Focus on: Governmental (State and Local) Accounting—Module 21

GOVERNMENTAL (STATE AND LOCAL) ACCOUNTING

Governmental Accounting and Standards Board (GASB) Concept Statements set forth fundamentals on which governmental accounting and reporting standards will be based

Objective of governmental accounting and reporting—accountability

- Provide useful information

- Benefit wide range of users

Concepts Statement No. 1 identified three primary users of the external state and local governmental financial reports

Governmental financial information should:

- Demonstrate operations within legal restraints imposed by citizens

- Communicate compliance with laws and regulations related to raising and spending money

- Demonstrate interperiod equity—Current period expenditures financed with current revenues

To demonstrate full accountability for all activities, information must include:

- Cost of services

- Sufficiency of revenues for services provided

- Financial position

The concepts statements encourage Service Efforts and Accomplishment (SEA) reporting

- SEA reporting provides more complete information about a governmental entity’s performance than can be provided by traditional financial statements and schedules.

Funds

Government comprised of funds—Self-balancing sets of accounts—three categories

Methods of Accounting

Funds of a governmental unit use two methods of accounting

Modified Accrual Accounting

Differs from accrual accounting:

- Focus of financial reporting is financial position and flow of resources

- Revenues are recognized when they become available and measurable

- Expenditures are recorded when goods or services are obtained

- Expenditures are classified by object, function, or character

Financial Statements of Governmental Units

General-purpose financial statements—referred to as comprehensive annual financial reports (CAFRs)—five components

A component unit is a legally separate organization for which the elected officials of a primary government are financially accountable.

Users should be able to distinguish between primary government and component units—Component units may be blended when:

- Governing body of component is essentially the same as that of the primary government

- The component provides services almost exclusively for the primary government

- The component unit’s total debt outstanding, including leases, is expected to be repaid entirely or almost entirely by the primary government

Most component units will be discretely presented

Management Discussion and Analysis (MD&A)

Introduces basic financial statements and provides analytical overview of government’s financial activities

Should include:

- Condensed comparison of current-year financial information to prior year

- Analysis of overall financial position and results of operations

- Analysis of balances and transactions in individual funds

- Analysis of significant budget variances

- Description of capital assets and long-term debt activity during the period

- Currently known facts, decisions, or conditions expected to affect financial position or results of operations

Government-Wide Financial Statements

Consist of:

- Statement of net position

- Statement of activities

Report on overall government

- Do not display information about individual funds

- Exclude fiduciary activities or component units that are fiduciary

- Distinction made between primary government and discretely presented component units

- Distinction made between government-type activities and business-type activities of primary government

- Government-type activities include governmental funds and internal service funds

- Business-type activities include enterprise funds only

Characteristics of Government-Wide Financial Statements

Use economic measurement focus for all assets, liabilities, revenues, expenses, gains, and losses

Apply accrual basis of accounting

Revenues from exchanges or exchange-like transactions recognized in period of exchange

Revenues from nonexchange transactions:

- Derived tax revenues imposed on exchange transactions recognized as asset and revenues when exchange occurs

- Imposed nonexchange revenues imposed on nongovernment agencies recognized as asset when government has enforceable claim and as revenues when use of resources required or permitted

- Government-mandated nonexchange transactions provided by one level of government for another recognized as asset and revenue (or liability and expense) when all eligibility requirements met

- Voluntary nonexchange transactions recognized similarly to government-mandated nonexchange transactions

Statement of Net Position

Presents assets, liabilities, deferred outflows of resources, and deferred inflows of resources

- Assets and liabilities in order of liquidity

- Current and noncurrent portions of liabilities reported

- Assets + Deferred outflows of resources—Liabilities—Deferred inflows of resources = Net position

Three categories of net position:

Format of Statement of Net Position

Assets, deferred outflows of resources, liabilities, deferred inflows of resources and net position reported for primary government

- Separate columns for government-type activities and business-type activities

- Amounts combined in total column

Assets, deferred outflows of resources, liabilities, deferred inflows of resources and net position also reported for component units

- Amounts reported similarly as those for primary government

- Column not combined with totals for primary government

Statement of Activities

Self-financing activities distinguished from those drawing from general revenues

For each government function:

- Net expense or revenue

- Relative burden

Governmental activities presented by function

Business-type activities presented by business segment

Items reported separately after net expenses of government’s functions:

- General revenues

- Contributions to term and permanent endowments

- Contributions to permanent fund principal

- Special items—those that are unusual or infrequent

- Extraordinary items—those that are unusual and infrequent

- Transfers

Items on Statement of Activities

Depreciation—Indirect expense charged to function with asset

- Allocated among functions for shared assets

- Not required to be allocated to functions for general capital assets

- Not allocated to functions for eligible general infrastructure assets

- Government uses an asset management system

- Government documents assets preserved appropriately

Revenues classified into categories:

- Amounts received from users or beneficiaries of a program always program revenues

- Amounts received from parties outside citizenry are general revenues if unrestricted or program revenues if restricted to specific programs

- Amounts received from taxpayers always general revenues

- Amounts generated by the government usually general revenues

- Contributions to term and permanent endowments, contributions to permanent fund principal, special and extraordinary items, and transfers reported separately

Format of Statement of Activities

Information for each program or function reported separately:

- Expenses

- Charges for services

- Operating grants and contributions

- Capital grants and contributions

Difference between expenses and revenues reported for each program:

- Equal to change in net position

- Separated into columns for governmental activities and business-type activities

- Combined into a total column

Remaining items (general revenues, grants and contributions, special and extraordinary items, and transfers) reported separately below functions and programs:

- Divided into governmental activities and business-type activities with total column

- Provides change in net position and ending net position with same amounts as statement of net position

- Separate column for component units not combined into total

Additional Characteristics of Government-Wide Financial Statements

Internal amounts

- Eliminated to avoid doubling up

- Interfund receivables and payables eliminated

- Amounts due between government-type and business-type activities presented as offsetting internal balances

Capital assets include the following:

- Land, land improvements, and easements

- Buildings and building improvements

- Vehicles, machinery, and equipment

- Works of art and historical treasures

- Infrastructure

- All other tangible and intangible assets with initial useful lives greater than a single period

- Only identifiable intangibles

- Internally generated intangibles begin to be capitalized if

- Objective and capacity identified

- Feasible

- Intent to complete

- Pension plans

- Single-employer defined benefit plan or agent defined benefit plan

- Reports a net pension liability, which is measured as the portion of the actuarial present value of projected benefit payments attributable to past periods of employee service minus the pension plan’s fiduciary net position

- Single-employer defined benefit plan or agent defined benefit plan

Accounting for Capital Assets and Infrastructure

Capital assets reported at historical cost

- Includes capitalized interest and costs of getting asset ready for intended use

- Depreciated over useful lives

- Inexhaustible assets not depreciated

- Infrastructure assets may be depreciated under modified approach

Infrastructure includes:

- Capital assets with longer lives than most capital assets that are normally stationary

- Roads, bridges, tunnels, drainage systems, water and sewer systems, dams, and lighting systems

Eligible infrastructure assets not depreciated

- Must be part of network or subsystem maintained and preserved at established condition levels

- Additions and improvements increasing capacity or efficiency capitalized

- Other expenditures expensed

Fund Financial Statements

Governmental funds include:

- General fund

- Special revenue funds

- Capital projects funds

- Debt service funds

- Permanent funds

Proprietary funds include:

- Enterprise funds

- Internal service funds

Fiduciary funds include:

- Pension and other employee benefit trust funds

- Investment trust funds

- Private purpose trust funds

- Agency funds

Financial Statements of Governmental Funds

Statements of governmental funds

- Balance sheet

- Statement of revenues, expenditures, and changes in fund balances

Focus is to report sources, uses, and balances of current financial resources

- Apply modified accrual accounting.

- Capital assets and long-term debt not reported as assets or liabilities

Reports include separate columns for each major governmental fund and single column for total of all nonmajor funds:

- General fund is always major

- Others major if assets, liabilities, revenues, expenditures meet the 5% and 10% tests:

- Fund at least 5% of “total” column in government-wide financial statements

- Fund at least 10% of “government-type” column in government-wide financial statements

Balance Sheet

Reports assets, liabilities, and fund balances

- Reported separately for each major governmental fund

- Fund balances segregated into reserved and unreserved

Total fund balances reconciled to net position of governmental activities in government-wide financial statements

Statement of Revenues, Expenditures, and Changes in Fund Balances

Reports inflows, outflows, and balances of current financial resources

- Reported separately for each major governmental fund

- Revenues classified by major source

- Expenditures classified by function

Format of statement:

Change in fund balances reconciled to change in net position of governmental activities in government-wide financial statements

Financial Statements of Proprietary Funds

Statements of proprietary funds

- Statement of net position

- Statement of revenues, expenses, and changes in fund net position

- Statement of cash flows

Preparation of statements

- Emphasis is measurement of economic resources

- Prepared under accrual basis of accounting

- Reports include separate column for each enterprise fund meeting 5% and 10% tests:

- Fund at least 5% of “total” column in government-wide financial statements

- Fund at least 10% of “business-type” column in government-wide financial statements.

