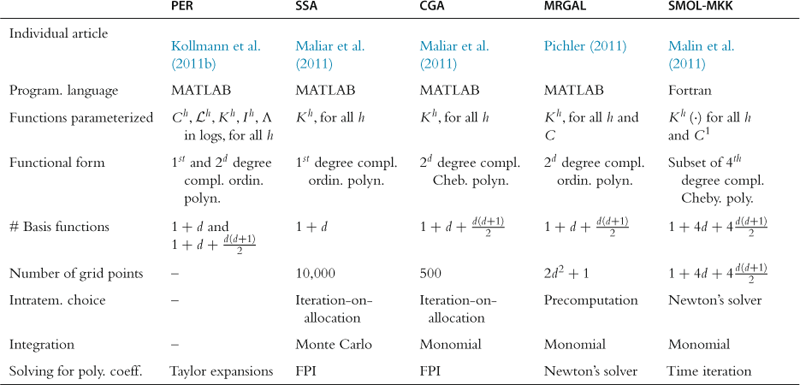

7.2.3 Shall We Use the Envelope Condition with Endogenous Grid?

Four combinations are possible to obtain from two alternative conditions for ![]() (i.e., FOC (83) and envelope condition (92)) and two alternative grids (i.e., exogenous and endogenous). So far, we have distinguished two competitive methods: one is EGM of Carroll (2005) (FOC (83) and endogenous grid) and the other is our ECM (envelope condition (92) and exogenous grid). Conventional VFI (FOC (83) and exogenous grid) is not competitive. Therefore, we are left to check the remaining combination (envelope condition (92) and endogenous grid).

(i.e., FOC (83) and envelope condition (92)) and two alternative grids (i.e., exogenous and endogenous). So far, we have distinguished two competitive methods: one is EGM of Carroll (2005) (FOC (83) and endogenous grid) and the other is our ECM (envelope condition (92) and exogenous grid). Conventional VFI (FOC (83) and exogenous grid) is not competitive. Therefore, we are left to check the remaining combination (envelope condition (92) and endogenous grid).

Solving (94) involves costly evaluation of ![]() for many candidate solution points

for many candidate solution points ![]() . We conclude that the combination of the envelope condition and endogenous grid does not lead to a competitive method. Our results are suggestive for other applications.

. We conclude that the combination of the envelope condition and endogenous grid does not lead to a competitive method. Our results are suggestive for other applications.

7.2.4 EGM and ECM in a Model with Elastic Labor Supply

Maliar and Maliar (2013) apply ECM and EGM for solving the one-agent model with elastic labor supply under assumption (17). Under EGM, Carroll’s (2005) change of variables does not avoid rootfinding in the model with elastic labor supply. The variable ![]() depends on future labor

depends on future labor ![]() , and

, and ![]() cannot be computed without specifying a labor policy function. Barillas and Fernández-Villaverde (2007) propose a way of extending EGM to the model with elastic labor supply. Namely, they fix a policy function for labor

cannot be computed without specifying a labor policy function. Barillas and Fernández-Villaverde (2007) propose a way of extending EGM to the model with elastic labor supply. Namely, they fix a policy function for labor ![]() , construct the grid of

, construct the grid of ![]() , solve the model on that grid holding

, solve the model on that grid holding ![]() fixed, and use the solution to reevaluate

fixed, and use the solution to reevaluate ![]() ; they iterate on these steps until

; they iterate on these steps until ![]() converges. See also Villemot (2012) for an application of EGM for solving a model of sovereign debt.

converges. See also Villemot (2012) for an application of EGM for solving a model of sovereign debt.

The implementation of EGM in Maliar and Maliar (2013) for the model with elastic labor supply differs from that in Barillas and Fernández-Villaverde (2007). First, Maliar and Maliar (2013) use future endogenous state variables for constructing grid points but they do not use Carroll’s (2005) change of variables. Second, to deal with rootfinding, Maliar and Maliar (2013) use a numerical solver, while Barillas and Fernández-Villaverde (2007) iterate on a state contingent policy function for labor ![]() . Maliar and Maliar (2013) find that ECM and EGM have very similar performances in that they produce solutions of similar (high) accuracy and have similar computational expenses. Even though neither ECM nor EGM allows us to solve the system of intratemporal choice conditions in a closed form, these two methods still lead to far simpler systems of equations than does conventional VFI.

. Maliar and Maliar (2013) find that ECM and EGM have very similar performances in that they produce solutions of similar (high) accuracy and have similar computational expenses. Even though neither ECM nor EGM allows us to solve the system of intratemporal choice conditions in a closed form, these two methods still lead to far simpler systems of equations than does conventional VFI.

7.3 Increasing the Accuracy of Dynamic Programming Methods

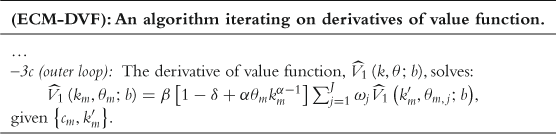

So far, we have been concerned with the inner loop: all the methods we have considered differ in the way in which they solve for the intratemporal choice. Maliar and Maliar (2012b, 2013) modify the outer loop as well by introducing versions of EGM and ECM that solve for the derivative of value function, ![]() , instead of or in addition to the value function itself

, instead of or in addition to the value function itself ![]() . Since only the derivative of the value function enters optimality conditions (83) and (92) but not the value function itself, we can find a solution to problem (82)–(84) without computing

. Since only the derivative of the value function enters optimality conditions (83) and (92) but not the value function itself, we can find a solution to problem (82)–(84) without computing ![]() explicitly.

explicitly.

In terms of our example, combining (83) and (92) yields

![]() (95)

(95)

This equation is used in Maliar and Maliar (2012b, 2013) to implement iteration on the derivative of the value function similar to the one we implement for value function using the Bellman equation. Iteration on the derivative of the value function is compatible with all previously described DP methods such as conventional VFI, EGM, and ECM. In particular, ECM modifies as follows:

In some experiments, Maliar and Maliar (2012a,b) approximate the value function ![]() and its derivative

and its derivative ![]() jointly. A robust finding is that methods approximating derivatives of value function lead to far more accurate solutions than the methods approximating the value function itself.

jointly. A robust finding is that methods approximating derivatives of value function lead to far more accurate solutions than the methods approximating the value function itself.

7.4 Numerical Illustration of Dynamic Programming Methods

Under Maliar and Maliar’s (2012a) implementation, the rootfinding problems under EGM and ECM are comparable in their complexity. In both cases, we must find a solution to a nonlinear equation in each grid point. Such an equation does not involve either interpolation or approximation of expectations. Below, we reproduce from Maliar and Maliar (2013) the results about a numerical comparison of ECM with EGM in the context of the model with elastic labor supply parameterized by (17).

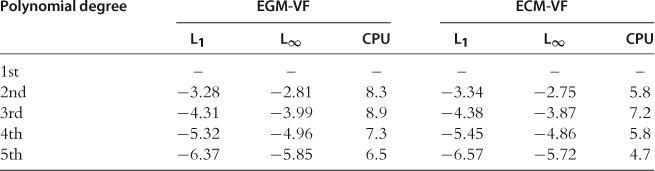

We first solve for ![]() by iterating on the Bellman equation (82)–(84) ; we refer to the corresponding methods as EGM-VF and ECM-VF. The results are shown in Table 12. The performance of EGM-VF and ECM-VF is very similar. EGM-VF produces slightly smaller maximum residuals, while ECM-VF produces slightly smaller average residuals. EGM-VF is somewhat slower than ECM-VF.

by iterating on the Bellman equation (82)–(84) ; we refer to the corresponding methods as EGM-VF and ECM-VF. The results are shown in Table 12. The performance of EGM-VF and ECM-VF is very similar. EGM-VF produces slightly smaller maximum residuals, while ECM-VF produces slightly smaller average residuals. EGM-VF is somewhat slower than ECM-VF.

Table 12

Accuracy and speed of EGM-VF and ECM-VF in the one-agent model with elastic labor supply.a

aNotes: ![]() and

and ![]() are, respectively, the average and maximum of absolute residuals across optimality condition and test points (in log10 units) on a stochastic simulation of 10,000 observations; CPU is the time necessary for computing a solution (in seconds). These results are reproduced from Maliar and Maliar (2013), Table 1.

are, respectively, the average and maximum of absolute residuals across optimality condition and test points (in log10 units) on a stochastic simulation of 10,000 observations; CPU is the time necessary for computing a solution (in seconds). These results are reproduced from Maliar and Maliar (2013), Table 1.

