THE OBJECTIVE OF THIS CHAPTER IS TO ACQUAINT THE READER WITH THE FOLLOWING CONCEPTS:

Defining governance and IT governance

Identifying who is responsible for implementing governance

The fiduciary responsibility and security requirements that every organization must exercise to protect assets and information

Defining the executive strategy, direction, and objectives

Accepted management practices that are in use to optimize allocation of available resources

How management establishes adequate internal controls for the IT organization

What management needs to do to protect the critical dependencies of information systems in economic transactions

How an organization demonstrates that it has exercised the best available management options to protect itself

Using business process reengineering to fix missing and nonworking processes

To be successful, management must define a strategy and provide for effective corporate governance. Strategy is defined as "an adaptation of behavior or structure with an elaborate and systematic plan of action." Another more specific definition of strategy is "to create a fundamental change in the way the organization conducts business." Obviously the second definition indicates that there are only a handful of people with that much authority. Corporate governance is often defined as "ethical behavior of corporate executives toward shareholders and the stakeholders to maximize the return of a financial investment." To clarify who is responsible for corporate governance, we could use this definition: "to lead by position or authority."

Three high-level management objectives to be verified by the auditor are as follows:

A strategic alignment between IT and the enterprise objectives (formal strategy). Proper planning is required to deploy resources in the right place for the right reason. Management is always responsible for getting it done (corporate governance, preventive controls).

A process of monitoring assurance practices for executive management. The senior executives need to understand what is actually occurring in the organization (staying involved by using detective controls).

An intervention as required to stop, modify, or fix failures as they occur (corrective action). Everyone has some kind of problem. Management should be working to resolve the issue immediately rather than covering it up by hiding the truth.

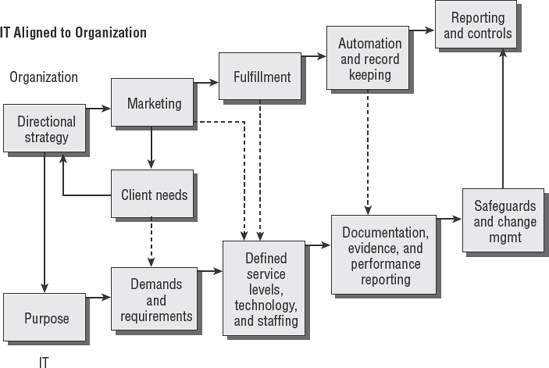

Each organization needs to develop their directional strategy. What direction should the business take to fulfill its goals? The strategy selected progresses to focus on client needs and how to fulfill that market. Critical success factors are selected. Marketing initiatives are designed to generate revenue with plans for fulfillment to the buyer. Figure 3.1 demonstrates the path of organizational requirements in conjunction with the IT requirements.

The revenue process entails a significant amount of administrative overhead and record keeping. The expectation in every business is to make money and not be hampered by a particular technology nor tied to a particular vendor.

The IT department is looking for a clearly stated purpose that IT is expected to fulfill. The department looks at the demands and requirements necessary to be successful. A structured service-level agreement can be generated with this data, complete with staffing and technology growth plans.

Technology plans have to fulfill a business objective. For instance, take Amazon.com. This very successful bookseller isn't necessarily hung up on using Microsoft Windows, Macintosh, or Unix. What the executives want to know is that all the money is processed and the product arrives on time to fulfill their customers' expectations. Systems management and auditing on the back end will verify that all their bookkeeping and internal controls are functioning effectively. In an industry leading move, Amazon added same-day shipping as a $5 option on select stock for customers geographically located in vicinity of the Amazon warehouses. The bookseller downloaded the daily courier route schedules, and then compares the pickup and delivery schedule to the buyer's address. Orders placed in the morning can arrive the same afternoon in select major cities. A same day delivery option is automatically added to the shopping cart for eligible purchases. Amazon demonstrates excellent integration of the business and IT strategy.

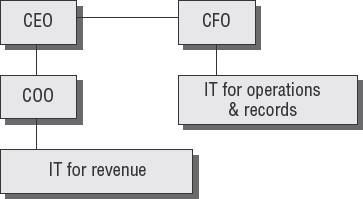

The top side of this diagram is motivated by gains in revenue. Executives take calculated risks to exploit new opportunities for their business to make more money. Conversely, IT is expected to prevent service failures that hurt revenue. IT may also be expected to focus on activities that enable revenue and concurrent activities to prevent loss based on risk management planning. This can make it difficult to determine which problem or goal is the priority. Auditors can gain insight by looking into the IT reporting structure. IT functions reporting to the chief operating officer (COO) are services that generate revenue. IT functions reporting to the chief financial officer (CFO) are internal functions of reporting and processing controls. Refer to Figure 3.2.

The principal mechanism for ensuring IT alignment is to implement an IT steering committee.

Most organizations use an IT strategy committee or IT steering committee. An IT steering committee is used to convey the current business requirements from business executives to the IT executive. The name of the committee is not as important as the function that it performs; a committee may perform more than one function. An IT steering committee may possibly be the same committee used for the purpose of a business continuity steering committee, but with a slightly different charter (focus). What's important is that the job of steering operations to business requirements is occurring.

Steering committees should have a formal charter designating the participation of each member. This charter grants responsibility and authority in a concept similar to an audit charter. An absence of a steering committee charter would indicate a lack of formal controls—a condition warranting management oversight review.

The steering committee is also discussed in Chapter 5, "Life Cycle Management."

Note

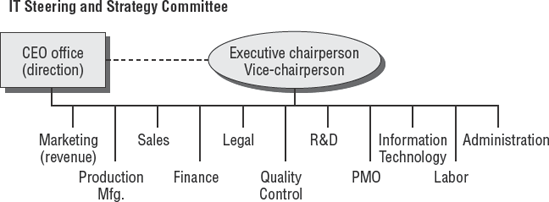

The steering (or strategy) committee is made up of quite a few individuals. Each individual is required to have the authority to act on behalf of their department. These members are vice president–level or higher in the organization so they can help align the IT efforts to specific business requirements. Figure 3.3 shows the basic organizational structure of the steering committee.

The committee is managed by an executive chairperson. The CEO is expected to provide directional guidance in person or via a representative, such as the COO, to identify targeted sources of revenue. Each member of the committee is expected to participate in focus discussions concerning business issues. On occasion, the committee may invite trusted observers or presenters to the meeting to increase awareness of a particular area.

After the business objectives are identified, the next step is to determine the business objectives for IT to fulfill. The steering committee sticks to high-level objectives rather than dictating technical detail.

Let's look at the representation necessary on the steering committee:

- Marketing

Marketing should be represented on the steering committee. The purpose of all marketing is to attract buyers for the organization's product or service. Even if the organization builds the world's finest product, it will not matter unless a steady stream of buyers make a purchase.

- Manufacturing/Software Development

The input from manufacturing or software development is required to align production efforts to sales efforts.

- Sales

The sales function is to convert interested prospects from marketing campaigns into closed sales. Sales executives are interested in using technology to facilitate more sales. The cooperation of manufacturing and technology is necessary to assist the sales effort.

- Finance

Financial guidance and budgeting skills are essential to optimize the organization's investment. Obtaining funding approval for projects would be difficult without the cooperation of the finance comptroller.

- Legal

The executive from the legal department should ensure compliance to the law. Qualified legal counsel advises management in areas of uncertainty. Expert legal counsel should help protect the company from excessive liability or undue risk as a result of a control failure.

- Quality Control

The quality process provides consistency in operations, manufacturing, and risk mitigation. A well-run quality process is a major contributor to the organization's survival. Failures in quality control can damage market image or lead to liability problems.

