Focus on: Fixed Assets—Module 11

PROPERTY, PLANT, AND EQUIPMENT

General Rule

Capitalized amount = Cost of asset + Costs incurred in preparing it for its intended use

Gifts:

| Asset (FMV) | xx | |

Income |

xx |

Other capitalized costs for assets acquired by gift or purchase:

Land and Building

Total cost:

- Purchase price

- Delinquent taxes assumed

- Legal fees

- Title insurance

Allocation to land and building—Relative Fair Market Value Method

Land = FMV of land ÷ Total FMV × Total cost

Building = FMV of building ÷ Total FMV × Total cost

Capitalization of Interest

Capitalize on:

- Assets constructed for company’s use

- Assets manufactured for resale resulting from special order

Do not capitalize on:

- Inventory manufactured in the ordinary course of business

Interest capitalized:

- Interest on debt incurred for construction of asset

Interest on other debt that could be avoided by repayment of debt

Computed on:

- Weighted-average accumulated expenditures

Costs Incurred After Acquisition

Capitalize if:

- Bigger—The cost makes the asset bigger, such as an addition to a building

- Better—The cost makes the asset better, such as an improvement that makes an asset perform more efficiently

- Longer—The cost makes the asset last longer, extends the useful life

Do not capitalize:

Depreciation and Depletion

Basic Terms:

Straight-line rate = 100% ÷ Useful life (in years)

Book value = Cost – Accumulated depreciation

Depreciable basis = Cost – Salvage value

Selection of Method:

Use straight-line when benefit from asset is uniform over life

Use accelerated when:

- Asset more productive in earlier years

- Costs of maintenance increase in later years

- Risk of obsolescence is high

Use units-of-production when usefulness decreases with use

| Straight-Line | Double-Declining Balance |

| Annual depreciation = | Annual depreciation = |

Depreciable basis |

Book value |

× Straight-line rate |

× Straight-line rate |

× 2 |

|

| Partial year = | Partial year = |

Annual depreciation |

Book value |

× Portion of year |

× Straight-line rate |

× 2 |

|

× Portion of year |

Sum-of-the-Years’ Digits

Annual depreciation = Depreciable basis × Fraction

Partial year:

| 1st year = | 1st year’s depreciation × Portion of year |

| 2nd year = | Remainder of 1st year’s depreciation |

| + 2nd year’s depreciation × Portion of year | |

| 3rd year = | Remainder of 2nd year’s depreciation |

| + 3rd year’s depreciation × Portion of year |

Units of Production

Depreciation rate = Depreciable basis ÷ Total estimated units to be produced (hours)

Annual depreciation = Depreciation rate × Number of units produced (hours used)

Group or Composite

Based on straight line

Gains or losses not recognized on disposal

| Cash (proceeds) | xx | |

| Accumulated depreciation (plug) | xx | |

Asset (original cost) |

xx |

Impairment

Occurs if undiscounted future cash flow less than asset carrying amount from events such as:

- A decrease in the market value of the asset

- An adverse action or assessment by a regulator

- An operating or cash flow loss associated with a revenue producing asset

When an impairment loss occurs:

- Asset is written down to fair market value (or discounted net cash flow):

| Loss due to impairment | xx | |

Accumulated depreciation |

xx |

Note that test for impairment (future cash flow) is different from write-down amount (net realizable value).

Application of Impairment Rules

Example 1:

Example 2:

Disposal of Property, Plant, and Equipment

| Cash (proceeds) | xx | |

| Accumulated depreciation (balance) | xx | |

| Loss on disposal (plug) | xx | |

Gain on disposal (plug) |

xx | |

Asset (original cost) |

xx |

A disposal in involuntary conversion is recorded in the same manner as a sale.