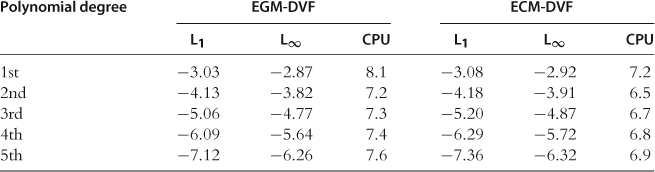

We next solve for ![]() by iterating on (95); we call the corresponding methods EGM-DVF and ECM-DVF. The results are provided in Table 13. Again, EGM-DVF and ECM-DVF perform very similarly. Both methods deliver accuracy levels that are about an order of magnitude higher than those of EGM-VF and ECM-VF.

by iterating on (95); we call the corresponding methods EGM-DVF and ECM-DVF. The results are provided in Table 13. Again, EGM-DVF and ECM-DVF perform very similarly. Both methods deliver accuracy levels that are about an order of magnitude higher than those of EGM-VF and ECM-VF.

Table 13

Accuracy and speed of EGM-DVF and ECM-DVF in the one-agent model with elastic labor supply.a

aNotes: ![]() and

and ![]() are, respectively, the average and maximum of absolute residuals across optimality condition and test points (in log10 units) on a stochastic simulation of 10,000 observations; CPU is the time necessary for computing a solution (in seconds). These results are reproduced from Maliar and Maliar (2013), Table 2.

are, respectively, the average and maximum of absolute residuals across optimality condition and test points (in log10 units) on a stochastic simulation of 10,000 observations; CPU is the time necessary for computing a solution (in seconds). These results are reproduced from Maliar and Maliar (2013), Table 2.

Iterating on (95) produces more accurate solutions than iterating on (82) because the object that is relevant for accuracy is ![]() and not

and not ![]() (

(![]() identifies the model’s variables via (83), (85), and (92)). Approximating a supplementary object

identifies the model’s variables via (83), (85), and (92)). Approximating a supplementary object ![]() and computing its derivative

and computing its derivative ![]() involves an accuracy loss compared to the case when we approximate the relevant object

involves an accuracy loss compared to the case when we approximate the relevant object ![]() directly. For example, if we approximate

directly. For example, if we approximate ![]() with a polynomial, we effectively approximate

with a polynomial, we effectively approximate ![]() with a polynomial which is one degree lower, i.e., we “lose” one polynomial degree. In our experiments, EGM-DVF and ECM-DVF attain accuracy levels that are comparable to the highest accuracy attained by the Euler equation methods.

with a polynomial which is one degree lower, i.e., we “lose” one polynomial degree. In our experiments, EGM-DVF and ECM-DVF attain accuracy levels that are comparable to the highest accuracy attained by the Euler equation methods.

8 Precomputation Techniques

Precomputation is a technique that computes solutions to some model’s equations outside the main iterative cycle. Precomputation techniques can be analytical, numerical, or a combination of both. We describe two numerical techniques: a technique of precomputing integrals in the intratemporal choice introduced in Judd et al. (2011d) and a technique of precomputing the intratemporal choice manifolds introduced in Maliar and Maliar (2005b) and developed in Maliar et al. (2011). We then briefly discuss an analytical technique of imperfect aggregation of Maliar and Maliar (2001, 2003a) which allows us to characterize aggregate behavior of certain classes of heterogeneous-agent economies in terms of one-agent models.

8.1 Precomputation of Integrals

In existing iterative methods for solving dynamic stochastic models, a conditional expectation function is computed in each iteration. Recomputing expectations in each iteration is costly. Judd et al. (2011d) show a simple technique that makes it possible to compute conditional expectation functions just once, in the stage of initialization. The proposed technique is called precomputation of integrals. We first show how to precompute the expectation for polynomial functions, and we then use the resulting polynomial functions to approximate expectations in the Euler and Bellman equations outside the main iterative loop.

8.1.1 Precomputation of Expectations for Polynomial Functions

Let us consider the one-agent model (1)–(3). Consider a complete ordinary polynomial function in terms of the current state ![]() ,

,

![]() (96)

(96)

where ![]() is a vector of polynomial coefficients, and

is a vector of polynomial coefficients, and ![]() is a polynomial degree. Taking into account that

is a polynomial degree. Taking into account that ![]() is known at present and that

is known at present and that ![]() , we can represent the conditional expectation of

, we can represent the conditional expectation of ![]() as follows:

as follows:

(97)

(97)

where ![]() , and

, and ![]() ,

, ![]() with

with

(98)

(98)

The integrals ![]() can be computed up-front without solving the model (i.e., precomputed). Once

can be computed up-front without solving the model (i.e., precomputed). Once ![]() ’s are computed, an evaluation of conditional expectation becomes very simple. Namely, the conditional expectation of a polynomial function is given by the same polynomial function but evaluated at a different coefficient vector, i.e.,

’s are computed, an evaluation of conditional expectation becomes very simple. Namely, the conditional expectation of a polynomial function is given by the same polynomial function but evaluated at a different coefficient vector, i.e., ![]() . Effectively, precomputation of integrals converts a stochastic problem into a deterministic one.

. Effectively, precomputation of integrals converts a stochastic problem into a deterministic one.

8.1.2 Precomputation of the Expectation in the Euler Equation

We now show how to precompute conditional expectation functions in Euler equation (74). Let us parameterize a variable inside the conditional expectation function with a polynomial function,

![]() (99)

(99)

By (99), we can write Euler equation (74) as

(100)

(100)

where ![]() are integrals that are known (precomputed) using (98). With this result, we formulate a system of four equations to feed into a grid-based Euler equation method:

are integrals that are known (precomputed) using (98). With this result, we formulate a system of four equations to feed into a grid-based Euler equation method:

![]() (101)

(101)

![]() (102)

(102)

![]() (103)

(103)

![]() (104)

(104)

We can now implement the following iterative scheme: fix some ![]() , use the intratemporal choice equations 101, 102, (103) to solve for

, use the intratemporal choice equations 101, 102, (103) to solve for ![]() in each grid point

in each grid point ![]() , and use the intertemporal choice equation (104) to recompute

, and use the intertemporal choice equation (104) to recompute ![]() . There is an explicit OLS formula for

. There is an explicit OLS formula for ![]() , namely,

, namely, ![]() , where

, where ![]() is a matrix of the coefficients and

is a matrix of the coefficients and ![]() is a vector of marginal utilities. However, the OLS method can be numerically unstable, and we may need to use regression methods that are robust to ill-conditioning studied in Section 4.2.

is a vector of marginal utilities. However, the OLS method can be numerically unstable, and we may need to use regression methods that are robust to ill-conditioning studied in Section 4.2.

With precomputation of integrals, we can also construct a version of the Euler equation method that operates on an endogenous grid ![]() and that is analogous to Carroll’s (2005) EGM. The iterative scheme modifies as follows: fix some

and that is analogous to Carroll’s (2005) EGM. The iterative scheme modifies as follows: fix some ![]() , use the intratemporal choice equations (102)–(104) to solve for

, use the intratemporal choice equations (102)–(104) to solve for ![]() in each grid point

in each grid point ![]() , and use the intertemporal choice condition (101) to recompute

, and use the intertemporal choice condition (101) to recompute ![]() . Again, there is an explicit OLS formula for

. Again, there is an explicit OLS formula for ![]() , where

, where ![]() is a matrix of the coefficients and variable

is a matrix of the coefficients and variable ![]() is defined as

is defined as ![]()

![]() .

.

8.1.3 Precomputation of the Expectation in the Bellman Equation

We now show how to precompute conditional expectation functions in Bellman equation 8,9 and 10. Let us parameterize the value function with complete ordinary polynomial,

![]() (105)

(105)

Then, according to (97), expectation ![]() can be precomputed as

can be precomputed as

![]() (106)

(106)

With this result, we rewrite the Bellman equation (8) as

![]() (107)

(107)

The system of the optimality conditions under precomputation of integrals becomes

![]() (108)

(108)

![]() (109)

(109)

![]() (110)

(110)

![]() (111)

(111)

A version of ECM with precomputation of integrals is as follows: fix some ![]() , use intratemporal choice equations (108)–(110) to solve for

, use intratemporal choice equations (108)–(110) to solve for ![]() in each grid point

in each grid point ![]() , and use the intertemporal choice equation (111) to recompute

, and use the intertemporal choice equation (111) to recompute ![]() ; iterate until convergence.

