The Changing Face of Business

![]() Define the term business.

Define the term business.

![]() Identify and describe the factors of production.

Identify and describe the factors of production.

![]() Describe the private enterprise system.

Describe the private enterprise system.

![]() Identify the six eras in the history of business.

Identify the six eras in the history of business.

![]() Explain how today's business workforce and the nature of work itself are changing.

Explain how today's business workforce and the nature of work itself are changing.

![]() Identify the skills and attributes needed for the 21st century manager.

Identify the skills and attributes needed for the 21st century manager.

![]() Outline the characteristics that make a company admired.

Outline the characteristics that make a company admired.

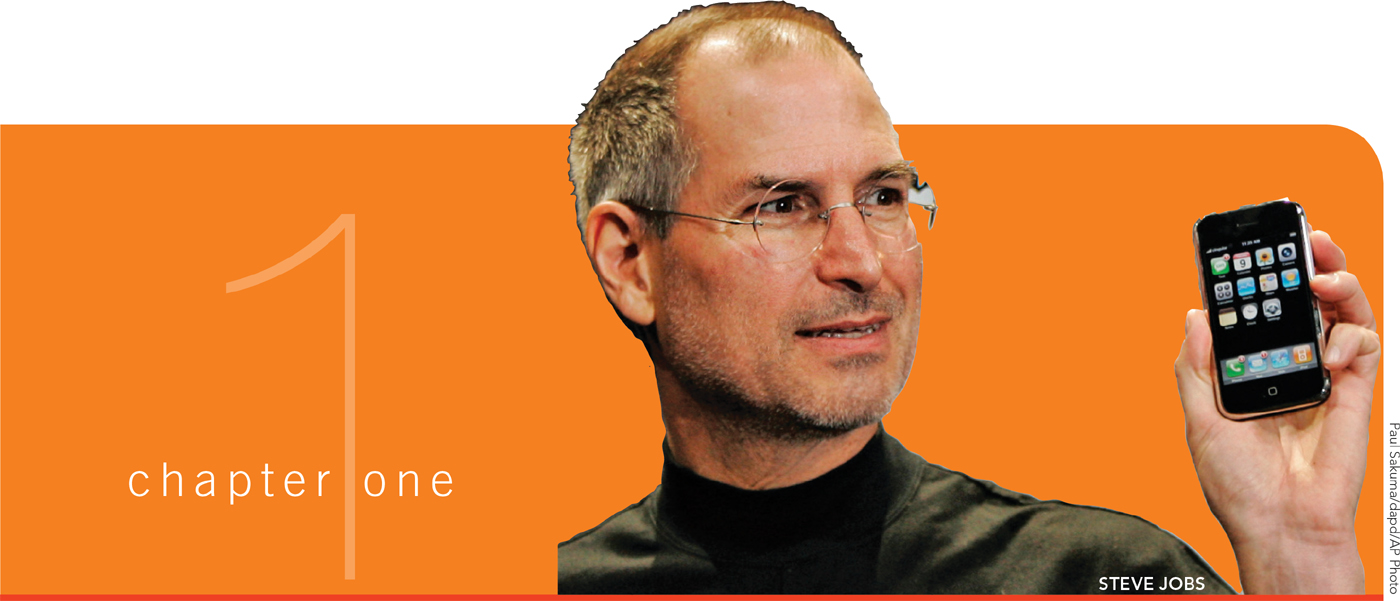

Apple and Steve Jobs: Business Leadership as Art

When Apple's visionary founder and leader Steve Jobs passed away at the age of 56, he was widely hailed as someone whose extraordinary career had transformed the world of business. But Apple's unsurpassed string of successful technological innovations had done far more. The Apple II, the Mac, iTunes, the iPod, the iPhone, the MacBook, and the iPad have transformed the communications industry, the music industry, the entertainment industry, and even the world of print.

Despite a 12-year absence from Apple, during which he founded another successful tech firm called NeXT and built Pixar Animation Studios into an Academy Award winner, Jobs brought his revolutionary computer company from humble start-up to unheard-of success. Apple is estimated to be worth nearly $400 billion today and has become one of the most valuable brand names of all time.

Jobs was passionately committed to innovation. His ability to understand how to make technology transparently simple to use ensured the success of many of Apple's iconic products, including generations of Mac personal computers and the iPod. These achievements, and their sleek and appealing designs, led many to think of him as a great business leader.

Jobs's unrelenting attention to detail and quest for perfection could also make him a difficult boss at times, but he inspired enormous devotion and loyalty among his employees. Some say he even transformed our idea of leadership, given his ability to inspire others with the same ideals that fueled his own drive to succeed.

Thanks to Apple, products we never knew we needed have become indispensable to our lives. Nothing about the way we write, listen, speak, text, view entertainment, present information, or surf the Internet will ever be the same. How does one company achieve so much?

An extraordinary leader is an obvious advantage, and few observers expect to see another CEO like Steve Jobs any time soon. But many business leaders today are as passionate and inspired, and their firms also seek to innovate and transform. Those companies that correctly assess what customers want, that deliver it at the right time and for the right price, and that keep ahead of the wave of relentless change they face, as Apple has done, will be more likely to succeed.1

Overview

In large part, a country depends on the wealth its businesses generate, from large enterprises like the Walt Disney Company to tiny online start-ups, and from venerable firms, like 150-year-old jeans maker Levi Strauss & Company to powerhouses like Google. What all these companies and many others like them share is the ability to meet society's needs and wants.

To succeed, business firms must know what their customers want so that they can supply it quickly and efficiently. That means they often reflect changes in consumer tastes, such as the growing preference for sports drinks and vitamin-fortified water. But firms can also lead in advancing technology and other changes. They have the resources, the know-how, and the financial incentive to bring about new innovations as well as the competition that inevitably follows, as in the case of Apple's iPhone and Google's Android.

You'll see throughout this book that businesses require physical inputs like auto parts, chemicals, sugar, thread, electricity, and money; the accumulated knowledge and experience of their managers and employees; and access to the latest technical innovations. Although these inputs will get an enterprise started, their long-term survivability may well depend on their ability to change with the marketplace. Flexibility is a key to long-term success—and to growth.