- Total of nonmajor enterprise funds in a single column

- Total of all internal service funds in a single column

- Four categories

- Derivatives: Reported at fair value

- Evaluated for effectiveness each financial reporting period

- Land held for investment reported at fair value

Statement of Net Position

Prepared in classified format

- Current and noncurrent assets and liabilities distinguished

- Net position reported in same categories as used in government-wide financial statements

Statement of Revenues, Expenses, and Changes in Fund Net Position

Amounts should be the same as net position and changes in net position shown for business-type activities in government-wide financial statements

- Revenues reported by major source

- Operating and nonoperating revenues and expenses distinguished

- Nonoperating revenues and expenses reported after operating income

Format of Statement of Revenues, Expenses, and Changes in Fund Net Position

Statement of Cash Flows

Shows sources and uses of cash by major classification

- Operating activities reported using direct method

- Noncapital financing activities

- Capital and related financing activities

- Investing activities

Operating income reconciled to cash flows from operating activities (indirect method)

Financial Statements of Fiduciary Funds

Statements of fiduciary funds

- Statement of net position

- Statement of changes in fiduciary net position

Focus of fiduciary financial statements:

- Emphasis on measurement of economic resources

- Prepared using accrual basis of accounting

Report includes separate column for each major fiduciary fund and column for total of all non-major fiduciary funds.

- Selection of major funds based on judgment of entity management

- No 5% and 10% tests since fiduciary funds weren’t included in government-wide financial statements

Notes to Government Financial Statements

Intended to provide information needed for fair presentation of financial statements

Notes include:

- Summary of significant accounting policies

- Disclosure about capital assets and long-term liabilities

- Disclosure about major classes of capital assets

- Disclosure about donor-restricted endowments

- Segment information

Required Supplementary Information

Presented in addition to MD&A

Consists of:

- Schedule of funding progress for all pension trust funds

- Schedule of employer contributions to all pension trust funds

- Budgetary comparison schedules for governmental funds (reporting basis is same as that chosen by legislative body for budget, and not necessarily that used for financial statements)

- Information about infrastructure reported under the modified approach

- Claims development information for any public entity risk pools

Governmental Funds

A governmental unit maintains five types of governmental funds:

- Only fund that reports positive unassigned fund balance

- Fixed assets and long-term debt not reported in governmental funds

- Instead, reported in government-wide financial statements

- Four fund balance classifications

General Fund Accounting

A governmental unit will have one general fund

- Annual budget is recorded at the beginning of the year

- Revenues, expenditures, and other financing sources and uses are recorded during the year

- Adjustments are made at the balance sheet date

- Budgetary accounts are closed at year-end

Beginning of Year

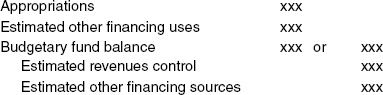

Governmental unit adopts annual budget for general fund

Budget recorded with following entry:

Estimated revenues control = Revenues expected to be collected during the year

Estimated other financing sources = Estimate of proceeds from bond issues and operating transfers in

Budgetary fund balance (plug) = Amount required to balance the entry

Appropriations = Expenditures expected during the year

Estimated other financing uses = Expected operating transfers out

During the Year

Revenue cycle consists of billing certain revenues, such as property taxes, collecting billed revenues, writing off uncollectible billings, and collecting unbilled revenues

Billing of revenues:

| Taxes receivable | xxx | |

Allowance for estimated uncollectible taxes |

xxx | |

Deferred revenues |

xxx | |

Revenues control |

xxx |

Taxes receivable = Amount billed

Allowance for estimated uncollectible taxes = Billings expected to be uncollectible

- This amount may be adjusted upward or downward during the year

- Offsetting entry will be to revenues control

Deferred revenues = Portion of billed taxes expected to be collected more than 60 days after close of current year

Revenues control = Portion of billed taxes expected to be collected during the current year or within 60 days of close

Collecting billed revenues:

| Cash | xxx | |

Taxes receivable |

xxx |

Writing off uncollectible amounts:

| Allowance for estimated uncollectible taxes | xxx | |

Taxes receivable |

xxx |

Collecting unbilled revenues:

| Cash | xxx | |

Revenues control |

xxx |

Spending cycle consists of ordering goods and services, receiving the goods and services, and paying for them

Ordering goods and services:

| Encumbrances control (estimated cost) | xxx | |

Budgetary fund balance reserved for encumbrances |

xxx |

Receiving goods and services:

| Budgetary fund balance reserved for encumbrances (estimated cost) | xxx | |

Encumbrances control |

xxx | |

| Expenditures control (actual cost) | xxx | |

Vouchers payable |

xxx |

Payment:

| Vouchers payable | xxx | |

Cash |

xxx |

Other financing sources and uses are recorded as the transactions occur:

- Proceeds of long-term debit issues are recorded as other financing sources when received

- Operating transfers to or from other funds are reported as other financing uses or sources as the funds are transferred

Adjustments at Balance Sheet Date

Closing entry—Eliminating revenues, expenditures, and encumbrances:

The remaining balance in the budgetary fund balance reserved for encumbrances is transferred to a nonbudgetary account:

| Budgetary fund balance reserved for encumbrances | xxx | |

Fund balance reserved for encumbrances |

xxx |

The governmental unit may decide to recognize inventory as an asset:

| Inventories (increase) | xxx | |

Fund balance reserved for inventories |

xxx | |

Or |

||

| Fund balance reserved for inventories | xxx | |

Inventories (decrease) |

xxx |

End of Year

Budget recorded in beginning of year is reversed:

Special Revenue Fund

Used to account for revenues that must be used for a particular purpose

- Accounting identical to general fund

Capital Projects Fund

Used to account for construction of fixed assets

- Fund opened when project commences and closed when project complete

- Accounting similar to general fund

Differences in accounting for capital projects fund:

- Credit contracts payable

- Credit retention payable for deferred payments

Debt Service Fund

Used to account for funds accumulated to make principal and interest payments on general obligation debts

- Expenditures include principal and interest payable in current period

- Resources consist of amounts transferred from other funds (other financing sources) and earnings on investments (revenues)

Amounts used for interest payments separated from amounts used for principal payments

| Cash for interest | xxx | |

| Cash for principal | xxx | |

Other financing sources |

xxx |

Proprietary Funds

Account for governmental activities conducted similarly to business enterprises

Enterprise fund:

- Used to account for business-type activities

- Uses accrual basis accounting

- Earned income recognized as operating revenues

- Shared taxes reported as nonoperating revenues

Internal service fund:

- Used to account for services provided to other governmental departments on a fee or cost-reimbursement basis

- Resources come from billings to other funds

- Reported as operating revenues

Fiduciary Funds

Pension Trust Fund

Accounts for contributions made by government and employees using accrual accounting

Additional information in notes and supplementary information following notes includes:

- Descriptive information about the plan

- Information about plan investments

- Information about the terms of receivables and nature of reserves

- Components of the pension liability

- Significant assumptions to measure the pension liability

- The measurement date

- A 10-year schedule of changes in pension liability

- A 10-year schedule of the amounts of total pension liability, fiduciary net position, net pension liability, the covered-employee payroll, and selected ratios

- A 10-year schedule of the actuarial computed required contribution, the required contribution, the actual contribution to the plan, and selected ratios

- A 10-year schedule of the annual money-weighted return on pension plan assets

Investment Trust Fund

Accounts for assets received from other governments units to be invested on their behalf.

- Uses accrual accounting

Private Purpose Trust Fund

Accounts for resources held on behalf of private persons or organizations.

- Uses accrual accounting

Agency Fund

Accounts for money collected for various funds, other governments, or outsiders

- Includes only balance sheet accounts

- Assets always equal liabilities

- Uses modified accrual accounting

Interfund Transactions

Nonreciprocal transfers are transfers of resources from one fund to another without any receipts of goods or services, such as a transfer of money from the general fund to a capital projects fund.

Paying fund:

| Other financing uses control | xxx | |

Cash |

xxx |

Receiving fund:

| Cash | xxx | |

Other financing uses control |

xxx |

Reciprocal transfers occur when one fund acquires goods or services from another in a transaction similar to one that would occur with outsiders.

Paying fund:

| Expenditures control or Expenses | xxx | |

Cash |

xxx |

Receiving fund:

| Cash | xxx | |

Revenues control |

xxx |

Reimbursements occur when one fund makes payments on behalf of another fund

Reimbursing fund:

| Expenditures control or Expenses | xxx | |

Cash |

xxx |

Receiving fund:

| Cash | xxx | |

Expenditures control or Expenses |

xxx |

Loans may be made from one fund to another

Lending fund:

| Due from other fund (fund identified) | xxx | |

Cash |

xxx |

Receiving fund:

| Cash | xxx | |

Due from other fund (fund identified) |

xxx |

Solid Waste Landfill Operations

The Environmental Protection Agency imposes requirements on solid waste landfills

- Procedures for closures

- Procedures for postclosure care

Procedures represent long-term obligations accounted for as long-term debt

- Costs to be incurred by governmental funds accounted for in general long-term debt account group

- Expenditures in governmental funds reduce general long-term debt account group balances

- Costs to be incurred by proprietary funds accounted for directly in funds

- Costs associated with closure and postclosure procedures accounted for during periods of operation

Government Consolidations

- A merger is a government combination of legally separate entities in which no significant consideration is exchanged.

- An acquisition is a government combination in which a government acquires another entity, or the operations of another entity, in exchange for significant consideration.

- A transfer of operations is a government combination involving the transfer of operations of a government or nongovernmental entity in which no significant consideration is exchanged.

- Disposal of Operations. A disposing government should recognize a gain or loss on disposal of operations.