; iterate until convergence.

Precomputation of integrals can also be performed for the DP methods iterating on derivatives of value function as discussed in Section 7. Interestingly, a method that iterates on a derivative of value function coincides with the previously described Euler equation method that solves (101)–(104). This is because in this specific example, a variable in (99) which is parameterized to precompute the expectations in the Euler equation (74) coincides with the derivative ![]() . However, precomputation of integrals in the Euler equation is possible even for those problems for which we do not have a Bellman equation.

. However, precomputation of integrals in the Euler equation is possible even for those problems for which we do not have a Bellman equation.

Similar to the Euler equation case, there is an explicit OLS formula for ![]() , where

, where ![]() is a matrix of coefficients, and

is a matrix of coefficients, and ![]() is a vector of values of the utility functions. Finally, we can construct a version of Carroll’s (2005) EGM with precomputation of integrals. In this case, we compute the intratemporal choice

is a vector of values of the utility functions. Finally, we can construct a version of Carroll’s (2005) EGM with precomputation of integrals. In this case, we compute the intratemporal choice ![]() on the grid

on the grid ![]() to satisfy (109)–(111), and we use (108) to recompute

to satisfy (109)–(111), and we use (108) to recompute ![]() .

.

8.1.4 Relation of Precomputation of Integrals to the Literature

Effectively, precomputation of integrals allows us to solve stochastic economic models as if they were deterministic, with the corresponding reduction in cost. Precomputation of integrals is a very general technique that can be applied to any set of equations that contains conditional expectations, including the Bellman and Euler equations. Furthermore, precomputation of integrals is compatible with a variety of approximating functions, solution domains, integration rules, fitting methods, and iterative schemes for finding unknown parameters of approximating functions. That is, apart from precomputation of integrals, the rest of our solution procedure is standard. Finally, given that we must approximate integrals just once, we can use very accurate integration methods that would be intractable if integrals were computed inside an iterative cycle.

We must emphasize that, in order to precompute integrals, it is critical to parameterize the integrand, i.e., the expression inside the expectation function. Other parameterizations such as the capital function or the expectation function do not allow us to precompute integrals using accurate deterministic integration methods.

There are two other methods of approximating integrals that have similar computational complexity as does the method of precomputation of integrals (they also evaluate integrals in just one point). First, Marcet (1988) approximates an expectation function in each simulated point using a next-period realization of the integrand (which is a version of a Monte Carlo method with one random draw); the accuracy of this approximation is low and limits dramatically the accuracy of solutions; see our discussion in Section 5.8. Second, Judd et al. (2011a) propose to use a one-node Gauss-Hermite quadrature method, which approximates the integral with the expected value of the integrand; this method is far more accurate than the one-node Monte Carlo integration and is even more accurate than Monte Carlo integration with thousands of random nodes in the class of problems studied. Still, for high-degree polynomials, the one-node quadrature method limits the accuracy of solutions. In contrast, the method of precomputation of integrals delivers the highest possible accuracy that can be produced by deterministic integration methods at the lowest possible cost.

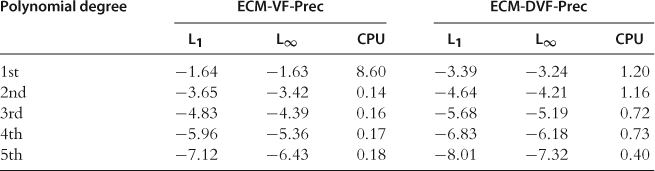

8.1.5 Numerical Illustration of the Precomputation Methods

In Table 14, we provide the results for the model with inelastic labor supply parameterized by (18) that are delivered by the Bellman and Euler equation methods with precomputation of integrals (these results are reproduced from Judd et al. (2011d)).

Table 14

Accuracy and speed of the Bellman equation algorithm in the one-agent model with inelastic labor supply.a

aNotes: ![]() and

and ![]() are, respectively, the average and maximum of absolute residuals across optimality condition and test points (in log10 units) on a stochastic simulation of 10,000 observations; CPU is the time necessary for computing a solution (in seconds). The results for ECM-VF-Prec and ECM-DVF-Prec are reproduced from Judd et al. (2011d), Table 1 and 2, respectively.

are, respectively, the average and maximum of absolute residuals across optimality condition and test points (in log10 units) on a stochastic simulation of 10,000 observations; CPU is the time necessary for computing a solution (in seconds). The results for ECM-VF-Prec and ECM-DVF-Prec are reproduced from Judd et al. (2011d), Table 1 and 2, respectively.

As we can see, the residuals decrease with each polynomial degree by one or more orders of magnitude. High-degree polynomial solutions are very accurate. Under ECM-VF-Prec (which is a DP algorithm), the maximum residuals for the fifth-degree polynomial approximations are of the order ![]() . Under ECM-DVF-Prec (which is an Euler equation algorithm), the maximum residuals are about one order of magnitude smaller. The tendencies are similar to those we observe for the corresponding methods without precomputation; see Tables 12 and 13 for a comparison.

. Under ECM-DVF-Prec (which is an Euler equation algorithm), the maximum residuals are about one order of magnitude smaller. The tendencies are similar to those we observe for the corresponding methods without precomputation; see Tables 12 and 13 for a comparison.

8.2 Precomputation of Intratemporal Choice Manifolds

The precomputation technique of intratemporal choice manifolds constructs solutions to the intratemporal choice conditions outside the main iterative cycle and uses the constructed solutions to infer the intratemporal choice inside the main iterative cycle. Consider the intratemporal choice conditions for model (1)–(3) under parameterization (17)

![]() (112)

(112)

![]() (113)

(113)

We denote a solution for ![]() and

and ![]() for given

for given ![]() as

as ![]() and

and ![]() , respectively, and we call

, respectively, and we call ![]() and

and ![]() solution manifolds.

solution manifolds.

Observe that it is sufficient for us to construct a manifold for labor ![]() since we can infer consumption from (113) if labor is given. To compute the intratemporal choice inside the main iterative cycle, first we use

since we can infer consumption from (113) if labor is given. To compute the intratemporal choice inside the main iterative cycle, first we use ![]() to find

to find ![]() and

and ![]() ; then we use

; then we use ![]() to compute

to compute ![]() and

and ![]() ; and, finally, we can get

; and, finally, we can get ![]() and

and ![]() from (113). In the remainder of the section, we focus on constructing

from (113). In the remainder of the section, we focus on constructing ![]() .

.

In simple cases, the intratemporal choice manifolds can be constructed analytically. Consider the following example.

Example 18

Assume (17) under ![]() . Then, system (112), (113) admits a closed-form solution in the form

. Then, system (112), (113) admits a closed-form solution in the form

![]() (114)

(114)

However, under more general parameterizations, ![]() cannot be constructed analytically from (112), (113). We therefore construct it numerically.

cannot be constructed analytically from (112), (113). We therefore construct it numerically.

Example 19

Assume (17). Consider system (112), (113). We proceed as follows:– Outside the main iterative cycle:

In the above example, we had to compute values for labor using a numerical solver. We now show how to “invert” the problem and to precompute the same manifold but without using a solver.

Maliar and Maliar (2005b) show an example of precomputation of the labor choice in a similar model but assuming that the intertemporal choice is parameterized with a consumption decision function instead of a capital decision function. In this case, the labor choice can be precomputed in terms of just one artificial variable and, thus, is easier to construct in the main iterative cycle; see the example below.

Example 21

Assume (17). Consider the system (112), (113). Let us define a new variable ![]() by

by

![]() (117)

(117)

We proceed as follows:– Outside the main iterative cycle:

(i) Take a grid ![]() within the relevant range.

within the relevant range.

(ii) For each grid point ![]() , compute the value of variable

, compute the value of variable ![]() satisfying (117).

satisfying (117).

(iii) Construct a labor manifold ![]() (by fitting the values

(by fitting the values ![]() to a polynomial function, splines, etc., on the grid

to a polynomial function, splines, etc., on the grid ![]() ).

).

Inside the main iterative cycle, given a value of ![]() , we compute

, we compute ![]() using the precomputed manifolds

using the precomputed manifolds ![]() , and we compute

, and we compute ![]() using (113).

using (113).

