Financial Management

![]() Define the role of the financial manager.

Define the role of the financial manager.

![]() Describe financial planning.

Describe financial planning.

![]() Outline how organizations manage their assets.

Outline how organizations manage their assets.

![]() Discuss the sources of funds and capital structure.

Discuss the sources of funds and capital structure.

![]() Identify short-term funding options.

Identify short-term funding options.

![]() Discuss sources of long-term financing.

Discuss sources of long-term financing.

![]() Describe mergers, acquisitions, buyouts, and divestitures.

Describe mergers, acquisitions, buyouts, and divestitures.

Raising Capital

Like other phone companies in Europe, Telecom Italia is struggling to fund improvements in its fixed and mobile networks. Raising capital for these projects is never easy, and given the economic conditions in Europe, this task is likely more difficult for company executives.

Recently, the company launched a plan to raise up to 3 billion euros ($4 billion) in a costly hybrid debt offering while halving its dividend to help fund its infrastructure spending. In raising new capital, Telecom Italia said it had opted for hybrid debt—which combines elements of both debt and equity—instead of a straightforward share issue because it did not want to upset its shareholding structure.

“Our shareholders have to be protected,” Chairman Franco Bernabe said in a conference call. “We want to strengthen our infrastructure both in Italy and in Brazil and Argentina but at the same time we want to keep our deleveraging path.”1

The chairman's comments mean that the company needs to walk a very fine line with its investors. Raising money solely by issuing stock dilutes the value of the existing shareholders' positions, causing the per-share price of the stock to decline. On the other hand, issuing bonds causes the company to become increasingly leveraged (that is, increasing debt), resulting in higher interest payments and reduced earnings. Thus, Bernabe and his finance team settled on a hybrid approach, offering some debt and some equity to raise the necessary funds.

Organizations often use complicated financial transactions like this to meet their capital needs. And getting it right is a challenge, particularly for a telecommunications company that requires significant amounts of capital to build and maintain their networks.

Overview

finance planning, obtaining, and managing a company's funds to accomplish its objectives as effectively and efficiently as possible.

Previous chapters discuss two essential functions a business must perform: producing a good or service and marketing it to prospective customers. This chapter introduces a third, equally important, function: ensuring that an organization has enough money to perform its other tasks successfully, in both the present and the future, and that these funds are invested properly. Adequate funds must be available to buy materials, equipment, and other assets; pay bills; and compensate employees. This third business function is finance—planning, obtaining, and managing the company's funds in order to accomplish its objectives as effectively and efficiently as possible.

For an organization like Telecom Italia, financial objectives include not only meeting expenses and investing in assets but also maximizing overall worth, often determined by the value of the firm's common stock. Financial managers are responsible for meeting expenses, investing in assets, and increasing profits to shareholders. Solid financial management is critical to the success of a business.

This chapter focuses on the finance function of organizations. It begins by describing the role of financial managers, their place in the organizational hierarchy, and the increasing importance of finance. Next, the financial planning process and the components of a financial plan are outlined. Then the discussion focuses on how organizations manage assets as efficiently and effectively as possible. The two major sources of funds—debt and equity—are then compared, and the concept of leverage is introduced. The chapter also discusses major sources of short-term and long-term funding and concludes with a description of mergers, acquisitions, buyouts, and divestitures.

The Role of the Financial Manager

The Role of the Financial Manager

financial managers executives who develop and implement the firm's financial plan and determine the most appropriate sources and uses of funds.

Because of the intense pressures they face today, organizations are increasingly measuring and reducing the costs of business operations as well as maximizing revenues and profits. As a result, financial managers—executives who develop and implement their firm's financial plan and determine the most appropriate sources and uses of funds—are among the most vital people on the corporate payroll.

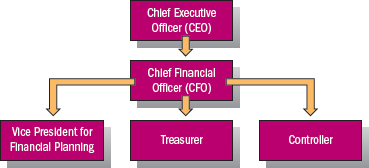

FIGURE 17.1 shows what the finance function of a typical company might look like. At the top is the chief financial officer (CFO). The CFO usually reports directly to the company's chief executive officer (CEO) or chief operating officer (COO). In some companies, the CFO is also a member of the board of directors. In the case of the software maker Oracle, both the current CFO and the former CFO serve on that company's board. Moreover, it's not uncommon for CFOs to serve as independent directors on other firms' boards, such as HP, Microsoft, and Target. As noted in Chapter 15, the CFO, along with the firm's CEO, must certify the accuracy of the firm's financial statements.

Reporting directly to the CFO are often three senior managers. Although titles can vary, these three executives are commonly called the vice president for financial management (or planning), the treasurer, and the controller. The vice president for financial management or planning is responsible for preparing financial forecasts and analyzing major investment decisions, such as new products, new production facilities, and acquisitions. The treasurer is responsible for all of the company's financing activities, including cash management, tax planning and preparation, and shareholder relations. The treasurer also works on the sale of new security issues to investors. The controller is the chief accounting manager. The controller's functions include keeping the company's books, preparing financial statements, and conducting internal audits.

risk-return trade-off process of maximizing the wealth of a firm's shareholders by striking the optimal balance between risk and return.