- Research and Development (R&D)

The Research and Development staff is constantly working on creating new products and improving existing products. The R&D effort is focused on developing products that will generate revenue six months to two years in the future.

Note

Depending on the organization, R&D may be suspended during times of financial shortfall. The planned R&D budget would be applied to projects with a faster return or to pay past-due obligations.

- Project and Program Management

The head of the Project Management Office, if one exists, should be on the committee to advise members on current and proposed projects. Ideas presented by customers may require changes, causing the need for new projects to modify existing programs. Change is required to be successful in business. Remember that projects are temporary, while programs are ongoing for multiple years or even perpetual.

- Business Continuity

The head of business continuity planning should always be in attendance. This person may possess the title of continuity manager or program manager and have the authority of a vice president or major director. This person's job is to assess impact or help exploit opportunities presented in support of the organizational strategy. It's important not to sacrifice continuity in favor of shortsighted decisions.

- Information Technology

The chief information officer (CIO) or vice president of IT listens to business ideas and objectives raised by committee members. This person acts as a liaison to facilitate the involvement of IT. The IT member may delegate planning and research activities to members of the IT organization.

- Human Resources

The management of personnel grows more complex each week. Compliance with federal labor standards is mandatory. International organizations require special assistance that is beyond the expertise of most non-HR executives. Noncompliance can carry stiff penalties.

- Labor Management

An executive representative from any labor organization, such as a labor union, may need to be involved in decisions concerning labor. This can be a touchy subject depending on the organization.

- Administration

Office administration functions include bookkeeping, record keeping, and the processing of paperwork. Every executive would be handicapped without an administrative assistant.

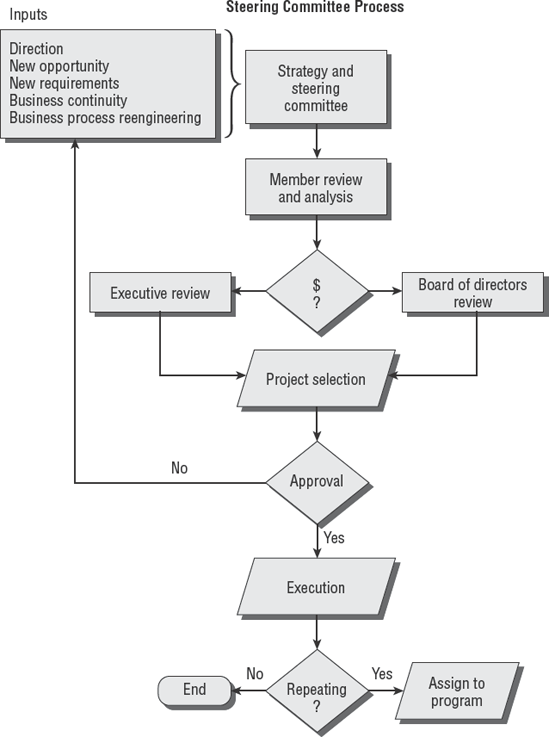

The steering committee reviews ideas and opportunities to make recommendations. Those recommendations go to the board of directors for review. If the idea receives preliminary approval, resources are allocated for project planning. The steering committee executives perform a final review of comparing the total cost and benefit to determine whether the project is a "go" or "no-go."

If a go decision is reached, the organization specifies details, charters the project, allocates funds, commits resources, and moves the plan into execution. If the project is scheduled to be a repeating event, the project is assigned to program status. Otherwise, it is managed as a project with fixed time duration, and the assigned project team members will disband after project completion.

Figure 3.4 is a flowchart of the IT steering process.

In strategic planning, plans generally run in a time frame of three to five years. A tactical plan is going to be carried out over six months to a year and it may go into two years. Daily plans are no more than steps in the tactical plan. When an organization projects three to five years, it is really developing a strategy. This strategy can be to run a streamlined low-cost airline operation like Southwest Airlines, offer the best market reach like eBay, provide competitive rate marketing like Progressive insurance, or use the shipping model of FedEx to assure your package is absolutely positively delivered overnight.

Table 3.1 compares strategic plans, long-term plans, and operational plans.

Table 3.1. Differences between Strategic, Long-Term, and Operational Plans

Item | |||

|---|---|---|---|

Time frame | 3 years + | 1–3 years | 1 year or less |

Question | What business are we in? Should we expand or contract? | What are the major business components? What should we concentrate on now? What products and services are planned? | What specific tasks must be done to meet the long-term plan? |

General broad statement of what business the company is in | Financial goals Market opportunities Management organization Next review period | Assumptions for the period Changes needing to be made Production times Responsibilities Budget |

Now that we have discussed the definition of strategic planning, it is time to get specific about the content of the executive strategy.

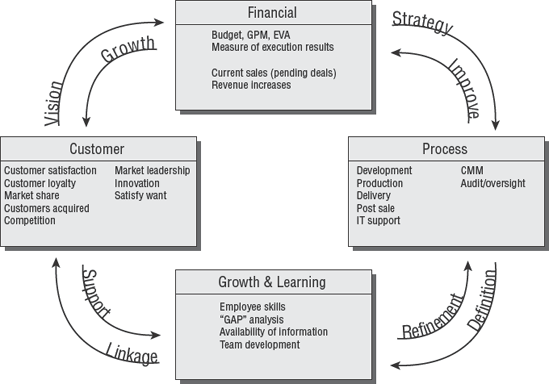

To set forth a strategic goal without proper planning and meaningful definitions would be both negligent and reckless. One of the most powerful executive planning tools available is the balanced scorecard (BSC). The BSC is a strategic methodology designed for senior executives.

Originally, the balanced scorecard was designed in a university environment to be used by business executives for reporting metrics. A very smart person once said, "the product's actual use will be invented at the customer site," meaning you can build what you want, but the customer will determine how it's used to solve their problem. It turns out that the most successful executives are using the BSC to define internal cause-effect relationships of smaller plans that run their business, not just to report metrics as originally conceived.

The scorecard approach converts organizational objectives of customer perception, business processes, employee growth and learning, and financial goals into a series of defined actions. We typically call these actions either projects or programs, but the BSC doesn't care. The BSC refers to projects and programs as initiatives (what you are doing).

Three years ago, after a less-than-successful board meeting, I set a personal goal to learn how to apply the BSC tool. I searched all websites in the first 200 Google results and read every book available from Barnes & Noble. Plenty of people claimed knowledge of the BSC, yet consistently failed to demonstrate how the inner details actually worked. Frankly, none provided enough direction to make it work. I fell into the same trap as everyone else. It takes special training with firsthand experience to receive the benefits that this type of advanced planning tool offers. ISACA just wants you to know it exists. I teach my students in our seminars how to use it, exceeding the exam study requirement. So this section is my short brochure-level introduction on how it works. I use BSC constantly each week and stand behind all my statements with supporting evidence.

When properly implemented, the scorecard concept enforces better alignment by defining details of strategic business objectives. Overused terms such as world class and customer driven are broken down into low-level definitions that the staff can actually implement. Using the scorecard should eliminate activities of little or no strategic value.

The scorecard methodology is common outside the IT environment. Information technology can benefit from using the balanced scorecard if it is implemented by the CEO or CFO. To be effective, the scorecard must be driven from the top down.

Table 3.2 illustrates the four scorecard perspectives and matching emphasis area of the BSC methodology. For example, the finance perspective will place emphasis on cost control and company profits.