We can also invert the task and construct the same manifold by choosing a grid for ![]() and by solving for

and by solving for ![]() using (117), in which case a numerical solver is not needed. See Maliar et al. (2011) for examples of precomputation of the intratemporal choice manifolds for heterogeneous-agent economies.

using (117), in which case a numerical solver is not needed. See Maliar et al. (2011) for examples of precomputation of the intratemporal choice manifolds for heterogeneous-agent economies.

Three comments are in order: First, the solution manifold ![]() depends on three arguments

depends on three arguments ![]() instead of the conventional decision function that depends on two arguments

instead of the conventional decision function that depends on two arguments ![]() : the relation between these objects is given by

: the relation between these objects is given by ![]() , where

, where ![]() is the optimal capital decision function; see Maliar et al. (2011) for a discussion. Second, there are many ways to define the intertemporal (and thus, intratemporal) choice manifolds; it is possible to fix any three variables in (112), (113) and solve for the remaining two variables; for example, we can fix

is the optimal capital decision function; see Maliar et al. (2011) for a discussion. Second, there are many ways to define the intertemporal (and thus, intratemporal) choice manifolds; it is possible to fix any three variables in (112), (113) and solve for the remaining two variables; for example, we can fix ![]() and find

and find ![]() . Finally, precomputation of the intratemporal choice can also be implemented in the context of DP methods described in Section 7.

. Finally, precomputation of the intratemporal choice can also be implemented in the context of DP methods described in Section 7.

8.3 Precomputation of Aggregate Decision Rules

Maliar and Maliar (2001, 2003a) study complete-market heterogeneous-agents economies in which agents differ in initial endowments and labor productivities (under some parameterizations, their model is identical to the multicountry model studied in Section 11). In particular, they show that under the standard assumptions of the CRRA or addilog utility functions and the Cobb-Douglas production function, it is possible to characterize the aggregate behavior of a heterogeneous-agents economy in terms of a one-agent model. This kind of result is referred to as imperfect aggregation and is in effect an analytical precomputation of some aggregate decision functions outside the main iterative cycle.

Imperfect aggregation is not an aggregation result in the traditional sense of Gorman (1953) since the behavior of the composite consumer does depend on a joint distribution of heterogeneity parameters. It is a special case of the aggregation in equilibrium point by Constantinides (1982) in which the social utility function can be constructed analytically. (In general, such utility function depends on the distribution of individual characteristics in a manner which is difficult to characterize). Models derived from aggregation are of additional interest because having explicit conditions relating aggregate variables is convenient for numerical work. See Maliar et al. (2011) for imperfect aggregation results in the context of the multicountry models studied in the JEDC comparison analysis.

9 Local (Perturbation) Methods

A local perturbation method computes a solution to an economic model in just one point—a deterministic steady state—using Taylor expansions of optimality conditions. Perturbation methods are introduced to economics in Judd and Guu (1993) and became a popular tool in the literature. The main advantage of perturbation methods is their low computational expense. The main shortcoming is that the accuracy of perturbation solutions may decrease rapidly away from the steady state. In this section, we discuss two techniques that can increase the accuracy of perturbation methods: a change of variables introduced in Judd (2003) and a hybrid of local and global solutions advocated in Maliar et al. (2013).16 We present these techniques in the context of Euler equation methods; however, our results apply to DP methods as well. See Judd (1998) for perturbation methods in the context of value function iteration.

9.1 Plain Perturbation Method

To present the perturbation techniques, we use a version of the one-agent model (1)–(3) with inelastic labor supply:

(118)

(118)

![]() (119)

(119)

![]() (120)

(120)

where ![]() is given. This model’s presentation differs from that in (1)–(3) in two respects: First, we use a separate notation for a net of depreciation production function

is given. This model’s presentation differs from that in (1)–(3) in two respects: First, we use a separate notation for a net of depreciation production function ![]() , where

, where ![]() is the gross production function. This helps us to simplify the presentation. Second, we explicitly introduce

is the gross production function. This helps us to simplify the presentation. Second, we explicitly introduce ![]() into the process for productivity (120). This is done because we compute a Taylor expansion not only with respect to the two state variables

into the process for productivity (120). This is done because we compute a Taylor expansion not only with respect to the two state variables ![]() but also with respect to parameter

but also with respect to parameter ![]() . In addition, we assume that

. In addition, we assume that ![]() .

.

We approximate the capital decision function in the form ![]() using the Taylor expansion around the deterministic steady state

using the Taylor expansion around the deterministic steady state ![]() , as follows:

, as follows:

In this section, notation of type ![]() and

and ![]() stands for the first-order partial derivative of a function

stands for the first-order partial derivative of a function ![]() with respect to a variable

with respect to a variable ![]() and the second-order partial derivative with respect to variables

and the second-order partial derivative with respect to variables ![]() and

and ![]() , respectively. The steady-state value

, respectively. The steady-state value ![]() follows by (120).

follows by (120).

To identify the derivatives of ![]() , we use a procedure suggested by an implicit function theorem. We write the Euler equation of problem (118)–(120) as follows:

, we use a procedure suggested by an implicit function theorem. We write the Euler equation of problem (118)–(120) as follows:

![]() (121)

(121)

where ![]() is determined by (120), and

is determined by (120), and ![]() and

and ![]() are determined by (119) in the current and next periods, respectively,

are determined by (119) in the current and next periods, respectively,

By definition, ![]() is a zero function in the true solution since the Euler equation must be satisfied exactly for any

is a zero function in the true solution since the Euler equation must be satisfied exactly for any ![]() . In particular, the value of

. In particular, the value of ![]() must be zero in the steady state,

must be zero in the steady state, ![]() , and all the derivatives of

, and all the derivatives of ![]() must be also zero in the steady state,

must be also zero in the steady state, ![]() , etc. This fact suggests a procedure for approximating a solution to the model. Namely, we evaluate the value of

, etc. This fact suggests a procedure for approximating a solution to the model. Namely, we evaluate the value of ![]() and its derivatives in the steady state and set them to zero to identify the unknown coefficients in the capital decision function

and its derivatives in the steady state and set them to zero to identify the unknown coefficients in the capital decision function ![]() .

.

We start by finding the steady state. Given ![]() , (121) implies

, (121) implies ![]() , which identifies

, which identifies ![]() and

and ![]() ). Let us show how to derive the first-order perturbation solution.

). Let us show how to derive the first-order perturbation solution.

First, ![]() is given by

is given by

where

![]()

Note that ![]() . Evaluating

. Evaluating ![]() in the steady state and equalizing it to zero, we obtain

in the steady state and equalizing it to zero, we obtain

Rearranging the terms yields

![]()

This is a quadratic equation in one unknown, ![]() .

.

Second, ![]() is given by

is given by

where

Evaluating ![]() in the steady state and equalizing it to zero, we obtain

in the steady state and equalizing it to zero, we obtain

This gives us a solution for ![]() :

:

Finally, ![]() is given by

is given by

where

Evaluating ![]() in the steady state and equalizing it to zero, we obtain

in the steady state and equalizing it to zero, we obtain

After all the derivatives of ![]() are found, we can form a first-order perturbation solution for capital,

are found, we can form a first-order perturbation solution for capital,

![]() (122)

(122)

Similarly, we can write a first-order perturbation solution for consumption ![]() ,

,

![]() (123)

(123)

where ![]() , and

, and ![]() . Finally, the first-order perturbation approximation for the productivity shocks

. Finally, the first-order perturbation approximation for the productivity shocks ![]() is

is

![]() (124)

(124)

where ![]() and

and ![]() . The first-order terms

. The first-order terms ![]() , and

, and ![]() are equal to zero in (122),(123)and(124), respectively. However, the higher-order derivatives of

are equal to zero in (122),(123)and(124), respectively. However, the higher-order derivatives of ![]() , and

, and ![]() with respect to

with respect to ![]() are not equal to zero, which makes higher-order perturbation solutions depend on the volatility of shocks.

are not equal to zero, which makes higher-order perturbation solutions depend on the volatility of shocks.

9.2 Advantages and Shortcomings of Perturbation Methods

Constructing perturbation solutions by hand is tedious even in the case of first-order approximation, as our example demonstrates. Fortunately, perturbation methods can be easily automated. Perturbation software commonly used in economics is Dynare. This software platform can solve, simulate, and estimate a wide class of economic models and delivers standard perturbation solutions up to the third order.17 Automated software for solving economic models is also developed by Jin and Judd (2002), Swanson et al. (2002), and Schmitt-Grohé and Uribe (2004). There are perturbation methods that can solve models with kinks using penalty functions; see Kim et al. (2010) and Mertens and Judd (2013).