IFRS Impairment

- Focuses on events (e.g., breach of contract or significant financial difficulty of the issuer)

- Loss recorded income

- IFRS: Reversal of losses on investments in debt allowed

Nonmonetary Exchanges

| Cash (amount received) | ||

| Asset—New (FMV) | xx | |

| Accumulated depreciation (balance on old asset) | xx | |

| Loss on disposal (plug) | ||

| Cash (amount paid) | ||

Gain on disposal (plug) |

xx | |

Asset—Old (Original cost) |

xx |

FMV

Use fair value of asset received or

Fair value of asset given

+ Cash paid

– Cash received

Exception

Applies to exchanges when:

- FMV is not determinable

- Exchange is only to facilitate subsequent sales to customers (e.g., ownership of inventory in one city is swapped for similar inventory in another to facilitate prompt delivery to customer in distant city)

- Transaction lacks commercial substance (risk, timing, and amount of future cash flows will not significantly change as a result of the transaction)

Loss—FMV of asset given < Carrying value of asset given

| Cash (amount received) | xx | |

| Asset—New (FMV) | xx | |

| Loss on disposal (plug) | xx | |

Cash (amount paid) |

xx | |

Asset—Old (carrying value) |

xx |

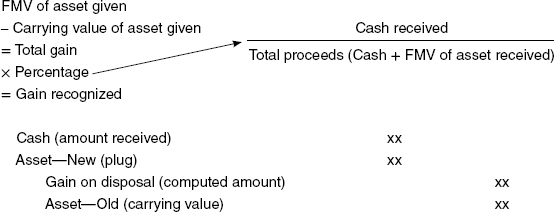

Gain—FMV of asset given > Carrying value of asset given

Gain recognized only when cash—received

No gain recognized when cash paid or no cash involved

| Asset—New (plug) | xx | |

| Accumulated depreciation (balance on old asset) | xx | |

Cash (amount paid) |

xx | |

Asset—Old (original cost) |

xx |

INTANGIBLES

General Characteristics

Lack physical substance

Uncertain benefit period

Associated with legal rights

Initial Accounting

Capitalize costs of purchasing intangibles

Expense costs of developing intangibles internally

Capitalize costs of preparing for use

Amortization

Straight-Line Amortization

Amortized over shorter of:

Units-of-sales amortization used if greater than straight-line amortization.

Tested for impairment when events suggest undiscounted future cash flow will be less than carrying value of intangible—written down to fair market value.

Intangibles with no clear legal or useful life (trademarks, perpetual franchises) must be examined annually for impairment either qualitatively or quantitatively. If impairment is likely, proceed to impairment test and write down whenever fair market value is less than carrying value.

Goodwill

Acquisition

Must be part of (an acquisition) business combination

Excess of acquisition price over fair value of underlying net assets

Internal Costs

May incur development or maintenance costs

All costs are expensed

Amortization

No amortization recorded

Impairment

Annually, qualitatively (or quantitatively) assess whether it is more likely than not that the fair value of a reporting unit is less than its carrying value. If so, perform the two-step impairment test:

IFRS: Property, Plant, and Equipment

- Elect either cost or revaluation model (RM). If RM is chosen:

- Carrying amount = Fair value at date of revaluation less subsequent accumulated depreciation and subsequent accumulated impairment loss

- Only for assets with value that can be reliably measured

- Entire class of assets

- Write asset up or down revaluation surplus account in Other comprehensive income (OCI)

- Can reverse impairment loss

- Cost method: reversal to income

- RM: reversal to OCI

- Requires component depreciation (e.g., parts of an airplane) and review of residual value and useful life each period

Leasehold Improvements

Amortize over shorter of:

- Useful life

- Remaining term of lease

Patents

Legal costs of defending a patent

- Successful—Capitalize legal costs as addition to carrying value of patent

- Unsuccessful—Recognize legal costs as expense and consider writing down patent

Research and Development (R & D)

R & D Assets:

IFRS allows capitalization of development costs if six criteria are met

Start-up Costs

Costs associated with start-up of organization should be immediately expensed

Franchises

Software

- Coding and testing

- Production of masters

Additional amortization:

Carrying value (after amortization) > Net realizable value (based on future revenues)

Excess is additional amortization