In short, business is at the forefront of our economy—and Contemporary Business Essentials is right there with it. This book explores the strategies that allow companies to grow and compete in today's interactive marketplace, along with the skills that you will need to turn ideas into action for your own success in business. This chapter sets the stage for the entire text by defining business and revealing its role in society. The chapter's discussion illustrates how the private enterprise system encourages competition and innovation while preserving business ethics.

What Is Business?

What Is Business?

What comes to mind when you hear the word business? Do you think of big corporations like ExxonMobil or Boeing? Or does the local dry cleaners or convenience store pop into your mind? Maybe you recall your first summer job. The term business is a broad, all-inclusive term that can be applied to many kinds of enterprises. Businesses provide the bulk of employment opportunities, as well as the products that people enjoy.

FOR-PROFIT ORGANIZATIONS

business all profit-seeking activities and enterprises that provide goods and services necessary to an economic system.

Business consists of all profit-seeking activities and enterprises. Some businesses produce tangible goods, such as automobiles, breakfast cereals, and digital music players; others provide services such as insurance, hair styling, and entertainment, ranging from the Six Flags theme parks and NFL games to concerts.

Business drives the economic pulse of a nation. It provides the means through which its citizens' standard of living improves. At the heart of every business endeavor is an exchange between a buyer and a seller. A buyer recognizes a need for a good or service and trades money with a seller to obtain that product. The seller participates in the process in hopes of gaining profits—a main ingredient in accomplishing the goals necessary for continuous improvement in the standard of living.

profits rewards earned by businesspeople who take the risks involved in blending people, technology, and information to create and market want-satisfying goods and services.

Profits represent rewards earned by businesspeople who take the risks involved in blending people, technology, and information to create and market goods and services. We often think of profits as the difference between a firm's revenues and the expenses it incurs in generating these revenues. And while this is true, it is the opportunity for profits that serves as incentive for people to start companies, expand them, and provide high-quality goods and services.

The quest for profits is a central focus of business, but businesspeople also recognize their social and ethical responsibilities. To succeed in the long run, companies must deal responsibly with employees, customers, suppliers, competitors, government, and the general public.

NOT-FOR-PROFIT ORGANIZATIONS

not-for-profit organization businesslike establishment that has primary objectives other than returning profits to owners.

What do a local food pantry, the U.S. Postal Service, the American Red Cross, and your local library have in common? They are all classified as not-for-profit organizations, businesslike establishments that have primary objectives other than returning profits to their owners. These organizations play an important role in society. It is important to understand that these organizations need to make or raise money so that they can operate and achieve their social goals. Not-for-profit organizations operate in both the private and public sectors. Private-sector not-for-profits include museums, libraries, trade associations, and charitable and religious organizations. Government agencies, political parties, and labor unions, all of which are part of the public sector, are also classified as not-for-profit organizations.

This cell phone store survives through the exchange between buyer and seller—in this case, the customer and the salesperson.

Not-for-profit organizations are a substantial part of the U.S. economy. Currently, more than 1.5 million non-profit organizations are registered with the Internal Revenue Service in the United States, in categories ranging from arts and culture to science and technology.2 These organizations control more than $2.6 trillion in assets and employ more people than the federal government and all 50 state governments combined.3 In addition, millions of volunteers work for them in unpaid positions. Not-for-profits secure funding from both private sources, including donations, and government sources. They are commonly exempt from federal, state, and local taxes.

The Red Cross mobilizes its efforts to respond to Superstorm Sandy relief.

Quick Review

![]() What activity lies at the heart of every business endeavor?

What activity lies at the heart of every business endeavor?

![]() What is the primary objective of a not-for-profit organization?

What is the primary objective of a not-for-profit organization?

Factors of Production

Factors of Production

factors of production four basic inputs: natural resources, capital, human resources, and entrepreneurship.

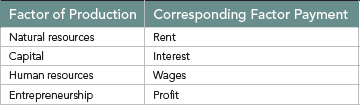

From the earliest human settlements to the modern societies of today, all economic systems require certain inputs for successful operation. Economists use the term factors of production to refer to the four basic inputs: natural resources, capital, human resources, and entrepreneurship. TABLE 1.1 identifies each of these inputs and the type of payment received by firms and individuals who supply them.

natural resources all production inputs that are useful in their natural states, including agricultural land, building sites, forests, and mineral deposits.

Natural resources include all production inputs that are useful in their natural states, including agricultural land, building sites, forests, and mineral deposits. One of the world's largest wind farms, the Roscoe Wind Complex, generates enough power to support almost a quarter million homes. Natural resources are the basic inputs required in any economic system.

capital an organization's technology, tools, information, and physical facilities.

Capital, another key resource, includes technology, tools, information, and physical facilities. Technology is a broad term that refers to machinery and equipment such as computers and software, telecommunications, and inventions designed to improve production. Information, frequently improved by technological innovations, is another critical factor because both managers and operating employees require accurate, timely information for effective performance of their assigned tasks. Technology plays an important role in the success of many businesses. Sometimes technology results in a new product, such as hybrid autos that run on a combination of gasoline and electricity. Most of the major car companies have introduced hybrid models in recent years.

To remain competitive, a firm needs to continually acquire, maintain, and upgrade its capital, and businesses need money for that purpose. A company's funds may come from owner-investments, profits plowed back into the business, or loans extended by others. Money then goes to work building factories; purchasing raw materials and component parts; and hiring, training, and compensating workers. People and firms that supply capital receive factor payments in the form of interest.

human resources in an organization, anyone who works, providing either the physical labor or intellectual inputs.

Human resources represent another critical input in every economic system. Human resources include anyone who works, from the chief executive officer (CEO) of a huge corporation to a self-employed writer or editor. This category encompasses both the physical labor and the intellectual inputs contributed by workers. Companies rely on their employees as a valued source of ideas and innovation as well as physical effort. Some companies solicit employee ideas through traditional means, such as an online “suggestion box” or in staff meetings. Others encourage creative thinking during company-sponsored hiking or rafting trips or during social gatherings. Effective, well-trained human resources provide a significant competitive edge because competitors cannot easily match another company's talented, motivated employees in the way they can buy the same computer system or purchase the same grade of natural resources.

