The Financial System

Learning Objectives

![]() Understand the financial system.

Understand the financial system.

![]() List the various types of securities.

List the various types of securities.

![]() Discuss financial markets.

Discuss financial markets.

![]() Understand the stock markets.

Understand the stock markets.

![]() Evaluate financial institutions.

Evaluate financial institutions.

![]() Explain the role of the Federal Reserve System.

Explain the role of the Federal Reserve System.

![]() Describe the regulation of the financial system.

Describe the regulation of the financial system.

![]() Discuss the global perspective of the financial system.

Discuss the global perspective of the financial system.

Community Banks Team Up to Fight the Megabanks

Here's what one customer recently had to say about her relationship with a major U.S. bank: “I'm sick of their fees. I'm sick of not knowing where my money goes.”

Does that sound familiar? Millions of bank customers who feel the same are finding smaller community banks and credit unions more appealing alternatives than megabanks, with their multiplying fees and impersonal service. But smaller institutions have been woefully lacking in competitive clout and product offerings compared to major banks like Bank of America and Citibank—until now.

Almost 130 banks and credit unions in 35 states have joined forces under a new national brand called Kasasa, pooling their resources to offer banking products that compete with the big names. BancVue is the parent company of Kasasa; it provides staff training to member institutions and does their marketing and promotion. Member banks pay Kasasa a fee based on their size and contribute some marketing funds. The small-bank alliance expects to double its membership soon, hoping to reach 1,000 members within a few years.

And how does the Kasasa bank alliance pay off for bank customers? How about a checking account that earns 4 percent interest with no fees and no minimum. Sound good? You are not alone. Consumers are moving their accounts, and Kasasa member banks have seen increases in checking and savings deposits between 15 and 25 percent.1

Overview

Businesses, governments, and individuals often need to raise capital. Assume the owner of a small business either forecasts a sharp increase or drop in sales; one might require more inventory and the other reduced production in order to survive. The owner might turn to a major bank or a nontraditional lender like a Kasasa member bank for a loan that would provide the needed cash for either situation. On the other hand, some individuals and businesses have incomes that are greater than their current expenditures and wish to earn a rate of return on the excess funds.

financial system process by which money flows from savers to users.

The two transactions just described are small parts of what is known as the financial system, the process by which money flows from savers to users. Virtually all businesses, governments, and individuals participate in the financial system, and a well-functioning one is vital to a nation's economic well-being. The financial system is the topic of this chapter.

The chapter begins by describing the financial system and its components in more detail. Then, the major types of financial instruments, such as stocks and bonds, are outlined. Next the chapter discusses financial markets, where financial instruments are bought and sold, and describes the world's major stock markets, such as the New York Stock Exchange.

Next, banks and other financial institutions are described in depth. The structure and responsibilities of the U.S. Federal Reserve System, along with the tools the Fed uses to control the supply of money and credit, are detailed. The chapter concludes with an overview of the major laws and regulations affecting the financial system and a discussion of today's global financial system.

Understanding the Financial System

Understanding the Financial System

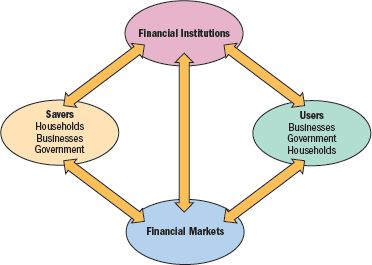

Households, businesses, government, financial institutions, and financial markets together form what is known as the financial system. A simple diagram of the financial system is shown in FIGURE 16.1.

On the left are savers—those with excess funds. For a variety of reasons, savers choose not to spend all of their current income, so they have a surplus of funds. Users are the opposite of savers; their spending needs exceed their current income, so they have a deficit. They need to obtain additional funds to make up the difference. Savings are provided by some households, businesses, and the government, but other households, businesses, and the government are also borrowers. Households may need money to buy automobiles or homes. Businesses may need money to purchase inventory or build new production facilities. Governments may need money to build highways and courthouses.

Generally, in the United States, households are net savers—meaning that as a whole they save more funds than they use—whereas businesses and governments are net users—meaning that they use more funds than they save. The fact that most of the net savings in the U.S. financial system are provided by households may be a bit of a surprise initially because Americans do not have a reputation for being thrifty. Yet even though the savings rate of American households is low compared with those of other countries, American households still save hundreds of billions of dollars each year.

Funds can be transferred between savers and users in two ways: directly and indirectly. A direct transfer means that the user raises the needed funds directly from savers. While direct transfers occur, the vast majority of funds flow through either financial markets or financial institutions. For example, assume a local school district needs to build a new high school. The district doesn't have enough cash on hand to pay for the school construction costs, so it sells bonds to investors (savers) in the financial market. The district uses the proceeds from the sale to pay for the new school and in return pays bond investors interest each year for the use of their money.

The other way in which funds can be transferred indirectly is through financial institutions—for example, commercial banks like Fifth Third Bank or Regions Bank. The bank pools customer deposits and uses the funds to make loans to businesses and households. These borrowers pay the bank interest, and it in turn pays depositors interest for the use of their money.

Quick Review

![]() What is the financial system?

What is the financial system?

![]() In the financial system, who are the borrowers and who are the savers?

In the financial system, who are the borrowers and who are the savers?

![]() Name the two most common ways funds are transferred between borrowers and savers.

Name the two most common ways funds are transferred between borrowers and savers.

Types of Securities

Types of Securities

securities financial instruments that represent obligations on the part of the issuers to provide the purchasers with expected stated returns on the funds invested or loaned.

For the funds they borrow from savers, businesses and governments provide different types of guarantees for repayment. Securities, also called financial instruments, represent obligations on the part of the issuers—businesses and governments—to provide the purchasers with expected or stated returns on the funds invested or loaned. Securities can be grouped into three categories: money market instruments, bonds, and stock. Money market instruments and bonds are both debt securities. Stocks are units of ownership in corporations like General Electric, McDonald's, Apple, and PepsiCo.