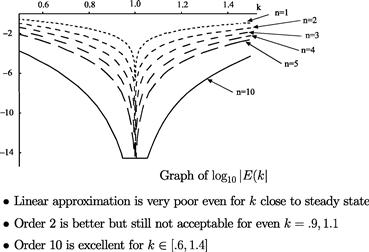

An important advantage of perturbation methods is that they have low computational expense, which makes them an ideal candidate for solving problem with high dimensionality. The shortcoming of perturbation methods is that the accuracy of local solutions may decrease rapidly away from the steady state. To provide an illustration, we reproduce some results from Judd and Guu (1993). In Figure 8, we plot the size of unit-free residuals in the Euler equation (in ![]() units) depending on how far we deviate from the steady state where the solution is computed (in this figure,

units) depending on how far we deviate from the steady state where the solution is computed (in this figure, ![]() denotes an order of approximation).

denotes an order of approximation).

Figure 8 Global Quality of Asymptotic Approximations. Notes: Reproduced from Judd and Guu (1993) with kind permission from Springer Science+Business.

We observe that the linear perturbation solutions are very inaccurate. The quadratic perturbation solutions are more accurate but are still not acceptable even in a relatively small range around the steady state (e.g., ![]() ). The perturbation solutions of order 10 are of acceptable accuracy in a large range (e.g.,

). The perturbation solutions of order 10 are of acceptable accuracy in a large range (e.g., ![]() ). Thus, high-order approximations are needed to attain accurate solutions. See also Kollmann et al. (2011b) and Judd et al. (2012) for the accuracy results of perturbation methods in the context of a large-scale multicountry model and a new Keynesian model, respectively.18

). Thus, high-order approximations are needed to attain accurate solutions. See also Kollmann et al. (2011b) and Judd et al. (2012) for the accuracy results of perturbation methods in the context of a large-scale multicountry model and a new Keynesian model, respectively.18

9.3 Change of Variables

Judd (2003) shows that the accuracy of perturbation methods can be considerably increased using a nonlinear change of variables. Specifically, he shows that the ordinary Taylor series expansion can be dominated in accuracy by other expansions implied by changes of variables. All the expansions are locally equivalent but differ globally. We must choose the one that performs best in terms of accuracy on the domain of interest. In the context of a deterministic optimal growth model, Judd (2003) finds that using alternative expansions can increase the accuracy of the conventional perturbation method by two orders of magnitude. Fernández-Villaverde and Rubio-Ramírez (2006) show how to apply the method of change of variables to a model with uncertainty and elastic labor supply.

9.3.1 An Example of the Change of Variables Technique

Let us consider the one-agent model (118)–(120) with inelastic labor supply as an example. Suppose ![]() is approximated as was discussed in Section 9 and that we have computed all the derivatives

is approximated as was discussed in Section 9 and that we have computed all the derivatives ![]() , and

, and ![]() . The objective is to find a change of variables

. The objective is to find a change of variables ![]() and

and ![]() , with

, with ![]() being a new variable, such that a Taylor approximation (122) of

being a new variable, such that a Taylor approximation (122) of ![]() in terms of a new variable

in terms of a new variable ![]() has two properties: (i) the derivatives are the same in the steady state; and (ii) the accuracy declines less rapidly when we deviate from the steady state.

has two properties: (i) the derivatives are the same in the steady state; and (ii) the accuracy declines less rapidly when we deviate from the steady state.

Using the identity, ![]() , we rewrite the capital function

, we rewrite the capital function ![]() as

as ![]() . With this result, we obtain a decision function for

. With this result, we obtain a decision function for ![]()

![]() (125)

(125)

Let us find a first-order Taylor expansion of the decision function for ![]() (125) around

(125) around ![]() , and

, and ![]() :

:

Substituting the steady-state value ![]() instead of

instead of ![]() , we obtain the formula for the change of variables

, we obtain the formula for the change of variables

![]() (126)

(126)

Consider now specific examples. In the trivial case, ![]() , we have

, we have ![]() , and we are back to (122). Under a logarithmic transformation of, i.e.,

, and we are back to (122). Under a logarithmic transformation of, i.e., ![]() , condition (126) implies

, condition (126) implies

(127)

(127)

For a power transformation ![]() , we obtain

, we obtain

(128)

(128)

In this way, we can try many different transformations (at a low cost). For each candidate change of variables, we evaluate accuracy using a selected accuracy test (e.g., we can evaluate the Euler equation residuals on a stochastic simulation), and we choose the representation that yields the most accurate solution globally.

Three observations are in order. First, we need not compute anything new to implement the change of variables: the derivatives ![]() , and

, and ![]() which determine the coefficients in (127) and (128) are the same as that we found in Section 9.1 using the plain perturbation method. Second, in the above example, we apply the same change of variables to

which determine the coefficients in (127) and (128) are the same as that we found in Section 9.1 using the plain perturbation method. Second, in the above example, we apply the same change of variables to ![]() and

and ![]() . More generally, we can use other transformations. For example, for

. More generally, we can use other transformations. For example, for ![]() , we may keep the same transformation as before,

, we may keep the same transformation as before, ![]() , but for

, but for ![]() , we may use a different transformation

, we may use a different transformation ![]() so that

so that ![]() . Finally, we may also apply some changes of variables to

. Finally, we may also apply some changes of variables to ![]() and

and ![]() . Ideally, a selection of the right change of variables must be automated; see Judd (2003) for more details.

. Ideally, a selection of the right change of variables must be automated; see Judd (2003) for more details.

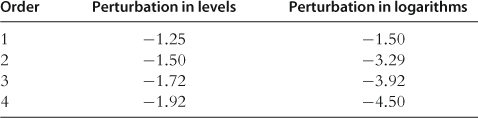

9.3.2 Numerical Illustration of the Change of Variables Technique

For a simple one-agent model with inelastic labor supply, Judd (2003) shows that logarithmic and power transformations of the variables may decrease the maximum residuals in the optimality conditions by several orders of magnitude. In Table 15, we reproduce his results for the logarithmic transformations of ![]() and

and ![]() (perturbation in logarithms) compared to ordinary perturbation in levels. As we can see, perturbation in logarithms produces significantly more accurate approximations than perturbation in levels; however, this accuracy ranking is model-specific and does not need to hold for other models.

(perturbation in logarithms) compared to ordinary perturbation in levels. As we can see, perturbation in logarithms produces significantly more accurate approximations than perturbation in levels; however, this accuracy ranking is model-specific and does not need to hold for other models.

Table 15

Perturbation in levels and logarithms in the one-agent model.a

aNotes: The numbers in the table are the maximum absolute Euler equation residuals (in log10 units); ![]() . These results are reproduced from Judd (2003), Table 2.

. These results are reproduced from Judd (2003), Table 2.

9.4 Hybrid of Local and Global Solutions

Maliar et al. (2013) develop a hybrid perturbation-based solution method that combines local and global approximation techniques. (The term hybrid method indicates that we combine policy functions produced by different solution methods.) This hybrid method computes a plain perturbation solution, fixes some perturbation functions, and replaces the rest of the perturbation functions by new functions that are constructed to satisfy the model’s conditions exactly. The construction of these new functions mimics global solution methods: for each point of the state space considered, we solve nonlinear equations either analytically (when closed-form solutions are available) or with a numerical solver. If the perturbation functions that were used to construct a hybrid solution are accurate, then the entire hybrid solution will inherit their high accuracy; such a hybrid solution may be far more accurate than the original perturbation solution. The cost of the hybrid method is essentially the same as that of the standard perturbation method. The hybrid method of Maliar et al. (2013) encompasses previous examples constructed on the basis of the standard loglinearization method in Dotsey and Mao (1992) and Maliar et al. (2011).

9.4.1 Description of the Hybrid Method

To exposit the idea of the hybrid method, we use the one-agent model (118)–(120) with inelastic labor supply. We assume that a plain perturbation method delivers an approximate solution in the form of two decision functions ![]() and

and ![]() , such as (122), (123) constructed in Section 9.1. Let us assume that the decision functions are not sufficiently accurate for our purpose.

, such as (122), (123) constructed in Section 9.1. Let us assume that the decision functions are not sufficiently accurate for our purpose.

We attempt to improve on the accuracy in the following way. We fix one decision function from the benchmark solution, for example, ![]() , and we solve for the other decision function,

, and we solve for the other decision function, ![]() , to satisfy some model’s nonlinear optimality conditions taking

, to satisfy some model’s nonlinear optimality conditions taking ![]() as given.

as given.