Hiring and keeping the right people matter. Google employees feel they have a great place to work, partly because of the sense of mission—and the perks—the company provides.4

A competent, effective workforce can be a company's best asset. Organizations strive to retain their workers by providing perks such as onsite fitness facilities.

entrepreneurship ability to see an opportunity and take the risks inherent in creating and operating a business.

Entrepreneurship is the ability to see an opportunity and take the risks inherent in creating and operating a business. An entrepreneur is someone who sees a potentially profitable opportunity and then devises a plan to achieve success in the marketplace and earn those profits. By age 20, Jessica Mah was CEO of inDinero, a Web site that helps small businesses keep track of their money. Mah had “noticed that anything that touches money is much harder for entrepreneurs than it should be,” so she took a risk and started a firm designed to help them.5

U.S. businesses operate within an economic system called the private enterprise system. The next section looks at the private enterprise system, including competition and private property.

Quick Review

![]() What are the four basic factors of any economic system?

What are the four basic factors of any economic system?

![]() List the four types of capital.

List the four types of capital.

![]() What is an entrepreneur?

What is an entrepreneur?

The Private Enterprise System

The Private Enterprise System

No business operates in a vacuum; rather, all operate within a larger economic system that determines how goods and services are produced, distributed, and consumed in a society. The type of economic system employed in a society also determines patterns of resource use. Some economic systems, such as communism, feature strict controls on business ownership, profits, and resources to accomplish government goals.

private enterprise system economic system that rewards firms for their ability to identify and serve the needs and demands of customers.

In the United States, businesses function within the private enterprise system, an economic system that rewards firms for their ability to identify and serve the needs and demands of customers. The private enterprise system minimizes government interference in economic activity. Businesses that are adept at satisfying customers gain access to necessary factors of production and earn profits.

capitalism economic system that rewards firms for their ability to perceive and serve the needs and demands of consumers; also called the private enterprise system.

Another name for the private enterprise system is capitalism. Adam Smith, often identified as the father of capitalism, first described the concept in his book The Wealth of Nations, published in 1776. Smith believed that an economy is best regulated by the “invisible hand” of competition, the battle among businesses for consumer acceptance. Smith thought that competition among firms would lead to consumers' receiving the best possible products and prices because less efficient producers would gradually be driven from the marketplace.

competitive differentiation unique combination of organizational abilities, products, and approaches that sets a company apart from competitors in the minds of customers.

The “invisible hand” concept is a basic premise of the private enterprise system. In the United States, competition regulates much of economic life. To compete successfully, each firm must find a basis for competitive differentiation, the unique combination of organizational abilities, products, and approaches that sets a company apart from competitors in the minds of customers. Businesses operating in a private enterprise system face a critical task of keeping up with changing marketplace conditions. Firms that fail to adjust to shifts in consumer preferences or ignore the actions of competitors leave themselves open to failure. Apple and Microsoft have long been known for their rivalry, despite the fact that on occasion they have teamed up. For instance, Microsoft recently partnered with Apple and Oracle in an effort to thwart Android phone makers from using patented technology.6

Throughout this book, the discussion focuses on the tools and methods that 21st century businesses apply to compete and differentiate their goods and services. The text also discusses many of the ways in which market changes will affect business and the private enterprise system in the years ahead.

BASIC RIGHTS IN THE PRIVATE ENTERPRISE SYSTEM

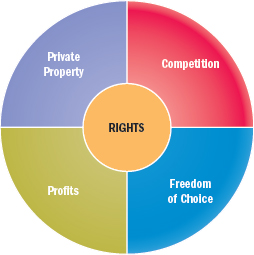

For capitalism to operate effectively, people living in a private enterprise economy must have certain rights. As shown in FIGURE 1.1, these include the rights to private property, profits, freedom of choice, and competition.

private property most basic freedom under the private enterprise system; the right to own, use, buy, sell, and bequeath land, buildings, machinery, equipment, patents, individual possessions, and various intangible kinds of property.

The right to private property is the most basic freedom under the private enterprise system. Every participant has the right to own, use, buy, sell, and bequeath most forms of property, including land, buildings, machinery, and equipment, patents on inventions, individual possessions, and intangible properties.

The private enterprise system also guarantees business owners the right to all profits—after taxes—they earn through their activities. Although a business is not assured of earning a profit, its owner is legally and ethically entitled to any income it generates in excess of costs.

Freedom of choice means that a private enterprise system relies on the potential for citizens to choose their own employment, purchases, and investments. They can change jobs, negotiate wages, join labor unions, and choose among many different brands of goods and services. A private enterprise economy maximizes individual prosperity by providing alternatives. Other economic systems sometimes limit freedom of choice to accomplish government goals, such as increasing industrial production of certain items or military strength.

The private enterprise system also permits fair competition by allowing the public to set rules for competitive activity. For this reason, the U.S. government has passed laws to prohibit “cutthroat” competition—excessively aggressive competitive practices designed to eliminate competition. It also has established ground rules that outlaw price discrimination, fraud in financial markets, and deceptive advertising and packaging.7

Quick Review

![]() What is an alternative term for private enterprise system?

What is an alternative term for private enterprise system?

![]() What is the most basic freedom under the private enterprise system?

What is the most basic freedom under the private enterprise system?

Six Eras in the History of Business

Six Eras in the History of Business

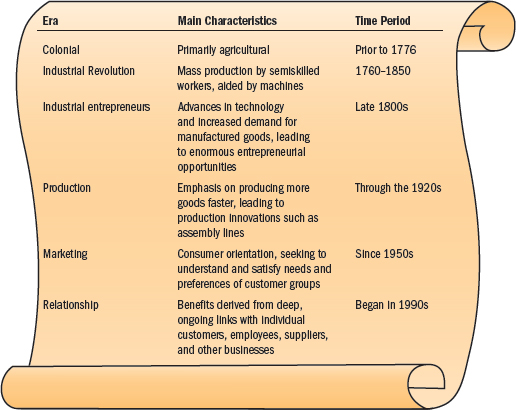

In the roughly 400 years since the first European settlements appeared on the North American continent, amazing changes have occurred in the size, focus, and goals of U.S. businesses. As FIGURE 1.2 indicates, U.S. business history is divided into six distinct time periods: (1) the Colonial period, (2) the Industrial Revolution, (3) the age of industrial entrepreneurs, (4) the production era, (5) the marketing era, and (6) the relationship era. The following sections describe how events in each of these time periods have influenced U.S. business practices.