Table 3.2. Balanced Scorecard Methodology

Perspective | Emphasis |

|---|---|

Customer | What is our market image? What makes us different? How should the organization appear to the customer? Why would a client want to do business with us? |

Business process | What is our mission? How can we create a genuine competitive advantage? What are our critical success factors? What are the key performance indicators? |

Financial | What are the financial goals? What are the shareholder goals? Are we a cash cow or a pioneer? |

Growth and learning | What information do we need to beat our competition? What are the organization's growth plans? How will we keep or obtain the knowledge and workers necessary to support the organization's plans? |

A smaller number of organizations are successful at using the balanced scorecard approach, while many fail. Upon investigation, several of the failing executives referred to BSC as old news. It did not take long to discover that these executives had a lack of BSC training, misunderstood the objective, and possessed little BSC experience. Let's investigate why this occurs.

The advantages and disadvantages of using the scorecard methodology are as follows:

- Scorecard advantages

It promotes a focus on the specific if-then linkage between different objectives and their budgets. The goal is direct support of organizational objectives. If you change funding or strategy on a linked initiative (project or program), the effect can be seen rippling through the scorecard. We are actually using the BSC to create well-defined articulated strategies.

All the initiatives (project or programs) are linked into a complete process flow that ignores departments and traditional boundaries. Never again will strategy be determined in one meeting and budget determined somewhere else.

When fully implemented, none of the departments will have their own budget to spend. The result is project-based, program-based staffing. It does not matter whether the department function is internal or external.

Each department pledges its level of support to a defined strategy initiative. The corresponding budget money is issued to the department, provided it is meeting its delivery goals. No support of the linked project means no money, no people, and no job. This blocks waste and personal agendas.

Each employee works from a personal scorecard created by cascading the BSC down into specific execution tasks. The combined effect of the personal scorecards will achieve their department's objective. Achievement of the departmental objectives will help fulfill the organizational objectives.

- Scorecard disadvantages

The scorecard requires a careful selection of initiatives by the CEO or CFO. It is reported in executive trade journals that metrics derived from a committee will consistently fail. Interestingly, observations indicate that executives unwilling to adapt to the scorecard methodology may lack a genuine interest in being a team player or may possess more interest in building their own empire within the organization. Politics can kill the BSC unless the sponsor eliminates the people creating political conflict.

The balanced scorecard can contain whatever you need to define. It is flexible in having three, four, or five perspectives depending on what your executives decide is needed. The typical approach of four perspectives is shown in Figure 3.5. Notice how the different initiatives are linked into a complete process.

There are several secrets involved in making the scorecard generate true results. Using a BSC will most likely take beginners at least 20–30 failed attempts, which end in frustration, before it begins to show a glimmer of success. Keep trying; the benefits will far outweigh the effort. Each failed attempt is simply an indicator of an existing relationship problem or definition problem. Problems need to be fixed one by one before you can build an effective linkage. Often this includes retreating a few steps to adapt for changes as they are discovered. That's part of the magic in using BSC. The strategy becomes more defined with each pass, forcing each problem to be fixed before it can effectively function inside the overall strategy plan.

Every planning exercise brings more clarity as you roll the linkages forward and backward to fine-tune the details. It's like using algebra to solve a problem and then using calculus to prove you actually did solve the problem by returning to zero. Now the strategy works forward and backward, with excellent definitions exploding all the details into specific action items. Initiatives (projects or programs) are now selected, scoped, and funded based on which ones generate the highest return on investment (ROI).

What if your project or program doesn't generate revenue? Simply put, it would be linked with a function that is generating revenue and used to calculate the combined operating costs. For example, security costs in a bank are coupled with the profits the bank generates. The final ROI estimate is used to decide whether that area of the business is expanded or shut down. What if you make more money from brokering mortgages? You may switch from being a full-service bank into focusing on mortgages. The final goal is to find the highest-earning ROI and quit wasting resources on marginal or losing activities.

Executives at AMR operate American Airlines and Sabre reservations as two separate companies. One reporter asked which one they would sell if necessary. The response was that American Airlines' business need created Sabre, yet they would keep Sabre, selling the airline if that day ever came. Sabre's reservation system is a better ROI.

The balanced scorecard fundamentally changes how employees prioritize and report their work. Activities and projects are selected on the basis of the value created under established metrics. This also results in a change in how the employee is evaluated. It is essential that management and staff receive proper training prior to implementation. Just remember, without full buy-in at all levels, the balanced scorecard is likely to fail.

The IT balanced scorecard should be a subset of the organization's overall balanced scorecard. When properly implemented, the scorecard methodology supports the highest-level business objectives.

As a CISA, you need to understand how the balanced scorecard can be applied specifically to information technology. ISACA describes the scorecard by using three layers that incorporate the more common four perspectives (customer, business process, financial, and growth and learning). The three layers for IT scoring according to ISACA are as follows:

- Mission

Develop opportunities for future needs. Become the preferred supplier of IT systems to the organization. Obtain funding from the business for IT investments. Deliver effective and cost-efficient IT services. Often the mission statement sounds like an advertising slogan. In reality, the mission statement should be less of a political statement and more specific in definition. Therefore, each mission statement needs supporting details contained in the strategy definition. The goal of the BSC is to convert vague mission statements into clear-cut action items that the staff can understand and then implement.

- Strategy

Attain IT control objectives. Obtain control over IT expenses. Deliver business value through IT projects. Provide ongoing IT training and education. Support R&D to develop superior IT applications. All these sound great, but they need significantly more detail before they can be implemented. Using the BSC can help define the lower-level initiatives necessary to make the mission functional. Far too many executives fail to provide a well-defined, articulate strategy. A definition is needed that maps detailed cross-coordination rolling across departmental boundaries.

- Metrics

Develop and implement meaningful IT metrics based on critical success factors and key performance indicators. We'll cover more in metrics in Chapter 6, "IT Service Delivery."

Tip

The balanced scorecard method is a wonderful tool for the auditor to gain invaluable insight into the organization. A simple BSC exercise will uncover the organization's critical path while illuminating its ROI dependencies.

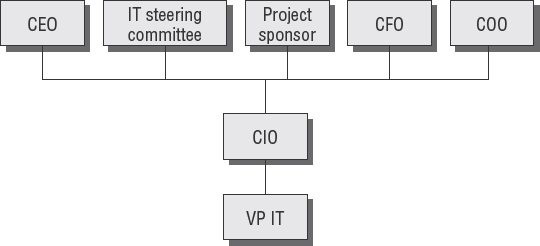

Executive management selects an IT strategy to fulfill their business objectives. The strategy should be approved from the top down. The strategy is then formalized into a policy and communicated throughout the organization. Figure 3.6 shows the executives involved at the strategy level (in policy making).

You should assume that the executives have already gone through the process of gathering requirements. Their strategy may be to insource or to outsource. However, one of their most important questions is to determine how the strategy will be funded. Each of the following methods of funding bears unique advantages and disadvantages:

- Shared cost

It is common for the bulk of IT costs to be allocated as a shared cost across all members of the organization. This method is relatively easy for the finance department to implement. Unfortunately, it may lead to user dissatisfaction. Some users and their managers may feel that they are paying for a service that is not received.

- Charge-back

Individual departments receive a direct charge for system use. This is designed to be a pay-as-you-go style of accounting for IT expenses. Charge-back schemes are quite effective if properly implemented. Mainframe charge-back schemes are particularly effective for usage billing.

- Sponsor pays

This last type can present a significant challenge to IT governance. The project sponsor pays all the bills. In exchange, the sponsor may demand more authority over decisions. This method is notorious for creating shadow support organizations. Shadow organizations indicate willful distrust between executives. Usually the basis of shadow groups is a self-centered agenda that creates a design contributing toward a functional failure. Additional conflicts usually occur with IT management in disputes over budget responsibilities, not implementing all the proper controls, lack of effective monitoring, and improper reporting of failures. The best way to solve the conflict is by fully enforcing separation of duties.

