the variables. That is, instead of consumption and capital being variables, the coefficients of the policy function have become the variables. The idea is now to solve for these functions using the perturbation approach. That is, we write ![]() as

as ![]() and its Taylor expansion around the steady state as

and its Taylor expansion around the steady state as

(39)

(39)

As in standard perturbation procedures, we can find the coefficients of the Taylor expansion by taking successive derivatives of Eq. (37).

This procedure assumes that ![]() is more than a very limited set of moments such as the mean capital stock. The elements of

is more than a very limited set of moments such as the mean capital stock. The elements of ![]() should pin down the complete cross-sectional distribution. One possibility would be to let

should pin down the complete cross-sectional distribution. One possibility would be to let ![]() be the set of values of the CDF at a very fine grid. The value of

be the set of values of the CDF at a very fine grid. The value of ![]() is then very large and one has to find the policy function for many variables.37 This could be especially problematic if higher-order perturbation solutions are considered or if

is then very large and one has to find the policy function for many variables.37 This could be especially problematic if higher-order perturbation solutions are considered or if ![]() is a nonlinear function of

is a nonlinear function of ![]() . In this case it may be better to impose some structure on the functional form of the cross-sectional distribution, so that the cross-sectional distribution is fully determined by a smaller set of coefficients. In particular, in Algan et al. (2008) it is shown that a sixth-order polynomial (whose coefficients are pinned down by six moments) describes the cross-sectional distributions generated by the model described in Section 2 through time well.

. In this case it may be better to impose some structure on the functional form of the cross-sectional distribution, so that the cross-sectional distribution is fully determined by a smaller set of coefficients. In particular, in Algan et al. (2008) it is shown that a sixth-order polynomial (whose coefficients are pinned down by six moments) describes the cross-sectional distributions generated by the model described in Section 2 through time well.

4 Models with Nontrivial Market Clearing

As long as the numerical solutions for the model described in Section 2 do not violate the condition that the rental rate and the wage rate are equal to the corresponding marginal products, then the solution is consistent with market clearing in all markets. Using these prices, the firms demand exactly the amount of capital and labor offered by households.

In many other models, it is not true that markets automatically clear exactly for the numerical solution. Nevertheless, market clearing is an important property. Consider a bond economy in which bonds are in zero net supply. Suppose that aggregated across households, the demand for bonds is close to, but not exactly, zero at each point in the state space. It is very unlikely that these small deviations from market clearing will average out as an economy is simulated at a long horizon. Instead, the total amounts of bonds held in the economy are likely to move further and further away from its equilibrium value, and it is not clear how to interpret such an economy given that the solution is based on the economy being in equilibrium.

To understand why market clearing is not automatically imposed exactly when numerically solving a model, consider adding one-period zero-coupon bonds to the economy developed in Section 2 and let the bond price be equal to ![]() . One possibility would be to specify a law of motion for the bond price as a function of the aggregate state variables, that is,

. One possibility would be to specify a law of motion for the bond price as a function of the aggregate state variables, that is, ![]() , and to solve for this law of motion. When simulating the economy, the bond price cannot adjust to ensure market clearing. Of course, a good numerical solution will be such that aggregate demand is close to zero, but—as pointed out above—we would need exact market clearing to prevent errors from accumulating.38

, and to solve for this law of motion. When simulating the economy, the bond price cannot adjust to ensure market clearing. Of course, a good numerical solution will be such that aggregate demand is close to zero, but—as pointed out above—we would need exact market clearing to prevent errors from accumulating.38

There are several ways to impose market clearing. One possibility would be to solve the individual problem using the approximation for ![]() to determine next period’s prices only and to treat the current-period price as a state variable for the individual problem. The individual policy functions are then a function of the bond price and in a simulation the price can be chosen such that the aggregate demand is equal to zero.

to determine next period’s prices only and to treat the current-period price as a state variable for the individual problem. The individual policy functions are then a function of the bond price and in a simulation the price can be chosen such that the aggregate demand is equal to zero.

Instead of solving for the individual demand for bonds, ![]() , Den Haan and Rendahl (2010) propose to solve for the individual demand for bonds plus the bond price, that is,

, Den Haan and Rendahl (2010) propose to solve for the individual demand for bonds plus the bond price, that is, ![]() . The advantage of this approach is that the bond price does not have to be added to the set of state variables. Since aggregate demand is equal to zero in equilibrium, aggregation of these individual choices across individuals gives the bond price. That is,

. The advantage of this approach is that the bond price does not have to be added to the set of state variables. Since aggregate demand is equal to zero in equilibrium, aggregation of these individual choices across individuals gives the bond price. That is,

![]() (40)

(40)

If ![]() is used to determine the individual demand for bonds, then markets clear by construction.

is used to determine the individual demand for bonds, then markets clear by construction.