THE COLONIAL PERIOD

Colonial society emphasized agricultural production. Colonial towns were small compared with European cities, and they functioned as marketplaces for farmers and craftspeople. The economic focus of the nation centered on rural areas because prosperity depended on the output of farms, orchards, and the like. The success or failure of crops influenced every aspect of the economy.

Colonists depended on England for manufactured items as well as financial backing for their infant industries. Even after the Revolutionary War (1775–1783), the United States maintained close economic ties with England. British investors continued to provide much of the financing for developing the U.S. business system, and this financial influence continued well into the 19th century.

THE INDUSTRIAL REVOLUTION

The Industrial Revolution began in England around 1750. It moved business operations from an emphasis on independent, skilled workers who specialized in building products one by one to a factory system that mass-produced items by bringing together large numbers of semiskilled workers. The factories profited from the savings created by large-scale production, bolstered by increasing support from machines over time. As businesses grew, they could often purchase raw materials more cheaply in larger lots than before. Specialization of labor, limiting each worker to a few specific tasks in the production process, also improved production efficiency.

Influenced by these events in England, business in the United States began a time of rapid industrialization. Agriculture became mechanized, and factories sprang up in cities. During the mid-1800s, the pace of industrialization increased as newly built railroad systems provided fast, economical transportation. In California, for example, the combination of railroad construction and the Gold Rush fueled a tremendous demand for construction.

THE AGE OF INDUSTRIAL ENTREPRENEURS

Building on the opportunities created by the Industrial Revolution, entrepreneurship increased in the United States. Henry Engelhard Steinway of Seesen, Germany, built his first piano by hand in his kitchen in 1825 as a wedding present for his bride. In 1850, the family immigrated to New York, where Henry and his sons opened their first factory in Manhattan in 1853. Over the next 30 years, they made innovations that led to the modern piano. Through an apprenticeship system, the Steinways transmitted their skills to the following generations. Steinway pianos have long been world famous for their beautiful tone, top-quality materials and workmanship, and durability. Now known as Steinway Musical Instruments, the company still builds its pianos by hand in its factory in Astoria, New York, under the same master-apprentice system that Henry and his sons began. Building each piano takes nearly a year from start to finish. In response to 21st century demands, the company has launched Etude, an app for the iPad that displays sheet music the user can play on an on-screen piano keyboard.8

Steinway pianos are world famous and are still built by hand in New York. The company is meeting the next generation's demands with iPad apps that allow users to play anywhere.

Inventors created a virtually endless array of commercially useful products and new production methods. Many of them are famous today:

- Eli Whitney introduced the concept of interchangeable parts, an idea that would later facilitate mass production on a previously impossible scale.

- Robert McCormick designed a horse-drawn reaper that reduced the labor involved in harvesting wheat. His son, Cyrus McCormick, saw the commercial potential of the reaper and launched a business to build and sell the machine. By 1902, the company was producing 35 percent of the nation's farm machinery.

- Cornelius Vanderbilt (railroads), J. P. Morgan (banking), and Andrew Carnegie (steel), among others, took advantage of the enormous opportunities waiting for anyone willing to take the risk of starting a new business.

The entrepreneurial spirit of this golden age in business did much to advance the U.S. business system and raise the country's overall standard of living. That market transformation, in turn, created new demand for manufactured goods.

THE PRODUCTION ERA

As demand for manufactured goods continued to increase through the 1920s, businesses focused even greater attention on the activities involved in producing those goods. Work became increasingly specialized, and huge, labor-intensive factories dominated U.S. business. Assembly lines, introduced by Henry Ford, became commonplace in major industries. Business owners turned over their responsibilities to a new class of managers trained in operating established companies. Their activities emphasized efforts to produce even more goods through quicker methods.

During the production era, business focused attention on internal processes rather than external influences. Marketing was almost an afterthought, designed solely to distribute items generated by production activities. Little attention was paid to consumer wants or needs. Instead, businesses tended to make decisions about what the market would get. If you wanted to buy a Ford Model T automobile, your color choice was black—the only color produced by the company.

THE MARKETING ERA

The Great Depression of the early 1930s changed the shape of U.S. business yet again. As incomes nosedived, businesses could no longer automatically count on selling everything they produced. Managers began to pay more attention to the markets for their goods and services, and sales and advertising took on new importance. During this period, selling was often synonymous with marketing.

consumer orientation business philosophy that focuses first on determining unmet consumer wants and needs and then designing products to satisfy those needs.

Demand for all kinds of consumer goods exploded after World War II. After nearly five years of doing without new automobiles, appliances, and other items, consumers were buying again. At the same time, however, competition also heated up. Soon businesses began to think of marketing as more than just selling; they envisioned a process of first determining what consumers wanted and needed and then designing products to satisfy those needs. In short, they developed a consumer orientation.

branding process of creating an identity in consumers' minds for a good, service, or company; a major marketing tool in contemporary business.

brand name, term, sign, symbol, design, or some combination that identifies the products of one firm and differentiates them from competitors' offerings.

Businesses began to analyze consumer desires before beginning actual production. Consumer choices skyrocketed. Car buyers, for example, could choose among a wide variety of colors and styles. Companies also discovered the need to distinguish their goods and services from those of competitors. Branding—the process of creating an identity in consumers' minds for a good, service, or company—is an important marketing tool. A brand can be a name, term, sign, symbol, design, or some combination that identifies the products of one firm and differentiates them from competitors' offerings.

Branding can go a long way toward creating value for a firm by providing recognition and a positive association between a company and its products. Some of the world's most famous—and enduring—brands include Coca-Cola, Apple, IBM, Google, Microsoft, GE, McDonald's, Intel, Samsung, and Toyota.9

The marketing era has had a tremendous effect on the way business is conducted today. Even the smallest business owners recognize the importance of understanding what customers want and the reasons they buy.

THE RELATIONSHIP ERA

transaction management building and promoting products in the hope that enough customers will buy them to cover costs and earn profits.