In performing their jobs, financial professionals continually seek to balance risks with expected financial returns. Risk is the uncertainty of gain or loss; return is the gain or loss that results from an investment over a specified period of time. Financial managers strive to maximize the wealth of their firm's shareholders by striking the optimal balance between risk and return. This balance is called the risk-return trade-off. For example, relying heavily on borrowed funds may increase the return (in the form of cash) to shareholders, but the more money a firm borrows, the greater the risks to shareholders. An increase in a firm's cash on hand reduces the risk of being unable to meet unexpected cash needs. However, because cash in and of itself does not earn much, if any, return, failure to invest surplus funds in an income-earning asset—such as in securities—reduces a firm's potential return or profitability.

Every financial manager must perform this risk-return balancing act. For example, in the late 1990s, Airbus wrestled with a major decision: whether to begin development and production of the giant A380 jetliner. The development costs for the aircraft—the world's largest jetliner—were initially estimated at more than $10 billion. Before committing to such a huge investment, financial managers had to weigh the potential profits of the A380 against the risk that profits would not materialize. With its future on the line, Airbus decided to go ahead with the A380, spending more than $15 billion on research and development. The A380 entered commercial service a few years ago. Airbus currently has 262 confirmed orders for the A380 and so far has delivered 103 planes to such carriers as Emirates, China Southern Airlines, Air France, Lufthansa, Qantas Airways, and Singapore Airlines.2

Financial managers must also learn to adapt to changes in the financial system. The recent credit crisis has made it more difficult for some companies to borrow money from traditional lenders such as banks. This, in turn, has forced firms to scale back expansion plans or seek funding from other sources such as commercial financing companies. In addition, financial managers must adapt to internal changes as well.

Quick Review

![]() How is the finance function structured at the typical firm?

How is the finance function structured at the typical firm?

![]() Explain the risk-return trade-off.

Explain the risk-return trade-off.

Before committing to building the A380 jetliner, financial managers at Airbus had to weigh the potential profits for the company against the risk that the investment would not be profitable. The plane entered commercial service a few years ago, and the company currently has more than 262 confirmed orders.

Financial Planning

Financial Planning

financial plan document that specifies the funds needed by a firm for a period of time, the timing of inflows and outflows, and the most appropriate sources and uses of funds.

Financial managers develop their organization's financial plan, a document that specifies the funds needed by a firm for a given period of time, the timing of inflows and outflows, and the most appropriate sources and uses of funds. Some financial plans, often called operating plans, are short term in nature, focusing on projections no more than a year or two in the future. Other financial plans, sometimes referred to as strategic plans, have a much longer time horizon, perhaps up to five or ten years.

Regardless of the time period, a financial plan is based on forecasts of production costs, purchasing needs, plant and equipment expenditures, and expected sales activities for the period covered. Financial managers use forecasts to determine the specific amounts and timing of expenditures and receipts. They build a financial plan based on the answers to three questions:

- What funds will the firm require during the planning period?

- When will it need additional funds?

- Where will it obtain the necessary funds?

Some funds flow into the firm when it sells its goods or services, but funding needs vary. The financial plan must reflect both the amounts and timing of inflows and outflows of funds. Even a profitable firm may face a financial squeeze as a result of its need for funds when sales lag, when the volume of its credit sales increases, or when customers are slow in making payments.

In general, preparing a financial plan consists of three steps:

- Forecast sales.

- Determine longer-term profits.

- Estimate what the firm will need to support projected sales.

The sales forecast is the key variable in any financial plan because without an accurate sales forecast, the firm will have difficulty accurately estimating other variables, such as production costs and purchasing needs. The best method of forecasting sales depends on the nature of the business. For instance, a retailer's CFO might begin with the current sales-per-store figure. Then he or she would look toward the near future, factoring in expected same-store sales growth, along with any planned store openings or closings, to come up with a forecast of sales for the next period. If the company sells merchandise through other channels, such as online, the forecast is adjusted to reflect those additional channels.

Next, the CFO uses the sales forecast to determine the expected level of profits for future periods. This longer-term projection involves estimating expenses such as purchases, employee compensation, and taxes. Many expenses are themselves functions of sales. For instance, the more a firm sells, generally the greater its purchases. Along with estimating future profits, the CFO would also determine what portion of these profits will likely be paid to shareholders in the form of cash dividends.

Costco has a lower asset intensity than a typical manufacturing business might have.

Next, the CFO estimates how many additional assets the firm will need to support projected sales. Increased sales, for example, might mean the company needs additional inventory, stepped-up collections for accounts receivable, or even new plants and equipment. Depending on the nature of the industry, some businesses need more assets than do other companies to support the same amount of sales. The technical term for this requirement is asset intensity. For instance, DuPont has approximately $0.68 in assets for every dollar in sales. So for every $100 increase in sales, the firm would need about $68 of additional assets. Costco, by contrast, has roughly $0.34 in assets for every dollar in sales. It would require an additional $34 of assets for every $100 of additional sales. This difference is not surprising; manufacturing is a more asset-intensive business than retailing.

A simplified financial plan illustrates these steps. Assume a growing company forecasts that next year's sales will increase by $40 million to $140 million. After estimating expenses, the CFO believes that after-tax profits next year will be $12 million and the firm will pay nothing in dividends. The projected increase in sales next year will require the firm to invest another $20 million in assets, and because increases in assets are uses of funds, the company will need an additional $20 million in funds. The company's after-tax earnings will contribute $12 million, meaning that the other $8 million must come from outside sources. So the financial plan tells the CFO how much money will be needed and when it will be needed. Armed with this knowledge, and given that the firm has decided to borrow the needed funds, the CFO can then begin negotiations with banks and other lenders.