5 Approximate Aggregation

Krusell and Smith (2006) point out that many models with heterogeneous agents and aggregate risk have the desirable property that the mean values of the cross-sectional distributions are sufficient statistics to predict next period’s prices. They also point out that this property is unlikely to be true for all models to be considered in the future.39 Given that approximate aggregation relies on a limited amount of variation across agents’ marginal propensities to save—a quite unrealistic property—this seems a safe prediction.

It is important to understand what approximate aggregation means and in particular what it does not mean. Approximate aggregation does not imply that the aggregate variables can be approximately described by a representative agent model in which the agent faces sensible preferences, and it definitely does not imply that the aggregate variables can be approximately described by a representative agent model in which the preferences of the representative agent are identical to the preferences of the individual agents in the model with heterogeneous agents.40

Approximate aggregation does not imply that there is perfect insurance and a perfect correlation of individual and aggregate consumption. In fact, even if agents start out with identical wealth levels, then the model of Section 2 generates a substantial amount of cross-sectional dispersion in individual consumption levels.

6 Simulation with a Continuum of Agents

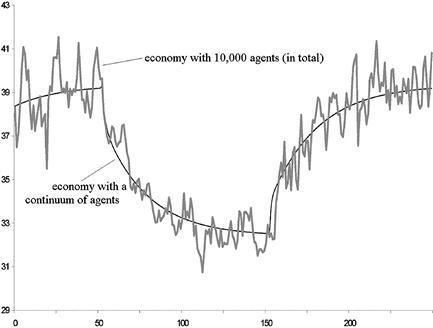

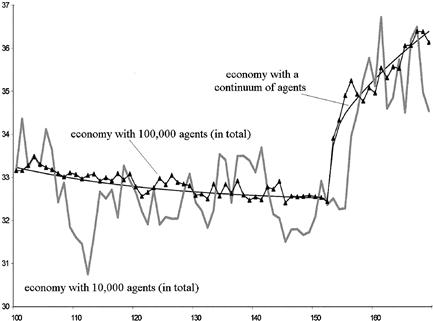

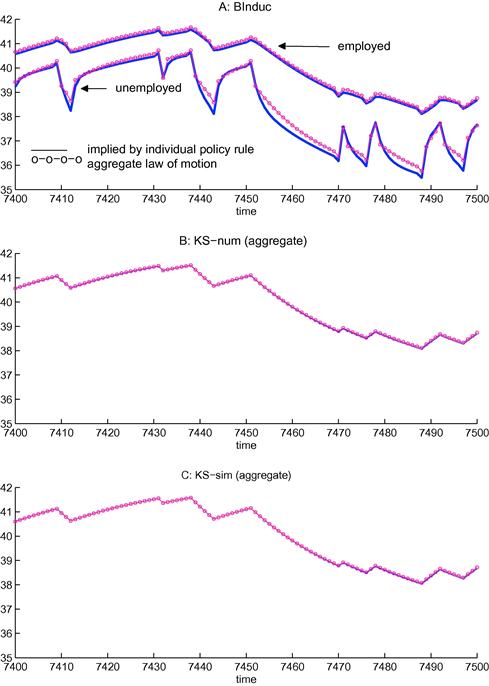

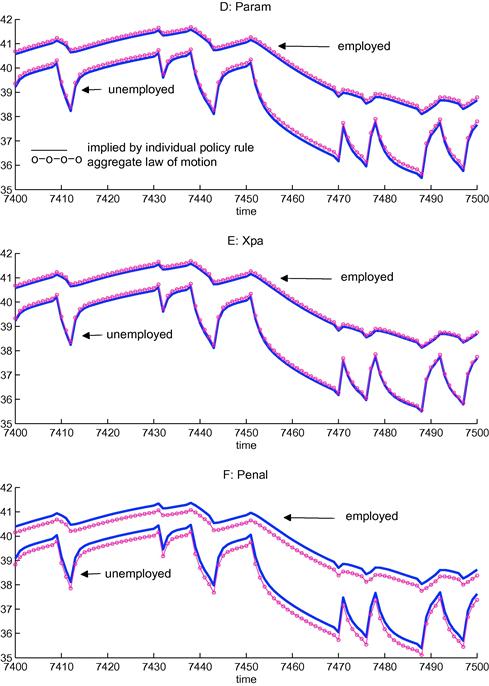

In this section, we discuss different procedures to simulate an economy with a continuum of heterogeneous agents taking as given numerical solutions for the individual policy rules. The most common procedure approximates the continuum with a large but finite number of agents and uses a random number generator to draw both the aggregate and the idiosyncratic shocks. With a finite number of agents, there will be cross-sectional sampling variation in the simulated cross-sectional data, while—conditional on the aggregate shock—there should be none if the model has a continuum of agents. Even when a large total number of agents is used, then some subgroups may still have a low number of agents and their cross-sectional characteristics are measured with substantial sampling noise. For example, Algan et al. (2008) document that moments of the capital holdings of the unemployed of the model described in Section 2 are subject to substantial sampling variation and that some properties of the true of law motion are not noticeable, even if the total number of agents is as high as 100,000.