As business continues in the 21st century, a significant change is taking place in the ways companies interact with customers. Since the Industrial Revolution, most businesses have concentrated on building and promoting products in the hope that enough customers will buy them to cover costs and earn acceptable profits, an approach called transaction management.

relationship era business era in which firms seek ways to actively nurture customer loyalty by carefully managing their interactions with buyers.

In contrast, in the relationship era, businesses are taking a different, longer-term approach to their interactions with customers. Firms now seek ways to actively nurture customer loyalty by carefully managing their interactions with buyers. They earn enormous paybacks for their efforts. A company that retains customers over the long haul reduces its advertising and sales costs. Because customer spending tends to accelerate over time, revenues also grow. Companies with long-term customers often can avoid costly reliance on price discounts to attract new business, and they find that many new buyers come from loyal customer referrals.

Business owners gain several advantages by developing ongoing relationships with customers. Because it is much less expensive to serve existing customers than to find new ones, businesses that develop long-term customer relationships can reduce their overall costs. Long-term relationships with customers enable businesses to improve their understanding of what customers want and prefer from the company. As a result, businesses enhance their chances of sustaining real advantages through competitive differentiation.

The relationship era is an age of connections—between businesses and customers, employers and employees, technology and manufacturing, and even separate companies. The world economy is increasingly interconnected as businesses expand beyond their national boundaries. In this new environment, techniques for managing networks of people, businesses, information, and technology are critically important to contemporary business success.

Quick Review

![]() Describe the Industrial Revolution.

Describe the Industrial Revolution.

![]() During which era was branding developed?

During which era was branding developed?

![]() What is the difference between transaction management and relationship management?

What is the difference between transaction management and relationship management?

Today's Business Workforce

Today's Business Workforce

A skilled and knowledgeable workforce is an essential resource for keeping pace with the accelerating rate of change in today's business world. Employers need reliable employees who are dedicated to fostering strong ties with customers and partners. They must build workforces capable of the efficient, high-quality production needed to compete in global markets. Savvy business leaders also realize that employee brainpower plays a vital role in a firm's ability to stay on top of new technologies and innovations. In short, a first-class workforce can be the foundation of a firm's competitive differentiation, providing important advantages over competing businesses.

CHANGES IN THE WORKFORCE

Companies now face several trends that challenge their skills for managing and developing human resources. Those challenges include an aging population and a shrinking labor pool, growing diversity of the workforce, the changing nature of work, the need for flexibility and mobility, and the use of collaboration to innovate.

AN AGING POPULATION AND SHRINKING LABOR POOL

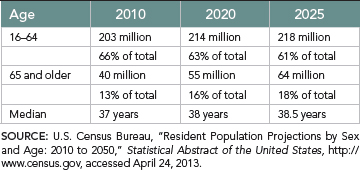

By 2025, the number of U.S. workers age 65 or older will reach 64 million—double what it is today—and many of them will soon retire from the workforce, taking their experience and expertise with them. As TABLE 1.2 shows, the U.S. population as a whole is trending older. Yet today, many members of the Baby Boom generation—the huge number of people born between 1946 and 1964—are still hitting the peaks of their careers. At the same time, members of so-called Generation X (born from 1965 to 1981) and Generation Y (born from 1982 to 2005) are building their careers, so employers are finding more generations in the workforce simultaneously than ever before. This broad age diversity brings management challenges, such as accommodating a variety of work–life styles, changing expectations of work, and varying levels of technological expertise. Still, despite the widening age spectrum of the workforce, some economists predict the U.S. labor pool could soon fall short by as many as 10 million people as Baby Boomers retire.

More sophisticated technology has intensified the hiring challenge by requiring workers to have ever more advanced skills. Companies are increasingly seeking—and finding—talent at the extreme ends of the working-age spectrum. Teenagers are entering the workforce sooner, and some seniors are staying longer—or seeking a new career after retiring from their primary career. Many older workers work part-time or flexible hours. Meanwhile, for older employees who do retire, employers must administer a variety of retirement planning and disability programs and insurance benefits.

INCREASINGLY DIVERSE WORKFORCE

The U.S. workforce is growing more diverse, in age and in every other way. The two fastest-growing ethnic populations in the United States are Hispanics and Asians. By the year 2060, the number of Hispanics in the United States will grow from a current 17 percent to 31 percent of the total population. The Asian population will increase from 5.1 percent to 8.2 percent of the total U.S. population.10 Considering that minority groups are growing, managers must learn to work effectively with diverse ethnic groups, cultures, and lifestyles to develop and retain a superior workforce for their company.

diversity in a workforce, the blending of individuals of different genders, ethnic backgrounds, cultures, religions, ages, and physical and mental abilities.

Diversity—the blending of individuals of different genders, ethnic backgrounds, cultures, religions, ages, and physical and mental abilities in a workforce—can enhance a firm's chances of success. In a recent list of top companies for diversity, the top ten were also leaders and innovators in their industries:

- Sodexo

- PricewaterhouseCoopers

- Kaiser Permanente

- Ernst & Young

- MasterCard Worldwide

- Novartis Pharmaceuticals Corporation

- Procter & Gamble

- Prudential Financial

- Accenture

- Johnson & Johnson.11

Several studies have shown that diverse employee teams and workforces tend to perform tasks more effectively and develop better solutions to business problems than homogeneous employee groups. This result is due in part to the varied perspectives and experiences that foster innovation and creativity in multicultural teams.

OUTSOURCING AND THE CHANGING NATURE OF WORK

outsourcing using outside vendors to produce goods or fulfill services and functions previously handled in-house or in-country.

Not only is the U.S. workforce changing, but so is the very nature of work. Manufacturing once accounted for most of U.S. annual output, but the balance has now shifted to services such as financial management and communications. This means firms must rely heavily on well-trained service workers with knowledge, technical skills, the ability to communicate and deal with people, and a talent for creative thinking. The Internet has made possible another business tool for staffing flexibility—outsourcing, or using outside vendors to produce goods or fulfill services and functions previously handled in-house. At its best, outsourcing allows a firm to reduce costs and concentrate its resources in the areas it does best while gaining access to expertise it may not have. But outsourcing also brings challenges, such as differences in language or culture.

offshoring relocation of business processes to lower-cost locations overseas.

nearshoring outsourcing production or services to locations near a firm's home base.

onshoring returning production to its original manufacturing location because of changes in costs or processes.

