Focus on: Not-for-Profit Accounting—Module 22

ACCOUNTING FOR NONPROFIT ENTITIES

Financial Statements of Not-for-Profit Organizations

All not-for-profit organizations must prepare at least three financial statements

Not-for-profit organizations include:

- Hospitals

- Colleges and universities

- Voluntary health and welfare organizations (VHW)

Required financial statements for all types include:

VHWs must also prepare a Statement of Functional Expenses

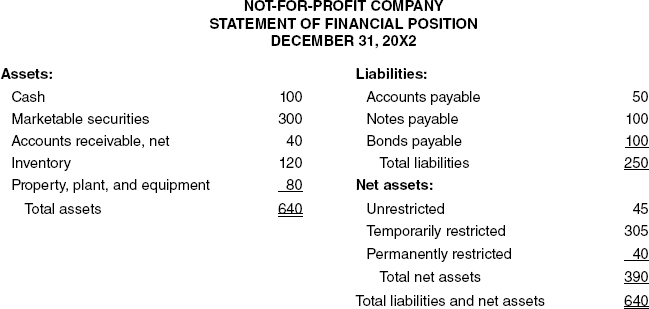

Statement of Financial Position

Includes assets, liabilities, and net assets

- Unrestricted net assets—Available for general use, including those set aside by board of trustees

- Temporarily restricted net assets—Donated by outside party and restricted to specific purpose

- Permanently restricted net assets—Donated by outside party and required to be invested with earnings restricted or unrestricted

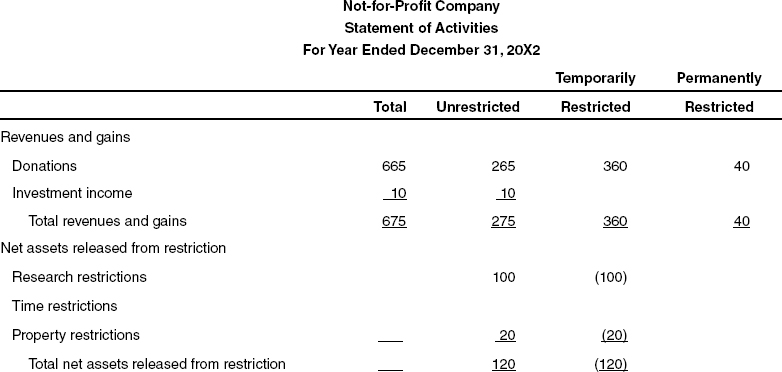

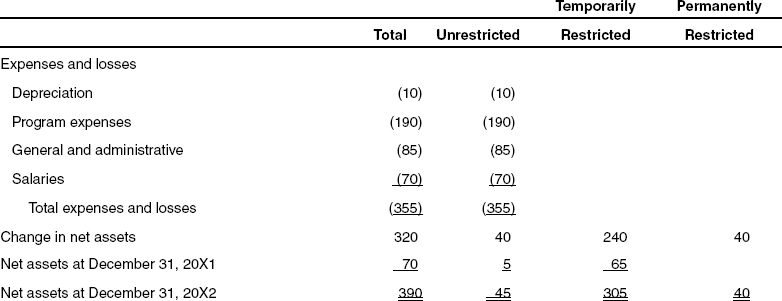

Statement of Activities for Not-for-Profit Organizations

Similar to income statement

- Reports revenues, gains, expenses, and losses

- Also reports temporarily restricted assets released from restriction

- Categorized activities among unrestricted, temporarily restricted, and permanently restricted to provide change in net assets for each

- Change added to beginning balance to provide ending net assets for each category

Expenses classified by:

- Object—Nature of item or service obtained

- Function—Program or activity to which attributed

- Character—Period or periods benefited from payments

Statement of Cash Flows for Not-for-Profit Organizations

Similar to statement of cash flows under GAAP

- Special treatment for donated assets restricted for long-term purposes

- Classified as cash flows from financing activities

Statement of Functional Expenses

Classifies expenses into program services and support services

- Program services—Expenses directly related to organization’s purpose

- Support services—Expenses necessary, but not directly related to organization’s purpose such as fundraising and administrative expenses

Expenses classified by (similar to statement of activities):

- Object

- Nature

- Character

Contributions Made to and Received by Not-for-Profit Organizations

In general, contributions are income to a not-for-profit organization

- Those that are part of the major, ongoing, and central operations are revenues

- Those that are not are gains

Unrestricted cash donations:

| Cash | xxx | |

Donations (unrestricted funds) |

xxx |

Permanently restricted donations:

| Cash | xxx | |

Donations (permanently restricted funds) |

xxx |

Donated services:

| Program expense (fair market value) | xxx | |

| Donations (unrestricted funds) | xxx |

Cash donations restricted for a specific purposes:

When made:

| Cash | xxx | |

Donations (temporarily restricted funds) |

xxx |

When used:

| Temporarily restricted net assets | xxx | |

Unrestricted net assets |

xxx | |

| Expense | xxx | |

Cash |

xxx |

Cash donated for purchase of property:

When made:

| Cash | xxx | |

Donations (temporarily restricted funds) |

xxx |

When used:

| Temporarily restricted net assets | xxx | |

Unrestricted net assets |

xxx | |

| Property | xxx | |

Cash |

xxx |

Pledges

Promises by outside parties to donate assets

- Recognized in period of pledge

- Allowance for uncollectible amount established

- Some or all may have time restriction—temporarily restricted

- Some or all may be unrestricted

| Pledges | xxx | |

Allowance for uncollectible pledges |

xxx | |

Donations (unrestricted funds) |

xxx | |

Donations (temporarily restricted funds) |

xxx |

Other Donations

Donations of art, antiques, or artifacts not recognized if:

- Asset held for research or exhibition

- Asset preserved and unaltered

- Proceeds from sale of asset to be used to buy additional art, antiques, and artifacts

Donated assets to be held in trust

- Not recognized by not-for-profit organization

- Disclosed in footnotes to financial statements

Hospital Revenues

Patient service revenue recorded at gross value of services

- Billing may be less due to Medicare allowance or employee discount

- Difference recorded in allowance account

- Statement of activities will report net amount

Services provided for free due to charity not recognized as revenues

Special transactions:

- Bad debts recognized as expense on statement of activities, not reduction of revenues

- Miscellaneous revenues from cafeteria, gift shop, parking lot fees, and educational programs classified as other revenue

- Donated supplies reported as operating revenue and expense when used

- Donations of essential services and unrestricted donations are nonoperating revenues

College Tuition Revenues

Students may receive refunds or price breaks

Refunds to students reduce tuition revenues

Price breaks may result from scholarships or reductions for family members of faculty or staff

- Tuition recognized at gross amount

- Price break recognized as expense