This is documented in Figures 1–3. Figure 1 plots the per capita capital stock of the unemployed when the total number of agents in the panel is equal to 10,000. The figure clearly documents the sampling uncertainty. Figure 2 zooms in on a subsample and adds the simulated path when there are 100,000 agents in the economy. Even with 100,000 agents in the economy there is still noticeable sampling uncertainty. Of course, the number of unemployed agents is substantially less than the total number of agents in the economy.

Figure 1 Simulated per capita capital of the unemployment. Notes: This graph plots the simulated aggregate capital stock of the unemployed using either a finite number (10,000) or a continuum of agents.

Figure 2 Simulated per capita capital of the unemployment. Notes: This graph plots the simulated aggregate capital stock of the unemployed using either a finite number (10,000) or a continuum of agents. It displays a subset of the observations shown in Figure 1.

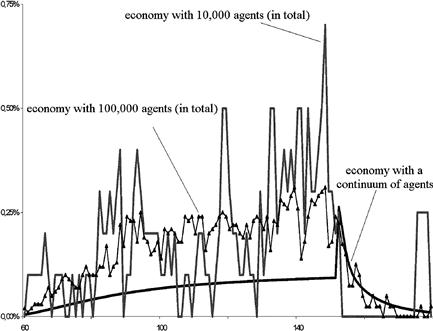

Figure 3 Simulated fraction of contrained agents. Notes: This graph plots the simulated fraction of unemployed agent at the borrowing constraint using either a finite number (10,000 or 100,000) or a continuum of agents.

Figure 3 plots the fraction of unemployed agents at the constraint. The sampling uncertainty in the time paths simulated with a finite number of agents is again striking, even when there are a total of 100,000 agents in the economy. In fact, the sampling uncertainty is so large that an interesting property of the model is completely dominated by sampling uncertainty. If the economy moves out of a recession into a boom, then the fraction of unemployed agents at the constraint increases according to the accurate simulation with a continuum of agents. The reason is that during a recession there is a higher chance that an unemployed agent was employed in the last period and employed agents never choose a zero capital stock.

This section discusses three procedures to simulate a time series of the cross-sectional distribution of a continuum of agents. The first two are grid methods that approximate the cross-sectional density with a histogram. One of these grid methods requires the inverse of the policy function, while the other does not. The third procedure uses polynomials. It imposes more structure on the functional form, but uses a lot fewer coefficients to characterize the distribution.

6.1 Grid Method I: Calculation of Inverse Required41

Consider a fine grid for the capital stock. This simulation procedure approximates at each point in time the CDF with a linear spline. This means that in between grid points the distribution is assumed to be uniform. Point mass at the borrowing constraint means that the value of the CDF at the first node is strictly positive. Calculating the CDF of the end-of-period capital holdings proceeds as follows. At each node, ![]() (which represents a value for the end-of-period capital holdings), calculate the value of the beginning-of-period capital stock,

(which represents a value for the end-of-period capital holdings), calculate the value of the beginning-of-period capital stock, ![]() , that would have led to the value

, that would have led to the value ![]() . That is,

. That is, ![]() is the inverse of

is the inverse of ![]() according to the individual policy function. The probability that the beginning-of-period capital stock is less than

according to the individual policy function. The probability that the beginning-of-period capital stock is less than ![]() is then used to calculate the value of the CDF value at

is then used to calculate the value of the CDF value at ![]() . Note that this last step requires the policy function to be monotone.

. Note that this last step requires the policy function to be monotone.

Information Used

The beginning-of-period ![]() distribution of capital holdings is fully characterized by the following:

distribution of capital holdings is fully characterized by the following:

• the fraction of unemployed agents with a zero capital stock, ![]() ,

,

• the fraction of employed agents with a zero capital stock,42 ![]() ,

,

• the distribution of capital holdings of unemployed agents with positive capital holdings, and

• the distribution of capital holdings of employed agents with positive capital holdings.

The goal is to calculate the same information at the beginning of the next period. Besides these four pieces of information regarding the cross-sectional distribution, one only needs (i) the realizations of the aggregate shock this period and next period and (ii) the individual policy function.

Grid

Construct a grid and define the beginning-of-period distribution of capital as follows:

2. Let ![]() be the fraction of agents with employment status

be the fraction of agents with employment status ![]() with a zero capital stock at the beginning of period

with a zero capital stock at the beginning of period ![]() .

.