Offshoring, the relocation of business processes to lower-cost locations overseas, can include both production and services. In recent years, China has emerged as a dominant location for production offshoring for many firms, while India has become the key player in offshoring services. Some U.S. companies are now structured so that entire divisions or functions are developed and staffed overseas. Another trend in some industries is nearshoring, outsourcing production or services to nations near a firm's home base. And in some cases, companies are onshoring—returning production to its original manufacturing location because of changes in costs or processes.

FLEXIBILITY AND MOBILITY

Younger workers in particular are looking for something other than the work-comes-first lifestyle exemplified by the Baby Boom generation. But workers of all ages are exploring different work arrangements, such as telecommuting from remote locations and sharing jobs with two or more employees. Employers are also hiring growing numbers of temporary and part-time employees, some of whom are less interested in advancing up the career ladder and more interested in using and developing their skills. While the cubicle-filled office will likely never become entirely obsolete, technology makes productive networking and virtual team efforts possible by allowing people to work where they choose and easily share knowledge, a sense of purpose or mission, and a free flow of ideas across any geographical distance or time zone.

Managers of such far-flung workforces need to build and earn employees' trust in order to retain valued workers and to ensure that all members are acting ethically and contributing their share without the day-to-day supervision of a more conventional work environment. Managers and employees must be flexible and responsive to change while work, technology, and relationships continue to evolve.

INNOVATION THROUGH COLLABORATION

Some observers also see a trend toward more collaborative work in the future, as opposed to individuals working alone. Businesses using teamwork hope to build a creative environment where all members contribute their knowledge and skills to solve problems or seize opportunities.

The old relationship between employers and employees was pretty simple: every day, workers arrived at a certain hour, did their jobs, and departed at the same time. Companies rarely laid off workers, and employees rarely left for a job at another firm. But all that—and more—has changed. Employees are no longer likely to remain with a single company throughout their entire career and do not necessarily expect lifetime loyalty from the company they work for. They do not expect to give that loyalty, either; rather, they build their own career however and wherever they can. These changes mean that many firms now recognize the value of a partnership with employees that encourages creative thinking and problem solving and rewards risk taking and innovation.

Quick Review

![]() Define outsourcing, offshoring, and nearshoring.

Define outsourcing, offshoring, and nearshoring.

![]() Describe the importance of collaboration and employee partnership.

Describe the importance of collaboration and employee partnership.

The 21st Century Manager

The 21st Century Manager

Today's companies look for managers who are intelligent, highly motivated people with the ability to create and sustain a vision of how an organization can succeed. The 21st century manager must also apply critical-thinking skills and creativity to business challenges and lead change.

IMPORTANCE OF VISION

vision the ability to perceive marketplace needs and what an organization must do to satisfy them.

To thrive in the 21st century, businesspeople need vision, the ability to perceive marketplace needs and what an organization must do to satisfy them. Nannu Nobis, co-founder and CEO of Nobis Engineering, is recognized for his firm's environmental work as well as its efforts to convert its own business operations to the highest standards of sustainability. With only 100 employees, Nobis Engineering recently won prestigious major contracts with the U.S. Army Corps of Engineers and U.S. Environmental Protection Agency valued at $40 million. When the firm expanded to meet client needs, Nobis authorized $5 million to renovate a 20,000-square-foot historic mill building according to the U.S. Green Building Council LEED process. Nobis Engineering employees are rewarded for carpooling and reducing energy use in other ways as well. So far, Nobis Engineering has reduced its carbon emissions by more than 13,000 pounds. CEO Nobis says companies must walk the talk. “Our clients take this [sustainability] seriously and are proud to be with a firm that takes it seriously.”12

Employees can be rewarded by some firms for their efforts to reduce energy use through carpooling.

IMPORTANCE OF CRITICAL THINKING AND CREATIVITY

Critical thinking and creativity are essential characteristics of the 21st century workforce. Today's businesspeople need to look at a wide variety of situations, draw connections between disparate information, and develop future-oriented solutions. This need applies not only to top executives but to mid-level managers and entry-level workers as well.

critical thinking ability to analyze and assess information to pinpoint problems or opportunities.

Critical thinking is the ability to analyze and assess information to pinpoint problems or opportunities. The critical-thinking process includes activities such as determining the authenticity, accuracy, and worth of information, knowledge, and arguments. It involves looking beneath the surface for deeper meaning and connections that can help identify critical issues and solutions. Without critical thinking, a firm may encounter serious problems.

creativity capacity to develop novel solutions to perceived organizational problems.

Creativity is the capacity to develop novel solutions to perceived organizational problems. Although most people think of it in relation to writers, artists, musicians, and inventors, that is a very limited definition. In business, creativity refers to the ability to see better and different ways of operating. A computer engineer who solves a glitch in a software program is thinking creatively. Creativity and critical thinking must go beyond generating new ideas, however. They must lead to action. In addition to creating an environment in which employees can nurture ideas, managers must give them opportunities to take risks and try new solutions.

ABILITY TO LEAD CHANGE

Today's business leaders must guide their employees and organizations through the changes brought about by technology, marketplace demands, and global competition. Managers must be skilled at recognizing employee strengths and motivating people to move toward common goals as members of a team. Throughout this book, real-world examples demonstrate how companies have initiated sweeping change initiatives. Most, if not all, have been led by managers comfortable with the tough decisions that today's fluctuating conditions require.

Factors that require organizational change can come from both external and internal sources; successful managers must be aware of both. External forces might include feedback from customers, developments in the international marketplace, economic trends, and new technologies. Internal factors might arise from new company goals, emerging employee needs, labor union demands, or production problems.

Quick Review

![]() Why is vision an important managerial quality?

Why is vision an important managerial quality?

![]() What is the difference between creativity and critical thinking?

What is the difference between creativity and critical thinking?

What Makes a Company Admired?

What Makes a Company Admired?