MONEY MARKET INSTRUMENTS

Money market instruments are short-term debt securities issued by governments, financial institutions, and corporations. Money market instruments are generally low-risk securities and are purchased by investors when they have surplus cash. Examples of money market instruments include U.S. Treasury bills, commercial paper, and bank certificates of deposit.

Treasury bills are short-term securities issued by the U.S. Treasury and backed by the full faith and credit of the U.S. government. Treasury bills are sold with a maturity of 30, 90, 180, or 360 days and have a minimum denomination of $1,000. They are considered virtually risk-free and easy to resell. Commercial paper is securities sold by corporations, such as Raytheon, that mature in from 1 to 270 days from the date of issue. Although slightly riskier than Treasury bills, commercial paper is still generally considered a very low risk security.

A certificate of deposit (CD) is a time deposit at a financial institution, such as a commercial bank, savings bank, or credit union. The sizes and maturity dates of CDs vary considerably and can often be tailored to meet the needs of purchasers. CDs in denominations of $250,000 or less per depositor are federally insured.

BONDS

Bondholders are creditors of a corporation or government body. Bonds are issued in various denominations, or face values, usually between $1,000 and $25,000. Each issue indicates a rate of interest to be paid to the bondholder—stated as a percentage of the bond's face value—as well as a maturity date on which the bondholder is paid the bond's full face value. Because bondholders are creditors, they have a claim on the firm's assets that must be satisfied before any claims of stockholders in the event of the firm's bankruptcy, reorganization, or liquidation.

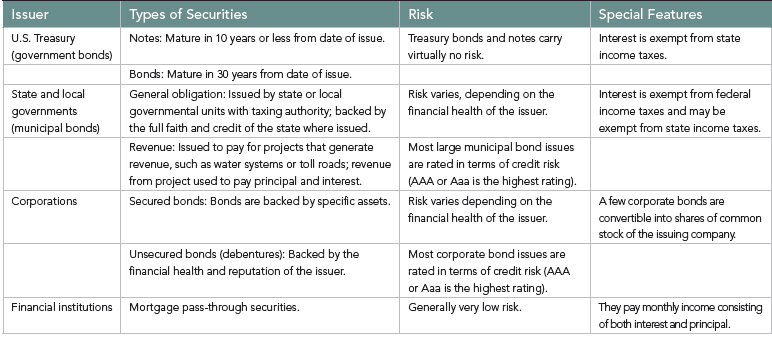

A prospective bond investor can choose among a variety of bonds. The major types of bonds are summarized in TABLE 16.1. Government bonds are bonds sold by the U.S. Department of the Treasury. Because government bonds are backed by the full faith and credit of the U.S. government, they are considered the least risky of all bonds. The Treasury sells bonds that mature in 2, 5, 10, and 30 years from the date of issue.

Municipal bonds are bonds issued by state or local governments. Two types of municipal bonds are available. A revenue bond is a bond issue whose proceeds will be used to pay for a project that will produce revenue, such as a toll road or bridge. The proceeds of a general obligation bond are to be used to pay for a project that will not produce any revenue.

Corporate bonds are a diverse group and often vary based on the collateral—the property pledged by the borrower—that backs the bond. For example, a secured bond is backed by a specific pledge of company assets. These assets are collateral, just like a home is collateral for a mortgage. However, many firms also issue unsecured bonds, called debentures. These bonds are backed only by the financial reputation of the issuing corporation.

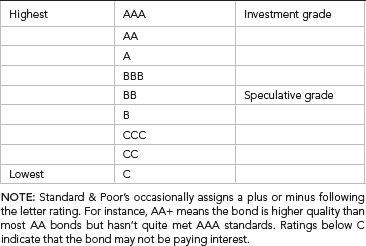

Two factors determine the price of a bond: its risk and its interest rate. Bonds vary considerably in terms of risk. One tool that bond investors use to assess the risk of a bond is its bond rating. Several investment firms rate corporate and municipal bonds, the best known of which are Standard & Poor's (S&P), Moody's, and Fitch. TABLE 16.2 lists the S&P bond ratings. Moody's and Fitch use similar rating systems. Bonds with the lowest level of risk are rated AAA. As ratings descend, risk increases. Bonds with ratings of BBB and above are classified as investment-grade bonds. By contrast, bonds with ratings of BB and below are classified as speculative or junk bonds. Junk bonds attract investors by offering high interest rates in exchange for greater risk.

Another important influence on bond prices is the market interest rate. Because bonds pay fixed rates of interest, as market interest rates rise, bond prices fall, and vice versa. For instance, the price of a ten-year bond, paying 5 percent per year, would fall by about 8 percent if market interest rates rose from 5 percent to 6 percent.

STOCK

common stock basic form of corporate ownership.

The basic form of corporate ownership is embodied in common stock. Purchasers of common stock are the true owners of a corporation. Holders of common stock vote on major company decisions, such as purchasing another company or electing a board of directors. In return for the money they invest, they expect to receive some sort of return. This return can come in the form of dividend payments, expected price appreciation, or both. Dividends vary widely from firm to firm. As a general rule, faster-growing companies pay less in dividends because they need more funds to finance their growth. Consequently, investors expect stocks paying little or no cash dividends to show greater price appreciation compared with stocks paying more generous cash dividends.

A certificate for General Motors' common stock.

Common stockholders benefit from company success, and they risk the loss of their investments if the company fails. If a firm dissolves, claims of creditors must be satisfied before stockholders receive anything. Because creditors have the first (or senior) claim to assets, holders of common stock are said to have a residual claim on company assets.