Executive management has the responsibility of setting goals. Each goal should be supported with a defined set of objectives. A strategy should be in place to achieve those objectives. The next step is to specify a policy to communicate management's desires to the subordinates.

Every policy should be designed to define a high-level course of action. The purpose of the policy is to inform interested parties of a chosen solution. A well-designed policy is based on a statement by management of the policy's importance. The statement explains how this particular policy supports a business objective. The policy is signed by the most senior person available to prove authorization.

We discussed the role of policies, standards, and procedures in Chapter 1, "Secrets of a Successful IS Auditor." Table 3.3 should serve as a memory refresher concerning the role of policies, standards, and procedures.

Successful policies are issued from the top down to all subordinates. The policy may designate a department director to create a standard in support of the policy. The final procedures are generated from the workers at the bottom of the hierarchy. Common procedures are intended to be implemented from the bottom up. The procedure is a lower-level person's response in support of the executive's policy.

Policies are designed to inform interested parties about a particular situation. The policy may be advisory, regulatory, or informational:

- Advisory policy

An advisory policy explains the condition to be prevented by the policy and provides notice as to the consequences of failure. The interested party may be an employee. The subject could be acceptable use of the Internet. In the Internet example, the advisory mandate is to either comply or be fired.

- Regulatory policy

The term regulatory indicates that this policy is mandated by some type of law. All organizations under the jurisdiction of the regulation are expected to comply. Failure to comply will result in criminal liability.

- Informational policy

Informational policies inform the public of the organization's operating policies. Examples include the customer privacy policy, the customer refund policy, and the customer exchange policy.

Note

IS auditors should be aware that undefined policies indicate a lack of control.

After the strategy is selected and the goals are set and the policy is created, it's time to begin the planning process. In planning, the strategy is broken down into useable definitions to move it closer to reality.

IT strategy plans must be created to aid the organization in the fulfillment of long- and short-term business objectives. Each IT plan should correlate to a specific organizational goal. The business goal may be to improve customer contact management, expand e-commerce services, or improve operating speed with better software integration. The supporting IT plan could define implementation and support for a new Customer Relationship Management (CRM) system. IT's role is that of a requirements facilitator and custodian. The true strategic value will be determined in the minds of the business executives. There should be a concern if IT's influence is overriding other non-IT business objectives. The IT strategy will be composed of plans for data, software applications, technology, personnel, and facilities.

IT data plans are created in support of the organization's intended use of the data. An example is the creation of a new customer survey system, database marketing system, or financial record-keeping system. The key is to determine what data you really need and how you will protect it. This is accomplished by implementing an information classification program with administrative policies and procedures. Well-run businesses and governments have been doing this for hundreds of years to explain how each piece of data should be handled. After the intended use of the data is recognized, the next step is to define the application to manipulate the data.

Computer software applications are actually methods of accomplishing work. Therefore, a software management plan is necessary to define the type of work to be performed. A consumer bank may be in the same industry as a debt collection company, for example. However, both organizations use different software applications. Computer software applications need to be tailored to fit the client's needs.

Note

Computer software is not an advantage if the competitor uses the same software, unless the implementation is unique and highly customized.

It is possible to gain a competitive advantage by using a different product than the competitor uses. The advantage is attaining a higher level of business integration and/or lower operating costs. The cost argument is the very reason why some software applications use open source MySQL for the database rather than Oracle. Both are fine products. The cost difference may allow for a significant investment in specialized customization by a guru to build highly integrated software, which can create a competitive advantage with a lower overall operating cost. The resulting integrated software may perform a unique function that the competitor will have difficulty obtaining because of required knowledge, lead time needed, or additional capital investment. Cost avoidance can be a competitive advantage. The application risk is that the integration does not occur or the intended application usage is flawed.

Computer application software represents a substantial investment in capital. Computer software creates business risks that must be managed. The risks include process failure, increased operating risk, ineffective results, waste of capital resources, lost time, and increased operating cost for the same effective output.

Technology plans address an organization's technical environment by indicating the types of hardware and software that will be used. Unfortunately, some organizations start with the hardware technology first and attempt to force the data and application requirements into their desired technology. Putting the technology plans first may hinder the results.

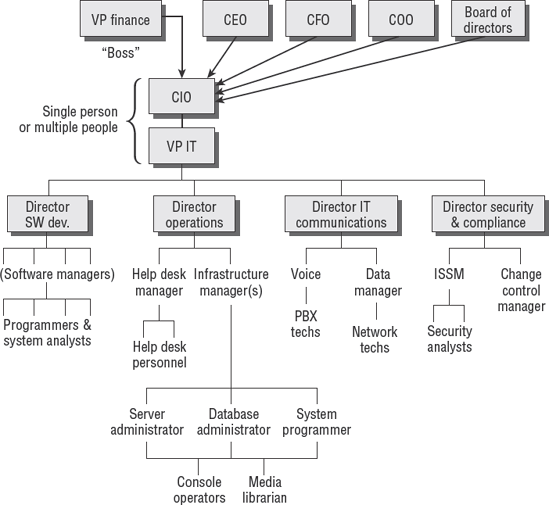

The IT organizational structure needs to be designed to support the business strategy. Information technology is usually regarded as a function of internal administration. This would place IT under the head of internal controls (the CFO, VP of finance, or the comptroller). Figure 3.7 illustrates a typical IT organization. We will discuss the individual positions as we proceed through this chapter.

Tip

Figure 3.7 can serve as a roadmap if you're unsure about the authority of positions we discuss in this chapter.

Finally, the strategy needs to incorporate a facilities plan. Where will the data applications and technology reside? Who will manage the environment? The final decision will be based on the desires of management. These desires can include increased control, insourcing, outsourcing, or a hybrid combination.

Knowing what to do is a challenge for all auditors. Discussions were occurring on this subject long ago in the old Electronic Data Processing (EDP) audit association, before it was renamed ISACA. One of the goals of every association is to add value by improving the performance of its members. ISACA has definitely delivered on this goal. The definitive framework for IS auditing is called the Control Objectives for Information and related Technology, also known as CObIT.

This framework contains a complete set of strategies, processes, and procedures necessary for executives to lead the IT organization. CObIT is now in its fourth edition. Within the supporting manuals, you will find the guidance provided in their audit toolkit invaluable. CObIT is protected under copyright, so it's a good idea not to lose your CISA certification by doing something stupid like having a bootleg copy.

The audit guideline section contains more than enough questions necessary for a first-class audit. It covers the entire spectrum from executive strategy down to device settings. BSC properly combined with CObIT would make a phenomenal audit practice.

Now let's get back to the auditing plan. We have discussed strategy, so the next step is to figure out the work location.

The next step is to identify sourcing locations. The sourcing decision may be based on the operating cost for particular geographic locations. Operating cost is a combined factor of facilities, labor, regulations, and available resources. Organizations may choose to perform functions onsite, in their facility. Alternatively, there may be an advantage to performing functions offsite, at other offices or with an outside vendor. This is a common practice for customer support, employee payroll, and manufacturing. Cheap labor may influence management's decision to move the location offshore, to another country.

Note

Three popular offshore locations include China, India, and Russia. The expected benefits include cheaper labor or lower standards for environmental compliance. The effective cost of steel, concrete, and materials to construct an office is approximately the same worldwide.

Performing functions offshore introduces both opportunities and burdens. The opportunities include a potentially lower production cost. There is also an advantage for an organization to operate 24 hours a day in order to lower turnaround times. Consider the effect when the day shift identifies a problem and the night shift in another country fixes it before the day shift returns in the morning.

Disadvantages include the potential loss of control or the disclosure of proprietary intellectual property. In some countries, the culture, language, or level of education presents unique challenges.