Who is your hero? Is it someone who has achieved great feats in sports, government, entertainment, or business? Why do you admire the person? Does he or she lead a company, earn a lot of money, or give back to the community and society? Every year, business magazines and organizations publish lists of companies that they consider to be “most admired.” Companies, like individuals, may be admired for many reasons. Most people would mention solid profits, stable growth, a safe and challenging work environment, high-quality goods and services, and business ethics and social responsibility. Business ethics refers to the standards of conduct and moral values involving decisions made in the work environment. Social responsibility is a management philosophy that includes contributing resources to the community, preserving the natural environment, and developing or participating in nonprofit programs designed to promote the well-being of the general public. You'll find business ethics and social responsibility examples throughout this book, as well as a deeper exploration of these topics in Chapter 2.

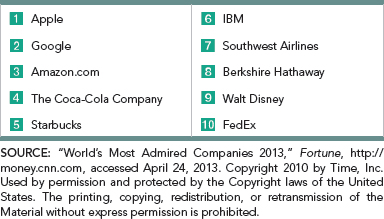

As you read this text, you'll be able to make up your mind about why companies should—or should not—be admired. Fortune publishes two lists of most admired companies each year, one for U.S.-based firms and one for the world. The list is compiled from surveys and other research conducted by the Hay Group, a global management consulting firm. Criteria for making the list include innovation, people management, use of corporate assets, social responsibility, quality of management, and quality of products and services.13 TABLE 1.3 lists the top ten World's Most Admired Companies for a recent year.

Quick Review

![]() Define business ethics and social responsibility.

Define business ethics and social responsibility.

![]() Name three criteria used to judge whether an organization might be considered admirable.

Name three criteria used to judge whether an organization might be considered admirable.

What's Ahead?

As business speeds along in the 21st century, new technologies, population shifts, and shrinking global barriers are altering the world at a frantic pace. Businesspeople are catalysts for many of these changes, creating new opportunities for individuals who are prepared to take action. Studying contemporary business will help you prepare for the future.

Through this book, you'll gain an understanding of how marketing, production, accounting, finance, and management work together to provide competitive advantages for firms. This knowledge can help you become a more capable employee and enhance your career potential.

Now that this chapter has introduced some basic terms and issues in the business world of the 21st century, Chapter 2 takes a detailed look at the ethical and social responsibility issues facing contemporary business. Chapter 3 deals with economic challenges, and Chapter 4 focuses on the difficulties and opportunities faced by firms competing in world markets.

Weekly Updates spark classroom debate around current events that apply to your business course topics. http://www.wileybusinessupdates.com

NOTES

1. Company Web site, http://www.apple.com, accessed May 15, 2013; Katie Marsal, “Former Apple Product Manager Recounts How Jobs Motivated First iPhone Team,” Apple Insider, February 3, 2012, www.appleinsider.com; Brian Caulfield, “The Steve Jobs Economy,” Forbes, November 7, 2011, p. 16; Gianpiero Petriglieri, “How Steve Jobs Reinvented Leadership,” Forbes, October 10, 2011, www.forbes.com; John Baldoni, “Learning from Steve Jobs: How to Lead with Purpose,” CNN Opinion, October 14, 2011, www.cnn.com; John Markoff, “Apple's Visionary Redefined Digital Age,” New York Times, October 5, 2011, www.nytimes.com; Joe Nocera, “What Makes Steve Jobs Great,” New York Times, August 26, 2011, www.nytimes.com; David Pogue, “Steve Jobs Reshaped Industries,” New York Times, blog post, August 25, 2011, www.nytimes.com.

2. National Center for Charitable Statistics, “Quick Facts about Nonprofits,” http://nccs.urban.org/statistics, accessed April 24, 2013.

3. National Center for Charitable Statistics, “Quick Facts about Nonprofits,” http://nccs.urban.org/statistics, accessed April 24, 2013; Foundation Center, Grant Space, http://grantspace.org/, accessed April 24, 2013; Bureau of Labor Statistics, Career Guide to Industries, 2010–11 Edition, http://www.bls.gov, accessed April 24, 2013.

4. “100 Best Companies to Work For (2013),” CNNMoney.com, http://money.cnn.com, accessed April 24, 2013.

5. Grace Austin, “inDinero: Helping Businesses Keep Tabs on Money,” Profiles in Diversity Journal, July 16, 2012, http://www.diversityjournal.com/9603-indinero-helping-businesses-keep-tabs-on-money/.

6. Brad Reed, “Apple Loses Latest Round in Android Patent Fight,” Network World, January 24, 2012, http://www.networkworld.com; Wayne Rash, “Apple, Microsoft, Oracle Lead Unholy Patent Alliance against Android,” July 11, 2011, http://www.eweek.com.

7. Government Web site, “Welcome to the Bureau of Competition,” Federal Trade Commission, http://www.ftc.gov/bc, accessed May 15, 2013.

8. Company Web site, “History,” http://www.steinway.com, accessed April 24, 2013.

9. “Best Global Brands 2012,” interbrand, http://www.interbrand.com, accessed April 24, 2013.

10. Jennifer M. Ortman, “U.S. Population Projections: 2012 to 2060,” U.S. Census Bureau, February 7, 2013, http://www.census.gov/population/projections.

11. “The 2013 DiversityInc Top 50 Companies for Diversity,” DiversityInc, n.d., http://www.diversityinc.com, accessed April 24, 2013.

12. Company Web site, http://www.nobisengineering.com, accessed April 24, 2013; Matthew J. Mowry, “Celebrating Business Excellence,” Business NH Magazine, May 2011, p. 54.

13. “World's Most Admired Companies 2013,” Fortune, http://money.cnn.com, accessed April 24, 2013.

CHAPTER ONE: REVIEW

Summary of Learning Objectives

![]() Define the term business.

Define the term business.

Business consists of all profit-seeking activities and enterprises. Some businesses produce tangible goods, such as automobiles, breakfast cereals, and digital music players; others provide services such as insurance, hair styling, and entertainment, ranging from Six Flags theme parks and NFL games to concerts.

business all profit-seeking activities and enterprises that provide goods and services necessary to an economic system.

profits rewards earned by businesspeople who take the risks involved in blending people, technology, and information to create and market goods and services.

not-for-profit organization businesslike establishment that has primary objectives other than returning profits to owners.

![]() Identify and describe the factors of production.

Identify and describe the factors of production.