The cash inflows and outflows of a business are similar to those of a household. The members of a household depend on weekly or monthly paychecks for funds, but their expenditures vary greatly from one pay period to the next. The financial plan should indicate when the flows of funds entering and leaving the organization will occur and in what amounts. One of the most significant business expenses is employee compensation.

A good financial plan also includes financial control, a process of comparing actual revenues, costs, and expenses with forecasts. This comparison may reveal significant differences between projected and actual figures, so it is important to discover them early to take quick action.

Quick Review

![]() What three questions does a financial plan address?

What three questions does a financial plan address?

![]() List the steps involved in creating a financial plan.

List the steps involved in creating a financial plan.

Managing Assets

Managing Assets

As we noted in Chapter 15, assets consist of what a firm owns. But assets also represent uses of funds. To grow and prosper, companies need to obtain additional assets. Sound financial management requires assets to be acquired and managed as effectively and efficiently as possible.

SHORT-TERM ASSETS

Short-term, or current, assets consist of cash and assets that can be (or are expected to be) converted into cash within a year. The major current assets are cash, marketable securities, accounts receivable, and inventory.

- Cash and marketable securities are used mainly to pay day-to-day expenses, much as when individuals maintain a balance in a checking account to pay bills or buy food and clothing. Most organizations also strive to maintain a minimum cash balance in order to have funds available in the event of unexpected expenses. As noted earlier, because cash earns little, if any, return, most firms invest excess cash in so-called marketable securities—low-risk securities that either have short maturities or can be easily sold in secondary markets. Money market instruments are popular choices for firms with excess cash.

- Accounts receivable are uncollected credit sales and can be a significant asset. The financial manager's job is to collect the funds owed the firm as quickly as possible while still offering sufficient credit to customers to generate increased sales. In general, a more liberal credit policy means higher sales but also increased collection expenses, higher levels of bad debt, and a higher investment in accounts receivable.

Management of accounts receivable is composed of two functions: determining an overall credit policy and deciding which customers will be offered credit. Formulating a credit policy involves deciding whether the firm will offer credit and, if so, on what terms. Will a discount be offered to customers who pay in cash? Often, the overall credit policy is dictated by competitive pressures or general industry practices. If all your competitors offer customers credit, your firm will likely have to as well. The other aspect of a credit policy is deciding which customers will be offered credit. Managers must consider the importance of the customer as well as its financial health and repayment history.

- Inventory management can be complicated because the cost of inventory includes more than just the acquisition cost. It also includes the cost of ordering, storing, insuring, and financing inventory as well as the cost of stockouts, or lost sales due to insufficient inventory. Financial managers try to minimize the cost of inventory, but production, marketing, and logistics also play important roles in determining proper inventory levels. Also, trends in the inventory turnover ratio can be early warning signs of impending trouble. For instance, if inventory turnover has been slowing for several consecutive quarters, it indicates that inventory is rising faster than sales. This may suggest that customer demand is softening and the firm needs to take action, such as reducing production or increasing promotional efforts.

At Bed Bath & Beyond, inventory is the most valuable asset. Managing inventory can be a costly and highly complicated undertaking, especially for retailers.

CAPITAL INVESTMENT ANALYSIS

In addition to current assets, firms also invest in long-lived assets. Unlike current assets, long-lived assets are expected to produce economic benefits for more than one year. These investments often involve substantial amounts of money. For example, as noted earlier in the chapter, Airbus invested more than $15 billion in development of the A380. In another example, a few years ago, auto manufacturer BMW spent $750 million to expand its production facility in Spartanburg, South Carolina, bringing its total investment in the state to $4.6 billion.

The process by which decisions are made regarding investments in long-lived assets is called capital investment analysis. Firms make two basic types of capital investment decisions: expansion and replacement. The A380 and the BMW South Carolina plant investments are examples of expansion decisions. Replacement decisions involve upgrading assets by substituting new ones. A retailer might decide to replace an old store with a new Supercenter, as Walmart did in Oxford, Ohio.

Financial managers must estimate all of the costs and benefits of a proposed investment, which can be quite difficult, especially for very long-lived investments. Only those investments that offer an acceptable return—measured by the difference between benefits and costs—should be undertaken. BMW's financial managers believed that the benefits of expanding the South Carolina production facility outweighed the high cost. The expansion will allow BMW to produce three new models designed mainly for the North American market, so the expected profit from the sale of these models would be considered in the decision. Some other benefits cited by BMW include lower production costs, improved logistics, and expanded use of renewable energy. The expansion is paying off, with the Spartanburg facility producing a record 301,000 vehicles in a recent year.3

Quick Review

![]() Why do firms often choose to invest excess cash in marketable securities?

Why do firms often choose to invest excess cash in marketable securities?

![]() Name the two aspects of accounts receivable management.

Name the two aspects of accounts receivable management.

![]() Explain the difference between an expansion decision and a replacement decision.

Explain the difference between an expansion decision and a replacement decision.

Sources of Funds and Capital Structure

Sources of Funds and Capital Structure

The use of debt for financing can increase the potential for return as well as increase loss potential. Recall the accounting equation introduced in Chapter 15:

![]()

capital structure mix of a firm's debt and equity capital.