The market value of a stock is the price at which the stock is currently selling. For example, Facebook's stock price fluctuated between $17.55 and $45.00 per share during a recent year. What determines this market value is complicated; many variables cause stock prices to move up or down. However, in the long run, stock prices tend to follow a company's profits.

In addition to common stock, a few companies also issue preferred stock—stock whose holders receive preference in the payment of dividends. General Motors and Ford are examples of firms with preferred stock outstanding. Also, if a company is dissolved, holders of preferred stock have claims on the firm's assets that are ahead of the claims of common stockholders. On the other hand, preferred stockholders rarely have any voting rights, and the dividend they are paid is fixed, regardless of how profitable the firm becomes. Therefore, although preferred stock is legally classified as equity, many investors consider it to be more like a bond than common stock.

Quick Review

![]() Name the major types of securities.

Name the major types of securities.

![]() What is a government bond? A municipal bond?

What is a government bond? A municipal bond?

![]() Why do investors buy common stock?

Why do investors buy common stock?

Financial Markets

Financial Markets

financial markets market in which securities are issued and traded.

primary markets financial market in which firms and governments issue securities and sell them initially to the general public.

Securities are issued and traded in financial markets. Although there are many different types of financial markets, one of the most important distinctions is between primary and secondary markets. In the primary markets, firms and governments issue securities and sell them initially to the general public. When a company needs capital to purchase inventory, expand a plant, make major investments, acquire another firm, or pursue other business goals, it may sell a bond or stock issue to the investing public.

A stock offering gives investors the opportunity to purchase ownership shares in a firm and to participate in its future growth in exchange for providing current capital. When a company offers stock for sale to the general public for the first time, it is called an initial public offering (IPO). Analysts predict IPOs from a number of American companies, notably Twitter and Box.2

Both profit-seeking corporations and government agencies also rely on primary markets to raise funds by issuing bonds. For example, the federal government sells Treasury bonds through an open auction to finance part of federal outlays such as interest on outstanding federal debt. State and local governments sell bonds to finance capital projects such as the construction of sewer systems, streets, and fire stations. Sales of most corporate and municipal securities are made via financial institutions such as Morgan Stanley. These institutions purchase the issue from the firm or government and then resell the issue to investors. This process is known as underwriting.

secondary market collection of financial markets in which previously issued securities are traded among investors.

While the primary market is the way corporations and governments raise finds, most of the stock and bond trading that happens on a daily basis happens in the secondary market, a collection of financial markets in which previously issued securities are traded among investors. The corporations or governments that originally issued the securities being traded are not directly involved in the secondary market. They make no payments when securities are sold nor receive any of the proceeds when securities are purchased. The New York Stock Exchange (NYSE), for example, is a secondary market. In terms of the dollar value of securities bought and sold, the secondary market is four to five times as large as the primary market. Each day, more than 1.4 billion shares worth about $55 billion are traded on the NYSE.3 The characteristics of the world's major stock exchanges are discussed in the next section.

Quick Review

![]() Distinguish between a primary and a secondary financial market.

Distinguish between a primary and a secondary financial market.

![]() Briefly explain the role of financial institutions in the sale of securities.

Briefly explain the role of financial institutions in the sale of securities.

Understanding Stock Markets

Understanding Stock Markets

stock markets (exchanges) market in which shares of stock are bought and sold by investors.

Stock markets, or exchanges, are probably the best known of the world's financial markets. In these markets, shares of stock are bought and sold by investors. The two largest stock markets in the world, the New York Stock Exchange (NYSE) and the NASDAQ stock market. are located in the United States. The Dow Jones Industrial Average (often referred to as the Dow) is a price-weighted average of the 30 most significant stocks traded on the NYSE and the NASDAQ.

THE NEW YORK STOCK EXCHANGE

The New York Stock Exchange—sometimes referred to as the Big Board—is the most famous and one of the oldest stock markets in the world, having been founded in 1792. Today, the stocks of about 2,800 companies are listed on the NYSE. These stocks represent most of the largest, best-known companies in the United States and have a total market value exceeding $18 trillion. In terms of the total value of stock traded, the NYSE is the world's largest stock market.

THE NASDAQ STOCK MARKET

The world's second-largest stock market, NASDAQ, is very different from the NYSE. NASDAQ—which stands for National Association of Securities Dealers Automated Quotation—is actually a computerized communications network that links member investment firms. It is the world's largest intranet. All trading on NASDAQ takes place through its intranet rather than on a trading floor. More than 3,300 companies have their stocks listed on NASDAQ. While NASDAQ-listed corporations tend to be smaller firms and less well known than NYSE-listed ones, NASDAQ is also home to some of the largest U.S. companies and iconic brands—for example, Amgen, Cisco Systems, Dell, Intel, and Microsoft.

FOREIGN STOCK MARKETS

Stock markets exist throughout the world. Virtually all developed countries and many developing countries have stock exchanges. Examples include Mumbai, Helsinki, Hong Kong, Mexico City, Paris, and Toronto. One of the largest stock exchanges outside the United States is the London Stock Exchange. Founded in the early 19th century, the London Stock Exchange lists approximately 3,000 stock and bond issues by companies from more than 70 countries around the world. Trading on the London Stock Exchange takes place using a NASDAQ-type computerized communications network.

Often referred to as the Dow, the Dow Jones Industrial Average is a price-weighted average of the 30 most significant stocks traded on the NYSE and the NASDAQ.

The London Stock Exchange is the most international of all stock markets. Approximately two-thirds of all cross-border trading in the world—for example, the trading of stocks of American companies outside the United States—take place in London. It is not uncommon for institutional investors in the United States to trade NYSE- or NASDAQ-listed stocks in London.

Established in the 1800s, the London Stock Exchange is one of the largest stock markets outside of the United States. The Exchange uses a trading communications network similar to the one used at the NASDAQ.

