Focus on: Stockholders’ Equity—Module 15

STOCKHOLDERS’ EQUITY

Issuance of Common Stock

Stock Issued for Cash, Property, or Services

Journal entry:

| Cash, property, or expense (fair value) | xxx | |

Common stock (par or stated value) |

xxx | |

Additional paid-in capital (APIC) (difference) |

xxx |

Common Stock Subscribed

Subscription—Journal entry:

| Cash (down payment) | xxx | |

| Subscriptions receivable (balance) | xxx | |

Common stock subscribed (par or stated value) |

xxx | |

APIC (difference) |

xxx |

Collection and issuance of shares—Journal entries:

| Cash (balance) | xxx | |

Subscriptions receivable |

xxx | |

| Common stock subscribed (par or stated value) | xxx | |

Common stock (par or stated value) |

xxx |

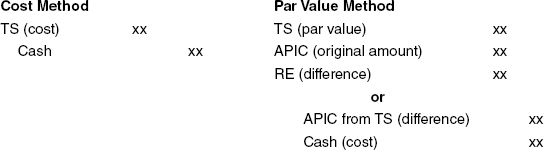

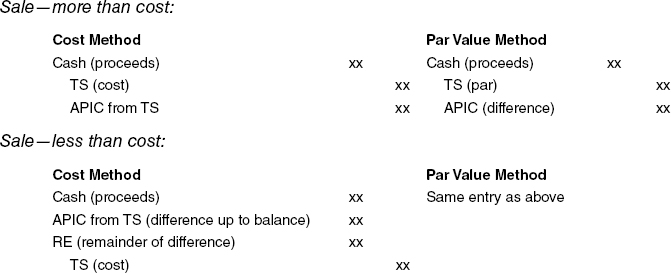

Treasury Stock

Acquisition of Shares

Characteristics of Preferred Stock

Preference over common stock

- Receive dividends prior to common stockholders

- Paid before common on liquidation

Cumulative preferred stock

- Unpaid dividends accumulated as dividends in arrears

- Paid in subsequent periods prior to payment of current dividends to common or preferred

- Not considered liability until declared

Participating preferred stock

- Receive current dividends prior to common stockholders

- Receive additional dividends, in proportion to common stockholders, in periods of high dividends

Equity Instruments with Characteristics of Liabilities

Financial instruments shares should be classified as liabilities on the balance sheet, even when they appear to be in the form of equity, when any of these characteristics apply:

- Preferred shares have a mandatory redemption date payable in cash.

- An obligation exists to repurchase shares through the transfer of assets to the shareholder.

- Shares are convertible to other shares when the exchange rate is based on a fixed monetary value of issuer shares or is tied to variations in the fixed value of something other than the issuer’s shares.

Note that convertible shares whose conversion rate is not adjusted for changes in values do not fall into this category (e.g., preferred stock convertible at a fixed 10 for 1 ratio to the common stock would not be a liability).

Dividends

Cash Dividends

Recorded when declared

- Allocated between common and preferred shares if preferred stock is participating

- Paid to common stockholders if preferred stock is nonparticipating

Property Dividends

Journal entry

Liquidating Dividends

Journal entry

| Retained earnings (balance) | xxx | |

| APIC (plug) | xxx | |

Cash or dividends payable |

xxx |

Stock Dividends

Journal entry—Normal stock dividend, usually 20% or less

| Retained earnings (fair market value of stock issued) | xxx | |

Common stock (par or stated value) |

xxx | |

APIC (difference) |

xxx |

Journal entry—Large stock dividend, usually more than 25%, referred to as stock split affected in the form of a stock dividend

| Retained earnings (par or stated value) | xxx | |

Common stock (par or stated value) |

xxx |

Preferred Stock—Special Issuances

Preferred with Detachable Warrants

| Cash (proceeds) | xxx | |

APIC from warrants (amount allocated) |

xxx | |

Preferred stock (par) |

xxx | |

| APIC from preferred stock (difference) | xxx |

Amount allocated to warrants using relative fair value method:

Allocation:

- Fair value of warrants ÷ Total fair value × Proceeds = Amount allocated to warrants

- Fair value of stock ÷ Total fair value × Proceeds = Amount allocated to stock

Convertible Preferred Stock

Journal entry—Issuance

| Cash (proceeds) | xxx | |

Preferred stock (par) |

xxx | |

APIC from preferred stock (difference) |

xxx |

Journal entry—Conversion

| Preferred stock (par) | xxx | |

| APIC from preferred stock (original amount) | xxx | |

Common stock (par or stated value) |

xxx | |

APIC (difference) |

xxx |

Retained Earnings

Appropriations

Set up to disclose to financial statement users future commitments that are not subject to accrual.

Journal entry:

| Retained earnings | xxx | |

Retained earnings appropriated for . . . |

xxx |

When the commitment is met, accrued, or avoided, the appropriation is reversed.