If you view this equation from a financial management perspective, it reveals that there are only two types of funding: debt and equity. Debt capital consists of funds obtained through borrowing. Equity capital consists of funds provided by the firm's owners when they reinvest earnings, make additional contributions, liquidate assets, issue stock to the general public, or raise capital from outside investors. The mix of a firm's debt and equity capital is known as its capital structure.

Companies often take very different approaches to choosing a capital structure. As more debt is used, the risk to the company increases since the firm is now obligated to make the interest payments on the money borrowed, regardless of the cash flows coming into the company. Choosing more debt increases the fixed costs a company must pay, which in turn makes a company more sensitive to changing sales revenues. Debt is frequently the least costly method of raising additional financing dollars, one of the reasons it is so frequently used.

Differing industries choose varying amounts of debt and equity to use when financing. Using the information provided by Datamonitor, we find that the automotive industry has debt ratios (the ratio of liabilities to assets) of over 60 percent for both Toyota and Honda and over 90 percent for Ford. These companies are primarily using debt to finance their asset expenditures. Food-service companies such as McDonald's and Starbucks use only 49 percent debt and 27 percent debt, respectively. The mixture of debt and equity a company uses is a major management decision.

LEVERAGE AND CAPITAL STRUCTURE DECISIONS

leverage increasing the rate of return on funds invested by borrowing funds.

Raising needed cash by borrowing allows a firm to benefit from the principle of leverage, increasing the rate of return on funds invested by borrowing funds. The key to managing leverage is to ensure that a company's earnings remain larger than its interest payments, which increases the leverage on the rate of return on shareholders' investment. Of course, if the company earns less than its interest payments, shareholders lose money on their original investment.

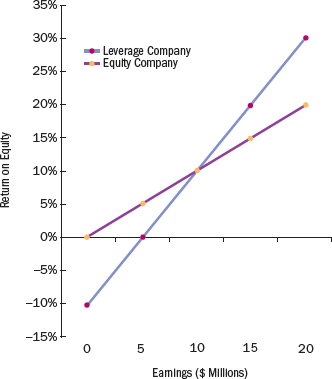

FIGURE 17.2 shows the relationship between earnings and shareholder returns for two identical hypothetical firms that choose to raise funds in different ways. Leverage Company obtains 50 percent of its funds from lenders who purchase company bonds. Leverage Company pays 10 percent interest on its bonds. Equity Company raises all of its funds through sales of company stock.

Notice that if earnings double—from, say, $10 million to $20 million—returns to shareholders of Equity Company also double, from 10 percent to 20 percent. But returns to shareholders of Leverage Company more than double, from 10 percent to 30 percent. However, leverage works in the opposite direction as well. If earnings fall from $10 million to $5 million—a decline of 50 percent—returns to shareholders of Equity Company also fall by 50 percent, from 10 percent to 5 percent. By contrast, returns to shareholders of Leverage Company fall from 10 percent to zero. Thus, leverage increases potential returns to shareholders but also increases risk.

FIGURE 17.2 How Leverage Works

NOTE: The example assumes that both companies have $100 million in capital. Leverage Company consists of $50 million in equity and $50 million in bonds (with an interest rate of 10 percent). Equity Company consists of $100 million in equity and no bonds. This example also assumes no corporate taxes.

A key component of the financial manager's job is to weigh the advantages and disadvantages of debt capital and equity capital, creating the most appropriate capital structure for the firm.

MIXING SHORT-TERM AND LONG-TERM FUNDS

Another decision financial managers face is determining the appropriate mix of short- and long-term funds. Short-term funds consist of current liabilities, and long-term funds consist of long-term debt and equity. Short-term funds are generally less expensive than long-term funds, but they also expose the firm to more risk. This is because short-term funds have to be renewed, or rolled over, frequently. Short-term interest rates can be volatile. During a recent 12-month period, for example, rates on commercial paper, a popular short-term financing option, ranged from a high of 0.22 percent (for 90-day loans) to a low of 0.04 percent (for 1-day loans).4

Because short-term rates move up and down frequently, interest expense on short-term funds can change substantially from year to year. For instance, if a firm borrows $50 million for ten years at 5 percent interest, its annual interest expense is fixed at $2.5 million for the entire ten years. On the other hand, if it borrows $50 million for one year at a rate of 4 percent, its annual interest expense of $2 million is only fixed for that year. If interest rates increase the following year to 6 percent, $1 million will be added to the interest expense bill. Another potential risk of relying on short-term funds is availability. Even financially healthy firms can occasionally find it difficult to borrow money.

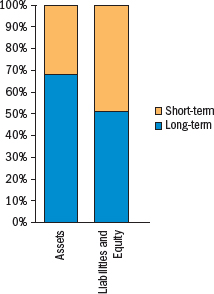

FIGURE 17.3 Johnson & Johnson's Mix of Short- and Long-Term Funds

SOURCE: Johnson & Johnson balance sheet, Yahoo! Finance, http://finance.yahoo.com, accessed June 20, 2013.

Because of the added risk of short-term funding, most firms choose to finance all of their long-term assets, and even a portion of their short-term assets, with long-term funds. Johnson & Johnson is typical of this choice. FIGURE 17.3 shows a recent balance sheet broken down between short- and long-term assets and short- and long-term funds.

DIVIDEND POLICY

Along with decisions regarding capital structure and the mix of short- and long-term funds, financial managers also make decisions regarding a firm's dividend policy. Dividends are periodic cash payments to shareholders. The most common type of dividend is paid quarterly and is often labeled as a regular dividend. Occasionally, firms make one-time special or extra dividend payments, as Microsoft did some years ago. Earnings that are paid in dividends are not reinvested in the firm and don't contribute additional equity capital.