INVESTOR PARTICIPATION IN THE STOCK MARKETS

Because most investors aren't members of the NYSE or any other stock market, they need to use the services of a brokerage firm to buy or sell stocks. Examples of brokerage firms include Edward Jones and TD Ameritrade. Investors establish an account with the brokerage firm and then enter orders to trade stocks. The most common type of order is called a market order. It instructs the broker to obtain the best possible price—the highest price when selling and the lowest price when buying. If the stock market is open, market orders are filled within seconds. Another popular type of order is called a limit order. It sets a price ceiling when buying or a price floor when selling. If the order cannot be executed when it is placed, the order is left with the exchange's market maker. It may be filed later if the price limits are met.

Quick Review

![]() Name the world's two largest stock markets.

Name the world's two largest stock markets.

![]() Why is the London Stock Exchange unique?

Why is the London Stock Exchange unique?

![]() Explain the difference between a market order and a limit order.

Explain the difference between a market order and a limit order.

Financial Institutions

Financial Institutions

financial institutions intermediary between savers and borrowers, collecting funds from savers and then lending the funds to individuals, businesses, and governments.

One of the most important components of the financial system is financial institutions. They are an intermediary between savers and borrowers, collecting funds from savers and then lending the funds to individuals, businesses, and governments. Financial institutions greatly increase the efficiency and effectiveness of the transfer of funds from savers to users. Because of financial institutions, savers earn more and users pay less than they would without them. In fact, it is difficult to imagine how any modern economy could function without well-developed financial institutions. Think about how difficult it would be for a businessperson to obtain inventory financing or an individual to purchase a new home without financial institutions. Prospective borrowers would have to identify and negotiate terms with each saver individually.

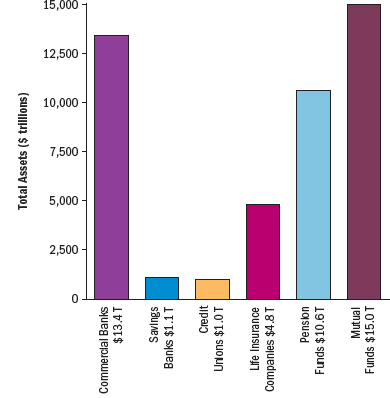

Traditionally, financial institutions have been classified into depository institutions—institutions that accept deposits that customers can withdraw on demand—and nondepository institutions. Examples of depository institutions include commercial banks, such as US Bancorp and Sun Trust; savings banks, such as Acacia Federal Savings Bank and Ohio Savings Bank; and credit unions, such as the State Employees' Credit Union of North Carolina. Nondepository institutions include life insurance companies, such as Northwestern Mutual; pension funds, such as the Florida state employee pension fund; and mutual funds. In total, financial institutions have trillions of dollars in assets. FIGURE 16.2 illustrates the size of the most prominent financial institutions.

FIGURE 16.2 Assets of Major Financial Institutions

SOURCES: American Council of Life Insurers Web site, “Life Insurer Fact Book 2012,” accessed June 16, 2013, http://www.acli.com; Federal Deposit Insurance Corporation, “Statistics at a Glance,” http://www.fdic.gov, updated May 29, 2013; Warren S. Hearsch, “U.S. Mutual Fund Assets Set to Pass $15 Trillion,” LifeHealthPro, February 13, 2013, http://www.lifehealthpro.com; Organization for Economic Co-Operation and Development Web site, “Pension Fund Assets Hit Record USD $20.1 T in 2011, but Investment Performance Weakens,” September 2012, Issue 9, page 21, http://www.oecd.org; National Credit Union Association Web site, “Credit Union Industry Assets Top $1 Trillion,” June 1, 2012, http://www.ncua.gov.

COMMERCIAL BANKS

Commercial banks are the largest and probably most important financial institution in the United States, and in most other countries as well. In the United States, the approximately 6,000 commercial banks hold total assets of more than $13.3 trillion.4 Commercial banks offer the most services of any financial institution. These services include a wide range of checking and savings deposit accounts, consumer loans, credit cards, home mortgage loans, business loans, and trust services. Commercial banks also sell other financial products, including securities and insurance.

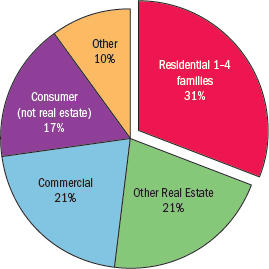

FIGURE 16.3 Distribution of Outstanding Commercial Bank Loans

SOURCE: Federal Deposit Insurance Corporation, “Quarterly Banking Profile: Table III-A, First Quarter 2013,” http://www2.fdic.gov, accessed June 13, 2013.

HOW BANKS OPERATE

Banks raise funds by offering a variety of checking and savings deposits to customers. The banks then pool these deposits and lend most of them out in the form of consumer and business loans. Recently, banks held over $8.6 trillion in domestic deposits and had about $7.0 trillion in outstanding loans.5 The distribution of outstanding loans is shown in FIGURE 16.3. As the figure shows, banks lend a great deal of money to both households and businesses for a variety of purposes. Commercial banks are an especially important source of funds for small businesses. When evaluating loan applications, banks consider the borrower's ability and willingness to repay the loan.

Banks make money primarily because the interest rate they charge borrowers is higher than the rate of interest they pay depositors. Banks also make money from other sources, such as fees they charge customers for checking accounts and using automated teller machines.

ELECTRONIC BANKING

More and more funds each year move through electronic funds transfer (EFT) systems, computerized systems for conducting financial transactions over electronic links. Millions of businesses and consumers now pay bills and receive payments electronically. Most employers, for example, directly deposit employee paychecks in their bank accounts rather than issue paper checks to employees. Today nearly all Social Security checks and other federal payments made each year arrive as electronic data rather than paper documents.