For model (118)–(120), we have two optimality conditions,

![]() (129)

(129)

![]() (130)

(130)

By considering all possible combinations of the two decision functions and the two optimality conditions, we construct four hybrid solutions ![]() , and

, and ![]() , as follows:

, as follows:

HYB1: Fix ![]() and define

and define ![]() using (130),

using (130),

![]()

HYB2: Fix ![]() and define

and define ![]() using (129),

using (129),

![]()

HYB3: Fix ![]() and define

and define ![]() using (130),

using (130),

![]()

HYB4: Fix ![]() and define

and define ![]() using (129),

using (129),

![]()

On the basis of this example, we can make the following observations: first, multiple hybrid solutions can be constructed for a given benchmark solution; in our example, there are four hybrid solutions. Second, the hybrid method mimics global solution methods in a sense that functions ![]() ,

, ![]() , and

, and ![]() are defined to satisfy the corresponding nonlinear optimality conditions globally, for any point

are defined to satisfy the corresponding nonlinear optimality conditions globally, for any point ![]() of the state space considered. Third, a hybrid solution can be either more accurate or less accurate than the benchmark solution. Assume that in the benchmark solution,

of the state space considered. Third, a hybrid solution can be either more accurate or less accurate than the benchmark solution. Assume that in the benchmark solution, ![]() is accurate and

is accurate and ![]() is not. Then, the hybrid solutions based on

is not. Then, the hybrid solutions based on ![]() (i.e., HYB1 and HYB2) will be more accurate, while the hybrid solutions based on

(i.e., HYB1 and HYB2) will be more accurate, while the hybrid solutions based on ![]() (i.e., HYB3 and HYB4) will be less accurate than the benchmark solution. Finally, hybrid solutions can differ in cost considerably. In our example, HYB1 and HYB3 are obtained using simple closed-form expressions, while HYB2 and HYB4 are defined implicitly and are far more costly to compute.

(i.e., HYB3 and HYB4) will be less accurate than the benchmark solution. Finally, hybrid solutions can differ in cost considerably. In our example, HYB1 and HYB3 are obtained using simple closed-form expressions, while HYB2 and HYB4 are defined implicitly and are far more costly to compute.

9.4.2 Numerical Illustration of the Hybrid Method

A potential usefulness of the hybrid solution method is well seen in examples constructed using the standard loglinearization method. In particular, Maliar et al. (2011) take the capital decision function produced by the standard loglinearization method and accurately solve for consumption and labor to satisfy the intertemporal choice conditions (using the iteration-on-allocation method) in the context of a two-agent version studied in the JEDC comparison analysis. In Table 16, we compare the accuracy of the resulting hybrid method, HYB, with that of the plain first-order and second-order perturbation methods (in levels), denoted PER1 and PER2, respectively. As the table indicates, the first-order hybrid method produces more accurate linear approximations (by more than an order of magnitude) than PER1. In terms of the maximum residuals, it is even more accurate than PER2.

Table 16

Perturbation method versus hybrid method in the two-agent model.a

aNotes: ![]() and

and ![]() are, respectively, the average and maximum of absolute residuals across optimality conditions and test points (in log10 units). PER1 and PER2 are the first- and second-order perturbation solutions (in levels), and HYB are the hybrid solutions. These results are reproduced from Maliar et al. (2011), Table 5.

are, respectively, the average and maximum of absolute residuals across optimality conditions and test points (in log10 units). PER1 and PER2 are the first- and second-order perturbation solutions (in levels), and HYB are the hybrid solutions. These results are reproduced from Maliar et al. (2011), Table 5.

9.5 Numerical Instability of High-Order Perturbation Solutions in Simulation

An important shortcoming of plain perturbation methods is a numerical instability in simulation. The instability occurs because perturbation methods produce an approximation that is valid only locally, i.e., in the steady-state point and its small neighborhood. If we use this approximation for simulation, there is a chance that the simulated series become explosive when some realizations of shocks drive the process outside the accuracy range. The chance of nonstationary behavior is higher if the model has a high degree of nonlinearity.

Pruning methods try to address this shortcoming of the standard perturbation methods. The term pruning is introduced by Kim et al. (2008) who point out that a simulation of high-order perturbation solutions may produce explosive time series. To restore numerical stability, they propose to replace cross-products of variables in the second-order perturbation solution with cross-products of variables obtained from the first-order perturbation solution. Other papers that focus on stabilizing perturbation methods are Lombardo (2010) and Den Haan and De Wind (2012). In particular, the latter paper uses a fixed-point iteration technique that is similar in spirit to iteration-on-allocation described in Maliar et al. (2010, 2011) for constructing hybrid-like solutions.

10 Parallel Computation

Technological progress constantly increases the speed of computers. Moore (1965) made an observation that the number of transistors on integrated circuits doubles approximately every 2 years, and the speed of processors doubles approximately every 18 months (both because the number of transistors increases and because transistors become faster). The Moore law continues to hold meaning that in 10 years, computers will become about 100 times faster.

What happens if we cannot wait for 10 years or if a 100-time increase in speed is not sufficient for our purpose? There is another important source of growth of computational power that is available at present, namely, parallel computation: we connect a number of processors together and use them to perform a single job. Serial desktop computers have several central processing units (CPUs) and may have hundreds of graphics processing units (GPUs), and a considerable reduction in computational expense may be possible. Supercomputers have many more cores (hundreds of thousands) and have graphical cards with a huge number of GPUs. Each processor in a supercomputer is not (far) more powerful than a processor on our desktop but pooling their efforts gives them a high computational power. Running a job on 10,000 cores in parallel can increase the speed of our computation up to a factor of 10,000. This is what supercomputers are.

Early applications of parallel computation to economic problems are Amman (1986, 1990), Chong and Hendry (1986), Coleman (1992), Nagurney (1996), Nagurney and Zhang (1998). More recent applications include Doornik et al. (2006), Creel (2005, 2008), Creel and Goffe (2008), Sims et al. (2008), Aldrich et al. (2011), Morozov and Mathur (2012), Durham and Geweke (2012), Cai et al. (2012), Valero et al. (2013), and Maliar (2013), among others.

The possibility of parallel computation raises new issues. First, to take advantage of this technology, we must design algorithms in a manner which is suitable for parallelization. Second, we need hardware and software that support parallel computation. Finally, we must write a code that splits a large job into smaller tasks, that exchanges information between different cores in the process of computation, and that gathers the information to produce final output. We discuss these issues in the remainder of the section.

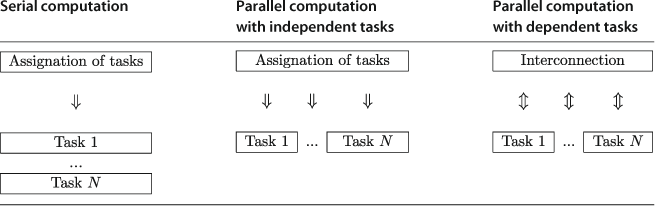

10.1 Serial Versus Parallel Computation

Assume that we must execute ![]() tasks. Traditional, one-core serial computation requires us to process the tasks one-by-one. The running time for executing

tasks. Traditional, one-core serial computation requires us to process the tasks one-by-one. The running time for executing ![]() tasks is

tasks is ![]() times larger than that for executing one task. If we have multiple cores, we can parallelize the computation. The easiest case for parallelization is when tasks are independent and no information is shared (exchanged) during the process of computation. This case is known in computer science literature as naturally parallelizable jobs. A more general case requires us to exchange information between the cores (implementing different tasks) during the computational process; see Table 17.

times larger than that for executing one task. If we have multiple cores, we can parallelize the computation. The easiest case for parallelization is when tasks are independent and no information is shared (exchanged) during the process of computation. This case is known in computer science literature as naturally parallelizable jobs. A more general case requires us to exchange information between the cores (implementing different tasks) during the computational process; see Table 17.

A coordinating unit, called a core 0 or master, assigns tasks to multiple cores (workers) and performs the information exchange if needed. Assuming that the implementation of parallel computation has no additional cost, the parallelized algorithm is ![]() times faster than the serial one if tasks are independent. When the information exchange is needed, the gain from parallelization depends on a specific application and a specific way in which the code is implemented.

times faster than the serial one if tasks are independent. When the information exchange is needed, the gain from parallelization depends on a specific application and a specific way in which the code is implemented.