Companies are under no legal obligation to pay dividends to shareholders of their common stock. However, some companies pay dividends every year, while others pay dividends sporadically. In 2012, Apple announced it would pay its first dividend in nearly 20 years.

Firms are under no legal obligation to pay dividends to shareholders of common stock. Although some companies pay generous dividends, others pay nothing. Until 2010, Starbucks never paid a dividend to its shareholders, and Apple recently announced it would pay its first dividend in nearly 20 years. In contrast, 3M has paid dividends for 30-plus consecutive years, during which time the amount has more than quadrupled.

Quick Review

![]() Explain the concept of leverage.

Explain the concept of leverage.

![]() Why do firms generally rely more on long-term funds than on short-term funds?

Why do firms generally rely more on long-term funds than on short-term funds?

![]() What is an important determinant of a firm's dividend policy?

What is an important determinant of a firm's dividend policy?

Short-Term Funding Options

Short-Term Funding Options

Many times throughout a year, an organization may discover that its cash needs exceed its available funds. Retailers generate surplus cash for most of the year, but they need to build up inventory during the late summer and fall to get ready for the holiday shopping season. Consequently, they often need funds to pay for merchandise until holiday sales generate revenue. Then they use the incoming funds to repay the amount they borrowed. In these instances, financial managers evaluate short-term sources of funds. By definition, short-term sources of funds are repaid within one year. Three major sources of short-term funds exist: trade credit, short-term loans, and commercial paper. Large firms often rely on a combination of all three sources of short-term financing.

TRADE CREDIT

Trade credit is extended by suppliers when a firm receives goods or services, agreeing to pay for them at a later date. Trade credit is common in many industries such as retailing and manufacturing. Suppliers routinely ship billions of dollars of merchandise to retailers each day and are paid at a later date. Without trade credit, the retailing sector would probably look much different—with fewer selections. Under this system, the supplier records the transactions as an account receivable, and the retailer records it as an account payable. Retailer Target alone currently has more than $6.5 billion of accounts payable on its books. The main advantage of trade credit is its easy availability because credit sales are common in many industries. The main drawback to trade credit is that the amount a company can borrow is limited to the amount it purchases.

Retailers like Target depend on trade credit to offer shoppers a broad array of merchandise.

SHORT-TERM LOANS

Loans from commercial banks are a significant source of short-term financing for businesses. Often businesses use these loans to finance inventory and accounts receivable. For example, late fall and early winter is the period of highest sales for a small manufacturer of ski equipment. To meet this demand, it has to begin building inventory during the summer. The manufacturer also has to finance accounts receivable (credit sales to customers) during the fall and winter. So it takes out a bank loan during the summer. As the inventory is sold and accounts receivable collected, the firm repays the loan.

There are two types of short-term bank loans: lines of credit and revolving credit agreements. A line of credit specifies the maximum amount the firm can borrow over a period of time, usually a year. The bank is under no obligation actually to lend the money, however. It does so only if funds are available. Most lines of credit require the borrower to repay the original amount, plus interest, within one year. By contrast, a revolving credit agreement is essentially a guaranteed line of credit—the bank guarantees that the funds will be available when needed. Banks typically charge a fee, on top of interest, for revolving credit agreements.

Another form of short-term financing backed by accounts receivable is called factoring. The business sells its accounts receivable to either a bank or finance company—called a factor—at a discount. The size of the discount determines the cost of the transaction. Factoring allows the firm to convert its receivables into cash quickly without worrying about collections.

COMMERCIAL PAPER

Commercial paper is a short-term IOU sold by a company (this concept was briefly described in Chapter 16). Commercial paper is typically sold in multiples of $100,000 to $1 million and has a maturity that ranges from 1 to 270 days. Most commercial paper is unsecured. It is an attractive source of financing because large amounts of money can be raised at rates that are typically 1 to 2 percent less that those charged by banks. Recently, almost $1.04 trillion in commercial paper was outstanding.5 Although commercial paper is an attractive short-term financing alternative, only a small percentage of businesses can issue it. That is because access to the commercial paper market has traditionally been restricted to large, financially strong corporations.

Quick Review

![]() What are the three sources of short-term funding?

What are the three sources of short-term funding?

![]() Explain trade credit.

Explain trade credit.

![]() Why is commercial paper an attractive short-term financing option?

Why is commercial paper an attractive short-term financing option?

Sources of Long-Term Financing

Sources of Long-Term Financing

Funds from short-term sources can help a firm meet current needs for cash or inventory. However, a larger project or plan, such as acquiring another company or making a major investment in real estate or equipment, usually requires funds for a much longer period of time. Unlike short-term sources, long-term sources are repaid over many years.

Organizations acquire long-term funds from three sources. One is long-term loans obtained from financial institutions such as commercial banks, life insurance companies, and pension funds. A second source is bonds—certificates of indebtedness—sold to investors. A third source is equity financing that is acquired by selling stock in the firm or reinvesting company profits.