ONLINE BANKING

Today, many consumers do some or all of their banking on the Internet. Two types of online banks exist: Internet-only banks (direct banks), such as ING Direct, and traditional brick-and-mortar banks with Web sites, such as JPMorgan Chase and PNC. It appears that direct banks are gaining in popularity. with a recent study showing market share gains for these types of banks compared with all other approaches.6 Convenience is the primary reason people are attracted to online banking. Customers can transfer money, check account balances, and pay bills at any time. Plus with no branch offices to support, direct banks should be able to offer lower fees and better rates than their brick-and-mortar counterparts.

FEDERAL DEPOSIT INSURANCE

Federal Deposit Insurance Corporation (FDIC) federal agency that insures deposits at commercial and savings banks.

Most commercial bank deposits are insured by the Federal Deposit Insurance Corporation (FDIC), a federal agency. Deposit insurance means that, in the event the bank fails, insured depositors are paid in full by the FDIC, up to $250,000. Federal deposit insurance was enacted by the Banking Act of 1933 as one of the measures designed to restore public confidence in the banking system. Before deposit insurance, so-called runs were common as people rushed to withdraw their money from a bank, often just on a rumor that the bank was in precarious financial condition. With more and more withdrawals in a short period, the bank was eventually unable to meet customer demands and closed its doors. Remaining depositors often lost most of the money they had in the bank. Deposit insurance shifts the risk of bank failures from individual depositors to the FDIC. Although banks still fail today, no insured depositor has ever lost any money on deposit up to the FDIC limit.

SAVINGS BANKS AND CREDIT UNIONS

Commercial banks are by far the largest depository financial institution in the United States, but savings banks and credit unions also serve a significant segment of the financial community. Today, savings banks and credit unions offer many of the same services as commercial banks.

Previously, savings banks were called savings and loan associations or thrift institutions. They were originally established in the early 1800s to make home mortgage loans. Savings and loans raised funds by accepting only savings deposits and then lent these funds to consumers to buy homes. Today, around 971 savings banks operate in the United States, with total assets of about $1.062 trillion.7 Although savings banks offer many of the same services as commercial banks, including checking accounts, they are not major lenders to businesses.

Credit unions are cooperative financial institutions that are owned by their depositors, all of whom are members. Around 92 million Americans belong to one of the nation's approximately 7,100 credit unions. Combined, credit unions have more than $962 billion in assets. By law, credit union members must share similar occupations, employers, or membership in certain organizations. This law effectively caps the size of credit unions. In fact, the nation's largest bank—JPMorgan Chase—holds more deposits than all the country's credit unions combined.8

NONDEPOSITORY FINANCIAL INSTITUTIONS

Nondepository financial institutions accept funds from businesses and households and invest it. Generally, these institutions do not offer checking accounts (demand deposits). Three examples of nondepository financial institutions are insurance companies, pension funds, and finance companies.

- Insurance companies are organizations that accept the risk from households and businesses in return for a series of payments, called premiums. Underwriting is the process insurance companies use to determine whom to insure and what to charge. During a typical year, insurance companies collect more in premiums than they pay in claims. After they pay operating expenses, they invest this difference. Life insurance companies alone have total assets of more than $4.8 trillion invested in everything from bonds and stocks to real estate.9 Examples of life insurers include Prudential and New York Life.

- Pension funds provide retirement benefits to workers and their families. They are set up by employers and are funded by regular contributions made by employers and employees. Because pension funds have predictable long-term cash inflows and very predictable cash outflows, they invest heavily in assets, such as common stocks and real estate. U.S. private pension funds have more than $10.58 trillion in assets.10

- Finance companies offer short-term loans to borrowers. Commercial finance companies, such as Ford Credit, John Deere Capital Corporation, and Dollar Financial, supply short-term funds to businesses that pledge tangible assets such as inventory, accounts receivable, machinery, or property as collateral for the loan. A consumer finance company plays a similar role for consumers.

Life insurance companies such as New York Life are a major source of financing for businesses. Considered a nondepository financial institution, insurance companies accept funds from consumers and businesses and invest most of the money.

MUTUAL FUNDS

One of the most significant types of financial institutions today is the mutual fund. Mutual funds are financial intermediaries that raise money from investors by selling shares. They then use the money to invest in securities that are consistent with the mutual fund's objectives, often hiring a professional manager to oversee the investments. Mutual funds have become extremely popular over the last few decades and currently have about $15 trillion in assets. 11

Quick Review

![]() Name the two main types of financial institutions.

Name the two main types of financial institutions.

![]() What are the primary differences between commercial banks and savings banks?

What are the primary differences between commercial banks and savings banks?

![]() What is a mutual fund?

What is a mutual fund?

The Role of the Federal Reserve System

The Role of the Federal Reserve System

Federal Reserve System (Fed) the central bank of the United States.

Created in 1913, the Federal Reserve System, or the Fed, is the central bank of the United States and an important part of the nation's financial system. The Fed has four basic responsibilities: regulating commercial banks, performing banking-related activities for the U.S. Department of the Treasury, providing services for banks, and setting monetary policy.

MONETARY POLICY

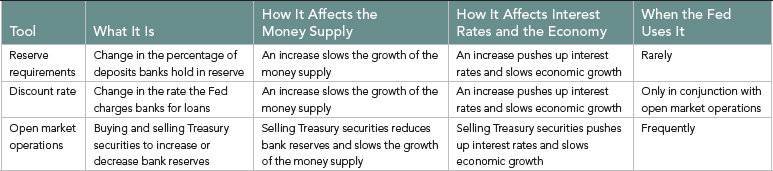

The Fed's most important function is monetary policy—that is, controlling the supply of money and credit. The Fed's job is to make sure the money supply grows at an appropriate rate, allowing the economy to expand and keeping inflation in check. If the money supply grows too slowly, economic growth will slow, unemployment will rise, and the risk of a recession will increase. If the money supply grows too rapidly, inflationary pressures will build. The Fed uses its policy to push interest rates up or down. By pushing the interest rates up, the growth rate of the money supply slows. By pushing the interest rates down, the growth rate of the money supply tends to rise.