Cultural examples of potential conflicts include India's caste system and Africa's ongoing tribal wars. Another example is the attitudes in some societies toward a woman in an authoritative role.

The world is growing smaller as transportation and communication services improve. Many of the old cultural barriers have been reduced by the global economy. This global economy also has increased the number of competitors in the fierce battle for revenue. An organization at one time worried only about servicing clients in a small number of local time zones. Now customers depend on businesses 24 hours a day, worldwide.

Most administrative and technical support functions can be performed from alternate locations. Some of the services that could be fulfilled from remote locations include the following:

Accounting and bookkeeping

Accounts payable (AP) and accounts receivable (AR)

Data entry and transcription

Live telephone support (including IT, customer service, order taking)

Legal and medical records management and processing

Human resources and benefits administration

Creative advertising production

Printing

Software development

Systems administration

In the following section, you will look at the various types of sourcing methods, what factors go into choosing a sourcing method, and why it is important for you as an IS auditor to be familiar with them.

The decision of location is usually based on the cost of operation, market pressures, or a centralization versus decentralization strategy. Management may choose to hire personnel by using a combination of insourcing and outsourcing. Services provided by internal staff are referred to as in-house (insourced). Services provided by an external vendor are referred to as outsourced. The insourced versus outsourced decision may be based on a case-by-case or project-by-project requirement.

On occasion, an opportunity may present itself that exceeds the capability of the existing service provider. Hybrid sourcing models may be effective under a joint venture or to provide additional capability. The hybrid model combines insourcing and outsourcing on a function-by-function basis.

The advantage of outsourcing is that someone else may be able to perform the work better or cheaper, or frankly may know how to do something others don't. Insourcing provides more control. The hybrid method retains control in selected areas and uses the outsource contractor for collateral work. Outsourcing may allow the client to focus on what they do best, their core revenue generator. A potential disadvantage is losing control under the contract. Maybe the methods used by a subcontractor will cost less because they are cutting corners that, if known, a company might find unacceptable.

The basic decision may result from an executive thinking about the following:

Is this something that the organization wants to do in-house?

Is this something the company should outsource?

Is there an advantage to sending this offshore?

Is the organization bringing it back from offshore?

Will local processing be a competitive advantage?

Is the location here, in this building, or is it in another building?

Businesses may encounter a variety of globalization issues, including international regulation, local laws, tribal rivalries, or cultural class or caste systems. As an organization begins to look at opportunities for global outsourcing, they have to keep in mind the controls and the total costs related to that decision.

A business looks for inexpensive operating facilities with a high-quality labor pool willing to work for lower wages. If the business is going to decide whether to outsource, it needs to look at all the practices and strategies that are in place.

A business can run into problems over the differences in legal regulations between governments. Additional concerns can arise in different currency exchange rates and government taxation methods. Some of these requirements may indicate that foreign outsourcing would not provide any advantage.

Competitive advantage should be a factor in the sourcing decision. For example, American Apparel manufactures clothing exclusively inside the United States and pays better-than-average wages for their industry. Their advantage is a shorter cycle time from market idea to delivery and sale in their stores. American Apparel touts a one-day turnaround from a finished idea. Their competition has to contend with manufacturing and shipping delays measured in months.

In the last few years, Russia and the Baltic states have benefited from increased popularity, as companies reconsider India or choose to outsource for the first time. Increasing operating costs and U.S. consumer rejection are troublesome to companies outsourcing to India. The cost of real estate in India is skyrocketing. China is reeling backward after a virtual tidal wave of product recalls. Additional reasons cited for Russian sourcing include a more convenient proximity to Western Europe, more positive consumer attitudes of acceptance, a well-educated population, financial savings in real estate prices, and the competitive low cost of labor.

When dealing with outsourcing issues, companies need to be aware that what might be legal in one country might not be legal in another. Examples include the European Union (EU) privacy laws, which are much stricter than those of the United States, or the shortfall of intellectual-property laws in China, which frankly don't exist. In China the attitude is that if someone has a copy, they own it. This is where business management needs to understand: How does that country or culture see it?

As a primitive example, just compare the religious holidays and lifestyles that different countries observe. For example, the flow of harmony in the office is considered upset in Japan if everyone does not go to lunch at the exact same time, and return within a couple of minutes of one another. In Mexico, the lunch hour is two hours and often includes drinking alcohol followed by a siesta (nap). It is not uncommon for employees to drink alcohol during the office lunch hour in the United Kingdom (referred to as having a few pints or getting pissed over a few drinks).

While management plans their labor strategy, there should be a provision ensuring continuity of operations for both in-house and outsourced activities.

The biggest downside of outsourcing is liability. Outsourcing permits an organization to reassign the tasks to be performed but not the liability. It's not possible to transfer the actual liability for failure. Insurance may help cover some of the expenses but not the damage to your reputation, the cancelled sales, or the costs of defending a lawsuit.

Consider the situation of Value Jet airlines. A subcontractor violated cargo-loading procedures when it placed a hazardous container in the cargo bay. The container exploded, causing the airplane to crash. A massive media circus was spawned by the event. Value Jet held their subcontractor liable. The public held Value Jet responsible. The public didn't pick the subcontractor; Value Jet did. Value Jet was expected to spend extra time and money to supervise the subcontractor. The airline folded.

Let's consider the long-term effects of the following well-publicized examples of food contamination:

Recently, problems surfaced in many well-known brands of canned pet food. A supplier of ingredients shipped tainted flour, which led to the death of many beloved family pets. Other pet owners reported paying expensive medical bills for emergency care by veterinarians. Retailers trashed their entire inventories of canned pet food and asked for refunds to cover the losses. Pet owners are pursuing lawsuits against the brand for the harm to their pets and their own emotional strain.

ConAgra is involved in legal battles over a bad batch of ingredients used in Peter Pan peanut butter. One lawyer is advertising on television to "keep the jar and call attorney Loncar," thus promoting possible monetary awards for the consumer to sue ConAgra. Wal-Mart sold the same ConAgra peanut butter under its own house brand.

Several products manufactured in China are now banned from the United States and other countries because of unacceptable chemicals in foods or illegal hormones used to grow vegetables and fish.

Outsourcing does not relieve the company's responsibility to test products or services for compliance. In fact, the outsourcer should be trusted less and tested more. The auditor is always interested in how the process of governing all outsourced services is handled.

It's interesting how some vendors can perform the task cheaper than in-house. Unfortunately, the cost and benefit structure might not be telling the whole story. Outsourcing is frequently an option when the organization

Is unable to get the right result

Considers the process is too much work

Fails to define their actual needs

As time goes by, it may be discovered that the outsource provider is taking unacceptable shortcuts or charging higher prices than expected. Additional issues to consider include turnaround time plus increased costs of supervision necessary to maintain the desired results.

Note

Heartland Payment Systems moved their processing back in-house after years of outsourcing. Their service provider was identified as the bottleneck slowing responses for customers and creating other delays in distributing information within Heartland. Management realized that the service provider was limiting their ability to compete in their market. Bringing their processing back in-house saved $3 million and enabled them to deliver next-day funding. Heartland is now able to respond faster to customers, thus winning new business. —Source: Information Week," 20 Great Ideas"

We have discussed strategy and sourcing. Next, we'll discuss the performance of the executives in delivering results.

The executive staff is subject to review by the audit committee. As you recall, it is this committee's job to challenge the assumptions and assurances in the organization. The audit committee is expected to provide management oversight and allow executives the opportunity to discuss confidential issues about the business. An effective audit committee will advise individual executives with an opinion for possible solutions to internal problems.

Independent auditors are hired by the audit committee to provide an impartial (independent) opinion as to the status of internal controls. Audit committees are frequently the client of external audit engagements.