PUBLIC SALE OF STOCKS AND BONDS

Public sales of securities such as stocks and bonds are a major source of funds for corporations. Such sales provide cash inflows for the issuing firm and either a share in its ownership (for a stock purchaser) or a specified rate of interest and repayment at a stated time (for a bond purchaser). Because stock and bond issues of many corporations are traded in the secondary markets, stockholders and bondholders can easily sell these securities. When a recent European debt crisis seemed likely, it caused a massive slowdown in bond sales. But as fears of a crisis eased later in the year, bond sales reached their highest level since the same time the previous year. Through the middle of a recent year, U.S. corporations have sold bonds worth almost $690 billion.6 Public sales of securities, however, can vary substantially from year to year, depending on conditions in the financial markets. Bond sales, for instance, tend to be higher when interest rates are lower.

Chapter 16 discussed the process by which most companies sell securities publicly—through investment bankers via a process called underwriting. Investment bankers purchase the securities from the issuer and then resell them to investors. The issuer pays a fee to the investment banker, called an underwriting discount.

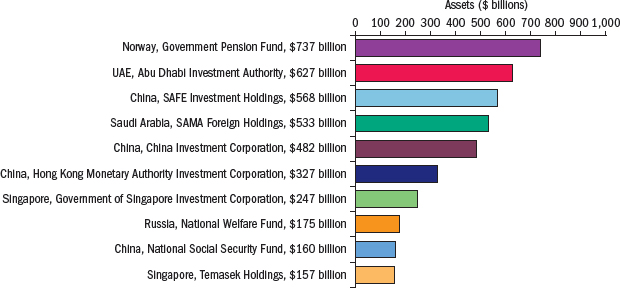

FIGURE 17.4 The World's Ten Largest Sovereign Wealth Funds

SOURCE: Sovereign Wealth Fund Institute, “Sovereign Wealth Fund Rankings,” http://www.swfinstitute.org, accessed June 17, 2013

PRIVATE PLACEMENTS

Some new stock or bond issues are not sold publicly but instead to a small group of major investors such as pension funds and insurance companies. Such a sale is referred to as a private placement. Companies will often raise funds with private placements as they are generally less expensive and quicker to complete than a public offering. Institutional investors such as insurance companies and pension funds buy private placements because they typically carry slightly higher interest rates than publicly issued bonds. In addition, the terms of the issue can be tailored to meet the specific needs of both the issuer and the institutional investors. Of course, the institutional investor gives up liquidity because privately placed securities do not trade in secondary markets.

PRIVATE EQUITY FUNDS

A private equity fund is an investment company that raises funds from wealthy individuals and institutional investors and uses those funds to make large investments in both public and privately held companies. Private equity funds invest in all types of businesses, including mature ones. For example, Cerberus Capital Management, a private equity fund, recently bought Supervalu's grocery chains, Albertsons, Acme, Jewel-Osco, Shaw's, and Star Market, for $3.3 billion.7 Often, private equity funds invest in a leveraged buyout—a transaction that takes a public company private. In such transactions, discussed in more detail in the next section, a public company reverts to private status.

A variation of the private equity fund is the so-called sovereign wealth fund. This type of company is owned by a government and invests in a variety of financial and real assets, such as real estate. Although sovereign wealth funds generally make investments based on the best risk-return trade-off, political, social, and strategic considerations also play a role in their investment decisions. The assets of the ten largest sovereign wealth funds are shown in FIGURE 17.4. Together, these ten funds have almost $4 trillion in assets.

HEDGE FUNDS

A hedge fund is a private investment company open only to qualified large investors. Operating much like a mutual fund, hedge funds raise capital from investors and then hire a manager to oversee investments matching the fund's stated goals. In recent years, hedge funds have become a significant presence in U.S. financial markets. Before the recent recession, some analysts estimated that hedge funds accounted for about 60 percent of all secondary bond market trading and around one-third of all activity on stock exchanges.

Quick Review

![]() Name the three sources of long-term funds for corporations.

Name the three sources of long-term funds for corporations.

![]() Why might a firm engage in a private placement of its stock or bonds?

Why might a firm engage in a private placement of its stock or bonds?

![]() What is a hedge fund?

What is a hedge fund?

Mergers, Acquisitions, Buyouts, and Divestitures

Mergers, Acquisitions, Buyouts, and Divestitures

Chapter 5 briefly described mergers and acquisitions. A merger is a transaction in which two or more firms combine into one company. In an acquisition, one firm buys the assets and assumes the obligations of another firm, such as Facebook's recent $1 billion acquisition of Instagram, a photo-sharing app for smart phones. Transactions like mergers, acquisitions, buyouts, and divestitures have financial implications.

Financial managers evaluate a proposed merger or acquisition in much the same way they would evaluate any large investment—by comparing the costs and benefits. Mergers are generally a transaction between two firms of roughly the same size. The merger between American Airlines Inc. and U.S. Airways Inc. is a good example of this type of merger. Unlike acquisitions, where the acquiring firm most often determines how the transaction will proceed, in mergers both firms have a significant stake in how the deal is structured. Who will be on the management team? Which corporate office will be the merged company headquarters? How much of the staff will be retained, doing what jobs, and in which locations? These and thousands of other questions must be discussed and resolved. To complete the American Airlines and U.S. Airways merger, the companies established 29 different committees, dealing with everything from in-flight service (will each customer receive a whole can of soda?) to who will be the new CEO (Doug Parker is currently the CEO and chairman of U.S. Airways).8 Whatever the reason for the merger, the term often used to describe the benefits produced by a merger or acquisition is synergy—the notion that the combined firm is worth more than the companies are individually. The American Airlines and U.S. Airways merger will result in a combined company that is better able to compete with other U.S. carriers.

leveraged buyout (LBO) transaction in which public shareholders are bought out and the firm reverts to private status.

