Focus on: Investments—Module 16

METHODS OF REPORTING INVESTMENTS

| Method | Conditions |

| Consolidation | Majority owned (> 50%) |

| Equity | Less than majority owned |

| Ability to exercise significant influence | |

| Ownership generally ≥ 20% | |

| Cost | Less than majority owned |

| Unable to exercise significant influence | |

| Ownership generally < 20% | |

| Not an investment in marketable securities | |

| Special Rules | Less than majority owned |

| (ASC 320/FASB #115) | Unable to exercise significant influence |

| Ownership generally < 20% | |

| Investment in marketable securities |

Equity Method

Carrying Value of Investment

Cost

+ Earnings

– Dividends

= Carrying value of investment

Earnings

Income reported by investee

× % of ownership

= Unadjusted amount

– Adjustments

= Investor’s share of investee’s earnings

Adjustments to Earnings

1. Compare initial investment to FMV of underlying net assets

2. Portion of excess may be due to inventory

Deduct from income in the first year (unless inventory not sold during year)

3. Portion of excess may be due to depreciable asset

Divide by useful life and deduct from income each year

4. Portion of excess may be due to land

No adjustment (unless land sold during year)

5. Remainder of excess attributed to goodwill

Test each year for impairment and deduct from income if it has occurred

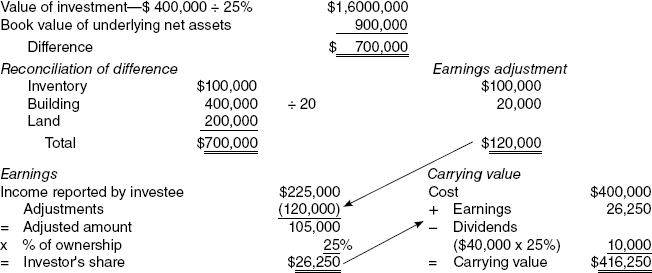

Application of Equity Method

Information given:

| Investment | 25% |

| Cost | $400,000 |

| Book value of investee’s underlying net assets | $900,000 |

| Undervalued assets: | |

Inventory |

100,000 |

Building (20 years) |

400,000 |

Land |

200,000 |

| Investee’s unadjusted income | $225,000 |

| Dividends | $40,000 |

Information Applied

Changes to and from the Equity Method

Equity Method to Cost Method

- No longer able to exercise significant influence

- Usually associated with sale of portion of investment

- Apply equity method to date of change

- Apply cost method from date of change

Cost Method to Equity Method

- Now able to exercise significant influence

- Usually associated with additional purchase

- Apply equity method retroactively

- Affects retained earnings and investment for prior periods

Fair Value Option

- An entity may elect to value its securities at fair value.

- If elected, available-for-sale, held-to-maturity, or equity method investments securities MTM and gain/loss goes to income

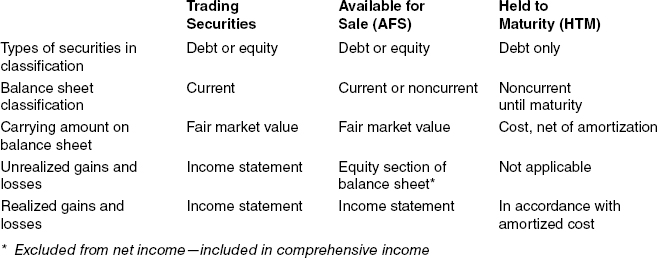

Marketable Securities (MES)

Transferring MES between Categories

When transferring between categories (e.g., trading to AFS), the transfer is

1. Accounted for at fair value

2. Unrealized holding gains/losses are adjusted so as not to be double counted

IFRS Investments

Similar to U.S. GAAP, IFRS classifies securities in categories but the account titles differ.

Held for trading (HFT)—further classified as a fair value through profit or loss (FVTPL) security.

- FVTPL securities are remeasured each accounting period.

- Available for sale (AFS)

- Held to maturity (HTM)

- Equity method investments (can use the equity method or FVTPL)

- Can elect to use the FVTPL method for AFS or HTM securities providing the security has an active market.

- Once the election is made, it may not be changed.

Instruments without quoted market prices should be accounted for using the cost method.

Life Insurance

Payment of premium:

| Cash surrender value of life insurance (increase in value) | xxx | |

| Insurance expense (plug) | xxx | |

Cash (premium amount) |

xxx |

Death of insured:

| Cash (face of policy) | xxx | |

Cash surrender value of life insurance (balance) |

xxx | |

Gain (difference) |

xxx |

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.