As an IS auditor, you need to find evidence of management governing IT and the enterprise. The composition and performance of the steering committee could be a powerful source of evidence. You may be able to review the plans and meeting minutes from the committee. The auditor's goal is to assess the performance of the CEO and executive management in developing and leading a successful strategy based on business objectives.

By using tactical management, an organization selects a maneuver or technique that will render a better result. The goal of tactical management is to manage the return on investment for information systems. The successful manager will need to establish a requirement for the collection of performance metrics. The performance metrics are used to determine whether the results are improving or deteriorating against a baseline. The same metrics are used to demonstrate management success to the executives and stakeholders.

Figure 3.8 illustrates the tactical level in the organizational chart.

Individuals at the tactical level should be providing support to the strategic objectives. The majority of planning work accomplished at the director level is tactical in nature. Strategic plans are handed down from top management. The director level is expected to fulfill the strategic goals by providing solutions without the authority to make changes in other areas of the organizational structure. A director's authority outside of their own department is limited to requesting and negotiating.

Every IS organization has a number of functions that it should implement to fulfill its strategic plan, its tactical plan, and its daily plan. An auditor looks at any industry-standard benchmarks for performance optimization that have been adopted. Several are available, including the National Institute of Standards and Technology's controls matrix and the Federal Information Security Management Act (FISMA). In addition, the organization may use an organizational planning maturity model such as the Organizational Project Management Maturity Model (OPM3) by the Project Management Institute.

It is possible that the organization benchmarks its business continuity plans and disaster plans after the public domain version of the Business Continuity Maturity Model (BCMM). The organization may have an information assurance program and be using the ISO 27002 or Capability Maturity Model (CMM).

The value of benchmarking is to determine the organization's position and progress as compared to a recognized reference. There are several competitive advantages to benchmarking, the first of which is the ability to attract respect and more-favorable terms from stakeholders. Every IS organization has an issue regarding financial management.

The question comes up, what does IS pay for?

What does the department pay for?

What does the project pay for?

Individual departments may be operating a shadow IT group funded by department budgets. This condition usually indicates some type of failure to align to the business objectives in the strategic plan.

All levels of management are responsible for providing leadership. Good leaders generate better performance from individual employees. To manage is to create an unnatural result. If the same result would naturally occur by itself, then you are not managing it. The objective of management is to get a better result. Every organization needs to plan for how to collect continuous evidence of performance. The minimum requirements of good management include the following:

Performance reporting

General record keeping

Safeguards and implementation details of controls

The auditor needs to review a variety of documents, including the organization's strategic plan, policies, IT plans, and operating procedures. These include plans for training, system mitigation, system certification, disaster recovery, continuity, and the inevitability of change. As an auditor, you will need input from people besides IT management to ensure alignment with the enterprise objectives.

Performance review refers to the identification of a target to be monitored, tracked, and assigned to a responsible party, and the resolution of any open issues.

Existing systems require a regular review to determine the ongoing level of compliance to internal controls and the next steps to take.

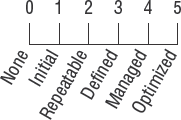

The Capability Maturity Model (CMM) is a method for evaluating and measuring the maturity of processes in organizations. A rating scale from 0 to 5 is used. A score of zero indicates that nothing is occurring. Level 1 maturity indicates that the initial activity was successful and may later progress up to level 5, when the activity is statistically controlled for continuous improvement. The CMM rating scale was developed by the Software Engineering Institute at Carnegie Mellon University and has been widely used for rating business process capabilities.

Note

The Capability Maturity Model is also discussed in Chapter 5.

Levels of the CMM are as follows:

- Level 0 = Nothing yet

The level of zero is implied in the CMM but may not be noticed. This is important when evaluating process maturity. Missing processes and controls without evidence will be rated as zero. Many individuals assume that all controls are present when, in fact, some may be missing. A process or control must have occurred in order to reach a level of maturity (1–5).

- Level 1 = Initial

Processes are unique and chaotic. The organization does not have a stable environment. Success is based on individual competencies and heroics. This level often produces products and services that work. However, output may exceed the available resources or be dependent on specific individuals. At level 1, people have the most freedom and flexibility to make their own decisions.

- Level 2 = Repeatable

Processes are repeatable. The organization uses project management to track projects. The project status is communicated by using milestones with a defined work breakdown structure. The basic standards, processes, descriptions, and procedures are documented.

- Level 3 = Defined

Processes are well documented and understood. Level 3 is more mature and better defined than level 2. Processes have objectives, measurements, improvement procedures, and standards. The results in level 3 are predictable by qualitative measure.

- Level 4 = Managed

Management can use precise measurement criteria to control the processes and identify ways to adjust the results. Processes at level 4 are predictable by quantitative measure.

- Level 5 = Optimized

This is the highest level, with continuous improvement of processes. Objectives for improvement are defined and continually revised to reflect business needs and objectives. Products at CMM level 5 have been so well defined that they are effectively converted into a commodity.

Level 5 is the ideal maturity for the maximum level of control in outsourcing. It allows the company to switch to using less-skilled people who are told what to do, pay less, and demand unquestionable authority. People have the least authority with the fewest decisions at level 5.

Note

CObIT version 4.1 uses the CMM approach to rate auditee performance by the maturity of their control environment.

Figure 3.9 shows the five maturity levels of the CMM in a lateral view.

Frankly, attaining higher levels in the maturity model increases the likelihood that internal controls are successful. A higher CMM grade indicates a definition of maturity with a higher degree of control.

Consider the typical hooks in an outsource contract. The buyer is hooked to it, and so the following questions should be asked:

Did the client give away resources, intellectual-property knowledge, or procedures of value that will not be recoverable?

Has the client given away highly qualified personnel who will no longer be in-house?

What will a contract change cost, if desired?

Can the contract be cancelled?

If a decision is made to cancel, what will it take to get the replacement function online?

This should be enough information for the prospective CISA. Let's take a look at two other sources of governance models. The first is the U.S. National Institute of Standards and Technology.

The U.S. government has set forth standards for engineering, weights and measures, and even computer processing. Management of the standards is assigned to the National Institute of Standards and Technology (NIST). The NIST standards for information technology management are mandatory for government agencies and optional for nongovernmental organizations. Many of the IT best practices were derived from NIST.

The U.S. government passed new internal control regulations under FISMA to unify the former Federal Information Processing Standards (FIPS). The U.S. internal control rating requirements for compliance are posted on the NIST website under the heading for special reports (http://csrc.nist.gov). NIST is an excellent resource with governance models that implement the CMM. Now let's look at an international standard.

Not to be outdone by the United States, the British government enacted their own security standard for government systems in 1995. The standard for British information security is British Standard 7799-1 (BS-7799 part 1). This uses similar internal controls for governance of IS systems. The ISO ratified the BS-7799-1 framework as ISO standard 17799. It then renamed 17799 as ISO standard 27002. ISO 27002 contains numerous points that are identical to the U.S. standards and work in concert. The ISO 27002 is actually functioning quite well as the executive summary for implementing the U.S. NIST 800-53 standard.

Just a reminder: ISO standards are protected by international copyright. Each country sells a single-user copy for the equivalent of $1 U.S. per page. That's how ISO gets funding. CISAs should not have bootleg copies under any condition. Besides the illegal issues, it violates your certification. Remember, the person who turns you in will usually get amnesty.

With so much attention on internal controls, the most important step an organization can take is the first—to implement controls. Any one of these best practices models should already be implemented.

We have already discussed the basics of quality management in Chapter 2, "Audit Process." Every organization should have processes in place to ensure that people are taking steps to do the right job at the right time. Quality management is a pervasive requirement.