In a leveraged buyout, or LBO, the shareholders of a public company are bought out and the firm reverts to private status. The term leverage comes from the fact that many of these transactions are financed with high degrees of debt—often in excess of 75 percent. Private equity companies and hedge funds provide equity and debt financing for many LBOs. The firm's incumbent senior management is often part of the buyout group. LBO activity decreased sharply with the recent economic downturn, but as the economy began to recover, LBO activity increased again.

divestiture sale of assets by a firm.

In a sense, a divestiture is the reverse of a merger—that is, a company sells an asset, such as a subsidiary, a product line, or a production facility. Two types of divestitures exist: sell-offs and spin-offs. In a sell-off, a firm sells an asset to another firm. After Verizon Wireless sold some of its assets to AT&T, AT&T announced plans to roll out 3G wireless service to about 1.6 million former Verizon subscribers in rural areas across 18 states.

The other type of divestiture is a spin-off. In this transaction, a new firm is formed by the sale of the assets. Shareholders of the divesting firm become shareholders of the new firm as well. For example, Motorola announced that it would split into two publicly traded firms. The parent company will handle its core business of mobile converged devices, digital home-entertainment devices, and video voice and data solutions. The spin-off firm will handle heavy-duty two-way radios, mobile computers, public security systems, wireless network infrastructure, and other business-oriented goods and services. Both entities will continue to use the Motorola brand name, with the parent company now named Motorola Solutions Inc. As part of the spin-off, Motorola shareholders received shares of the new company, Motorola Mobility Holdings, Inc.

Quick Review

![]() Define synergy.

Define synergy.

![]() What is a leveraged buyout?

What is a leveraged buyout?

![]() Name and describe the two types of divestitures.

Name and describe the two types of divestitures.

NOTES

1. Danilo Masoni, “Telecom Italia Plots Hybrid Debt Issue, Cuts Dividend,” Reuters, February 8, 2013, http://news.yahoo.com.

2. Company Web site, “Orders and Deliveries,” http://www.airbus.com, accessed June 26, 2013.

3. Joel Hans, “BMW's SC Plant Hits Record Production,” Manufacturing.net, January 10, 2013, http://www.manufacturing.net.

4. Federal Reserve Board, “Commercial Paper,” Federal Reserve Release, http://federalreserve.gov, accessed June 17, 2013.

5. Federal Reserve Board, “Commercial Paper Outstanding,” Federal Reserve Release, http://federalreserve.gov, accessed June 17, 2013.

6. Sarika Gangar, “Gross to Buffett, Omens Disregarded as Sales Soar: Credit Markets,” Bloomberg, May 20, 2013, http://www.bloomberg.com.

7. Elliot Zwiebach and Mark Hamstra, “Supervalu Completes Sale of Chains to Cerberus,” Supermarket News, March 21, 2013, http://supermarketnews.com.

8. Treey Maxon, “As American Airlines Merger Date Nears, Questions Abound,” Dallas News, June 3, 2013, http://www.dallasnews.com.

CHAPTER SEVENTEEN: REVIEW

Summary of Learning Objectives

![]() Define the role of the financial manager.

Define the role of the financial manager.

Finance deals with planning, obtaining, and managing a company's funds to accomplish its objectives efficiently and effectively. The major responsibilities of financial managers are to develop and implement financial plans and determine the most appropriate sources and uses of funds. The chief financial officer (CFO) heads a firm's finance organization. Three senior executives reporting to the CFO are the vice president for financial management, the treasurer, and the controller. When making decisions, financial professionals continually seek to balance risks with expected financial returns.

finance planning, obtaining, and managing a company's funds to accomplish its objectives as effectively and efficiently as possible.

financial managers executives who develop and implement the firm's financial plan and determine the most appropriate sources and uses of funds.

risk-return trade-off process of maximizing the wealth of a firm's shareholders by striking the optimal balance between risk and return.

![]() Describe financial planning.

Describe financial planning.

A financial plan is a document that specifies the funds needed by a firm for a given period of time, the timing of inflows and outflows, and the most appropriate sources and uses of funds. The financial plan addresses three questions:

- What funds will be required during the planning period?

- When will funds be needed?

- Where will funds be obtained?

Three steps are involved in the financial planning process:

- Forecasting sales over a future period of time

- Estimating the expected level of profits over the planning period

- Determining the additional assets needed to support additional sales.

financial plan document that specifies the funds needed by a firm for a period of time, the timing of inflows and outflows, and the most appropriate sources and uses of funds.

![]() Outline how organizations manage their assets.

Outline how organizations manage their assets.

Assets consist of what a firm owns and also comprise the uses of its funds. Sound financial management requires assets to be acquired and managed as effectively and efficiently as possible. The major current assets are cash, marketable securities, accounts receivable, and inventory. The goal of cash management is to have sufficient funds on hand to meet day-to-day transactions and pay any unexpected expenses. Excess cash should be invested in marketable securities, which are low-risk securities with short maturities. Managing accounts receivable, which are uncollected credit sales, involves securing funds owed the firm as quickly as possible while offering sufficient credit to customers to generate increased sales. The main goal of inventory management is to minimize the overall cost of inventory. Production, marketing, and logistics also play roles in determining proper inventory levels. Capital investment analysis is the process by which financial managers make decisions on long-lived assets. This involves comparing the benefits and costs of a proposed investment. Managing international assets poses additional challenges for the financial manager, including the problem of fluctuating exchange rates.