10.1.1 Applications with Independent Tasks

The restriction that tasks are independent is obviously limiting. Still, there are many interesting applications for which this restriction is satisfied. In econometrics, we may need to run many regressions of a dependent variable on different combinations of independent variables, and we may run each such a regression on a separate core; see Doornik et al. (2006) for a review of applications of parallel computation in econometrics. In a similar vein, we may need to solve an economic model under a large number of different parameterizations either because we want to study how the properties of the solution depend on a specific parameterization (sensitivity analysis) or because we want to produce multiple data sets for estimating the model’s parameters (e.g., nested fixed-point estimation; see Fernández-Villaverde and Rubio-Ramírez (2007), Winschel and Krätzig (2010), and Su and Judd (2012) for related examples). In this case, we solve a model under each given parameter vector on a separate core. Other examples of naturally parallelizable jobs are matrix multiplication, exhaustive search over a discrete set of elements, optimization of a function over a region of state space, etc.

10.1.2 Applications with Dependent Tasks

In general, a given problem will contain some tasks that can be parallelized, some tasks that cannot be parallelized, and some tasks that can be parallelized but will require information exchange during their implementation (dependence). This is in particular true for the solution methods described in Sections 4–9. Loops are an obvious candidate for parallelization. However, after each iteration on a loop, we must typically gather the output produced by all workers and to combine it in order to produce an input for the next iteration. Some of the surveyed computational techniques are designed to be parallelizable. In particular, Maliar et al. (2011) and Maliar and Maliar (2013) propose a separation of the model’s equations into the intratemporal and intertemporal choice equations under the Euler equation and dynamic programming methods. Such a separation provides a simple way to parallelize computation. Namely, we can first produce current and future endogenous state variables in all grid points and or integration nodes, and we can then solve for the intratemporal choice in each grid point and integration node using a separate core; see Sections 6 and 7 for a discussion.

10.1.3 Speedup and Efficiency of Parallelization

Two measures that are used to characterize gains from parallelization are the speedup and efficiency of parallelization. The speedup is defined as a ratio

![]() (131)

(131)

where ![]() and

and ![]() are the times for executing a job on one core and

are the times for executing a job on one core and ![]() cores, respectively. In turn, the efficiency of parallelization is defined as

cores, respectively. In turn, the efficiency of parallelization is defined as

![]() (132)

(132)

The efficiency shows gains from parallelization ![]() relative to the number of cores used

relative to the number of cores used ![]() . The upper bounds of (131) and (132) are

. The upper bounds of (131) and (132) are ![]() and

and ![]() , and they are attained if a job is perfectly parallelizable and the cost of information transfers is zero.

, and they are attained if a job is perfectly parallelizable and the cost of information transfers is zero.

The typical code has some parts that are parallelizable and other parts that must be executed serially. Nonparallelizable parts of the code restrict the speedup and efficiency of parallelization that can be attained in a given application. Moreover, the speedup and efficiency of parallelization depend on the cost of implementing the parallelization procedure and information transfers.

Consider the case when the parallelizable part of the code consists of a number of tasks that require the same execution time. The following condition can be used to characterize the speedup

![]() (133)

(133)

where ![]() and

and ![]() denote the execution times for parallelizable and nonparallelizable parts of the code, respectively,

denote the execution times for parallelizable and nonparallelizable parts of the code, respectively, ![]() , and

, and ![]() denotes the time for information transfers. The measure (133) is a version of Amdahl’s (1967) law, which we augment to include the cost of information transfers

denotes the time for information transfers. The measure (133) is a version of Amdahl’s (1967) law, which we augment to include the cost of information transfers ![]() ; see Nagurney (1996) for a further discussion.

; see Nagurney (1996) for a further discussion.

Two implications of the Amdahl’s (1967) law are the following. First, (133) implies that ![]() , i.e., the fraction of the code that is not parallelizable,

, i.e., the fraction of the code that is not parallelizable, ![]() , is a bottleneck for the speedup. For example, if

, is a bottleneck for the speedup. For example, if ![]() of the code is not parallelizable, i.e.,

of the code is not parallelizable, i.e., ![]() , we can reduce the running time of a code at most by a factor of 2, no matter how many cores we employ. Second, (133) shows that the speedup can be smaller than 1 (which is parallel slowdown) if the cost of information transfers

, we can reduce the running time of a code at most by a factor of 2, no matter how many cores we employ. Second, (133) shows that the speedup can be smaller than 1 (which is parallel slowdown) if the cost of information transfers ![]() is very large.

is very large.

It is straightforward to describe the implications of Amdahl’s (1967) law for the efficiency measure (132). Namely, efficiency of parallelization decreases with the number of cores ![]() reaching zero in the limit

reaching zero in the limit ![]() , which is another way to say that the gains from parallelization are bounded from above by the execution time of tasks that cannot be parallelized. Furthermore,

, which is another way to say that the gains from parallelization are bounded from above by the execution time of tasks that cannot be parallelized. Furthermore, ![]() decreases with the costs of parallelization and transfer, and it can be arbitrary close to zero if such costs are very large.

decreases with the costs of parallelization and transfer, and it can be arbitrary close to zero if such costs are very large.

Finally, different tasks executed in a parallel manner may differ in the amount of time necessary for their execution. For example, when searching for a maximum of a function over different regions of state space, a numerical solver may need considerably more time for finding a maximum in some regions than in others. The most expensive region will determine the speedup and efficiency of parallelization since all the workers will have to wait until the slowest worker catches up. The cost of information transfers may also differ across parallelizable tasks in some applications. These issues must be taken into account when designing codes for parallel computation.

10.2 Parallel Computation on a Desktop Using MATLAB

Most economic researchers write codes for solving dynamic economic models using a desktop and serial MATLAB software. The advantages of this choice are three: first, the user can concentrate exclusively on computations without being concerned with all subtle issues related to the operational system and computer architecture. Second, communication among multiple cores of a desktop is very fast, and can be much faster than that among cores in a cluster or supercomputer. Finally, MATLAB itself is a convenient choice. It is widespread, well-supported, and has an extensive documentation; it is easy to learn and to use; and it has many preprogrammed routines that can be easily integrated into other codes.

In particular, MATLAB provides a simple way to parallelize computations on either CPUs or GPUs; no additional software is needed. Valero et al. (2013) survey parallel computation tools available in MATLAB; below, we reproduce some discussion from this paper.

First, MATLAB has a “Parallel Computing Toolbox” which allows us to allocate the computational effort in different CPUs on multicore computers; see MATLAB (2011). Parallelizing in MATLAB is simple, we just need to replace “for” with its parallel computing version “parfor.” To use it, we must tell to the computer what part of the code we want to parallelize and when we want to finish parallel computation and to gather the output; this is done using “matlabpool open/matlabpool close.” Some restrictions must be imposed on variables that are used in parallel computing.

Second, MATLAB has tools for working with GPUs. Functions “gpuArray” and “gather” transmit data from CPUs to GPUs and vice versa, respectively. It is also possible to generate the data directly in GPUs which can help to save on transfer time, for example, “parallel.gpu.GPUArray.zeros ![]() ” creates an array of zeros of dimension

” creates an array of zeros of dimension ![]() in GPUs. Once you allocate an array in a GPU, MATLAB has many functions which allow you to work directly there. A useful function in MATLAB is “arrayfun” which, instead of multiple calls to perform separate GPU operations, makes one call to a vectorized GPU operation (it is analogous to MATLAB’s vectorized operations). MATLAB has functions that allow us to use native languages for GPU programming; for example, it allows us to use CUDA with the NVIDIA graphical card.19

in GPUs. Once you allocate an array in a GPU, MATLAB has many functions which allow you to work directly there. A useful function in MATLAB is “arrayfun” which, instead of multiple calls to perform separate GPU operations, makes one call to a vectorized GPU operation (it is analogous to MATLAB’s vectorized operations). MATLAB has functions that allow us to use native languages for GPU programming; for example, it allows us to use CUDA with the NVIDIA graphical card.19

Finally, MATLAB has other tools that are useful for parallel computation. “Jacket” and “GPUMat” toolboxes are useful alternatives to the standard “Parallel Computation Toolbox.” Another useful tool is “deploytool” which allows us to convert MATLAB codes into executable files. Also, MATLAB codes can be translated to other languages such as C/C++ or Fortran source code using the “mex” tool. Depending on a specific version of MATLAB, different software may be needed to create the mex files; we use a Microsoft Windows SDK 7.1 with NET Framework 4.0. Function “coder.extrinsic” makes it possible to export to other languages some functions that are specific to MATLAB, e.g., “tic” and “toc.” The above tools allow us to run MATLAB codes on machines that do not have MATLAB installed.