Note

We will discuss quality further in Chapter 5.

In Chapter 1, we discussed a few basics of project management and the defined project management processes. Every organization should be following a well-defined project management methodology. Larger organizations will implement a Project Management Office (PMO). The PMO is composed of project managers for the organization. Their function is to manage the larger or more-critical projects.

As a CISA, you should recall that each project will have at least four distinct phases. Recall that the Project Management Institute defines five phases of project management: Initiating, Planning, Executing, Monitoring and Controlling, and Closing. However, PMI considers the process of getting a sponsor as the phase of project initiation. Most employees will never be involved in the Initiating phase. Therefore, ISACA wants the IS auditor to understand the four common phases of Planning, Executing (scheduling), Monitoring and Controlling, and Closing.

Now let's look at risk management in IT governance.

Risks occur at all levels. There are strategic risks, tactical risks, operational risks, and inherent risks. We have discussed these definitions in Chapters 1 and 2. Now let's look at one of the more common risk management formulas.

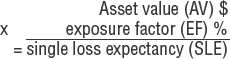

The first step in risk management is to calculate how much a single loss event would cost. This formula multiplies an asset value (expressed in dollars) by the percentage of loss for a particular event. For example, the percentage of loss of a stolen purse is likely to be 100 percent. In that example, the loss would be 100 percent of purse value. The loss due to data-entry errors may be equal to .007 percent of labor cost. This first formula is expressed as follows:

The single loss expectancy can be multiplied by the number of related events that are likely to occur for the year. The final result would be the estimated annual loss, as shown in the following formula:

Risk management should be pervasive in all areas of business, including the IT department. As you might recall, we covered risk management previously in Chapter 2. The choices are to avoid, mitigate, transfer, accept, or eliminate the risk, and the goal is to reduce the level of risk.

When developing a risk management program, the auditor wants to find evidence that the risk management function has been implemented with an established purpose—in other words, that someone has been assigned responsibility, and risk management is a formal ongoing process, not just a review by lawyers.

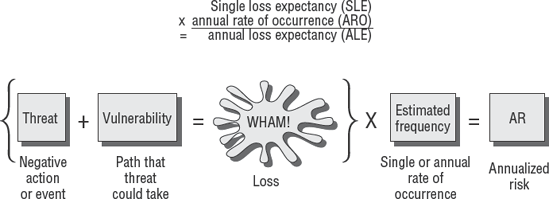

Risks can involve many areas of the business. Impacts can be direct or indirect, but in either case will damage the organization's position, capital, or future opportunities. Typical assets include the organization's customer list, general information (which could be information about marketing or development), data, files, hardware, and software. Assets could also include the facility, a particular document, or services rendered. The risks, or threats, could be terror acts, malicious fraud, executing the wrong procedure, theft, or failure of controls.

It's interesting that criminals do not look at vulnerabilities the same way as an upstanding individual. To a criminal mind, a window becomes an entry or exit point to a building with the aid of a brick.

Risk management operates at a variety of levels: Management at the strategic level focuses on whether going forward with a particular strategy over a period of years is a good idea. Management could be at a project level—is the project on track? Or it could be at a daily or hourly or by-the-minute operational level to ensure that personnel are doing what they are supposed to do. Frankly, most major disasters are caused by a domino effect of a tiny failure multiplying into multiple failures that become catastrophic.

Overall, situations of high risk—where high loss, high consequence, or high impact is possible—require a method to ensure that the problem receives adequate consideration and the appropriate level of effort to prevent an unfortunate outcome. It is extremely common for IT staff to execute poor change control when dealing with interruptions, failures, theft, fraud, or just general risk while under pressure.

Determining the requirements related to hiring or terminating outsourced personnel can be challenging. Several companies have discovered way too late that certain organizations in the European Union have some rather stout requirements for expatriation and repatriation. The company may be liable for future employee benefits and the individual's cost of relocation. The requirements could also include severance plans that provide advance pay of up to about a year, the company's purchase of the former employee's home because that person did not have time to sell it, and payment of medical expenses for six months to a year. These requirements can make a huge difference if a company is planning changes such as layoffs or is trying to determine whether hiring a contractor is a good idea.

Every organization communicates sensitive data over delicate communication lines, which are not necessarily secure. In fact, every government has mandates to conduct surveillance for foreign intelligence in order to provide trade advantages for their citizens. News articles indicate that government organizations from competing countries are attempting to bring foreign technology to domestic organizations. It's the old game of economic espionage and political advantage. Data security is the number one concern when planning for communication crossing the border. We refer to this as transborder communication. One of the challenges is determining whether the data is legal or regulated across the border. The next concern may be that infrastructure issues impede delivery or quality of service from a geographically remote location.

Note

France was the first country to implement an organized system of spying on foreign nationals, beginning in the fourteenth century. The United States was one of the later countries to follow this initiative. Surveillance is mandated in the United States under the Foreign Intelligence Surveillance Act of 1978 (USC Title 50 Chapter 36, FISA).

IT governance is founded on the implementation of formal policies and standards. Each standard is supported by a matching procedure. The purpose of IT governance is to ensure that the risks are properly managed by mitigation, avoidance, or transfer. Let's review a short list of the policies required to address issues faced by IT governance:

- Intellectual property

The term intellectual property refers to data and knowledge that is not commonly known. This information possesses a commercial value. The IS auditor should understand how the organization is attempting to protect its intellectual property. There is no method for registering a trade secret. The owner has to undertake all control measures necessary to keep it secret. The rights of intellectual property can be destroyed by a failure of the organization to take preemptive action.

- Data integrity

What mechanisms have been put in place to ensure data integrity? Does the organization have input controls? How is the data validated for accuracy? Are the systems formally reviewed in a certification and accreditation process? What level of security management and access controls are present? Internal controls for data integrity are required by most industries and government regulation. The goal of data integrity is to ensure that data is accurate and safely stored.

- Backup and restoration

What are the plans and procedures for data backup and restoration? The number one issue in IT is loss of data due to faulty backup. The failures can be procedural or technical.

- Security management

Without security controls, ensuring data integrity is impossible. Internal controls prevent unauthorized modifications. SOX and FISMA mandate strong security controls.

- Mandatory versus discretionary controls

Every control is based on the human implementation. The organization needs to clearly identify its management directives for implementation of controls. Every control will be one of two fundamental types:

- Mandatory control

This is the strongest type of control. The implementation may be administrative or technical. A mandatory control is designed to force compliance without exception. Mandatory controls are managed from a centralized authority.

- Discretionary control

The weakest type of control is discretionary. In a discretionary control, the user or delegated person of authority determines what is acceptable.

- Monitoring

The IT systems should be monitored throughout the entire life cycle and in daily operations. The monitoring process provides valuable metrics necessary to compare alignment to business objectives. The purpose of governance is to lead. It would be impossible to lead without understanding ongoing conditions. Monitoring may prove that the organization is well run or a ticking time bomb. Without monitoring, determining whether an incident needs attention would be impossible.

- Incident response

A response is required for skilled individuals to deal with technical problems or the failure of internal controls. An incident may be major or minor depending on the cir cumstances. It is necessary to have an established policy, standard, and procedure for handling the incident response. At the beginning of an incident, it is impossible to accurately foretell the full impact of possible consequences. An incident response team should be in place to investigate suspicious situations. Care and diligence is necessary because it may later be determined that the initial response area is a crime scene. The mishandling of evidence could lead to forfeiture of the organization's damage claims. Unproven allegations against an individual or organization will frequently result in financial liability by the accuser.

Note

We discuss the details of monitoring and incident response in Chapter 6.