The factors of production consist of four basic inputs: natural resources, capital, human resources, and entrepreneurship. Natural resources include all productive inputs that are useful in their natural states. Capital includes technology, tools, information, and physical facilities. Human resources include anyone who works for the firm. Entrepreneurship is the ability to see an opportunity and take the risks inherent in creating and operating a business.

factors of production four basic inputs: natural resources, capital, human resources, and entrepreneurship.

natural resources all production inputs that are useful in their natural states, including agricultural land, building sites, forests, and mineral deposits.

capital an organization's technology, tools, information, and physical facilities.

human resources in an organization, anyone who works, providing either the physical labor or intellectual inputs.

entrepreneurship ability to see an opportunity and take the risks inherent in creating and operating a business.

![]() Describe the private enterprise system.

Describe the private enterprise system.

The private enterprise system is an economic system that rewards firms for their ability to perceive and serve the needs and demands of consumers. Competition in the private enterprise system ensures success for firms that satisfy consumer demands. Citizens in a private enterprise economy enjoy the rights to private property, profits, freedom of choice, and competition. Entrepreneurship drives economic growth.

private enterprise system economic system that rewards firms for their ability to identify and serve the needs and demands of customers.

capitalism economic system that rewards firms for their ability to perceive and serve the needs and demands of consumers; also called the private enterprise system.

competitive differentiation unique combination of organizational abilities, products, and approaches that sets a company apart from competitors in the minds of customers.

private property most basic freedom under the private enterprise system; the right to own, use, buy, sell, and bequeath land, buildings, machinery, equipment, patents, individual possessions, and various intangible kinds of property.

![]() Identify the six eras in the history of business.

Identify the six eras in the history of business.

The six historical eras are the Colonial period, the Industrial Revolution, the age of industrial entrepreneurs, the production era, the marketing era, and the relationship era. In the Colonial period, businesses were small and rural, emphasizing agricultural production. The Industrial Revolution brought factories and mass production to business. The age of industrial entrepreneurs built on the Industrial Revolution through an expansion in the number and size of firms. The production era focused on the growth of factory operations through assembly lines and other efficient internal processes. During and following the Great Depression, businesses concentrated on finding markets for their products through advertising and selling, giving rise to the marketing era. In the relationship era, businesspeople focused on developing and sustaining long-term relationships with customers and other businesses. Technology promotes innovation and communication, while alliances create a competitive advantage through partnerships. Concern for the environment also helps build strong relationships with consumers.

consumer orientation business philosophy that focuses first on determining unmet consumer wants and needs and then designing products to satisfy those needs.

branding process of creating an identity in consumers' minds for a good, service, or company; a major marketing tool in contemporary business.

brand name, term, sign, symbol, design, or some combination that identifies the products of one firm and differentiates them from competitors' offerings.

transaction management building and promoting products in the hope that enough customers will buy them to cover costs and earn profits.

relationship era business era in which firms seek ways to actively nurture customer loyalty by carefully managing their interaction with buyers.

![]() Explain how today's business workforce and the nature of work itself are changing.

Explain how today's business workforce and the nature of work itself are changing.

The workforce is changing in several significant ways: (1) it is aging and the labor pool is shrinking, and (2) it is becoming increasingly diverse. The nature of work has shifted toward services and a focus on information. More firms now rely on outsourcing, offshoring, and nearshoring to produce goods or fulfill services and functions that were previously handled in-house or in-country. In addition, today's workplaces are becoming increasingly flexible, allowing employees to work from different locations. And companies are fostering innovation through teamwork and collaboration.

diversity in a workforce, the blending of individuals of different genders, ethnic backgrounds, cultures, religions, ages, and physical and mental abilities.

outsourcing using outside vendors to produce goods or fulfill services and functions previously handled in-house or in-country.

offshoring relocation of business processes to lower-cost locations overseas.

nearshoring outsourcing production or services to locations near a firm's home base.

onshoring returning production to its original manufacturing location because of changes in costs or processes.

![]() Identify the skills and attributes needed for the 21st century manager.

Identify the skills and attributes needed for the 21st century manager.

Today's managers need vision, the ability to perceive marketplace needs and the way their firm can satisfy them. Critical-thinking skills and creativity allow managers to pinpoint problems and opportunities and plan novel solutions. Managers are dealing with rapid change, and they need skills to help lead their organizations through shifts in external and internal conditions.

vision the ability to perceive marketplace needs and what an organization must do to satisfy them.

critical thinking ability to analyze and assess information to pinpoint problems or opportunities.

creativity capacity to develop novel solutions to perceived organizational problems.

![]() Outline the characteristics that make a company admired.

Outline the characteristics that make a company admired.

A company is usually admired for its solid profits, stable growth, a safe and challenging work environment, high-quality goods and services, and business ethics and social responsibility.

Quick Review

LO1

![]() What activity lies at the heart of every business endeavor?

What activity lies at the heart of every business endeavor?

![]() What is the primary objective of a not-for-profit organization?

What is the primary objective of a not-for-profit organization?

LO2

![]() What are the four basic factors of any economic system?

What are the four basic factors of any economic system?

![]() List the four types of capital.

List the four types of capital.

![]() What is an entrepreneur?

What is an entrepreneur?

LO3

![]() What is an alternative term for private enterprise system?

What is an alternative term for private enterprise system?

![]() What is the most basic freedom under the private enterprise system?

What is the most basic freedom under the private enterprise system?

LO4

![]() Describe the Industrial Revolution.

Describe the Industrial Revolution.

![]() During which era was branding developed?

During which era was branding developed?

![]() What is the difference between transaction management and relationship management?

What is the difference between transaction management and relationship management?

LO5

![]() Define outsourcing, offshoring, and nearshoring.

Define outsourcing, offshoring, and nearshoring.

![]() Describe the importance of collaboration and employee partnership.

Describe the importance of collaboration and employee partnership.

LO6

![]() Why is vision an important managerial quality?

Why is vision an important managerial quality?

![]() What is the difference between creativity and critical thinking?

What is the difference between creativity and critical thinking?

LO7

![]() Define business ethics and social responsibility.

Define business ethics and social responsibility.

![]() Name three criteria used to judge whether an organization might be considered admirable.

Name three criteria used to judge whether an organization might be considered admirable.