The drawbacks of MATLAB are typical for high-level programming languages: it is relatively slow and does not take into account the hardware characteristics to optimize computations. Also, MATLAB is not free software and can be executed only on those machines that have licenses.

Many other programming languages can be used on a desktop instead of MATLAB. Octave is almost identical to MATLAB and is freeware. Another freeware is Python, a high-level language that is growing in popularity. Significant speedups of calculations can be obtained using low-level languages such as C or Fortran. However, these languages may be more complicated to learn and to use. There are also languages that are specially designed to work with GPUs. A pioneering paper by Aldrich et al. (2010) shows how to apply GPUs using CUDA for solving economic problems; see also Morozov and Mathur (2012). CUDA can only be used with NVIDIA GPUs. However, there is software that can manage other kinds of GPUs, for example, OPEN CL (see http://www.khronos.org), VIENNA CL (http://viennacl.sourceforge.net); see Gallant’s (2012) conference slides for a concise and informative discussion and further references.

10.2.1 Numerical Example of GPU Computation Using MATLAB

The following example is borrowed from Valero et al. (2013). Consider a function with a unique input ![]() , which is randomly drawn from a uniform distribution

, which is randomly drawn from a uniform distribution ![]()

![]() (134)

(134)

We approximate the expectation of ![]() using a Monte Carlo integration method

using a Monte Carlo integration method ![]() .

.

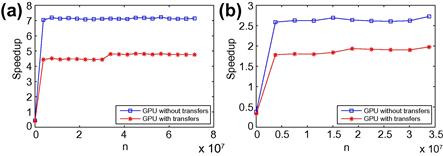

The calculations are implemented in GPUs using MATLAB. We report separately the cases with a single and double precision because the precision significantly affects the speed of GPU computations. To illustrate the cost of transfers between CPUs and GPUs, we report two speedups (a ratio of CPU to GPU running times, see definition (131)): the speedup without information transfers between CPUs and GPUs and that with such transfers.20 We first report the results obtained with “gpuArray” and “gather” functions in Figure 9a and b for the single and double precision cases, respectively.

If the transfer time is included, we observe speedups of order 4.5 and 1.7 under the single and double precision, respectively, when ![]() is sufficiently large (for small

is sufficiently large (for small ![]() , the speedup is negative as the gain from GPUs does not compensate for the high cost of transferring information between CPUs and GPUs).

, the speedup is negative as the gain from GPUs does not compensate for the high cost of transferring information between CPUs and GPUs).

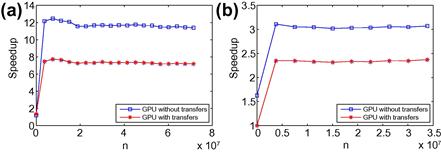

We next repeat the computations using a vectorized version of the code built on “arrayfun”; see Figure 10a and 10b for single and double precision, respectively.

Figure 10 (a) Speedup with GPUs (vectorized): single precision. (b) Speedup with GPUs (vectorized): double precision.

This improves the performance of GPUs considerably. Now, the speedups are of order 7 and 2.4 under the single and double precision, respectively. “Arrayfun” also allows for better allocations of memory. Our hardware for GPU computations is: Intel(®) Core(TM) i7-2600 CPU @ 3.400 GHz with RAM 12.0 GB and GPU GeFoce GT 545, and we use MATLAB 2012a.

10.3 Parallel Computation on Supercomputers

Clusters of computers and supercomputers can solve certain problems of very large size. Clusters are networks that have 16–1,000 cores, and supercomputers may have hundreds of thousands of cores, as well as graphical cards with a huge number of GPUs. However, two issues must be mentioned. First, the information exchange between CPUs or GPUs is generally slower than that between cores on a desktop, which may reduce the gains from parallelization in some applications. Second, using supercomputers requires certain knowledge of the computer architecture and the operational system (typically, Unix), as well as software that distributes and exchanges information among different cores, and the programming can be a nontrivial task.

Three different types of supercomputers are distinguished in the computer science literature; see Blood (2011).

1. High-performance computing (HPC) runs one large application across multiple cores. The user is assigned a fixed number of processors for a fixed amount of time, and this time is over if not used.

2. High-throughput computing (HTC) runs many small applications at once. The user gets a certain number of cores that are available at that time, and this computer time would be wasted otherwise.

3. Data-intensive computing focuses on input-output operations, where data manipulation dominates computation.

We are primarily interested in the first two types of supercomputing, HPC and HTC. An important issue for parallel computation is how to share the memory. Two main alternatives are shared memory and distributed memory.

• Shared memory programming. There is a global memory which is accessible by all processors, although processors may also have their local memory. For example, OpenMP software splits loops between multiple threads and shares information through common variables in memory; see http://www.openmp.org.

• Distributed memory programming. Processors possess their own memory and must send messages to each other in order to retrieve information from memories of other processors. MPI is a commonly used software for passing messages between the processors; see http://www.mpi-forum.org.

The advantage of shared memory is that it is easier to work with and it can be used to parallelize already existing serial codes. The drawbacks are that the possibilities of parallelization are limited and that sharing memory between threads can be perilous. The advantage of distributed memory is that it can work with a very large number of cores and is ubiquitous but it is also more difficult to program. There are also hybrids that use distributed memory programming for a coarse parallelization and that use shared memory programming for a fine parallelization.

High computational power becomes increasingly accessible to economists. In particular, the eXtreme Science and Engineering Discovery Environment (XSEDE) portal financed by the NSF provides access to supercomputers for US academic/nonprofit institutions. Currently, XSEDE is composed of 17 service providers around the world; see https://portal.xsede.org. We discuss two examples of supercomputers within the XSEDE portal, namely, Blacklight and Condor; see http://www.psc.edu/index.php/computing-resources/blacklight and https://www.xsede.org/purdue-condor, respectively.

Blacklight is an example of an HPC machine. It consists of 256 nodes each of which holds 16 cores, 4096 cores in total. Each core has a clock rate of 2.27 GHz and 8 Gbytes of memory. The total floating point capability of the machine is 37 Tflops, and the total memory capacity of the machine is 32 Tbytes. Blacklight has many software packages installed including C, C++, Fortran, R, Python, MATLAB, etc., as well as facilities for running MPI and OpenMP programs. See Maliar (2013) for an assessment of the efficiency of parallelization using MPI and OpenMP on a Blacklight supercomputer.

Condor is an example of an HTC machine. It is composed of a large net of computers. Computers in the net belong to priority users and are not always free (our own computers can become a part of the Condor network if we give them a permission). Condor software detects computers that are not currently occupied by priority users and assigns tasks to them. It passes messages between masters and workers, queues the tasks, detects failures and interruptions, collects the output, and delivers it to users. The Condor network is slower than that of HPC machines but the speed of communication is not essential for many applications, in particular, for those that are naturally parallelizable. Cai et al. (2013a,b) show how to use the Condor network to solve dynamic programming problems.

Computer time can be also bought in the Internet at relatively low prices. For example, Amazon Elastic Compute Cloud provides the possibility to pay for computing capacity by the hour; see http://aws.amazon.com/ec2/#pricing.

MATLAB is of a limited use on supercomputers. For example, at the moment, Blacklight has MATLAB licenses just on 32 cores, meaning that only a tiny fraction of its total capacity is available to MATLAB users. Such users have two alternatives. The first one is to convert MATLAB files into executable files as was discussed earlier (this can work well if we have independent tasks). The other alternative is to use Octave, which is a freeware clone of MATLAB. The problem is that there are still some differences between MATLAB and Octave, and it could happen that the MATLAB code does not work under Octave as expected. For working with a supercomputer, a better alternative is to use languages that are freeware and have no restrictions on the number of licenses (C, R, Python, etc.). These languages have developed parallel programming tools that can be used with MPI or OpenMP.

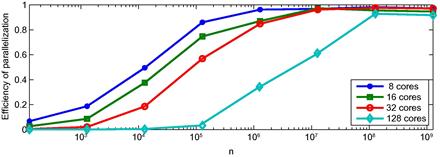

10.3.1 Numerical Example of Parallel Computation Using a Blacklight Supercomputer