3. For ![]() , let

, let ![]() be equal to the mass of agents with a capital stock bigger than

be equal to the mass of agents with a capital stock bigger than ![]() and less than or equal to

and less than or equal to ![]() . This mass is assumed to be distributed uniformly between grid points.

. This mass is assumed to be distributed uniformly between grid points.

Denote this beginning-of-period distribution function by ![]() .

.

End-of-Period Distribution

The first step is to calculate the end-of-period distribution of capital. For the unemployed, calculate the level of capital holdings at which the agent chooses ![]() . If we denote this capital level by

. If we denote this capital level by ![]() , then it is defined by43

, then it is defined by43

![]() (41)

(41)

This involves inverting the policy function and is the hardest part of the procedure. At each grid point, the period ![]() end-of-period values of the cumulative distribution function for the unemployed,

end-of-period values of the cumulative distribution function for the unemployed, ![]() , are given by

, are given by

(42)

(42)

where ![]() is the largest value of

is the largest value of ![]() such that

such that ![]() . The second equality follows from the assumption that

. The second equality follows from the assumption that ![]() is distributed uniformly between grid points.

is distributed uniformly between grid points.

A similar procedure is used to calculate the period ![]() end-of-period values of the cumulative distribution function for the employed,

end-of-period values of the cumulative distribution function for the employed, ![]() . That is,

. That is,

(43)

(43)

Next Period’s Beginning-of-Period Distribution

Let ![]() stand for the mass of agents with employment status

stand for the mass of agents with employment status ![]() that have employment status

that have employment status ![]() , conditional on the values of

, conditional on the values of ![]() and

and ![]() . For each combination of values of

. For each combination of values of ![]() and

and ![]() we have

we have

![]() (44)

(44)

This gives

![]() (45)

(45)

and

![]() (46)

(46)

![]() (47)

(47)

6.2 Grid Method II: No Calculation of Inverse Required44

This method also uses a grid and approximates the cross-sectional distribution with a histogram. Now it is assumed, however, that the distribution only has mass at the grid points. In terms of the information used, the notation, and the specification of the grid, everything is identical to the first procedure.45 An important advantage of this procedure is that it does not require using the inverse of the policy function and the policy function does not have to be monotone.

End-of-Period Distribution

The first procedure goes through a grid for the end-of-period capital holdings and then calculates which beginning-of-period capital values lead to this or a smaller grid value. The second procedure goes through the same grid values, but they now represent the beginning-of-period capital holdings. It then calculates the chosen capital stock and assigns the probability associated with this beginning-of-period capital stock to the two grid points that enclose the end-of-period capital choice.

Let ![]() be the mass of agents with employment status

be the mass of agents with employment status ![]() that have a capital level equal to

that have a capital level equal to ![]() at the end of the period. It can be calculated as follows:

at the end of the period. It can be calculated as follows:

(48)

(48)

(49)

(49)

The weights ![]() allocate the probabilities to the grid points and the magnitude of each weight is determined by the relative distance of

allocate the probabilities to the grid points and the magnitude of each weight is determined by the relative distance of ![]() to the two grid points that enclose

to the two grid points that enclose ![]() .46

.46

Next Period’s Beginning-of-Period Distribution

Given the end-of-period distribution, the distribution of next period’s beginning-of-period capital holdings can be calculated using Eq. (45). This step is identical to the one used for the first grid method.

6.3 Simulating Using Smooth Density Approximations

Algan et al. (2008) propose an alternative solution. Suppose that the beginning-of-period cross-sectional density is given by a particular density, ![]() , where

, where ![]() contains the coefficients of the density characterizing the density of capital holdings of agents with employment status

contains the coefficients of the density characterizing the density of capital holdings of agents with employment status ![]() in period 1.

in period 1. ![]() and

and ![]() together with individual policy rules and the values of

together with individual policy rules and the values of ![]() and

and ![]() are in principle sufficient to determine

are in principle sufficient to determine ![]() and

and ![]() . Algan et al. (2008) propose the following procedure. Let

. Algan et al. (2008) propose the following procedure. Let ![]() and

and ![]() be nth-order polynomials that describe the distributions in period 1. Below we will be more precise about the particular type of polynomial used, but this detail is not important to understand the main idea underlying the procedure.

be nth-order polynomials that describe the distributions in period 1. Below we will be more precise about the particular type of polynomial used, but this detail is not important to understand the main idea underlying the procedure.

Main Idea

The objective of the procedure is to generate a time series for the two cross-sectional distributions. Given that we use nth-order polynomials, this means generating the values of ![]() and

and ![]() . This is done as follows:

. This is done as follows:

1. Use ![]() , for

, for ![]() , together with individual policy rules to determine the first

, together with individual policy rules to determine the first ![]() moments of capital holdings at the end of period 1,