![]() Discuss the sources of funds and capital structure.

Discuss the sources of funds and capital structure.

Businesses have two sources of funds: debt capital and equity capital. Debt capital consists of funds obtained through borrowing, and equity capital consists of funds provided by the firm's owners. The mix of debt and equity capital is known as the firm's capital structure, and the financial manager's job is to find the proper mix. Leverage is a technique of increasing the rate of return on funds invested by borrowing. However, leverage increases risk. Also, overreliance on borrowed funds may reduce management's flexibility in future financing decisions. Equity capital also has drawbacks. When additional equity capital is sold, the control of existing shareholders is diluted. In addition, equity capital is more expensive than debt capital. Financial managers are also faced with decisions concerning the appropriate mix of short- and long-term funds. Short-term funds are generally less expensive than long-term funds but expose firms to more risk. Another decision involving financial managers is determining the firm's dividend policy.

capital structure mix of a firm's debt and equity capital.

leverage increasing the rate of return on funds invested by borrowing funds.

![]() Identify short-term funding options.

Identify short-term funding options.

The three major short-term funding options are trade credit, short-term loans from banks and other financial institutions, and commercial paper.

- Trade credit is extended by suppliers when a firm receives goods or services, agreeing to pay for them at a later date. Trade credit is relatively easy to obtain and costs nothing unless a supplier offers a cash discount.

- Loans from commercial banks are a significant source of short-term financing and are often used to finance accounts receivable and inventory. Loans can be either unsecured or secured, with accounts receivable or inventory pledged as collateral.

- Commercial paper is a short-term IOU sold by a company. Although large amounts of money can be raised through the sale of commercial paper, usually at rates below those charged by banks, access to the commercial-paper market is limited to large, financially strong corporations.

![]() Discuss sources of long-term financing.

Discuss sources of long-term financing.

Long-term funds are repaid over many years. There are three sources of long-term funds:

- Long-term loans obtained from financial institutions

- Bonds sold to investors

- Equity financing

Public sales of securities represent a major source of funds for corporations. These securities can generally be traded in secondary markets. Public sales can vary substantially from year to year depending on the conditions in the financial markets. Private placements are securities sold to a small number of institutional investors. Most private placements involve debt securities. Private equity funds are investment companies that raise funds from wealthy individuals and institutional investors and use the funds to make investments in both public and private companies. Sovereign wealth funds are investment companies owned by governments.

![]() Describe mergers, acquisitions, buyouts, and divestitures.

Describe mergers, acquisitions, buyouts, and divestitures.

A merger is a combination of two or more firms into one company. An acquisition is a transaction in which one company buys another. Even in a merger, there is a buyer and a seller (called the target). The buyer offers cash, securities, or a combination of the two in return for the target's shares. Mergers and acquisitions should be evaluated as any large investment is, by comparing the costs with the benefits. Synergy is the term used to describe the benefits a merger or acquisition is expected to produce.

A leveraged buyout (LBO) is a transaction in which shares are purchased from public shareholders and the company reverts to private status. Usually LBOs are financed with substantial amounts of borrowed funds. Private equity companies are often major financers of LBOs.

Divestitures are the opposite of mergers, in which companies sell assets such as subsidiaries, product lines, or production facilities. A sell-off is a divestiture in which assets are sold to another firm. In a spin-off, a new firm is created from the assets divested. Shareholders of the divesting firm become shareholders of the new firm as well.

leveraged buyout (LBO) transaction in which public shareholders are bought out and the firm reverts to private status.

divestiture sale of assets by a firm.

Quick Review

LO1

![]() How is the finance function structured at the typical firm?

How is the finance function structured at the typical firm?

![]() Explain the risk-return trade-off.

Explain the risk-return trade-off.

LO2

![]() What three questions does a financial plan address?

What three questions does a financial plan address?

![]() List the steps involved in creating a financial plan.

List the steps involved in creating a financial plan.

LO3

![]() Why do firms often choose to invest excess cash in marketable securities?

Why do firms often choose to invest excess cash in marketable securities?

![]() Name the two aspects of accounts receivable management.

Name the two aspects of accounts receivable management.

![]() Explain the difference between an expansion decision and a replacement decision.

Explain the difference between an expansion decision and a replacement decision.

LO4

![]() Explain the concept of leverage.

Explain the concept of leverage.

![]() Why do firms generally rely more on long-term funds than on short-term funds?

Why do firms generally rely more on long-term funds than on short-term funds?

![]() What is an important determinant of a firm's dividend policy?

What is an important determinant of a firm's dividend policy?

LO5

![]() What are the three sources of short-term funding?

What are the three sources of short-term funding?

![]() Explain trade credit.

Explain trade credit.

![]() Why is commercial paper an attractive short-term financing option?

Why is commercial paper an attractive short-term financing option?

LO6

![]() Name the three sources of long-term funds for corporations.

Name the three sources of long-term funds for corporations.

![]() Why might a firm engage in a private placement of its stock or bonds?

Why might a firm engage in a private placement of its stock or bonds?

![]() What is a hedge fund?

What is a hedge fund?

LO7

![]() Define synergy.

Define synergy.

![]() What is a leveraged buyout?

What is a leveraged buyout?

![]() Name and describe the two types of divestitures.

Name and describe the two types of divestitures.