The two common measures of the money supply are called M1 and M2. M1 consists of money in circulation and balances in bank checking accounts. M2 equals M1 plus balances in some savings accounts and money market mutual funds. The Fed has three major policy tools for controlling the growth in the supply of money and credit: reserve requirements, the discount rate, and open market operations.

The Fed requires banks to maintain reserves—defined as cash in their vaults plus deposits at district Federal Reserve banks or other banks—equal to a certain percentage of what the banks hold in deposits. For example, if the Fed sets the reserve requirement at 5 percent, a bank that receives a $500 deposit must reserve $25, so it has only $475 to invest or lend to individuals or businesses. By changing the reserve requirement, the Fed can affect the amount of money available for making loans. The higher the reserve requirement, the less banks can lend out to consumers and businesses. The lower the reserve requirement, the more banks can lend out. Because any change in the reserve requirement can have a sudden and dramatic impact on the money supply, the Fed rarely uses this tool.

Another policy tool is the so-called discount rate, the interest rate at which Federal Reserve banks make short-term loans to member banks. A bank may need a short-term loan if transactions leave it short of reserves. If the Fed wants to slow the growth rate in the money supply, it increases the discount rate. When this increase makes it more expensive for banks to borrow money, they in turn raise the interest rate they charge on loans to consumers and businesses. The end result is a slowdown in economic activity. Lowering the discount rate has the opposite effect.

The third policy tool, and the one most often used, is open market operations, the technique of controlling the money supply growth rate by buying or selling U.S. Treasury securities. If the Fed buys Treasury securities, the money it pays enters circulation, increasing the money supply and lowering interest rates. When the Fed sells Treasury securities, money is taken out of circulation and interest rates rise. When the Fed uses open market operations, it employs the so-called federal funds rate—the rate at which banks lend money to each other overnight—as its benchmark. TABLE 16.3 illustrates how the Federal Reserve uses tools to regulate the economy.

Quick Review

![]() What is the Federal Reserve System?

What is the Federal Reserve System?

![]() How is the Fed organized?

How is the Fed organized?

![]() List the three tools the Fed uses to control the supply of money and credit.

List the three tools the Fed uses to control the supply of money and credit.

Regulation of the Financial System

Regulation of the Financial System

Given the importance of the financial system, it is probably not surprising that many components are subject to government regulation and oversight. In addition, industry self-regulation is commonplace.

BANK REGULATION

Banks are among the nation's most heavily regulated businesses—primarily to ensure public confidence in the safety and security of the banking system. Banks are critical to the overall functioning of the economy, and a collapse of the banking system can have disastrous results. Many believe one of the major causes of the Great Depression was the collapse of the banking system that started in the late 1920s.

Banks and credit unions are subject to periodic examination by state or federal regulators. Examinations ensure that the institution is following sound banking practices and is complying with all applicable regulations. These examinations include the review of detailed reports on the bank's operating and financial condition as well as on-site inspections. Regulators can impose penalties on institutions deemed not in compliance with sound banking practices, including forcing the delinquent financial institution into a merger with a healthier one.

GOVERNMENT REGULATION OF THE FINANCIAL MARKETS

Regulation of U.S. financial markets is primarily a function of the federal government, although states also regulate them. Federal regulation grew out of various trading abuses during the 1920s. To restore confidence and stability in the financial markets after the 1929 stock market crash, Congress passed a series of landmark legislative acts that have formed the basis of federal securities regulation ever since. Many other regulations have followed, including the Dodd-Frank Wall Street Reform and Consumer Protection Act, signed into law in 2010.

The U.S. Securities and Exchange Commission, created in 1934, is the principal federal regulatory overseer of the securities markets. The SEC's mission is to administer securities laws and protect investors in public securities transactions. The SEC has broad enforcement power. It can pursue civil actions against individuals and corporations, but actions requiring criminal proceedings are referred to the U.S. Justice Department.

The SEC requires virtually all new public issues of corporate securities to be registered. As part of the registration process for a new security issue, the issuer must prepare a prospectus. The typical prospectus gives a detailed description of the company issuing the securities, including financial data, products, research and development projects, and pending litigation. It also describes the stock or bond issue and underwriting agreement in detail. The registration process seeks to guarantee full and fair disclosure. The SEC does not rule on the investment merits of a registered security. It is concerned only that an issuer gives investors enough information to make their own informed decisions.

The Securities and Exchange Commission is charged with regulating financial markets. Its Web site, shown here, is a good source of information for would-be investors.

insider trading use of material nonpublic information about a company to make investment profits.

One area to which the SEC pays particular attention is insider trading. Insider trading is defined as the use of material nonpublic information about a company to make investment profits. Examples of material nonpublic information include a pending merger or a major oil discovery, which could affect the firm's stock price.

Quick Review

![]() Who regulates banks?

Who regulates banks?

![]() What is insider trading?

What is insider trading?

The Financial System: A Global Perspective

The Financial System: A Global Perspective

Not surprisingly, the global financial system is becoming more and more integrated each year. With financial markets in existence throughout the world, shares of U.S. firms trade in other countries and shares of international companies trade in the United States. In fact, investors in China and Japan own more U.S. Treasury securities than do domestic investors.

Financial institutions have also become a global industry. Major U.S. banks—such as Wells Fargo and Bank of America—have extensive international operations where they maintain offices, lend money, and accept deposits from customers.

