Focus on: Statement of Cash Flows—Module 17

STATEMENT OF CASH FLOWS

Purpose of Statement

Summarizes sources and uses of cash and cash equivalents

Classifies cash flows into operating, investing, and financing activities

Cash Equivalents

Easily converted into cash (liquid)

Original maturity ≤ three months

Format of Statement

Cash provided or (used) by operating activities

± Cash provided or (used) by investing activities

± Cash provided or (used) by financing activities

= Net increase or (decrease) in cash and cash equivalents

+ Beginning balance

= Ending balance

Inputs to the Cash Flow Statement

Each item on the balance sheet (change from prior year) and income statement must be accounted for. In general:

Operating activities:

- Income statement items/adjustments (e.g., sales)

- Current assets and current liabilities (e.g., accounts receivable)

Investing activities:

- Noncurrent assets (e.g., building)

Financial activities:

- Noncurrent liabilities and equity (e.g., bank loan, stock)

Some changes do not involve cash (equipment purchased with stock), and some do not follow the general rule (e.g., dividends payable is a current liability, but since it is the result of stock ownership, its adjustment will appear in financing activities instead of operating activities).

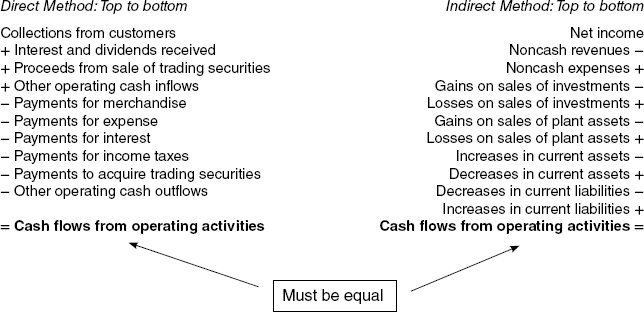

Operating Activities

Components of Direct Method

| Collections from customers (plug) | xxx | |

| Increase in accounts receivable (given) | xxx | |

Decrease in accounts receivable (given) |

xxx | |

Sales (given) |

xxx | |

| Increase in inventory (given) | xxx | |

| Decrease in accounts payable (given) | xxx | |

| Cost of sales (given) | xxx | |

Decrease in inventory (given) |

xxx | |

Increase in accounts payable (given) |

xxx | |

Payments for merchandise (plug) |

xxx |

Adjustments under Indirect Method

- Credit changes are addbacks/debit changes are subtractions, for example:

- Increase in accumulated depreciation added back

- Increase in accounts payable added back

- Increase in accounts receivable subtracted

- Decrease in accounts payable subtracted

Investing Activities

Principal collections on loans receivable

+ Proceeds from sale of investments (except trading securities)

+ Proceeds from sale of plant assets

– Loans made

– Payments to acquire investments (except trading securities)

– Payments to acquire plant assets

= Cash flows from investing activities

Financing Activities

Proceeds from borrowings

+ Proceeds from issuing stock

– Debt principal payments

– Payments to reacquire stock

– Payments for dividends

= Cash flows from financing activities

Other Disclosures

With direct method:

Reconciliation of net income to cash flows from operating activities (indirect method)

With indirect method:

Payments for interest

Payments for income taxes

With all cash flow statements:

Schedule of noncash investing and financing activities

IFRS and Cash Flows

- Interest/dividends in either financing or operations sections but must be consistent

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.