Journal entry:

| Retained earnings appropriated for . . . | xxx | |

Retained earnings |

xxx |

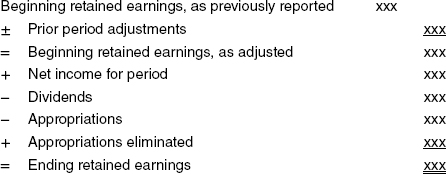

Prior-Period Adjustments

Made to correct errors in financial statements of prior periods

Adjustment to beginning retained earnings

- Equal to net amount of errors from periods prior to earliest period presented

- Reduced by tax effect

Presented on statement of retained earnings

- Unadjusted beginning balance reported

- Increased or decreased for prior-period adjustment

- Result is adjusted beginning balance

Statement of Retained Earnings

IFRS and Owner’s Equity

- Unlike U.S. GAAP, statement of changes in owners’ equity required

Stock Options Plans

Noncompensatory Plans

Noncompensatory when:

- All employees participate

- Participation uniform among employees

- Option period limited to reasonable time

- Discount below market price limited to reasonable amount

Compensatory Plans

Journal entry

| Deferred compensation | xxx | |

APIC—Options |

xxx |

Options must be accounted for using FMV at date of grant based on:

- Market price of options with similar characteristics

- Option pricing model

- Binomial distribution model

- Black-Scholes model

- Intrinsic value (Stock price—Exercise price) only used when FMV cannot be determined at grant date and must be replaced by FMV as soon as estimate is available

Compensation recognized over service period

IFRS and Stock Options

- Applies to all share-based payments

- Requires fair-value method in all cases

- Measurement of deferred tax asset is based on estimate of future tax deduction at end of each period.

- Changes in stock prices change to deferred tax asset

- Excess tax benefits (windfalls) are recorded first in equity (up to amount of cumulative book compensation expense) and then in equity

- Shortfalls become income tax expense

- Excess tax benefits are reported as cash inflows from operations; all employee stock ownership plans (ESOPs) are compensatory

Stock Appreciation Rights

Calculating liability

Amount needed to increase or decrease liability is recognized as compensation expense

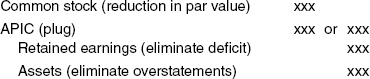

Quasi Reorganizations

Journal entry:

Book Value per Share

Calculation:

Disclosure of Information about Capital Structure

Rights and privileges of various debt and equity securities outstanding:

- Number of shares of common and preferred stock authorized, issued, and outstanding

- Dividend and liquidation preferences

- Participation rights

- Call prices and dates

- Conversion or exercise prices or rates and pertinent dates

- Sinking fund requirements

- Unusual voting rights

- Significant terms of contracts to issue additional shares

Reporting Stockholders’ Equity

| 6% cumulative preferred stock, $100 par value, 200,000 shares authorized, 120,000 shares issued and outstanding | $12,000,000 |

| Common stock, $10 par value, 1,500,000 shares authorized, 1,150,000 shares issued and 1,090,000 shares outstanding | 11,500,000 |

| Additional paid-in capital | 3,650,000 |

| 27,150,000 |

Retained Earnings:

Unappropriated |

$6,925,000 | |

Retained earnings appropriated for plant expansion |

1,400,000 | 8,325,000 |

| Accumulated other comprehensive income: | ||

Accumulated unrealized gain due to increase value of marketable securities available for sale |

||

| Accumulated translation adjustment | (515,000) | 235,000 |

| Less: Treasury stock, 60,000 shares at cost | 780,000 | |

| Total Stockholders’ Equity | $34,930,000 |

Earnings per Share (EPS)

Reporting Earnings per Share

Simple capital structure

- No potentially dilutive securities outstanding

- Present basic EPS only

Complex capital structure

- Potentially dilutive securities outstanding

- Dual presentation of EPS—basic EPS and diluted EPS

Potentially dilutive securities—Securities that can be converted into common shares

- Convertible bonds and convertible preferred stock

- Options, rights, and warrants

Basic EPS

Numerator

Income available to common stockholders

Denominator

Weighted-average common shares outstanding on the balance sheet date

Diluted EPS

Adjust numerator and denominator for dilutive securities

- Assume conversion into common shares

- Dilutive if EPS decreases

Convertible Preferred Stock

Dilutive if basic EPS is greater than preferred dividend per share of common stock obtainable:

- Add preferred dividends back to numerator

- Add common shares that preferred would be converted into to denominator

Convertible Bonds

Dilutive if basic EPS is greater than interest, net of tax, per share of common stock obtainable

- Add interest, net of tax, to numerator

- Add common shares that bonds would be converted into to denominator

Options, Rights, and Warrants

Dilutive when market price exceeds exercise price (proceeds from exercise)

The treasury stock method is applied

Calculation done on quarter-by-quarter basis

Presentation of EPS Information

Income Statement

Simple capital structure—Basic EPS only

- Income from continuing operations

- Net income

Complex capital structure—Basic and diluted EPS

- Income from continuing operations

- Net income

Additional Disclosures (Income Statement or Notes)

- Discontinued operations

- Extraordinary items