Although most Americans recognize large U.S. banks such as Citibank among the global financial giants, three of the world's 20 largest banks (measured by total assets) are U.S. institutions—JPMorgan Chase (ranked 12th), Bank of America (ranked 19th), and Citibank (ranked 20th). The other 17 are based in continental Europe, Great Britain, and Asia. The world's largest bank is Deutsche Bank AG, based in Germany, with $2.8 trillion in assets. These international banks operate worldwide, including locations in the United States.12

Like the United States, virtually all nations have some sort of a central bank. These banks play roles much like that of the Federal Reserve, controlling the money supply and regulating the banks. Policymakers at those banks often respond to changes in the U.S. financial system by making changes in their own system. For example, if the Fed lowers interest rates, the central bank in Japan may do the same. Such changes can influence events around the world.

In Frankfurt, Germany, a sculpture of the euro—the symbol for the European Union's currency—stands outside the headquarters of Europe's central bank. The 12 gold stars represent all the peoples of Europe.

Quick Review

![]() Where do U.S. banks rank compared with banks around the world?

Where do U.S. banks rank compared with banks around the world?

![]() How are foreign banks controlled?

How are foreign banks controlled?

What's Ahead?

This chapter explored the financial system, a key component of the U.S. economy and something that affects many aspects of contemporary business. The financial system is the process by which funds are transferred between savers and borrowers and includes securities, financial markets, and financial institutions. The chapter also described the role of the Federal Reserve and discussed the global financial system. Chapter 17 discusses the finance function of a business, including the role of the financial managers, financial planning, asset management, and sources of short- and long-term funds.

Weekly Updates spark classroom debate around current events that apply to your business course topics. http://www.wileybusinessupdates.com

NOTES

1. Herb Welsbaum, “Better Checking: No Fee, No Minimum, 4% Interest,” NBC News Business, February 11, 2013, http://www.nbcnews.com; Blake Ellis, “Community Banks Team Up to Fight the Megabanks,” CNN Money, February 17, 2012, http://money.cnn.com; Jim Bruene, “Is BancVue's Kasasa to Checking What ‘Intel Inside’ Was to PCs?” Net Banker, January 11, 2012, http://www.netbanker.com; Eric Wilkinson, “Americans Urged to ‘Break Up’ with Big Banks Saturday,” King5.com, November 4, 2011, http://www.king5.com.

2. Eric Markowitz, “All Signs Point to 2014 Twitter IPO,” Inc., May 21, 2013, http://www.inc.com; Douglas MacMillan & Mark Millan, “Box CEO Levie Targets 2014 IPO after Global Expansion,” Bloomberg, January 16, 2013, http://www.bloomberg.com.

3. NYSE Euronext Web site, “NYSE Statistics Archive,” May 2013, http://www.nyxdata.com.

4. Federal Deposit Insurance Corporation, “Statistics at a Glance,” http://www.fdic.gov, updated May 29, 2013.

5. Ibid.

6. Maryalese LaPonsie, “Are Direct Banks the Future?” MoneyRates.com, March 15, 2013, http://www.money-rates.com.

7. Federal Deposit Insurance Corporation, “Statistics at a Glance,” http://www.fdic.gov, updated May 29, 2013.

8. Jeff Blumenthal, “Which Local Banks Are among the 50 Largest?” Philadelphia Business Journal, June 4, 2013, http://www.bizjournals.com; Online Credit Union Data Analytics Systems, “1st Quarter 2013 Industry Trends Report,” CuData.com, http://cudata.com.

9. American Council of Life Insurers Web site, “Life Insurer Fact Book 2012,” http://www.acli.com, accessed June 16, 2013.

10. Organization for Economic Co-Operation and Development Web site, “Pension Fund Assets Hit Record USD $20.1 T in 2011, but Investment Performance Weakens,” September 2012, Issue 9, page 21, http://www.oecd.org.

11. Warren S. Hearsch, “U.S. Mutual Fund Assets Set to Pass $15 Trillion,” LifeHealthPro, February 13, 2013, http://www.lifehealthpro.com.

12. “Top Banks in the World,” Bankers Almanac, February 18, 2013, http://www.bankersaccuity.com.

CHAPTER SIXTEEN: REVIEW

Summary of Learning Objectives

![]() Understand the financial system.

Understand the financial system.

The financial system is the process by which funds are transferred between those having excess funds (savers) and those needing additional funds (users). Savers and users are individuals, businesses, and governments. Savers expect to earn a rate of return in exchange for the use of their funds. Financial markets, financial institutions, and financial instruments (securities) make up the financial system. Although direct transfers are possible, most funds flow from savers to users through the financial markets or financial institutions, such as commercial banks. A well-functioning financial system is critical to the overall health of a nation's economy.

financial system process by which money flows from savers to users.

![]() List the various types of securities.

List the various types of securities.

Securities, also called financial instruments, represent obligations on the part of issuers—businesses and governments—to provide purchasers with expected or stated returns on the funds invested or loaned. Securities can be classified into three categories: money market instruments, bonds, and stock.

- Money market instruments and bonds are debt instruments. Money market instruments are short-term debt securities and tend to be low-risk securities.

- Bonds are longer-term debt securities and pay a fixed amount of interest each year. Bonds are sold by the U.S. Department of the Treasury (government bonds), state and local governments (municipal bonds), and corporations. Mortgage pass-through securities are bonds backed by a pool of mortgage loans. Most municipal and corporate bonds have risk ratings.

- Common stock represents ownership in corporations. Common stockholders have voting rights and a residual claim on the firm's assets.

securities financial instruments that represent obligations on the part of the issuers to provide the purchasers with expected stated returns on the funds invested or loaned.

common stock basic form of corporate ownership.

![]() Discuss financial markets.

Discuss financial markets.