IT governance is conjoined with requirements to properly manage people. Good management is founded on human resource management that is well defined, fair, and consistent. Let's take a look at a few of the HR-related policies that affect IT management:

- Hiring

What are the organization's policies for selecting the best candidate? How should the interview process be handled? Quality management is required during the hiring process to ensure that the organization is in compliance with equal opportunity standards.

- Termination

Personnel may be terminated via either friendly or unfriendly procedures. The requirements for layoffs are relatively clear. What are the procedures for terminating personnel over extended periods of time? A special procedure may be necessary in the case of an upcoming personal retirement. A different procedure may apply to an employee who will be returning as a contractor on the same project. A hostile termination could stem from workplace violence, a criminal act, fraud, or a dispute with other personnel.

- Employee contracts

Many organizations use employee contracts to specify terms of employment. This technique is typically in effect in states with a Right to Work law. Right to Work laws are primarily about union versus nonunion employment—that people have a right to decide whether they want to be part of a union, that union membership can't be a condition of employment. The use of employment contracts is invaluable for identifying the ownership of new discoveries. The employment contract details that the individual is performing work for hire, to the benefit of the employer organization.

- Confidentiality agreement

A standard practice is for employees and contractors to sign a confidentiality agreement. The purpose is to ensure that strategic, tactical, and operational details are not divulged outside the organization. Operating without a confidentiality agreement is usually a significant risk.

- Noncompetition agreement

The employer may implement a noncompete agreement to prevent the employee from working for a competitor until after a specific period of time. The terms of this type of agreement may be successful as long as they are not overly restrictive for the amount of money paid to the employee.

- Ethics statements

The organization should provide a statement of what is acceptable and unacceptable behavior. The best method for preventing a problem is to explain to an individual what actions are acceptable. Unacceptable behavior includes any activities for personal gain at the expense of the organization.

- Performance evaluation

A standardized process should be in place for reviewing an employee's performance. Each employee in the same basic role should be judged by their manager on defined criteria, pertinent to their organizational role. A quarterly or annual review is customary. More-progressive organizations may conduct reviews on a weekly or monthly basis. The morale of hard-working employees is damaged if the boss fails to notice their good work. The results of each review fall under HR record retention requirements for several years.

- Promotion policy

What is the organization's promotion policy? Is it based on job performance, education, or something else? The organization is required to demonstrate a fair and objective promotion policy in order to meet equal opportunity compliance.

- Work schedule

Work schedules and vacation schedules should be clearly defined. In some financial organizations, the vacation schedule is implemented as a detective control. An individual is forced to take vacations in one- or two-week increments. During their absence, another individual performs that job, and a discovery audit may take place to ensure that no irregular or illegal acts have been committed by the employee.

- Corrective counseling

What are the organization's policies for corrective counseling after poor performance from the employee? Care must be taken to prevent discrimination. An improper termination can create a financial liability. An employee may collect monetary damages if able to prove wrongful termination.

These are just a few of the many policies and procedures necessary to manage human resources. The IS auditor should be concerned about activities that increase the organization's level of risk. This includes Human Resources activities.

All computer systems need to be managed through their entire life cycle. Each system will go through a series of phases starting with a feasibility study. Next, requirements are generated and followed by system design. Systems are tested for integrity, and their fitness of use is determined. The life cycle continues into system implementation. After successful implementation, the system can migrate into production use. Each year of production, the system should undergo a review. The annual post implementation review focuses on the system's present condition compared to the more current requirements. A system may be upgraded to the new requirements or retired. This is just a summary.

The CISA is interested in understanding how the organization manages each phase of this process. Evidence should be obtained to support the auditor's conclusions.

Note

We cover the system life cycle in more depth in Chapter 5.

Information technology systems are so pervasive today that most organizations would cease to operate if their computers were unavailable. IT governance requires continuity planning for systems and data. Any disruption to operations could have far-reaching effects. Members of the media can be merciless in their quest to report an interesting story. The damage to an organization's reputation and brand can be fatal. ISACA wants every CISA to be aware of the need for continuity planning. We have expanded coverage of business continuity in Chapter 8, "Business Continuity and Disaster Recovery."

Adequate insurance is the minimum response for asset protection. This is a corrective administrative control. There are issues concerning insurance including the cost versus actual benefits received. Insurance does not replace lost market share, nor damage from unauthorized disclosure of confidential information. Acts of god, war, and terrorism are exempt from coverage in most insurance policies. Proper risk management reduces the organization's exposure. Risk reduction efforts, combined with insurance, are a good practice.

Note

Normally, the term self-insurance implies a level of protection that does not exist. Self-insurance means the organization is accepting the risk with full liability for any consequences.

The CISA should be aware that there is a difference between real insurance and self-insurance.

Performance management serves to inform executives and stakeholders as to the progress of current activities. A fair and objective scoring system should be used. Scores may be based on a current service-level agreement. Another method is to use key performance indicators (KPIs), which tend to represent a historical average of monitored events. Unfortunately, a key performance indicator may indicate a failing score too late to implement a change. A perfect example of a KPI is the high-school report card. By the time the score is reported, the target child may not be eligible to graduate.

A process should exist to report the performance of IT budgets and noncompliant activities. Executive management should encourage the reporting of issues without punishing the messenger. Some effort is necessary to ensure the accurate and timely flow of information upward to the executives. False information can be very damaging.

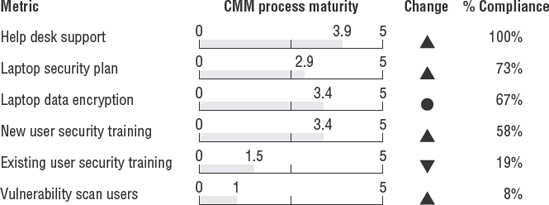

Instead of just having a qualitative assessment of good or bad, or high, medium, or low, this should be an accounting exercise using a quantitative measure. It could be semi quantitative, using a ranking scale similar to scoring in a school: 70 to 79 is a C, 80 to 89 is a B, 90 to 100 represents an A, and then percentages such as A– or A+. This technique will convert a subjective decision into a more objective review. The Capability Maturity Model is very effective for communicating performance metrics.

Figure 3.10 shows a brief glimpse of the CMM used to report metrics.

When an organization decides to consider outsourcing, one of the concerns is that the organization may lose the visibility necessary to effectively operate the processes. The outsource contract should require a right to audit the service provider. Occasionally the response is that they cannot be audited by everyone because they do not have the time or the money, but will give you a copy of the SAS-70 service provider's audit report, which is a standard audit format.

Unfortunately, the report may be insufficient to management needs, because the report is probably vetted and groomed to ensure it states the level of information the service provider wants to convey, not necessarily what may be observed during your own audit.

Our suggestion is that if a company is considering outsourcing, the auditor could ask, "Why not run a controls audit and an SLA audit using the client's auditor, or a full audit before signing the contract?" The goal is to determine whether the service provider is fulfilling their entire obligation before signing a contract. Why risk the time and money to sign a contract while silently hoping and praying that the requirements are met?

Tip

An excellent idea is to implement a business process review before outsourcing.

One of the principles in business that remains constant is the need to improve your processes and procedures. Most trade magazines today contain discussions of the detailed planning necessary for implementing change in an organization. The concept of change must be accepted as a fundamental principle. Terms such as business evolution and continuous improvement ricochet around the room in business meetings. It's a fact that organizations which fail to change are destined to perish.

As a CISA, you must be prepared to investigate whether process changes within the organization are accounted for with proper documentation. All internal control frameworks require that management be held responsible for safeguarding all the assets belonging to their organization. Management is also responsible for increasing revenue. Let's discuss why business process reengineering (BPR) review is important.

Tip