A financial market is a market where securities are bought and sold. The primary market for securities serves businesses and governments that want to sell new security issues to raise funds. Securities are sold in the primary market either through an open auction or a process called underwriting. The secondary market handles transactions of previously issued securities between investors. The New York Stock Exchange is a secondary market. The business or government that issued the security is not directly involved in secondary market transactions. In terms of the dollar value of trading volume, the secondary market is about four to five times larger than the primary market.

financial market market in which securities are issued and traded.

primary market financial market in which firms and governments issue securities and sell them initially to the general public.

secondary market collection of financial markets in which previously issued securities are traded among investors.

![]() Understand the stock markets.

Understand the stock markets.

The best-known financial markets are the stock exchanges. They exist throughout the world. The two largest—the New York Stock Exchange (NYSE) and NASDAQ—are located in the United States. Measured in terms of the total value of stock traded, the NYSE is bigger. Larger and better-known companies dominate the NYSE. Buy and sell orders are transmitted to the trading floor for execution. The NASDAQ stock market is an electronic market in which buy and sell orders are entered into a computerized communication system for execution. Most of the world's major stock markets today use similar electronic trading systems.

stock market (exchange) market in which shares of stock are bought and sold by investors.

![]() Evaluate financial institutions.

Evaluate financial institutions.

Financial institutions act as intermediaries between savers and users of funds.

- Depository institutions—commercial banks, savings banks, and credit unions—accept deposits from customers that can be redeemed on demand. Commercial banks are the largest and most important of the depository institutions and offer the widest range of services. Savings banks are a major source of home mortgage loans. Credit unions are not-for-profit institutions, offering financial services to consumers. Government agencies, most notably the Federal Deposit Insurance Corporation, insure deposits at these institutions.

- Nondepository institutions include pension funds and insurance companies. Nondepository institutions invest a large portion of their funds in stocks, bonds, and real estate. Mutual funds are another important financial institution. These companies sell shares to investors and in turn invest the proceeds in securities. Many individuals today invest a large portion of their retirement savings in mutual fund shares.

financial institution intermediary between savers and borrowers, collecting funds from savers and then lending the funds to individuals, businesses, and governments.

Federal Deposit Insurance Corporation (FDIC) federal agency that insures deposits at commercial and savings banks.

![]() Explain the role of the Federal Reserve System.

Explain the role of the Federal Reserve System.

The Federal Reserve System is the central bank of the United States. The Federal Reserve regulates banks, performs banking functions for the U.S. Department of the Treasury, and acts as the bankers' bank (clearing checks, lending money to banks, and replacing worn-out currency). It controls the supply of credit and money in the economy to promote growth and control inflation. The Federal Reserve's tools include reserve requirements, the discount rate, and open market operations. Selective credit controls and purchases and sales of foreign currencies also help the Federal Reserve manage the economy.

Federal Reserve System (Fed) the central bank of the United States.

![]() Describe the regulation of the financial system.

Describe the regulation of the financial system.

Commercial banks, savings banks, and credit unions in the United States are heavily regulated by federal or state banking authorities. Banking regulators require institutions to follow sound banking practices and have the power to close noncompliant ones. In the United States, financial markets are regulated at both the federal and state levels. Markets are also heavily self-regulated by the financial markets and professional organizations. The chief regulatory body is the Securities and Exchange Commission. It sets the requirements for both primary and secondary market activity, prohibiting a number of practices, including insider trading. The SEC also requires public companies to disclose financial information regularly. Professional organizations and the securities markets also have rules and procedures that all members must follow.

insider trading use of material nonpublic information about a company to make investment profits.

![]() Discuss the global perspective of the financial system.

Discuss the global perspective of the financial system.

Financial markets exist throughout the world and are increasingly interconnected. Investors in other countries purchase U.S. securities, and U.S. investors purchase foreign securities. Large U.S. banks and other financial institutions have a global presence. They accept deposits, make loans, and have branches throughout the world. Foreign banks also operate worldwide. The average European or Japanese bank is much larger than the average American bank. Virtually all nations have central banks that perform the same roles as the U.S. Federal Reserve System. Central bankers often act together, raising and lowering interest rates as economic conditions warrant.

Quick Review

LO1

![]() What is the financial system?

What is the financial system?

![]() In the financial system, who are the borrowers and who are the savers?

In the financial system, who are the borrowers and who are the savers?

![]() Name the two most common ways funds are transferred between borrowers and savers.

Name the two most common ways funds are transferred between borrowers and savers.

LO2

![]() Name the major types of securities.

Name the major types of securities.

![]() What is a government bond? A municipal bond?

What is a government bond? A municipal bond?

![]() Why do investors buy common stock?

Why do investors buy common stock?

LO3

![]() What is a financial market?

What is a financial market?

![]() Distinguish between a primary and a secondary financial market.

Distinguish between a primary and a secondary financial market.

![]() Briefly explain the role of financial institutions in the sale of securities.

Briefly explain the role of financial institutions in the sale of securities.

LO4

![]() Name the world's two largest stock markets.

Name the world's two largest stock markets.

![]() Why is the London Stock Exchange unique?

Why is the London Stock Exchange unique?

![]() Explain the difference between a market order and a limit order.

Explain the difference between a market order and a limit order.

LO5

![]() Name the two main types of financial institutions.

Name the two main types of financial institutions.

![]() What are the primary differences between commercial banks and savings banks?

What are the primary differences between commercial banks and savings banks?

![]() What is a mutual fund?

What is a mutual fund?

LO6

![]() What is the Federal Reserve System?

What is the Federal Reserve System?

![]() How is the Fed organized?

How is the Fed organized?

![]() List the three tools the Fed uses to control the supply of money and credit.

List the three tools the Fed uses to control the supply of money and credit.

LO7

![]() Who regulates banks?

Who regulates banks?

![]() What is insider trading?

What is insider trading?

LO8

![]() Where do U.S. banks rank compared with banks around the world?

Where do U.S. banks rank compared with banks around the world?

![]() How are foreign banks controlled?

How are foreign banks controlled?